Sample Category Title

Pound In Bullish Mode Despite Syria Strikes, US Retail Sales Pending

Here are the latest developments in global markets:

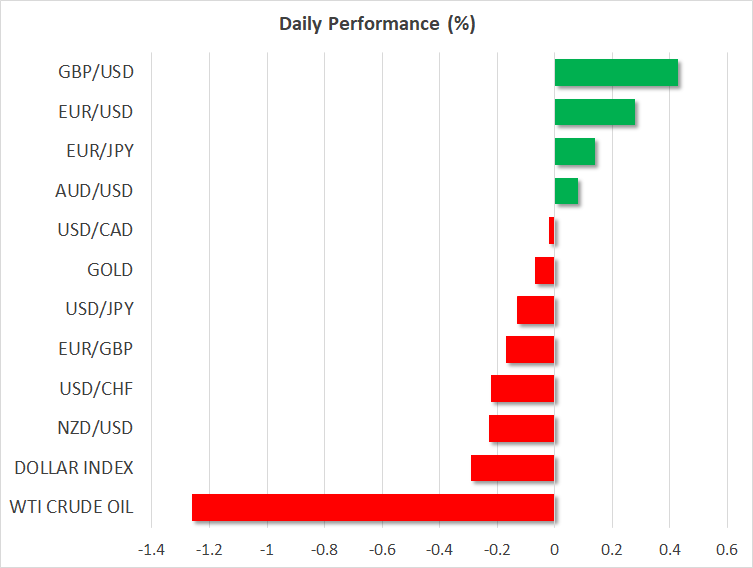

FOREX: The dollar was struggling to gain ground during the early European afternoon against the Japanese yen (-0.11%) ahead of the US retail sales released later in the day. The yen was making a comeback during today’s European session as geopolitical risks were hanging in the background following Saturday’s military attack in Syria conducted by the US, France, and Britain, though the negative market reaction has been muted so far. It is worth mentioning that Japan and China agreed to improve ties after the first high-level meeting in eight years, a few days before the US and Japanese leaders meet to discuss on trade and North Korea. The dollar index, which gauges the greenback’s strength versus six major currencies, slipped below the 20- and 40-day SMAs, losing 0.28% on the day. Euro/dollar was trading higher by 0.30% after a flat Friday as German bonds yields reached three-week highs today and Spain got an upgrade in ratings from Moody’s. Pound/dollar remained resilient, rising by 0.48% despite Britain’s military intervention in Syria. Six days have now passed without a pullback in Cable, with prices reaching a fresh 2 ½-month high today. The Canadian dollar will be in focus this week as the Bank of Canada will meet to decide on interest rates on Wednesday. No changes in policy are expected but there could be a hint of optimism. After the strong sell-off in the preceding week, dollar/loonie was trading slightly higher by 0.04% at 1.2600. The antipodean currencies were mixed, with aussie/dollar up at 0.7772 (+0.08%) and kiwi/dollar down at 0.7343 (-0.19%).

STOCKS: European stocks were mixed at 0932 GMT. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were trading near their opening levels, down by 0.06% and up by 0.08% respectively. The German DAX 30 rose by 0.19%, the French CAC 40 was slightly up by 0.01%, while the Italian FTSE MIB was unchanged. The UK’s FTSE 100 slipped by 0.33%. Asian markets ended mixed as selling in bank shares slugged Chinese indexes, while futures tracking the US indices were pointing to a positive open.

COMMODITIES: In energy markets, oil fell aggressively on Monday as the market wagered the latest US-led strike on Syria would not escalate into a wider conflict. WTI crude oil plunged by 1.25% after it hit a fresh 3-year high of $67.73 on Friday. Brent crude oil plummeted by 1.25% as well following five winning daily sessions. In precious metals, gold prices were little changed, falling by 0.06% to $1,344.10 an ounce.

Day ahead: US data to come to light but geopolitical developments could dominate headlines

Monday’s economic calendar will feature US data later in the day, but any potential headlines linked to Saturday’s military strikes in Syria will probably steal the attention, bringing further volatility to the greenback.

Early on Saturday, the US, France, and Britain launched 105 missiles on chemical weapon facilities in Syria aimed to punish the Syrian government for the chemical attack in the town of Douma on April 7. The action escalated war fears in the region, but the market reaction was limited on Monday as Russia and Iran, which are accused of backing Syrian government, have so far avoided responding in the same manner despite both heavily criticizing the attack. Besides that, the story took an economic turn as well, with the US warning to impose new sanctions on Russia. The ball is now in Russia’s hands and investors are eagerly waiting to see how Putin will retaliate after the Russian ambassador to Washington said that “such actions will not be left without consequences”. If the US-Russia conflict exaggerates, the dollar could face additional pressure, probably sliding below the 107 key-level. However, if Russia decides not to fight back, the dollar could pare some losses.

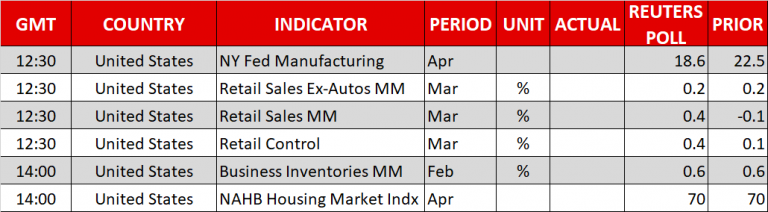

Regarding today’s data releases, retail sales (1230 GMT), the New York Fed manufacturing index (1230 GMT), business inventories (1400 GMT), and the NAHB housing market index (1400 GMT) will be closely watched in the US. Particularly analysts believe that in March, retail sales have increased by 0.4% on a monthly basis after recording declines in the past two months. Excluding vehicles, though, the measure is expected to rise at February’s pace of 0.2% m/m. February’s business inventories and April’s NAHB housing index are also anticipated to remain unchanged, while April’s NY Fed manufacturing index could show some weakness.

At the same time, Fed speakers will also be in the spotlight. At 1400 GMT, Dallas Fed President, Robert Kaplan, and Minneapolis Fed President, Neel Kashkari – neither of who hold voting rights within the FOMC in 2018 – will be delivering speeches, while a few hours later at 1715 GMT, Atlanta Fed Governor, Raphael Bostic, a voting member within the FOMC, will be making comments.

In equity markets, earnings season continues, with Bank of America and Netflix being among the companies to report quarterly results.

Early on Tuesday at 0300 GMT, Chinese growth, retail sales, and industrial readings will take the center stage amid trade uncertainties following the US-China recent import tariff game which could add fuel to what markets fear of a global trade war if the countries decide to implement their punitive measures. Note that the US has threatened to impose additional tariffs on Chinese imports besides the ones on aluminum and steel which are already in effect, finding resistance from China who warned to target 128 US products as well. According to forecasts, Chinese GDP growth has slowed down slightly to 6.7% y/y in the first quarter of the year, but it is too early to blame the US trade policy for this softness. Separately, Chinese industrial production for the month of March could have eased as well on yearly terms, whereas retail sales are said to have improved in the same period. Should the numbers disappoint, the Chinese yuan could move to the downside, while the antipodean currencies such as the aussie and the kiwi could increase negative momentum as Australia and China hold tight trade relations with China.

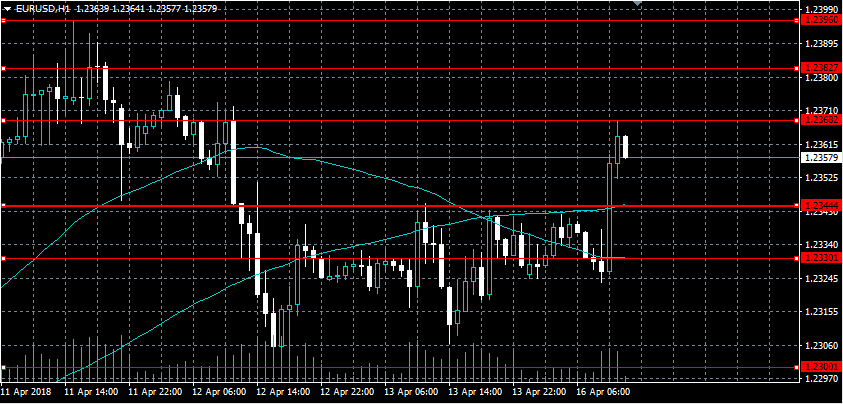

EURUSD Weekly Bullish Above 1.2344 Level

The euro continues to press higher against the U.S dollar in early week trading after sellers failed to move price-action below the key 1.2300 support level. The EURUSD has so far found intraday resistance from the 1.2368 level, with buyers needing a higher-time frame close above the 1.2382 level needed to cement the pairs medium-term bullish bias. Traders now look towards the release of U.S Retail Sales data, and a host of Federal Reserve members delivering scheduled speeches.

The EURUSD pair is weekly bullish while trading above the 1.2344 level, resistance is currently set at the 1.2382 and 1.2396 levels.

Should the EURUSD pair move below 1.2344 level, key intraday technical support is found at the 1.2333 and 1.2300 levels.

GBPUSD Buyers Target Above 1.4344 Level

The British pound has broken to a new monthly trading high against the U.S dollar, hitting 1.4303, during the European trading session. The GBPUSD pair has moved higher on intraday U.S dollar weakness, and increased optimism that the Bank of England will soon raise UK interest rates. Should price-action close above the 1.4300 level on a higher time-frame basis, sterling buyers will likely attempt a technical price-test of the January price-high, at 1.4344.

The GBPUSD pair retains a bullish bias while trading above the 1.4255 level, key resistance is found at the 1.4344 and 1.4390 levels.

If the GBPUSD pair fails to hold price above the 1.4300 level, sellers will likely test towards the 1.4255 and 1.4230 support levels.

US-Led Syria Missile Attack Seen As A ‘One-Off Event’

Notes/Observations

- Limited spillover from military strikes on Syria; but hard for trading sentiment to look beyond geopolitics and trade war developments.

- Focus on US Retail sales; analysts expect a rebound in March data

- China Q1 GDP data due for release on Tuesday

Asia:

- Japan PM Abe said to plans to propose new framework for trade talks in hopes of persuading Trump to rejoin TPP

- Japan companies raised wages by avg 2.41% in 2018 (largest increase in 20-yrs)

- China PBoC raised the Open Market Operation (OMO) Interest Rate on the 14-Day Reverse Repo by 5bps to 2.70%

- Hong Kong money market rates rise after HKMA acted last week to defend currency peg

- Hong Kong Fin Sec Chan: Weakness in the HK$ was not too much of a concern, as the govt had prepared early and had enough money to deal with the capital outflow; HKMA had intervened in the FX market four times as of Sunday

Europe:

- BoE said to have warned lenders back in Dec that the withdrawal of its £127B low interest rate funding scheme poses systemic risks to the UK financial system. The term funding scheme (TFS) that was launched after the UK’s Brexit vote. The warning from the BoE came before the scheme ended in Feb 2018

- UK PM May to make Brexit appeal that will see her call on the Commonwealth (the former UK colonies) to boost trade and forge new relationships

- UK Q1 Visa Spending y/y: -1.4% v -1.3% prior (largest fall since Q4 2012)

- SNB's Jordan reiterated view that now was not the right time to change Swiss monetary policy as FX market environment remained fragile. Noted that changes in monetary policy in other countries could give the SNB more room to maneuver

- Russia President Putin said to have warned of 'chaos' in international order if Syria was attacked again

- Moody' raised Spain sovereign rating by 1 notch to Baa1 from Baa2; outlook Stable

- Fitch affirmed Luxembourg sovereign rating at AAA; outlook Stable

- S&P affirmed Poland sovereign rating at BBB+; outlook revised to Positive from Stable

Americas:

- US, UK and France launched missile strikes against Syrian chemical weapons facilities; Pentagon says the strikes successfully hit every target; Trump tweets "Mission Accomplished!". 105 missiles were fired against 3 targets in Syria, including chlorine and sarin gas research facilities

- US Defense Sec Mattis: strikes are a “one time shot” to send a strong message to Assad

- US to implement new sanctions on Russia after Syria air strike that are aimed at companies dealing with equipment related to Syria

- UN Security Council: failed to adopted a Russian-drafted resolution that would have condemned Syrian strikes

- Treasury Semi-annual Currency Report again declined to name China as currency manipulator; added India to its 'watchlist'. Kept China, Japan, Germany, South Korea and Switzerland on watchlist

Economic Data:

- (DE) Germany Mar Wholesale Price Index M/M: 0.0% v -0.3% prior; Y/Y: 1.2% v 1.2% prior

- (DK) Denmark Mar PPI M/M: -0.4% v 0.0% prior; Y/Y: 1.7% v 1.1% prior

- (NO) Norway Mar Trade Balance (NOK): 15.0B v 21.3B prior

- (IN) India Mar Wholesale Prices (WPI) Y/Y: 2.5% v 2.4%e

- (TR) Turkey Feb Industrial Production M/M: -0.2% v +0.1%e; Y/Y: 9.9% v 10.4%e

- (TR) Turkey Jan Unemployment Rate: 10.8% v 10.4% prior

- (CH) Swiss Mar Producer & Import Prices M/M: -0.2% v +0.3% prior; Y/Y: 2.0% v 2.3% prior

- (TR) Turkey Mar Central Gov't Budget Balance (TRY): -20.2B v -1.9B prior

- (CH) SNB Total Sight Deposits for Week Ended Apr 13th (CHF): 575.1B v 574.9B prior

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.1% at 378.7, FTSE -0.3% at 7244, DAX +0.1% at 12449, CAC-40 +0.1% at 5311, IBEX-35 +0.1% at 9775, FTSE MIB +0.1% at 23358, SMI -0.2% at 8757, S&P 500 Futures +0.4%]

Market Focal Points/Key Themes:

- European Indices trade little changed in a lackluster session so far ahead of earnings which are set to ramp up the back end of this week. Shares of WPP trade lower after founder and CEO Sir Martin Sorrell resigned amid allegations of personal misconduct, having been with the company for 33 years. Elsewhere Software AG trades lower after missing estimates; Carr's group trades sharply higher after strong results; Whitbread outperforms after Elliot discloses >5% stake and calls for spinoff of Costa Coffee chain; Shire divested Oncology unit for $2.4B.

- Looking ahead notable earners include banking giant Bank of America and M&T Bank.

Movers

- Consumer Discretionary [ WPP [WPP.UK] -3.8% (CEO Sorrell steps down), Whitbread [WTB.UK] +6.2% (Elliot stake over 5%) ]

- Materials [ Vedanta [VED.UK] -3.3% (Names new CEO), Amerisur Resources [AMER.UK] +3.8% (Earnings)]

- Consumer Staples [Carr's Group [CARR.UK] +10.6% (Earnings)]

- Healthcare [Shire [SHP.UK] +1.9% (Divestment)]

- Technology [Software AG [SOW.DE] -4.1% (Prelim earnings), Rocket Internet [RKET.DE] +2.1% (Terminates share buyback)]

Speakers

- Sweden Government Spring Budget Proposal maintained 2018 GDP growth at 2.8% and 2019 GDP growth at 2.2%. It forecasted 2018 budget surplus at 1.0% of GDP

- Russia Dep Foreign Min Ryabkov stated that the govt would not delay in adopting further legislation in retaliation against US sanctions (**Note: Responds to reports that US to implement new sanctions on Russia after Syria air strike that are aimed at companies dealing with equipment related to Syria)

- EU said to consider widening sanctions against Iran

- Bank of Japan (BOJ) Deputy Gov Wakatabe: Doing what was needed to be done in order to achieve the 2% inflation target. Yield curve will steepen if central bank patiently maintains its current easing policy and help to heighten inflation expectations. Noted that the benefits outweighed the costs of its policy. Aware of the cumulative effect on bank profits from prolonged low rates and acknowledged that balance sheet loss was possible when interest rates are raised

- Japan Cabinet Office (Gov’t) Monthly Economic Report for Apr: Maintained its overall assessment that economy was recovering at a moderate pace

- Kuwait Oil Min Almarzooq: OPEC/Non-Opec production cuts to continue through end of 2018. Would consider extending cuts into 2019 when OPEC met at the June semi-annual meeting

Currencies

- FX markets were subdued in the session. Dealers noted that the US Treasury biannual report on FX policies of major trading partners delivered a relatively measured tone and did not name any country as a FX manipulator. Price action also saw limited spillover from weekend military strikes on Syria

- EUR/USD well contained within recent ranges and around 1.2360 just ahead of the NY morning.

- GBP/USD was firmer by 0.2% and trying to reach the 1.43 handle. Markets to focus on EU-UK meeting to discuss post-Brexit trading relationship during the week

- USD/JPY holding above the 107 level.

Fixed Income

- Bund Futures trade 40 ticks lower at 158.90 as Germany's 10-year bond yield surges to a 3-week high. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 121.75 lower by 38 ticks and near the session lows. Support continues stands at 121.25 then 120.85, with upside resistance at 123.35 then 123.85.

- Monday’s liquidity report showed Friday's excess liquidity rose to €1.869T from €1.855T prior. Use of the marginal lending facility increased from €136M to €561M.

- Corporate issuance saw $12.2B sold in the primary market last week

Looking Ahead

- (UK) EU-UK official meet to discuss post-Brexit trading relationship during the week

- (CO) Colombia Mar Consumer Confidence: -6.4e v -7.8 prior

- (BE) Belgium Debt Agency (BDA) announces upcoming OLO bond issuance for Thursday, Apr 19th

- 05:30 (NL) Netherlands Debt Agency (DSTA) to sell €2.0-4.0B in 3-month and 6-month bills

- 06:00 (IL) Israel Mar Consumer Confidence: No est v 128 prior

- 06:00 (IL) Israel Q4 Final GDP Annualized (3rd Reading): No est v 3.6% prelim

- 06:00 (IE) Ireland Feb Trade Balance: No est v €5.5B prior

- 06:00 (IL) Israel to sell Bonds

- 06:45 (US) Daily Libor Fixing

- 07:00 (RO) Romania to sell Bills

- 07:00 (RO) Romania to sell Bonds

- 07:00 (BR) Brazil Apr FGV Inflation IGP-10 M/M: 0.4%e v 0.5% prior

- 07:25 (BR) Brazil Central Bank Weekly Economists Survey

- 07:30 (BR) Brazil Feb Economic Activity Index (Monthly GDP) M/M: +0.1%e v -0.6% prior; Y/Y: 0.8%e v 3.0% prior

- 08:00 (PL) Poland Mar CPI Core M/M: 0.2%e v 0.0% prior; Y/Y: 0.8%e v 0.8% prior

- 08:00 (RO) Romania Apr Central Bank Minutes

- 08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming actions in week

- 08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Apr Empire Manufacturing: 19.6e v 22.5 prior

- 08:30 (US) Mar Advance Retail Sales M/M: +0.4%e v -0.1% prior; Retail Sales Ex Auto M/M: 0.2%e v 0.2% prior, Retail Sales (Ex Auto and Gas): 0.4%e v 0.3% prior; Retail Sales Control Group: 0.3%e v 0.1% prior

- 08:55 (FR) France Debt Agency(AFT) to sell combined €4.5-5.7B in 3-month, 6-month and 12-month bills

- 09:00 (IL) Israel Central Bank (BOI) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.10%

- 09:00 (BE) Belgium Feb Trade Balance: No est v -€0.2B prior

- 09:30 (EU) ECB announces Covered-Bond Purchases

- 09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

- 09:45 (UK) BOE to buy £1.22B in in APF Gilt purchase operation (3-7 years); Bid-to-cover: 3.07x prior

- 10:00 (US) Feb Business Inventories: 0.6%e v 0.6% prior

- 10:00 (US) Apr NAHB Housing Market Index: 70e v 70 prior

- 11:00 (CO) Colombia Feb Industrial Production Y/Y: 1.4%e v 1.0% prior

- 11:00 (CO) Colombia Feb Retail Sales Y/Y: 5.7%e v 6.2% prior

- 11:30 (US) Treasury to sell 3-Month and 6-Month Bills

- 13:15 (US) Fed's Bostic speaks on the Economy and Rural Market Trends

- 16:00 (US) Weekly Crop Progress Report

- 16:00 (US) Feb Total Net TIC Flows: No est v $119.7B prior; Net Long-term TIC Flows: No est v $62.1B prior

Bitcoin Recovery Bbounce Extends

Bitcoin sideways trading phase started in April is interrupted, heading along the 8175 range. Bitcoin bearish pattern started in March 2018 is however maintained as long as the 9000 range is not reached. The pair is contained between hourly support and resistance given at 6306 (13/11/2017 low) and 10232 (01/02/2018 high). The technical structure suggests further shortterm increase.

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 7'000 - 12'000 in 2018. Bitcoin is trading below its 200 DMA (7800 range)

Crude Oil Slight Pullback

Crude oil has weaken slightly after breaking 66.66 resistance. Crude Oil is trading at its December 2014 high. The bullish pattern started in November 2017 is confirmed. Hourly support at 63.20 (10/04/2018 low) is distanced. The technical structure suggests short-term increase.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading above its 200 DMA

Silver Wide Range

Silver is rising back following recent decline at 16.44, approaching the 16.60 range. Silver is contained between hourly support and resistance given at 16.03 (18/12/2017 low) and 16.98 (15/02/2018 high). The short-term technical structure suggests short-term upward moves.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. The pair is trading below its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).

Gold Choppy Trading

Gold is bouncing off from 1334 low, approaching the 1342 range. Hourly support and resistance are given at 1318 (14/02/2018 low) and 1366 (25/01/2018 high). The technical structure suggests short-term increase.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1'392 (17/03/2014) is required to confirm it. A major support can be found at 1'045 (05/02/2010 low).

EUR/CHF Consolidating Around 1.1889

EUR/CHF is holding below 1,1889 resistance. Strong resistance at 1.20 (level before the unpeg) remains. Hourly support given at 1.1715 (07/01/2018 low) remains. The short-term technical structure suggests short-term decrease.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's slowing QE program is likely to cause buying pressures on the euro, which should weigh in favour of the EUR/CHF. Support can be found at 1.0624 (24/06/2016 low).

EUR/GBP Weak Bounce

EUR/GBP is still weak after declining from 0.8723 high and heading along the 0.8628 range. EUR/GBP bearish pattern started in March is reinforced. Hourly support at 0.8652 (08/06/2017) is now broken while hourly resistance at 0.8834 (14/12/2017 high) is distanced. The technical structure suggests short-term decrease.

In the long-term, the pair has largely recovered from 2015 lows. The technical structure suggests further upside pressure. Strong resistance can be found at 0.9500 (psychological level) while support remains at 0.8304 (05/12/2016 low). The pair is trading below its 200 DMA