Sample Category Title

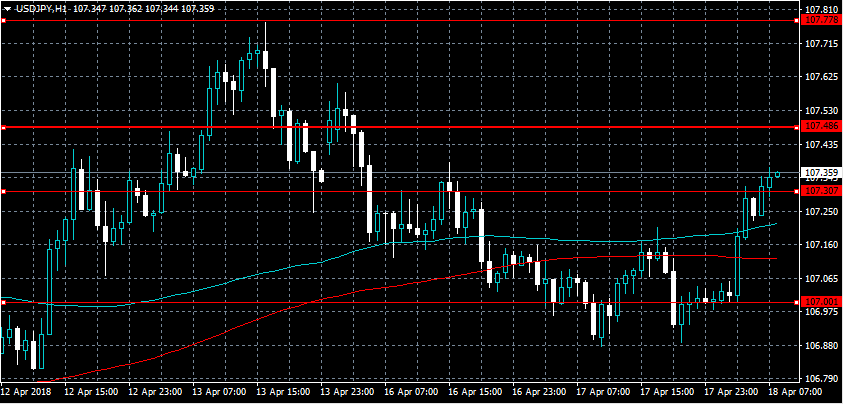

USDJPY Intraday Bullish Above 107.30

The U.S dollar has regained upside momentum against the Japanese yen currency, as a peace deal between North and South Korea and rising global stock markets help to lift market sentiment. The USDJPY pair currently trades around the level 107.30 level, after hitting a new weekly price-low of 106.88, on Tuesday. Traders continue to look to the 107.30 level for intraday direction, with medium-term USDJPY dip-buyers now starting to emerge.

The USDJPY pair is only bearish while trading below the 107.30 level, key weekly support remains at the 106.88 and 106.60 levels.

If the USDJPY pair maintains price-action above the 107.30 level, buyers may be encouraged to retest towards the 107.48 and 107.77 resistance levels.

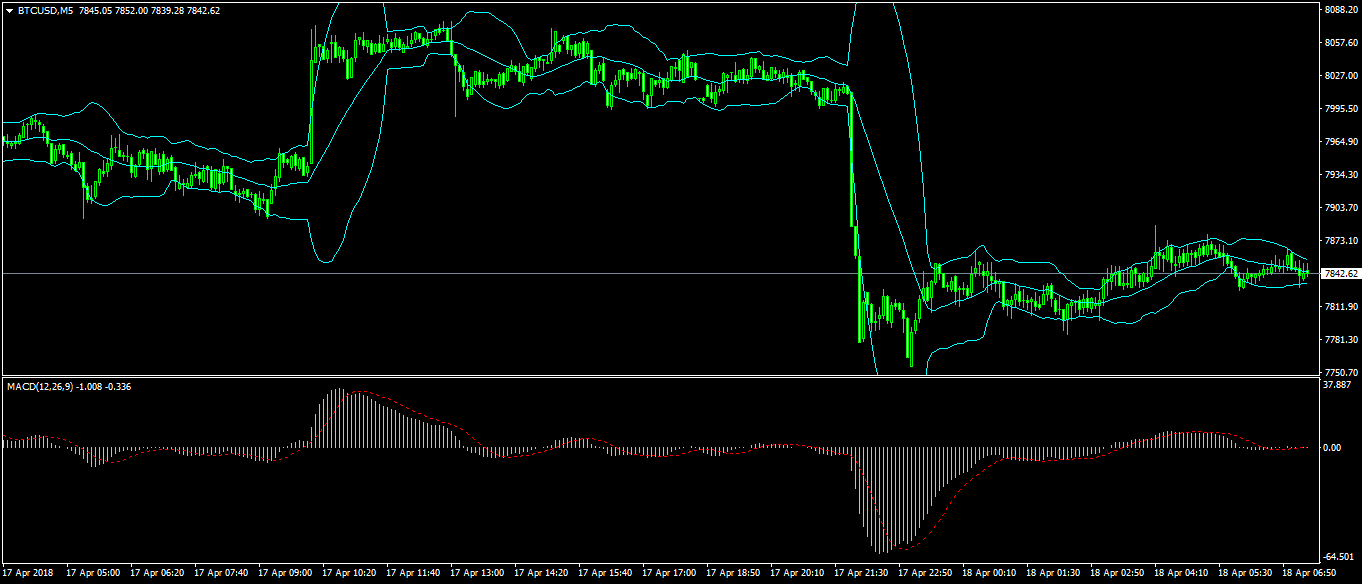

Bitcoin Falls As New York Launches Investigation

In late December, bitcoin reached an all-time high of almost $20,000. After that, the currency started falling, reaching a year to date low of $5,800 in February amidst concerns of increased government regulation. A series of other negative news and commentary from leading analysts contributed to the decline in its price.

After weeks of declines, bitcoin’s price started going up last week amid optimism that the end of the US tax season could attract more traders. It moved from a low of $6670 to a high of $8350.

Yesterday, its price declined after reports emerged that the New York Attorney General was launching an investigation into 13 major cryptocurrency exchanges including Coinbase and Gemini. The officials sent a detailed questionnaire to the firms seeking explanation about their business practices. Their goal for the investigation is to protect the consumers. Traders believe that the investigation will result in the introduction of more regulations.

The news of the investigation came a day after Christine Lagarde, Managing Director of the International Monetary Fund (IMF), called on governments to come up with regulations targeting cryptocurrencies in a bid to make them safe for consumers. In a blog post, she compared cryptocurrencies to other life-changing technologies that have emerged over the past few decades.

BTC/USD is now trading at $7843, at the middle of the Bollinger Bands with the MACD indicator showing that the pair could move in either direction.

Inflation And Monetary Policy Headline Mid-Week Session

Economic data and monetary policy are in the headlines Wednesday, putting currency traders on high alert for big moves in the market.

The European session begins at 08:00 GMT with a report on Italian industrial sales. The Eurozone's third-largest economy reported industrial sales growth of 9.8% year-over-year in February.

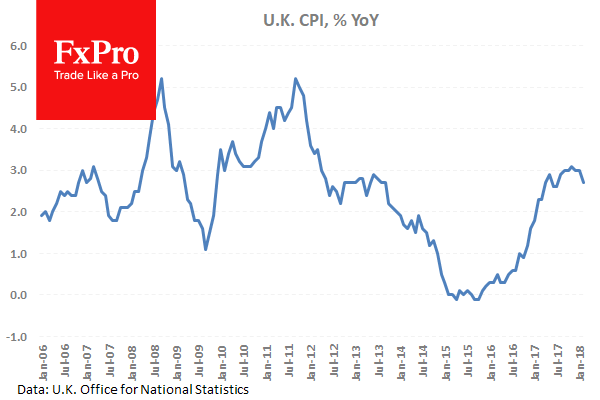

Shifting gears to the United Kingdom, the Office for National Statistics will release a spate of inflation data at 08:30 GMT. This will include the retail price index, producer price index and consumer price index for the month of March.

UK consumer prices are forecast to rise 2.7% annually, unchanged from the previous month. So-called core consumer prices, which exclude volatile items such as food and energy, are projected to climb 2.5% annually.

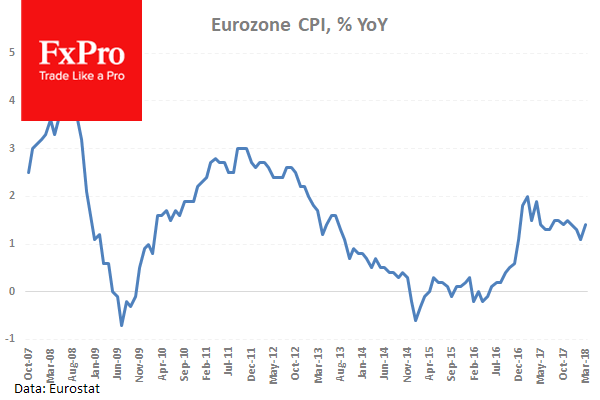

At 09:00 GMT, the European Commission will release the March consumer price index for the 19-member euro area. Consumer inflation is forecast to rise 1.4% annually in March, unchanged from the previous month.

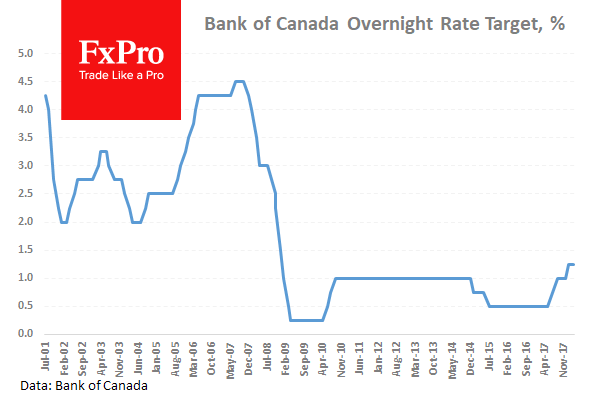

The Bank of Canada (BOC) will headline the North American session with a policy statement at 14:00 GMT. While officials are widely expected to hold off on raising interest rates, the official statement could provide clues about the future of monetary policy. BOC Governor Stephen Poloz is scheduled to hold a press conference at the time of the rate decision.

South of the border, a pair of Federal Reserve officials will deliver speeches on Wednesday. At 19:15 GMT, New York Fed Bank President William Dudley will deliver remarks. One hour later, Fed Governor Randall Quarles is scheduled to speak.

Oil traders will be keeping a close watch on weekly crude inventory data courtesy of the US Energy Information Administration (EIA). EIA stockpiles are forecast to fall 1.9 million barrels in the week ended 13 April. Crude inventories jumped by 3.3 million barrels the week before.

EUR/USD

Europe's common currency reversed sharply on Tuesday after failing to hold above 1.2400 US. EUR/USD plunged from a high of 1.2413 to a low of 1.2346. It was last seen trading at 1.2371, where it finds itself in a familiar range. Immediate support is located at 1.2335.

GBP/USD

Cable also made a decisive break lower on Tuesday, falling below 1.4300 US. GBP/USD touched an intraday high of 1.4367 before falling 80 pips. It was last seen trading just below 1.4300. Investors can expect big moves for the pound should Wednesday's inflation data deviate from the consensus forecast.

USD/CAD

USD/CAD is coming off a volatile session on Tuesday, with prices fluctuating between 1.2527 and 1.2577. The pair was last seen trading near the session highs with attention shifting to the BOC. Canadian monetary policy is now seen trailing the Federal Reserve in terms of hawkishness, which could mean renewed weakness for the loonie.

Europe Awaits Consumer Price Data

At 08:30 GMT, UK Consumer Price Index (YoY) (Mar) will be released and is expected to be unchanged at 2.7%. Core Consumer Price Index (YoY) (Mar) is expected at 2.5% from 2.4% prior. Consumer Price Index (MoM) (Mar) is expected at 0.3% from 0.4% prior. Producer Price Index – Output (MoM) n.s.a. (Mar) is expected at 0.2% from 0.0% previously. Producer Price Index – Output (YoY) n.s.a. (Mar) is expected at 2.3% from 2.6% previously. Producer Price Index – Input (MoM) n.s.a. (Mar) is expected at 0.3% from -1.1% previously. Producer Price Index – Input (YoY) n.s.a. (Mar) is expected at 4.1% from 3.4% previously. Retail Price Index (MoM) (Mar) is expected at 0.3% against 0.8% previously. Retail Price Index (YoY) (Mar) is expected to be unchanged at 3.6%. These data points are expected to show CPI holding steady. The yearly figure has been above the Bank of England’s 2% target since March of 2017, due to the change in the value of the pound after Brexit. However, the BOE says that inflation is likely to move back to 2% in 2018. Easter was early this year and that may affect some of the figures, particularly the airfare numbers. Producer Prices are expected to increase in March after the drop in February. GBP crosses may be moved by the data released at this time.

At 09:00 GMT, Eurozone Consumer Price Index – Core (YoY) (Mar) will be released and is expected to be unchanged at 1%. Consumer Price Index (MoM) (Mar) is expected to be 1.0% from 0.2% previously. Consumer Price Index (YoY) (Mar) is expected to be unchanged at 1.4%. Consumer Price Index – Core (MoM) (Mar) is expected at 1.4% from 0.4% prior. Inflation moved up to 2.0% late in 2016 and early in 2017, the highest levels in five years, but has stabilized around 1.3% since June (YoY). The ECB is looking for inflation to “approach 2%”. CPI data is expected to show an increase in the monthly figures. EUR pairs may see volatility pick up due to this data.

At 12:30 GMT, FOMC Member William Dudley is due to speak at a scheduled event. Any comments could affect USD pairs.

At 14:00 GMT, Bank of Canada Rate Statement will be made public and the Monetary Policy Report and the Interest Rate Decision will also be released. The Interest Rate is expected to remain unchanged at 1.25% but the BOC is likely to signal a reduction in GDP projections, as growth fell short of the mark in Q4 and Q1. This may delay any rate hikes past May and into July.

At 15:15 GMT, the Bank of Canada Press Conference based on the decisions made earlier at 14:00 GMT.

At 18:00 GMT, US Fed’s Beige Book data will be released. USD crosses may be impacted.

At 19:15 GMT, FOMC Member William Dudley is due to speak about the economic outlook and monetary policy at the City University of New York’s Lehman College. Any comments may affect USD pairs.

At 20:15 GMT, Fed Member Quarles is due to speak at the Bretton Woods Committee Annual Meeting, in Washington DC. USD may be impacted by any comments made.

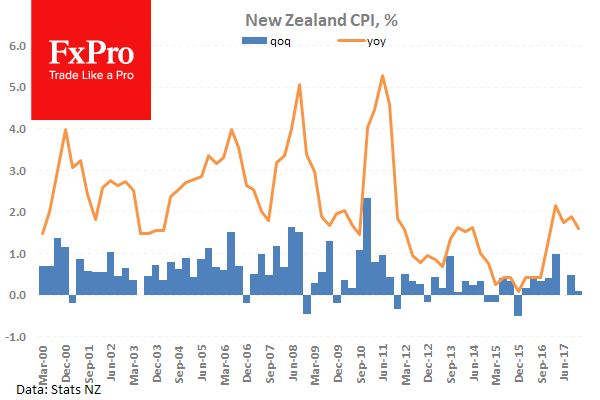

At 22:45 GMT, New Zealand Consumer Price Index (QoQ) (Q1) is expected to come in at 0.5% against a previous 0.1%. Consumer Price Index (YoY) (Q1) is expected to come in at 1.1% against a previous 1.6%. The forecasted numbers for this release are mixed, with the quarterly figure expected to increase but the yearly figure set to drop. This data is lagging quite a bit but is important for NZD traders to gauge the strength of the economy.

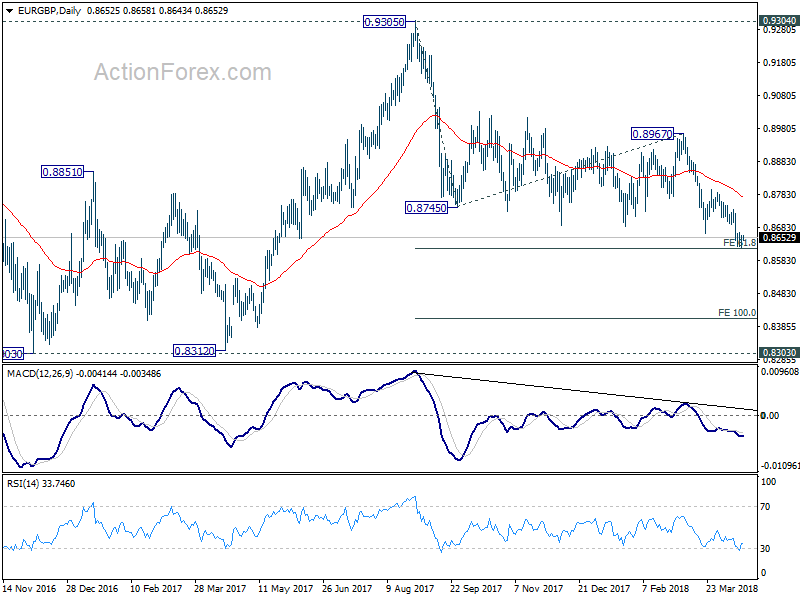

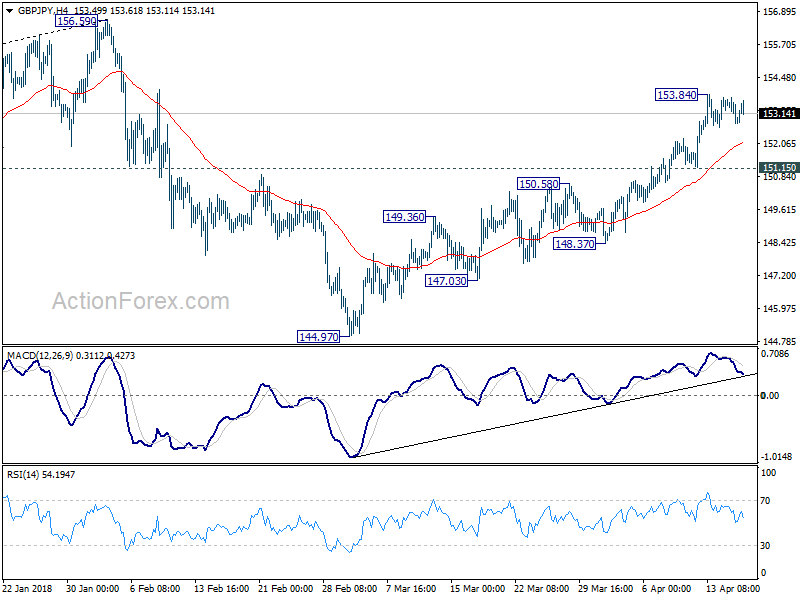

A look at EURGBP and GBPJPY ahead of UK CPI

It's now less than an hour before UK CPI release. The piece of data is even more important after yesterday's wage growth miss. To recap, headline CPI is expected to be unchanged at 2.7% yoy in March. Core CPI is expected to rise to 2.5% yoy, up from 2.4% yoy.

So far, expectations on May BoE hike are firm. According to the latest Reuters poll, all but 7 of the 76 economists surveyed expected a 25bps hike in the Bank rate to 0.75% in May. Barring any disastrous result today, BoE should still be on course for a May hike. The question is indeed on whether BoE would hike again in November.

Technically, GBP's rally stalled this week, particular clear against EUR and JPY.

61.8% projection of 0.9305 to 0.8745 from 0.8967 at 0.8621 is so far a difficult level to break.

But from the EURGBP action bias table and D action bias chart, downside momentum remains firm. It should be just a matter of time that this 0.8621 level is taken out.

But from the EURGBP action bias table and D action bias chart, downside momentum remains firm. It should be just a matter of time that this 0.8621 level is taken out.

GBP/JPY also stalled after hitting 153.84.

GBP/JPY also stalled after hitting 153.84.

But near term strengthen is quite apparent as seen in GBPJPY action bias table and D action bias chart.

Hence, while a CPI miss today might trigger setback in GBP, that should be temporary. On the other hand, GBP could skyrocket if we get something that beat market expectations.

Markets Firmly In Risk-On Mode

Global markets synchronised their appetite for risk after the US stock market broke out earlier in the week, with the German Index and UK 100 following suit. This followed on from positive news on the geopolitical arena, as Syrian tensions eased and trade talks made progress. Corporate earnings are showing good results. The US 500 was up 1.07% yesterday to 2706.39, with the German 30 up 1.57% to 12585.57. The UK 100 was up only 0.39% to 7226.05, despite GBPUSD moving down to retest the 1.42850 area and Oil prices moving higher. USDJPY dipped yesterday in a contrarian move to retest 107.000 but is recovering this morning. Gold traded in a range between 1348.50 and 1338.00, as EURUSD had a brief move above 1.24000.

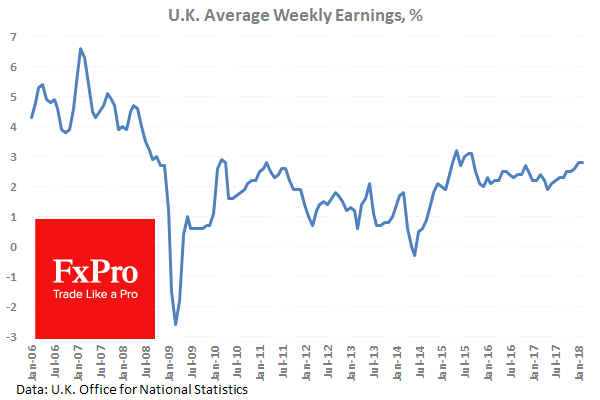

UK Average Earnings excluding Bonus (3Mo/Yr) (Feb) was as expected at 2.8%, from 2.6% previously. Claimant Count Change (Mar) was 11.6K v an expected 5.0K, from a previous reading of 9.2K, which was revised up to 15.1K. ILO Unemployment Rate (3M) (Feb) was 4.2% v an expected 4.3%, versus 4.3% previously. Average Earnings including Bonus (3Mo/Yr) (Feb) was 2.8% v an expected 3.0%, from 2.8% previously. Claimant Count Rate (Mar) was unchanged at 2.4%. Wage growth continued to tick up after stabilizing at 2.5% and moving up last month. The unemployment rate is at multi-decade lows, putting some pressure on wage growth. The Claimant count showed an increase in the number of people claiming benefits, with last month’s number revised higher also. GBPUSD fell from 1.43632 to 1.43057 following this data release.

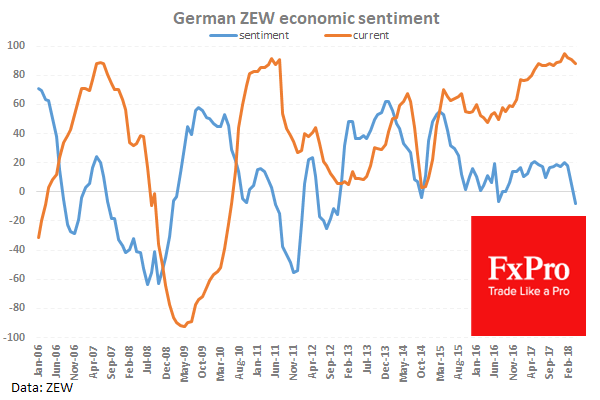

German ZEW Survey – Current Situation (Apr) was 87.9 v an expected 88.0, against a prior 90.7. ZEW Survey – Economic Sentiment (Mar) was -8.2 v an expected -1.0, from 5.1 previously. These data points continued to soften, as the strengthening in the Euro affects business. The deteriorating trade environment is also a headwind for business outlook. The Sentiment was very negative, reaching a low not seen since 2012 and forecasting a growing pessimism in the German economy, in line with the drop seen in other data points. EURUSD moved up from 1.23799 to 1.23867 after this data.

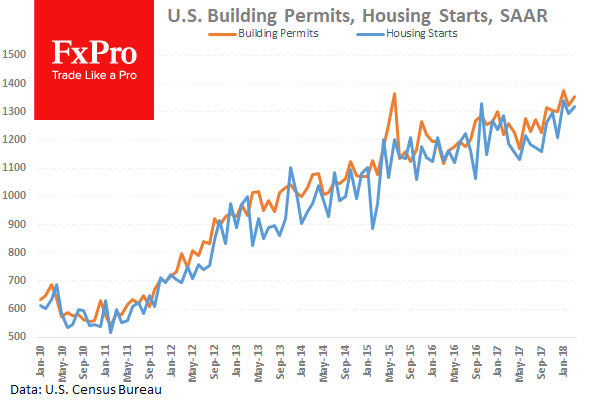

US Housing Starts (MoM) (Mar) was 1.319M v an expected 1.269M, from a previous number of 1.236M, which was revised up to 1.295M. Building Permits (MoM) (Mar) was 1.354M v an expected 1.328M, from a prior reading of 1.298M, which was revised up to 1.321M. This data was expected to show a pick-up in residential construction activity as the weather improves and summer approaches. These data points have been recovering since hitting lows of 0.46M and 0.49M respectively in 2009, after the financial crisis. The numbers exceeded both forecasts.

FOMC Member Williams spoke about monetary policy at a global symposium co-hosted by the National Association for Business Economics and the Bank of Spain, in Madrid. He said that the Fed needs to continue on the path of gradual rate hikes which reduce the risk that the economy could overheat. The outlook for the US economy is very positive. Core inflation is to hit 2% sometime this year. He said he doesn’t expect an inverted yield curve in the next few years. Long-term yields should rise gradually as the Fed hikes. Yield curve inversion would be a warning sign. The biggest risks to the US lie outside its borders.

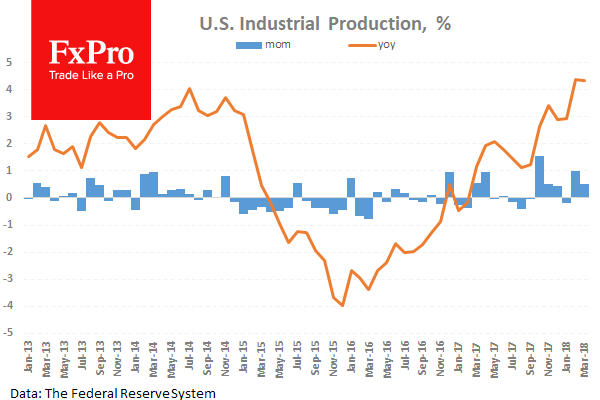

US Industrial Production (MoM) (Mar) was released at 0.5% v a consensus of 0.4%, from 0.9% previously, which was revised up to 1.0%. This measure rebounded strongly to reach the highest reading since December 2014 last month, after slipping below zero in the previous reading. The forecast was lower this month but the data still exceeded expectations, showing relative strength. Capacity Utilization (Mar) was also released at this time coming in at 78.0% v an expectation for 77.9%, against 77.7% prior, which was revised down from 78.1%. This number shows strong performance in capacity utilization.

New Zealand Global Dairy Trade Price Index was 2.7% v a previous reading of -0.6%. NZDUSD moved higher from 0.73266 to 0.73437 following this data release.

FOMC Member Harker gave a scheduled speech in Philadelphia, commenting that the labour market is fairly tight. He also warned that student loan debt could burden workers and dissuade others from higher education.

FOMC Member Bostic discussed the economic outlook in an interview conducted by Bloomberg at an executive workshop, in Atlanta. He said that he was hearing about labour shortages everywhere he went. The goal for Fed policy should be to get to a more neutral stance. The US economy is in a good place but businesses are confused about the direction of US trade policy. He expects to see inflation build. PCE is moving higher and he expects it to be at target in a month or two.

EURUSD is up 0.06% overnight, trading around 1.23763.

USDJPY is up 0.34% in early session trading at around 107.363.

GBPUSD is up 0.15% this morning, trading around 1.43063.

Gold is down -0.30% in early morning trading at around $1,343.00.

WTI is up 0.55% this morning, trading around $67.08.

Currencies: Dollar Still Facing Conflicting Signals Preventing A Clear Directional Trend

Rates: Traditional risk correlation rather loose of late

Core bonds eked out some gains yesterday despite an impressive risk rally. The traditional risk correlation between stocks and bonds is rather loose of late. Today’s calendar isn’t really enticing suggesting more consolidation ahead. The next key event only arrives next week with a new ECB meeting.

Currencies: Dollar still facing conflicting signals preventing a clear directional trend

Yesterday, the EUR/USD rally was blocked after a poor ZEW confidence. However, the dollar also has no convincing momentum. Today, there are few eco data. Risk sentiment will set the tone for global trading. EUR/USD is perfectly holding within the established range. USD/JPY shows cautious signs of a ST bottoming out process

The Sunrise Headlines

- Strong earnings and easing geopolitical tensions lifted US stock markets 1% higher with Nasdaq outperforming (+1.75%). Asian bourses are positively oriented as well this morning with China underperforming.

- The People’s Bank of China said it will cut the reserve-requirement ratio for some banks to reduce their funding costs and in turn help ease conditions for businesses and individuals. (BB)

- The EC has drafted 30-40 proposals to amend laws and give special powers to regulators so that the union can deal with a no-deal Brexit scenario in March 2019 or after a transition period. (FT)

- Atlanta Fed Bostic said “we have been clear our goal is to get to a more neutral stance in terms of interest rates. We are short of that right now.” He expects PCE inflation to be on target in the next month or two

- Beijing has conceded to US policymakers by lifting ownership rules that limit foreign investment in Chinese carmakers, the first significant sign China is willing to bend to American demands. (FT)

- German unions and employers ended marathon pay talks with a phased agreement to boost the pay of more 2 million public sector workers by some 7.5% over two-and-a-half years. (Reuters)

- Today’s eco calendar contains UK and EMU (final) inflation data. The Bank of Canada holds a policy meeting. Fed Dudley and Quarles speak and the Fed releases its Beige Book. Germany taps the bond market

Currencies: Dollar Still Facing Conflicting Signals Preventing A Clear Directional Trend

Dollar still at the mercy of conflicting signals

Yesterday, dollar weakness was replaced by euro softness. EUR/USD traded temporary north of 1.24, but the gain could not be sustained. A poor ZEW investor confidence confirmed recent soft EMU data and weighed on the euro. US eco data were OK but the dollar simply continued the established intraday rebound. Fed Williams was positive on the US economy and on inflation, but hints that the Fed could shift more to price targeting rather than inflation targeting were mixed for the dollar. EUR/USD closed the session at 1.2370. USD/JPY closed at 107.01, despite a good run of US equities.

Overnight, Asian equities join the rebound on WS yesterday. China continues to underperform, despite the PBOC easing monetary conditions. In Japanese investors on the summit between US President Trump and Japan’s PM Abe. For now, no further high profile turbulence on trade issues is expected. US yields are marginally higher after yesterday’s remarkable rise of core bonds (given the equity rally). The impact on currencies is again mixed/diffuse. EUR/USD is holding stable in the 1.2375 area. USD/JPY profits from an easing global tensions and rebounds to the 107.35 area.

Today, there are no US data, but the Beige Book preparing the May 2 Fed meeting will be released. Fed’s Duddley and Quarles will speak. In the EMU the final March CPI will be released. An upward revision might be slightly supportive for the euro, but the report remains a bit of old news. Equities/earnings will probably remain the focus for trading. Trade issues might always resurface, we have the impression that this theme is moving a bit to the background. However, global risk sentiment recently had only a modest impact on major FX cross rates. In this context, we expect more technical trading within the established range. EUR/USD is perfectly holding the 1.2155/1.2550 consolidation pattern. USD/JPY shows tentative signs of a ST bottoming out proces.

Yesterday, UK labour data were close to expectations but kept the door open for modest BoE tightening. Intraday euro softness also pushed the pair further below 0.8650, but sterling falls prey to profit taking later. Today, the UK CPI is expected stable at 2.7%. Brexit ripples might resurface as the House of Lords debates amendments to PM May’s Brexit bill. The scenario of a May BoE rate hike won’t be questioned. In a day-to-day perspective, we look out whether the sterling rally might slow as the break below 0.8650 proves difficult.

USD (tradeweighted): dollar going nowhere

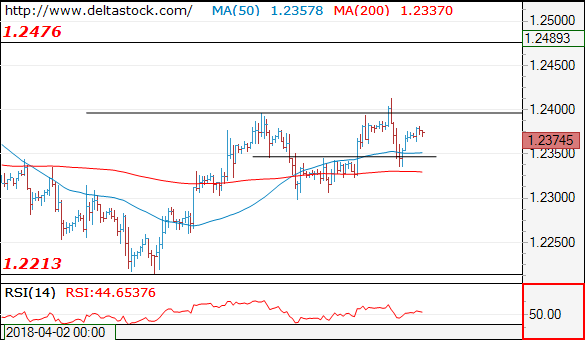

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2374

The reversal at 1.2413 has neutralized the positive outlook and signals, that the prolonged consolidation pattern below 1.2560 is still on the run. The intraday bias is bearish, for a break through 1.2340, towards 1.2280-60 zone.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2380 | 1.2560 | 1.2340 | 1.2160 |

| 1.2470 | 1.2560 | 1.2260 | 1.2090 |

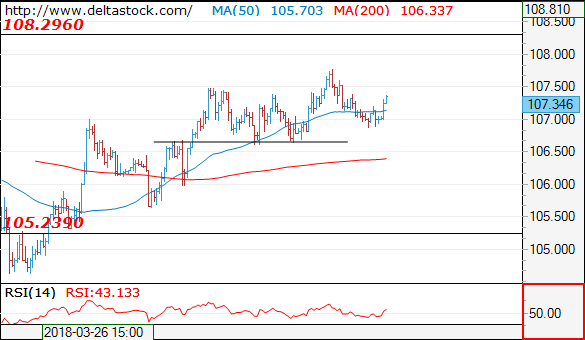

USD/JPY

USD/JPY

Current level - 107.34

The rebound after 106.88 low signals another bull leg towards 107.77 peak, en route to 108.30 major hurdle. Minor intraday support is projected at 107.15. Crucial on the downside is 106.60.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 107.15 | 108.30 | 107.15 | 105.20 |

| 107.80 | 110.40 | 106.60 | 104.60 |

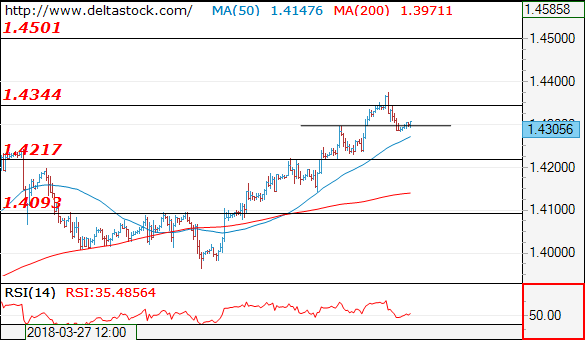

GBP/USD

GBP/USD

Current level - 1..4305

The recent reversal at 1.4375 signals a bearish intraday bias, for a slide towards 1.4217 support area. On the senior frames the outlook is bullish, for 1.4501 zone.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4375 | 1.4501 | 1.4217 | 1.4090 |

| 1.4501 | 1.4770 | 1.4090 | 1.3960 |

UK Inflation Data For March Is Also On The Agenda

Market movers today

In the euro area, the final HICP figures for March are due out. The initial prints surprised on the downside, where non-energy industrial goods in particular were a drag on core inflation. The details will show whether the weak core figure was a result of the lagged impact of the euro appreciation or one-off factors with less concern for the ECB (see tweet ).

UK inflation data for March is also on the agenda. We estimate CPI inflation was unchanged at 2.7% y/y in March (but lower second decimal), while core CPI inflation may have risen to 2.5% from 2.4%. Our base case is still that CPI inflation will move lower this year, as food price inflation has peaked, energy prices are stabilising and the impact of past GBP depreciation is fading.

We have no market movers in Scandinavia today.

Selected market news

The US earnings season is in high gear and the S&P 500 advanced by 1.1% yesterday, propelled by strong results from Netflix, Amazon and Twitter. Asian stocks are also in the green this morning, supported by the weak yen and China's decision yesterday to cut the Reserve Requirement Ratio by 1pp, a measure we think is targeted at increasing loans to small and micro enterprises, to stimulate innovation and entrepreneurship in the country. EUR/USD and 10Y US Treasury yields were steady. Yesterday was another positive day in the European government bond market with a decline in yields combined with a spread compression and especially Italy was the big winner. The 10Y spread between the peripheral markets and Bunds continues to grind lower as the peripheral markets are being supported by higher ratings as seen last Friday in Spain and an expected upgrade of Portugal on Friday.

In the ongoing trade dispute, China seems to have adopted a 'carrot-and-stick approach', promising to abolish foreign ownership caps on electric vehicles, shipping and aircraft manufacturing by the end of the year, while at the same time imposing a 178% import duty on US sorghum crops

German ZEW expectations for April surprised on the downside and dropped to the lowest level since 2012, continuing the recent streak of weak euro area economic data. It was a first indication of how much the latest US-China trade war tensions and geopolitical risks around Syria have dented investor sentiment and we expect similar declines in the April Ifo and PMI readings next week. ZEW expectations now point to a clear growth deceleration (see tweet ), but we still look for solid GDP growth of 2.1% in the eurozone in 2018. In its new WEO projection released yesterday, the IMF comes to a similarly positive assessment, expecting eurozone growth of 2.4% and 2.0% for 2018 and 2019, respectively.

Japanese exports grew by 2.1% in March, less than expected. Foreign demand remains the key growth driver in Japan, as exporters enjoyed the tailwind from the strong global economic upturn. However, recently we have seen the beginning of export weakness, with the yen strengthening and sentiment indicators such as PMIs and Tankan pointing towards some slowdown.

High Level Talks Between US And N. Korea Disclosed

General Trend:

- Another mixed trading session for Asia, despite US gains

- Nikkei outperforms as Trump and Abe meet; Fast Retailing and Softbank rise

- Australia’s Rio Tinto rises over 1%; affirmed iron ore shipment forecast, to revise aluminum guidance

- Asian chipmakers track US gains; Nanya Technology said to see DRAM supply constraints until Q3

- Shanghai Composite has swung between gains and losses, despite targeted RRR cut by PBoC; Banks gain, while automakers underperform

- China govt said to allow foreign auto companies to set up more than two ventures

- Large bad bank China Huarong Asset Management placed on trading halt amid government probe

- Chinese bond yields decline after PBoC RRR cut

- Hong Kong 3-month money market rate rises amid continued currency interventions by the HKMA

- China March new home prices rise at slowest pace since 2016

- Japan March Trade surplus above ests, imports have first decline since 2016; Exports to the US slow

- AUD/NZD in focus as New Zealand Q1 CPI and Australia March Employment data due for release on Thursday

- Taiwan Semi expected to report earnings tomorrow

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.4%; closed +1.4%

- TOPIX Real Estate index +2%, Information/Communications +1.7%, Electrical Appliances +1.4%, Retail Trade +1.3%, Securities +0.9%, Iron & Steel +0.7%

- (JP) Opposition party members call for resignation of Japan Finance Min Aso amid political scandals – Japanese Press

- (JP) JAPAN MAR TRADE BALANCE: ¥797.3B V ¥449BE; ADJ TRADE BALANCE: ¥119.2B V ¥104BE

- (CN) China and Japan to cooperate in relation to services, technology innovation and tourism sectors

- Suruga Bank, [-16%], 8358.JP Japanese Press reports the firm said to have given out loans based on false documents

Korea

- Kospi opened +0.6%

- (KR) IMF affirms South Korea 2018 GDP outlook of 3%, 2019 at 2.9%

- (US) President Trump: Have been speaking directly with North Korea leader Kim

- (US) The then US CIA Director Pompeo said to have met with North Korea leader Kim during visit to North Korea over Easter – Washington Post

- (KR) Bank of Korea (BOK) sells KRW2.9T in 2-yr Monetary Stabilization Bonds (MSB) at 2.105%

- Posco, 005490.KR CEO Kwon said to offer to resign early, he said company needs a new, young leader, but he will remain CEO until a replacement is found - South Korean press

- (KR) South Korea Q1 long term unemployment reaches 18-yr high - Korean press

China/Hong Kong

- Hang Seng opened +0.1%, Shanghai Composite +0.8%

- Hang Seng Energy index +1.3%, Financials +0.7%, Services +0.7%, Property/Construction +0.4% ; Consumer Goods -1.5%, Industrial goods -0.9%

- Shanghai Property sub-index trades flat

- (CN) CHINA PBOC CUTS RESERVE RESERVE RATIO (RRR) BY 100BPS FOR QUALIFIED BANKS (targeted cut); effective Apr 25th (after the close)

- (HK) Hong Kong Monetary Authority (HKMA): buys HK$5.1B to defend currency peg

- (CN) China bond yields move lower after PBoC RRR cut: 1-year swap rate declines over 10bps, China Development Bank 10-year yield declines over 15bps

- (CN) China PBoC Open Market Operation (OMO): Injects CNY150B in 7-day reverse repos v skips prior; Net: injects CNY150B

- (CN) China PBoC sets yuan reference rate at 6.2817 v 6.2771 prior

- (CN) China Feb Avg New Home Prices M/M: 0.4% v +0.3% prior; Y/Y: 4.9% v 5.2% prior

- (CN) China NDRC: Expects 2018 consumer price inflation to be mild, producer price inflation to ease

- China Huarong Asset Management, 2799.HK Chairman being investigated by Central Commission for Discipline Inspection (CCDI) for possible serious disciplinary violations, no further details given

Australia/New Zealand

- ASX 200 opened +0.1%

- ASX 200 Consumer Discretionary index +1.6%, Energy +1.4%, Resources +1.2%, REIT +0.9%; Telecom -0.8%, Financials -0.2%

- Rio Tinto, RIO.AU Reports Q1 Pilbara iron ore shipments 80.3Mt v 80.5Mte; Pilbara iron production 83.1Mt v 77.2Mt y/y

- Woodside Petroleum, WPL.AU Reports Q1 Rev $1.17B v $902.4M y/y; Production 22.2MMBOE v 21.4 y/y

- (AU) Australia Mar Westpac Leading Index m/m: -0.2% v 0.4% prior

- (AU) Australia sells A$600M v A$600M indicated in 3.00% March 2047 bonds, avg yield 3.3628% v 3.4359% prior, bid to cover 3.0x v 2.53x prior

- (AU) Australia Mar Skilled Vacancies m/m: 0.9% v 1.2% prior

North America

- US equities end higher: Dow +0.9%, S&P500 +1.1%, Nasdaq +1.7%, Russell 2000 +1.1%

- S&P500 Technology +1.9%, Consumer Discretionary +1.9%

- VMware [VMW]: Carl Icahn said to acquire less than 5% stake - US financial media

- LUV Follow Up: NTSB Chairman: The company to perform additional inspections on fleet

- IBM [IBM] declines over 5% in the afterhours amid FY18 earnings guidance

- (US) Fed's Bostic (FOMC voter, dove): Businesses are confused by direction of US trade policy; hearing about labor shortages everywhere

- (US) Fed's Williams (moderate, voter): sees US economy continuing to improve; A reassessment of low 10-year yields poses risks

- During Asian session, US 2-year Treasury yield hit 2.4000% (highest since Sept 2008)

- (US) Weekly API Oil Inventories: Crude: -1M v +1.8M prior

- Looking Ahead: Bank of Canada rate decision expected later today

Europe

- (DE) German Chancellor Merkel wants to strengthen role of economic ministers in EU - German press

- Looking Ahead: UK March CPI data due later today

Levels as of 02:00ET

- Hang Seng +0.9%; Shanghai Composite +0.7%; Kospi +0.9%; ASX 200 +0.3%

- Equity Futures: S&P500 +0.3%; Nasdaq100 +0.3%, Dax +0.3%; FTSE100 +0.1%

- EUR 1.2382-1.2365; JPY 107.38-107.00; AUD 0.7773-0.7759;NZD 0.7344-0.7328

- Jun Gold -0.3% at $1,345/oz; May Crude Oil +0.9% at $67.11/brl; May Copper +0.2% at $3.09/lb