Sample Category Title

UK CPI and BoC to Guide the Markets as Sentiments Improved

Markets sentiments turned positive as there were now continuous flow of bad news. All three of DOW, S&P 500 and NASDAQ closed higher overnight, with NASDAQ scoring the best performance. Technically, all three have taken out 55 day EMA decisively which suggests more near term upside. Nikkei follow and is trading up more than 1.4% at the time of writing. In such environment, Japanese yen is trading broadly lower while Euro is generally higher in Asian session.

Looking at the currency markets, Sterling remains the strongest one for the week, together with Euro, despite yesterday's setback. Swiss Franc is trading as the weakest one. EUR/CHF is now back trading at 1.1970 and is on track for the historical level at 1.2000, which SNB tried to defend and gave up in 2015. Many of us remember that day.

Sterling retreated, but stays strong on expectation of May BoE hike

UK inflation data will be the first major focus of today. Headline CPI is expected to be unchanged at 2.7% yoy in March. Core CPI is expected to rise to 2.5% yoy, up from 2.4% yoy. RPI, PPI and house price index will also be featured.

The Pound has pared back some gains after yesterday's mixed job. Unemployment rate dropped to 4.2%, lowest level since 1975. Employment also rose to a record high between December and February, adding 55k jobs. However, average weekly earnings grew only 2.8% 3moy, unchanged from January's reading. That's a disappointing to markets who expected 3.0% 3moy growth.

Nonetheless, the retreat is Sterling is so far shallow and it's quickly regained some ground in Asian session. Also for the moment, the Pound remains the strongest one for the week, and the second strongest for the month, on firm expectation of May BoE hike.

According to the latest Reuters poll, all but 7 of the 76 economists surveyed expected a 25bps hike in the Bank rate to 0.75% in May. The question is indeed on whether BoE would hike again in November. According to the poll, only 37 of 62 economists expected the Bank Rate to be at 1.00% or higher by the end of Q1 next year.

Sterling needs something from there CPI report to give it another bull run.

BoC to stand pat, but may signal readiness for another hike

BoC rate decision is another major focus of today. For now OSI is only pricing 20% chance of a hike today. And it's generally expected that BoC will keep the policy interest rate unchanged at 1.25%. Strong employment data and business outlook survey prompted speculation that BoC would hike again soon. And sentiments were also lifted by surge in oil price, as well as positive sign in NAFTA talks. It's know that Trump is pushing to have a quick resolution to NAFTA for many reasons.

However, it should be noted that trade dispute with the US could remain an ongoing problem. And the 232 steel and aluminum tariff could come back should NAFTA talks collapse. That's seen as one of the biggest risks for the Canadian economy. Additionally, we'd like to point out that IMF has lowered Canada growth projection by -0.2% to 2.1% in 2018. (A summary table can be found here). All advanced economy but Japan's and Canada's projection for 2018 were revised up. The outlook of the Canadian economy might not be as strong as others think.

Traders will certainly look for clues that BoC is ready for another rate hike. If not, focus will turn to Friday's CPI and retail sales.

Japan PM Abe meeting Trump on trade, North Korea and TPP

Japanese Prime Minister Shinzo Abe is meeting Trump in Florida now. Facing domestic political turmoil, Abe is seeking to achieve something out of the summit. The first and foremost is the 232 steel and aluminum tariff of the US. While most other major partners, like South Korea, got exemptions, there is no progress for Japan yet. White House economic advisor Larry Kudlow said waiver on the tariffs, negotiation of new trade agreement are "all on the table".

Abe could try to persuade Trump in rejoining the Trans-Pacific Partnership, which Japan has been leading since Trump's withdrawal. There were signs that Trump is reconsidering. But he continued to pour cold water. Trump just tweeted today that "while Japan and South Korea would like us to go back into TPP, I don't like the deal for the United States. Too many contingencies and no way to get out if it doesn't work. Bilateral deals are far more efficient, profitable and better for OUR workers. Look how bad WTO is to U.S."

The Korean Peninsula issue is another focus of the summit. Japan, as the leader and closet ally of the US in the region, has so far been bypassed regarding the issue. There could be public perception that Abe is not being consulted, or even being involved in the talks between the US and North Korea. And that would hurt Abe's own political credibility, which is already at risk.

Regarding the summit between North Korea and the US, Trump said that "we have had talks at the highest level." But later White house spokesman Sarah Huckabee Sanders clarified those talks were not with Trump directly. Meanwhile, give locations are being considered for the highly anticipated between Trump and North Korean leader Kim Jong-un.

Chicago Fed Evans: No outsized risk of inflation breakout

Chicago Fed President Charles Evans he didn't see an "outsized risk of a breakout in inflation". And as long as that picture continues Fed can "increase rates gradually while monitoring any rising inflationary pressures."

Evans was indeed referring to the risk of 70s style overheating in inflation, as central banks fell behind the curve. And Fed was forced to push up interest rates aggressively in response, which ensued a recession.

But this time, he didn't expect inflation to pick up as quickly or as problematically as it did in the 70s. And therefore, "the federal funds rate does not need to be increased as much above its neutral setting as in the past when trend inflation needed to be taken down several notches." And, "gradual policy increases in this context make sense—certainly as a way to limit the damage if policy ever actually becomes overly tight too soon."

San Francisco Fed Williams: Inflation will stay above target for another couple of years

San Francisco Fed President John Williams said yesterday that inflation is going to rise to and then stay above the 2% target for "another couple of years" even though Fed continues with its tightening path. And he's not worried because "there are global factors that are holding inflation down."

Also, Williams was not concerned with the problem on inverted yield curve. Fed's rate hike will push up short term rates. But at the same time, Fed is unwinding its balance sheet and that will also push up long-term rates. He added that "I personally don't anticipate having an inverted yield curve in the next few years." But he would see "an inversion of the yield curve as a warning sign that sentiment is that growth is going to slow markedly."

Regarding the trade spat between Trump and other countries, he said "what worries me about trade discussion beyond what's happened is if we have continued uncertainty over trade policy what's going to happen over the next few years." And, the uncertainty itself can have a "negative" effect of businesses.

Elsewhere

Japan trade balance came in at JPY 0.12T in March. Australia Westpac leading index dropped -0.2% mom in March. Eurozone will release March CPI final while Fed will release Beige Book economic report today.

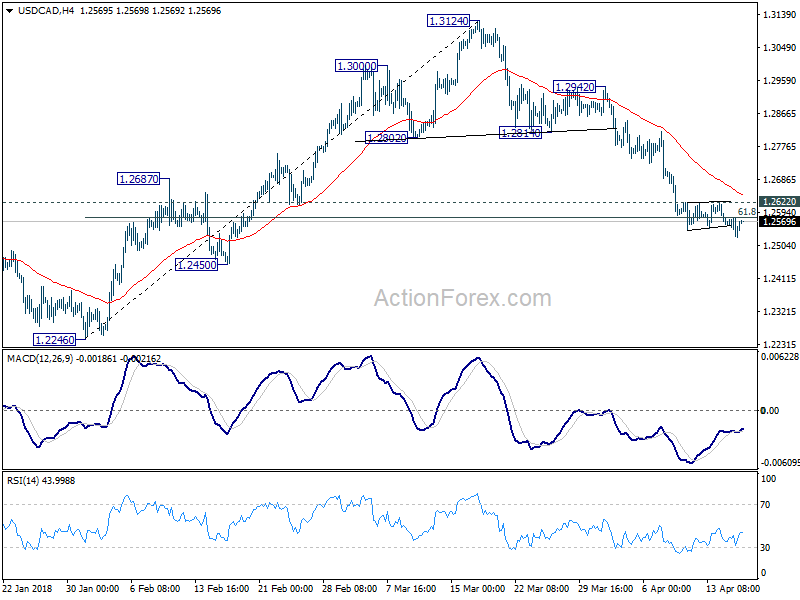

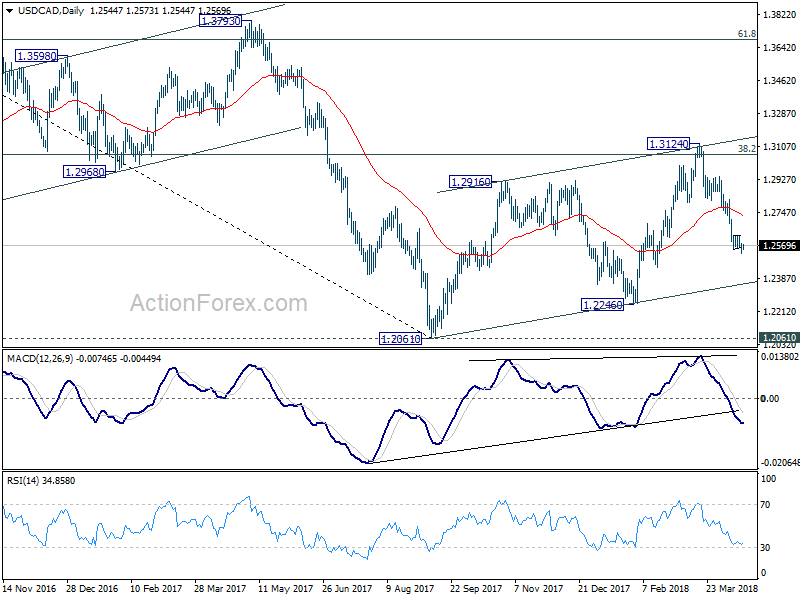

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2526; (P) 1.2552; (R1) 1.2577; More....

USD/CAD's decline from 1.3124 resumed and dipped to 1.2526. But downside momentum is weak and there is no follow through selling yet. Nonetheless, intraday bias will now stay on the downside. Further fall would be seen to 1.2061/2246 support zone. However, break of 1.2622 minor resistance will indicate short term bottoming. And lengthier consolidation would be seen before another fall.

In the bigger picture, current development turns favors to the case that rise from 1.2061 is a corrective three wave pattern. It could have completed at 1.3124 after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Focus is now back on 1.2061 and 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Decisive break there will resume larger down trend from 1.4689 (2016 high) to 61.8% retracement of 0.9406 to 1.4689 at 1.1424.

In the bigger picture, current development turns favors to the case that rise from 1.2061 is a corrective three wave pattern. It could have completed at 1.3124 after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Focus is now back on 1.2061 and 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Decisive break there will resume larger down trend from 1.4689 (2016 high) to 61.8% retracement of 0.9406 to 1.4689 at 1.1424.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Mar | 0.12T | 0.10T | -0.20T | -0.21T |

| 00:30 | AUD | Westpac Leading Index M/M Mar | -0.20% | 0.29% | 0.40% | |

| 08:30 | GBP | CPI M/M Mar | 0.30% | 0.40% | ||

| 08:30 | GBP | CPI Y/Y Mar | 2.70% | 2.70% | ||

| 08:30 | GBP | Core CPI Y/Y Mar | 2.50% | 2.40% | ||

| 08:30 | GBP | RPI M/M Mar | 0.30% | 0.80% | ||

| 08:30 | GBP | RPI Y/Y Mar | 3.50% | 3.60% | ||

| 08:30 | GBP | PPI Input M/M Mar | 0.30% | -1.10% | ||

| 08:30 | GBP | PPI Input Y/Y Mar | 4.20% | 3.40% | ||

| 08:30 | GBP | PPI Output M/M Mar | 0.10% | 0.00% | ||

| 08:30 | GBP | PPI Output Y/Y Mar | 2.30% | 2.60% | ||

| 08:30 | GBP | PPI Output Core M/M Mar | 0.20% | 0.20% | ||

| 08:30 | GBP | PPI Output Core Y/Y Mar | 2.20% | 2.40% | ||

| 08:30 | GBP | House Price Index Y/Y Feb | 4.50% | 4.90% | ||

| 09:00 | EUR | Eurozone CPI M/M Mar | 1.00% | 0.20% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Mar F | 1.40% | 1.40% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Mar F | 1.00% | 1.00% | ||

| 14:00 | CAD | BoC Rate Decision | 1.25% | 1.25% | ||

| 14:30 | USD | Crude Oil Inventories | 3.3M | |||

| 18:00 | USD | Federal Reserve Beige Book |

China Unexpectedly Loosens Monetary Policy by Cutting RRR

People’s Bank of China (PBOC) announced to cut 100 bps in the reserve requirement ratio (RRR), effective from April 25, for large commercial banks, joint-stock banks, city commercial banks, rural commercial banks, and foreign banks. While it would be applied to large and small-to -medium banks with current RRR at 17% and 15% respectively, it would not be applied to those having a RRR below 15%. It is estimated that the reduction would unleash about RMB 1.3 trillion of liquidity. However, about RMB 900B of which would be used for repaying the MLF lending, while the remaining RMB 400B, would largely go to small city and rural banks. Obviously, PBOC’s aim of this move is to avoid over-tightening policy on small banks and small businesses.

During a number of conferences held among Chinese officials, including the 19th National Party Congress, it has been reinforced that the government strives to ensure that financial sector would better serve the “real” economy, that financial institutions deleverage and that banks have appropriate liquidity. In the accompanying statement following the RRR cut, PBOC reaffirmed that its monetary policy would remain “prudent and neutral”. In our opinion, the central bank’s stance appears to have derailed from “prudent and neutral with a tightening bias” adopted since last year to “prudent and neutral”.

The adjustment has probably driven by rising uncertainties, both at home and across the globe, this year. Domestically, despite being distorted by seasonal factors, first quarter macroeconomic data signaled that Chinese economic activities might have slowed. March credit data came in weaker than expected as a result of significant decline in off-balance-sheet lending. Total social financing (TSF) growth slowed to +10.5% in March, compared with +11.3% and +11.2% in January and February, respectively. Externally, while this is not our base case, there are still risks that US-China trade tensions could escalate to a full-blown trade war. These, together with geopolitical risks, could pose downside risk to full-year Chinese GDP growth.

GBP/USD Could Correct Further Toward 1.4250

Key Highlights

- The British Pound faced a strong selling interest near the 1.4375 level against the US Dollar.

- There is a crucial bullish trend line in place with support at 1.4280 on the 4-hours chart of GBP/USD.

- The UK Claimant Change in March 2018 was 11.6K, more than the forecast of 5.0K.

- Today, the UK CPI report for March 2018 will be released, which is forecasted to increase by 0.3% (MoM).

GBPUSD Technical Analysis

The British Pound traded nicely above the 1.4300 level against the US Dollar. However, the GBP/USD pair faced a major resistance at 1.4375 and started a downward correction.

Looking at the 4-hours chart, the pair formed a short-term top at 1.4376 and moved lower. An initial support is near the 23.6% Fib retracement level of the last wave from the 1.3965 low to 1.4376 high.

There is also a crucial bullish trend line in place with support at 1.4280 on the same chart. The most important support is near the 1.4250 level, which was a significant resistance earlier and now it will most likely protect declines.

On the upside, the pair must clear the 1.4350-75 region to extend gains. Above 1.4375, the next major hurdle for buyers is around 1.4400.

Recently, the UK saw the release of the Claimant Change by the National Statistics. The market was looking was a chance of 5K in the Claimant Count.

However, the result was disappointing as the change was on the higher side at 11.6K. Moreover, the last reading was revised up from 9.2K to 15.1K. As a result, there was a downside reaction in GBP/USD from the 1.4375 swing high.

If sellers remain in action, the pair could correct further lower towards the 1.4250 support in the near term.

Economic Releases to Watch Today

- UK Consumer Price Index March 2018 (YoY) – Forecast +2.7%, versus +2.7% previous.

- UK Core Consumer Price Index March 2018 (YoY) – Forecast +2.5%, versus +2.4% previous.

- UK Producer Price Index Input March 2018 (YoY) – Forecast +4.1%, versus +3.4% previous.

- Euro Zone CPI for March 2018 (YoY) – Forecast +1.4%, versus +1.4% previous.

- Euro Zone CPI for March 2018 (MoM) – Forecast +1.0%, versus +0.2% previous.

- Euro Zone Core CPI for March 2018 (YoY) – Forecast +1.0%, versus +1.0% previous.

- BoC Interest Rate Decision – Forecast 1.25%, versus 1.25% previous.

Market Morning Briefing: Euro Saw A High Of 1.2414

STOCKS

Dow (24786.63, +0.87%) continued to rise as per our expectation mentioned yesterday. While above 24500, there is scope for the index to rise towards 25000-25200 in the coming sessions.

Dax (12585.57, +1.57%) has broken above the 12500 resistance following the movement in Dow. While above 12500, the price looks bullish towards 12800.

Nikkei (22130.25, +1.29%) has moved up too along with strength in the other major indices. A rise towards 22500-23000 is on the cards for the near term.

Shanghai (3054.98, -0.39%) is amongst the first indices mentioned in this section to have sharply broken below the medium term support trendline and may indicate upcoming weakness in the overall index for the coming sessions. A fall towards 3000-2900 is possible in the near to medium term. View is bearish.

Nifty (10548.70, +0.19%) and Sensex (34395.06, +0.26%) closed at higher levels yesterday and may continue to move higher in the near term. Sensex is likely to move towards 34500-34600 levels while Nifty closed just near the important resistance at 10550. If the Nifty manages to move higher, it could head towards 10650-10700 levels; else a fall back from current levels would be seen (less likely)

COMMODITIES

Brent (71.93) and Nymex WTI (66.86) could spend some time consolidation below the crucial resistances of 74 and 68 respectively.WTI could re-test 68 while is likely to remain stable just now.

Gold (1346.70) is almost stable just now. 1340 is a short term support on the 3-day chart and while that holds, Gold could test 1370/80 in the next few sessions.

Copper (3.0840) is likely to trade in the 3.05-3.15 region in the next few sessions. Interim resistance is visible near 3.15 while 3 provides long term support.

FOREX

Dollar index (89.51) saw a low of 89.23 yesterday, thereby testing support on daily candles near 89.25. The 13 days and 21 days moving average lines on daily line chart near 89.8 could provide immediate resistance. Higher resistance on 3 day candles near 90.0-90.5 could also be a decent resistance level, producing a dip.

Euro (1.2377): Euro saw a high of 1.2414 yesterday, thereby almost testing the immediate resistance near 1.2400-1.2420 on daily line chart. However it dropped from those levels to close near 1.237 and continues to hover around that level. It could possibly find some support from 21 moving averages on daily and 3 day line chart near 1.233-1.235, which is also seen as immediate support level on 3 day candles.

Dollar Yen (107.25) saw a low near 106.88 yesterday, thereby breaking below immediate support trendline on daily candles but closed above 107 and is currently back to levels near 107.2-107.3. However, it could dip from here again back below 107 and turn bearish in the near term. If that happens, it could target levels near 106.5 soon (close to support on weekly candles).

Euro Yen (132.74) as we predicted is respecting resistance near 133, being provided by 21 moving average on the weekly line charts. The range for this week is likely to be between 133-132 as the Dollar Yen could again drop below 107, while the Euro could dip towards 1.235.

Pound (1.43) is likely to see some resistance near 1.43-1.435 (seen as interim resistance on 3 day line chart and horizontal resistance on daily and 3 day candles). As we have mentioned earlier, this is a crucial level, whose break could imply bullishness towards 1.45-46 in the medium term (seen as resistance on weekly line chart).

Dollar Rupee (65.6475): Trend clearly on the upside. Downside limited to 65.50-30. A rise past 65.70-80 targets 66.15+

INTEREST RATES

Positivity towards the US economy continues to grow as the Industrial Production and Capacity Utilization figures came out higher than expected yesterday. Earlier, US Retail Sales data, unemployment claims data and the Fed minutes had all indicated a growing US economy. Consequently, shorter term yields have risen to record highs, with investors plausibly moving towards more risky assets.

US 10 Yr Yield (2.834%), 30 Yr (3.018%), 5 Yr (2.69%), 2 Yr (2.398%):

The US 2 year yield touched 2.4% yesterday and could rise higher towards 2.45% in the days to come.

The US 10-5 Yr Yield Spread (0.14%) has broken below strong channel support on short term chart near 0.15%. Let’s see if this break sustains.

The 10 Year yield continues to stay near resistance on short term charts and could dip lower to 2.8% in the coming sessions. If risk appetite amongst investors increases, we could see the 10 year break above 2.83-2.85. However, that is less preferred.

The 30 yr yield as per expectation has dipped and could rise from these levels.

Familiar Themes With Little Inference

Familiar Themes With Little Inference

The absence of geopolitical escalations (for now) has helped market sentiment steady as traders work familiar themes with little inference. But outside of earnings-inspirited gains in equities, global markets remain incredibly uncommitted with despondent G-10 currency traders desperately seeking some direction.

Wall Street pushed higher overnight on robust corporate earnings, encouraged by a stellar showing from Netflix powered technology shares higher. Indeed a breath of fresh air as traders turn focus to data and corporate profits, yet remain cautious knowing stock markets are only one presidential tweet away from upsetting the apple cart.

Yesterday's China Data continued to be discussed but in negative context despite Q1 GDP coming in on expectations. Indeed, escalating trade tensions amid China's deleveraging policies, on the surface, does suggest domestic growth may be cresting.

The PBoC announced it would cut reserve requirement ratio (RRR) by 1 ppts for most banks by next week, but this is being widely viewed as a reprieve for the banks to repay MLF loans and not a tweak in monetary policy.

Oil Markets

The American Petroleum Institute figures for the week ended April 13 showed a 1.0 million barrel decline in US crude oil inventories as crude oil imports fell 644,000 bpd, more than enough to counter the 35,000 declines in refinery crude runs. The draw was slightly more than the consensus expectation. Which has provided a late NY afternoon fillip to oil prices

While geopolitical concerns and supply disruption implication simmering on the back burner, and with few new conclusions on that front, traders were in consolidation mode while debating China ‘s economic view in the wake of post Q1 GDP

However, focus remain squarely on the possible re-imposition of sanctions against Iran as this would boost oil prices dramatically as that the country is a weighty player in the global oil supply chain.

Gold Market

Gold prices traded below 1340 overnight on the back of fall out from yesterday China data bump which has some trader thinking the mainland economy could slow down much faster than expected.But with geopolitical and trade war concerns still fermenting the move provided was short lived. But with the lack of any geopolitical or trade war headlines, Gold will also be very susceptible to shifting dollar sentiment which also played a factor in the overnight sell-off as the dollar picked up some steam on the softer China economic view. Finally, positivity from US earnings season has likely caused a bit of asset rotation out of gold into equities. All of this is suggesting long gold trade will continue to be a patience game over the short term.

Currency Market

“Money is made by sitting, not trading.” – Jesse Livermore: I hope that comes true as we currency traders have been doing a lot of sitting lately.

The British Pound

Sterling Bulls have tamed overnight on the back of a very sobering wages data. But not to fret, they get the second kick of the can tonight when the critical CPI data is released. Indeed Sterling Bulls got ahead of themselves way too long but with little else to take a view on, G-10 currency traders need something to run with, unfortunately, it wasn't the running of the GBP bulls most had expected.

The Japanese Yen

Equity markets are alive and kicking, and with the US yield holding steady there's very little to suggest. Similar to yesterday view, we're waiting for the next headline

The Euro

A tug of war on many levels with weakness in core data but ECB members suggestions it's transitory. However, with trade war rhetoric still echoing in the White House halls, there doesn't appear to be a great deal of upside on the trade. Again waiting for a more definitive signal from the USD

The Malaysian Ringgit

Bond market continued to run quiet and traded slightly softer tracking the overnight move in UST which continued to weigh on Ringgit sentiment. The bottom line, inflows should remain low we expected trade to stay in a sideways direction. But with energy prices holding up well it should limit any further deterioration in the Ringgit and unlikely we will test 3.90 unless oil prices surprisingly upend.

US Oil Inventories Fell Across the Board

The industry- sponsored API estimated that crude oil inventory decreased -1 mmb in the week ended April 13. Cushing stock also dropped -1 mmb for the week. For refined oil products, gasoline stockpile declined -2.5 mmb while distillate slid -0.85 mmb for the week. The agency also estimated that US crude imports fell -0.66 mmb last week. This should remain the trend in coming years as abundant US shale production should reduce demand for overseas oil.

EIA, the US governmental agency, today probably reports a -1.43 mmb draw in crude oil inventory. Gasoline and distillate stockpiles might have dropped -0.23 mmb and -0.27 mmb respectively.

Japan PM Abe meeting Trump on trade, North Korea and TPP

Japanese Prime Minister Shinzo Abe is meeting Trump in Florida now. Facing domestic political turmoil, Abe is seeking to achieve something out of the summit. The first and foremost is the 232 steel and aluminum tariff of the US. While most other major partners, like South Korea, got exemptions, there is no progress for Japan yet. White House economic advisor Larry Kudlow said waiver on the tariffs, negotiation of new trade agreement are "all on the table".

Abe could try to persuade Trump in rejoining the Trans-Pacific Partnership, which Japan has been leading since Trump's withdrawal. There were signs that Trump is reconsidering. But he continued to pour cold water. Trump just tweeted today that "while Japan and South Korea would like us to go back into TPP, I don't like the deal for the United States. Too many contingencies and no way to get out if it doesn't work. Bilateral deals are far more efficient, profitable and better for OUR workers. Look how bad WTO is to U.S."

The Korean Peninsula issue is another focus of the summit. Japan, as the leader and closet ally of the US in the region, has so far been bypassed regarding the issue. There could be public perception that Abe is not being consulted, or even being involved in the talks between the US and North Korea. And that would hurt Abe's own political credibility, which is already at risk.

Regarding the summit between North Korea and the US, Trump said that "we have had talks at the highest level." But later White house spokesman Sarah Huckabee Sanders clarified those talks were not with Trump directly. Meanwhile, give locations are being considered for the highly anticipated between Trump and North Korean leader Kim Jong-un.

Chicago Fed Evans: No outsized risk of inflation breakout

Chicago Fed President Charles Evans he didn't see an "outsized risk of a breakout in inflation". And as long as that picture continues Fed can "increase rates gradually while monitoring any rising inflationary pressures."

Evans was indeed referring to the risk of 70s style overheating in inflation, as central banks fell behind the curve. And Fed was forced to push up interest rates aggressively in response, which ensued a recession.

But this time, he didn't expect inflation to pick up as quickly or as problematically as it did in the 70s. And therefore, "the federal funds rate does not need to be increased as much above its neutral setting as in the past when trend inflation needed to be taken down several notches." And, "gradual policy increases in this context make sense—certainly as a way to limit the damage if policy ever actually becomes overly tight too soon."

San Francisco Fed Williams: Inflation will stay above target for another couple of years

San Francisco Fed President John Williams said yesterday that inflation is going to rise to and then stay above the 2% target for "another couple of years" even though Fed continues with its tightening path. And he's not worried because "there are global factors that are holding inflation down."

Also, Williams was not concerned with the problem on inverted yield curve. Fed's rate hike will push up short term rates. But at the same time, Fed is unwinding its balance sheet and that will also push up long-term rates. He added that "I personally don't anticipate having an inverted yield curve in the next few years." But he would see "an inversion of the yield curve as a warning sign that sentiment is that growth is going to slow markedly."

Regarding the trade spat between Trump and other countries, he said "what worries me about trade discussion beyond what's happened is if we have continued uncertainty over trade policy what's going to happen over the next few years." And, the uncertainty itself can have a "negative" effect of businesses.

DOW and S&P 500 broke 55 Day EMA firmly, heading higher in near term

The strong close in US indices overnight now cleared up the near term direction. DOW closed up 213.59 pts or 0.87% at 24786.63. S&P 500 gained 28.55 pts or 1.07% to 2706.39. NASDAQ was even better, rising 124.82 pts or 1.74% to 7281.10. All three indices took out nearly flat 55 day EMA respectively.

DOW's break of the near term trend resistance at the same time confirms that fall from 25800.35 has completed 2344.52. For the near term further rise could be see back to 25800.35 first. But then, rise from 23344.52 is still having a somewhat corrective look. It's likely just a leg inside the whole corrective pattern from 26616.71 high. Hence, it could start to feel heavy again when it approaches 25800.35.

For S&P 500, first hurdle will be trend line resistance at 2746, and then 2081.90 resistance.

For S&P 500, first hurdle will be trend line resistance at 2746, and then 2081.90 resistance.