Sample Category Title

BoC Holds Rates Steady

The U.S. dollar was seen trading mixed across the board on Wednesday. Data from the UK showed that consumer prices slowed even further, rising just 2.5% on the year ending March. This was well below expectations of a 2.7% increase. Core CPI was also weaker, posting an increase of 2.3% on the year, slowing from 2.4% previously.

Inflation data from the Eurozone showed that headline inflation rate slowed to a pace of 1.3% in the year ending March compared to February's print of 1.4%. Core CPI for the Eurozone was steady at 1.0% as forecast.

The Bank of Canada was seen holding the interest rates steady at 1.25% but the central bank signaled hawkish views which sent the Canadian dollar briefly higher on the day.

Looking ahead, the economic calendar for the day will start off with the release of the retail sales report from the UK. Economists' polled forecast a 0.5% decline in retail sales for the month of March. This marks a contraction in retail sales compared to February's print of 0.8%.

Later in the day, FOMC member, Lael Brainard will be speaking. Brainard is expected to maintain her hawkish views on the economy. On the economic front, the data from the U.S. will cover the Philly Fed manufacturing index which is expected to fall to 20.8.

Other Fed members due to speak over the week include Loretta Mester.

Investors Switch Focus From Trade To Fundamentals

Equities in Asia received a boosttoday, as a result of higher commodity prices and strong U.S. earnings announcements. Energy and mining stocks are leading the gains this morning, as Brent and WTI traded at their highest levels since late 2014. Oil found support after data from the Energy Information Administration showed that crude inventories dropped 1.1 million barrels in the week to 13 April, while gasoline and distillate stockpiles fell by more than 3 million barrels. Now it is OPEC and Co.’s turn to capitalize on the bullish report as they meet in Jeddah on Friday.

While the elimination of oversupply has been a critical factor pushing oil prices, I still believe there’s a significant risk premium being priced in, specifically the fear of supply disruption from the Middle East and possible renewed sanctions on Russia and Iran. Although OPEC may send signals of extending the supply cut deal, I think a target price of $80 to $100 is unrealistic. U.S. Shale now has more incentive to boost production,especiallysincethey can hedge at very attractive prices. Now, we can expect U.S. output to exceed 11 million barrels sooner than expected.

Base and precious metals also rose strongly, pushing the CoreCommodity CRB Index to itshighest level since mid-2015. Should central banks be worrying about being behind the curve when it comes to inflation? Next month, we will probably get to know the impact of rising commodity prices on consumer inflation.

While the rise in commodities and robust earnings send positive signals to investors, fixed income markets are sending opposite signs. The U.S. yield curve has been making headlines for some time, and the yield between 10 and 2-year treasury bonds shrank to 41 basis points yesterday, the lowest since 2007. If the yield curve inverted within sixmonths, as St. Louis Fed President James Bullard suggested, it will be an indication that a chance of a recession becomes very likely. This is happening at a time when global debt is at historic highs, according to the IMF. Total debt reached a record $164 trillion last year.

In currency markets, Sterling will attract the most attention, after disappointing economic data pulled GBPUSD from its highest levels since the Brexit vote. While wage growth data supported the chance of a Bank of England rate hike, yesterday’s Consumer Price Index report showed there’s no need to hurry. If today’s retail sales badly disappoint, I think there’s a high chance that the BoE will postpone the rate hike until June, suggesting that Sterling could see further declines towards 1.40.

Ethreum Boosted By The End Of US Tax Season

After weeks of decline, ethereum soared yesterday to reach a multi-week high of $530. The gains corresponded with the end of the US tax season. Traders believe that the submission of capital gains taxes will attract more capital to cryptocurrencies.

The boost also came after Reuters reported major funding for a company creating a stable coin built on the ethereum blockchain. Intangible Labs received more than $133 million from leading private equity and venture firms like Bain Capital, Andreessen Horowitz and Lightspeed Ventures.

Other cryptocurrencies have also gained with bitcoin, litecoin, and ripple rising by 4%, 12%, and 13% respectively in the past five days.

The currencies rose despite an investigation by the New York Attorney General, Eric Schneiderman, into major exchanges including Coinbase and Binance. According to Mr. Schneiderman, the firms are not being investigated for any crimes. Instead, his office wants to learn about their businesses with the aim of protecting customers.

Meanwhile, cryptocurrency risks were highlighted yesterday when a company that raised $50 million in an ICO disappeared. The German company’s CEO sent a tweet thanking his investors and saying “Over and Out”. The website of the company showed a picture mocking his investors.

The RSI of ETH/USD is currently at 65, heading south while the MACD is showing signs of further upward moves. There is a likelihood that the pair will continue moving higher if the current market conditions – based on no major negative news – remain.

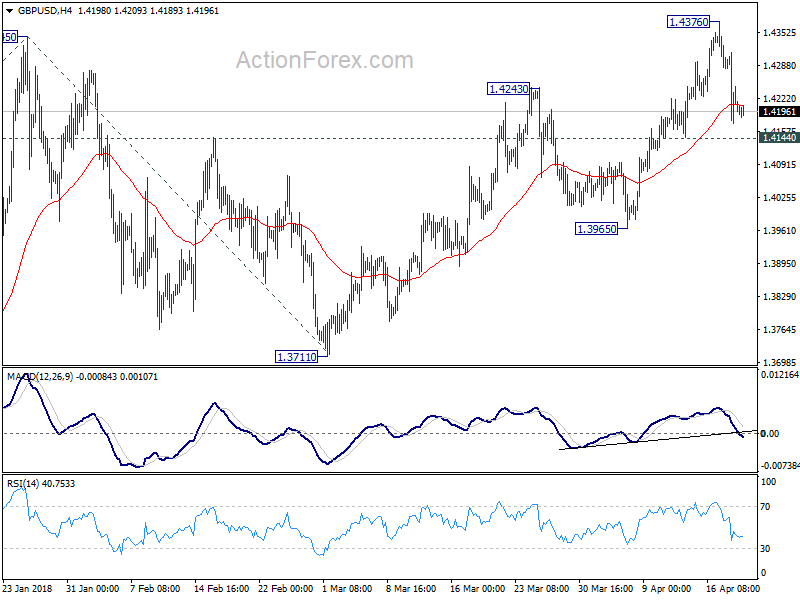

GBPUSD Trading Below Key Weekly Pivot

The British pound remains under downside pressure against the U.S dollar, as softer than expected UK inflation data continues to weigh on sterling sentiment. The GBPUSD pair currently trades around the 1.4200 level, after earlier being swiftly sold-off from the 1.4245 resistance level, after finding interim technical support from the 1.4171 level. Traders now look to key Retail Sales data from the United Kingdom economy, with the pair now weekly bearish while trading below the 1.4230 level.

The GBPUSD pair remains bearish while trading below the 1.4230 level, key intraday resistance is now found at the 1.4181 and 1.4146 levels.

If the GBPUSD pair holds above the 1.4230 level, buyers may move price-action back towards the 1.4260 and 1.4300 levels.

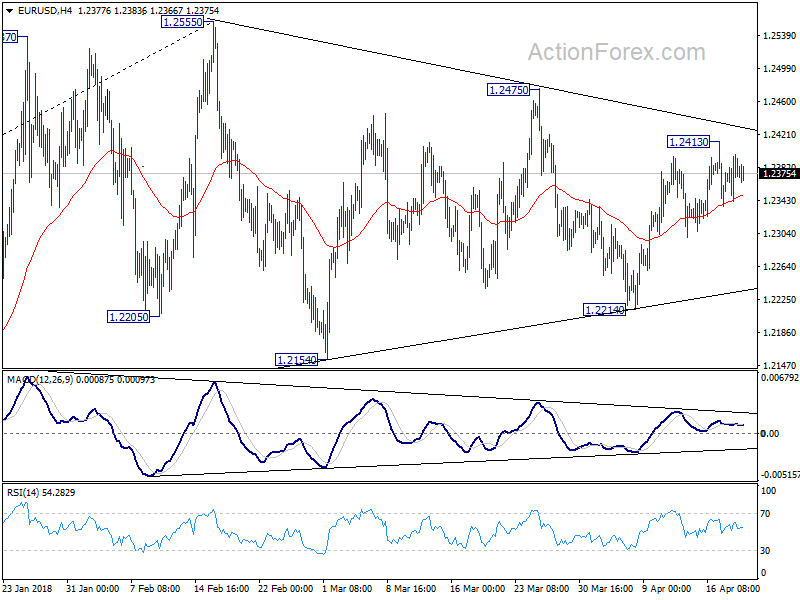

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2345; (P) 1.2371 (R1) 1.2401; More....

Intraday bias in EUR?USD remains neutral. On the upside, above 1.2413 will extend the rebound from 1.2214 to 1.2475 resistance. Break will target 1.2516/2555 key resistance zone. On the downside, however, break of 1.2214 will revive the case of trend reversal and turn outlook bearish.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

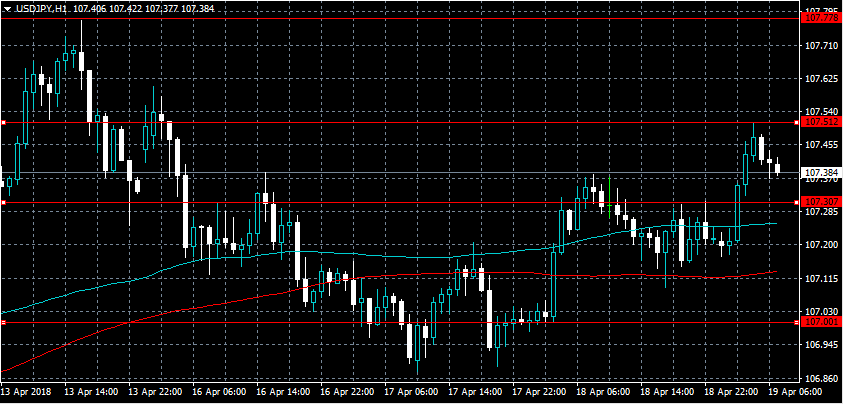

USDJPY Short-Term Range Break Looms

The U.S dollar continues to trade in an increasingly narrow-range against the Japanese yen, as financial market participants look for a clear trading catalyst to emerge. The USDJPY pair has so far found weekly support from the 106.88 level, while the weekly trading high is found at the 107.51 level. Traders now look towards the release of key United States Jobs and Manufacturing data, while the Japanese economy releases crucial CPI inflation numbers.

The USDJPY pair remains bullish while trading above the 107.00 level, key upside resistance is found at the 107.51 and 107.77 levels.

Should price-action on the USDJPY pair move below 107.00 level, sellers will likely test towards the 106.88 and 106.60 support levels.

British, US Data Make Headlines Thursday

A steady stream of economic data will flow through the financial markets on Thursday, with reports from the United Kingdom and the United States set to make headlines.

Action begins at 08:00 GMT with a report on the Eurozone current account balance. Brussels' current account surplus is forecast to weaken to €32.3 billion in February from €37.6 billion in January.

Shifting gears to the United Kingdom, the Office for National Statistics will report on retail sales at 08:30 GMT. Receipts at retail stores, long considered to be a proxy for consumer spending, is expected to decline 0.5% in March. That translates into an annualized gain of 2%.

Excluding fuel, retail receipts are projected to fall 0.4% in March, which translates into a year-over-year gain of 1.4%.

The North American session begins with a speech from Federal Open Market Committee (FOMC) member Lael Brainard, who is scheduled to give her talk at 12:00 GMT. Later in the session, Fed Governor Randal Quarles is expected to deliver remarks.

In terms of economic data, the Department of Labor will issue a report on initial jobless claims at 12:30 GMT. The number of Americans filing for first-time unemployment benefits likely fell by 3,000 to a seasonally adjusted 230,000 in the week ended 14 April.

The Philadelphia Fed is scheduled to release its monthly manufacturing survey at 12:30 GMT. The monthly gauge is forecast to fall 2.2 points to 20.1 in April.

A report on Canada's employment situation courtesy of ADP will be also be released at 12:30 GMT.

Earlier in the day, the Australian government reported a much slower than expected rise in March employment. Overall employment rose by 4,900 in March, compared with expectations of 21,000. Full-time jobs plunged by 19,900 after surging 64,900 the previous month. Meanwhile, part-time work rose by 24,800 positions after shedding 47,400 the previous month.

AUD/USD

Australia's dollar was little changed in the presence of weaker than expected jobs data. AUD/USD was last seen trading at 0.7784. The pair has been choppy as of late, with prices hovering between 0.7700 and 0.7800 for most of April.

EUR/USD

Europe's common currency traded within a tight range during the early Asian trade, with prices hovering around 1.2380 US. EUR/USD has stabilized over the past two days, although prices have failed to make a decisive break above 1.2400. Immediate resistance is located at 1.2413, which is the top from 17 April.

GBP/USD

Like other dollar pairs, cable was little changed on Thursday. GBP/USD has plunged nearly 200 pips from the Tuesday swing high near 1.4400. UK retail sales figures could provide the pair with direction on Thursday. In the meantime, immediate support is located at 1.4145, the low from 12 April.

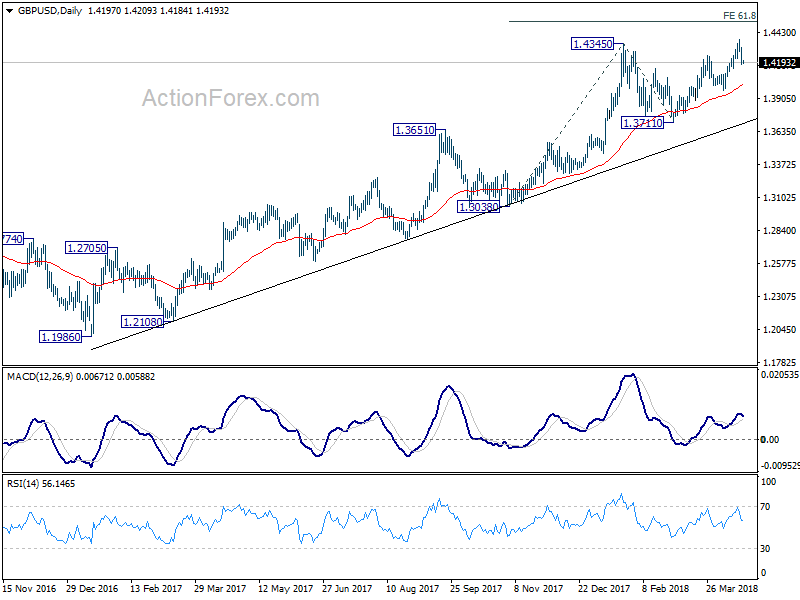

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4145; (P) 1.4229; (R1) 1.4287; More...

Intraday bias in GBP/USD stays neutral with 1.4144 minor support intact. Price actions from 1.4376 short term top is possibly just developing in to a consolidation pattern. ON the upside, break of 1.4376 will confirm up trend resumption. In that case, GBP/USD would target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519. However, on the downside, firm break of 1.4144 will be and early sign of medium term topping and turn focus back to 1.3965 support.

In the bigger picture, rise from 1.1946 (2016 low) is in progress and resuming. It is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. We'd continue to favor this medium term bullish view as long as 1.3711 support holds, even in case of deep pull back.

In the bigger picture, rise from 1.1946 (2016 low) is in progress and resuming. It is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. We'd continue to favor this medium term bullish view as long as 1.3711 support holds, even in case of deep pull back.

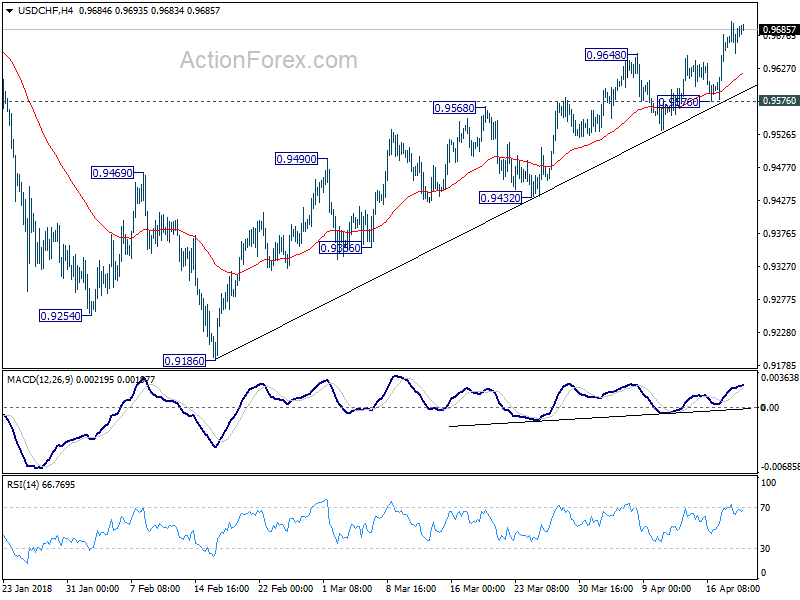

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9658; (P) 0.9678; (R1) 0.9706; More...

No change in USD/CHF's outlook. Intraday bias remains on the upside and current rise from 0.9186 should target 0.9900 fibonacci level next. On the downside, break of 0.9576 minor support is needed to be the first sign of short term topping. Otherwise, outlook will remain bullish in case of deeper retreat.

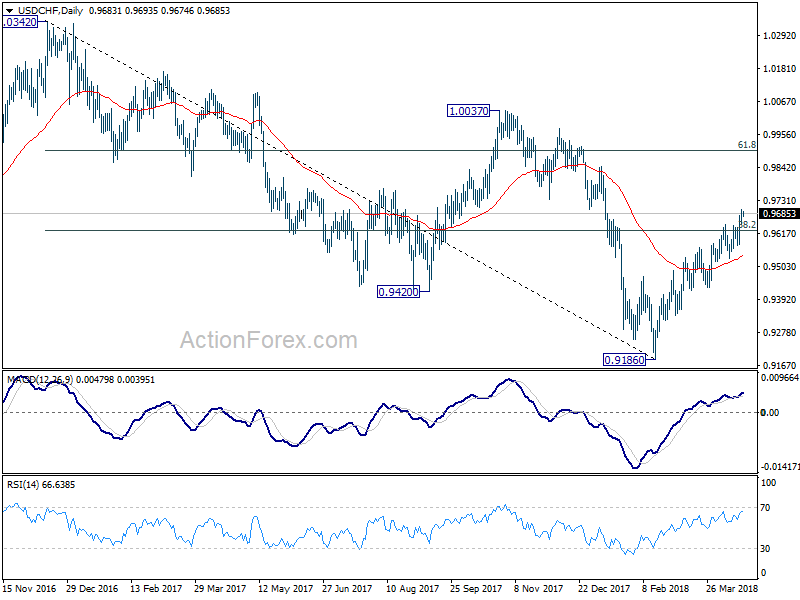

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next.

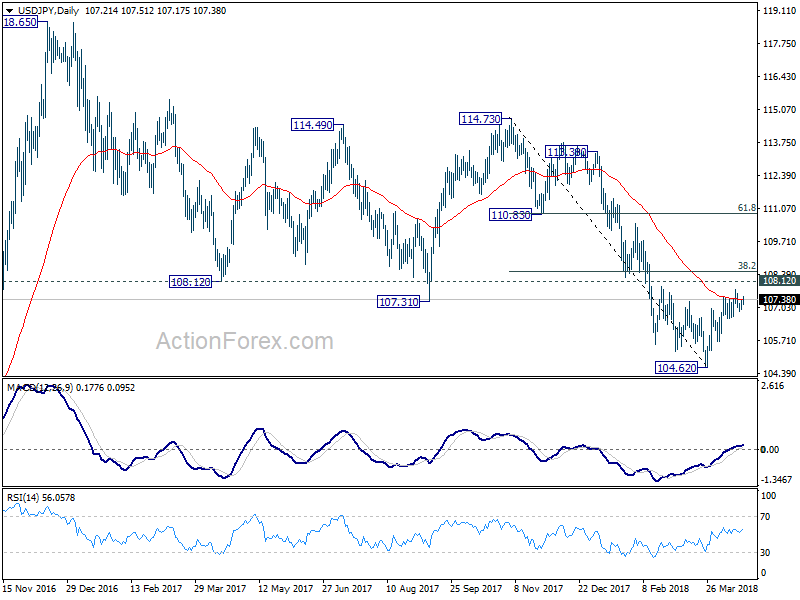

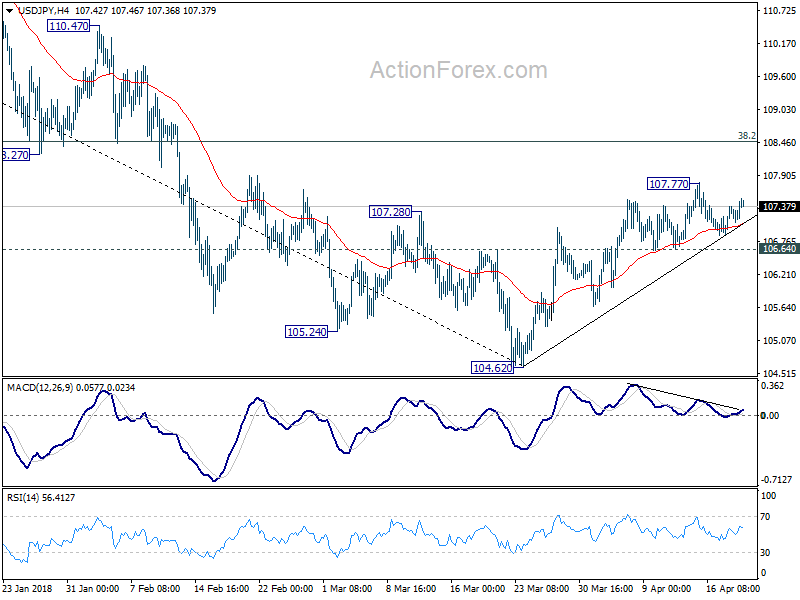

USD/JPY Daily Outlook

Daily Pivots: (S1) 107.00; (P) 107.19; (R1) 107.41; More...

No change in USD/JPY's outlook as it's still bounded in range of 106.64/107.77. Intraday bias remains neutral and more consolidative could be seen. Further rise would be mildly in favor as long as 106.64 minor support holds. Break of 107.77 will target 38.2% retracement of 114.73 to 104.62 at 108.48 which is close to 108.12. This level is crucial in determining the medium outlook. On the downside, break of 106.64, however, will indicate the rebound from 104.62 has completed. And in that case, bias will be turned back to the downside for retesting 104.62.

In the bigger picture, as long as 108.12 support turned resistance holds, the medium term down trend from 118.65 (2016 high) should still continue lower, at least to retest 98.97 (2016 low). However, sustained break of 108.12 will be an early sign of medium term reversal. In that case, further rise would be seen to 114.73 resistance to confirm completion of the fall from 118.65.

In the bigger picture, as long as 108.12 support turned resistance holds, the medium term down trend from 118.65 (2016 high) should still continue lower, at least to retest 98.97 (2016 low). However, sustained break of 108.12 will be an early sign of medium term reversal. In that case, further rise would be seen to 114.73 resistance to confirm completion of the fall from 118.65.