Sample Category Title

Silver: White Metal Trading Slightly Lower In The Asian Session

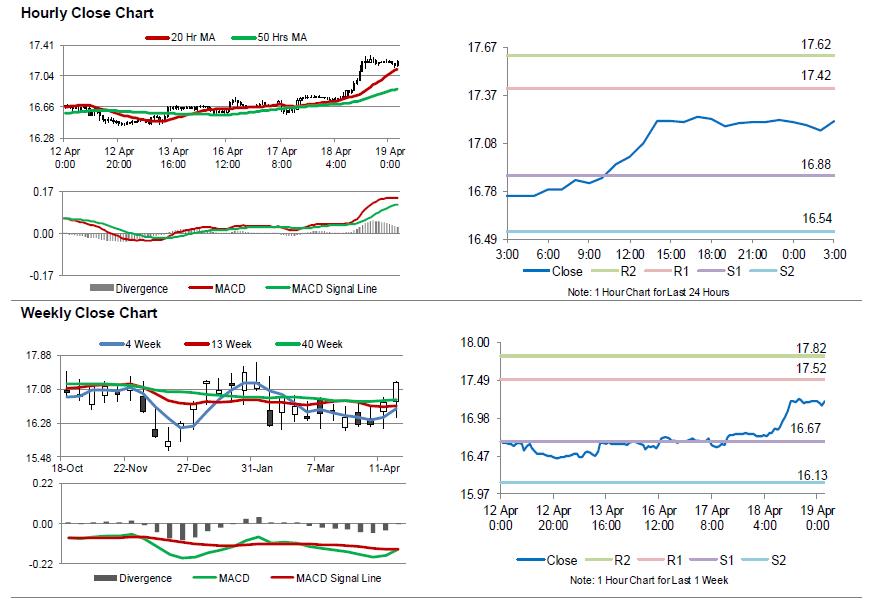

For the 24 hours to 23:00 GMT, Silver rose 2.65% against the USD and closed at USD17.22 per ounce, tracking gains in gold prices.

In the Asian session, at GMT0300, the pair is trading at 17.22, with silver trading marginally lower against the USD from yesterday’s close.

The pair is expected to find support at 16.88, and a fall through could take it to the next support level of 16.54. The pair is expected to find its first resistance at 17.42, and a rise through could take it to the next resistance level of 17.62.

The white metal is trading above its 20 Hr and 50 Hr moving averages.

Crude Oil: Oil Trading Lower In The Asian Session

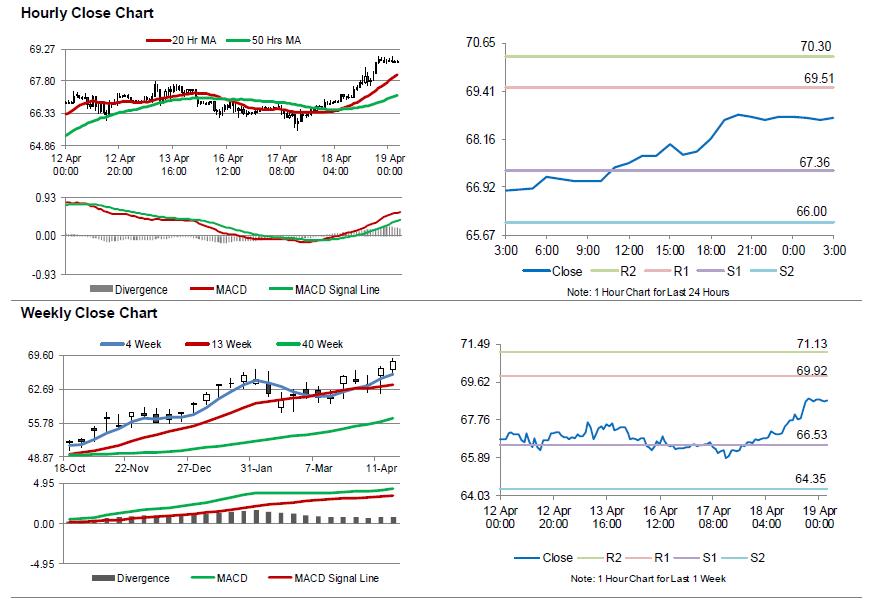

For the 24 hours to 23:00 GMT, Crude Oil rose 3.24% against the USD and closed at USD68.75 per barrel, after the Energy Information Administration (EIA) indicated that US crude oil stockpiles unexpectedly fell by 1.1 million barrels to 427.6 million barrels in the week ended 13 April. Additionally, news reports indicated that Saudi Arabia seeks to hike crude prices to as high as USD80 to USD100 per barrel.

In the Asian session, at GMT0300, the pair is trading at 68.71, with oil trading 0.06% lower against the USD from yesterday’s close.

The pair is expected to find support at 67.36, and a fall through could take it to the next support level of 66.00. The pair is expected to find its first resistance at 69.51, and a rise through could take it to the next resistance level of 70.30.

Crude oil is trading above its 20 Hr and 50 Hr moving averages.

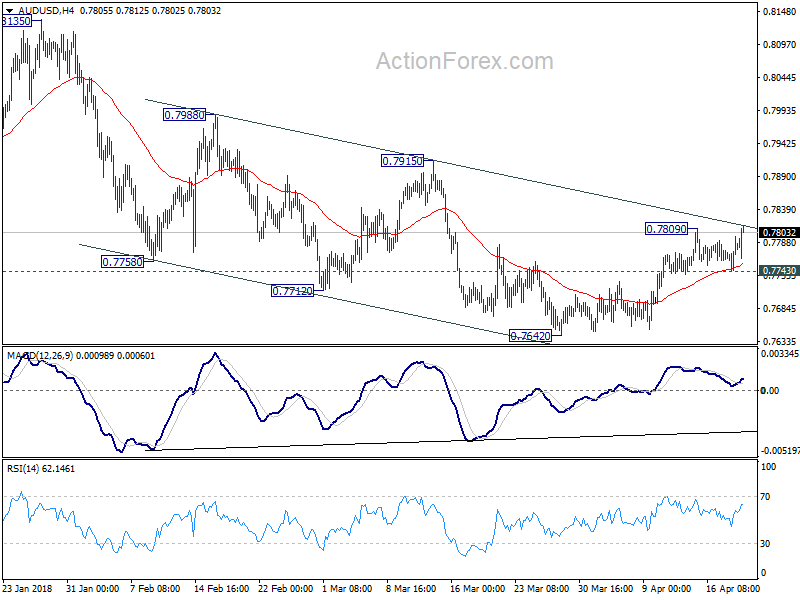

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7752; (P) 0.7775; (R1) 0.7805; More...

Breach of 0.7809 temporary top suggests rebound from 0.7642 is resuming. Intraday bias in AUD/USD is back on the upside for 0.7915 resistance next. Decisive break there should confirm whole decline from 0.8135 has completed at 0.7642. In that case, further rally should be see back to retest 0.8135 high. However, break of 0.7743 minor support will turn bias back to the downside for 0.7642 low instead.

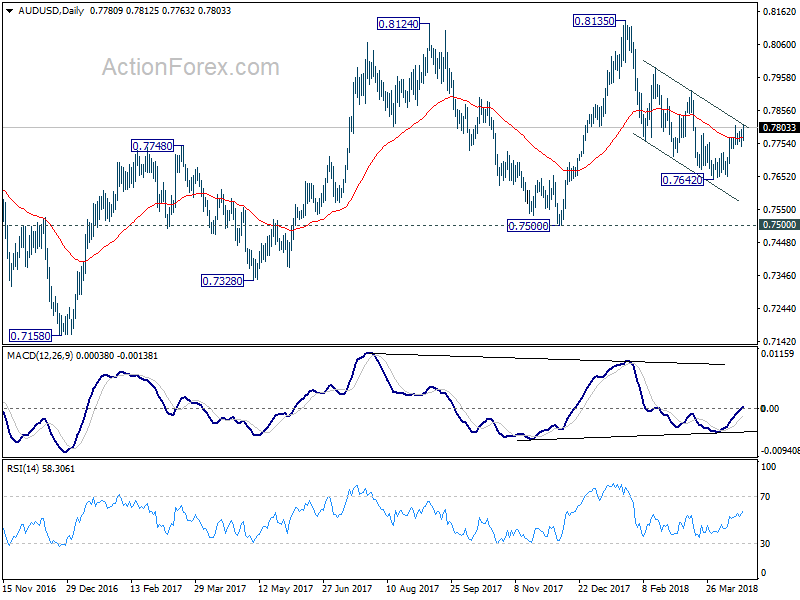

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

Australian Dollar Shrugs off Job Data Miss, Sterling Looks into Retail Sales

Commodity currencies are trading broadly higher today as led by Australian Dollar. Strong rebound in the Chinese stock markets is seen as factor helping the Aussie, as SSE is gaining more than 1% at the time of writing. Canadian Dollar is also recovering some of yesterday's post-BoC loss. Sterling, on the other hand, is back under some pressure. But it's the Japanese that's weakest so far today. For the week up to this point, Swiss Franc is trading as the weakest one while Aussie is the strongest.

Technically, EUR/JPY's breach of 132.96 indicates recent rebound from 128.94 is extending, even though momentum is a bit unconvincing. AUD/USD's break of 0.7809 also indicates resumption of recent rebound from 0.7642. Focus will be on Sterling pairs. For now, despite yesterday's selloff in the Pound, GBP/USD is holding above 1.4144, GBP/JPY above 151.15 and EUR/GBP below 0.8739. These level will be vulnerable on another data miss in UK retail sales today. In particular, EUR/GBP will be a pair that's worth some attention.

Australia employment data miss is not a disaster

Australia Dollar is not too bothered by the weaker than expected headline job data from Australia. 4.9k jobs were added in March, below expectation of 20.3k. Full time jobs dropped by 19.9k to 8.51m while part time jobs rose 24.8k to 3.9m. Total employment was at 12.484m. Prior month's figure was revised down from 17.5k to -6.3k. February now had the first monthly drop in employment since September 2016. The record streak of consecutive monthly job growth has shorted to 16 months.

Seasonally adjusted unemployment rate was unchanged at 5.5%, after downward revision in February's figure from 5.6% to 5.5%. However, labor force participation rate rose to 65.7%, sitting at a record high in since the series began back in 1978. The figures just showed that growth in the Australian labor market is slowing after a very strong period since late 2016. .

Australia NAB business condition rose to highest since 2007

Australia quarterly NAB business confidence was unchanged at 7 in Q1. Quarterly business conditions rose from 15 to 17. In the release, NAB noted that the quarterly business condition was at its highest level since 2007 even though the monthly survey data eased later in the quarter. Business confidence has been relatively stable since Q3 2016, staying within a range of 6 to 8, and was a little above historical average of 5. While there is no upward wage pressure, the conditions are in place due to tightening labor market.

Regarding RBA monetary policy, NAB noted that businesses are pricing in around 80% chance of a 25bps hike within 12 months. RBA itself noted that " RBA will want clear evidence that wages growth and inflation are moving higher before removing some policy accommodation, and we don't expect sufficient evidence of this until late 2018". NAB expects RBA to have the first hike in November "with the risk that it occurs later".

RBNZ Orr: Very benign inflation going forward without doubt

New Zealand CPI slowed notably to 1.1% yoy in Q1, down from prior quarter's 1.6%, meeting expectation. RBNZ Governor Adrian Orr said in Radio New Zealand interview that he expected "very benign inflation going forward without doubt, as we've forecast".

He added that "what really matters is the confidence and expectation and belief that we are aiming for that midpoint of 2 percent all of the time." And he pledged that "we are doggedly determined to aim for two percent, but the accuracy around...that is very limited."

Overall, with CPI now close to bottom of RBNZ's target band, there is little pressure for the central bank to raise interest rates.

Canadian Dollar recovers some ground after post BoC selloff

Canadian Dollar suffered some selling pressure overnight, but recovers in Asian session today. BoC has sent a mixed message with yesterday's statement. Although the next rate adjustment remains a hike, the timing remains data-dependent and hinged on a number of uncertainties, including NAFTA negotiations and geopolitical tensions, something critical to Canada due to its position as oil exporter. Policymakers upgraded the assessment over the global economic outlook and remained optimistic over the domestic developments. However, they revised lower the forecast of GDP growth this year. The market has priced in 34% chance of a rate hike in May. We expect the next move to come in June. More in BOC Revised Lower Growth Forecast for 2018, Sent a Mixed Message

More on BoC:

- Bank of Canada Holds Rates Steady, Maintains Flexible Tightening Bias

- Bank of Canada Maintains Benchmark Rate

Looking ahead

UK retail sales will be a focus in European sessions. Eurozone will release current account. Later in the day, US jobless claims, Philly Fed survey and leading index will be released.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7752; (P) 0.7775; (R1) 0.7805; More...

Breach of 0.7809 temporary top suggests rebound from 0.7642 is resuming. Intraday bias in AUD/USD is back on the upside for 0.7915 resistance next. Decisive break there should confirm whole decline from 0.8135 has completed at 0.7642. In that case, further rally should be see back to retest 0.8135 high. However, break of 0.7743 minor support will turn bias back to the downside for 0.7642 low instead.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q1 | 0.50% | 0.50% | 0.10% | |

| 22:45 | NZD | CPI Y/Y Q1 | 1.10% | 1.10% | 1.60% | |

| 1:30 | AUD | Employment Change Mar | 4.9K | 20.3K | 17.5K | -6.3K |

| 1:30 | AUD | Unemployment Rate Mar | 5.50% | 5.50% | 5.60% | 5.50% |

| 1:30 | AUD | NAB Business Confidence Q1 | 7 | 6 | 7 | |

| 8:00 | EUR | Eurozone Current Account (EUR) Feb | 32.3B | 37.6B | ||

| 8:30 | GBP | Retail Sales M/M Mar | -0.60% | 0.80% | ||

| 12:30 | CAD | ADP Payrolls Mar | 32.7K | |||

| 12:30 | USD | Initial Jobless Claims (APR 14) | 230K | 233K | ||

| 12:30 | USD | Philadelphia Fed Business Outlook Apr | 21.2 | 22.3 | ||

| 14:00 | USD | Leading Index Mar | 0.30% | 0.60% | ||

| 14:30 | USD | Natural Gas Storage | -19B |

RBNZ Orr: Very benign inflation going forward without doubt

New Zealand CPI slowed notably to 1.1% yoy in Q1, down from prior quarter's 1.6%, meeting expectation. RBNZ Governor Adrian Orr said in Radio New Zealand interview that he expected "very benign inflation going forward without doubt, as we've forecast".

He added that "what really matters is the confidence and expectation and belief that we are aiming for that midpoint of 2 percent all of the time." And he pledged that "we are doggedly determined to aim for two percent, but the accuracy around...that is very limited."

Overall, with CPI now close to bottom of RBNZ's target band, there is little pressure for the central bank to raise interest rates.

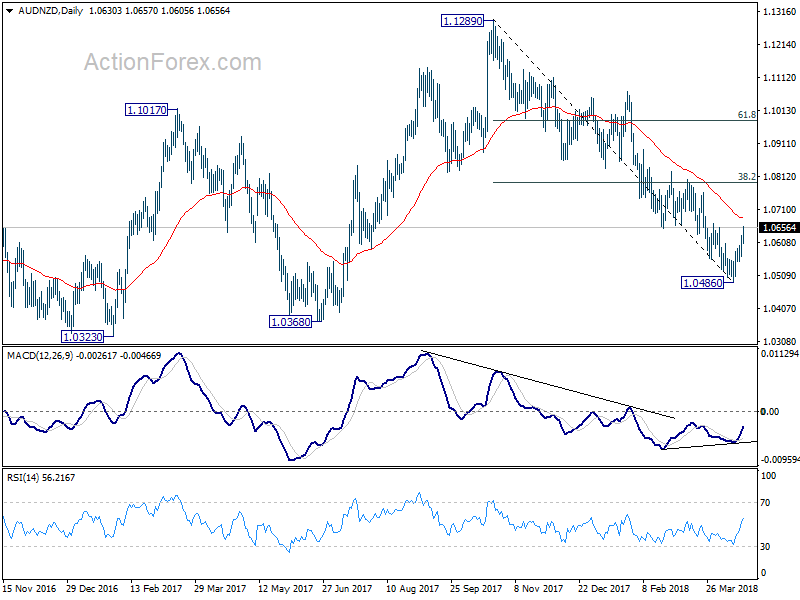

Today's upside acceleration in AUD/NZD further affirm the case that it's bottomed in short term at 1.0486. This is supported by bullish convergence condition in daily MACD. Further rise is now likely in near term back to 55 day EMA (now at 1.0683). But the real test will be at 38.2% retracement of 1.1289 to 1.0486 at 1.0793.

Australia NAB business condition rose to highest since 2007

Australia quarterly NAB business confidence was unchanged at 7 in Q1. Quarterly business conditions rose from 15 to 17.

Highlights from the release:

- Business conditions (an average of trading conditions/sales, profitability and employment) increased by 2pts to +17, its highest level since 2007, although the monthly survey indicates conditions, while still strong, eased late in the quarter.

- Business confidence was unchanged at +7 and it has been relatively stable since 2016 Q3, staying within a range of 6 to 8 pts, a little above its historical average of +5.

- Overall, leading indicators continue to look positive, although there was some easing in expectations for the next three months.

- Labour indicators point to a tightening labour market. While there is no upwards move yet in wage growth the conditions are in place for this to occur.

FINANCIAL MARKET EXPECTATIONS

- On average, businesses are pricing in around an 80% probability of a 25bp rate hike in the next 12-months. NAB Economics' view is that the RBA will want clear evidence that wages growth and inflation are moving higher before removing some policy accommodation, and we don't expect sufficient evidence of this until late 2018 (with the first hike expected in November), with the risk that it occurs later.

- Exchange rate expectations in the Survey (6-months-ahead) rose to almost US$0.78, which is around the average level at the time the Survey was taken.

Full release here.

AUD stays firm as employment data miss is not a disaster

AUD is not too bothered by the weaker than expected headline job data from Australia. 4.9k jobs were added in March, below expectation of 20.3k. Full time jobs dropped by 19.9k to 8.51m while part time jobs rose 24.8k to 3.9m. Total employment was at 12.484m.

Prior month's figure was revised down from 17.5k to -6.3k. February now had the first monthly drop in employment since September 2016. The record streak of consecutive monthly job growth has shorted to 16 months.

Seasonally adjusted unemployment rate was unchanged at 5.5%, after downward revision in February's figure from 5.6% to 5.5%. However, labor force participation rate rose to 65.7%, sitting at a record high in since the series began back in 1978.

The figures just showed that growth in the Australian labor market is slowing after a very strong period since late 2016. .

AUD quickly regained some strength after initial dip as markets realized that the data is not a disaster.

BOC Revised Lower Growth Forecast for 2018, Sent a Mixed Message

BoC has sent a mixed message in yesterday's statement. Although the next rate adjustment remains a hike, the timing remains data-dependent and hinged on a number of uncertainties, including NAFTA negotiations and geopolitical tensions, something critical to Canada due to its position as oil exporter. Policymakers upgraded the assessment over the global economic outlook and remained optimistic over the domestic developments. However, they revised lower the forecast of GDP growth this year. The market has priced in 34% chance of a rate hike in May. We expect the next move to come in June.

BOC left the overnight rate unchanged at 1.25% in April. Policymakers maintained a cautious tone, noting that future monetary policy change would be “guided by incoming data”. On inflation, the members acknowledged recent improvement has been “consistent with an economy operating with little slack”.

They noted that “core measures of inflation have continued to edge up and are all now close to 2%” and “wages have continued to pick up as expected, even after factoring out recent minimum wage increases in Ontario and Alberta”. The wage reference appears more upbeat than the previous meeting which noted that the growth remained “lower than would be typical in an economy with no labour market slack”.

They noted that “core measures of inflation have continued to edge up and are all now close to 2%” and “wages have continued to pick up as expected, even after factoring out recent minimum wage increases in Ontario and Alberta”. The wage reference appears more upbeat than the previous meeting which noted that the growth remained “lower than would be typical in an economy with no labour market slack”.

The most notable change in the accompanying statement was the concluding paragraph which suggested that some “progress has been made on the key issues being watched closely by Governing Council”. Policymakers were reinforced with the view that “higher interest rates will be warranted over time”. This appears more upbeat that the March statement which indicated that “the economic outlook is expected to warrant higher interest rates over time”. Yet, the BOC reiterated that stance in April that “some continued monetary policy accommodation will likely be needed”.

The most notable change in the accompanying statement was the concluding paragraph which suggested that some “progress has been made on the key issues being watched closely by Governing Council”. Policymakers were reinforced with the view that “higher interest rates will be warranted over time”. This appears more upbeat that the March statement which indicated that “the economic outlook is expected to warrant higher interest rates over time”. Yet, the BOC reiterated that stance in April that “some continued monetary policy accommodation will likely be needed”.

On economic forecasts, BOC revised higher global growth outlook to +3.8% for 2018 and +3.6% for 2019, up from previous forecasts of +3.6% and +3.5%, respectively. Growth is expected to ease to +3.4% in 2020. Growth in the US was revised higher to +2.7% for both this year and in 2019, from +2.6% and +2.3%, respectively. Growth is expected to ease to +2% in 2020.

In Canada, the members revised lower the growth forecast, by -0.2 percentage point, to + 2% for this year, before upgrading it by +0.5 percentage point, to 2.1%. Growth in 2020 is expected to ease to +1.8%. The member revised the CPI forecast higher to +2.3% for this year (+2% previous) and +2.1% for both 2019 (unchanged from previously) and 2020.

The members cautioned over “escalating geopolitical and trade conflicts risk” which could undermine global expansion. At the press conference, governor Poloz noted that, while a positive outcome on the May 30 NAFTA renegotiation would result in upward revisions in forecasts, the monetary policy decision would remain data-dependent, rather than pre-empting an expected improvement.

The members cautioned over “escalating geopolitical and trade conflicts risk” which could undermine global expansion. At the press conference, governor Poloz noted that, while a positive outcome on the May 30 NAFTA renegotiation would result in upward revisions in forecasts, the monetary policy decision would remain data-dependent, rather than pre-empting an expected improvement.

Market Morning Briefing: Euro Tested Resistance Near 1.2400-1.2420

STOCKS

Dow (24748.07,-0.16%) is in a pause mode just now. It could test 25000-25500 in the medium term while it holds above the 24500 support. Overall medium term looks bullish for Dow.

Dax (12590.83, +0.042%) is looking bullish too. If the index sustains a rise above 12600, it could target 12800 in the next few sessions.

Nikkei (22309.15, +0.68%) has been moving up for the last few sessions now is likely to move further towards 23000. This could pull up Dollar Yen in the coming sessions and may keep the rate above 107.00.

Shanghai (3115.42, +0.78%) has paused near 3100 levels and if the index does not bounce back immediately, it could fall towards 3000 and could open up chances of a further fall towards 2900-2800.

Nifty (10526.20, -0.21%) tested crucial near term resistance near 10600 and while that holds, a decent correction from current levels is possible towards 10450. Sensex (34331.68, -0.18%) also tests similar resistance near 34600 and could come off towards 34000 in the near term. Overall the Indian equity indices could face some corrective dip in the coming sessions.

COMMODITIES

Brent (73.77) and Nymex WTI (68.72) have risen sharply and look bullish towards 75-76 and 70 respectively. Thereafter a short corrective dip is possible in the medium term.

Gold (1351.90) is trying hard to move up towards 1370 levels but faces tough rejection near those levels. A break above 1370 is needed for Gold to start rising sharply or to trigger a move towards 1400 in the medium term. Crucial level to watch would be 1370.

Copper (3.1570) rose sharply yesterday to close above 3.15 which is now the interim support for the coming sessions. While above 3.15, Copper looks bullish towards 3.20 or even higher.

FOREX

Dollar index (89.69) has risen after testing support on daily candles near 89.25 day before yesterday. As mentioned yesterday as well, the 13 days and 21 days moving average lines on daily line chart near 89.8 could provide immediate resistance. If it breaches 89.8, higher resistance on 3 day candles near 90.00-90.25 could then provide decent resistance, producing a dip.

Euro (1.2375): Euro tested resistance near 1.2400-1.2420 on daily line chart day before yesterday. It has been ranging between 1.239-1.234 since then. As mentioned yesterday, there could possibly be some support from 21 moving averages on daily and 3 day line chart near 1.233-1.235, which is also seen as support level on 3 day candles.

After breaking below 107 day before yesterday, Dollar Yen (107.40), contrary to our expectation, has again risen to see a high near 107.5. However it is still below earlier support trendline on daily candles and could soon take a bearish turn towards 106.5 (close to support on weekly candles).

Euro Yen (132.97) continues to respect resistance near 133, being provided by 21 moving average on the weekly line chart and also seen as horizontal resistance on daily candles. As mentioned yesterday, the range for this week is likely to be between 133-132 as the Dollar Yen might not rise much beyond current level, and the Euro could remain ranged between 1.239-1.233. As per our April ’18 Yen report (available on demand), Euro Yen could possibly turn bearish in the medium term.

Pound (1.419) has dipped after testing strong resistance near 1.43-1.435 (seen as interim resistance on 3 day line chart and horizontal resistance on daily and 3 day candles). It could now dip towards immediate support near 1.415-1.410 on daily line chart before rising again.

Dollar Rupee (65.665): Dips to 65.50-40 may be bought for a target of 66.15 by end-April/ early May.

INTEREST RATES

US Yields continue to rise as positivity towards the US economy grows. We mentioned yesterday that the last 2 weeks has seen crucial US economic indicators throw up improved numbers, which is plausibly causing investors to move away from bonds towards more risky assets. Industrial Production, Capacity Utilization, US Retail Sales data, unemployment claims data and the Fed minutes had all indicated a growing US economy.

US 10 Yr Yield (2.8635%), 30 Yr (3.048%), 5 Yr (2.724%), 2 Yr (2.4231%):

The US 2 year yield after touching 2.4% has risen higher as we expected and could move up further towards 2.45% in the days to come.

The US 10-5 Yr Yield Spread (0.14%) had yesterday broken below strong channel support on short term chart near 0.15%. This could be a false break and the spread could possibly rise back into the channel from here. Let’s wait and watch.

Yesterday, we predicted that the 10 Year yield could possibly rise higher towards 2.85% if risk appetite amongst investors increases. The same has happened. The upside in the near term could be restricted till 2.89-2.90.

The 30 yr yield as we expected, has risen back towards 3.05%. It could possibly rise more towards 3.1% before dipping.

Fed: Beige Book Indicates Solid Economic Momentum amid Rising Costs and Tariff Concerns

Today's Beige Book indicated that economic activity across all twelve Federal Reserve Districts expanded at a modest to moderate pace in March and April, unchanged from the previous month's characterization. While on aggregate outlook remained positive, contacts in manufacturing, agriculture, and transportation industries expressed concern about newly imposed or proposed tariffs, with tariffs mentioned 36 times in this publication.

Weather-related disruptions also stood out in the report, particularly in districts located in the Northeast, where it impacted retail and tourism activity as well as construction.

In tandem with the March retail sales report, consumer spending rose in most regions in March and early April, with gains in non-auto sales and tourism. Auto sales were reported to be mixed, which is somewhat contrary to the national vehicle sales report that showed auto sales jumping to 17.4 million (annualized) in March from 17.0 million in February.

Prices increased at a moderate pace on aggregate, however there were widespread reports about rising steel prices in the aftermath of the tariff announcement. Prices for building materials, such as lumber, drywall, and concrete, also continued to rise briskly. Transportation costs, meanwhile, rose on the back of higher fuel prices and rising labor costs due to shortages of truck drivers. There were some scattered reports of companies successfully passing through price increase to consumers. The frequency of these incidents is likely to increase in the future if input costs continue to climb as businesses are anticipating.

Extending last year's trend, residential real estate inventories remained thin, restraining sales activity in several districts and buoying home prices. Rising labor and material costs as well as lack of available land continues to limit construction of homes. This is in contrast to the commercial real estate segment, where demand and construction activity both improved since the last report.

Widespread job growth continued, with modest to moderate gains across districts. Labor markets remained tight across the nation, weighing on job growth in some regions. Labor shortages were reported across a wide range of industries and skills, but were most apparent in high-skill positions, such as engineering, healthcare, IT as well as in construction and transportation. Companies were responding to tight labor supply in a variety of ways, such as raising compensation, investing in training and automation and increased use of overtime. While wage pressures continued to build, most districts reported wage growth as only modest.

Key Implications

Building inflationary pressures stood front and center in this Beige Book report. Businesses are increasingly facing rising input costs for both labor and raw materials. With declining unemployment, strong economic growth and the risk of further trade tariffs, this trend looks set to continue. For now, many businesses are finding creative ways to absorb rising costs, but some are starting to pass them onto consumers. As a result, we expect that core inflation will continue to rise enabling the Fed to raise rates another two times this year.

Rising input costs will strain housing construction, limiting the already-tight inventory of houses available for sale and boosting home prices, which continue to outpace income gains. Limited inventory and falling affordability, as well as tax changes, will weigh on home sales even as incomes and employment continue to rise. It will also likely sway consumers and builders toward cheaper and smaller units. Recent housing starts data suggests that multifamily construction is making a comeback. While it may be too soon to declare it a trend, particularly amid weather-related disruptions in some parts of the country, it is worth keeping an eye on.