Sample Category Title

AUD/USD Sharp Short-Term Increase

AUD/USD short-term momentum is increasing again, approaching hourly resistance at 0.7810 (28/12/2018 high) and heading along the 0.7805 range. Hourly support at 0.7638 (15/12/2017 low) is distanced. The technical structure suggests short-term upward moves.

In the long-term, the upward trend slows down after failing to reach key resistance at 0.8164 (14/05/2015 low). Key support stands at 0.6009 (31/10/2008 low). A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Moving Sideways

USD/CAD pick up some marginal demand within short term range. Hourly support and resistance are now given at 1.2504 (06/02/2018 low) and 1.2755 (22/02/2018 high). The shortterm technical structure suggests short-term decrease.

In the longer term, the pair is trading between resistance point at 1.3805 (05/05/2017 high) and support at 1.2128 (18/06/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head lower. The pair is trading below its 200 DMA

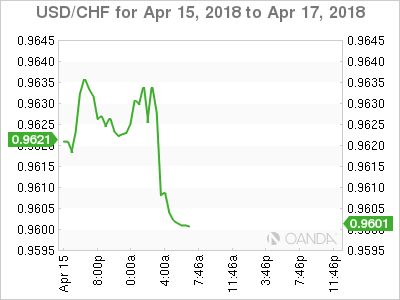

USD/CHF Bullish Bounce

USD/CHF has recovered momentum targeting 0.9668 resistance. The bullish pattern started from 0.9188 (16/02/2018 low) continues. The pair is contained between hourly support and resistance given at 0.9296 (05/02/2018 low) and 0.9668 (17/01/2018 high). The technical structure suggests short-term downward moves.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support lies at 0.9072 (07/05/2015 low) while resistance at 1.0344 (15/12/2016 high) is distanced. The technical structure favours a long term bullish bias since the unpeg in January 2015.

USD/JPY Rising On Trendline

USD/JPY keeps on pushing higher. The bearish pattern started in January 2018 is somewhat weakening. Hourly support and resistance are given at 107.00 (rising trendline) and 107.90 (14/02/2018 high). The short-term technical structure suggests continued short-term upward moves.

We favor a long-term bearish bias. Support remains at 101.20 (09/11/2016 low). A gradual rise toward the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 101.20 (09/11/2016 low). The pair trades below its 200 DMA

GBP/USD Bullish Momentum Is Strong

GBP/USD's short-term momentum is still lively. Hourly support and resistance are now given at 1.3451 (23/02/2018 low) and 1.4345 (25/01/2018 high). The technical structure suggests shortterm upward moves.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

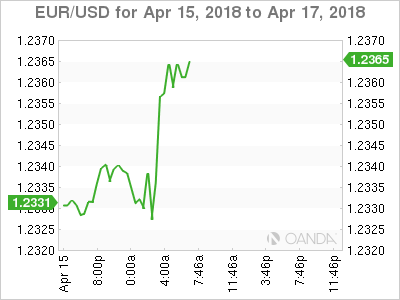

EUR/USD Consolidation

EUR/USD is now pausing between 1.2300 and .2345 range. The pair is currently maintained between hourly support and resistance given at 1.2165 (17/01/2018 low) and 1.2506 (25/01/2018 high). The technical structure suggests shortterm increase.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

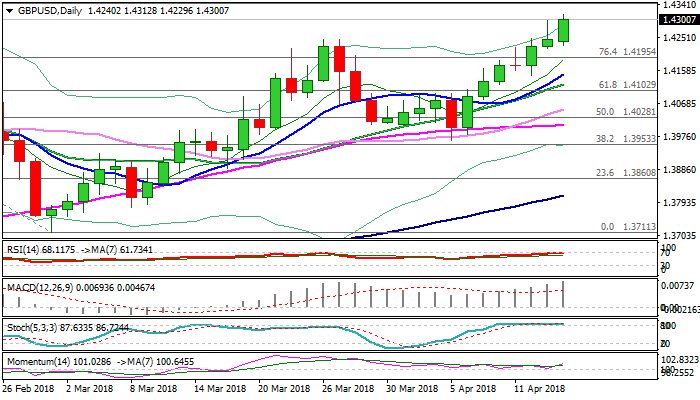

GBPUSD: Cable Probes Above 1.43 For The First Time Since Jan 25

Cable broke above 1.4300 barrier for the first time since 25 Jan, in fresh bullish acceleration on Monday, which offset initial signal of stall from Friday’s Shooting star.

Sterling extends bull-leg off 1.3965 (05 Apr trough) and is on track to fully retrace 1.4344/1.3711 corrective phase, as fresh bulls pressure key barrier at 1.4344 (post-Brexit recovery peak).

Expectations of BoE rate hike next month keep the pound supported, with eventual break through 1.4344 pivot needed to signal continuation of recovery phase from 1.1930 (07 Oct 2016 post flash-crash low).

Extension above 1.4344 pivot would face another strong barrier at 1.4401 (Fibo 61.8% of 1.5928/1.1930 descend), break of which would generate another strong bullish signal.

Caution of hesitation on approach to 1.4344 barrier as slow stochastic is overbought on daily chart, which could result in extended but limited consolidation before bulls continue.

Former tops of 26/27 Mar at 1.4244 and today/Friday’s lows at 1.4230/20, mark solid support zone which should ideally keep the downside protected.

Res: 1.4314, 1.4344, 1.4401, 1.4450

Sup: 1.4244, 1.4220, 1.4190, 1.4147

Dollar Downside Risks Remain After Syria Airstrikes

Monday April 16: Five things the markets are talking about

Dealers and investors seem comfortable to start this week in a risk-taking mood as short-term geopolitical uncertainties continue to scale back for the time being.

Note: Missile strikes late Friday (April 13) by joint coalition forces – U.S, U.K and France – on Syria, have not lead to a major escalation.

Overnight, global sovereign bonds prices have declined, equities are steady and oil is a tad weaker on anticipation that the fallout in Syria will be limited.

The market is now refocusing its effort on a number of economic data and corporate earnings coming out this week.

Today in the U.S, investors will be looking at the latest retail sales data (08:30 am EDT), which is an important gauge of the health of the domestic economy.

On Tuesday, U.S housing starts and building permits (08:30 am EDT) are also expected to be upbeat, while industrial production (09:15 am EDT) is expected to be soft.

On Wednesday, general inflation signals will be a focus of the Fed’s Beige Book (02:00 pm EDT).

On Thursday (08:30 am EDT), weekly jobless claims will be the focus – is the demand in the U.S labor market easing?

Also on tap this week are more earnings out of the U.S. and speeches by Federal Reserve officials.

Elsewhere, in Canada, the Bank of Canada (BoC) is expected to leave overnight rates unchanged (+1.25%) on Wednesday (April 18) due to a combination of soft economic data and NAFTA uncertainties. The BoC will also publish its quarterly Monetary Policy Report (MPC).

On Friday (April 20), Canada will release consumer prices for March.

Later today, China will release Q1 GDP data along with March industrial output and retail sales (10:00 pm EDT).

On Tuesday, the U.K releases its important labor market report for March along with consumer and producer prices (April 18) and retail sales (April 19).

1. Stocks mixed after Syria air strikes

In Asian overnight, stocks early gains were eroded, led by declines in Hong Kong and China over worries about the HKD.

In Japan, equities rallied modestly on relief that a U.S led missile strike on Syria appeared to be a one-off event. Nevertheless, ongoing concerns about a trade war had investors seeking defensive shares. The Nikkei rose +0.26%, while the broader Topix gained +0.40%.

Down-under, Aussie shares pared earlier gains to finish higher overnight, with strength in commodities countered by a fall in financials. The S&P/ASX 200 index rose +0.2%. In Korea, the Kospi closed +0.1% higher.

In Hong Kong, shares dropped amid worries that slowing credit growth and tightening regulatory requirements in China will hurt economic growth. The Hang Seng index fell -1.6%, while the China Enterprises Index lost -2.1%.

In China, indexes fell and posted their worst day in three-weeks, on slowing credit growth. The blue-chip CSI300 index ended down -1.6%, while the Shanghai Composite Index slid -1.5%.

Note: The People’s Bank of China (PBoC) raised the Open Market Operation (OMO) interest rate on the 14-day reverse repo by +5bps to +2.70%.

In Europe, regional indices trade little changed in a lackluster session ahead of corporate earnings.

U.S stocks are set to open in the black (+0.4%).

Indices: Stoxx600 -0.1% at 378.7, FTSE -0.3% at 7244, DAX +0.1% at 12449, CAC-40 +0.1% at 5311, IBEX-35 +0.1% at 9775, FTSE MIB +0.1% at 23358, SMI -0.2% at 8757, S&P 500 Futures +0.4%

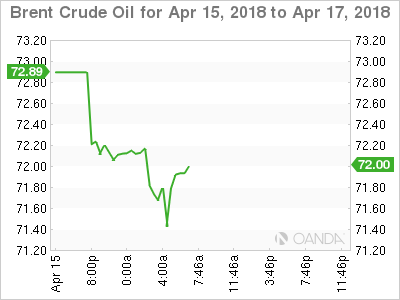

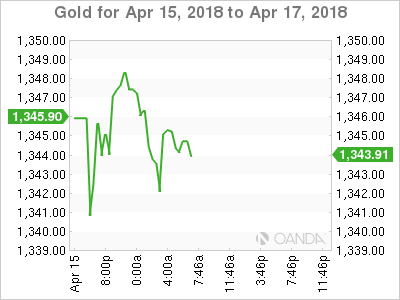

2. Oil prices drop as fears about Syria strikes fallout wane, gold lower

Oil prices are under pressure ahead of the U.S open after data showed that U.S drilling activity rose and fears waned about escalating tensions in the Middle East.

Brent crude oil futures have slipped -$1.34 to +$71.24 a barrel, while U.S crude futures are down -$1.16 at +$66.23 a barrel.

Baker Hughes data on Friday showed that U.S drilling companies added seven rigs in the week to April 13, bringing the total to 815, the highest in three years.

Note: Despite this, Brent is still up more than +16% since February’s 2018 low.

Ahead of the U.S open, gold prices are little changed as overnight markets assess the possible consequences of a U.S.-led missile strike against Syria over the weekend. Spot gold is down -0.1% at +$1,344.03 an ounce.

3. Yields back up

Sovereign bond prices have edge lower, lifting yields overnight, as the market shrugs off coordinated missile attacks in Syria.

Also supporting higher U.S yields is the FOMC minutes last week showing officials leaning towards a slightly faster pace of tightening at their March meeting as their growth outlook and confidence in hitting inflation targets strengthened.

Yields on both German and U.S 10-year government bonds are both at their highest level in four-weeks.

The yield on U.S 10’s has climbed +3 bps to +2.85%. In Germany, the 10-year Bund yield has advanced +3 bps to +0.55%, while in the U.K the 10-year Gilt yield has advanced +2 bps to +1.455%.

4. Dollar downside risks remain

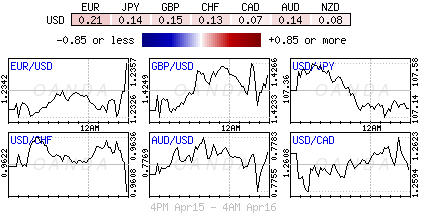

Despite geopolitical and Middle East risks the FX market remains somewhat subdued overnight.

Nevertheless, with the U.S pushing its twin deficits up while also increasing interest rates, dollar bears continue to look for selling opportunities.

The U.S Treasury’s bi-annual report on FX policies of G20 trading partners delivered a relatively “measured” tone and did not name any country as a currency manipulator. Even the weekend military strikes on Syria saw limited price action.

EUR/USD (€1.2364) remains contained within recent ranges ahead of the U.S open.

GBP/USD (1.4303) trades atop of the euro session high and has penetrated the strong psychological resistance level of £1.4300. Expect investors to focus on the E.U/U.K meeting to discuss post-Brexit trading relationship during the week.

USD/JPY (¥107.08) is holding above the key ¥107 level. Techies are looking for the yen to remain susceptible to further weakness ahead of next week’s BoJ meeting and PM Abe’s falling approval numbers.

5. Swiss inflationary pressures under control

Data this morning show that inflationary pressures remain well contained in Switzerland.

The combined producer and import price index fell -0.2% in March versus February. On an annual basis, the index was up +2%.

Digging deeper, annual consumer price inflation (CPI) is running at +0.8%, which would suggest that the Swiss National Bank (SNB) should be in any hurry to tighten interest rates in the coming months.

Minneapolis Fed Kashkari: Fed might be one hike away from achieving neutral

Minneapolis Fed President Neel Kashkari is seen clearly as a dove as he voted against al three of Fed's rate hikes last year.

He said in a WSJ interview published today that fiscal stimulus of the federal government, including tax cuts would make Fed meeting its 2% inflation target more likely. The tax cuts and spending increases are "macroeconomically significant, and they are big enough to have an effect on the trajectory of the economy... that could change things in a meaningful way." And with that development, Fed can move ahead with the planned tightening.

But he also argued that "it isn't going to be obvious to me once we achieve our inflation target that we need to now put the brakes on the economy." He reiterated his stance that " once we achieve our inflation target, we should try to get to neutral in a reasonable period of time,"

And he added that "we might be one hike away from achieving neutral."

US Futures Higher Despite Weekend Air Strikes

- Investors At Ease After Western Strikes in Syria;

- US Dollar Softer as Yields Rise;

- Retail Sales and Manufacturing Survey Eyed.

Stock markets have got off to a relatively positive start on Monday, despite the US, UK and France carrying out targeted strikesu in Syria over the weekend in response to the chemical weapons attack a couple of weeks ago.

'For now, investors appear at ease with the situation and as long as no further escalation occurs, attention may now switch to other matters such as first quarter earnings season'

It was feared that a Western response could trigger an escalation in the region, further damaging relations with Russia in the process due to its backing of the Assad regime. Instead, an apparent one-off limited strike by the three countries on chemical weapons sites in an attempt to prevent further attacks in the future has not yet stoked such fears and instead, investors appear relatively at ease.

Of course, we'll find out in the coming days just what the response to the strikes will be, assuming there will be any. For now, investors appear at ease with the situation and as long as no further escalation occurs, attention may now switch to other matters such as first quarter earnings season which got underway late last week.

'traders potentially seeing easing trade tensions and no significant escalation in Syria as being hawkish for interest rates'

We have continued to see a weakening of the US dollar at the start of the week which has coincided with higher US yields, with traders potentially seeing easing trade tensions and no significant escalation in Syria as being hawkish for interest rates. Naturally, anything that is seen as being a risk for the US economy weighs on yields so the events of the last few weeks has seen them drop from close to 3% to just above 2.7% but this is gradually improving.

This may also be being aided by Eric Rosengren's comments on Friday when he claimed he back at least three more rate hikes this year, which is above the current consensus. Rosengren may not be a voting member this year but he is typically among the moderate hawks on the committee so it could be a view that is becoming increasingly shared, as long as some of the greater risks don't materialise.

'Retail sales have taken a dip at the start of the year but the trend remains solid'

While earnings and geopolitics may be of most interest to traders this week, there are a number of data points that will attract attention. Monday can often be among the quieter days but this week we've got retail sales and empire state manufacturing figures which will be of interest. Retail sales have taken a dip at the start of the year but the trend remains solid and you would expect tax reforms to be supportive for spending over the course of the year.