Sample Category Title

Sterling Firm as Markets Look into UK Unemployment Rate and Wage Growth, Aussie Lower after RBA Minutes

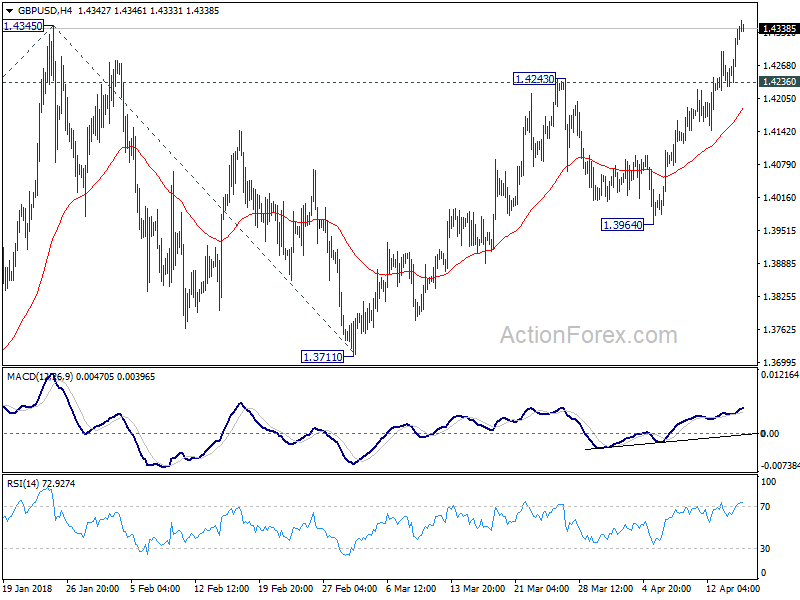

Sterling retreats mildly in Asian session today, against Dollar, Euro and Yen. But it remains the strongest one for the week. The breach of 1.4345 resistance in GBP/USD overnight signals medium term up trend resumption. But the rally slowed a little bit above there. For now, GBP/JPY is limited below last week's high at 133.83 while EUR/GBP is held by equivalent level at 0.8627. Traders are awaiting UK employment data today and CPI tomorrow, which would be important to determine BoE's rate path this year.

Elsewhere in the currency markets, Australian Dollar is trading broadly lower today after RBA minutes reiterated its patient stance on tightening. New Zealand and Canadian Dollar are also soft. Dollar was under some selling pressure yesterday but it's so far holding on to near term support levels. Most notably, EUR/USD is staying below 1.2396 and USD/CAD is holding above 1.2544. These two level, though, look vulnerable.

UK job data and wage growth to be watched closely

UK job data will be a key focus in the upcoming session. Unemployment rate is expected to be unchanged at 4.3% in February. And more importantly, average weekly earnings is expected to accelerate to 3.0% 3moy. Wage growth, together with tomorrow's CPI release, will be crucial to determine the rate path of BoE this year.

According to a Bloomberg survey just released today, three quarters of analyst now expect a May BoE hike, up from 54% last month. After that, the majority expected BoE to stand pat through the rest of 2018 until another hike in Feb 2019.

For now, with good progress seen in Brexit negotiations, the uncertainties are lying more on economic data. There are still a couple of possible scenarios. If data worsen, BoE might choose to hold fire until November. Or if inflation stays robust with acceleration in wage growth, BoE might add another hike in November, making it two this year.

RBA minutes: Growth to exceed potential, but still not strong case for near term hike

Minutes of April RBA meeting appeared to be rather balance. RBA sounded upbeat and said over 2018, GDP growth was expected to "exceed potential. CPI inflation was expected to "increase gradually" to a little above 2% target. Also, leading indicators continued to point to "above-average growth in employment" in the period ahead.

However, RBA also warned that "the possibility of an escalation in trade restrictions represented a risk to the global outlook that needed to be monitored closely". Additionally, "the high level of debt in China and the significant share of financial market activity in unregulated sectors continued to pose important risks to the outlook for the Chinese economy".

Regarding exchange range, RBA reiterated that "an appreciation of the Australian dollar would be expected to result in a slower pick-up in economic activity and inflation than forecast." On monetary policy, RBA also reiterated that the next move "would be up, rather than down". But still, "there was not a strong case for a near-term adjustment in monetary policy".

China GDP grew 6.8% in Q1, added USD 8.5B US debt holdings in Feb

Released from China, Q1 GDP grew 6.8% yoy, same as prior quarter and met expectation. Retail sales rose 10.1% yoy in March, up from prior 9.7% yoy and beat expectation of 9.7% yoy. Industrial production, however, rose 6.0% yoy, slowed from prior 7.2% yoy and missed expectation of 6.9% yoy. Fixed assets investment also slowed to 7.5% yoy, down from 7.9% yoy and missed expectation of 7.7% yoy. Overall, the set of data showed robust growth momentum.

Separately, US Treasury data showed showed that China remained the largest foreign creditor to the US, holding USD 1.18T in US bonds, bills and notes in February. Debt holding by China has indeed by USD 8.5B for the month, the largest rise in six months. But it should be noted that the data was for the period even before the 232 steel tariffs of the US, not to mention the Section 301 tariffs against China. The impact of trade tensions on Chinese interest in US debts remains to be seen. Meanwhile, Japan came as second largest foreign holder of US debts, dropped slightly from USD 1.07T to USD 1.06T.

Elsewhere

German ZEW economic sentiment will be another feature in European session. Canada will release international securities transactions later in the day. US will release housing starts and building permits, industrial production and capacity utilization.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4261; (P) 1.4302; (R1) 1.4379; More....

GBP/USD's rally continues to as high as 1.4353 so far and breach of 1.4345 indicates resumption of medium term up trend. Intraday bias stays on the upside for 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 next. On the downside, below 1.4236 minor support will turn intraday bias neutral again. But retreat should be contained well above 1.3964 support to bring another rally.

In the bigger picture, rise from 1.1946 (2016 low) is in progress and resuming. It is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. We'd continue to favor this medium term bullish view as long as 1.3711 support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | RBA April Meeting Minutes | ||||

| 2:00 | CNY | GDP Y/Y Q1 | 6.80% | 6.80% | 6.80% | |

| 2:00 | CNY | Retail Sales YTD Y/Y Mar | 10.10% | 9.70% | 9.70% | |

| 2:00 | CNY | Industrial Production YTD Y/Y Mar | 6.00% | 6.90% | 7.20% | |

| 2:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Mar | 7.50% | 7.70% | 7.90% | |

| 4:30 | JPY | Industrial Production M/M Feb F | 4.00% | 4.10% | ||

| 8:30 | GBP | Jobless Claims Change Mar | 9.2k | |||

| 8:30 | GBP | ILO Unemployment Rate 3Mths Feb | 4.30% | 4.30% | ||

| 8:30 | GBP | Average Weekly Earnings 3M/Y Feb | 3.00% | 2.80% | ||

| 9:00 | EUR | German ZEW Economic Sentiment Apr | 88 | 90.7 | ||

| 9:00 | EUR | German ZEW Expectations Apr | -1 | 5.1 | ||

| 9:00 | EUR | Eurozone ZEW Economic Sentiment Apr | 7.3 | 13.4 | ||

| 12:30 | CAD | International Securities Transactions (CAD) Feb | 5.68B | |||

| 12:30 | CAD | Manufacturing Sales M/M Feb | 1.00% | -1.00% | ||

| 12:30 | USD | Housing Starts Mar | 1.27M | 1.24M | ||

| 12:30 | USD | Building Permits Mar | 1.33M | 1.30M | ||

| 13:15 | USD | Industrial Production M/M Mar | 0.40% | 1.10% | ||

| 13:15 | USD | Capacity Utilization Mar | 77.90% | 78.10% |

Market Morning Briefing: Pound Is Again Testing Levels Near 1.43-1.435

STOCKS

Dow (24573.04, +0.87%) has broken above the immediate resistance near 24500 and if that sustains, a rise towards 25000-25200 or higher could be seen in the coming sessions. Near term likely to remain bullish while above 24500.

Dax (12391.41, -0.41%) again dipped a bit from immediate resistance at 12500. Unless the index breaks on the upside, we could again see some consolidation while the index comes off to re-test 12200 or lower.

Nikkei (21837.39, +0.0085%) has been stagnant near 21800 for the last 3-sessions. The fall to 20500 has been recovered on the weekly candle charts and while the recovery keeps the index above 21800, a rise in the coming weeks looks possible. A break below 21500 could then be treated as a false break which recovered within 2-weeks. Price action near current levels is crucial to keep an eye on.

Shanghai (3109.01, -0.051%) has not been able to sustain a rise from 3100 and is likely to test support near 3080/3070 on the 3-day candles. If the support holds, some more consolidation in the 3200-3080 is possible else a sharp break below 3080 could turn bearish for the near to medium term.

Nifty (10528.35, +0.46%) and Sensex (34305.43, +0.33%) have moved up sharply. Nifty faces resistance at 10550 while Sensex has scope of testing 34500-34750 levels in the near term. Crucial levels to watch for the Indian equity indices.

COMMODITIES

Brent (71.66) is down from 74 which is likely to hold for sometime, pushing Brent towards 70 again in the next few sessions. Nymex WTI (66.52) has also come off from resistance just below 68 and while that holds, a fall towards 65-64 levels look possible.

Although Gold (1349.30) has some resistance near 1370, overall the price has some chances of breaking above 1370 in April itself, taking an attempt to test levels of 1380-1400. Medium term looks bullish.

Copper (3.0985) is likely to re-test 3.15 on the upside before coming off from there again. 3.15 is an important near term resistance for Copper is is likely to hold in the medium term.

FOREX

Dollar index (89.42) in line with our expectation, has dipped from levels near 89.7-89.8 towards 89.4 and could move down further towards support on daily candles near 89.25 this week. On 3 day candles, there might be some support at current levels itself; which if holds, would take the Dollar Index upwards from here. US Retail Sales data came out higher than expectation but didn’t lend any strength to the Dollar.

Euro (1.2380): As per our expectation, Euro is rising towards 1.2400-1.2420 (seen as immediate resistance on daily line chart). If it breaks this resistance, it could then target previous highs near 1.25-1.26 (or max, go up to 1.28), from where a medium term correction could be possible. A straight rise past 1.26-1.28 would imply medium term bullishness for the Euro.

Dollar Yen (107.04) after having seen a high near 107.8 on Friday, has come off from there. As per our expectation, it is trading at levels near 107 (just below support trendline on daily candles). If this break sustains, it could target levels near 106.5 soon (close to support on weekly candles).

As we mentioned yesterday as well, Euro Yen (132.51) could face resistance near 132.5-133.0, being provided by 21 moving averages on 3 day and weekly line charts. The range in this week could be 132.5-132.0 as the Dollar Yen could sustain its break below 107, while the Euro stays below 1.24.

Exactly as we predicted yesterday, Pound (1.4337) is again testing levels near 1.43-1.435 (which is seen as interim resistance on 3 day candles and is also the previous high seen in Jan end). This is a crucial level, whose break could imply bullishness towards 1.45-46 in the medium term (seen as resistance on weekly line chart).

Dollar Rupee (65.4950) - Could face interim resistance near 65.535 (high seen in Nov '17). Above that, 65.60-65 (Oct '17 high and possible channel resistance) could act as decent intra week resistance. Downside could be restricted to 65.35.

INTEREST RATES

Limited US airstrikes on Syria hasn’t adversely affected risk appetite amongst investors and on Monday, bond prices in fact fell (thereby raising yields), indicating a possible shift towards equity. US Retail Sales coming in higher than expected might have also contributed to the rise in yields. Earlier last week, outlook on economic growth had been uplifted due to improvement in data on unemployment claims and the positivity reflected in the Fed minutes.

US 10 Yr Yield (2.8322%), 30 Yr (3.029%), 5 Yr (2.685%), 2 Yr (2.3732%):

The 10 Year yield saw a high near 2.86%, thereby causing a false break of resistance in the downward channel on short term charts. However, the yield has again dipped back into the channel and could possibly dip further towards 2.8%.

The 30 yr also broke above resistance on short term chart by seeing a high of 3.07% but is again back into the channel. It should dip lower towards 3% now.

RBA minutes: Growth to exceed potential, but still not strong case for near term hike

Minutes of April RBA meeting appeared to be rather balance. RBA sounded upbeat and said over 2018, GDP growth was expected to "exceed potential. CPI inflation was expected to "increase gradually" to a little above 2% target. Also, leading indicators continued to point to "above-average growth in employment" in the period ahead.

However, RBA also warned that "the possibility of an escalation in trade restrictions represented a risk to the global outlook that needed to be monitored closely". Additionally, "the high level of debt in China and the significant share of financial market activity in unregulated sectors continued to pose important risks to the outlook for the Chinese economy".

Regarding exchange range, RBA reiterated that "an appreciation of the Australian dollar would be expected to result in a slower pick-up in economic activity and inflation than forecast."

On monetary policy, RBA also reiterated that the next move "would be up, rather than down". But still, "there was not a strong case for a near-term adjustment in monetary policy".

Chinese ambassador to EU: Without a Brexit deal, there’s nothing to talk about with UK

Chinese ambassador to EU Zhang Ming told UK that a Brexit deal with EU is a prerequisite to trade talk with China. He said "if the EU and the U.K. fail to reach agreement in the first place, the U.K.'s agreements with other parties may have to face great uncertainties." He added that "only with an EU-U.K. deal can the U.K. be in a better position to have more detailed discussions with other players of the international community."

Zhang noted that is a "solid basis" in place for trade engagement and "not everything will start from zero after Brexit." And, "if Brexit goes well, I believe there will not be a big impact on U.K.'s cooperation with other members of the international community."

China GDP grew 6.8% in Q1, Added USD 8.5B US debt holdings in Feb

Released from China, Q1 GDP grew 6.8% yoy, same as prior quarter and met expectation. Retail sales rose 10.1% yoy in March, up from prior 9.7% yoy and beat expectation of 9.7% yoy. Industrial production, however, rose 6.0% yoy, slowed from prior 7.2% yoy and missed expectation of 6.9% yoy. Fixed assets investment also slowed to 7.5% yoy, down from 7.9% yoy and missed expectation of 7.7% yoy. Overall, the set of data showed robust growth momentum.

Separately, US Treasury data showed showed that China remained the largest foreign creditor to the US, holding USD 1.18T in US bonds, bills and notes in February. Debt holding by China has indeed by USD 8.5B for the month, the largest rise in six months. But it should be noted that the data was for the period even before the 232 steel tariffs of the US, not to mention the Section 301 tariffs against China. The impact of trade tensions on Chinese interest in US debts remains to be seen.

Meanwhile, Japan came as second largest foreign holder of US debts, dropped slightly from USD 1.07T to USD 1.06T.

Crude Oil Price Remains In Uptrend Above $65.40

Key Highlights

- Crude oil price moved higher this past week and settled above $65.00 against the US dollar.

- There was a break above a crucial declining channel with resistance at $63.80 on the 4-hours chart of XTI/USD.

- The US Retail Sales in March 2018 increased 0.6% (MoM), more than the +0.4% forecast.

- China’s GDP in Q1 2018 grew 6.8%, compared with the forecast of 6.7%.

Crude Oil Price Technical Analysis

This past week, there was a decent upside move in crude oil price from $61.80 against the US Dollar. The price moved higher and broke many resistances, including the $65.00 barrier.

Looking at the 4-hours chart of XTI/USD, the price is in a solid uptrend from the $62.00 swing low. It broke both 100 (red) and 200 (green) simple moving averages (4-hours) to move into a positive zone.

During the upside move, there was a break above a crucial declining channel with resistance at $63.80 on the 4-hours chart. The price traded as high as $67.74 before a downside correction was initiated.

It tested the 23.6% Fibonacci retracement level of the last wave from the $61.78 low to $67.74 high. There are also many supports on the downside near the $65.40 zone and the 38.2% Fibonacci retracement level of the last wave from the $61.78 low to $67.74 high.

Therefore, if the price dips further, buyers are likely to appear around the $65.40 area. On the upside, the price must clear the $67.50-70 resistance to move past $68.00 in the near term.

Recently in the US, the Retail Sales report for March 2018 was released by the US Census Bureau. The market was looking for a 0.4% rise in sales in March 2018, compared with the previous month.

The actual was better as there was a rise of 0.6% in sales, which was a lot better than the last decline of 0.1%. The report stated:

Advance estimates of U.S. retail and food services sales for March 2018, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $494.6 billion, an increase of 0.6 percent (±0.5 percent) from the previous month, and 4.5 percent (±0.5 percent) above March 2017.

Overall, there could be a short-term consolidation in crude oil price, but it remains supported for more gains.

Economic Releases to Watch Today

- UK Claimant Count Change March 2018 – Forecast 5.0K, versus 9.2K previous.

- UK ILO Unemployment Rate Feb 2018 (3M) – Forecast 4.3%, versus 4.3% previous.

- US Housing Starts March 2018 (MoM) – Forecast 1.269M, versus 1.236M previous.

- US Building Permits March 2018 (MoM) – Forecast 1.328M, versus 1.321M previous.

- US Industrial Production March 2018 (MoM) – Forecast +0.3%, versus +0.9% previous.

NZDUSD – Declines Further On Corrective Pullback

NZDUSD - The pair looks to build on its Friday correction in the new week as it saw price weakness during early Monday trading session today. Support lies at the 0.7300 level. Further down, the 0.7250 level comes in as the next downside target. Conversely, resistance resides at the 0.7400 level where a break will aim at the 0.7450 level. A break of here will have to occur to create scope for a run at the 0.7500 level. Further out, resistance stands at the 0.7550 level. All in all, NZDUSD faces further downside pressure

Positivity Prevails

Positivity Prevails

Global capital markets stayed in a positive mood overnight, but investors remain on guard for any escalations in geopolitical tensions while trade tariffs remain bubbling under the surface. On the latter view, the latest headline scrolling across the ” terminal” * THE US IS SAID MULLING NEW ACTION AGAINST CHINA’S TECH LIMITS: WSJ. As usual, any headline development in this market is worth keeping an eye on.

In the meantime, investors are breathing a sigh of relief that their portfolios survived the weekend as geopolitical tensions have not escalated following the weekend’s military action in Syria. Indeed a bit of a relief rally has ensued giving investors more wiggle to focus on the critical task at hand, first-quarter earnings season.

The markets didn’t dodge a bullet so far this month but have eluded a double barrel cannon in the form of trade wars and middle east military escalation.

Turning to the day ahead, the initial focus will be on China’s data dump and specifically the Q1 GDP report. According to Bloomberg, the consensus expects growth to have remained steady at 6.8% yoy. Its interesting given the robust GDP calls that China’s economy is showing little wear and tear from trade tension nor deleveraging.

Oil Markets

The easing of tensions in the middle east between Russia and the US saw oil prices continue to slide overnight. President Trump even walked back supposed planned sanction against Russia over Syria.

While Syria in itself is not a significant player in the oil supply chain, but indeed a sense of relief has set in that the US-led airstrikes on Syria didn’t trigger a broader response from Russia which could potentially have sent the region into chaos and introduced many more players into the escalation matrix.

But today is a new day and with so many potential supply disruptors in play and few signs that the current market upheaval will end any time soon, traders continue to pay the geopolitical risk premium. So Oil prices should remain bid on the dip at least through the Iran nuclear deal deadline ( May 12) if not for the remainder of 2018.

Gold Markets

After bulking up on gold hedges ahead of the weekend, paid in premiums continued to gradually unwind as investors are back gingerly testing the global equity market waters again. But with investors focusing on positive trade headlines and Syria de-escalation the markets is only a headline away from reigniting the Middle East Powder Keg. Few safe havens offer the safety and appeal gold has in this highly disruptive market and despite a quieting of negative headline overnight, its unlikely we’ve seen the last of China trade tension or a weaker US dollar for that fact. All of which continues to provide the most apparent reasons to own gold.

Currency Markets

The British Pound

The Sterling Bulls are charging ahead of the crucial UK wages data which is anticipated to come in strong. With positive vibes from the Brexit negotiations suggesting more hawkish policy room for the BOE, a robust wages data will provide the boost to May rate hike expectations and will underpin GBP sentiment.

The Euro

Outside of the Pound G-10 currency markets feel very dispassionate. Neither US CPI nor FOMC minutes had a lasting impact on the market last week; the latter considered dated after Fed Powell somewhat dovish signals last Friday. The Euro is running hot on ECB speakers playing down the dovish turn on the economic data, but it’s difficult to see the EURUSD moving out of its well-trodden near term ranges anytime before the ECB sets the tone at the next policy meeting April 26.

The Japanese Yen

The market looks very heavy moving towards 107 but with US yields and Global equity market on the ups there little incentive to push lower at this stage. “Abexit” continues to weigh on local sentiment, which could be the eventual trigger to move below 106.75, but in the meantime, the market is doing little more than biding time until the next headline risk.

But with so much risk permeating the markets, there’s still substantial support for long JPY.

The Malaysian Ringgit

Local traders think GE14 can’t get here quick enough. Election risk is not something unique to Malaysia, but unlike some of the recent surprising election results in the UK or the US, its highly unlikely Malaysia current ruling party will get upended.

None the less, that slight chance is keeping Malaysian bond buyers on hold. So with the Malaysia Bond market expected to remain quiet ahead of the election, currency markets will remain equally silent and will continue to trade with a defensive posture ahead of the polls.

The Market was positioning for a stronger MYR into the election, so with a base forming around 3.87, the logical move it to reduce shorts and wait for the better level to re-engage long MYR positions. So we should expect the USDMYR to trade within and continue to revert to the upper levels of the current ranges.

Bank Of Canada Could Hold Rates Amid Trade Uncertainty

The Canadian dollar is one of the best performers in the month of April versus the US dollar. The loonie has appreciated more than 4 percent versus the greenback as the softness in the USD has combined with stronger oil prices due to geopolitics. Canadian fundamentals have been mixed with strong employment data but a weaker housing sector. Last year the Bank of Canada (BoC) raised rates two times and once already this year leaving the benchmark rate at 1.25 percent unchanged in March. The hawkish tone of 2017 is gone from the central bank’s rhetoric and replaced with rising concerns for the uncertainty of NAFTA and inflationary pressures.

The BoC will release its rate statement on Wednesday, April April 18 at 10:00 am EDT. At the same time the quarterly Monetary Policy Report will be published with BoC Governor Stephen Poloz hosting a press conference at 11:15 am EDT. The central bank is expected to keep rates on hold awaiting a more clear outcome on trade negotiations and other internal economic factors.

- Canadian inflation to hit above 2 percent target in coming months

- GDP growth anticipated to pick up

- BoC between inflationary pressure and high household debt

Canadian Dollar Oil Correlation Makes a Comeback

The USD/CAD started the month of April at 1.2898 and has depreciated steadily as the Trump administration has opened multiple fronts engaging in trade disputes that have hurt the dollar despite a growing economy and the support of the U.S. Federal Reserve with a rate hike in March. The loonie lost ground at the beginning of the year as concerns about NAFTA started to rise given the hardball tactics from the Trump Administration. Canada and Mexico did not back down what they deemed unreasonable demands and that strategy appears to have paid off as the US is back at the table with a softer stance. The deal has not been renegotiated and the escalation of the Syrian conflict has probably pushed the timetable a few weeks out.

The Canadian dollar has gained after the news that Prime Minister Justin Trudeau attended an emergency summit to deal with an oil pipeline. The loonie historically has been highly correlated with energy prices due to them being one of Canada’s biggest exports. The fall in crude prices in 2015 tested that correlation but it appears its back in play. Oil prices rose after the Organization of the Petroleum Exporting Countries (OPEC) and other major producers agreed to limit crude output. Tensions in the Middle East have kept prices above $60 per barrel.

Last month inflation beat expectations to record a gain of 2.2 percent year over year. Statistics Canada will release monthly inflation data on Friday, April 20 at 8:30 am EDT with the prices of gasoline, cars and mortgage interest costs the main contributors to an increase in inflation. The pickup in consumer prices is adding pressure on the Bank of Canada to keep rising rates to cool down the economy. The slowdown in the last quarter of 2017 has put the central bank in a tough spot. Delaying the hike could rev up growth, but waiting too long could end up causing a recession. To complicate matters more for Mr Poloz’s decision is the fact that Canadian household took advantage of record low rates, to incur in their own record debt levels. A recent poll shows that one third of respondents said that rising rates could push them towards bankruptcy.

The BoC will update its quarterly growth projections with a possible downgrade in the cards. In January the bank had GDP growth for 2018 at 2.2 percent and 1.6 percent in 2019, these could be adjusted lower but there is also the fact that in March Govenor Poloz stressed that he is not afraid to let rates at current levels to boost the economy. Canadian banks are forecasting at least two rate hikes, with some going as high as three from the central bank, but not necessarily in the next couple of meetings. The big NAFTA unknown would have to be sorted before Poloz can commit to a monetary policy move that would not have to be reversed by an external event.

Market events to watch this week:

Wednesday, April 18

4:30am GBP CPI y/y

10:00am CAD BOC Monetary Policy Report

10:00am CAD BOC Rate Statement

10:00am CAD Overnight Rate

10:30am USD Crude Oil Inventories

11:15am CAD BOC Press Conference

6:45pm NZD CPI q/q

9:30pm AUD Employment Change

9:30pm AUD Unemployment Rate

Thursday, April 19

4:30am GBP Retail Sales m/m

Friday, April 20

8:30am CAD CPI m/m

8:30am CAD Core Retail Sales m/m

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Members Present

Philip Lowe (Governor and Chair), Guy Debelle (Deputy Governor), Mark Barnaba AM, Kathryn Fagg, John Fraser, Ian Harper, Allan Moss AO, Carol Schwartz AM, Catherine Tanna

Others Present

Michele Bullock (Assistant Governor, Financial System), Luci Ellis (Assistant Governor, Economic), Christopher Kent (Assistant Governor, Financial Markets), Alexandra Heath (Head, Economic Analysis Department), Jonathan Kearns (Head, Financial Stability Department)

Anthony Dickman (Secretary), Andrea Brischetto (Deputy Secretary)

Domestic Economic Conditions

Members commenced their discussion of the domestic economy by noting that domestic demand had grown by around 3 per cent over the year to the December quarter. Consumption and non-mining business investment had made significant contributions to growth. In contrast, there had been declines in mining and dwelling investment. GDP had not grown as solidly as domestic demand over 2017 because net exports had subtracted from growth. However, given the momentum in domestic demand and expectations that the decline in export volumes would be temporary, members noted that the economy appeared likely to record faster growth over 2018 than the previous year.

Household consumption had increased strongly in the December quarter and had been revised higher in preceding quarters. Members noted that following these revisions, consumption growth over 2017 had been more consistent with the strength seen in the labour market over that period. More recently, growth in retail sales values had been below average in early 2018. At least some of this was likely to reflect ongoing retail price deflation, owing to strong competition in this sector. Consumer confidence had declined a little over recent months, but remained above average.

Growth in household disposable income had picked up over 2017, partly reflecting the strength in employment growth over the course of the year. Income of unincorporated small businesses, which is attributed to the household sector, had increased in the December quarter. The national accounts measure of wages growth had continued to be lower than wages growth recorded in the wage price index. This suggested that compositional changes in the labour force had continued to have a dampening effect on household earnings. By sector, the national accounts measure of wages growth had picked up significantly for business services, but had fallen further for household services. At the same time, there had been strong employment growth in the household services sector, as well as for goods-related industries.

Members noted that year-ended growth in employment had remained strong in the first few months of 2018, although the monthly increases in employment had moderated. Nationwide, employment had continued to grow strongly in the household services sector, particularly in the health and social assistance industry. Employment in goods-related industries had picked up sharply over the year to February, mainly reflecting strength in construction employment. Members observed that migration flows from Western Australia had served to mitigate the effect of the end of the mining investment boom on the labour market in that state. The national employment-to-population ratio had remained at a high level, as employment growth had been strong enough to absorb growth in the working-age population, although not high enough to reduce the unemployment rate further. The unemployment rate had been little changed over the preceding six months at around 5½ per cent and measures of underemployment had remained at relatively high levels. Taken together, these indicators suggested that there was still some spare capacity in the labour market. Leading indicators continued to point to above-average growth in employment in the period ahead.

In the residential housing market, dwelling investment had declined a little over 2017 but was expected to remain at a high level over the following year or so, supported by the large pipeline of residential construction work yet to be completed associated with the increase in residential building approvals over 2017. Housing prices had declined further in Sydney and Melbourne. Members noted that Sydney housing prices had declined by a little under 5 per cent since their peak in mid 2017. Members also noted that declines in housing prices of around 10 per cent in some cities had occurred several times over the preceding 15 years or so. Over recent months, housing prices had been little changed in Brisbane and Perth.

Members noted that most components of business investment had increased over 2017, with the exception of construction activity in the mining sector. Private non-mining business investment had increased by more than 12 per cent. Public spending had supported growth in economic activity over 2017 and this momentum was expected to continue in the period ahead. Data on firms' capital expenditure plans and on the pipeline of non-residential construction work yet to be done also suggested that non-mining business investment was expected to grow solidly over the following few years. Consistent with this, survey measures indicated that business conditions had been around record highs and above average in all industries and states.

Export volumes had fallen in the December quarter. The decline in coal exports was expected to reverse gradually over the first half of 2018 as shipments from Queensland recover following a number of temporary disruptions. Rural export volumes had fallen as a result of lower crop production, which was unlikely to be reversed in the near term. Members noted that the spot prices of iron ore and coal had declined significantly since the previous meeting, reflecting concerns about the resilience of Chinese iron ore and coal demand after the Chinese New Year holiday period, although contract prices for coal had increased. Concerns that an escalation in global trade protectionism could damage prospects for global growth had also contributed to lower commodity prices. In contrast, the price of oil had increased in recent weeks. Recent developments in commodity prices suggested that the terms of trade for Australia had been little changed in the March quarter.

International Economic Conditions

As a backdrop to their discussion on international economic conditions, members noted that global industrial activity and trade had strengthened over the prior couple of years. They observed that although the tariff announcements by the US administration – and by the Chinese authorities in response – were unlikely to have a significant direct effect on global trade, the possibility of an escalation in trade restrictions represented a risk to the global outlook that needed to be monitored closely.

Above-trend growth in the major advanced economies had led to a further tightening in labour markets. Business conditions had remained around their highest levels in several years, despite having declined from their peaks in Europe recently. In the United States, fiscal stimulus was expected to support growth in output over the period ahead and was likely to add to inflationary pressures as the US economy encountered capacity constraints. Actual and expected growth in wages in the advanced economies had increased but remained low. Core inflation had also remained low, although it had picked up over recent months in the United States and Japan, and inflationary pressures were expected to build in the major advanced economies in the period ahead.

In China, the authorities had recently announced a growth target of around 6.5 per cent for 2018, which was similar to the target for 2017, and a continuation of policies designed to reduce pollution and manage financial stability risks. Members recognised that economic data for China were difficult to interpret early in the calendar year owing to the effect of the Chinese New Year holidays. Nevertheless, the available data suggested that private investment growth had picked up but remained low. Growth in industrial output had also been subdued, partly because of policies designed to reduce excess capacity and pollution. However, indicators of consumer spending suggested that consumption growth would continue to run above GDP growth, even though consumption growth had eased in recent years. Growth in total social financing had eased in prior months and housing prices had fallen in the largest cities where housing market restrictions had been most prominent; growth in dwelling investment in these cities had moderated. Nationwide, conditions in the housing market had been broadly stable.

In some parts of east Asia, output growth had been a little slower around the turn of the year, reflecting an easing in export growth in particular. However, more recent data suggested that domestic demand conditions had been somewhat stronger in early 2018 in the high-income economies. In India, growth had increased over 2017, driven by strong growth in investment; growth in exports of business and financial services had also picked up.

Financial Markets

Members commenced their discussion of developments in financial markets by noting that, as expected, the US Federal Reserve had raised the federal funds rate by 25 basis points at its March meeting. The Federal Open Market Committee (FOMC) had published upwardly revised projections for the US economy and a slightly steeper path for expected future policy rates than previously, partly owing to the US fiscal stimulus. The median of the FOMC's revised projections implied that the policy rate will reach a neutral stance in 2019, and move a little above the FOMC's estimate of the neutral rate in 2020. Financial market pricing suggested market participants expected a more modest increase in the policy rate over 2019 and 2020.

Members noted that long-term government bond yields in the United States and some other economies had risen over the preceding six months, but had declined a little recently, in part reflecting a slight lowering of inflation expectations. Share prices had fallen over the preceding month, reflecting concerns about international trade policy developments, as well as regulatory and company-specific developments in the technology sector. Australian equity prices had moved broadly in line with global markets, with prices of resources sector stocks having declined in response to lower commodity prices.

Members also observed that corporate bond spreads in the United States and euro area had risen a little over March, which was likely to have reflected investor concerns about trade policies and reduced demand for corporate debt relating to US tax changes.

Members discussed developments in US dollar money markets, noting the marked increase in the cost of borrowing US dollars at short terms since the beginning of 2018. The increase in US dollar short-term interest rates appeared to have reflected a number of factors, including a sharp increase in US Treasury bill issuance in the early part of the year and changes to US tax arrangements, which had encouraged US subsidiaries of foreign financial institutions to source more of their funding from onshore US money markets. In addition, demand for a range of money market instruments from a number of large US corporations was thought to have declined following changes to US tax arrangements.

Members noted that the developments in US money markets had flowed through to higher short-term borrowing costs in financial markets in Australia. In part, this reflected the use by Australian banks of funds raised in US markets to finance their domestic assets, in contrast to banks from other jurisdictions, which funded US dollar assets with the funds raised. There had also been some flow-through to short-term interest rates in a few other markets, though to a lesser extent. Futures pricing suggested that these pressures in US money markets were expected to abate somewhat over the coming months.

Members discussed the announced reorganisation of Chinese financial regulatory agencies, which was designed to strengthen oversight and reduce the scope for regulatory arbitrage. The changes were consistent with greater policy coordination and a continued focus on reducing risks in the Chinese financial system.

There had been fairly modest movements in most major exchange rates over the previous month. The Australian dollar had depreciated a little further against the US dollar and in trade-weighted terms, but remained within the relatively narrow range of the preceding two years. The recent depreciation had occurred in the context of lower commodity prices and interest rates in the United States having moved above those in Australia.

In Australia, corporate bond spreads had risen slightly over the preceding month, in line with developments in international markets, but remained at relatively low levels. Major banks' net bond issuance had been relatively strong over 2018 to date. Members noted that major banks' marginal cost of debt funding had increased a little over the preceding month, reflecting the higher cost of borrowing in short-term money markets related to the developments in US money markets. At the same time, there had been little change in retail deposit rates, limiting the overall effect on bank funding costs.

Growth in housing credit had stabilised in 2018, having slowed over the course of 2017, and the data on loan approvals suggested that banks had comfortably met the requirements of the Australian Prudential Regulation Authority (APRA) in relation to interest-only lending. Members noted that there had been a number of reductions in banks' advertised interest rates on investor and interest-only mortgages over the preceding month.

Financial market pricing continued to imply that the cash rate was expected to remain unchanged for a considerable period, with a 25 basis point increase expected in mid 2019.

Financial Stability

Members were briefed on the Bank's regular half-yearly assessment of the financial system.

At the margin, global financial stability risks had eased. Stronger economic growth had improved banks' loan performance and underlying profitability. For some banks, the increase in profits had also reflected the absence of large asset write-downs, fines and restructuring expenses, which had affected previous outcomes. In China, the authorities had taken measures to contain the risks to the financial system emanating from the high level of debt and some higher-risk forms of credit intermediation, although risks to the stability of the Chinese financial system remained.

Low risk-free interest rates continued to underpin the valuations of many assets around the world. Members noted that a sharp increase in interest rates toward historically more normal levels that is not associated with stronger growth could see simultaneous price falls across a range of assets. In addition, investors had been accepting low levels of compensation for bearing risk, so a reassessment of this would accentuate possible price falls for risky assets. Past episodes had shown that such price falls could be large for equities and high-yield corporate bonds.

Housing markets had been strong in a number of small open economies that did not experience significant housing market downturns during the financial crisis, including Australia. Low interest rates had contributed to strong growth in household borrowing and housing prices in these countries. National authorities had implemented ‘macroprudential’ measures to curtail the associated build-up in risks. Members discussed these prudential measures more broadly, observing that the frameworks differed across countries and were still evolving. Measuring the effectiveness of these policies was difficult. Internationally they had successfully constrained the type of borrowing targeted, although in some instances there was switching of activity to other forms of finance. While governance arrangements varied across countries, members noted that the strength of the relationships among the different agencies involved was crucial to the smooth operation and effectiveness of these policies. Members noted that an important aspect of the arrangements in Australia was the strong relationships among the regulatory agencies, supported by the Council of Financial Regulators. The Reserve Bank and APRA had worked closely to address risks in the housing market.

Domestically, risks remained from the high level of household debt and the growth of riskier lending in earlier years, but regulatory measures had helped to contain the build-up of risks. Members noted that while the growth of household debt had outpaced that of income over recent years, household net wealth had continued to grow and, in aggregate, households' housing and financial assets far exceeded their borrowing. Members noted, however, that this was not reflective of the financial positions of all individual households. Nevertheless, measures of household financial stress did not indicate a high level of financial stress at present. Members also noted that the share of interest-only loans in new lending had fallen sharply and the share of loans with high loan-to-valuation ratios had also declined since the regulatory measures were implemented by APRA, which had further tightened lending standards. Housing prices had declined in Sydney, and to a lesser extent in Melbourne. Price falls had been larger for more expensive properties, suggesting that the regulatory measures, which would have had a greater impact on investors and therefore prices of apartments and cheaper dwellings, had not been the sole drivers of the slowdown. Members noted that a number of structural factors had also been at work.

Turning to developments in the commercial property sector, members noted that office property conditions had been strongest in Sydney and Melbourne, where the limited net increase in supply and robust tenant demand had pushed vacancy rates to low levels. Prices had continued to rise faster than rents, with sale prices implying very low rental yields for some properties, although overall the spread of commercial property yields to government bond yields had remained within its historical range. Demand had been strong from both domestic and international buyers. Rents for retail properties had not increased, reflecting the strong competition retailers were facing. In this environment, some retail property was being re-purposed to include a greater mix of entertainment and hospitality services or to incorporate a greater residential component.

Members noted that the resilience of the Australian financial system had continued to improve. Australian banks' profits had increased in the latest half-year period. Growth in profits had been driven by a wider net interest margin and a decline in bad and doubtful debt charges. Bank analysts generally expected the contribution of these factors to profit growth to dissipate in the near term. Banks' asset performance remained robust, with non-performing loan ratios falling for business lending and remaining low for housing lending. Members noted that loan performance remained weaker in Western Australia, reflecting the end of the mining investment boom in that state. However, they observed that the deterioration in loan performance had been relatively modest given the significant decline in economic activity and decline in housing prices in the state.

The capital ratios of Australian banks had risen further over the preceding half-year and were substantially higher than a decade prior. Further, a greater share of this was high-quality capital. The capital ratios of the four major banks were well above the current regulatory minimum and close to the ‘unquestionably strong’ prudential benchmark to apply from 2020. The increase in banks' capital ratios had reflected retained profits and subdued growth in risk-weighted assets as the large banks had reduced the size of their non-mortgage portfolios, which carry higher risk weights. Banks continued to hold a large stock of liquid assets, well exceeding the requirements under the Liquidity Coverage Ratio.

Members were briefed on the proposed revisions to the capital framework outlined in a consultation paper released by APRA in February 2018. The proposal would see changes in the capital required for different loans to make the capital requirement more sensitive to the risk of the loans, but would not raise the aggregate capital requirement for the industry. Members noted that the banking sector was the subject of several inquiries, the outcomes of which could affect how they operate.

Considerations for Monetary Policy

In considering the stance of monetary policy, members noted that conditions in the global economy had remained positive in the preceding month. Output in the advanced economies was expected to continue to grow at above-trend rates, supported by accommodative monetary policy and, in the case of the United States, more expansionary fiscal policy. Over time, this was expected to lead to even tighter labour market conditions and further upward pressure on labour costs. Globally, inflation remained low, but was expected to increase. A number of central banks had withdrawn some monetary stimulus and further steps in this direction were expected.

In China, recent policy announcements were consistent with the trend towards a more sustainable growth path. Of particular note was the ongoing commitment to reducing financial stability risks through changes to policy and the regulatory structure. Members noted that the high level of debt in China and the significant share of financial market activity in unregulated sectors continued to pose important risks to the outlook for the Chinese economy.

Long-term bond yields had risen in the United States and some other economies over the preceding six months and credit spreads had widened a little recently, but financial conditions generally remained expansionary. There had been some tightening of conditions in US dollar short-term money markets, which had flowed through to higher short-term interest rates in a few other countries, including Australia. Equity market volatility had increased from very low levels, partly because of concerns about the direction of trade policy internationally. The Australian dollar had declined a little since the previous meeting.

Domestically, the recent data had generally been consistent with the forecast for a gradual improvement in growth. The outlook for non-mining business investment growth remained positive, supported by solid domestic demand conditions, the spillover from public infrastructure work and the pipeline of non-residential building work to be completed. Forward-looking indicators suggested that spare capacity in the labour market would continue to decline gradually over 2018. Consequently, wages growth was expected to rise gradually from its current low rate. Low growth in labour costs in combination with strong competition in the retail sector suggested that inflation would remain low for some time before also picking up gradually as the economy and labour market strengthen.

Conditions in the housing markets in Sydney and Melbourne had eased, while conditions in housing markets elsewhere had been relatively stable. Tighter credit standards and APRA's supervisory measures had been helpful in containing the build-up of risk on household balance sheets. However, household debt levels remained high, which continued to pose an element of uncertainty for the outlook for consumption growth.

The low level of interest rates had supported growth over 2017, which had reduced the unemployment rate and brought inflation closer to the target. Further progress on these goals was expected in the period ahead, but this progress was likely to be gradual. Over 2018, GDP growth was expected to exceed potential growth and CPI inflation was expected to increase gradually to be a little above 2 per cent. Members noted that an appreciation of the Australian dollar would be expected to result in a slower pick-up in economic activity and inflation than forecast.

In current circumstances, members agreed that it was more likely that the next move in the cash rate would be up, rather than down. As progress in lowering unemployment and having inflation return to the midpoint of the target was expected to be only gradual, members also agreed that there was not a strong case for a near-term adjustment in monetary policy. Taking into account the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

The Decision

The Board decided to leave the cash rate unchanged at 1.5 per cent.