Sample Category Title

Loonie Softens On Cautious BoC, UK Retail Sales In Focus

Here are the latest developments in global markets:

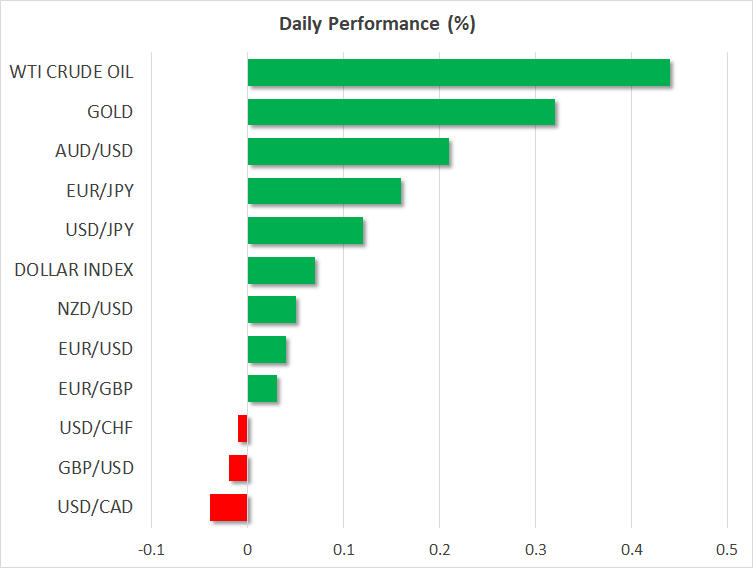

FOREX: The US dollar index is higher today, but by less than 0.1%. Aussie/dollar is up by 0.2%, lifted by a notable rally across commodities. Meanwhile, the loonie steadied against the dollar, after it plunged yesterday on the back of cautious signals from the BoC.

STOCKS: US markets closed mixed yesterday. While the Nasdaq Composite and the S&P 500 advanced 0.2% and 0.1% respectively, the Dow Jones fell nearly 0.2%, weighed on by disappointing earnings from IBM (-7.5%). Futures tracking the Dow, S&P and Nasdaq 100 are all currently very close to neutral territory, suggesting these indices could open at similar levels today. Japan was a similar story, with the Nikkei 225 and the Topix closing in the green, but only by 0.15% and 0.03% correspondingly. In Hong Kong though, the Hang Seng surged 1.0%. In Europe, futures tracking the major benchmarks were mixed.

COMMODITIES: Oil prices skyrocketed yesterday and extended their gains today, with both WTI and Brent reaching fresh highs last seen in 2014. The trigger for the surge was a report that Saudi Arabia would be happy to see oil reach $80 or $100, fueling speculation the nation and OPEC will continue to restrict supply to achieve this. The cherry on the pie were the weekly EIA inventory data, which showed a larger-than-expected drawdown in US crude stockpiles. In precious metals, gold edged higher by 0.3% today. There was no risk-off catalyst behind the gains, so its outperformance seems to be owed to the broader rally across commodities. Nickel climbed to a three-year high, while aluminum touched a fresh six-year high, boosted by concerns US sanctions against Russian companies could impact the supply of such materials. News China is set to impose anti-dumping measures on rubber may have helped the moves too.

Major movers: Loonie slumps on cautious BoC; sterling drops after disappointing CPIs

The Canadian dollar dived yesterday, following the BoC's policy decision. The Bank remained on hold, as was widely anticipated, while the statement accompanying the decision erred on the side of caution, disappointing those looking for hawkish signals that a rate hike is imminent. Officials dismissed the recent surge in inflation, attributing it mostly to transitory factors, while they also highlighted escalating geopolitical and trade conflicts as key risks to the economy's outlook.

The implied probability for a July rate hike fell alongside the loonie, declining from nearly 95% prior to the gathering to 80% currently, according to Canada's OIS. It's worthy to note though, that the surge in oil prices yesterday likely limited any greater declines in the loonie. Focus now turns to the release of the nation's inflation and retail sales data, due out tomorrow.

Elsewhere, the British pound slumped after the UK CPI data for March disappointed. Both the headline and the core inflation rates surprisingly declined, missing their forecasts for staying unchanged and ticking up respectively. Interestingly enough, while sterling responded as one would expect, the probability for a BoE rate hike in May barely budged, staying elevated at 67%. Thus, markets did not see these prints as derailing the prospect for a May action. That said, the overall soft data recently do suggest the Bank could deliver another “cautious” hike. Recall that although the BoE raised rates in November, sterling dropped in the aftermath, as the hike was accompanied by dovish signals.

The antipodeans are slightly higher today. Aussie/dollar advanced 0.2% even despite lackluster jobs data out of Australia overnight, most likely supported by the broader gains in commodities. Kiwi/dollar was up as well, but by less than 0.1%, responding little to the release of New Zealand's CPI for Q1, which slowed in line with expectations.

In emerging markets, the Turkish lira surged yesterday, touching a 2-week high against the dollar after Turkish President Erdogan announced the nation will head to early elections in June.

Day ahead: UK retail sales on the horizon

Thursday's economic calendar is relatively light, with UK retail sales perhaps constituting the day's most important release.

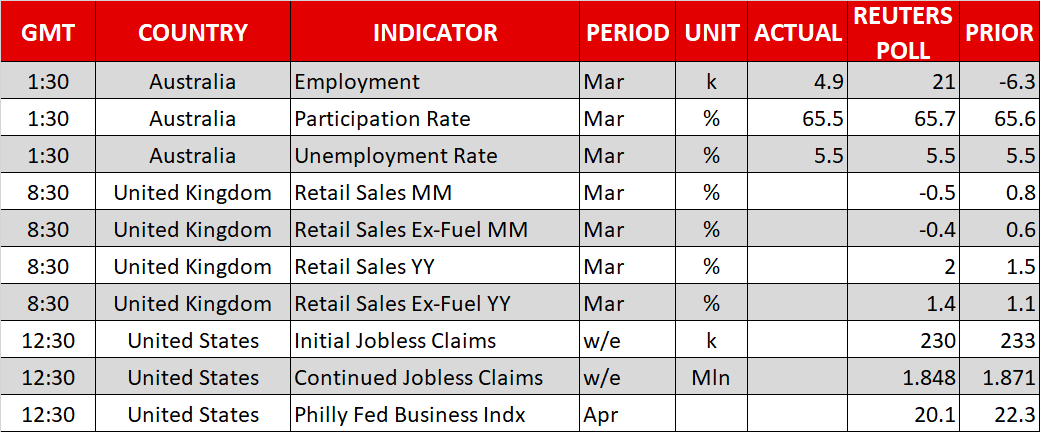

UK retail sales for the month of March are due at 0830 GMT. Those are projected to have fallen on a monthly basis, but to have risen annually. Core retail sales, that exclude fuel from their calculations, will also be watched and are expected to exhibit the same pattern, i.e. reflect an improvement relative to a year ago and a decline compared to February's reading. Sterling's tumble over the last couple of days in the aftermath of data on wage growth and inflation coming in below analysts' forecasts perhaps adds an additional element of interest to today's release.

In North America, the US will see the release of initial and continued jobless claims data for the week ending April 14, as well as the Philly Fed's business index, at 1230 GMT. Out of Canada, the ADP nonfarm employment report due at the same time might generate some attention.

Corporate earnings remain in focus in the equity space and could drive overall market sentiment.

Permanent FOMC voting members Lael Brainard and Randal Quarles will be among policymakers making appearances today. The two will be talking at 1200 GMT and 1330 GMT respectively. Also of interest might be a news conference (1245 GMT) by IMF Managing Director Christine Lagarde and World Bank President Jim Yong Kim ahead of the Spring Meetings of the two organizations; among notable names attending the meeting is ECB President Mario Draghi.

Lastly, geopolitical and trade developments, particularly the latter, have been themes driving the markets for weeks now and it is not unlikely for markets to move on the back of updates on those fronts during today's trading.

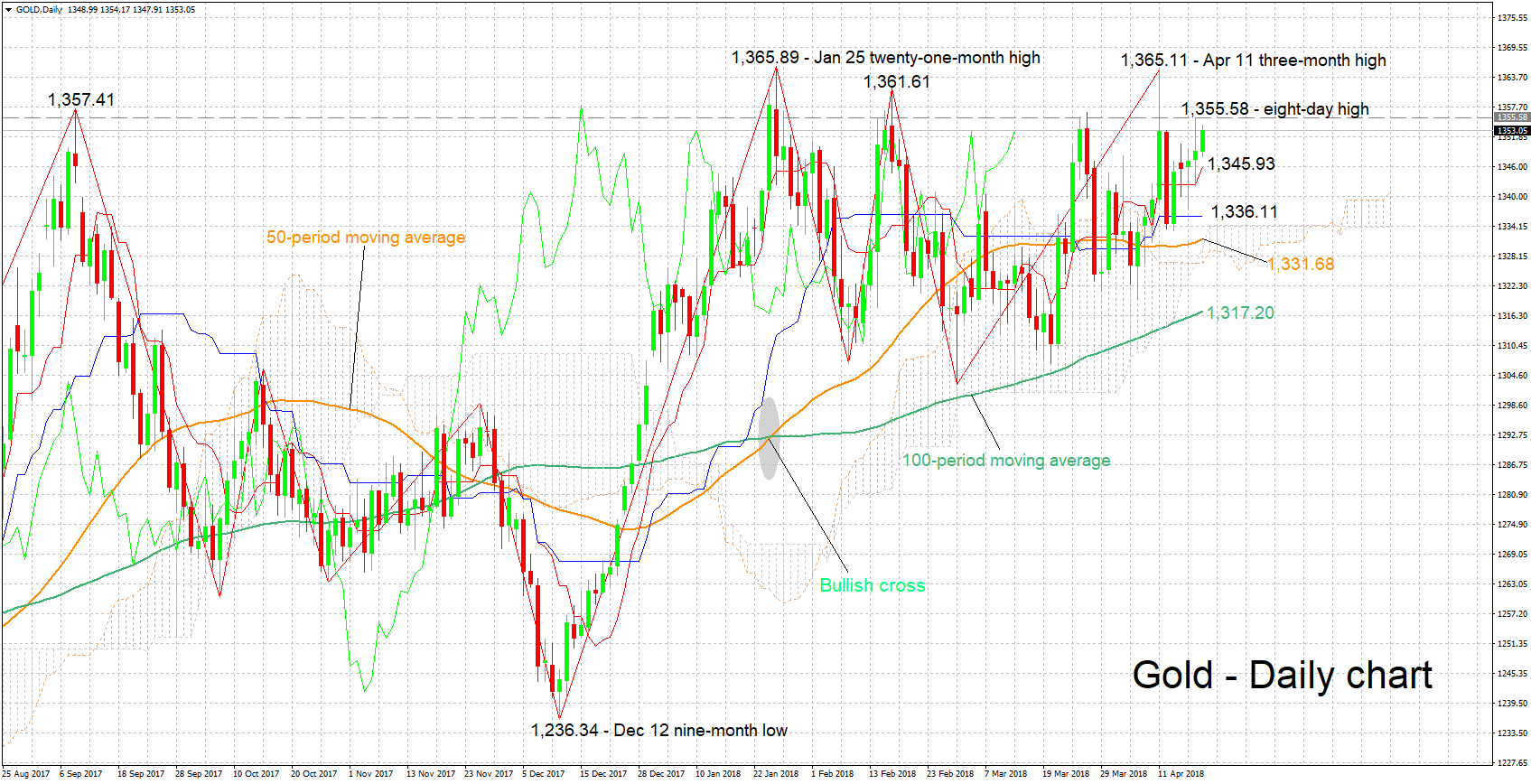

Technical Analysis: Gold short-term bullish, rises for fifth straight day

Gold is posting gains for the fifth day in a row and is currently trading nor far below Wednesday's eight-day high of 1,355.58 (this being a three-week high if one were to exclude April 11's spike higher). The Tenkan-sen is above the Kijun-sen, projecting a bullish picture in the short-term. The flat Kijun-sen though may be pointing to easing positive momentum.

Rising trade and/or geopolitical uncertainty could boost the safe-haven perceived asset. Immediate support may be taking place around yesterday's high of 1,355.58, with an upside break turning the attention to April 11's three-month high of 1,365.11 – the area around this mark also includes the 21-month high of 1,365.89 from late January.

Conversely, receding uncertainties might drive funds out of the yellow metal, pushing it lower. Support to declines could come around the current level of the Tenkan-sen at 1,345.93.

A rising greenback is also likely to act to the detriment of the dollar-denominated metal and vice versa.

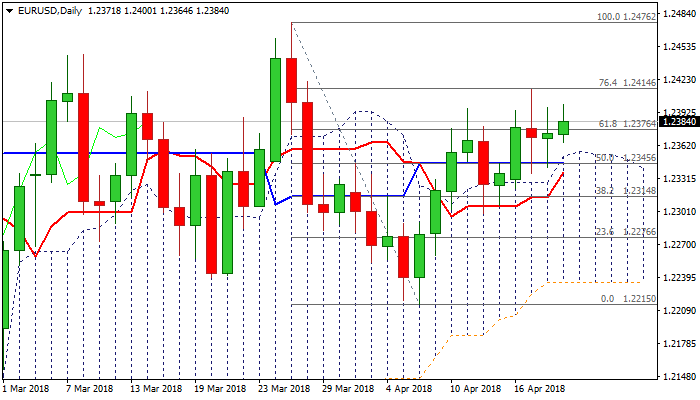

EURUSD – Bullish Bias Above Daily Cloud But Break Above 1.2414 Needed To Signal Continuation

The Euro moved higher and retested 1.24 barrier on Thursday, after strong indecision in past two days, signaled by double long-legged Doji. Overall bullish bias remains intact after strong upside rejection above 1.24, as subsequent easing was contained above a cluster of supports, provided by MA's and daily cloud top. Multiple bull-cross of rising 10SMA over 20/30 /55SMA's, offered fresh boost to the pair for renewed probes above 1.24 barrier and retest of 1.2414 (Fibo 76.4% of 1.2476/1.2215 bear-leg), clear break of which would open way towards key near-term barrier at 1.2476 (27 Mar peak). EU's current account surplus widened (35.1 B in Feb vs 32.3B f/c) offering additional support, with no further data from the Eurozone scheduled today. Daily cloud top marks key support at 1.2351 and bullish bias is expected to remain intact while the price holds above, as cloud top kept the downside protected for over one week. Conversely, stronger bearish signal could be expected on break and close below cloud top.

Res: 1.2400, 1.2413, 1.2446, 1.2476

Sup: 1.2364, 1.2351, 1.2333, 1.2314

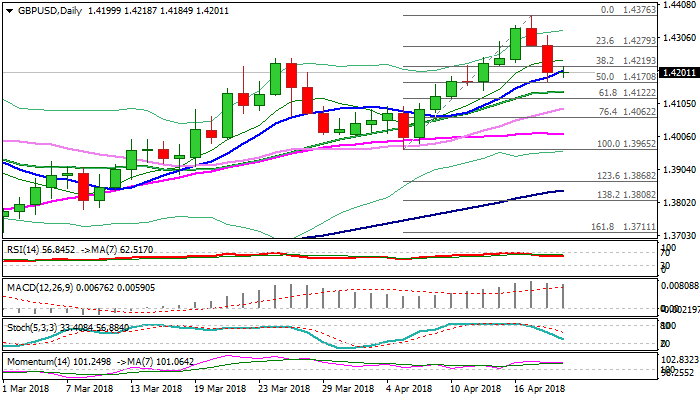

GBPUSD Stands At The Back Foot Ahead Of UK Retail Sales

Cable traded within narrow consolidation range in Asia on Thursday, following strong fall in past two days and awaiting the third key release this week, UK retail sales.

Pound was hit by weak data in past two days, as downbeat UK wages and inflation sparked strong pullback from new post-Brexit recovery high at 1.4376.

Pullback dented solid support at 1.4185 (rising 10SMA) but managed to close above on Wednesday, while today’s repeated probes below 10SMA (currently at 1.4207) were so far short-lived. Two-day pullback on Tue/Wed generated bearish signal on close below 1.4219 (Fibo 38.2% of 1.3965/1.4376 upleg) which needs confirmation on repeated close below and also close below rising 10SMA.

Reversal pattern is forming on daily chart and sees risk of deeper pullback towards 1.4243/22 (rising 20SMA/Fibo 61.8% of 1.3965/1.4376).

Pullback has dented bulls on daily chart, however, daily indicators are still in bullish setup and require repeated close above 10SMA to generate initial signal of correction end and formation of higher low, with confirmation on recovery extension and close above 1.4250 (Fibo 38.2% of 1.4376/1.4172 pullback).

Forecast for UK retail sales is negative (Mar -0.5% f/c vs 0.8% in Feb/core -0.4% f/c Mar vs 0.6% in Feb) and release in line with expectations or below would put sterling under fresh pressure.

Positive sentiment among investors over strong expectations for BoE rate hike next month faded after disappointing wages and CPI and picture could be soured further on retail sales miss.

Res: 1.4220, 1.4250, 1.4274, 1.4298

Sup: 1.4185, 1.4170, 1.4143, 1.4122

Yesterday, Global Core Bonds Initially Held Tight Ranges

Markets

Yesterday, global core bonds initially held tight ranges, but came under pressure later in the session. A further receding of global trade/geopolitical tensions, a constructive equity sentiment and higher oil prices all reduced demand for safe haven bonds. US yields rose between 3.5 bp (2.yr) and 4.4 bp (10-year). The 2-year US yields set a new cycle top north of 2.40%. The rise in European yields was more modest. A downward revision of March EMU inflation probably supported the outperformance for German bunds. Today there are no important data in Europe. In the US, the jobless claims, the Philly Fed outlook and the leading indicators will be published. The data will only be of intraday significance for bond trading. Global risk sentiment will probably remain the main driver for bond trading. There are tentative signs that core bond yields could again move further north. However, for now, we don’t see any news that is important enough to push 10-yields (Bunds and Treasuries) out of the established ranges.

Yesterday morning, there were tentative signs that the dollar could capture a better bid. EUR/USD spiked temporary lower to the mid 1.23 area as EMU March inflation was downwardly revised to 1.3% from 1.4%. However, the dollar wasn’t able to build on this temporary euro weakness. EUR/USD rebounded back higher in the 1.23 big figure; despite late session rise in US yields. Today, the eco calendar probably won’t break the recent stalemate in USD trading. EUR/USD is locked in the middle of the 1.2155/1.2555 trading range. USD/JPY profits slightly from the positive risk sentiment. Markets will also look forward to comments on FX on the sidelines of the IMF spring meeting.

Yesterday, sterling fell prey to profit taking after UK March inflation was reported softer than expected (2.5% M/M). EUR/GBP rebounded north of 0.87. So, recent extensive attempt of the EUR/GBP cross rate to break below the 0.8650 support was rejected, at least for now. The UK Upper House also complicated the Brexit strategy of UK PM may as it voted an amendment pushing the UK government to keep a customs union with the EU post Brexit. Today, the UK retail sales will be published. A setback (-0.6% M/M) is expected after a rebound in February. UK retail sales were rather soft over the previous months. Even so, we are keen to see the market reaction in case of decent UK retail sales. Decent activity data might convince markets that the easing in inflation shouldn’t prevent the BoE to gradually bring interest rate to a more neutral level further out this year.

News Headlines

US President Trump and Japanese PM Abe agreed to step up talks aiming for ‘free, fair and reciprocal’ trade deals. Trump reiterated its preference from bilateral trade deals. At the same time, President Trump didn’t openly criticize the valuation of the Japanese yen or Japanese monetary policy.

Brent Crude Oil touched $ 74 p/b. The move was supported by press headlines (Reuters) that OPEC intents to keep the supply cutting measures in place. It was also indicated that Saudi Arabia won’t have any objections for the oil price the return to the $80/100 p/b range.

Australian labour market data disappointed. March employment growth printed at a soft 4 900 and February jobs growth was revised sharply lower from a gain of 17 500 to a job loss of 6.3%. The easing of momentum in the Australian labour market might be a good reason for the Reserve bank of Australia to maintain a wait-and-see approach. For now, it shouldn’t feel pressured to raise the policy rate anytime soon.

Today, the eco calendar in Europe is thin. In the US, the jobless claims, the Philadelphia Fed business outlook and the leading indicators will be released. In the UK, the focus will be on the March retail sales. Spain and France will hold bond auctions. Fed’s Brainard and Quarles will speak, but will address non-monetary policy issues.

House Of Lords Sinks PM May’s Plans, Wants Stronger Customs Union With EU

A vote in the UK's House of Lords last night defeated the Government's plan to leave the customs union with the EU. The House voted down the proposal 348 to 225. While this does not prevent the UK leaving, it does show some of the opposition that is building up against aspects of the withdrawal. The vote now demands that the Government explores the option of staying in the customs union with the EU. Market reaction to the vote was muted but it does change the playing field, as investment in the UK suffers. UK retail sales will be released later today, with an expectation for a fall in monthly numbers. Gold is higher to 1352.00 as asset prices increase globally and stock markets outperform on positive earnings reports. The FTSE is up to 7320.00 after rising 1.26% yesterday.

UK Consumer Price Index (YoY) (Mar) was 2.5% v an expected 2.7%, from 2.7% previously. Core Consumer Price Index (YoY) (Mar) was 2.3% v an expected 2.5%, from 2.4% prior. Consumer Price Index (MoM) (Mar) was 0.1% v an expected 0.3%, from 0.4% prior. Producer Price Index – Output (MoM) n.s.a. (Mar) was as expected at 0.2%, from 0.0% previously. Producer Price Index – Output (YoY) n.s.a. (Mar) was 2.4% expected at 2.3%, from 2.6% previously. Producer Price Index – Input (MoM) n.s.a. (Mar) was -0.1% v an expected 0.3%, from -1.1% previously, which was revised up to -0.4%. Producer Price Index – Input (YoY) n.s.a. (Mar) was 4.2% v an expected 4.1%, from 3.4% previously, which was revised up to 3.8%. Retail Price Index (MoM) (Mar) was 0.1% v an expected 0.3% against 0.8% previously. Retail Price Index (YoY) (Mar) was 3.3% v an expected 3.6%, from 3.6% prior. These data points showed CPI dipping. The yearly figure has been above the Bank of England's 2% target since March of 2017, due to the change in the value of the pound after Brexit. However, the BOE says that inflation is likely to move back to 2% in 2018. Despite the drop yesterday, the pressure is on the BOE to increase rates sooner rather than later, as wage growth moves past inflation. Producer Prices increased in March after the drop in February, including higher revisions. GBPUSD tumbled exactly 100 pips from 1.42731 to a low of 1.41731 following the release of this data. EURGBP moved up from 0.86609 to 0.87206.

Eurozone Consumer Price Index – Core (YoY) (Mar) was released coming in as expected, unchanged at 1.0%. Consumer Price Index (MoM) (Mar) was also as expected, at 1.0%, from 0.2% previously. Consumer Price Index (YoY) (Mar) was 1.3% v an expected 1.4%, from 1.4% previously. Consumer Price Index – Core (MoM) (Mar) was as expected at 1.4%, from 0.4% prior. Inflation rose to 2.0%, the highest levels in five years, in late 2016 and early in 2017 but has stabilized around 1.3% since June. The ECB is looking for inflation to “approach 2%”. The target was hit on the yearly metric in March 2017 but has slipped since a year ago. CPI data came in largely as expected for the monthly figures but slipped slightly for the yearly figures. EURUSD fell from1.23594 to a low of 1.23412 but recovered to 1.23745 on the release of this data.

Bank of Canada Rate Statement was made public. The Monetary Policy Report was released and the Interest Rate Decision was left unchanged, as expected, at 1.25%. The GDP Q1 forecast was cut to 1.3% from 2.5%, as growth fell short of the mark in Q4 and Q1, but a rebound is expected in Q2 at 2.5%. Inflation is close to 2%, as temporary factors dissipate and the rises in core are consistent with little economic slack. The potential output growth has been raised to 1.8% in 2018-2020 period and 1.9% in 2021. The BOC says it is monitoring the economy's sensitivity to higher interest rates. It repeats that the BOC will be cautious with respect to future hikes. Escalating geopolitical and trade conflicts risk undermining global expansion. Wages have continued to pick up as expected and the labour market will continue to be assessed for signs of remaining slack. Some of the Q1 weakness in housing and exports will be unwound as 2018 progresses. 2018 growth was trimmed to 2.0%, from 2.2% and 2019 growth was boosted to 2.1%, from 1.6%. USDCAD rose on the headlines to 1.2610 from 1.2550.

The US Fed's Beige Book data was released. The Fed sees only modest wage gains in most districts, with businesses turning to automation and more training to deal with shortfalls. Businesses in manufacturing, agriculture, transport and other sectors ‘expressed concern' about the newly imposed and proposed tariffs. There were widespread reports of higher steel prices due to the new tariffs. Employment growth continued, with the labour markets being described as tight across the country, with shortages in high-skill positions, construction and transportation. Prices increased across all districts, generally at a moderate pace. The prices of building materials have been rising.

Fed Member Quarles spoke at the Bretton Woods Committee Annual Meeting, in Washington DC, making the following comments: The labor market may have more slack, inflation under 2%. He does not support raising the Fed's inflation target and the case for retaining the current floor system is compelling. He believes the Fed should return to neutral to ensure price stability and that trade and fiscal policies have raised longer-term risks. He added that the case for more aggressive tightening is not compelling. He said he expects inflation to rise slowly towards the target and sees year-over-year gains in April numbers. He supports only gradual rate hikes given inflation remains below target. He expects US monetary policy to be slightly restricted in the years ahead. He suggests an inflation range from 1.5% to 2.5%.

New Zealand Consumer Price Index (QoQ) (Q1) came in as expected at 0.5%, against a previous 0.1%. Consumer Price Index (YoY) (Q1) was also as expected, at 1.1%, against a previous 1.6%. NZDUSD moved up to resistance at 0.73429 from 0.73250, before slipping back to a low of 0.73085 after the data release.

Australian Employment Change s.a. (Mar) was 4.9K v an expected 21.0K, from 17.5K previously. The Unemployment Rate s.a. (Mar) was as expected, at 5.5%, from 5.6% previously. The Participation Rate (Mar) was 65.5% v an expected 65.7%, from 65.7% previously. National Australia Bank's Business Confidence (QoQ) (Q1) was 7 against a previous reading of 6 last quarter. Upon the release of this data, AUDUSD fell from 0.77946 to support at 0.77636, before rallying past the earlier high to the 0.78091 level.

EURUSD is up 0.02% overnight, trading around 1.23760.

USDJPY is up 0.17% in early session trading at around 107.410.

GBPUSD is up 0.02% this morning, trading around 1.42035.

USDCAD is down -0.02%, trading around 1.26241.

Gold is up 0.19% in early morning trading at around $1,351.60.

WTI is down -0.04% this morning, trading around $68.78.

UK Retail Sales And US Unemployment Data On The Agenda Today

At 08:30 GMT, UK Retail Sales (YoY) (Mar) is expected to be 2.0% from 1.5% previously. Retail Sales (MoM) (Mar) is expected at -0.5% against a prior 0.8%. Retail Sales Ex-Fuel (YoY) (Mar) is expected to be 1.4% from 1.1% previously. Retail Sales Ex-Fuel (MoM) (Mar) is expected at -0.4% against a prior 0.6%. Yearly figures are expected to show an increase but monthly numbers are expected to miss expectations and show a fall in sales. It is a volatile data set, however, it does provide an overview of consumer spending. GBP crosses may experience an increase in volatility following this data release.

At 12:00 GMT, FOMC Member Brainard is due to speak about regulatory reform at the Global Finance Forum, in Washington DC. Audience questions are expected and any comments made could affect USD pairs.

At 12:30 GMT, US Continuing Jobless Claims (Apr 6) is expected to be 1.848M against a previous 1.871M. Initial Jobless Claims (Apr 13) is expected to be 230K from 233K previously. Philadelphia FED Manufacturing Survey (Mar) is expected to be 20.1 against 22.3 previously. Although low, the Claims data is still above its lowest levels. It is expected to fall and come in lower than expected, as the labour market struggles to find more workers. USD pairs may be moved by this data.

At 13:30 GMT, Fed Member Quarles is due to testify on supervision and regulation before the Senate Banking Committee, in Washington DC. The USD may be impacted by any comments made.

At 16:30 GMT, UK MPC Member Cunliffe is due to speak at the Global Finance Forum, in Washington DC. Audience questions are expected, with comments potentially impacting GBP crosses.

At 22:45 GMT, FOMC Member Mester is due to speak about the economic outlook and monetary policy at the University of Pittsburgh’s Joseph M. Katz Graduate School of Business. Audience questions are expected and USD pairs could be impacted by any comments made.

GBP/USD Bearish Breakout Creates Strong Momentum And Reversal

The GBP/USD broke below the support trend line (dotted green) after bouncing at the previous top (red). Price could either be building a bearish reversal or larger retracement within the overall uptrend. A bearish continuation of the correction could take price down to or close to the next support trend line (blue) whereas a bullish bounce could see price challenge the previous tops.

The GBP/USD made a larger downside after strong bearish momentum appeared in the first leg down. The bearish breakout was even stronger and could be a potential wave 3 (purple). In that case, price is now in a wave 4 and could make one more dip for a wave 5. The alternative wave count is that price completed a bearish ABC (orange) instead and price could build an expanded correction within a WXY (red). The key level to keep an eye on are the Fibonacci retracement levels of wave 4 vs 3.

The USD/JPY is still moving up slowly within the bullish channel.Price remains at a key decision zone: a bullish breakout above the 50% Fib invalidates the bearish wave structure whereas a break below the support trend line (blue) makes a downtrend continuation within wave 5 (blue) more likely.

The USD/JPY could be building a potential wave 2 pullback(orange). This wave pattern is invalidated once price breaks above the 100% Fib level of wave 2.

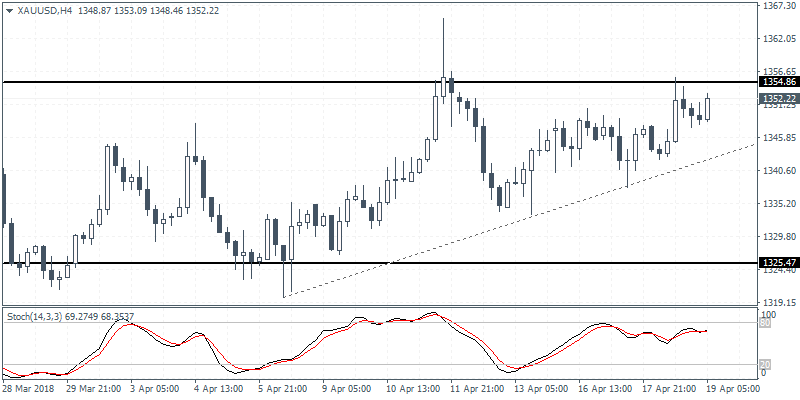

XAUUSD Intraday Analysis

XAUUSD (1352.22): Gold prices were seen erasing the minor losses with price action pushing higher at the time of writing. The resistance level at 1354 remains a strong level which could see the current gains being stalled. There is scope for gold prices to breakout higher if the resistance level is breached. To the downside, the rising trend line is expected to hold prices support, but a break of the rising trend line could signal a decline back towards the support level at 1325.50 level

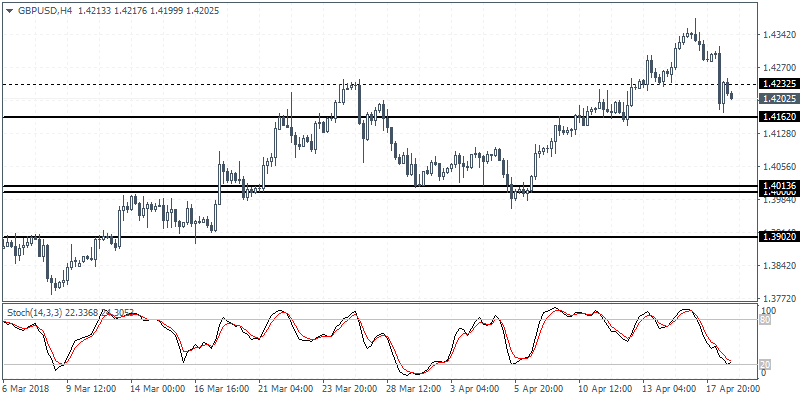

GBPUSD Intraday Analysis

GBPUSD (1.4202): The British pound is seen extending the declines for a second day as price action is currently seen trading below the minor support level of 1.4232 level. The break down below this level signals a move toward the major support level at 1.4162. A retest of this support level could see prices posting a rebound. To the downside, further declines could be expected in the event that GBPUSD fails to hold the support. The next lower support is seen at 1.4013.

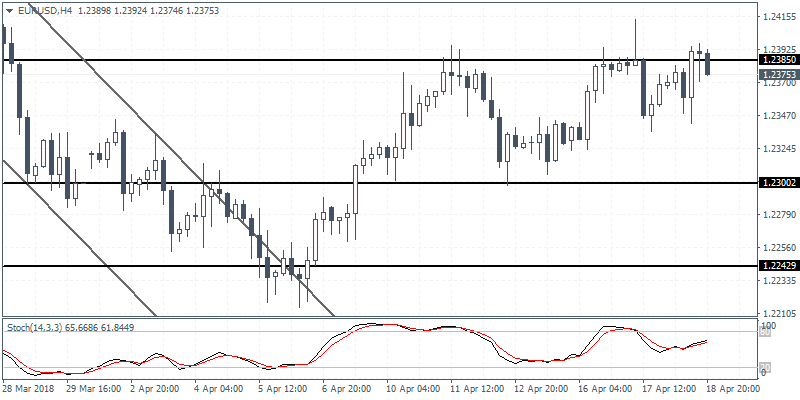

EURUSD Intraday Analysis

EURUSD (1.2375): The EURUSD was seen trading slightly bullish on the day as price action retraced the losses from the previous day. The consolidation near the 1.2400 level of resistance continues with the common currency unable to break past this level. The failure to break past the resistance level signals a continued sideways range in EURUSD. To the downside, EURUSD could see a retest of the lower support at 1.2300. The price action also points to a potential ascending triangle pattern with higher lows being formed. Therefore, further gains cannot be ruled out on a breakout above 1.2400 which could signal a move toward 1.2430.