Sample Category Title

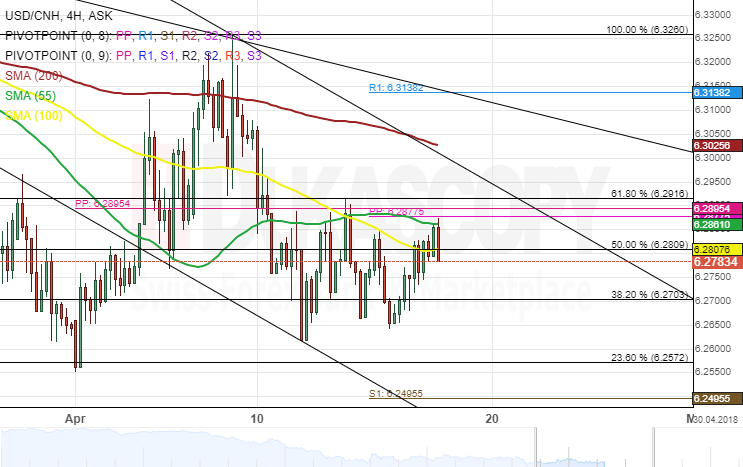

USD/CNH 4H Chart: All Signals Point Downwards

The US Dollar's movements against the Chinese one currency have not been mapped for some time, because some consider them rather boring. The bottom line about the pair is that the US Dollar is losing value against the Yuan.

However, the movements of various timeframes can be mapped in various scale patterns. Moreover, it can be observed that the currency exchange rate has a rather notable tendency to respect Fibonacci retracement lines.

In regards to the near term future, the pair is either set to trade sideways or decline. The reason for such assumption is the fact that the pair has fallen below a very strong resistance cluster, which is located from 6.28 to 6.29 levels.

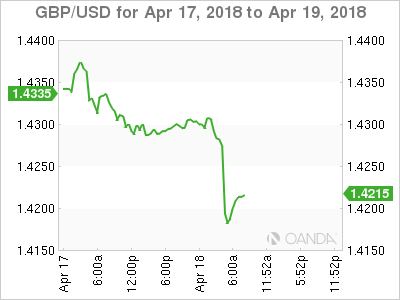

Sterling Sinks As Inflation Eases, Gold Range-Bound

Sterling's abrupt and aggressive depreciation following disappointing UK inflation data, continues to highlight how sensitive the currency is to monetary policy speculation.

UK headline inflation rate unexpectedly dropped to 2.5% in March, which immediately raised doubts over the Bank of England raising interest rates next month. With UK wage growth rising faster than inflation, the squeeze on consumers is slowly coming to an end. However, price action suggests that market players are concerned that today's soft inflation figures will lead the BoE to leave interest rates unchanged in May. Personally, I believe today's figures are unlikely to prevent the central bank from taking action next month. But if inflation continues to cool, this could cloud the prospects of higher interest rates beyond May, subsequently weighing on the British Pound.

Focusing on the technical picture, the GBPUSD has found itself under pressure on the daily charts, with prices tumbling towards 1.4180. Previous support around 1.4230 could transform into a dynamic resistance that encourages a decline towards 1.4100. If bulls are able to push the GBPUSD back above 1.4230, the next level of interest will be at 1.4300.

Dollar steady, but for how long?

Dollar steady, but for how long?

The Dollar remained steady against a basket of major currencies on Wednesday, after upbeat U.S data from the previous session supported appetite for the currency. Hawkish comments from Fed member John Williams supported the upside, with the Dollar Index trading around 89.66 as of writing.

The impact of Trump's tweet earlier in the week about China and Russia playing the “currency devaluation game” can still be seen in the Dollar's overall depressed price action. While positive economic data and U.S rate hike expectations could boost the Dollar, gains are at risk of being limited by geopolitical tensions, lingering trade war fears and Donald Trump. A lingering sense of caution over the U.S-China trade developments may still weigh on the Dollar, forcing the currency to remain shaky and wobbly.

Taking a look at the technical picture, the Dollar Index has found comfort within a wide range on the daily charts, with support at 88.50 and resistance at 90.50. A breakdown below the 89.50 could encourage a decline back towards 89.00. In an alternative scenario, bulls have a chance of challenging 90.50 if the Dollar Index is able to secure a daily close above 90.00.

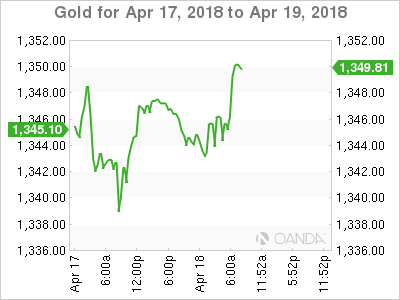

Commodity spotlight - Gold

Gold edged slightly lower during Wednesday's trading session with prices trading towards $1346 as the Dollar stabilised.

Price action suggests that the yellow metal remains in a wide range on the daily charts, with a directional catalyst needed for the next major move. While geopolitical tensions and U.S political uncertainty have inspired bulls, bears remain heavily supported by Fed rate hike expectations. There is clearly a fierce tug of war between bulls and bears. From a technical standpoint, the yellow metal has found minor support around $1340. If this level proves supportive, prices could venture towards $1353 and $1360, respectively. Alternatively, a decline back below $1340 may encourage a selloff towards $1324.

Phew! Dollar Finds Support Or Does It?

Wednesday April 18: Five things the markets are talking about

Global equities have drifted higher overnight, as investors take heart from a solid start to the earnings season and signs of improving relations between the U.S. and N. Korea.

In FX, the 'big' dollar has found a small bid after the Fed said yesterday that U.S industrial production rose last month, a sign of underlying strength in the economy. Output at factories, mines and utilities rose a seasonally adjusted +0.5% from the previous month.

Note: Market consensus had expected the index to rise +0.4%, while February's industrial production was revised to a +1% gain.

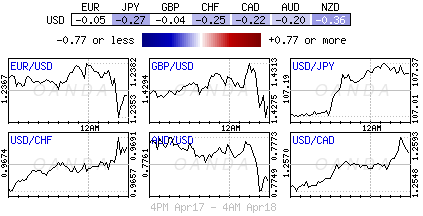

Sterling (£1.4186, down -0.75%) has been the big mover ahead of the U.S open, falling after U.K annual inflation for March came in below expectations (see below) – the headline print has hurt rate 'hawks' as the miss may reduce the prospects for a May rate hike by the Bank of England (BoE).

In Europe, regional annual inflation rate also missed expectations in March (+1.3% vs.+1.4%e), which highlights the recent cautious rhetoric from ECB officials.

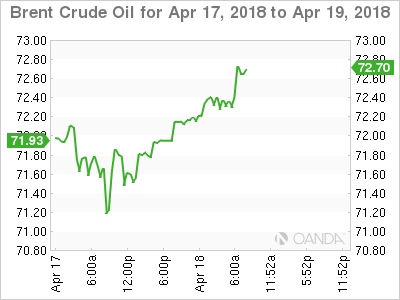

Elsewhere, oil has rebounded a tad after U.S crude stockpiles fell, while safe haven assets such as gold have declined.

On tap: The Bank of Canada (BoC) is next up with its monetary policy decision at 10:00 am EDT. Press conference is to follow at 11:15 am EDT.

1. Stocks in the 'black'

In Japan, the Nikkei share average raced to a seven-week high overnight, supported by risk appetite and a weaker yen lifting shares across the board. Also helping the mood was an easing political tension on the Korean peninsula. The Nikkei ended +1.4% higher, while the broader Topix rallied +1.1%.

Down-under, Australia's S&P ASX 200 rallied +0.3% on Wednesday, buoyed by mining shares, but gains were capped by losses in banking and healthcare stocks. In N. Korea, the Kospi ended higher, closing up +1.07%.

In Hong Kong, stocks rallied overnight, breaking a four-day losing streak, as China's surprise cut in banks' RRR supported financial shares. The Hang Seng index rose +0.7%, while the China Enterprises Index also gained +0.7%.

In China, banking firms also buoyed stocks. The blue-chip CSI300 index rose +0.5%, while the Shanghai Composite Index gained +0.8%.

In Europe, regional indices trade higher once again with notable strength in the FTSE 100 as weaker U.K inflation data lifts the index.

U.S stocks are set to open in the 'black' (+0.2%).

Indices: Stoxx600 +0.1% at 381.2, FTSE +0.8% at 7286, DAX +0.1% at 12601, CAC-40 +0.4% at 5374, IBEX-35 +0.2% at 9823, FTSE MIB +0.1% at 23675, SMI +0.7% at 8883, S&P 500 Futures +0.2%

2. Oil bid on fall in U.S inventories and global supply risks, gold lower

Oil prices are better bid, lifted by a reported decline in U.S crude inventories and by the ongoing risk of supply disruptions.

Brent crude oil futures are at +$72.07 per barrel, up +49c or +0.7%from Tuesdays close. U.S West Texas Intermediate (WTI) crude futures are up +49c, or +0.7% at +$67.01 a barrel.

Note: In the U.S, yesterday's API crude inventories numbers fell by -1m barrels last week to +428m barrels,

Expect the market to take its cue from today's weekly EIA report (10:30 am EDT).

Outside the U.S, oil markets continue to receive support from potential supply disruptions concerns in the Middle East, renewed U.S sanctions against Iran and falling output as a result of political and economic crisis in Venezuela.

Ahead of the U.S open, gold prices have slipped after rising for three consecutive sessions as investors opted for riskier assets, with the dollar holding its gains on the back of upbeat domestic economic data. Spot gold is down -0.3% at +$1,343.31 per ounce, while U.S gold futures for June delivery has fallen -0.2% to +$1,346.30 per ounce.

3. U.S short-term notes extend declines, narrowing 2/10's yield gap

The gap between short and long-term U.S. Treasury yields continued to shrink, which is reflecting market confidence that the Fed will keep raising interest rates even as investors grow sceptical about the outlook for economic growth and inflation.

Note: U.S 10-year Treasury note has backed up to +2.840%, while the yield on the two-year note is at +2.398%.

After widening early this year, the 2-10 spread has been shrinking for more than two months, resulting in a flatter yield curve. It's at +0.442% vs. +0.78% in early February.

Elsewhere, on weaker E.U and U.K inflation expectations Germany's 10-year yield has dipped -1 bps to +0.50%, the lowest in a week, while the 10-year Gilt yield sank -4 bps to +1.436% percent, the lowest in a week.

In China, their 10-year bond yield has also plummeted after the PBoC cut the reserve-requirement ratio for banks yesterday.

4. Dollar finds some support

The 'big' dollar is slightly better bid against G10 currency pairs, supported mostly by the continued disappointing inflation data out of Europe.

GBP/USD (£1.4191) is trading below the key £1.42 handle, falling -0.77% outright after this morning's disappointing March inflation data (see below). Market expectations for a May BoE rate hike have moved only marginally lower from +86% to around +78%, however, any additional hikes down the road is very much put in question.

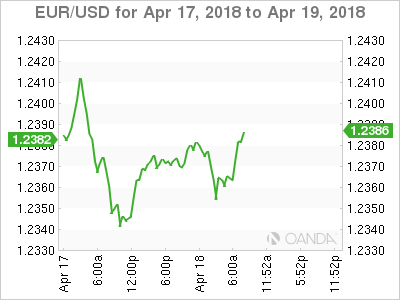

Like wise for the 'single' unit, the EUR/USD (€1.2365) is softer by -0.2% as this mornings March Final CPI data was revised lower to +1.3% vs. +1.4%e. The headline print supports the recent patience rhetoric from ECB members on achieving the inflation target.

USD/JPY (¥107.25) is a tad higher, helped by prospects of reduced trade tensions and an easing in geo-political tensions.

Note: President Trump to meet Japan's PM Abe today and there are reports that CIA Director Pompeo met with N. Korea leader Kim during visit to N. Korea over Easter.

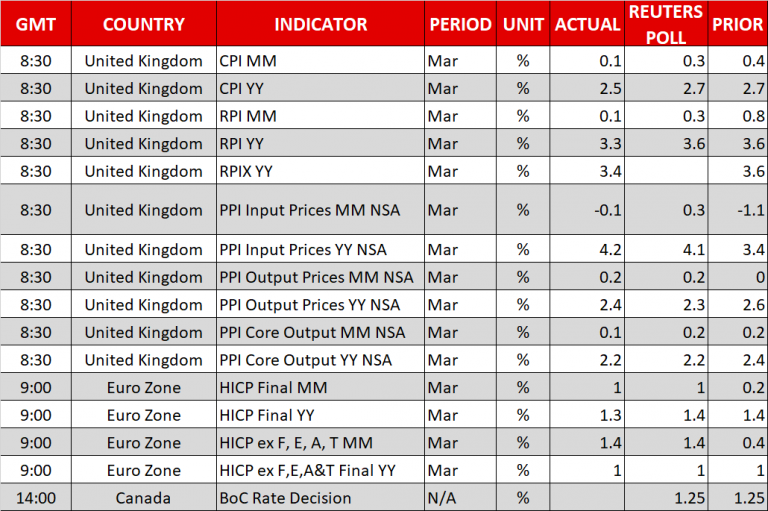

5. U.K inflation cooled in March

Data this morning that inflation in the U.K cooled by more than expected in March, but price-growth nevertheless remains well above the BoE's +2% annual target.

Consumer prices rose an annual +2.5% in March, which is a slower rate of growth than the +2.7% annual pace recorded in February.

Digging deeper, the slowdown was driven by clothing prices and prices for tobacco and alcohol, which increased in March at a much slower rate than they did a year earlier.

Note: The cooling in inflation may suggest that the squeeze on household budgets is coming to an end.

The BoE has telegraphed that it expects to lift its benchmark interest rate two or three times in the next few years to bring inflation back to its +2% annual target.

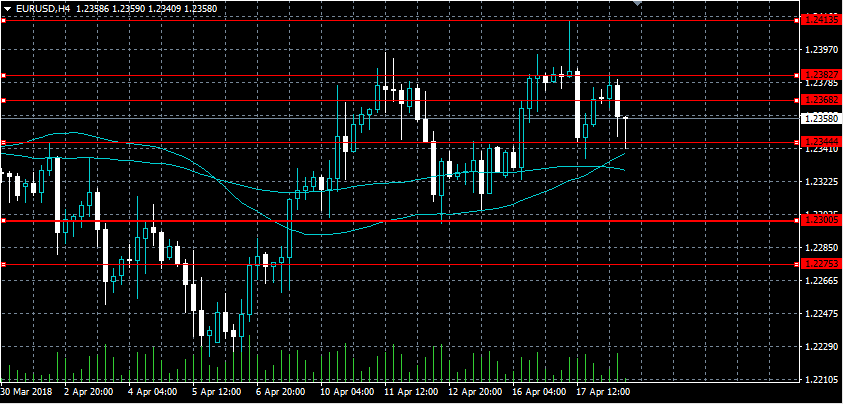

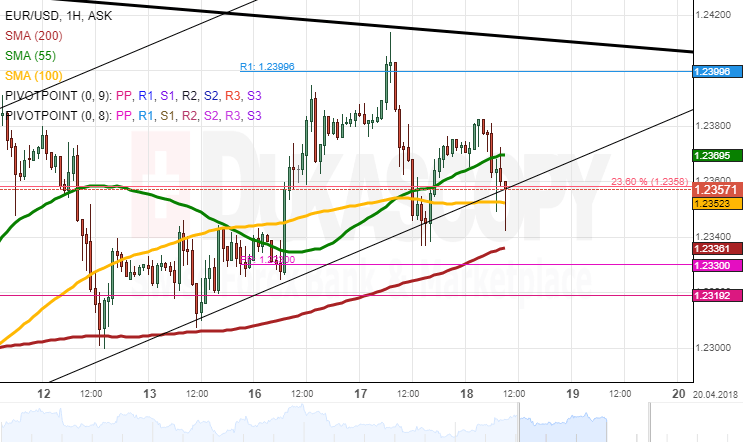

EURO Still Bearish Below 1.2382 Level

The euro remains under pressure against the U.S dollar, as weaker than expected EU inflation data, and a strong technical rejection from the key 1.2382 level weigh on intraday sentiment. The EURUSD pair currently trades around the 1.2360 level, after finding interim technical support from the 1.2341 level during the European trading session. Traders now look towards the next directional move in the U.S dollar index, and the release of the Federal Reserve Beige Book.

The EURUSD pair is intraday bearish while trading below the 1.2382 level, weekly support is found at the 1.2300 and 1.2275 levels.

Should the EURUSD pair start to trade above the 1.2382 resistance level, buyers may test the 1.2413 and 1.2430 levels.

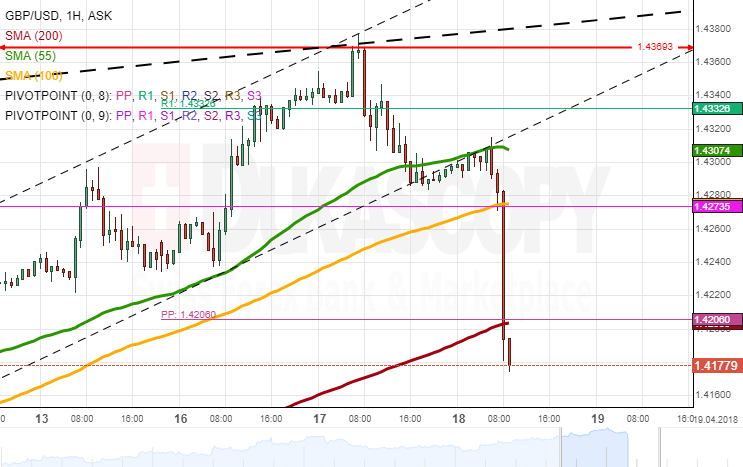

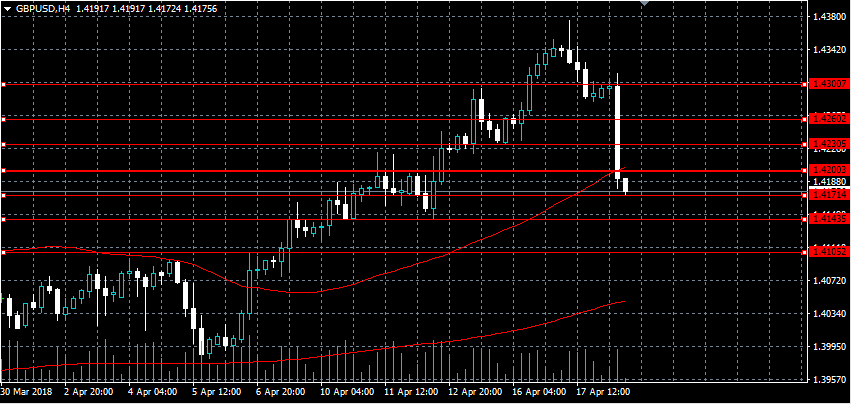

GBPUSD Weekly Bearish Below 1.4230 Level

The British pound has moved sharply lower against the U.S dollar, as key monthly inflation data from the United Kingdom economy came in much weaker than expected. The GBPUSD pair has so far lost over one-hundred and thirty pips, finding support from the 1.4171 technical level. Downside pressures are continuing to build around sterling, as today’s weaker than expected UK inflation data lessons the possibility of an upcoming rate hike from the BOE.

The GBPUSD pair is weekly bearish while trading below the 1.4230 level, key support is now found at the 1.4135 and 1.4105 levels.

If GBPUSD buyers manage to gain traction above the 1.4230 level, the pair may test back towards the 1.4260 and 1.4300 levels.

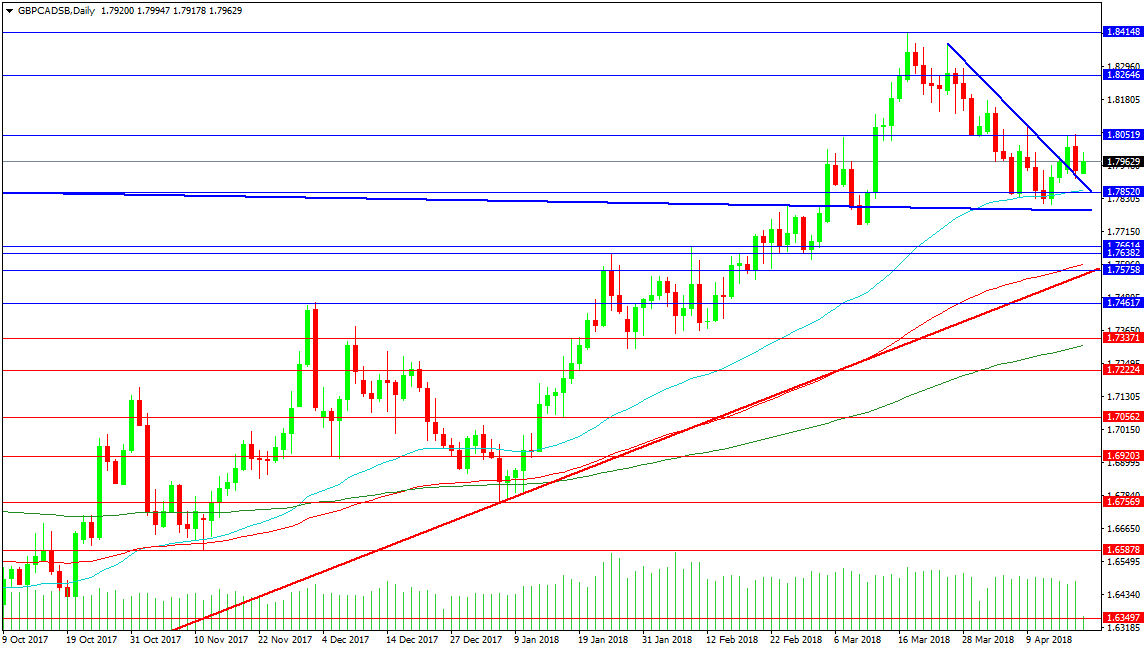

Forex Analysis: GBPCAD And USDJPY

The GBPCAD pair is holding just under 1.80000 after testing the level yesterday. The high at 1.80922 from the 9th of April takes on an important significance, as a move above this level would create a higher high and confirm a resumption of the move higher. The current retracement reached a low of 1.78080 last week, and this is forming the base that price has built from. A move higher would target the 1.82646 area, with the previous high at 1.84148. A break above here would target 1.85000, followed by 1.86254 in extension.

Support below the current price comes from last week’s low, followed by trend line support at 1.77936. A loss of this level would see price fall towards the dual supports at 1.76614 and 1.76382. The 100 DMA is located at 1.75965, with the rising red trend line at 1.75758, and this whole area is strongly supportive. Only a loss of this area would hand control over to bearish traders, by forcing longs to close, who would look to target the 200 DMA at 1.73117. A successful move under here could see the 1.70000 level tested.

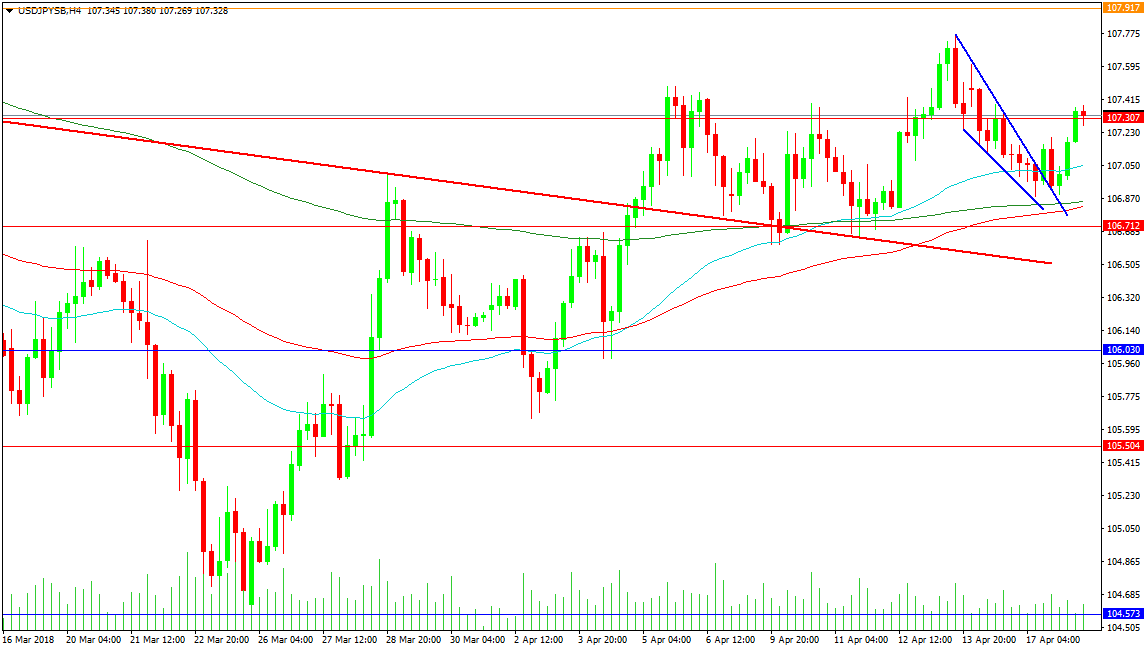

USDJPY

The USDJPY pair is painting a bullish picture and has tested the breakout at 107.000, which was supported by the 100 and 200-period MAs. A sustained move higher would target the recent high at 107.773, followed by the 107.917 level and the 108.000 area. Further resistance is found at 108.277 and 108.885, with 109.000 close by.

Support comes from the 107.000 area, with 106.712 providing support, before the red descending trend line at 106.450. A move below this area would target 106.000, followed by 105.500. The lows from late March come in at 104.573 and a visit of this area could provide the opportunity for a double bottom to form. However, if this level is breached, 104.000 may be retested, with 103.600 below, and, ultimately a move down to parity could be on the cards.

Pound Takes A Knock After CPI Miss, BoC Rate Decision Next

Here are the latest developments in global markets:

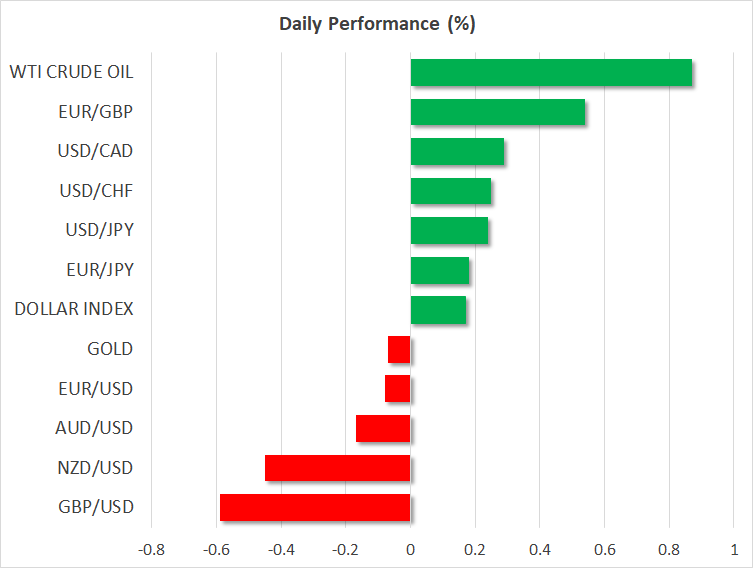

FOREX: The US dollar traded higher against the Japanese yen by 0.28% during the early European afternoon as risk-off sentiment continued to ease while encouraging data out of the US on Tuesday increased confidence on the US economy even further. Sterling plummeted near to a one-week trough of 1.4172 (-0.73%) versus the greenback today after UK CPI figures missed expectations, falling to one-year lows. The yearly Eurozone CPI (second estimate) also ticked below expectations today, adding some pressure to euro/dollar, but headlines stating that the President of the center-right Forza Italian party is meeting the Italian President on Wednesday in an effort to break the deadlock that has prevented the formation of a government, provided some support to the pair, driving it up to 1.2365 (-0.04%). Dollar/loonie extended gains towards 1.2584 (+0.33%) ahead of a policy meeting by Bank of Canada. Kiwi/dollar and aussie/dollar slipped by 0.46% and 0.21% respectively on the back of a stronger dollar. Swiss Franc was one of the worst performers. Euro/swissie rallied towards a fresh three-year peak of 1.1980, its highest level in three years – ever since the SNB removed the floor in the pair.

STOCKS: European markets were on the forefront on Wednesday at 0930 GMT, as investors monitored a fresh batch of corporate earnings and economic data. The benchmark European STOXX 600 rose by 0.09%. The blue-chip Euro STOXX 50 was up by 0.33%, while the German DAX 30 climbed by 0.07%. The French CAC 40 headed higher by 0.36%, the Spanish IBEX 35 rose by 0.19% and the British FTSE 100 moved up by 0.76%. In Asia, Japan’s Nikkei 225 and Topix surged by 1.42% and 1.14% respectively. In the US, the S&P, Dow Jones and the Nasdaq all surged yesterday, futures tracking these indices are currently in the red, pointing to a lower open today.

COMMODITIES: Oil prices extended their uptrend after the API report showed a surprising decline in US crude inventories on Tuesday. WTI crude surged by 1.17% to $67.30 per barrel and Brent moved up by 1.0% to $72.30 Gold fell by 0.19% to $1,344 per ounce.

Day ahead: Bank of Canada to stand pat on rates; Trump-Abe meeting concludes

A policy meeting by the Bank of Canada (BoC), discussions between the US President and the Japanese Prime Minister, as well as a Parliamentary Brexit vote in the UK will be the main economic events of the day.

At 1400 GMT, the BoC will reveal its decision on interest rates and expectations are for the central bank to keep rates unchanged at 1.25% after raising borrowing costs three times since July 2017. Although economic growth slowed down in Canada, the economy showed some positive signs since the previous policy gathering, including a pickup in inflation, a decline in the unemployment rate and an improvement in manufacturing activity, all of which could keep policymakers optimistic about the path of policy normalization. Moreover, and perhaps most importantly, NAFTA talks are seemingly showing progress lately, a fact that could give some relief to the central bank and be a reason for the BoC Governor, Steven Poloz, to use a more hawkish tone at his press conference today at 1515 GMT. However, Poloz could remain cautious on the face of trade uncertainties arising from the US trade policy which has spread fears of a global trade war. Should the BoC send hawkish messages, the loonie could erase today’s losses, while if the central bank gives more weight on trade risks, the currency could extend its losses.

In the US, the US President, Donald Trump, and the Japanese Prime Minister, Shinzo Abe, are concluding their two-day meeting and it would be interesting to see whether discussions have brought the countries closer on the trade front, as well their stance on North Korea. Earlier, Trump expressed his dissatisfaction with the Pacific free-trade pact which Japan is a proponent of, saying that he did not like the deal despite recent headlines supporting that he was thinking of re-join the partnership. On the other hand, his views on North Korea were more positive, commenting that “high level of talks” are underway between the US and North Korea, while also stating that five places are considered for the crucial summit between Trump and the North Korean leader, Kim Yong Un. Any references to China’s growing economic and military power could also attract attention.

Meanwhile in the UK, the House of Lords, the upper house of Parliament, where May’s Conservatives don’t hold a majority, is expected to vote on a Brexit bill on Wednesday. If the Lords oppose May’s proposal to exit the customs union with the EU, then the Prime Minister’s efforts to unify her party over Brexit could get more difficult given that some Conservatives also favour tariff-free trade with the EU.

Turning to data releases, the Energy Information Administration will report on US crude oil stocks for the week ending April 13 at 1430 GMT before the Federal Reserve’s Beige Book, which gives an overview on the current economic conditions in the US, comes into view at 1800 GMT. At 2245 GMT, New Zealand’s CPI readings are anticipated to indicate that inflation has picked up, rising by 0.5% q/q in the first quarter of 2018 compared to the 0.1% seen in the previous quarter, while on a yearly basis, the gauge is forecasted to slow down from 1.6% to 1.1%. Early on Thursday ( 0130 GMT), Australia will see the release of employment figures. Projections are for the number of positions added to the economy to increase by 21,000 in March – more than in February – and the unemployment rate to inch down by 0.1 percentage points to 5.5%.

In equity markets, eyes will be on Morgan Stanley’s earnings release delivered before Wednesday’s US market open.

In today’s public appearances, the New York Fed President William Dudley and Fed Vice Chair for Supervision Randal Quarles will be making comments at 1900 GMT and 2015 GMT respectively. Both hold permanent voting rights within the FOMC.

UK CPI Data Misses Expectations And Deflates BOE Hawks

Notes/Observations

- UK CPI misses expectations and hits a 1-year low; deflates some hawkish expectations of BOE but May hike still viewed but further hikes in question

- Euro Zone March Final CPI revised lower from 1.4% to 1.3%; highlights recent cautious rhetoric from ECB officials

Asia:

- Then US CIA Director Pompeo said to have met with North Korea leader Kim during visit to North Korea over Easter

- China NDRC noted that the impact from US/China trade frictions on domestic macro economy was limited and manageable. Trade protectionism to weigh on some sectors exports but had various contingency plans and policy reserves to deal with trade frictions started by the US

- Japan Mar Trade Balance beat expectations (¥797.3B v ¥449Be) as imports decline for the 1st time since 2016

Europe:

- PM May’s Brexit strategy said to face a renewed threat in House of Lords as a proposal to keep Britain in a customs union with the EU after leaving the bloc might pass by more than 50 votes

- EU said to prepare up to 40 law amendments in event of hard Brexit. Measure would cover a wide range of areas and also give special powers to regulators

- German Chancellor Merkel said to seek to strengthen role of economic ministers in EU

Americas:

- Fed's Bostic (FOMC voter, dove): Businesses are confused by direction of US trade policy; hearing about labor shortages everywhere

- Fed's Evans (non-voter, dove): can patiently react to incoming data; do not see outsized risk of inflation accelerating

- Trump administration reportedly to implement new policy that speeds up approval process for allies to complete major arms deals

- President Trump noted that Japan and South Korea would like US to go back into TPP. Trump did not like TPP deal for the US; bilateral trade deals were more efficient and profitable

Energy:

- Weekly API Oil Inventories: Crude: -1.0M v +1.8M prior

Economic Data:

- (EU) EU27 Mar New Car Registrations: -5.3% v +4.3% prior

- (AT) Austria Mar CPI M/M: 0.6% v 0.3% prior; Y/Y: 1.9% v 1.8% prior

- (CZ) Czech Feb Export Price Index Y/Y: -4.7% v -4.1% prior; Import Price Index Y/Y: -6.5% v -5.8% prior

- (CZ) Czech Mar PPI Industrial M/M: 0.3% v 0.0%e; Y/Y: +0.1% v -0.2%e

- (ZA) South Africa Mar CPI M/M: 0.4% v 0.6%e; Y/Y: 3.8% v 4.1%e

- (ZA) South Africa Mar CPI Core M/M: % v 0.8%e; Y/Y: 4.1% v 4.2%e

- (PL) Poland Mar Employment M/M: 0.1% v 0.1%e; Y/Y: 3.7% v 3.7%e

- (PL) Poland Mar Average Gross Wages M/M: 6.2% v 6.1%e; Y/Y: 6.7% v 6.6%e

- (IT) Italy Feb Industrial Orders M/M: -0.6% v -4.6% prior; Y/Y: 3.4% v 9.6% prior

- (IT) Italy Feb Industrial Sales M/M: +0.5% v -2.9% prior; Y/Y: 3.4% v 5.3% prior

- (UK) Mar CPI M/M: 0.1% v 0.3%e; Y/Y: 2.5% v 2.7%e (slowest annual pace in a year); CPI Core Y/Y: 2.3% v 2.5%e; CPIH Y/Y: 2.3% v 2.5%e

- (UK) Mar RPI M/M: 0.1% v 0.3%e; Y/Y: 3.33.5%e, RPI-X (ex-mortgage interest payment) Y/Y: 3.4% v 3.6%e, Retail Price Index: 278.3 v 278.8e

- (UK) Mar PPI Input M/M: -0.1% v +0.3%e; Y/Y: 4.2% v 4.3%e

- (UK) Mar PPI Output M/M: 0.2% v 0.1%e; Y/Y: 2.4% v 2.3%e

- (UK) Mar PPI Output Core M/M: 0.1% v 0.2%e; Y/Y: 2.2% v 2.2%e

- (UK) Feb ONS House Price Index Y/Y: 4.4% v 4.7%e

- (EU) Euro Zone Mar CPI M/M: 1.0% v 1.0%e; Y/Y (final): 1.3% v 1.4%e; CPI Core Y/Y (final): 1.0% v 1.0%e

- (EU) Euro Zone Feb Construction Output M/M: -0.5% v -0.8% prior; Y/Y: % v 6.9% prior

Fixed Income Issuance:

- (IN) India sold total INR150B vs. INR150B indicated in 3-month, 6-month and 12-month bills

- (DK) Denmark sold total DKK2.18B in 2023 and 2027 bonds

- (IT) Italy Debt Agency (Tesoro) bond exchange results: Sold €2.0B in Nov 2021 BTP in switch; bought €2.0B via 5 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.1% at 381.2, FTSE +0.8% at 7286, DAX +0.1% at 12601, CAC-40 +0.4% at 5374, IBEX-35 +0.2% at 9823, FTSE MIB +0.1% at 23675, SMI +0.7% at 8883, S&P 500 Futures +0.2%]

- Market Focal Points/Key Themes: European Indices trade higher once again with notable strength in the FTSE 100 as weaker inflation data lifted the index. European Indices track US futures higher on the back of positive earnings out of the US and Europe, with shares of Danone rising after Q1 results and LFL sales which came ahead of estimates. In other earnings related moves, Vopak, Telford Homes and Barco trade higher, while Heineken and Remy Cointreau among some of the names moving lower. Continental shares fell after cutting outlook currency valuation effects. In the M&A space, Direct Energie trades over 30% higher after Total acquired a majority stake for €1.4B; Shares of Intu trade lower after Hammerson recommends withdrawal of its $5B offer. Looking ahead, notable earners include Textron, Morgan Stanley and Abbot Labs.

Movers

- Consumer Discretionary [Heineken [HEIA.NL] -2.1% (Earnings)]

- Consumer Staples [ Danone [BN.FR] +3.0% (Earnings)]

- Industrials [Getlink [GET.FR] +0.7% (Earnings), Continental [CON.DE] -3.3% (Cuts Margin outlook)]

- Utilities [ Direct Energie [DIREN.FR] +30.3% (Total acquires majority stake)]

- Technology [ ASML [ASML.NL] -1.2% (Earnings) ]

- Real Estate [ Vopak [VPK.NL] +4.1% (Earnings), Intu [INTU.UK] -4.5%, Hammerson [HMSO.UK] +2.2% (hammerson recommends withdrawal of offer for INTU), Telford [TEF.UK] +2.8% (Earnings)]

Speakers

- EU's Tusk stated that saw positive momentum in Brexit talks adding that the UK must help resolve the Irish border issue. EU economy was back at pre-crisis level and that strengthening of EU banking union was a priority. Reiterated call for permanent exemption from US metal tariffs

- EU Trade Chief Malmstrom reiterated the view of seeking an unconditional waiver on US metal tariffs; move by US seen as pure protectionism

- Italy President Mattarella to meet with Senate Speaker Casellati (**Note: reports circulated that Italy Senate Speaker Casellati could be selected by President Mattarella for an exploratory mandate aimed at building a parliamentary majority for the next govt)

- Hungary Central Bank Dep Gov Nagy: Needed to increase lending in economy and target a 12% annual pace

- Japan Chief Cabinet Sec Suga: Will explain to Parliament why Fin Min Aso needs to attend G20; need to fulfill responsibility as next-year G20 host (**Note: Japan Diet Committee would not approve request for FIn Min Aso to attend G-20 meeting)

Currencies

- USD began the session with a slight bid against the major pairs. The greenback aided by continued disappoint inflation data out of Europe

- GBP/USD fell over 100 pips as March CPI data missed expectations with the YoY reading coming in at 2.5%. This was the lowest CPI reading in a year but still above the BOE inflation target of 2% for the 16th straight month. Algo trading initially sold the GBP currency in the aftermath of the data then real money flows kicked in. Expectations of a May BOE rate hike moved only marginally lower from 86% to around 80% but any additional hike doown the road was put into question. Pair below 1.42 just ahead of the NY morning.

- EUR/USD softer by 0.2% as the March Final CPI data was revised lower to 1.3%. The data reinforced recent patience from ECB members on achieving the inflation target.

- USD/JPY higher aided by prospects of reduced trade tensions and an easing in geo-political tensions. PresidentTrump to meet Japan PM Abe in Florida today. Yen also softer after reports that then US CIA Director Pompeo met with North Korea leader Kim during visit to North Korea over Easter

- EUR/CHF edged closer towards the 1.2000 handle which is a level last tested back in Jan 2015 when the SNB abandon its floor in the cross.

Fixed Income

- Bund Futures trade 8 ticks higher at 159.47 as Germany's 10-year bond yield falls back below the 0.50% level. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 122.73 higher by 62 ticks, extending its gains after softer than expected UK inflation data. Support continues stands at 121.25 then 120.85, with upside resistance at 123.35 then 123.85.

- Wednesday’s liquidity report showed Tuesday's excess liquidity fell to €1.857T from €1.868T prior. Use of the marginal lending facility increased from €133M to €170M.

Looking Ahead

- (SA) Saudi Arabia Feb Oil production – JODI

- 05:30 (DE) Germany to sell €3.0B in 0.05% Feb 2028 Bunds

- 06:00 (PT) Portugal Mar PPI M/M: No est v 0.1% prior; Y/Y: No est v 1.4% prior

- 06:45 (US) Daily Libor Fixing

- 07:00 (RU) Russia to sell OFZ bonds

- 07:00 (US) MBA Mortgage Applications w/e Apr 13th: No est v -1.9% prior

- 07:00 (BR) Brazil Apr IGP-M Inflation (2nd Preview): 0.3%e v 0.6% prior

- 07:00 (ZA) South Africa Feb Retail Sales M/M: 0.1%e v -1.6% prior; Y/Y: 3.0%e v 3.1% prior

- 08:05 (UK) Baltic Dry Bulk Index - 08:30 (US) Fed’s Dudley (dove, FOMC voter) at community bank conference

- 09:00 (RU) Russia Mar Unemployment Rate: 5.0%e v 5.0% prior; Real Wages Y/Y: 8.0%e v 9.7% prior; Real Disposable Income Y/Y: 3.1%e v 4.4% prior

- 09:00 (RU) Russia Mar Real Retail Sales Y/Y: 2.1%e v 1.8% prior

- 09:15 (UK) BOE FPC Brazier, Kohn and Taylor testify in Parliament

- 10:00 (CA) Bank of Canada (BOC) Interest Rate Decision: Expected to leave Interest Rate unchanged at 1.25%

- 09:45 (UK) BOE to buy £1.22B in in APF Gilt purchase operation (7-15-years)

- 10:30 (US) Weekly DOE Crude Oil Inventories

- 15:15 (US) Fed's Dudley (dove, FOMC voter) on economic outlook

- 16:15 (US) Fed's Quarles (hawk, FOMC voter) in Washington DC

- 17:00 (KR) South Korea Mar PPI Y/Y: No est v 1.3% prior

- 17:30 (US) Trump-Abe press conference

Euro Ajnalysis: Likely To Push For Senior Channel

On Tuesday, the common European currency once again failed to overcome the psychological 1.24 mark which has worked as a strong resistance this month.

Being pressured by the weekly R1, the pair reversed from this level and was pushed back down to the 55– and 100-hour SMAs and a junior channel line circa 1.2350. The Euro could go for a re-test of the senior pattern during the first part of the day, as the 55-hour SMA is likely to hinder an immediate breakout south.

However, given the pair's ability to accelerate during the past trading sessions, the bearish sentiment should eventually take the dominant hand. A significant fall is not expected to occur today due to the 100– and 200-hour SMAs and the weekly and monthly PPs located nearby in the 1.2350/1.2300 area.

GBPUSD Analysis: Rades Along 55-Hour SMA

After hitting the upper boundary of a short-term channel and a trend-line at 1.4370, the Sterling began its decline towards the 1.43 mark.

This bearish momentum was caused primarily by sluggish US average earnings report. It caused a fall of 50 pips as a result of which the Pound breached the 55-hour SMA. However, it remained at this line during the Asia session, demonstrating that bulls are still trying to regain their lost positions.

If this moving average is breached, the next target should be the weekly R2 at 1.4424. On the other hand, the pair is supported by the 100-hour SMA near 1.4270. This line is likely to restrict a deeper fall down to the weekly PP and the 200-hour SMA at 1.42 for some time.

The British CPI at 0830GMT is likely to guide the market sentiment for several hours.