Sample Category Title

Can EUR/GBP Hold Gains Above 0.8680?

Key Highlights

- The Euro started a nice upside move from the 0.8620 low against the British Pound.

- The EUR/GBP pair is attempting an upside break above a crucial bearish trend line at 0.8695 on the 4-hours chart.

- The UK CPI in March 2018 increased 2.5% (YoY), less than the forecast of +2.7%.

- Today, the UK Retail Sales report for March 2018 will be released, which is forecasted to decline by 0.5% (MoM).

EURGBP Technical Analysis

The Euro found a strong support near the 0.8620 level against the British Pound recently and started an upside move. The EUR/GBP pair grinded higher and broke the 0.8650 and 0.8680 resistance levels.

More importantly, the pair moved above the 50% Fib retracement level of the last decline from the 0.8739 high to 0.8620 low. The pair seems to be trading with a bullish bias above the 0.8680 level.

Additionally, the pair is attempting an upside break above a crucial bearish trend line at 0.8695 on the 4-hours chart. On the upside, the 100 simple moving average (red, 4-hours) is positioned at 0.8718 to act as a hurdle for buyers.

A push above the 100 SMA and the 0.8720 level could open the doors for more gains in the near term. On the flip side, if the pair corrects lower, the 0.8680 and 0.8650 levels are likely to act as a strong support levels.

Recently, the UK saw the release of the CPI by the National Statistics. The market was looking was a rise of 0.3% in the CPI in March 2018 compared with the previous month.

However, the result was on the lower side as there was a rise of 0.1% in the CPI, which was also less than the last +0.4%. In terms of the yearly change, the CPI came in at 2.5%, which was less than the forecast of +2.7%.

The report added:

Price movements for alcoholic drinks and tobacco also made a downward contribution to the change in the rate; this in part reflects changes to the Budget cycle that were introduced in 2017, with tax changes for tobacco being announced in November 2017 instead of March 2018.

There was a downside reaction in GBP/USD and EUR/GBP moved higher. Going forward, today’s retail sales report could define the next move in the British Pound.

Economic Releases to Watch Today

- UK Retail Sales for March 2018 (YoY) – Forecast +2.0%, versus +1.5% previous.

- UK Retail Sales for March 2018 (MoM) – Forecast -0.5%, versus +0.8% previous.

- UK Retail Sales ex-fuel for March 2018 (YoY) – Forecast +1.4% versus +1.1% previous.

- US Initial Jobless Claims – Forecast 230K, versus 233K previous.

Commodities Steal The Show

Commodities Steal the Show

Commodities stole the show overnight led by WTI which soared to a three year on the DOE report while industrial metals catapulted higher on the likelihood that an extension of Russian sanctions will hit like a sledgehammer at the heart of the nation’s mining complex. But not to be outdone, Gold shot up in glittering fashion on haven demand while catching a fillip from the underlying move in commodity prices.

Following two days of scintillating gains, Wall Street investors were quick to pare some risk after shaky earning results from IBM. Also, US Treasury yields have woken from their slumber and were playing a bit of catch-up on the back of improved risk sentiment, which also contributed to mixed day on Wall Street.

Earnings will remain the key this week so even with the energy sector surging; investors are still looking for specific evidence of strong corporate performance.

Oil prices

If you need any convincing, we are in the midst of an oil bull market look no further than the abundance of signals overnight. Oil Bulls shifted into overdrive when official DoE inventory report confirmed overly bullish indications on US supply. Total inventories showed a draw of -1.07mn in line with the API print on Tuesday. But Gasoline inventories declined more than expected with a draw of -2.968mn vs -2.5mn shown in API. These are peak driving season type gasoline numbers, and we’re only in April, not July !!

Also, further OPEC compliance appears on the cards as the partners are unlikely to change the oil supply deal in June regardless of the state of global inventories. But the icing on the cake was a Saudi report ( recycled mind you as it was kicked around last week) that the kingdom targeting $80, “or even $100,” according to reports from a closed-door meeting of Saudi officials from last week.

In Canada, a possible rail strike could bottleneck flow from Western Canadian oil producers which adds to the bullish tone.

Supply disruptions and lower US inventories make a very compelling argument to enter or stay long OIL, even at these lofty levels.

Gold Prices

A very productive overnight session for Gold despite the relaxation of global political risks. But in reality, there remains immense practicability to store gold in inventory these days. But again we find ourselves testing the upper end of the current range and looking for that key catalyst to get the market over the top. Without rehashing the contemporary risk narratives ( Trade war and Middle East tension ) that are providing few if any conclusions this week, But given that any one of some catalysts could trigger a global stock market meltdown, for that reason alone gold has to be an essential component in any portfolio.

Currency Markets

The British Pound

The Sterling Bulls got summarily smacked on the disappointing CPI miss overnight. But with trader positions, much more balanced and CPI considered an infamously lagging indicator, Sterling at this critical support level would likely attract some buying interest. The UK economic activity does warrant a rate hike in May, and despite the market getting spooked, we could see calmer head prevail over the near term and another push higher.

The Japanese Yen

It feels like we’re in Fast Forward to summer doldrums but despite equity market trading constructively a very positive US macro backdrop. While current market conditions suggest a push higher to 108+, headline risk is likely holding traders at bay.

The Malaysian Ringgit

Energy prices remain incredibly supportive for the Ringgit which will likely temper any further weakness ahead of the elections. But we expect tight trading ranges to persist on the back of little local bond activity. And what is trading is moving in a sideways fashion.

Risk sentiment is improving, and the Yuan traded favourably all suggesting that the MYR should trend positively. But with the pre-election political malaise hanging over Malaysia Capital markets local currency gains will be relatively muted.

Eco Data 4/19/18

[php_everywhere instance="1"]

Bank of Canada Holds Rates Steady, Maintains Flexible Tightening Bias

Highlights:

- The overnight rate was held steady at 1.25% for a second consecutive meeting.

- The BoC marked down their Q1 growth forecast but attributed some of the slowing to temporary factors. Activity is expected to rebound in Q2.

- Annual GDP growth is expected to be close to 2% this year and next—a slight upward revision, on balance, that reflects additional fiscal stimulus and slightly stronger potential growth.

- The bank revised up their potential growth estimates to 1.8% this year and next (previously 1.6%). Stronger estimated potential growth last year means the economy likely ended 2017 with slightly more slack than previously thought.

Inflation is expected to rise above the bank’s 2% target this year though the overshoot reflects transitory factors such as higher energy prices and the impact of minimum wage hikes. Inflation is expected to return to target next year.

Our Take:

Today’s steady rate decision was widely expected (analyst expectations close to unanimous, markets priced for only ~10% odds of a hike) but Governor Poloz still managed to land on the dovish side. The BoC’s forward guidance has been that interest rates are likely to move higher over time but policy will have to remain somewhat accommodative to counteract a number of headwinds facing the economy (competitiveness challenges, concerns about trade policy, high household debt). More emphasis on those headwinds, along with shifting goal posts for the economy’s output gap and potential growth, left the bank sounding more cautious than we were expecting.

Today’s meeting provided little clarity on when the BoC will next raise rates. Governor Poloz indicated that most of the Governing Council’s deliberations “concerned the appropriate pace of interest rate increases” but he declined to reveal whether a rate hike was discussed. The bank once again emphasized data dependence but that wasn’t fully evident in today’s comments. An upward trend in wages and inflation was only enough to increase the bank’s confidence in their tightening bias. And a positive Business Outlook Survey, flagged by Deputy Governor Lane as an “important indicator” just last month, seemed to take a backseat to the bank’s judgment on how trade uncertainty and competitiveness challenges are affecting the economy. Slower growth early this year might have provided some justification for a cautious tone, but the bank attributed much of the shortfall to temporary factors.

We still think a further increase in inflation and rebound in Q2 GDP growth will keep the Bank of Canada raising interest rates this year. But today’s emphasis on caution over data underlined downside risks to our forecast for three more hikes in 2018.

Bank of Canada Maintains Benchmark Rate

The Bank of Canada (BoC) kept its benchmark rate at 1.25 percent in April, and is taking a more cautious approach to adjusting rates in the face of softer economic data and geopolitical uncertainty.

Overnight Lending Rate Steady at 1.25 Percent

The BoC maintained its overnight target lending rate at 1.25 percent at its April policy announcement, in line with consensus expectations. The BoC has increased benchmark rates three times since July 2017, most recently in January, but is taking a more restrained approach to further rate hikes.

Economic data came in somewhat softer to start 2017, giving space to hold off on further rate increases. Employment growth surprised to the downside in February, posting a flat-out decline, though a pickup in full-time jobs in March helped employment recover for Q1. GDP growth also came in weaker than expected, posting a 0.1 percent decline in January that reflected housing market and export weakness.

The BoC concluded its policy statement, which accompanies the rate announcement, with what we interpret as a dovish tone. It highlighted "some" progress on key issues of inflation and wage growth, which should warrant higher interest rates "over time." However, the Bank also emphasized a "cautious" near-term approach, informed by monitoring the economy's sensitivity to interest rates and economic capacity.

How Close to Full Capacity?

Canada's economy grew a breakneck 3.0 percent in 2017 as a whole, lifted by strong contributions from consumer spending and business investment. Even with some slowing in 2018 so far, the fast pace of growth has eaten up resource slack; industrial capacity utilization rates edged up in every quarter of 2017 and the Canadian unemployment rate, at 5.8 percent in March, is the lowest in 40 years. These measures paint a picture of a Canadian economy operating near full capacity, and would point to rising inflation pressures.

While the BoC acknowledges that "the economy is projected to operate slightly above its potential over the next the years," Governor Stephen Poloz has emphasized that untapped potential remains. In a March speech to students at Queen's University, Poloz highlighted that there remains room to draw more youth and women into the labor force, which would ease labor supply constraints. Additionally, increased business investment brought by stronger economic growth is likely to help build out capacity in the economy.

Core measures of consumer price inflation in Canada have edged up, and are currently right around the BoC's symmetric 2 percent target. Along with resource constraints, higher gasoline prices and minimum wage increases this year in Ontario and Alberta are likely to be supportive of inflation over the near term. However, an inflation overshoot is not a large enough concern at this point to force the BoC's hand in doling out faster rate increases. More significant right now than inflation are risks to the economic outlook posed by slower growth, elevated household debt and uncertainty over NAFTA. Given these considerations, we maintain our call for one more hike in 2018.

AUD’s unconvincing strength ahead of Australia employment data

After a rather long day with UK CPI and BoC as main events, GBP and CAD are set to end as the weakest ones. CAD is performing worst, as followed by GBP. GBP is indeed quite resilient from our point of view. For the time being, GBP/USD is still holding above 1.4144, GBPJPY above 151.15 and EUR/GBP below 0.8379. There is no avalanche selloff. On the other hand, EUR and AUD are being the strongest ones.

Taking a look at AUD action bias table, it's rather neutral against USD, EUR and JPY. GBPAUD shows downside action bias in H and 6H, neutral D and upside W. H and 6H movements look counter trend and that's why D is neutral.

Taking a look at AUD action bias table, it's rather neutral against USD, EUR and JPY. GBPAUD shows downside action bias in H and 6H, neutral D and upside W. H and 6H movements look counter trend and that's why D is neutral.

Similarly, AUDCAD show upside action bias in H and 6H, neutral D and downside W. The H and 6H movements are counter trend.

Similarly, AUDCAD show upside action bias in H and 6H, neutral D and downside W. The H and 6H movements are counter trend.

These counter trend movements are ok for quick intraday or swing pattern trades. But until they're prove to be reversals, for position trading, they're rather forgettable.

And, bear in mind that Australian employment data is upcoming in Asian session. Probably by then, AUD will show its true color.

-- What is trade is as important as how to trade.

Gold Steady, Markets Await Unemployment Claims

Gold has edged higher in the Wednesday session. In the North American session, the spot price for an ounce of gold is $1350.29, up 0.23% on the day. In economic news, there are no major indicators. On Thursday, the US releases unemployment claims and the Philly Fed Manufacturing Index.

After last week’s strong fluctuations, gold prices have steadied this week. The volatility has been closely connected to escalating tensions over a chemical attack by the Syrian government on rebel positions. There was uncertainty throughout last week about whether the US would respond, but the markets have settled down since a US-led strike hit Syrian weapon centers on the weekend. Investor risk appetite has improved, but concerns that tensions could quickly reignite have meant that investors are not dumping gold holdings in favor of riskier assets just yet. After the weekend attack, President Trump declaration of “mission accomplished” means that things will remain relatively quiet in Syria. However, further chemical attacks by the Syrian regime could trigger a response from the US and its allies, which could result in volatility in the markets, similar to what occurred last week.

The recent trade battle between the US and China has been overshadowed by events in Syria, but the threat of further tariffs between the world’s largest two economies could again roil the markets and in turn, send gold prices higher. Another salvo was fired on Tuesday, as China slapped a tariff of some 179% on US sorghum crops, which is a livestock feed. China imports about $1 billion of sorghum annually, and the tariff, if it remains in place, will essentially halt US exports of sorghum to China. The Chinese government has threatened to impose tariffs on US soybean exports, valued at some $12 billion each year. If the US opts to retaliate, the specter of an ugly trade war between the US and China could spook investors and send gold to higher levels.

Pound Slips as Inflation Comes Up Short

The British pound has posted losses in the Wednesday session. In North American trade, GBP/USD is trading at 1.4220, down 0.48% on the day. On the release front, the UK released a host of inflation indicators, led by the consumer price index. CPI for March dipped to 2.5%, falling short of the estimate of 2.7%. There are no major US indicators on the schedule. On Thursday, the UK releases retail sales. The US will publish unemployment claims and the Philly Fed Manufacturing Index.

Inflation continues to weaken in the UK. The April consumer price index dropped to 2.5%, after six consecutive readings of around 3.0 percent. The soft reading surprised the markets, and the pound responded with losses. The real producer index and other inflation indicators also missed their estimates. However, the markets still expect the Bank of England to raise rates at next month’s policy meeting. Policymakers in favor of a rate hike can point to the fact that inflation still remains well above the BoE target of 2 percent and the labor market remains tight. The pound has jumped more than 5% against the greenback this year, and if the BoE raises rates next month, the pound will likely make further gains.

The recent trade battle between the US and China has been overshadowed by events in Syria, but the threat of further tariffs between the world’s largest two economies could again roil the markets and in turn, send gold prices higher. Another salvo was fired on Tuesday, as China slapped a tariff of some 179% on US sorghum crops, which is a livestock feed. China imports about $1 billion of sorghum annually, and the tariff, if it remains in place, will essentially halt US exports of sorghum to China. The Chinese government has threatened to impose tariffs on US soybean exports, valued at some $12 billion each year. If the US opts to retaliate, the specter of an ugly trade war between the US and China could spook investors and boost the US dollar against the British pound and other rivals.

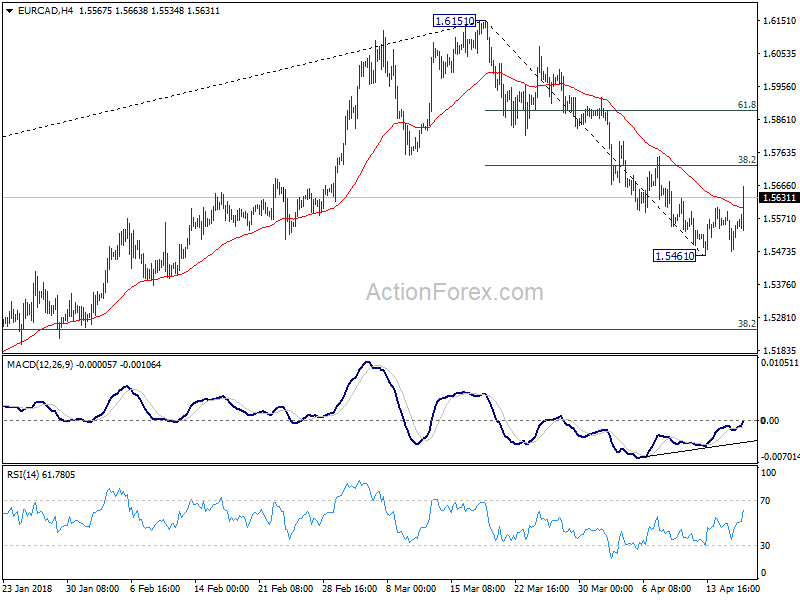

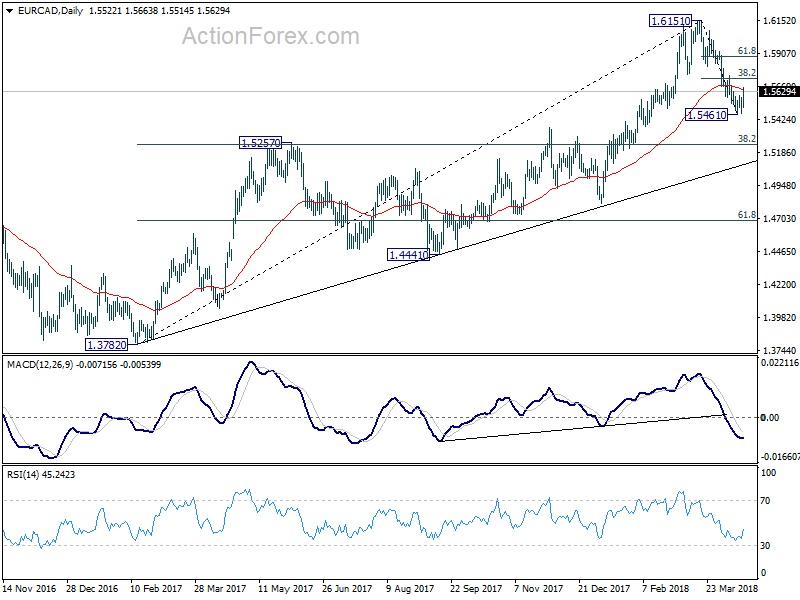

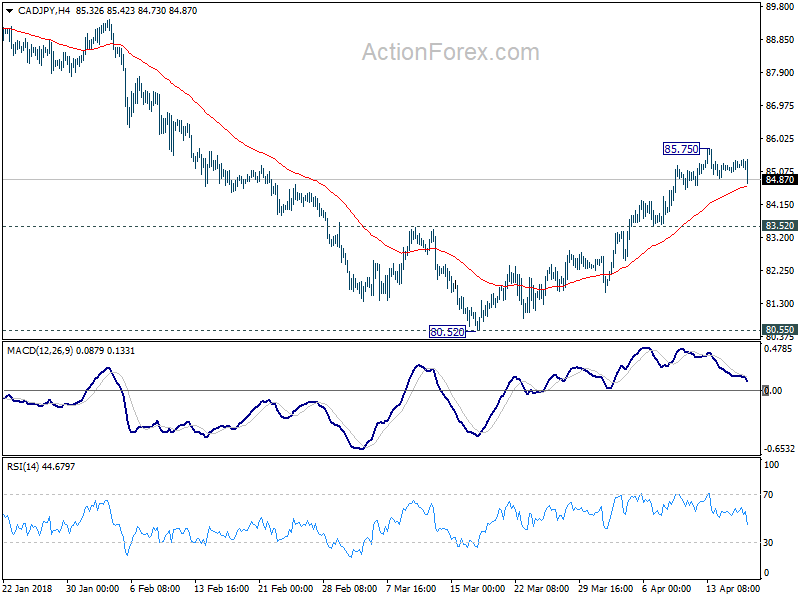

CAD selloff resumes as BoC Poloz offered nothing special, a look at EURCAD and CADJPY

CAD's selloff resumes after BoC governor Stephen Poloz's press conference offered nothing special.

EUR/CAD's rebound today indicates short term bottoming at 1.5461, on bullish convergence condition in 4 hour MACD. Further rise would be seen to 38.2% retracement of 1.6151 to 1.5461 at 1.5725 first.

Currently, the decline from 1.6151 is seen as a corrective move, as it's held well above 1.5257 key cluster support. Hence, break of 1.5725 will target 61.8% retracement at 1.5887 and above.

Currently, the decline from 1.6151 is seen as a corrective move, as it's held well above 1.5257 key cluster support. Hence, break of 1.5725 will target 61.8% retracement at 1.5887 and above.

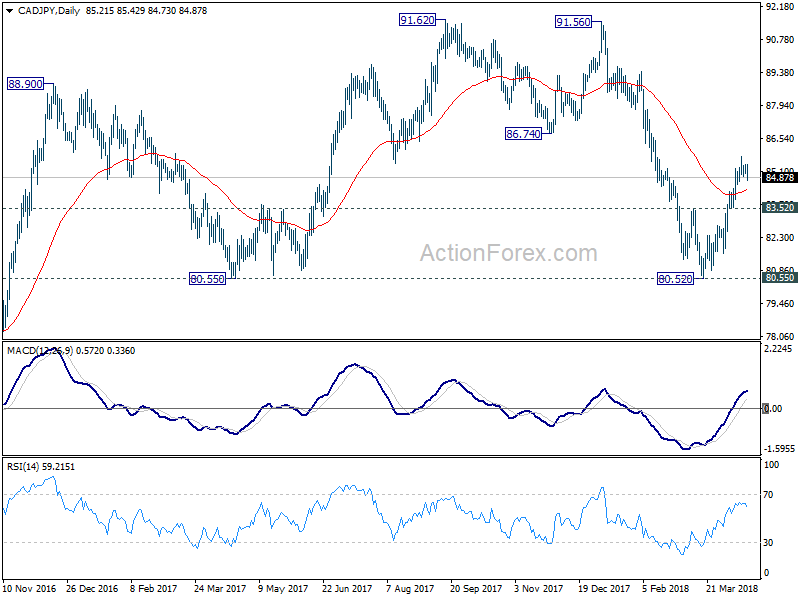

CAD/JPY's pull back also suggest that short term topping at 85.75. And deeper retreat could be seen.

CAD/JPY's pull back also suggest that short term topping at 85.75. And deeper retreat could be seen.

However, note that CAD/JPY drew strong support from 80.55 and rebounded. The fall from 91.56 is likely completed at 80.52. For now, we'd stay bullish as long as 83.52 minor support holds. And, we'd expect another rise through 85.75 to 91.56 high later.

However, note that CAD/JPY drew strong support from 80.55 and rebounded. The fall from 91.56 is likely completed at 80.52. For now, we'd stay bullish as long as 83.52 minor support holds. And, we'd expect another rise through 85.75 to 91.56 high later.

Oil Prices Extend Rally as US Inventories Unexpectedly Declined

The report from the US Energy Information Administration (EIA) shows that total crude oil and petroleum products stocks slumped -10.58 mmb to 1180.97 mmb in the week ended April 13. Crude oil inventory dropped -1.07 mmb to 427.57 mmb, amidst decreases in 3 out of 5 PADDs. Stockpile in PADD 3 dropped -1.5 mmb for the week. Cushing stock dropped -1.12 mmb to 34.91 mmb. Utilization rate decreased -1.1% to 92.4%. Meanwhile, crude production increased +0.14M bpd to 10.54M bpd for the week.

For refined oil products, gasoline inventory plunged -2.97 mmb to 235.97 mmb as demand jumped +6.3% to 9.86M bpd. Production added +0.53% to 10.2M bpd while imports gained +7.63% to 0.71M bpd during the week. Distillate inventory reduced -3.12 mmb to 125.34 mmb as demand soared +4.46% to 4.36M bpd. Production fell -3.08% to 5.09M bpd while imports declined -17.6% to 0.1M bpd during the week.