Sample Category Title

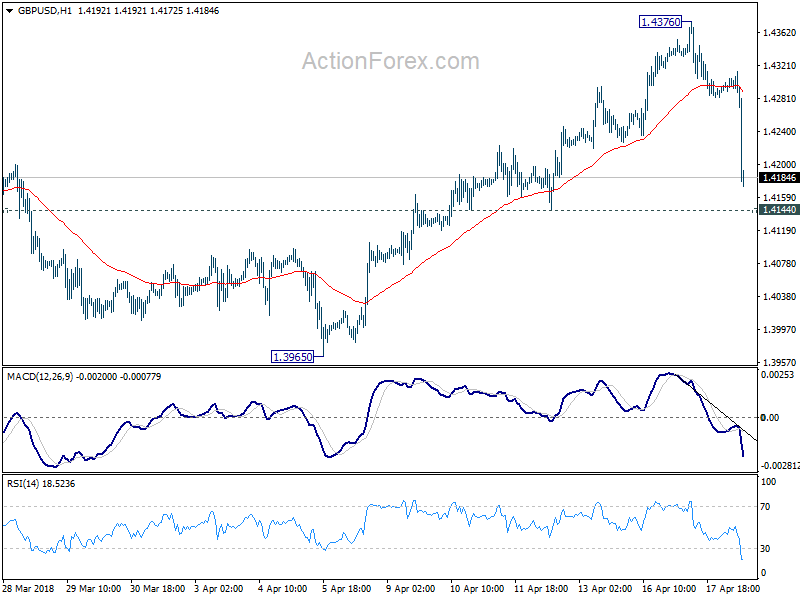

GBP/USD Bearkish Breakout

GBP/USD strong decline from 1.4377 high continues, trading at end March high and heading along the 1.4190 range. Hourly support and resistance are given at 1.3451 (23/02/2018 low) and 1.5018 (24/06/2016 high). The technical structure suggests short-term decline.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

EUR/USD Neutral

EUR/USD slight decline stops, currently trading sideways. The pair is currently maintained between hourly support and resistance given at 1.2165 (17/01/2018 low) and 1.2506 (25/01/2018 high). The technical structure suggests shortterm sideways trading moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

Bitcoin Continued Increase

Bitcoin rise started in mid April continues, trading above 8000 and heading along the 8180 range. Bitcoin bearish pattern started in March 2018 is however maintained as long as the 9000 range is not reached. The pair is contained between hourly support and resistance given at 6306 (13/11/2017 low) and 10232 (01/02/2018 high). The technical structure suggests further short-term increase.

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 7'000 - 12'000 in 2018. Bitcoin is trading slightly above its 200 DMA (8000 range).

USD Bounces Back, GBP In The Doldrum Amid Diappointing Inflation Data

What would Trump do?

This is supremely difficult to answer. Anything can happen, and sometimes does. The Trump administration seems to be more focused on domestic scandals than anything else and is flying by the seat of its pants in most other matters. The President’s disruptive antics could cause an economic contraction, by accident. Nonetheless, the tax cut and the federal spending hike should keep the late-stage business cycle from slowing too quickly. Core inflation should continue to rise gradually, as labour supply tightens, so we still expect the Federal Reserve Bank to hike interest rates three times in 2018 and two in 2018.

Risk aversion is overdone

Concerns over Syria, protectionism and repricing of credit risk have pushed Asian forex lower, especially in the indebted economies. The sell-off provide opportunities to buy the tiger cubs – India, Indonesia and Philippines – with solid structural and cyclical upturns expected. The region’s growth engine is revving strongly. China’s GDP rose 6.8% annually in Q1 2018, beating the market expectations. China’s retail sales increased 10.1% month-on-month in February, up from 9.7% in January

Japan exports less in March

Japan trade surplus continues to arouse the envy of its commercial partners. Maintained at 10 years high, Japan trade balance given at JPY 797.3 billion (USD 7.51 billion) continues to expand, though trade tensions started earlier in the year with the United States. Japan trade surplus also benefitted from intensified trade with its Asian partners, equivalent to JPY 1’005 billion, a level not seen in eight years (5 years average: JPY 255 billion). Accordingly, trade surplus with the US, its second commercial partner after China, slightly decreased at JPY 623.10, a level maintained slightly above its 5 years average.

On the other hand, March exports growth have drastically fallen, valued at 2.10% (consensus: 5.20%), hampered by a decline in mineral fuels, transport equipment and raw materials. Imports endured the same downtrend, decreasing by -0.60% (prior: 16.60%) as shipments from China and Hong Kong slowed down amid US-China confrontation. Decline is felt in electric components, food and manufactured goods.

From a general perspective, yen appreciation since February 2018 remains a big hurdle for Japanese competitiveness (USD/JPY and EUR/JPY -4.73% and -1.89% year to date) and export potential. We remain confident that exports already reaching January lows are not expected to decrease further as the currency impact currently affecting its value in foreign currency is forecasted to decline for the periods to come.

USD/JPY ascension started in March 25th continues, approaching hourly resistance at 107.90 (14/02/2018 high) and heading higher, along the 107.40 in the short-term

Lower Inflation Poses Challenges For Central Banks

- BoC Expected to Leave Rates Unchanged;

- UK Inflation Drop Poses a Challenge For BoE;

- Eurozone Inflation Data Unlikely to Prevent QE End This Year.

'With the Dow steadily creeping back towards 25,000, investors are becoming increasingly comfortable again'

US futures are pointing to a third session in the green for equity markets on Wednesday, extending the good run which has come on the back of a slightly less volatile geopolitical environment. While unemployment is at

While nothing has necessarily improved, per say, the absence of retaliation since the air strikes by the US, UK and France in Syria last weekend has been welcomed by investors who are relieved at the current lack of escalation. With the Dow steadily creeping back towards 25,000, investors are becoming increasingly comfortable again although I feel it will not take much to shake things up again and send markets spiralling lower.

Attention will once again be on first quarter earnings season today with another 10 S&P 500 companies reporting, including Morgan Stanley and American Express. We’ll also hear from the Bank of Canada which is expected to leave interest rates on hold, having only raised them to 1.25% in January. With inflation picking up though and unemployment at pre-financial crisis lows, it’s unlikely that they’ll remain unchanged for too long, even if growth has slowed over the last few quarters.

'The UK inflation data this morning may have thrown a spanner in the works for the Bank of England'

The UK inflation data this morning may have thrown a spanner in the works for the Bank of England, which has for months been preparing markets for an interest rate hike, most likely in May. The central bank has long highlighted the above target inflation as a concern that requires a rate hike in order to bring it back towards target, despite the fact that it was primarily driven by a one-time currency depreciation, more than half of which has since been reversed.

Just as it looked as though everything was falling into line for a rate hike – 43-year low in unemployment, record high employment, wages rising and inflation well above target – the data today has cast a shadow of doubt over it. If inflation is naturally trending back towards target, wage growth is only moderate and Brexit is causing uncertainty for the economic outlook of the UK, can the central bank afford to wait until later in the year before hiking?

While I think that would make sense, I wonder whether policy makers will feel somewhat compelled to raise in May having spent so long hinting at doing so and will compensate for this by stressing that another this year is unlikely. The inflation numbers today were well below expectations and represented another decline after peaking in November but that are still above target which may afford the MPC the ability to hike while still expressing concern about price pressures and the lack of slack in the labour market.

'While the lower inflation numbers may not get in the way of them ending the QE program, it could cause delays in the start of rate hikes next year'

Inflation in the eurozone also fell short of expectations this morning, causing another headache for the European Central Bank as it approaches the end of quantitative easing. The program currently expires in September and could end altogether then or be extended for another short period at a reduced rate as policy makers respond to an improved economic environment by removing the exceptional policy tools that have been used in recent years.

While the lower inflation numbers may not get in the way of them ending the QE program, it could cause delays in the start of rate hikes next year as it will act as evidence that there is still plenty of slack in the labour market.

GBP dives as CPI slowed to 2.5% yoy versus expectation of 2.7% yoy

GBP drops sharply after CPI miss. Headline CPI slowed to 2.5% yoy in March versus expectation of 2.7% yoy. Core CPI dropped to 2.3% yoy versus expectation of rising to 2.5% yoy. Now, slowing consumer inflation is putting a May BoE hike in doubt.

GBP/USD's fall from 1.4376 accelerates after the release. And focus is back on 1.4144 minor support. Break will threaten near term reversal.

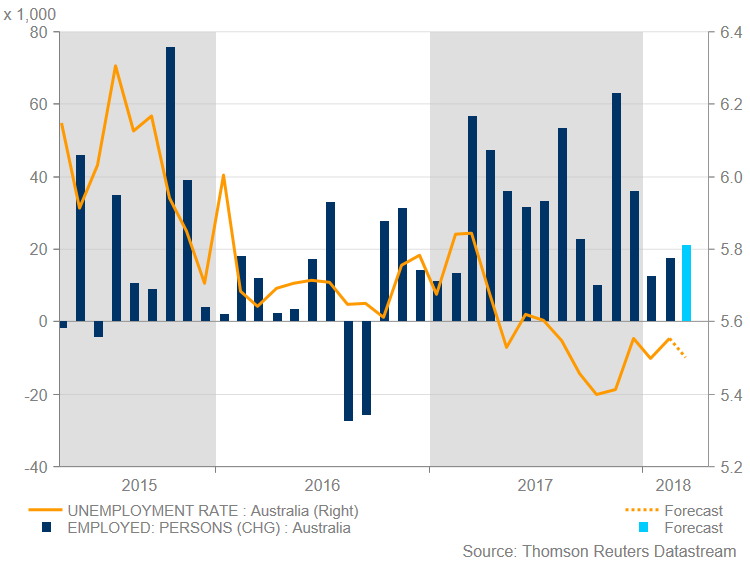

Australia Turns Its Sights To Employment Report And May Help Aussie To Regain Some Poise

Australia’s employment report for March is likely to attract attention and is scheduled for release on Thursday at 0130 GMT. The unemployment rate is forecasted to tick lower to 5.5% for the month of March versus 5.6% the preceding month, while the employment change is expected to show that the economy added 3,500 jobs, much more from the previous month. Meanwhile, the participation rate is predicted to remain unchanged at 65.7%. Could a stronger than expected employment data affect the local currency?

The employment report overnight could drive aussie/dollar higher if the releases beat expectations. It is worth mentioning that Australian employment increased by 17,500 in February compared with 12,500 the prior month, while in the month of March it is forecasted to grow by 21,000 jobs. However, weaker releases could push the RBA to be neutral for a longer period.

Turning to monetary policy, during Tuesday’s Asian session, the Reserve Bank of Australia (RBA) released its latest meeting minutes and showed its Board to agree the next move in rates was more likely to be up than down, assuming the economy gathered momentum as expected. But policymakers saw no important reason for a move in the short term, even as it notched up the longest period without a change. The last move was a cut to 1.5% in August 2016, and financial markets are wagering this steady spell could last until 2019. The Bank has gone more than seven years without raising rates, the longest span since the official cash rate was introduced in 1990. Members noted that growth in employment had remained strong in the first few months of 2018, although the monthly increases in employment had moderated.

Consumer prices in Australia rose 1.9% through the year to the December quarter of 2017, following a 1.8% rise in the previous quarter. Next week’s inflation is predicted to climb by 0.1 percentage points to 2.0% y/y in the first quarter. Crucially, wage growth and inflation has undershot expectations for some years and showed little sign of heating up soon, while GDP for Q4 disappointed, although the nation’s trade balance returned to a surplus in January. Additionally, if commodity prices continue to rise in a longer timeframe and Australian data continues to show a strengthening economy, the market may start pricing in more aggressive RBA policy tightening. The next RBA interest rate decision is coming out on May 8.

Meanwhile, developments in Syria will continue to attract attention, as investors are waiting to see how the US and its allies will act now on following the April 13 strike. Australia’s Foreign Minister Julie Bishop said on April 11 that the government would support a potential military strike by the US on Syria in connection with the alleged chemical weapons attack in Damascus suburb of Eastern Ghouta. However, Australia was not involved in the coalition air strikes against Syria on Saturday but has strongly backed the “calibrated, proportionate and targeted” action taken by US President Donald Trump. Those developments would affect the risk sentiment as well as the market movement in aussie/dollar.

Last week, aussie/dollar snapped the four losing weekly sessions and posted a positive candle, adding more than 1% to its performance, while it continues to pare some of the previous losses. Moreover, the price rebounded on the significant ascending trend line, which has been holding since January 2016 and is ready for a new bullish rally.

If the employment report surpasses the consensus, then the price could create a rally until the 0.7920 strong resistance level in case of a jump above the 23.6% Fibonacci retracement level of 0.7825 from 0.6820 to 0.8135. A break above the aforementioned obstacle could open the door towards the next immediate resistance of 0.7990.

A worse-than-expected figure could create a downward pressure for the pair and would retest the 0.7640 support level in the daily timeframe. In case of a penetration of this area, the strong bullish movement could shift to bearish, as the price would break the medium-term ascending trend line as well. The next support is coming from the 0.7500 handle, taken from the low on December 2017.

Strong Earning Season Lifted Optimism

- Stocks closed higher once again

- Fears around trade war or geopolitical concerns have faded

- UK's wage data posted its best level since 2015

There is one strong force driving the equity markets higher on Wall Street - the stellar earning season. Stocks closed higher once again last night over in the US and the spillover effects of higher equity markets can be seen over in Asia as well. Investors in Europe are also set to build on yesterday’s momentum, generally speaking, it is just one of those risk on days - at least for now.

Fears around trade war or geopolitical concerns have faded very much as the US and North Korea have started high-level talks to de-escalate tensions. Investors focus on the tech and banking sector for now. The earning results of Goldman Sachs confirmed yesterday that higher volatility is something they feed on. Under this environment, their trading revenue could only increase. Although, the confirmation of the same trend is yet to be seen- when other major investment banks will post their earnings.

On the central bank side, the new move by the People Bank Of China under which it has cut the bank reserve requirement by 100 basis points has also stimulated the risk on trade.

As for the forex market, evidence was clear in the U.K. wage data that things have started to move in the right direction. The wage data posted its best level since 2015. We had an evidence yesterday that higher inflation is outpaced by higher wages. The data confirmed that the wage growth was 2.8% while the inflation was 2.7% for the same period. With the further decline in the headline unemployment number, one would hope that the wage growth has only one way to go and that is to the upside.

Traders will be watching the upcoming U.K. CPI number very carefully today. The forecast is that the rising force of Sterling against the dollar would help the number to print a reading of 2.6% while the previous number was at 2.7%

Canadian Dollar Edges Lower, Investors Eye BoC Rate Announcement

The Canadian dollar has posted slight losses in the Wednesday session, erasing the gains seen on Tuesday. Currently, USD/CAD is trading at 1.2584, up 0.26% on the day. In economic news, it’s Rate Day in Ottawa, with the BoC expected to remain on the sidelines. There are no major events in the US, but we’ll hear from FOMC members Williams and Quarles.

The Bank of Canada will be on center stage on Wednesday, with the release of the monthly rate statement. The markets are expecting the bank to maintain the benchmark rate at 1.25 percent. A quarter-point rate hike is expected in the near future, most likely in May or June. The BoC has overestimated Canada’s economic growth, as the economy has fallen well short of the bank’s forecast of 2.5% expansion in both the fourth quarter of 2017 and the first quarter of 2018. In actuality, GDP expanded 1.7% in Q4 and is expected between 1.5% – 2.0% in the first quarter of 2018. Policymakers have some major issues on their plate. The escalating trade war between China and the US could hurt international trade, which would be disastrous for Canada’s export-oriented economy. The protectionist US administration has reopened the NAFTA agreement, threatening to walk away if its demands for major concessions in favor of the US are not met. NAFTA is a crucial component of the Canadian economy, and the loss of NAFTA would be a nightmare for Canada. As well, the Federal Reserve plans a number of rate hikes in 2018, and if the BoC does not raise rates on its end, the Canadian dollar could fall sharply against US currency that is more attractive to investors.

Recent developments in Syria, including a US-led missile strike over the weekend has overshadowed the escalating trade war between the US and China. However, the threat of further tariffs between the world’s largest two economies could again roil the markets. Another salvo was fired on Tuesday, as China slapped a tariff of some 179% on US sorghum crops, which is a livestock feed. China imports about $1 billion of sorghum annually, and the tariff, if it remains in place, will essentially halt US exports of sorghum to China. The Chinese government has threatened to impose tariffs on US soybean exports, valued at some $12 billion each year. If the US opts to retaliate, the specter of an ugly trade war between the US and China could spook investors and hurt minor currencies like the Canadian dollar.

DAX Jumps To 10-Week High On Better Risk Appetite

The DAX index has steadied on Wednesday, after posting sharp gains in the Tuesday session. Currently, the DAX is trading at 12,615 points, up 0.25% on the day. On the release front, the focus is on eurozone inflation indicators. Eurozone Final CPI is expected to climb to 1.4%, while Final Core CPI is forecast to remain unchanged at 1.0%.

The recent trade battle between the US and China has been overshadowed by events in Syria, but the threat of further tariffs between the world’s largest two economies could again roil the stock markets Another salvo in the escalating trade war was fired on Tuesday, as China slapped a tariff of some 179% on US sorghum crops, which is a livestock feed. China imports about $1 billion of sorghum annually, and if the tariff remains in place, will essentially halt US exports of sorghum to China. The Chinese government has threatened to impose tariffs on US soybean exports, valued at some $12 billion each year. If the US administration decides to retaliate, the specter of an ugly trade war between the US and China could spook investors and send global markets into a tailspin.

The German and eurozone economies have looked solid in 2018, making soft ZEW Economic Sentiment reports for April all the more surprising. The April reports were much weaker than expected, but investors shrugged off the numbers as risk appetite has improved. The German release of -8.2 points showed pessimism on the part of institutional investors and analysts and marked the weakest reading since November 2012. The eurozone release of 1.9 was the lowest since July 2o16. The readings are a major disappointment, as the eurozone economy has been performing well and key indicators have been steady. Investors will be hoping that these ZEW releases are one-time blips and that the May readings will be in line with recent releases.