Sample Category Title

Fresh Airstrikes On Syria, US Denies Involvement

There have been fresh airstrikes on Syria overnight, with an attack on targets and airfields near the Israeli border. The US has said that it isn’t conducting any military activity in the area. Syrian air defences have engaged and intercepted missiles. This has led to very little reaction in markets so far, as details surrounding the origin of the attack are currently unavailable. Yesterday’s trading showed a break down in correlation as FX took control and indices moved in conjunction with their currencies. European indices were down; the UK 100 fell -0.91% to close at 7198.20, while GBPUSD rose to 1.43377 from 1.42366. US Indices climbed higher, with the US 500 Index up 0.81% to 2677.84.

China has told the UK that a failure to reach a deal with the EU regarding Brexit would lead to no trade deal between the two nations. “Only a deal with the European Union will pave the way for the UK to hold more detailed” talks with big markets”, according to Zhang Ming, head of the Chinese mission to the European Union. This reflects the weaker position the UK will face upon leaving the EU. “If there is not a Brexit deal, there won’t be things to talk about after that,” he told Politico. “If the EU and the UK fail to reach agreement in the first place, the UK’s agreements with other parties may have to face great uncertainties.”

US Retail Sales (MoM) (Mar) was released at 0.6% v an expected 0.4%, from -0.1% previously. Retail Sales Ex-Autos (MoM) (Mar) was as expected, unchanged at 0.2%. Retail Sales Control Group (Mar) was also as expected at 0.4%, from 0.1% prior, which was revised down to 0.0%. This data rebounded this month after slipping below zero over the previous two readings and missing expectations. This month matched or exceeded expectations, putting the data back on track and making up for the seasonal and weather-related drop. USDJPY moved higher from 107.242 to 107.386 after this data release.

FOMC Member Kaplan gave a speech with the following comments: Cyclical wage pressure will build in 2018 and unemployment will fall to 3.7%. The pricing power of business is more limited than we are used to seeing at this stage in the cycle. Sub 2% growth is expected in 2020 as fiscal stimulus fades and monetary policy tightens. Trade is a critical opportunity for faster growth. Without structural reforms, the US will be sluggish in the mid and long-term. He remains very concerned fiscal stimulus will turn into a headwind in 3 to 5 years. He expects 3 rate hikes this year, more next year. The 10-year yield at 2.85% puts a limit on how high they can raise rates. He thinks Powell is likely to continue with a gradual, patient approach. He states that the US cannot cut immigration and simultaneously grow GDP and the workforce.

FOMC Member Bostic spoke about the economy at the Shoals Chamber of Commerce, in Alabama. The following comments were made: The Fed is trying to achieve some notion of full employment. The Fed has not seen much movement in wages. The Fed gets mixed reactions from firms on pricing power.

FOMC Member Kashkari spoke at an event and made the following comments: We must look beyond U3 to gauge slack. No signs of sudden acceleration in inflation. Slow wage growth shows slack. Main Street hasn’t fully recovered from the crisis. We are forgetting the lessons of the financial crisis.

The RBA Meeting Minutes were released. There was broad agreement that there was not a strong case for a near-term move in policy and the next move in rate is likely to be up. Progress on unemployment and inflation is likely to only be gradual. Inflation is to remain low for some time given retail competition and slow wage growth. The economy appeared likely to grow faster than in 2017. An appreciation in the AUD would slow the expected acceleration in the economy. Wages to pick up gradually, as leading indicators pointed to more job gains. There is still spare capacity in the labour market and underemployment is at high levels. High household debt creates uncertainty for the consumption outlook. Conditions in the global economy remain positive, while Chinese debt levels are an important risk. AUDUSD fell from 0.77870 to 0.77603 after the publication of the minutes.

Chinese Gross Domestic Product (YoY) (Q1) came in at 6.8% against 6.7% expected, from 6.8% prior. Gross Domestic Product (QoQ) (Q1) came in at 1.4% against 1.5% expected, from 1.6% prior. This data shows a stabilisation in the yearly figure and a slight dip in the quarterly number.

EURUSD is up 0.07% overnight, trading around 1.23875.

USDJPY is down -0.08% in early session trading at around 107.026.

GBPUSD is up 0.05% this morning, trading around 1.43428.

Gold is down -0.02% in early morning trading at around $1,345.39.

WTI is up 0.23% this morning, trading around $66.52.

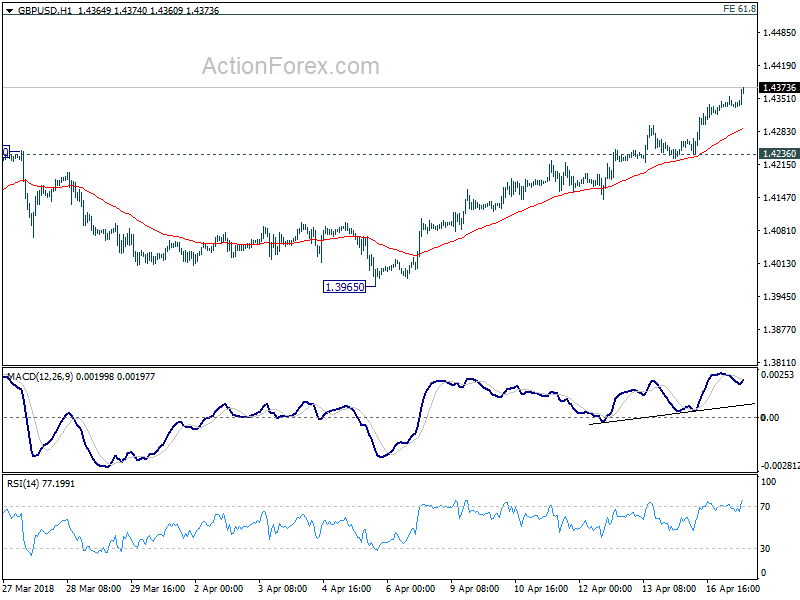

GBPUSD Further Bullish Headed In UK Jobs Data

The British pound continues to firm above the 1.4300 handle against the U.S dollar, with price-action moving to its highest trading level since, June 2016, hitting 1.4353. The GBPUSD pair currently trades around the 1.4340 level, after briefly piercing the former yearly price-high, at 1.4344. Sterling traders now turn their attention to key UK Jobs data, with a better than expected monthly headline number likely to further anchor bets that the BOE will soon raise UK rates.

The GBPUSD pair remains strongly bullish bias while trading above the 1.4300 level, with key resistance is now located at the 1.4353 and 1.4390 levels.

If the GBPUSD pair moves below the 1.4300 level for a sustained period, sellers may test back towards the 1.4260 and 1.4230 levels.

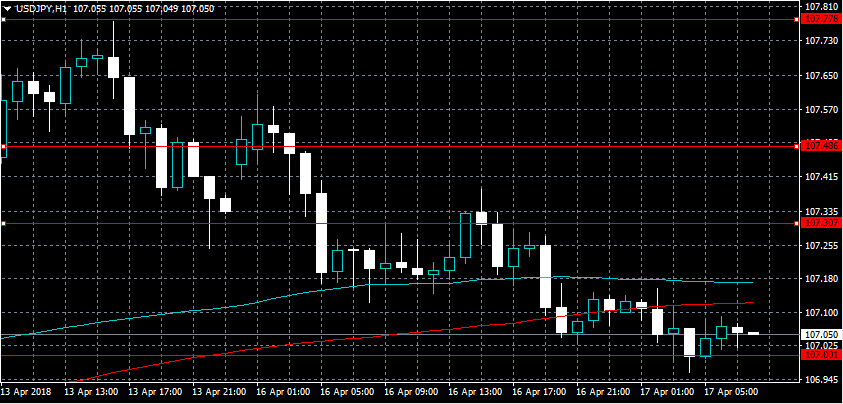

USDJPY Pair Testing Below Key Pivot

The U.S dollar continues to trade to the downside against the Japanese yen currency, as the greenback comes under selling pressure across the board. The USDJPY pair currently trades around the level 107.00 level, as buyers looked past better than expected United States Retail Sales data on Monday. Traders now look towards U.S Housing and Industrial Production data, and scheduled speeches from four FOMC members.

The USDJPY pair is intraday bearish while trading above below the 107.00 level, support is currently found at the 106.60 and 106.00 levels.

Should price-action on the USDJPY pair move back above the 107.30 level, buyers may test towards the 107.48 and 107.77 levels.

Global Economic Data In Focus On Tuesday

Investors are bracing for an active Tuesday session in the financial markets, with headline data from the United States and Europe scheduled for release.

The economic calendar kicks off with a report on Italian consumer prices at 08:00 GMT. The monthly report is expected to show annual CPI growth of 1.1% for March.

Attention quickly shifts to UK employment data where the Office for National Statistics is expected to report an unemployment rate of 4.3% between December and February. The same report will likely show a 3% annual rise in hourly earnings over the same three-month period.

Germany's ZEW survey of institutional investor sentiment will make headlines at 09:00 GMT. The current situation index is projected to fall to 88 in April form 90.7 the previous month. The gauge of economic sentiment also likely fell into negative territory.

ZEW will also report on euro-wide investor sentiment at 09:00 GMT. The region's economic sentiment indicator likely fell to 7.3 from 13.4 in March.

The start of North American trading at 12:30 GMT will feature headline housing data courtesy of the US Department of Commerce. Housing starts are projected to rise to 1.269 million in March from 1.236 million the month before (all in seasonally adjusted terms). Meanwhile, new permits to build homes is forecast to climb 0.7% to 1.328 million.

About 45 minutes later, the Federal Reserve will issue its monthly report on factory output. Industrial production likely rose 0.3% in March.

On the monetary policy front, three Federal Reserve speakers will deliver a public address on Tuesday, including Patrick Harker, Charles Evans and Raphael Bostic. Harker and Bostic are both members of the Federal Open Market Committee (FOMC), which is the Fed's policy-setting board.

In terms of commodity news, the American Petroleum Institute will issue its weekly crude stockpiles report, a precursor to the official data release on Wednesday.

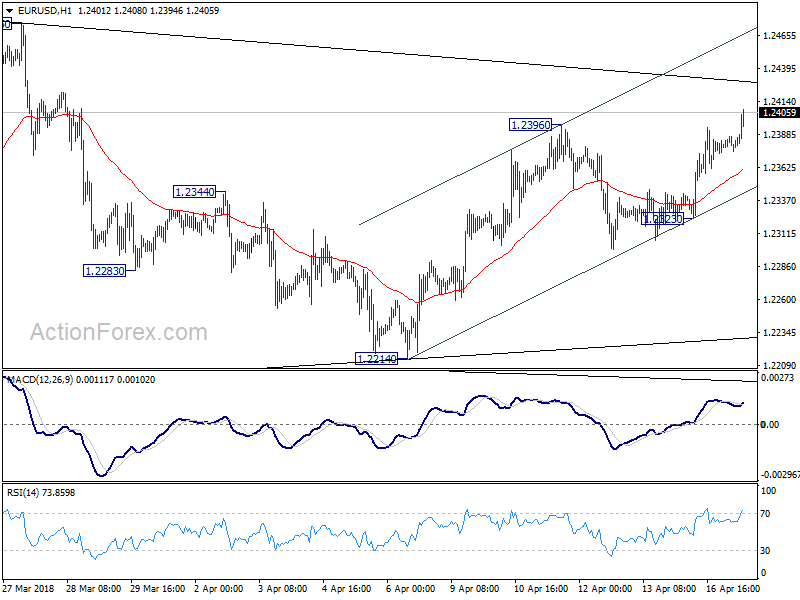

EUR/USD

Europe's common currency held higher on Monday amid prevailing dollar weakness. EUR/USD came within a few pips of 1.2400 before consolidating around 1.2386. The currency pair faces strong resistance at 1.2395 and immediate downside support near 1.2300.

GBP/USD

Cable's upward momentum continued Monday, with prices hitting their highest level since the Brexit vote. GBP/USD briefly traded above 1.4350 and has since consolidated just below those levels. At press time, the currency pair was trading at 1.4343. Further upside appears to be in store as investors set their sights on Brexit.

USD/JPY

After roaring to a high near 107.70, USD/JPY has backtracked to 107.00 territory. The pair could get plenty of attention on Tuesday as the presidents of both countries meet. There's still a bullish case to be made for this pair given the yen's prevailing weakness.

Bullish EUR/USD Challenges Fibs And USD/JPY Breaks Rising Wedge

The EUR/USD made a bullish bounce, which could either be part of a larger ABC correction (gold) within a wave B (brown) or the start of an uptrend in wave 3 (green). The key level for determining whether it’s a 123 or ABC are the Fibonacci target levels. A bullish breakout above the 100% Fib level when comparing wave C versus A makes a wave 3 more likely.

The EUR/USD broke above the resistance trend line (dotted red) and is now challenging the previous high (orange). A bullish breakout could expand the bullish momentum but the Fib levels remain key. A bearish breakout below the support trend lines could indicate weakness and a bearish reversal.

The USD/JPY has made a bearish reversal at the key 50% Fibonacci resistance level and price is now challenging and breaking below the support trend line (blue). The support is part of a rising wedge chart pattern and the bearish breakout could indicate a trend change.

The USD/JPY is pushing below support (dotted blue) but price will need to reach at least the 161.8% Fibonacci target of wave 3 v1 before the wave 3 pattern becomes more likely. A bear flag chart pattern that appears after price hits this target could indicate a potential continuation setup.

Elliott Wave View: USDCAD Calling Intraday Bounce

USDCAD Elliott Wave short-term view suggests that the bounce to 1.2942 high ended Intermediate degree wave (2). Then the decline from there is unfolding in an impulse sequence with an internal sub-division of each leg lower is showing 5 waves structure thus favored it to be an impulse. Below from 1.2942 high, Intermediate wave (3) remains in progress in 5 waves structure looking for 1 more push lower before a bounce in Intermediate wave (4) takes place.

Now let’s take a quick look at the short-term price action in the pair from 1.2942 high. The decline from there can be seen in 5 waves impulse sequence, where Minor wave 1 of (3) ended in 5 waves at 1.2744. Minor wave 2 of (3) ended 1.2818, Minor wave 3 of (3) ended in another 5 waves at 1.2543 low. And above from there Minor wave 4 of (3) bounce ended in 3 swings as a Flat structure at 1.2622 high. Below from there, the pair is expected to see another marginal push lower towards the inverse 1.236-1.618% ext area of Minor wave 4 at 1.2524-1.2493 area approximately to end the Minor wave 5 of (3) lower. However, in case of further downside extension pair can extend in Minor wave 5 of (3) towards wave 5=1 target area as well at 1.2418-1.2373 area before a bounce in intermediate wave (4) takes place against 1.2942 high. Which should then expected to fail in 3, 7 or 11 swings against 1.2942 high for further downside extension, so don’t like buying the pair into proposed bounces.

USDCAD Elliott Wave 1 Hour Chart

Dollar selling picks up pace. GBP leads, EUR follows, CAD could be next

Dollar selling is picking up pace in early European session.

GBP/USD leads the way higher ahead of UK job data. Hitting as high as 1.4374 so far. It's on track for 1.4519 projection level.

GBP/USD leads the way higher ahead of UK job data. Hitting as high as 1.4374 so far. It's on track for 1.4519 projection level.

EUR/USD finally makes up its mind and breaks 1.2396. Trend line resistance at 1.2429 is the first hurdle. But we'd expect an easy break there to 1.2475.

EUR/USD finally makes up its mind and breaks 1.2396. Trend line resistance at 1.2429 is the first hurdle. But we'd expect an easy break there to 1.2475.

And, USD/CAD could be the next one coming. A break of 1.2544 temporary low looks around the corner.

And, USD/CAD could be the next one coming. A break of 1.2544 temporary low looks around the corner.

Stock Index Futures Trended Up After S&P 500 Closed 0.8% Higher

Market movers today

Today, we will get the UK labour market report for February. We expect the annual growth rate of average hourly earnings excluding bonuses (3M average) to increase to 2.8% y/y from 2.6% y/y, as the weight of the monthly fall in December 2016 becomes less important. We believe the unemployment rate (3M average) will remain at 4.3%.

In the euro area, German ZEW expectations for April are being released where consensus is for another fall to -1.0 from 5.1. The survey will give some early insights on how much recent geopolitical uncertainty and US-China trade war tensions have weighed on investor economic sentiment.

In the US, industrial production data for March is due out. Industrial production is quite volatile but both PMI and ISM manufacturing are signalling that expansion will continue.

Another set of Fed speakers is on the agenda today, including Williams (voter, neutral).

The IMF will publish its semi-annual World Economic Outlook today, containing its new global and country level economic projections.

Selected market news

Stock index futures trended up after S&P 500 closed 0.8% higher, as investors shift their focus to corporate results from geopolitical tension. However, President Trump has rediscovered the currency topic, tweeting yesterday that both Russia and China are playing an unfair devaluation game against the Americans. USD sold off on this and extended losses against most peers in Asian trading this morning, with EUR/USD trading at 1.238 at the time of writing. We do not think that China is keeping its currency artificially weak to gain a competitive advantage and neither does the US Treasury department in its latest currency report, where none of the US's primary trading partners were labelled a currency manipulator (see tweet ). Instead, we think the rhetoric is clearly linked to the ongoing trade dispute with China, where the next round of escalation could start this week (see also Flash Comment: Is Trump preparing for a round of trade escalation - again? ).

Last night it was made official that Trump is nominating Richard Clarida for Fed Vice Chair, succeeding Stanley Fisher, who stepped down in October. In our view, it is a good choice given Clarida's very strong background as he has done much research on monetary policy, served as Vice Treasury Secretary and has worked at a financial institution (PIMCO, one of the largest fixed income investment firms). Clarida still needs Senate approval before taking up the position. Based on Clarida's recent comments, he is likely to be a centrist supporting the current policy of gradual hikes (three to four hikes this year). While we think the Fed is on autopilot at the moment, it is good in the long run with a very skilled Vice Chair, as the Fed has lost a lot of human capital with Janet Yellen, Stanley Fischer and soon William Dudley leaving the FOMC. Besides Clarida, Trump has nominated Michelle Bowman for Fed Governor (also requiring Senate approval).

China Q1 GDP Came In In-Line And Higher Than Govt Target

General Trend:

- Asian equities trade mixed; HK and China property sectors remain weak

- Australia’s Bank of Queensland declines on weaker than expected H1 results

- China/US trade back in the spotlight as US acts against telecom ZTE

- China Q1 GDP in line, industrial production slows in March

- PBoC raises rate on 1-year medium-term lending facility (MLF)

- Reserve Bank of Australia (RBA) minutes reiterate more likely next rate move is up, no strong case for near term adjustment

- Hong Kong Monetary Authority (HKMA) steps up currency market interventions, HKD remains near weaker end of trading band

- Singapore March exports to China decline

- US said to be looking into sanctions against China tech firms, China Commerce dept bans US companies from supplying ZTE

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.2%; closed +0.1%

- TOPIX Retail Trade index +0.1%; Securities -1.1%, Iron & Steel -0.9%, Real Estate -0.9%, Electrical Appliances -0.3%

- (JP) Japan Cabinet Office (Gov’t) Monthly Economic Report for Apr: Maintains its overall assessment that economy was recovering at a moderate pace

- (JP) Japan MoF sells ¥2.0T v ¥2.0T indicated in 0.10% (prior 0.10%) 5-yr bonds; avg yield -0.1200% v -0.108% prior; bid to cover 4.40x v 4.18x prior

Korea

- Kospi opened +0.1%

- (KR) Policymakers and private economists have different opinions if South Korea will reach 3% GDP target in 2018; Most private research institutes expect the 2018 growth rate to hover below the government-set target of 3% - Korean press

- Samsung, 005930.KR Ministry of Trade, Industry and Energy: committee on the protection of industrial technologies failed to reach an agreement on whether to give chipmaking technologies protection as national core assets amid an ongoing dispute over the firm’s workplace safety

- (KR) North and South Korea said to discuss announcing end to military conflict – South Korean Press

China/Hong Kong

- Hang Seng opened +0.1%, Shanghai Composite +0.1%

- Hang Seng Industrial Goods index -1.3%, Consumer Goods -0.8%, Info Tech -0.8%, Property/Construction -0.5%, Telecom -0.4%, Financials -0.3%; Services +0.7%, Energy +0.3%

- Shanghai Property sub-index declines over 0.5%

- (CN) CHINA Q1 GDP Q/Q: 1.4% V 1.5%E; Y/Y: 6.8% V 6.8%E; YTD Y/Y: 6.8% V 6.8%E

- (CN) CHINA MAR INDUSTRIAL PRODUCTION Y/Y: 6.0% V 6.3%E; YTD Y/Y: 6.8% V 6.9%E

- (CN) CHINA MAR RETAIL SALES Y/Y: 10.1% V 9.7%E; YTD Y/Y: 9.8% V 9.7%E

- (CN) China Mar Urban Fixed Assets YTD y/y: 7.5% v 7.7%e

- (CN) China Stats Bureau (NBS): Q1 economic performance set good foundation for full year; china pursues balanced trade

- (CN) US Trade Rep said to be putting together new trade complaint against China over cloud computing and other high-tech services – press

- (HK) Hong Kong Monetary Authority (HKMA): See no need for any interest rate adjustment mechanism; no need for 'proactive' rate adjustment mechanism

- (HK) During Monday’s NY session, HKMA purchased additional HK$5.77B in local currency in order to keep HKD within trading band

- (CN) US Treasury Department Feb data shows China holdings of Treasuries rose $8.5B to $1.18T (biggest growth in 6-months)

- (CN) China President Xi: I am personally opposed to life-long rule, foreign observers have misinterpreted a recent constitutional amendment that revoked the two-term limit on the presidency

- ZTE, 763.HK (CN) China MOFCOM to keep a close watch on US order on ZTE, prepared to take necessary measures

- (CN) China PBoC sets yuan reference rate at 6.2771 v 6.2884 prior (2-week high)

- (CN) China PBoC Open Market Operation (OMO): skips OMO v injects CNY150B in 7-day and 14-day reverse repos prior

- (CN) PBOC CONDUCTS CNY367.5B IN 1-YR MLF AT 3.3% V 3.25% PRIOR

Australia/New Zealand

- ASX 200 opened flat

- ASX 200 Telecom index +0.7%, REIT +0.4%, Resources +0.3%; Utilities -0.5%, Financials -0.2%

- (NZ) New Zealand REINZ Mar House Sales Y/Y: -9.9% v +1.2% prior

- OZ Minerals, OZL.AU Reports Q1 copper production 27.5K tons v 25.1K y/y; Affirms all production for FY18 and FY19

- (NZ) IMF comments: NZ Current monetary policy is appropriately expansionary; doubts that New Zealand foreign buyer ban will help housing market

- (AU) Reserve Bank of Australia (RBA) Minutes of April 2018 Monetary Policy Meeting: Reiterates more likely next rate move is up than down, but sees no strong case for near term adjustment

Other Asia

- (SG) Singapore Mar Non-Oil Domestic Exports M/M: -1.8% v +2.4%e; Y/Y: -2.7% v +1.2%e; Electronic Exports Y/Y: -7.1% v -12.3% prior

- (PH) Philippines sells PHP10B in 10-year bonds; Avg Yield: 6.213% (highest since Jun 2011) v 6.184% prior; bid-to-cover: 1.73x

North America

- US equity markets ended higher: Dow +0.9%, S&P500 +0.8%, Nasdaq +0.7%, Russell 2000 +0.9%

- S&P500 Utilities +1.4%, Materials +1.3%

- (MX) Mexico President front runner Lopez Obrador Fin Min pick Urzua: Pledges 'free floating' Peso currency (MXN)

- Tesla TSLA Said to be temporarily shutting down production of the 'Model 3'; The company points to prior statements and says the rampup of the Model 3 includes planned factory downtime to address bottlenecks.

- Whirlpool WHR Raises dividend 4.5% to $1.15 from $1.10 (indicated yield 3%)

- (US) Fed's Dudley (dove, FOMC voter): 3 or 4 hikes this year seem like a reasonable number; more than 4 hikes would no longer be moving at a gradual tightening pace; 3% is reasonable starting point for neutral rate policy - CNBC interview

- (US) Fed's Kaplan (dove, non-voter): Near term outlook looks solid, but underlying trends are concerning

- (US) Fed's Kashkari (dove, non-voter): Main Street hasn't fully recovered from the financial crisis

- (US) Pres Trump to nominate Richard Clarida as Fed Vice Chair and Kansas banking regulator Michelle Bowman to Fed Board - press

Europe

- (EU) ECB's Praet (Belgium): an ample amount of monetary stimulus remains necessary

- (EU) EU demands talks with US at WTO, asking for compensation over US steel & aluminum tariffs - press

- (DE) Germany Fin Min Scholz: Germany will maintain its budget without new borrowing

- (RU) Pres Trump reportedly halts plan to implement new sanctions on Russia - Wash Post

- GBP/USD Pound (GBP) trades above $1.4346, highest since June 2016 Brexit vote; Up less than 0.10% on session

Levels as of 02:00ET

- Hang Seng -0.4%; Shanghai Composite -0.7%; Kospi -0.2%; ASX 200 +0.1%

- Equity Futures: S&P500 +0.4%; Nasdaq100 +0.3%, Dax +0.4%; FTSE100 +0.2%

- EUR 1.2388-1.2376; JPY 107.16-106.97; AUD 0.7787-0.7760;NZD 0.7372-0.7339

- Jun Gold -0.2% at $1,347/oz; May Crude Oil +0.5% at $66.52/brl; May Copper +0.2% at $3.09/lb

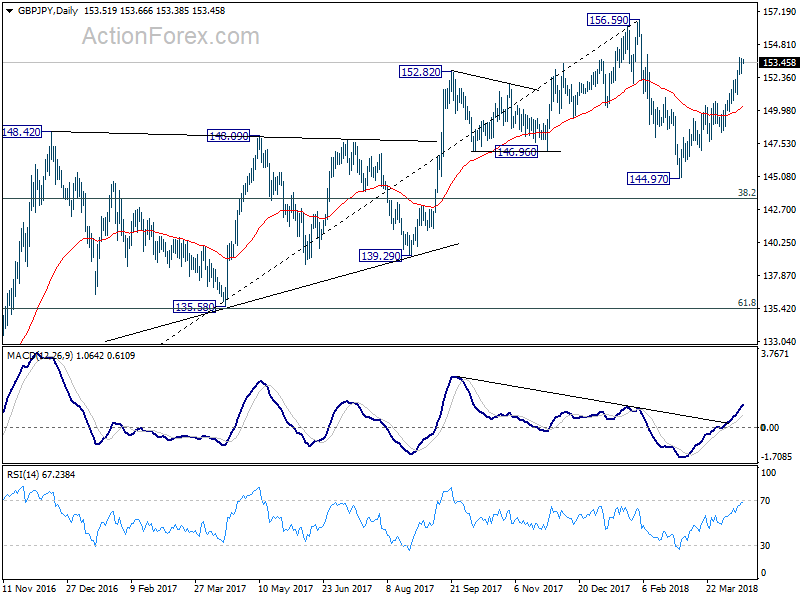

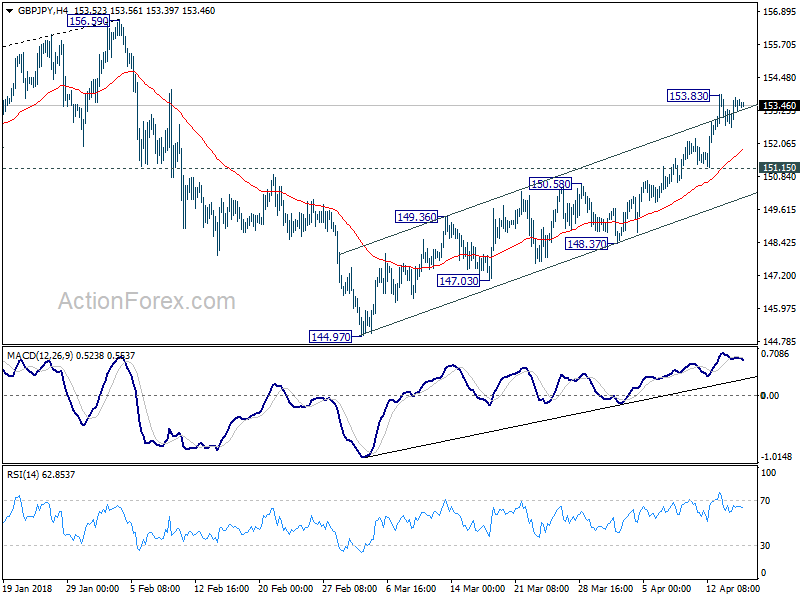

GBP/JPY Daily Outlook

Daily Pivots: (S1) 152.89; (P) 153.32; (R1) 154.00; More...

GBP/JPY is staying in consolidation below 153.83 temporary top and intraday bias remains neutral first. In case of another retreat, downside should be contained by 151.15 minor support to bring rise resumption. Above 153.83 will extend the rally from 144.97 and target to retest 156.96 high. However, break of 151.15 will suggest that such rebound from 144.97 has completed and bring retest of this support.

In the bigger picture, price actions from 156.59 are viewed as a corrective pattern. For now, we'd expect at least one more fall for 38.2% retracement of 122.36 to 156.59 at 143.51 before the consolidation completed. Though, firm break of 156.59 will resume whole up trend from 122.36 (2016 low) to 50% retracement of 195.86 (2015high) to 122.36 at 159.11 next.

In the bigger picture, price actions from 156.59 are viewed as a corrective pattern. For now, we'd expect at least one more fall for 38.2% retracement of 122.36 to 156.59 at 143.51 before the consolidation completed. Though, firm break of 156.59 will resume whole up trend from 122.36 (2016 low) to 50% retracement of 195.86 (2015high) to 122.36 at 159.11 next.