Sample Category Title

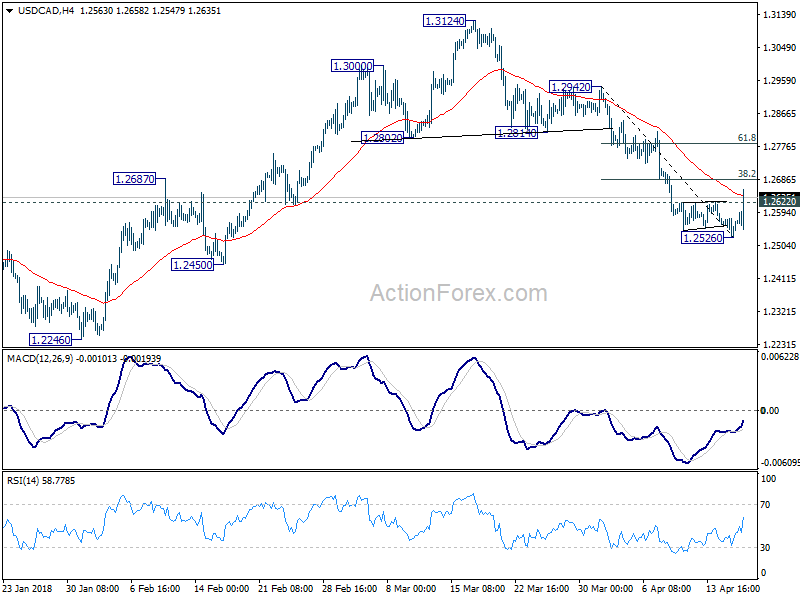

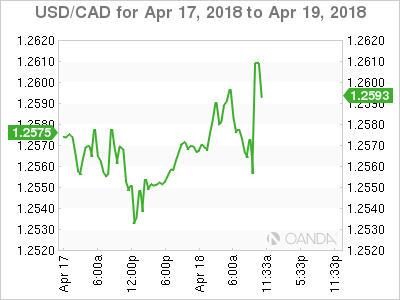

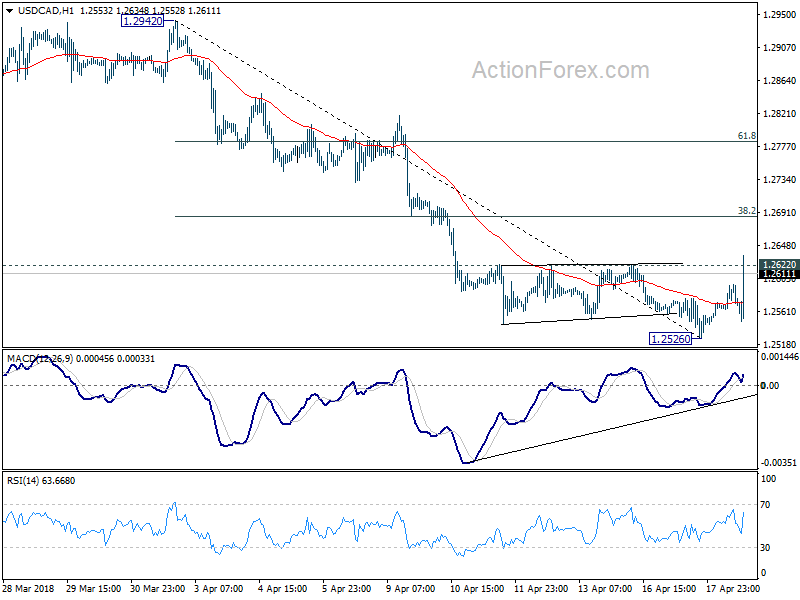

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2526; (P) 1.2552; (R1) 1.2577; More....

USD/CAD's strong rebound and break of 1.2622 minor resistance indicates short term bottoming at 1.2526. Intraday bias is mildly on the upside for recovery back to 38.2% retracement of 1.2942 to 1.2526 at 1.2685, or even further to 55 day EMA (now at 1.2730). But upside should be limited well below 1.2814 support turned resistance and bring fall resumption. We'd expect decline from 1.3124 to extend later to 1.2061/2246 support zone.

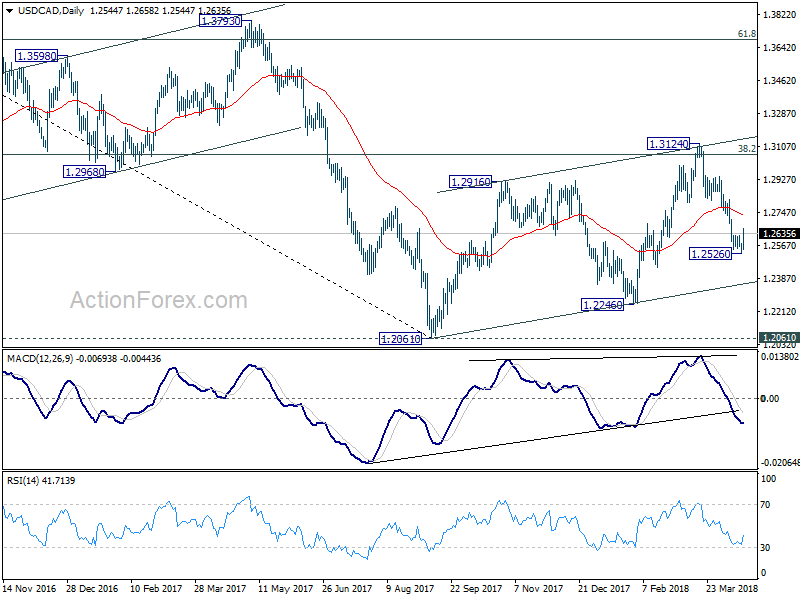

In the bigger picture, current development turns favors to the case that rise from 1.2061 is a corrective three wave pattern. It could have completed at 1.3124 after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Focus is now back on 1.2061 and 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Decisive break there will resume larger down trend from 1.4689 (2016 high) to 61.8% retracement of 0.9406 to 1.4689 at 1.1424.

In the bigger picture, current development turns favors to the case that rise from 1.2061 is a corrective three wave pattern. It could have completed at 1.3124 after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Focus is now back on 1.2061 and 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Decisive break there will resume larger down trend from 1.4689 (2016 high) to 61.8% retracement of 0.9406 to 1.4689 at 1.1424.

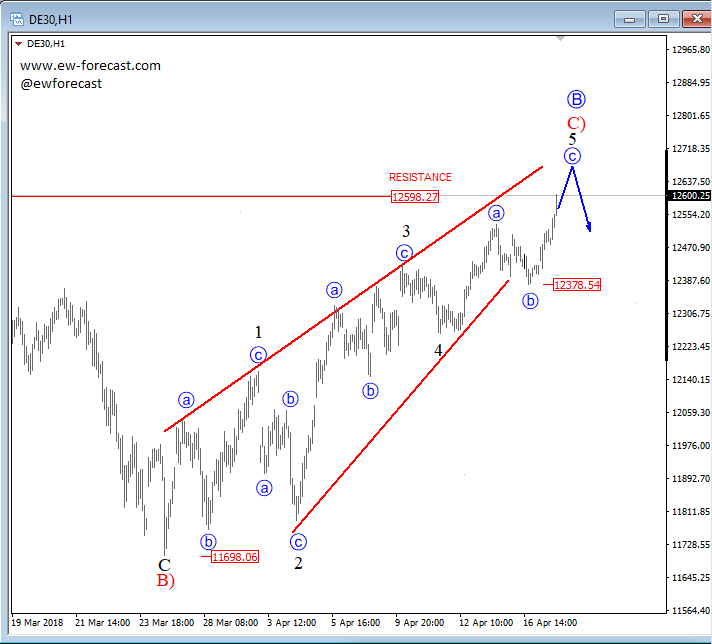

Elliott Wave Analysis: German DAX Can Be At Resistance

German Dax is pointing to a bearish reversal after price unfolded a five-wave recovery within higher degree wave C). We are tracking a five-wave, overlapping recovery which just touched potential resistance levels at 12598-12641 level, which can push price lower. Also the equality measurement of waves a and b project end of a sub-wave 5 of C). If we get a turn in impulsive fashion and below the 12378 level, then bears will be confirmed.

German Dax, 1h

BoC: Poloz Holds for Today with an Unchanged Message

As was widely expected, the Bank of Canada held its key monetary policy interest rate at 1.25%.

The Bank simultaneously released its latest Monetary Policy Report (MPR), providing an update on how the Bank sees the economy evolving. In the event, the growth outlook for this year was revised down slightly, to 2% (from 2.2%). This appears to largely reflect the soft start to the year, which is expected to give way to healthy growth in the second quarter. In contrast, the 2019 forecast saw a marked upgrade, from 1.6% to 2.1% on a stronger consumption outlook and slower imports. Newly included, a 1.8% growth pace is seen for 2020, in line with the economy's (upwardly revised) trend.

On that front, perhaps the most notable part of today's communications is a sizeable change to the Bank's view of potential (or trend) real GDP growth. The range for 2017-2019 has been raised by roughly 0.4 percentage points. As a result, the Bank now sees the economy as having almost, but not quite reached its potential, rather than being at or slightly above it at the end of last year.

Most standard frameworks suggest that with more slack comes less inflationary pressure, and this appears to be the case for the Bank. Recent inflationary pressures are seen as partially temporary, owing to minimum wage increases and other transitory effects. Inflation is expected to moderate to just above the 2% target in 2019 and 2020 as these effects diminish.

A key focus for the Bank of Canada has been assessing labour market slack. The MPR notes improving conditions, but areas of concern remain: youth labour market participation is still seen as soft, while long-term unemployment is seen as elevated. All told, the Bank maintains a constructive outlook for labour markets, and has provided something of a benchmark: 3% growth in wages are seen as consistent with no labour market slack. For reference, their preferred measure, 'Wage-common', read 2.7% in 2017Q4, the most recent data available.

The MPR also provided an update to the key economic risks as seen by the Bank of Canada. First on the list is weaker investment and exports, a reflection of both recent soft trade data and uncertainty around NAFTA and the global trading system more generally. The second risk was also to the downside, with a sharp tightening in global financial conditions possible. Rounding out the risks were the possibility of stronger U.S. GDP growth (upside), stronger consumption (and debt growth) here in Canada (near-term upside), and a pronounced decline in Canadian home prices (downside).

Key Implications

The core message sent today appears to be that Poloz and company remain set on further hikes, but are in no rush to get there. The statement accompanying the decision may have had a hint of hawkishness to it, but the details of the Monetary Policy Report were decidedly dovish.

Indeed, with the Banks assessment of the economy's 'cruising speed' getting a sizeable upgrade (and economic 'tightness' getting a downgrade by extension), it is no surprise that the Bank sees only modest underlying inflationary pressures. Moreover, the Bank continues to see pockets of weakness in labour markets, and while recent developments have been promising, NAFTA negotiations and trade developments more generally remain a cloud over the forecast.

As a result, despite many moving pieces, the outlook for rates remains effectively unchanged. More hikes are coming, with this summer remaining the likely target for the next move, but the path is by no means set. Labour market developments (particularly wages), core inflation measures, and the evolution of business investment are likely to be the key domestic metrics influencing the timing of the next hike.

Yen Ticks Higher, Japanese Inflation Report Next

USD/JPY has posted small gains in the Wednesday session. In North American trade, USD/JPY is trading at 107.15, up 0.13% on the day. On the release front, there are no key US events. The markets will be listening to speeches from FOMC members John Williams and Randal Quarles. On Thursday, the US releases unemployment claims and the Philly Fed Manufacturing Index. Japan will release National Core CPI.

The recent trade battle between the US and China has been overshadowed by events in Syria, but the threat of further tariffs between the world’s largest two economies could again roil the markets and in turn, send gold prices higher. Another salvo was fired on Tuesday, as China slapped a tariff of some 179% on US sorghum crops, which is a livestock feed. China imports about $1 billion of sorghum annually, and the tariff, if it remains in place, will essentially halt US exports of sorghum to China. The Chinese government has threatened to impose tariffs on US soybean exports, valued at some $12 billion each year. If the US opts to retaliate, the specter of an ugly trade war between the US and China could spook investors and boost the safe-haven Japanese currency.

With the huge fluctuations that Bitcoin has exhibited in recent months, there has been plenty of press about cryptocurrencies. The proliferation of cryptocurrencies has led to discussions about central bank-issued digital currencies (CBDC), and their effect on the global financial scene. At a banking conference earlier this week, BoJ Deputy Governor Masayoshi Amamiya said that CBDC would have a negative impact on the current financial system, but added that cryptocurrencies could find a role with central banks, such as in payment and settlement transactions. Currently, the BoJ and ECB are involved in a joint initiative, Project Stella, which is examining the use of Blockchain in securities transactions.

BoC Stands Pat – CAD Plummets

No Surprise

As expected the Bank of Canada (BoC) held its benchmark interest rate steady (+1.25%) this morning as it warned “rising geopolitical and trade conflicts risk undermining global growth.”

The BoC expects inflation will move higher this year before returning close to its +2% target in 2019.

“Despite strengthening global demand, growth of business investment in export-oriented goods industries is anticipated to be restrained by elevated uncertainty around trade policy, regulatory concerns and incentives to shift investment to the United States following the U.S. tax reform,” the Bank of Canada said in a policy report that accompanied the rate decision.

Note: The BoC has raised its key interest rate three times since mid-2017, most recently in January.

It said on Wednesday that it anticipates higher rates will be warranted over time but added that it would remain cautious and use incoming economic data to guide its decisions.

Loonie Takes a Dive

CAD (C$1.2638) has come under immediate pressure, falling -80 pts outright to take shy of strong dollar resistance at C$1.2650.

Next up is Governor Poloz press conference at 11:15 am EDT

CAD dips as BoC signals it’s not ready for rate hike yet

CAD trades notably lower after BoC rate announcement. Overnight rate target was kept at 1.25% as widely expected. The key takeaway from the statement is that the "higher interest rates will be warranted over time", but "some monetary policy accommodation" will be needed. "Governing Council will remain cautious in considering future policy adjustments", as "guided by incoming data". And the "economy's sensitivity to interest rates, the evolution of economic capacity" and "dynamics of both wage growth and inflation" will be watched. Basically, these were the elements mentioned in the last paragraph of March statement, just juggled into different place.

In short, BoC is making itself quite clear that it's not ready to have another rate hike yet.

USD/CAD's rebound and break of 1.2622 minor resistance suggests that a short term bottom was formed at 1.2526. More consolidation would be seen, with risk of stronger recovery. But still, decline from 1.2942 is expected to resume at a later stage.

Sunset Market Commentary

Markets:

Global core bond trading remained constraint to existing consolidation ranges. Both the Bund and the US Note future set an intraday high after the release of lower than forecast UK inflation numbers (spill-over via UK Gilt market) However, that uptick was short-lived and both had a slightly downwardly oriented bias afterwards in absence of strong trading themes. A small downward revision to EMU headline inflation couldn’t change that. Risk sentiment on stock markets was stable. The US yield curve bear flattened again with yield changes ranging between +1.7 bps (2-yr) and -0.8 bps (30-yr). Hawkish March FOMC Minutes and recent Fed comments triggered the new underperformance of the front end of the US yield curve with the 2-yr yield above 2.4% for the first time since 2008. German yields increase by 0.1 bp (30-yr) to 1.4 bps (5-yr).

There were some tentative signs of a USD rebound this morning. During the morning session, EUR/USD even spiked temporary lower to the mid 1.23 area as EMU March inflation was downwardly revised to 1.3% from 1.4%. However, the dollar wasn’t able to build on this temporary euro weakness later in the session. On the contrary, EUR/USD rebounded back higher in the 1.23 big figure. USD/JPY also reversed part this morning’s cautious gains. The pair trades again in the 107.20 area even as risk sentiment remains constructive. EUR/USD and USD/JPY continue trading within the established ranges. For now any USD up-ticks are still used to reduce USD long positions.

Sterling tested important MT technical resistance against the euro (EUR/GBP 0.8650 area) and the dollar (GBP/USD 1.4345) over the previous days. It even looked that sterling was ready for a sustained break higher. However, today’s UK inflation data finally aborted the sterling positive momentum, at least temporary. UK headline inflation declined to 2.5% Y/Y from 2.7% Y/Y (a stabilization was expected). Core inflation also eased to 2.3%. The inflation outcome is softer than expected. However, we don’t expect today’s inflation outcome to derail the scenario of a May BoE rate hike. Over the previous year and a half, higher inflation eroded Britons real wages/income. This process might halt if the decline in inflation persists. This is a positive for private consumption/growth. The report thus shouldn’t make the BoE change its mind on implementing some cautious policy normalization in May. The jury is still out whether a further rate hike later this year will be needed. Inflation data understandably triggered profit taking in sterling. EUR/GBP jumped from the 0.8640 area and settled in the low 0.87 area. Cable dropped from 1.43+ levels and trades currently in the 1.42 area. The report broke the short-term positive momentum of sterling, However, we don’t expect it to become a start of a real sterling downtrend, unless other high profile news kicks in.

News Headlines:

Turkish President Erdogan called for early elections on June 24, moving them forward by more than a year from their scheduled date. The Turkish lira gains ground after the announcement with EUR/TRY dropping from 5.08 to 5.02.

Top oil exporter Saudi Arabia would be happy to see crude rise to $80 or even $100 a barrel, three industry sources said, a sign Riyadh will seek no changes to an OPEC supply-cutting deal even though the agreement's original target is within sight.

Italian President Mattarella offered Senate leader Casellati (Forza Italia) an “exploratory mandate” to form a government nearly seven weeks after an inconclusive election led to a hung parliament.

(BoC) Bank of Canada Maintains Overnight Rate Target at 1 ¼ Per cent

The Bank of Canada today maintained its target for the overnight rate at 1 ¼ per cent. The Bank Rate is correspondingly 1 ½ per cent and the deposit rate is 1 per cent.

Inflation in Canada is close to 2 per cent as temporary factors that have been weighing on inflation have largely dissipated, as expected. Consistent with an economy operating with little slack, core measures of inflation have continued to edge up and are all now close to 2 per cent. The transitory impact of higher gasoline prices and recent minimum wage increases will likely cause inflation in 2018 to be modestly higher than the Bank expected in its January Monetary Policy Report (MPR), returning to the 2 per cent target for the rest of the projection horizon.

The global economy is on a modestly stronger track than forecast in January, with upward revisions to growth and potential output in a number of major advanced economies. The outlook for the U.S. economy has been further boosted by new government spending plans. However, escalating geopolitical and trade conflicts risk undermining the global expansion.

In Canada, GDP growth in the first quarter was weaker than the Bank had expected, but should rebound in the second quarter, resulting in 2 per cent average growth in the first half of 2018. The economy is projected to operate slightly above its potential over the next three years, with real GDP growth of about 2 per cent in both 2018 and 2019, and 1.8 per cent in 2020. This stronger profile for GDP incorporates new provincial and federal fiscal measures announced since January. It also reflects upward revisions to estimates of potential output growth, which suggest the Canadian economy has made some progress in building capacity.

Slower economic growth in the first quarter primarily reflects weakness in two areas. Housing markets responded to new mortgage guidelines and other policy measures by pulling forward transactions to late 2017. Exports also faltered, partly owing to transportation bottlenecks. Some of the weakness in housing and exports is expected to be unwound as 2018 progresses.

The Bank anticipates that Canadian exports will strengthen as foreign demand increases, but not sufficiently to recover the ground lost during recent quarters. Export growth is being increasingly limited by capacity constraints in some sectors. Continued gains in business investment should build additional capacity in those sectors and in the economy more generally. However, both exports and investment are being held back by ongoing competitiveness challenges and uncertainty about trade policies.

Growth in consumption remains robust, supported by strong labour income growth. Wages have continued to pick up as expected, even after factoring out recent minimum wage increases in Ontario and Alberta. The Bank will continue to assess labour market data for signs of remaining slack.

Some progress has been made on the key issues being watched closely by Governing Council, particularly the dynamics of inflation and wage growth. This progress reinforces Governing Council’s view that higher interest rates will be warranted over time, although some monetary policy accommodation will still be needed to keep inflation on target. The Bank will also continue to monitor the economy’s sensitivity to interest rate movements and the evolution of economic capacity. In this context, Governing Council will remain cautious with respect to future policy adjustments, guided by incoming data.

Information note

The next scheduled date for announcing the overnight rate target is May 30, 2018. The next full update of the Bank’s outlook for the economy and inflation, including risks to the projection, will be published in the MPR on July 11, 2018.

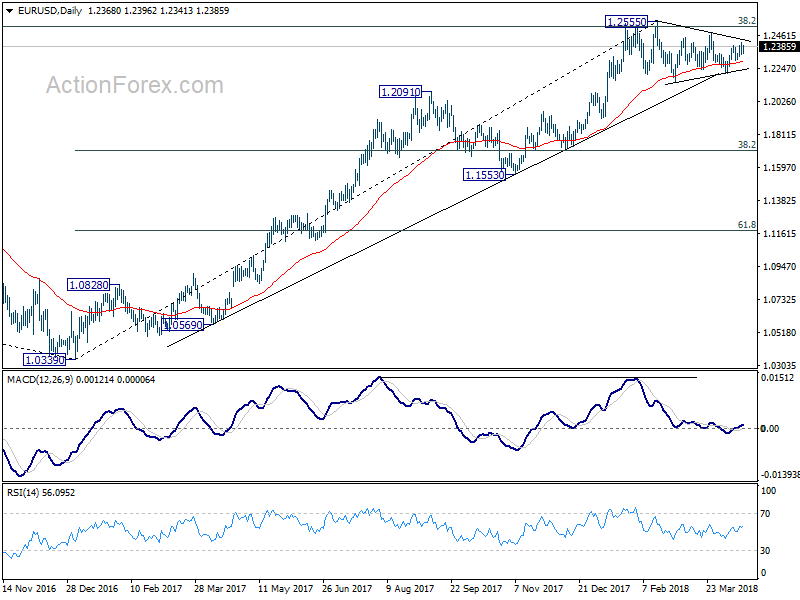

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2332; (P) 1.2372 (R1) 1.2410; More....

EUR/USD is drawing support from 4 hour 55 EMA, but it's staying below 1.2413 temporary top. Intraday bias remains neutral first. On the upside, above 1.2413 will extend the rebound from 1.2214 to 1.2475 resistance. Break will target 1.2516/2555 key resistance zone. On the downside, however, break of 1.2214 will revive the case of trend reversal and turn outlook bearish.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

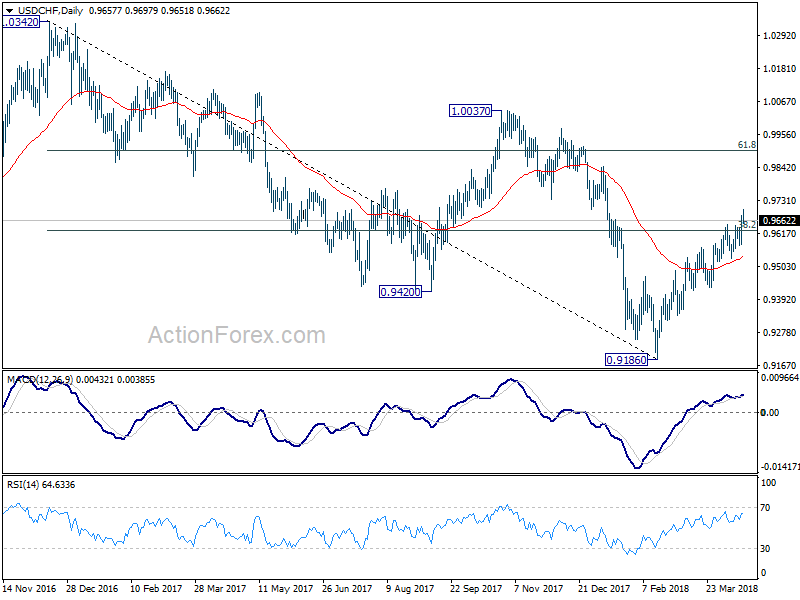

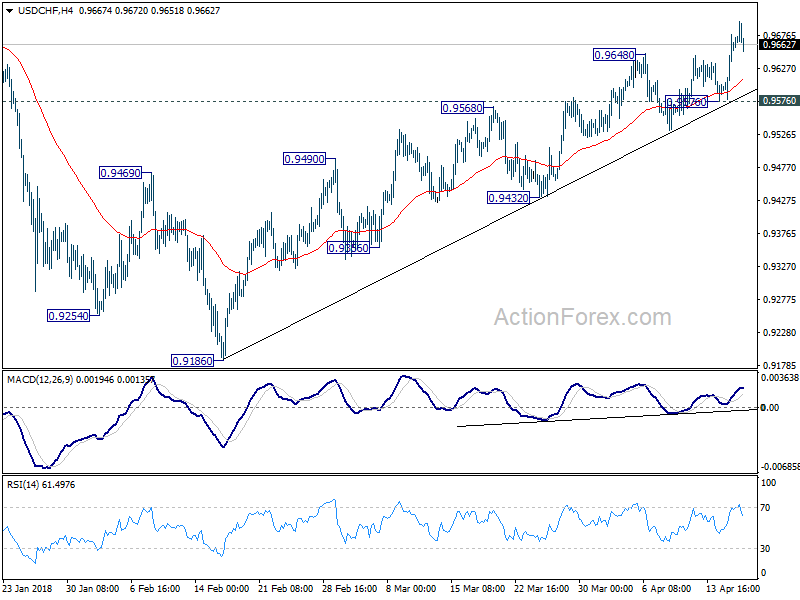

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9571; (P) 0.9604; (R1) 0.9631; More...

Intraday bias in USD/CHF remains on the upside despite slight retreat from 0.9697. Current rally from 0.9186 should target 0.9900 fibonacci level next. On the downside, break of 0.9576 minor support is needed to be the first sign of short term topping. Otherwise, outlook will remain bullish in case of deeper retreat.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next.