Sample Category Title

Dollar surges broadly and… Mnuchin said Trump fired warning shots to Russia and China on devaluation

US Treasury Steven Mnuchin talked to CNBC today and he mentioned President Donald Trump's tweet regarding Russia and China currency devaluation. Mnuchin said that was a "warning shot at China and Russia about devaluation. China has devalued their currency in the past." Mnuchin added that "they've used a lot of their reserves to actually support the currency. The president wants to make sure they don't change their plans, and he's watching it."

Regarding the economy, Mnuchin said "we're now at a point where we're comfortably within our 3 percent or higher sustained economic growth". He added that "we literally have met with hundreds of executives, small companies, big companies, and thousands of workers. We're beginning to see the impact of the tax cuts, specifically people investing large amounts of money back into the United States." Also, "the difference between 2.2 and 3 percent will pay for the tax cuts."

Regarding rejoining TPP, Mnuchin just said that Trump would opt to join only when there are more favorable terms to the US. And Mnuchin is "cautiously optimistic.

Dollar is broadly higher today, entering into US session, after Mnuchin's comments. Is it a coincidence? Or...?

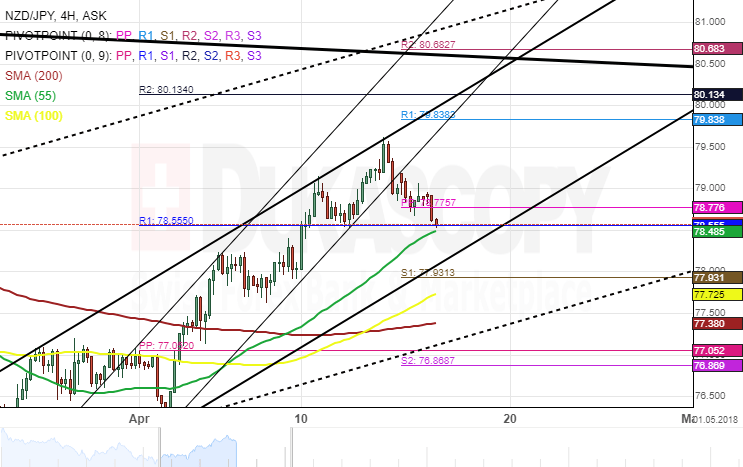

NZD/JPY 4H Chart: Breaking Of Junior Pattern

The New Zealand Dollar has broken the support of the previously drawn too narrow pattern against the Japanese Yen. However, the newly booked high level can be useful.

Our analysts used is as a reference point of the upper trend line of a medium term channel up pattern. The new pattern reveals that the currency exchange rate was facing additional support on Tuesday morning near the 0.78 mark. Moreover, during the next trading sessions, the trend line was set to join and support the monthly R1 near the 0.78.50 level.

Due to these reasons this pair is highly possibly going to soon reverse its direction and resume to surge.

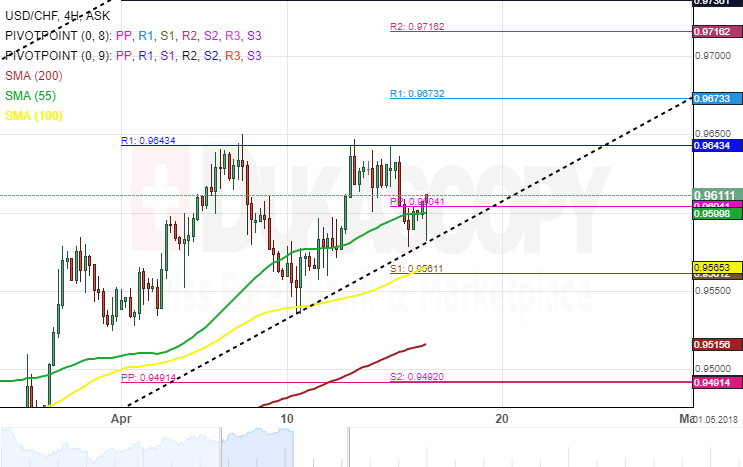

USD/CHF 4H Chart: Reconfirms Pattern

The USD/CHF chart does not require additional drawing, as the pair has been trading while being influenced by technical indicators and lines, which were drawn already last week.

Namely, the pair has bounced off the resistance of the monthly R1 at 0.9640 and retreated down to the lower trend line of the dominant channel up pattern. The currency exchange rate has once more confirmed the location of the trend line by bouncing off of it.

In regards to the short term future, the pair has passed the 55-period SMA and the weekly PP, near 0.96 mark. This indicates at an upcoming surge back up to the mentioned monthly resistance

Trump Shifts From Trade To Currency War, Sterling In Focus

Trump shifts from trade to currency war; Sterling in focus The strong performance of U.S. equities on Monday and better than expected Chinese GDP failed to inspire Asian markets today. Equity benchmarks in Tokyo were slightly lower along with China's CSI and Kospi 200, while Australian ASX rose on support from the materials and consumer sector.

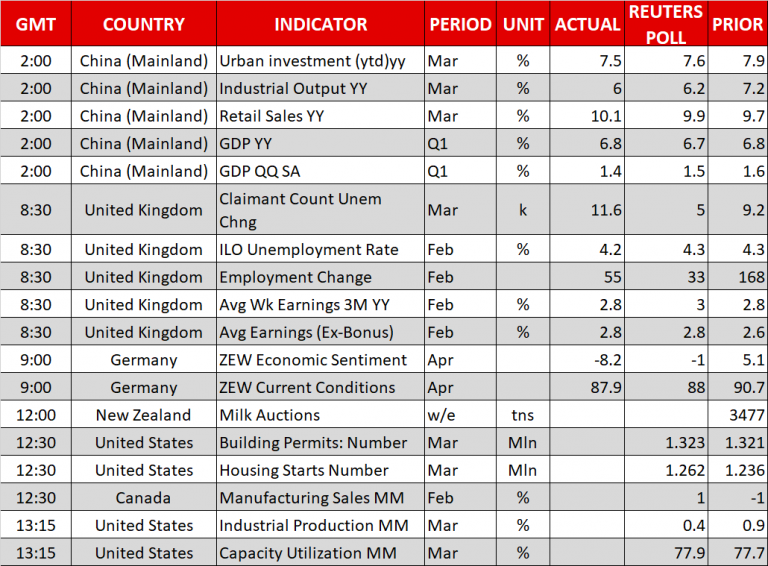

China's GDP managed to beat expectations coming well above the government's target of 6.5% and economists' expectations of 6.7%. The economy grew 6.8% in the first quarter of 2018, supported by robust property investments and consumer consumption. However, there's a lot of doubts that China can sustain the pace of growth, given the uncertainty around trade. Separate data today showed that industrial production in February declined to 6% from 7.2% and fixed asset investment also fell by 0.4% to 7.5%, which supports expectations of the economic slowdown ahead.

Sterling – the best performing currency

Currency traders were impressed by Sterling's performance which has been on the rise for seven days straight. GBPUSD reached a high of 1.4354 in Asian trading session, a level last seen on the Brexit vote. With more than 6% gains since the beginning of the year, the pound is currently the best performing major currency. While the dollar weakness partly explains sterling's strength, higher risk appetite, Brexit negotiations, and surging short-term interest rates were the key attributes to the surging pound. Whether the next level is 1.45 or a correction is due, most likely depends on today's data release. Expectations for a rate hike in May rose above 90%, and now a confirmation from average earnings to justify this move is needed. If average earnings for the three months to February edged up to 2.8% from 2.6%, this would be the first-time wages grow above inflation levels, which currently stand at 2.6%. Unemployment is expected to remain steady at four decades low of 4.3%.

'Russia and China are playing the Currency Devaluation game as the U.S. keeps raising interest rates. Not acceptable!' President Trump

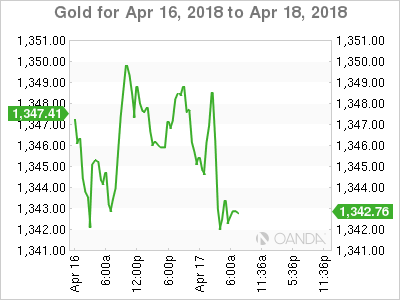

The U.S. dollar took another hit after President Trump said on Twitter that Russia and China are playing the devaluation game as the U.S. keeps raising interest rates. His statement contradicted the Treasury Department report which said no U.S. trading partner is manipulating its exchange rate. In fact, the USD has depreciated by almost 10% against the CNY since the beginning of 2017 and has been declining against the RUB until he decided to scrap new sanctions against Russia on 6 April. It seems that President Trump might be looking to focus on currencies next to influence his trade battle. This explains why the gold didn't fall despite the risk-on mode seen yesterday.

Pound Erases Gains As Wage Growth Disappoints

Here are the latest developments in global markets:

FOREX: Sterling extended yesterday’s rally towards a 22-month high of 1.4375 early today, its highest level since Britain voted to leave the European Union. However, after a disappointing wage growth print today, cable lost ground falling to 1.4315 (-0.14%) despite the unemployment rate inching down to a new 42-year low of 4.2% in February. Dollar/yen was slowly recovering losses made after Trump accused Russia and China of devaluating their currencies, something seen as indicating Trump’s preference for a weaker dollar. The pair was last seen at 107.80 (-0.03%). Euro/dollar slipped back to 1.2364 (-0.11%) after the German ZEW economic sentiment index posted the largest decline since November 2012, while the Eurozone equivalent touched the lowest growth since July 2016. The antipodean currencies weakened, with aussie/dollar and kiwi/dollar being down by 0.04% and 0.31% respectively. Earlier in the day, Chinese yearly GDP growth and retail sales data came in better than expected but discouraging readings on industrial production kept market gains limited. Moreover, the RBA meeting minutes proved once again that a rate hike is not expected anytime soon. Dollar/loonie was trading near its opening level at 1.2562 (-0.01%).

STOCKS: European stocks traded higher today, tracking modest overnight gains after data showed China’s economy grew slightly more than anticipated in the first quarter while easing tensions between Russia and the US provided further support. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.35% and 0.60% respectively. The German DAX 30 climbed by 0.82%, the French CAC 40 gained 0.47%, the Italian FTSE MIB rose by 0.28% while the UK’s FTSE 100 moved higher by 0.26%. Asian equities closed mixed. Futures tracking the major US stock indices were pointing to a positive open.

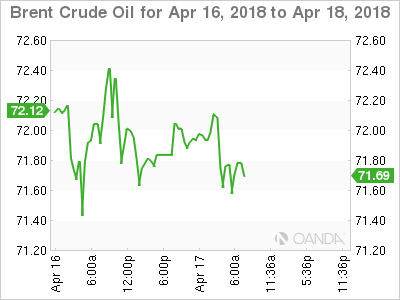

COMMODITIES: WTI crude and Brent were trading higher at $66.31 (+0.12%) and $71.53 (+0.07%) a barrel respectively, following the pullback from their respective three-year highs. In precious metals, gold was falling, last seen $1,342.70 per ounce (- 0.23%)

Day ahead: US industrial production to ease; Abe flies to meet Trump

In the US, building permits and housing starts are scheduled for release at 1230 GMT, with both indicators expected to slightly improve in March, though industrial production due at 1315 GMT could attract more attention. Particularly, analysts expect that American factories have slowed down production in March, with the output growing by 0.4% on a monthly basis compared to 0.9% in February. Manufacturing output, a subset of industrial production, will also be eyed.

In Canada, investors will be taking a look at February’s manufacturing sales due at 1230 GMT which are projected to expand by 1.0% m/m following two consecutive months of declines. A few hours later at 2030 GMT, the focus will turn to the API weekly oil report for the week ending April 13; this might also affect the loonie as Canada is a major oil exporter.

Elsewhere, an update on global dairy prices published at a tentative time will be in focus for the New Zealand dollar (Reuters projects the report to come out around 1200 GMT). Note that the global dairy trade price index was on the backfoot the past six weeks. Should the measure stretch its negative pattern, the kiwi could face additional pressure.

In Japan, trade data will be under the spotlight at 2350 GMT, anticipated to indicate a wider trade surplus in March. Forecasts are for exports to pick up by 4.7% y/y, surpassing February’s growth mark of 1.8% which was the lowest in a year, while imports are projected to post a single-digit expansion of 5.4% for the first time since February 2017. Meanwhile, the Japanese Prime Minister, Shinzo Abe, will be holding a two-day meeting with the US President, Donald Trump, in Florida starting today. Discussions are likely to revolve around trade and North Korea ahead of a crucial summit between Trump and the North Korean leader, Kim Yong Un, in late May or early June. Abe, who has met with Trump on six other occasions already, more than any other leader, might attempt to ensure that the US and Japan are on the same page regarding North Korea’s nuclear program. Moreover, on the trade front, he could negotiate an alternative trade deal with the US as a bilateral partnership seems to be not in his interests. Note that Japan failed to receive an import tariff exemption from the US on aluminum and steel.

In terms of public speeches, it will be a busy day for FOMC speakers, with John Williams (voter), Randal Quarles (permanent-voter), Patrick Harker (non-voter) and Charles Evans (non-voter) delivering comments at 1315 GMT, 1400 GMT, 1500 GMT and 1740 GMT respectively.

In equity markets, Goldman Sachs and Johnson & Johnson will be among companies to report quarterly earnings before the US market open.

Developments in Syria will continue to attract interest, as investors are waiting to see how the US and its allies will act from now on following Saturday’s strike.

Risk Appetite Improves Ahead Of Earnings Reports

- Earnings Provide Distraction From Geopolitical Risk;

- UK Labour Market Strengthens Ahead of May BoE Meeting;

- German Economic Sentiment Slumps to Five and a Half Year Low.

'Earnings season could provide a welcome good news distraction'

With geopolitical concerns appearing to ease in recent days, risk appetite is gradually returning to financial markets with US indices poised to open in the green for a second consecutive session.

Sentiment naturally remains quite fragile but in the absence of an escalation after the US, UK and French strikes in Syria over the weekend and assuming no more trade war threats – both of which are far from guaranteed – indices could continue to gradually pare the losses made since late January. Earnings season could provide a welcome good news distraction in the meantime, with 13 S&P 500 companies due to report.

'The data this morning goes some way to supporting the need for a rate hike'

The economic data from the UK this morning – the first of three important reports this week – was more positive than negative but questions remain about whether it justifies a rate hike from the Bank of England next month. The central bank has strongly hinted in recent months at an increase next month, citing above target inflation and a tight labour market as necessitating such a move but many are questioning the rationale for such a move, particularly given the cloud of uncertainty that hangs over the economy due to Brexit.

The data this morning goes some way to supporting the need for a rate hike. Unemployment is at a 43-year low, employment is the highest since records began and wages are rising, surpassing inflation for the first time in a year, albeit only by 0.1%. On the face of it, all looks positive and with inflation well above target, a rate hike looks sensible. The only issue is that inflation was driven by a one-off currency devaluation, not demand, and is falling while wages are only growing moderately after a prolonged consumer squeeze. Not the ideal environment to be raising rates.

With the pound doing well, that could apply further downside pressure on inflation going forward, although it has slipped a little after the data, more likely due to profit taking after recording seven straight days of gains against the dollar, rather than lower rate expectations. With inflation and retail sales data still to come, it could take something significant to derail the BoE's rate hike plans.

'A number of factors are likely feeding into this though including the potential for a trade war involving the US'

The data from Germany looks more concerning at first sight, with economic sentiment slipping to its lowest level since November 2012, according to ZEW. A number of factors are likely feeding into this though including the potential for a trade war involving the US. While this may point to a slight slowdown in the economy, I don't think it's anything to be concerned about and growth is still expected to remain quite strong.

There's plenty more data to come from the US today, with building permits, housing starts, capacity utilization and industrial production figures all being released. We'll also hear from a number of Federal Reserve policy makers today including John Williams, Randal Quarles, Patrick Harker and Charles Evans, the first two of which are voting members on the FOMC and in recent speeches have stuck to the central banks message of gradual tightening, with Williams having hinted at three to four hikes this year

China’s PBoC lowers RRR by 1% for most banks to release CNY 400b funding support to small and micro...

In a move to increase support for small and micro businesses, the People's Bank of China lowered Reserve Requirement Ratio for most commercial and foreign banks by 1%, effective April 26. On the same day, those banks included could use the funds released by RRR reduction to repay borrowing from the PBoC, on the basis of "borrowed first, repaid first".

PBoC went further to explain that China's small and micro businesses still face difficulties in financing and expensive financing. Lowering the RRR for some banks could release funding to support these businesses. The move could also increase long terming funding and lower costs of the funds. CNY 400B in funds will be released and these funds are required to be used mainly for loans to small and micro businesses

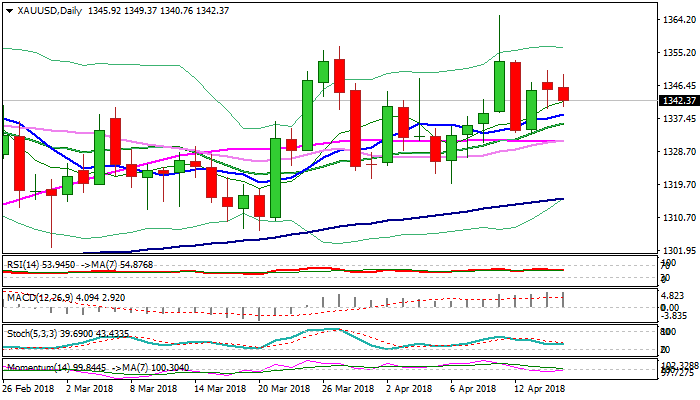

Spot Gold Stands At The Back Foot On Reduced Safe-Haven Demand But Overall Structure Is Still Bullish

Gold price remains in red on Tuesday on reduced safe-haven demand as geopolitical tensions over Syria eased, but holds for now above Monday’s low at $1340.

Rising 10SMA (currently at $1338) reinforces support zone, where dips should be contained, to keep bullish setup of daily techs intact.

Near-term action is also underpinned by thickening daily cloud which twisted on Monday.

Renewed upside attempts could be expected while 10SMA holds, but firm break above $1350 (Monday’s high / recovery rejection) is needed to signal fresh recovery extension towards next barrier at $1356 (27 Mar high / 20-d upper Bollinger band).

Bearish scenario sees increased downside risk on close below 10SMA which would expose next pivot at $1333 (12/13 Apr double-bottom) and turn near-term bias into bearish mode on break.

Res: 1350, 1353, 1356, 1360

Sup: 1340, 1338, 1336, 1333

Dollar Softer Tone Deepens

Tuesday April 17: Five things the markets are talking about

Despite geopolitical concerns lingering in the background, investor focus is back on corporate earnings and on a number of Fed speakers this week.

Overnight, China data showed that their economy expanded in line in Q1 (GDP q/q: +1.4% vs. +1.4%e), March retail sales came in stronger than expected (y/y +10.1% vs. +9.7%e), while industrial production missed estimates (+6% vs. +6.3%e).

The greenback remains under pressure, falling to its lowest level in two months against G7 countries, after President Trump accused Russia and China of devaluing their currencies, contradicting an assessment from the Treasury Department.

Global sovereign yields continue to edge a tad higher and West Texas crude futures drifted higher toward $67 a barrel.

On Tap: The next N.Y Fed head, John Williams, speaks on “the economic outlook” in Madrid today (09:15 EDT), while Fed Governor Randal Quarles is to speak in Washington. President Trump will meet Japan's PM Abe and expect N. Korea and trade to be discussed.

1. Stocks mixed results

In Japan, the Nikkei ended little changed overnight as the market turned a tad cautious ahead of today's Trump/Abe meeting in Mar-a-largo. The Nikkei share average ended up +0.1% after trading in negative territory for most of the session, while the broader Topix fell -0.4%.

Down-under, Aussie shares closed flat on Tuesday, as gains in material and telecom stocks were offset financials. In S. Korea, the Kospi closed lower, falling -0.2%.

In China, stocks fell further overnight amid concerns over trade tensions between China and the U.S, and as investors' pondered China's GDP data for Q1. The CSI300 index fell -1.5%, while the Shanghai Composite Index lost -1.4%. In Hong Kong, the Hang Seng Index closed lower by -0.8%.

In Europe, regional indices trade higher across the board following on from yesterday's stronger U.S trade and stronger futures this morning. The FTSE is underperforming on the overall strength of sterling over the past few sessions.

U.S stocks are set to open in the black (+0.3%).

Indices: Stoxx600 +0.3% at 378.7, FTSE flat at 7199, DAX +0.7% at 12472, CAC-40 +0.3% at 5329, IBEX-35 +0.4% at 9807, FTSE MIB +0.6% at 23467, SMI +0.4% at 8764, S&P 500 Futures +0.3%

2. Oil prices rise amid risk of supply disruptions, gold stronger

Oil prices are better bid amid worries there could be a high risk of disruptions to supply, especially in the Middle East.

Brent crude oil futures are at +$71.75 per barrel, up +33c cents, or +0.5%, from yesterday's close. U.S West Texas Intermediate (WTI) crude futures are up +36c, or +0.5%, at +$66.58 a barrel.

Traders remain concerned about a potentially spreading conflict in the Middle East, renewed U.S sanctions against Iran and falling output as a result of political and economic crisis in Venezuela.

Note: Oil markets have generally been well supported this year, with Brent up by around +16% from it's 2018-low in February, due to healthy demand, supported by OPEC's supply cuts aimed at tightening the market.

Gold prices rise as the dollar slips to its lowest in nearly three-weeks. The metal is also supported by festering worries over U.S/China trade tensions. Spot gold has gained +0.2% to +$1,347.81 an ounce, while U.S. gold futures are steady at +$1,350.60 an ounce.

3. Yields continue to back up

Sovereign bond prices have edge lower again, lifting yields overnight, as the market shrugs off coordinated missile attacks in Syria.

Also supporting higher U.S yields is the FOMC minutes last week showing officials leaning towards a slightly faster pace of tightening at their March meeting as their growth outlook and confidence in hitting inflation targets strengthened.

Yields on both German and U.S 10-year government bonds are both at their highest level in four-weeks.

In Japan, government bond prices remain mixed ahead of today's closely watched meeting between PM Abe and Trump.

The yield on U.S 10-year notes increased +1 bps to +2.84%. In Germany, the 10-year Bund yield climbed +1 bps to +0.53%, while in U.K, the 10-year Gilt yield gained +1 bps to +1.463%, the highest in three-weeks.

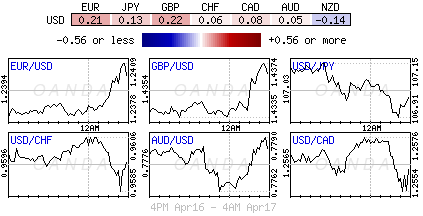

4. Dollar softer tone deepens

The ‘mighty' USD continues to remain soft against the G10 trading pairs.

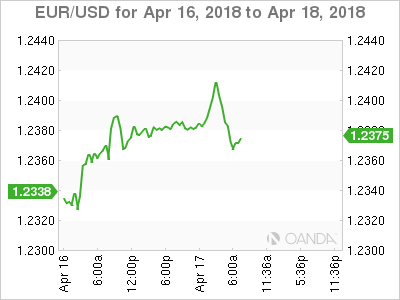

EUR/USD (€1.2379) briefly probed new three-week highs above the psychological €1.24 level before consolidating. The techies see key resistance seen at €1.2470 and break above could ignite upside momentum.

GBP/USD (£1.4320) probed its highest level since the Brexit as it tested the £1.4375 area. However, the pound sound gains evaporate after February earnings data missed expectations. The Bank of England (BoE) is expected to raise interest rates in May. Dealers noted that U.K CPI pressures might have peaked, but the upcoming inflation report is expected to support.

5. U.K jobless rate lowest since 1975

Data in the U.K this morning showed that the unemployment rate declined in February to its lowest level in more than 40 years, while wage growth strengthened.

The jobless rate declined to +4.2% in the three months through February, compared with +4.3% in the three months through January.

Digging deeper, the fall was driven by a rise in employment, while the number of people not seeking work registered a small decline.

Wage growth ex-bonuses accelerated to an annual +2.8% during the three-month period, the fastest rate of growth in three years, driven by higher pay settlements in construction and manufacturing.

Note: This data would suggest that the BoE should remains on track to hike rates in May.

Euro Shrugs Off Soft ZEW Economic Sentiment, Touches 3-Week High

EUR/USD is almost unchanged in the Tuesday session. Currently, the pair is trading at 1.2369, down 0.03% on the day. This is the pair’s highest level since the end of March. On the release front, German ZEW Economic Sentiment surprised the markets with a sharp drop of 8.2 points. This was much weaker than the estimate of -0.8 points. Eurozone ZEW Economic Sentiment also headed lower, dropping from 13.4 to 1.9 points. This fell well short of the estimate of 7.3 points. In the US, the focus is on construction numbers. Building Permits are expected to rise to 1.33 million, and Housing Starts are forecast to improve to 1.27 million. The markets will be listening closely as three FOMC members deliver speeches. On Wednesday, the key event is Eurozone Final CPI.

Syria remains a geopolitical hot spot, where a US-led missile strike destroyed three chemical weapons sites on the weekend. Predictably, Syria and Russia strongly condemned the attack, with Russian President Putin warning that the attack would lead to global “chaos”. Still, a Russian response is unlikely, despite the strong rhetoric. Investors did not show much reaction to the attack, as the markets had already priced in a strike. After the weekend attack, President Trump declaration of “mission accomplished” means that things will remain relatively quiet in Syria. However, further chemical attacks by the Syrian regime could trigger a response from the US and its allies, which could result in volatility in the markets, similar to what occurred last week.

The well-respected ZEW Economic Sentiment reports were surprisingly soft in April. The German reading of -8.2 showed pessimism on the part of institutional investors and analysts and marked the weakest reading since November 2012. The eurozone release of 1.9 was the lowest since July 2o16. The readings are surprising, as the eurozone economy has been performing well and key indicators have been steady. Investors will be hoping that these ZEW releases are one-time blips and that the May readings will be in line with recent releases.