Sample Category Title

Today’s Focus On US Retail Sales As Markets Look To The Week Ahead

At 12:30 GMT, US Retail Sales (MoM) (Mar) will be released, with an expected 0.4% from -0.1% previously. Retail Sales Ex-Autos (MoM) (Mar) is expected to be unchanged at 0.2. Retail Sales Control Group (Mar) is expected to be 0.4% from 0.1% prior. This data is expected to rebound this month, after slipping down over the previous two readings and missing expectations. A miss this time would give the market cause for concern. USD crosses could see increased volatility around this data release.

At 17:15 GMT, FOMC Member Bostic is due to speak about the economy at the Shoals Chamber of Commerce, in Alabama. Audience questions are expected and comments may affect USD pairs.ui

Major data releases for this week:

On Tuesday, at 01:30 GMT, the Reserve Bank of Australia Meeting Minutes will be published.

At 02:00 GMT, Chinese Gross Domestic Product data will be released.

At 08:30 GMT, UK Average Earnings Excluding Bonus data will be out.

On Wednesday, at 08:30 GMT, UK Consumer Price Index data will be released.

At 09:00 GMT, Eurozone Consumer Price Index data will be out.

At 14:00 GMT, the Bank of Canada Interest Rate Decision, Rate Statement and Monetary Policy Report data will be out. A press conference will follow at 15:15 GMT.

At 22:45 GMT New Zealand Consumer Price Index data will be released.

On Thursday, at 01:30 GMT, Australian Jobs data will be released including the Unemployment Rate.

On Friday, at 12:30 GMT Canadian Retail Sales data and Consumer Price data will be out.

Syrian Strikes Limited In Nature, Risk-On Markets Result

The US, UK and France took military action against Syrian Government forces over the weekend. Three targets were hit in combined missile and airstrikes, after the US had been in contact with Russia during the week, to give pre-warning and limit collateral damage. The strikes took place after market close on Friday night/Saturday morning, giving the market time over the weekend to note the limited nature of the attack. Russia has condemned the attack but no further response is expected. This has sent the markets into risk-on mode this morning, with stock markets moving higher. In FX, the response had been risk-on but has since cooled, with the USDJPY erasing its earlier gains. USDTRY moved lower but has rallied up to 4.10209. US WTI Oil has also fallen with the relief in tensions.

German Harmonised Index of Consumer Prices (YoY) (Mar) was as expected, unchanged at 1.5%. Harmonised Index of Consumer Prices (MoM) (Mar) was also as expected, unchanged at 0.4%. Coming in as expected, this data release created little movement in the markets. EURUSD fell from 1.23287 to a low at 1.23171 after the data was released.

US Fed Boston President, Rosengren, delivered the keynote speech at the Greater Boston Chamber’s Economic Outlook Breakfast. He made the following comments: there should be at least 3 more US hikes this year. He’s more optimistic than the already ‘quite positive’ FOMC on forecasts for growth. Trade tariffs risk disruption in hard-to-predict ways. Q1 jobs growth is strong, although there is a risk of boom/bust if unemployment drops too low. He expects the jobless rate to drop to 3.7% by end of 2018. The fiscal stimulus could leave the economy vulnerable in the next downturn. He also expects Powell to be consistent with Yellen but it’s a bit early to talk about the Powell Fed. Finally, momentum could drive unemployment to the low-3s this year.

US Michigan Consumer Sentiment Index (Apr) was 97.8 v an expected 100.5, against a previous 101.4. The previous reading was a record high for the index and this slight slip lower is not really a big concern considering the elevated levels. USDJPY fell from 107.647 to 107.501 following the data release.

Baker Hughes US Oil Rig Counts was released, with a headline number of 815 from last week’s number of 808. This was the highest level reached in some time, reflecting an increase in production as prices increase and operations become more viable. We are seeing some downward pressure on prices in early trading.

EURUSD is down -0.09% overnight, trading around 1.23281.

USDJPY is down -0.13% in early session trading at around 107.216.

GBPUSD is up 0.02% this morning, trading around 1.42463.

Gold is down 0.12% in early morning trading at around $1,344.18.

WTI is down -0.86% this morning, trading around $66.77.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

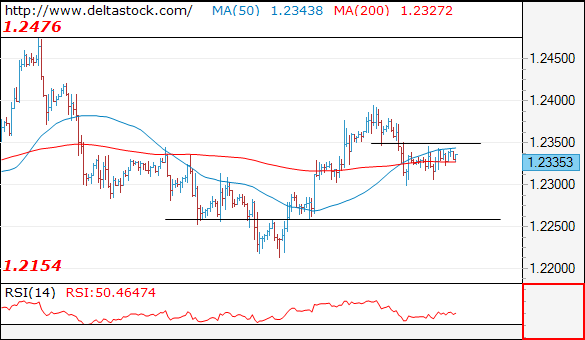

EUR/USD

Current level - 1.2335

The bias is bearish below 1.2350 intraday hurdle, for a slide towards 1.2260 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2350 | 1.2560 | 1.2300 | 1.2160 |

| 1.2420 | 1.2560 | 1.2260 | 1.2090 |

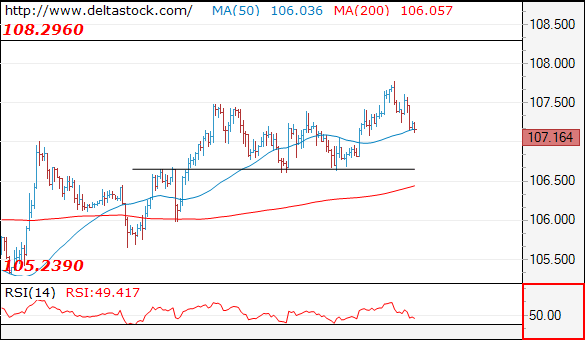

USD/JPY

USD/JPY

Current level - 107.16

Current pullback after 107.77 should be considered corrective, preceding another leg upwards, to 108.30 major resistance. Crucial on the downside is 106.60 and only a violation of the latter will signal a reversal of the whole rise since 104.60 low.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 107.90 | 108.30 | 106.60 | 105.20 |

| 108.30 | 110.40 | 105.60 | 104.60 |

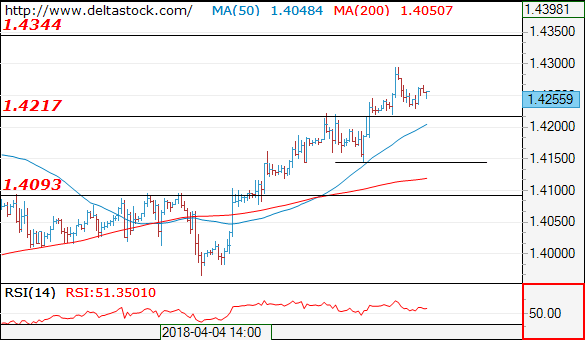

GBP/USD

Current level - 1..4255

The reversal at 1.4296 managed to provoke a minor pullback, but I favor a continuation of the slide, for a break through 1.4217 static support, towards 1.4145 and 1.4090.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4296 | 1.4340 | 1.4217 | 1.3910 |

| 1.4340 | 1.4340 | 1.4145 | 1.3710 |

GBPUSD Intraday Bullish Above 1.4255 Level

The British pound has opened the new trading week with a bullish tone against the U.S dollar, despite buyers failing to close the former weekly candle above the pairs 200-week moving average. The GBPUSD pair currently trades around the 1.4250 level, after finding strong technical resistance from the 1.4295 level on Friday. Traders continue to look towards the pairs 200-week moving average for guidance, with sterling’s last week close above this key technical indicator dating back to November 2015.

The GBPUSD pair maintains a strong intraday bullish bias while trading above the 1.4255 level, with key resistance is located at the 1.4295 and 1.4345 levels.

Should the GBPUSD pair fail to hold above the 1.4255 level, sellers may test towards the 1.4200 and 1.4146 support levels.

USDJPY Only Bearish Below 107.00 Handle

The U.S dollar has pulled back against the Japanese yen on risk-aversion, after putting in a bullish seven-week trading high on Friday, hitting 107.76. The USDJPY pair currently trades around the 107.20 level, as financial markets move into safe-haven asset classes, following the military action from the U.S, UK and France in Syria. USDJPY traders now look to the European and U.S markets reactions and key monthly Retail Sales data from the United States economy.

The USDJPY pair retains a bullish bias while trading above the 107.00 level, key resistance is now located at the 107.77 and 108.45 levels.

If the USDJPY pair trades below the 107.00 level, key sellers may test towards the 106.60 and 106.00 support levels.

US Retail Sales Headline Monday Session

Heading into the new trading week, investors across different asset classes feared that the U.S.-led strike on Syria would become the new catalyst to sell risk assets. However, Saturday's operation, that also included the U.K. and France was a limited one, and intended to be a one-off as President Trump declared ‘mission accomplished'. Many feared the attack would probably lead to a broader confrontation, but the conducted strike was not strong enough to bring Russian retaliation. The limited reaction in currency markets on Monday shows investors are relieved somehow, and expect no significant escalation.

The fall in oil prices is another sign of relief, after the geopolitical tensions last week drove Brent to its highest levels since 2014. Another source of pressure came from U.S. energy companies; seven oil rigs were added in the week to 13 April, bringing the total count to 815, a level last seen in March 2015. Despite the 1% fall in early trading, I think there's still a lot of risk premium in current prices, and with further ease in geopolitical tensions, I expect to see an additional drop below $70.

It's going to be a busy week ahead for financial markets, specifically on the earning front, with about 60 S&P 500 companies due to report results. So far, 70% of companies that already reported actual results managed to beat Wall Street expectations on EPS. If the positive surprise didn't diverge from current levels, there's a high likelihood of companies reporting 20% growth in earnings. Tax cuts are the undoubtedly the key factor behind the expected earnings growth. Additional factors were also in play, including the dollar's weakness which boosted multinational overseas earnings, and the rise in the price of oil, which is expected to boost earnings growth in the energy sector by 79%, according to FactSet.

With such a positive earning season and with better valuations compared to a year ago, there's a good reason for the bulls to take over control. However, this also depends on how much noise we'll have in the background,whether it is Russia-U.S. relations, Middle East geopolitics, trade tensions or higher inflation expectations; the list goes on.

There's also a lot of data releases this week to attract traders' attention. In the U.S., the economic calendar focuses on housing and manufacturing sectors, but retail sales figures released later today are likely to move the dollar the most. Chinese first quarter GDP results will be released on Tuesday and markets expect a 6.7% growth The global financial markets have a lot to ponder on Monday: Syrian airstrikes, corporate earnings and a few high-profile data releases from the world's largest economy.

After a quiet European session, trading in North America opens with the New York Empire State Manufacturing Index. The monthly release, which is scheduled for 12:30 GMT, gauges business conditions in one of America's most populous states. The April edition of the index is expected to show weakness to 20.1 from 22.5 in March. Nevertheless, a positive figure is normally considered bullish.

The Commerce Department will also report on retail sales at 12:30 GMT. The monthly report is widely considered to be one of the best gauges of consumer spending, which accounts for more than two-thirds of US economic output. Receipts at retail stores are forecast to rise 0.3% in March after falling 0.1% the month before. Excluding automobiles, the retail sales category likely rose 0.3%.

Sales are down in each of the last three months, capping off the worst stretch in over five years. Some analysts have expressed concerns over the health of the US economy as a result.

Commerce economists will also report on business inventories at 14:00 GMT. The monthly data set, which has direct implications on gross domestic product (GDP), is expected to show an increase of 0.5% for February.

The National Association of Home Builders (NAHB) will deliver its latest housing market index at 14:00 GMT. The gauge of homebuilder confidence is projected to hold at 70 for April.

In terms of monetary policy, Federal Open Market Committee (FOMC) member Raphael Bostic will deliver a speech at 17:15 GMT. Bostic was a member of the policy-setting committee that voted to raise interest rates last month. At least two more upward adjustments are expected this year.

EUR/USD

EUR/USD edged slightly higher on Monday, as the pair continued to recover from last Thursday's swing low near 1.2300. The pair was last seen trading at 1.2336, having gained 0.1% from the previous close. EUR/USD faces interim support at 1.2290 and resistance up at 1.2370.

GBP/USD

Cable's bullish upside faded on Friday, as the British pound fell from highs near 1.4300 US. However, the currency remains in a firm uptrend now that Brexit talks are mobilizing. GBP/USD was last seen trading at 1.4248. It faces immediate resistance at the 1.4300 psychological hurdle.

USD/JPY

The Japanese yen has been caught in a firm downtrend stretching back three weeks even as the dollar struggled to make gains against other currencies. USD/JPY rose 0.1% on Monday to 107.42. The pair is testing the 13 April high of 107.70. Immediate support is likely found at the 11 April swing low of 106.78.

YoY. Trade tensions will be an important factor to focus on over the coming quarters, but so far China continues to grow at healthy levels. Any upside surprise in China's GDP could potentially send the Aussie higher.

Investors Unmoved By Syria Attack

Heading into the new trading week, investors across different asset classes feared that the U.S.-led strike on Syria would become the new catalyst to sell risk assets. However, Saturday's operation, that also included the U.K. and France was a limited one, and intended to be a one-off as President Trump declared ‘mission accomplished'. Many feared the attack would probably lead to a broader confrontation, but the conducted strike was not strong enough to bring Russian retaliation. The limited reaction in currency markets on Monday shows investors are relieved somehow, and expect no significant escalation.

The fall in oil prices is another sign of relief, after the geopolitical tensions last week drove Brent to its highest levels since 2014. Another source of pressure came from U.S. energy companies; seven oil rigs were added in the week to 13 April, bringing the total count to 815, a level last seen in March 2015. Despite the 1% fall in early trading, I think there's still a lot of risk premium in current prices, and with further ease in geopolitical tensions, I expect to see an additional drop below $70.

It's going to be a busy week ahead for financial markets, specifically on the earning front, with about 60 S&P 500 companies due to report results. So far, 70% of companies that already reported actual results managed to beat Wall Street expectations on EPS. If the positive surprise didn't diverge from current levels, there's a high likelihood of companies reporting 20% growth in earnings. Tax cuts are the undoubtedly the key factor behind the expected earnings growth. Additional factors were also in play, including the dollar's weakness which boosted multinational overseas earnings, and the rise in the price of oil, which is expected to boost earnings growth in the energy sector by 79%, according to FactSet.

With such a positive earning season and with better valuations compared to a year ago, there's a good reason for the bulls to take over control. However, this also depends on how much noise we'll have in the background,whether it is Russia-U.S. relations, Middle East geopolitics, trade tensions or higher inflation expectations; the list goes on.

There's also a lot of data releases this week to attract traders' attention. In the U.S., the economic calendar focuses on housing and manufacturing sectors, but retail sales figures released later today are likely to move the dollar the most. Chinese first quarter GDP results will be released on Tuesday and markets expect a 6.7% growth YoY. Trade tensions will be an important factor to focus on over the coming quarters, but so far China continues to grow at healthy levels. Any upside surprise in China's GDP could potentially send the Aussie higher.

Currencies: (Geo)Political Tensions Still Prevent Further USD Gains

- Rates: Better to err on the safe side for now

Risk barometers suggest a neutral start to today's trading session, but we think that geopolitical tensions still warrant to err on the safe side. We have a positive intraday bias for core bonds today. Apart from risk sentiment, US eco data including retail sales might disappoint. - Currencies: (Geo)political tensions still prevent further USD gains

Dollar dollar improved temporary at the end of last week. However, a coalition taking action against Syria apparently isn't able to reduce the global level of geopolitical uncertainty. This is slightly weighing on the dollar. There is also no guarantee that US eco data will be strong enough to support further USD gains.

The Sunrise Headlines

- US stock markets corrected 0.5% lower on Friday with geopolitical uncertainty looming over the weekend. Financials underperformed as first Q1 earnings couldn't convince. Asian trading is mixed with China underperforming (-1.5%).

- Russian President Putin warned that further Western attacks on Syria would bring chaos to world affairs, as Washington prepared to increase pressure on Russia with new economic sanctions (Reuters).

- The FT reports that the UK House of Lords is expected to vote for Britain to remain in an EU customs union this week, inflicting a damaging defeat on the government.

- President Trump's top economic advisor Kudlow said he is optimistic the US can avoid a broader trade fight with China and that the Trump administration is “making progress” on Nafta renegotiation, the WSJ reports, citing an interview.

- China, Japan, Germany, Korea, Switzerland and new addition, India, will be subject to US monitoring despite findings that they did not manipulate FX rates in the US Report on International Economic and Exchange Rate Policies.

- Moody's raised the Spanish Baa2 rating to Baa1 (stable). Enhanced economic resiliency and improved banking sector fundamentals outweigh the drag from political/institutional factors, according to the rating agency.

- Today's eco calendar contains US retail sales and Empire Manufacturing. Fed Kaplan, Kashkari and Bostic speak. Bank of America and Netflix report earnings

Currencies: (Geo)Political Tensions Still Prevent Further USD Gains

(Geo)political uncertainty still prevents USD gains

On Friday, the dollar initially held a slightly positive bias against the yen as geopolitical tensions eased slightly. The US/German interest rate differential reached a new cycle peak, but had only a limited impact on EUR/USD. The dollar (and US equities) reversed earlier gains towards the end of the session. Investors took a cautious approach going into the weekend awaiting the consequences of potential action against Syria during the weekend. EUR/USD finished the week at 1.2331. USD/JPY closed at 107.35. Both cross rates were little changed on a daily basis.

A coalition of the US, France and the UK indeed executed selective strikes on targets in Syria this weekend. This morning, there were tentative signs that the action removed some of political uncertainty. However, Asian equities failed to sustain opening gains (if any) with China underperforming. USD/JPY slipped from the 107.60 area to the 107.20 area. EUR/USD trades little changed in the 1.2330 area. The Hong Kong dollar is holding near the weak band against the US currency even as the monetary authority is said to execute further

Today, the US retail sales are interesting, but geopolitics will also remain in play. US retail sales are expected to rebound (0.4% M/M) after three months of a rather poor sales. A really positive surprise is probably needed to support the US dollar. There is no guarantee for that. This morning's equity performance is also a bit disappointing given that Syria might become less important for markets after this weekend's action. Markets apparently aren't convinced that the geopolitical noise is out of the way. Ongoing uncertainty could also keep some USD caution in place. End last week, sentiment on the dollar improved slightly. For now, there is little reason to expect the dollar to start a real up leg. Fed speakers remain a wildcard. EUR/USD perfectly holding in the middle of the 1.2155/1.2550 consolidation pattern.

End last week, sterling showed 'remarkable' strength. Technical factors played a role. The data mostly weren't sterling supportive. Of late, several political analysises suggested that a bigger role for Parliament could support the case for a soft Brexit or even open the way for a new referendum. For now, we see too little political backing in the UK government for that scenario. The test of the EUR/GBP 0.8652 support is ongoing. The day-to-day momentum is sterling positive, but we see too little substance for a sustained acceleration of the sterling rebound. This week, the data UK data will get more attention

USD (trade-weighted): still going nowhere

HKMA bought HKD 3.59b in fifth intervention move

The Hong Kong Monetary Authority (HKMA) intervenes in the markets again today to defend the peg to US Dollar. HKD 3.59b (USD 457m) was bought by HKMA (at around 3pm HKT) as the currency remains persistently weak and continues to press its trading band.

This is the fifth action intervention in recent period and the first time that happens during HK stock trading house. Accumulatively, HKMA bought HKD 13.55b in total.

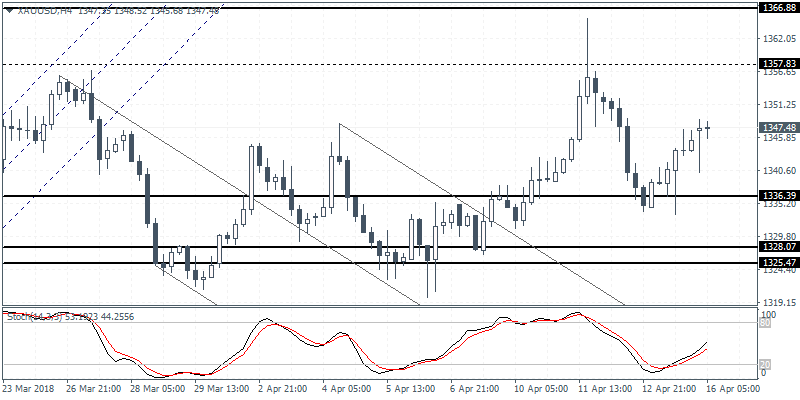

XAUUSD Intraday Analysis

XAUUSD (1347.48): Gold prices managed to rebound from 1336 level after the precious metal gave up the gains initially from 1357 level. The sideways range could be maintained within these levels in the near term with the likelihood that gold prices could once again test the support at 1336 level to establish firm support. In the near term, we expect gold prices to move sideways with a breakout from the established support and resistance level likely to provide the next leg in the direction of the trend