Sample Category Title

Sterling Rallies Ahead Of Crucial Economic Data

Here are the latest developments in global markets:

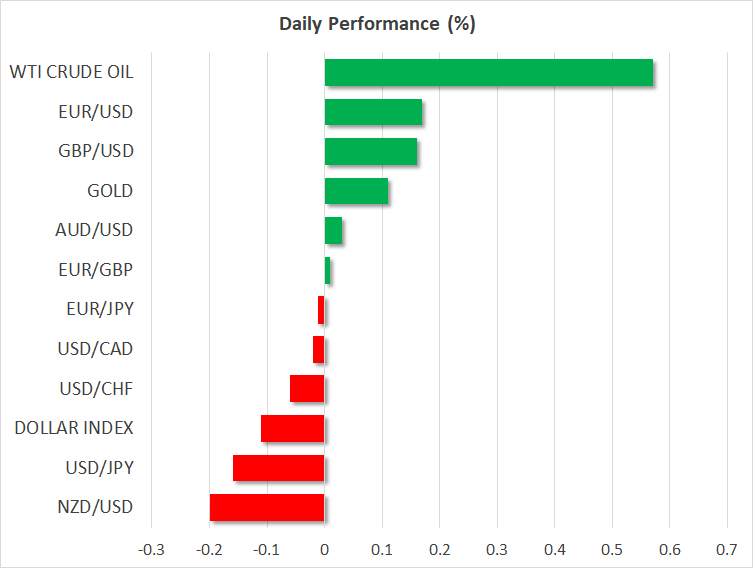

FOREX: The US dollar index was 0.1% lower on Tuesday, extending the losses it posted yesterday amid renewed speculation that the US administration is seeking a weaker currency. Sterling/dollar traded 0.15% higher today after surging yesterday as well, reaching a fresh high last seen in June 2016, amid speculation that upcoming UK economic data will “green light” a rate hike by the Bank of England in May.

STOCKS: US markets closed higher yesterday, buoyed by a decline in geopolitical risks, as the US-led strike in Syria was seen as being an isolated, contained incident that will not escalate any further. The Dow Jones led the pack, gaining nearly 0.9%, while the S&P 500 and the Nasdaq Composite rose by 0.8% and 0.7% respectively. The recovery looks set to continue today, as futures tracking the Dow, S&P and Nasdaq 100 are all pointing to a higher open. In Asia, most of the major benchmarks traded lower. In Japan, the Nikkei 225 closed practically flat, while the Topix fell by 0.36%. In Hong Kong, the Hang Seng slipped 0.37% as China’s GDP data for Q1 were a touch softer than expected. In Europe, futures tracking all the major indices were flashing green.

COMMODITIES: Oil prices rose on Tuesday, with WTI and Brent crude climbing by nearly 0.6% and 0.5% respectively. There was no clear fundamental trigger behind the recovery, with market chatter attributing it to lingering concerns over potential supply disruptions, most notably in Iran in case of new sanctions, and in Venezuela that has experienced a sharp drop in production. Today, oil traders will turn their sights to the private API crude inventory data, ahead of the official EIA figures tomorrow. In precious metals, gold was trading 0.1% higher today, last seen near the $1347/ounce mark. The dollar-denominated safe haven struggled to advance yesterday amid a risk-on environment, even despite a drop in the US dollar.

Major movers: Sterling comes back in fashion, dollar softens despite decent data

The British pound staged an impressive rally yesterday, that seems to be continuing today. Against the dollar, sterling reached fresh highs last seen in June 2016, without any clear fundamental catalyst behind the move. A reasonable explanation for the surge is investors adding to their long-GBP positions in anticipation of strong UK economic data this week. The nation will release its jobs figures today, followed by inflation numbers tomorrow and retail sales on Thursday. Markets currently see a 72% probability for the Bank of England (BoE) to hike rates in May and an overall strong set of data could seal the deal for such an action, at least from the market’s perspective, and thereby boost sterling. Conversely, a soft set of prints could generate doubts about a May hike, leading to profit-taking in the pound.

The dollar was trading on a soft note yesterday, unable to draw support from the slightly-stronger-than-expected US retail sales for March. The currency’s underperformance may be related to a tweet by US President Trump yesterday, in which he accused China and Russia of being currency manipulators, even though the US Treasury did not label them as such in its latest report. The tweet was seen as reinforcing earlier rhetoric from the White House favoring a weaker US dollar. In other news, President Trump nominated Richard Clarida for Fed Vice Chair, a former Vice Treasury Secretary and a managing director at investment firm PIMCO.

Elsewhere, the loonie is practically flat against the dollar today, after gaining ground yesterday amid the broader risk-on market sentiment. Some signs of progress in the NAFTA talks may have helped as well. Mexico’s Economy Minister noted on Monday that several chapters of a deal were now virtually settled, and that the three sides may meet again on Thursday as they push for a swift settlement.

Day ahead: UK wage growth and employment figures, German ZEW and US housing data on the agenda

Important releases out of the UK might attract the lion’s share of attention during today’s trading, especially in light of sterling trading at elevated levels at the moment relative to other major currencies.

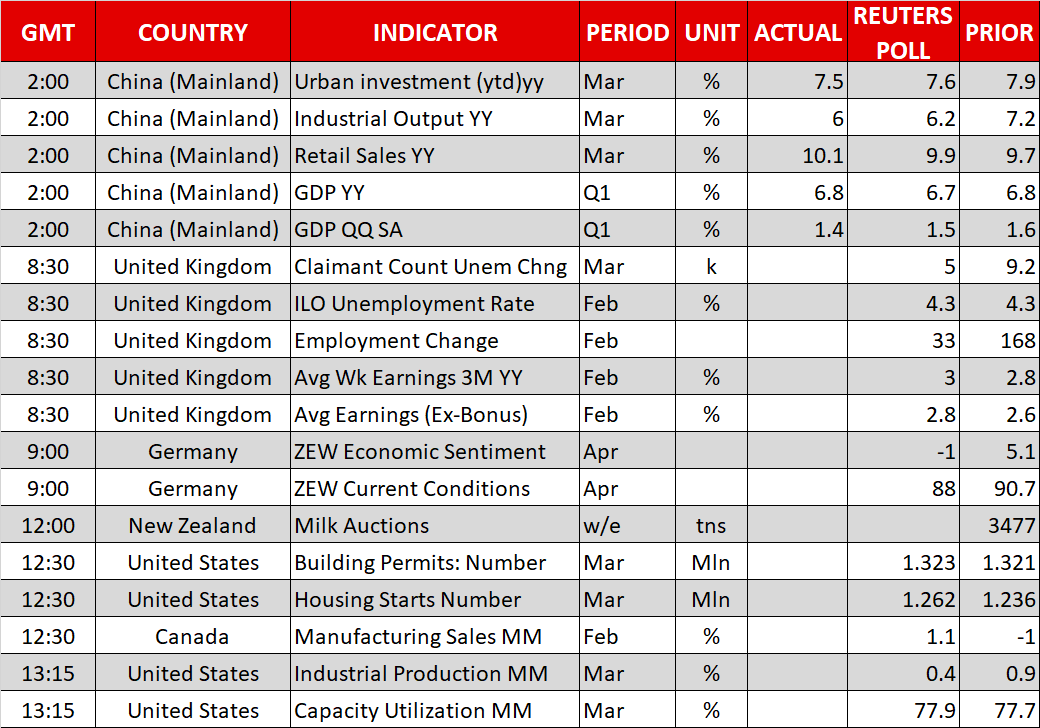

UK data on employment and wage growth will be made public at 0830 GMT. Average weekly earnings, both including and excluding bonuses, are anticipated to have accelerated in February, rising by 3.0% and 2.8% correspondingly on an annual basis. Should the figures materialize, in conjunction with inflation readings coming in as expected on Wednesday, this would push real income growth back into positive territory (i.e. wage growth would exceed price increases). Such an outcome is likely to more conclusively put on the table a May rate hike by the Bank of England and consequently provide an additional boost to the British currency. The odds of an interest rate increase currently stand at 72% according to UK overnight index swaps. Elsewhere, the unemployment rate is projected to remain at the multi-decade low of 4.3%.

Germany, the euro area’s largest economy, will see the release of the ZEW institute’s surveys on economic sentiment – a measure gauging the outlook – and current conditions at 0900 GMT. The two business confidence gauges declined in the two months that preceded, with the economic sentiment index falling to its lowest since September 2016 in March – rising trade risks were cited as reasons for the tumble. A further decline is projected for the two measures in April.

At 1230 GMT, the number of building permits and housing starts for the month of March will be made public out of the US, while Canadian manufacturing sales for February are scheduled for release as well. A few minutes later (at 1315 GMT), the US will be on the receiving end of industrial production figures for March. Manufacturing output, a subset of industrial production, will also be generating interest. Data on capacity utilization will be released at the same time.

Kiwi pairs could face volatility as the outcome of the bi-weekly milk auction is made public later today; dairy products are New Zealand’s largest goods export earner. The relevant print lacks a specific time of release, with most calendars having it slated for 1200 GMT.

Oil traders will be paying attention to API’s weekly report on crude stockpiles due at 2030 GMT.

Some of the big names releasing quarterly results on Tuesday are Goldman Sachs and Johnson & Johnson; both companies’ reports will be made public before the US market open.

Fed policymakers John Williams (voter), Randal Quarles (permanent-voter) and Patrick Harker (non-voter) will be making appearances today at 1315 GMT, 1400 GMT and 1500 GMT respectively. Also of interest in terms of policymakers’ appearances might be a news conference by German Finance Minister Olaf Scholz during which he could touch on the trade dispute between the US and the EU.

In politics, US President Donald Trump will be meeting Japanese Prime Minister Shinzo Abe on Tuesday; discussions are scheduled to continue tomorrow. Developments on the Korean peninsula and trade issues are likely to be discussed.

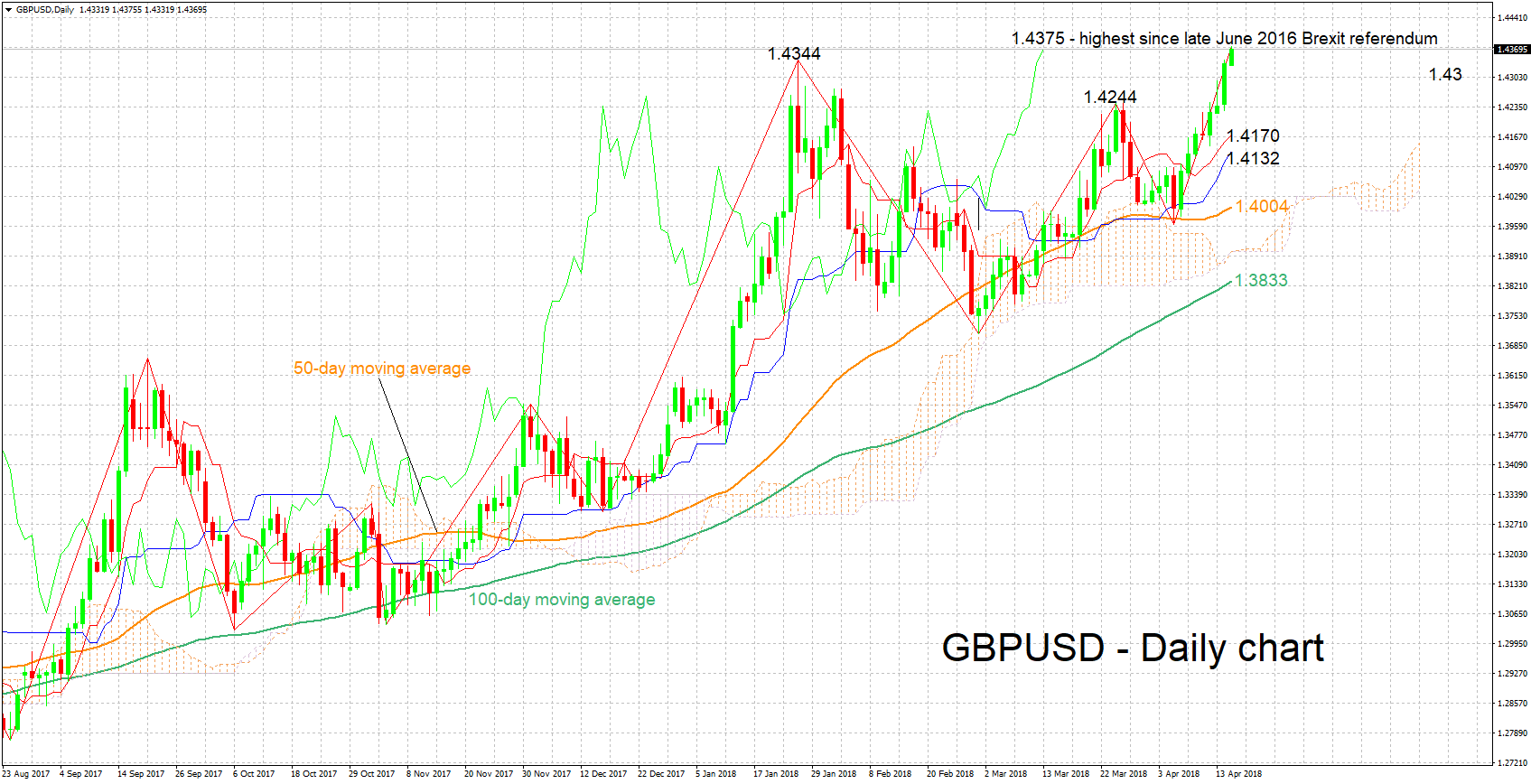

Technical Analysis: GBPUSD at highest since June 2016; possibly overbought

GBPUSD is rising for the fourth straight day, having reached 1.4375 earlier on Tuesday, its highest since the late June 2016 Brexit referendum; price action is currently close to this level. The Tenkan- and Kijun-sen lines are positively aligned in support of a bullish short-term picture, though the Chikou Span might be signaling an overbought market.

Stronger-than-expected UK data are anticipated to be met with gains in GBPUSD, with resistance potentially coming at the 1.44 and 1.45 round figures.

On the downside and in case of disappointing figures, support could be met around the 1.43 handle that may also hold psychological importance, and further below near the area of 1.4244, this being a peak from the recent past.

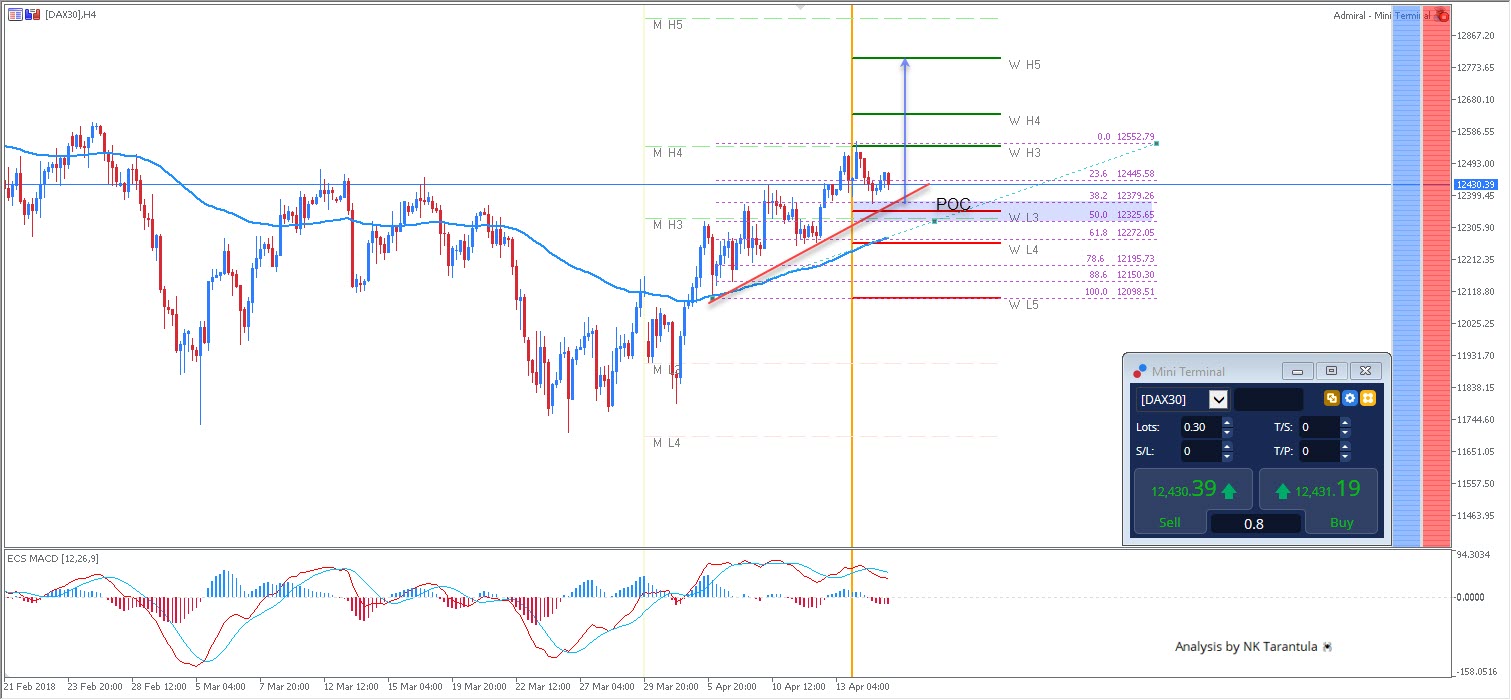

DAX30 Ascending Trend Line At Fibonacci 50.0 Retracement

US retail sales overnight exceeded expectations, and in particular car sales were higher in the US, which is good news for Dax30 car exporters. European Equities have been a little bit under pressure as the EUR continues to gain strength, making their exports more expensive. Monthly trend is still intact, with the price still finding support to the upside, and therefore we might expect some support at the POC zone. US Equities continue to climb, and with the positive correlation than should improve the Dax30 chances to continue higher. Be mindful of the POC zone especially W L3 - 50% Fib at 12325-79 zone. If the price spikes 12550 and 12633 are targets. Only a clear 4h close above 12633 should target 12800.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

M H4 - Monthly Camarilla Pivot (Very Strong Monthly Resistance)

M L3 – Monthly Camarilla Pivot (Monthly Support)

M L4 – Monthly H4 Camarilla (Very Strong Monthly Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

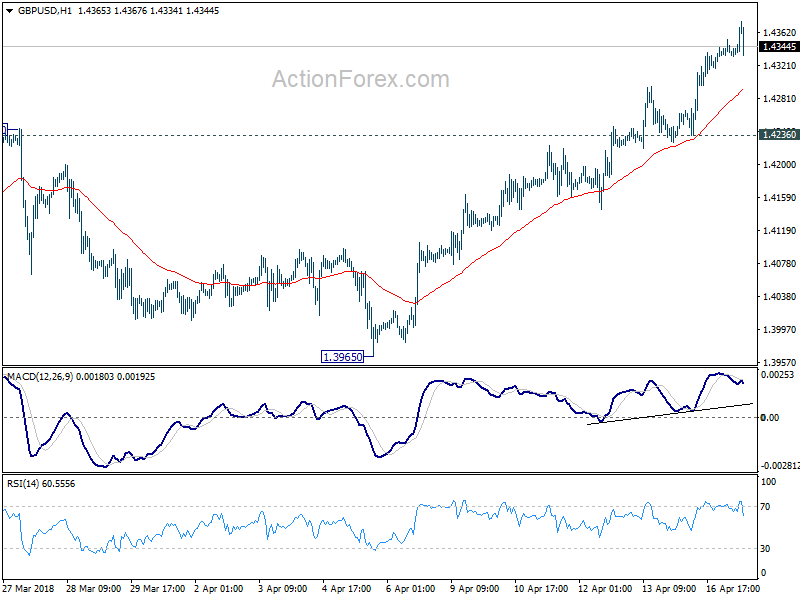

UK wage growth disappoints, caps GBP gains

UK unemployment rate dropped to 4.2% in February, down from 4.3% and beat expectation of 4.3%. That's also the lowest level since 1975.

Employment also rose to a record high between December and February, adding 55k jobs.

However, average weekly earnings grew only 2.8% 3moy, unchanged from January's reading. That's a disappointing to markets who expected 3.0% 3moy growth.

GBPUSD clearly pares back some gains after the release.

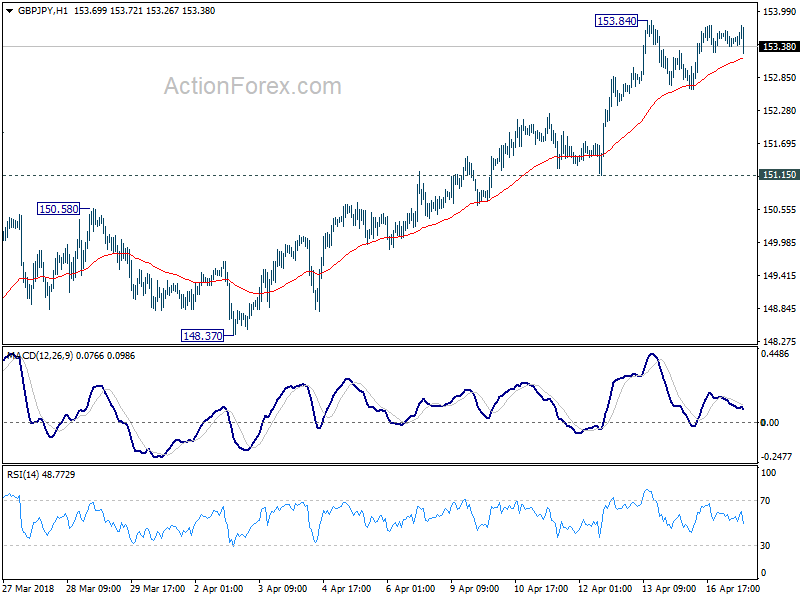

GBPJPY continues to be held below 153.84 temporary top.

GBPJPY continues to be held below 153.84 temporary top.

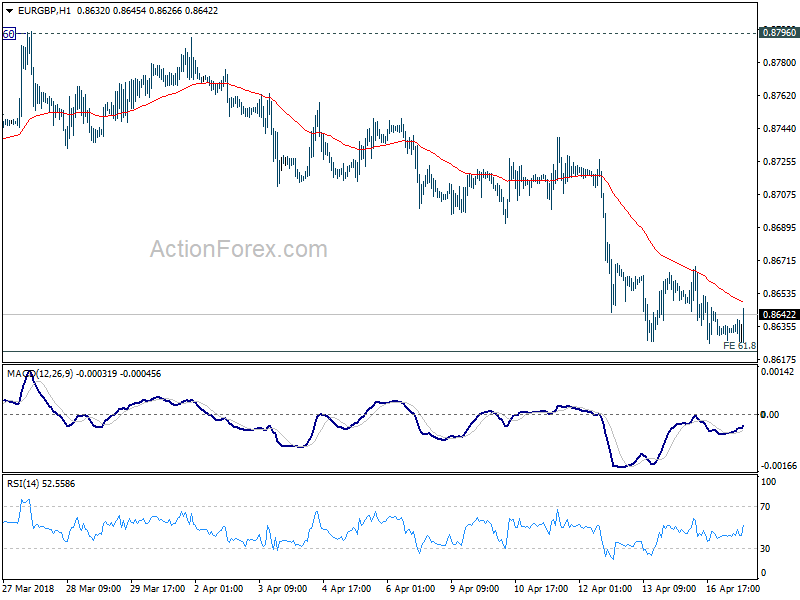

EURGBP also recovers as bounded in tight range.

EURGBP also recovers as bounded in tight range.

GBP bulls will probably need to wait for tomorrow's CPI before making another strike.

GBP bulls will probably need to wait for tomorrow's CPI before making another strike.

Currencies: Dollar Stays In The Defensive

Rates: Consolidation on core bond markets continues

Risk sentiment and speeches by Fed governors will probably set the tone for today's trading session. Fed governors are expected to keep the scenario of at least 2 additional rate hikes this year alive. We have a minor downward bias for core bonds today, but within the established sideways consolidation ranges.

Currencies: Dollar stays in the defensive

Geopolitical tensions eased yesterday. US equities outperformed and US yields rose slightly. However, it couldn't help the dollar. A mercantile approach of US president Trump supports the view that the US likes a weaker dollar. Focus for USD trading is on Fed's Williams' assessment today. Sterling traders will keep a close eye at the UK labour data.

The Sunrise Headlines

- US stock markets outperformed yesterday, closing up to 0.8% higher. Netflix reported strong Q1 earnings after the close, putting US equity futures in the green overnight. Asian equity indices are mixed with China underperforming.

- US President Trump revealed his latest picks to fill empty seats on the Fed Board, saying he would nominate Columbia University economist Clarida as vice chairman and Kansas banking regulator Bowman as a governor. (WSJ)

- China's economic expansion held up in Q1 (6.8% Y/Y) amid robust consumer spending (10.1% Y/Y), underpinning global growth, while the industrial sector showed signs of modest slowdown (6% Y/Y).

- The Washington Post reports that President Trump pit the brakes on a preliminary plan to impose additional economic sanctions on Russia, walking back a Sunday announcement by US Ambassador to the UN Haley.

- China's holdings of US Treasuries rose in February, as net new foreign purchases increased to their largest since May 2017, data from the Treasury Department showed.

- Australia's central bank saw scant reason to raise interest rates this month given inflation remained below target and likely to remain subdued in the face of sluggish wage growth. (Reuters)

- Today's eco calendar contains German ZEW investor confidence, US housing starts, building permits and industrial production. Fed governors Williams, Quarles, Harker, Evans and Bostic are scheduled to speak

Currencies: Dollar Stays In The Defensive

US dollar stays in the defensive

The easing of geopolitical tensions had an uneven impact on markets. Core yields initially rose a few basis points. Equities traded mixed with the US outperforming. US retail sales were close to expectations, being not strong enough to support the dollar. At the same time, US president Trump accused Russia and China to play a 'currency devaluation game'. The Trump headlines weighed on the dollar, giving the impression that the US likes a weaker dollar. EUR/USD jumped to just below 1.24 and closed at 1.2380. USD/JPY finished at 107.12, near the intraday lows, despite a decent US equity performance and (slightly) higher US yields.

Overnight, Chinese Q1 GDP printed close to expectations (6.8% Y/Y). Retail sales were good. Industrial production disappointed slightly. The data didn't prevent a further underperformance of Chinese equities. The dollar remains in the defensive (USD/JPY near 107, EUR/USD 1.2385). The Aussie dollar dropped from 0.7790 to the 0.7765 area as the RBA in the Minutes saw no reason for an interest rate hike in the near future.

Today, German ZEW investor sentiment is expected to ease further, confirming the easing in other EMU sentiment indicators. This might be a slightly negative for the euro. US housing data are expected to recover modestly. March production is expected soft (0.3% M/M). However, the focus in US dealings will be on Fed speeches, especially of Fed Williams and on corporate earnings. Williams will probably keep the door open for a total of four rate hikes this year. Of late the dollar showed an inconvincing picture. USD/EUR and USD/JPY held slightly above recent/ cycle lows, but didn't profit from potentially USD supportive news, including higher US yields/interest rate differentials. This pattern might continue today. Fed speakers remain a wildcard. However, there is little reason to expect the dollar to start a real upleg. EUR/USD is perfectly holding in the 1.2155/1.2550 consolidation pattern.

Yesterday, sterling preserved last week's gains, also against a rather strong euro. The EUR/GBP 0.8650 support remained under intense pressure. Today, the UK labour market data will be published. Average weekly earnings are expected to rise to 3.0%. Positive real wage growth might support the case for more than one BoE rate hike this year. In a longer term perspective, we assume that enough good news on Brexit is discounted for now. However, good eco data and the prospect of further BoE rate hikes might keep sterling supported short-term. 0.8541 is the next intermediate support. 0.8305 is key.

EUR/USD:drifting higher in the established range as USD doubts persist

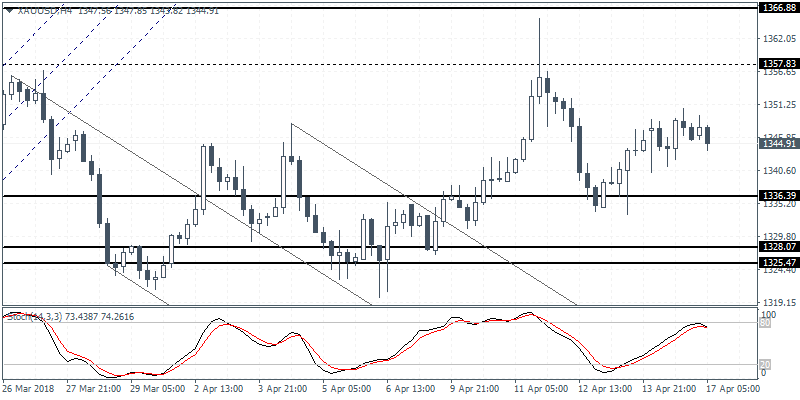

XAUUSD Intraday Analysis

XAUUSD (1344.91): Gold prices were seen easing back after initially rising on the day on Monday. Price action is seen retreating following the brief rally to 1347 level. The downside momentum could push gold prices to test the old support level at 1336. To the upside, gold prices will have to post a higher high above the recent highs near 1347. This will put the previous resistance level at 1357 back into target to the upside.

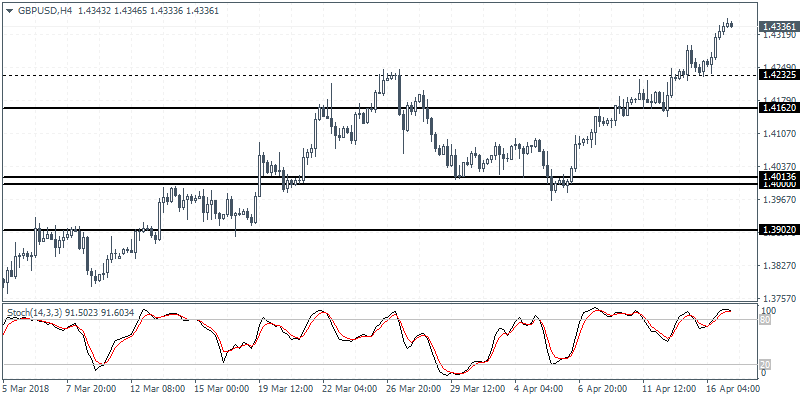

GBPUSD Intraday Analysis

GBPUSD (1.4336): The British pound posted strong gains with price action rallying to fresh highs of 1.435 earlier today. The gains come ahead of today's jobs report where expectations are high that wage growth increased strongly in the three months ending March. We expect to see some near term correction in prices as GBPUSD is likely to retest the support level at 1.4232. A rebound off this level could keep the bullish momentum supported for further gains.

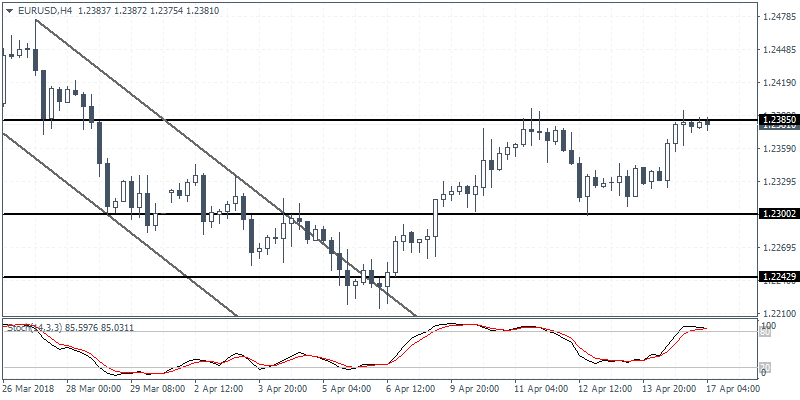

EURUSD Intraday Analysis

EURUSD (1.2381): The EURUSD was bullish on Monday with price action rallying to test the resistance level at 1.2400 briefly before pulling back. The retest to this resistance level could once again see some downside momentum in price action. With the EURUSD trading sideways within 1.2400 and 1.2300, further gains can be expected only on a breakout above 1.2400. To the downside, we expect the declines to be limited to the support level at 1.2300.

Markets Shrug Geo-Politics, UK Jobs Data Awaited

The markets opened on Monday shrugging aside the weekend news on the targeted air strikes by the U.S. and its allies on Syria. Lack of response from Russian authorities saw the markets gaining risk appetite.

On the economic front, the day was relatively quiet. U.S. retail sales report released showed a 0.6% jump in retail sales on the month in March. This beat analysts’ forecasts of a 0.4% increase. Core retail sales excluding autos and gasoline sales rose 0.2% on the month as expected. Other data during the day included the U.S. Empire State Manufacturing index which fell to 15.8 missing forecasts of 19.8 and easing sharply from 22.5 that was seen previously.

Looking ahead, the economic data today will see the release of the UK jobs report. The unemployment rate is expected to remain steady at 4.3% while wage growth is expected to accelerate. Later in the week, the UK's inflation report will be released which will show if wage growth has managed to catch up with the strong pace of inflation increase.

In the NY trading session, the building permits data will be coming out alongside the industrial production figures. FOMC members, Williams, Bostic and Quarles are expected to speak later in the day.

UK Earnings Data To Show An Increase In Consumer Inflation

At 08:30 GMT, UK Average Earnings excluding Bonus (3Mo/Yr) (Feb) is expected to come in at 2.8% from 2.6% previously. Claimant Count Change (Mar) is expected at 5.0K from a previous reading of 9.2K. ILO Unemployment Rate (3M) (Feb) is expected to be unchanged at 4.3%. Average Earnings including Bonus (3Mo/Yr) (Feb) is expected to be 3.0% from 2.8% previously. Claimant Count Rate (Mar) was 2.4% previously. Wage growth is expected to continue to tick up, after stabilizing at 2.5% and moving up last month. This is despite the fact that the unemployment rate is at multi-decade lows when wage growth would normally be higher as competition to attract workers takes hold. The BOE will study wage data to see any indication of a pick up so they know whether to maintain their hawkish tone. GBP crosses could be influenced by this data release.

At 09:00 GMT, German ZEW Survey – Current Situation (Apr) is expected at 88.0 against a prior 90.7. ZEW Survey – Economic Sentiment (Mar) is expected to be -1.0 from 5.1 previously. These data points are expected to soften as the strengthening in the Euro affects business. The deteriorating trade environment is also a headwind for business outlook. This is the first negative forecast in sentiment since Brexit. EUR crosses may be affected by this data.

At 12:30 GMT, US Housing Starts (MoM) (Mar) is expected at 1.262M from a previous number of 1.236M. Building Permits (MoM) (Mar) is expected to come in at 1.323M with the prior reading of 1.298M, which was revised up to 1.321M. This data is expected to show a pick-up in residential construction activity as the weather improves and summer approaches. These data points have been recovering since hitting lows of 0.46M and 0.49M respectively in 2009 after the financial crisis. The readings last month were the highest since those lows. USD crosses may see increased volatility around this data release.

At 13:15 GMT, FOMC Member Williams is due to speak about monetary policy at a global symposium co-hosted by the National Association for Business Economics and the Bank of Spain, in Madrid. Audience questions are expected and comments made could affect USD pairs.

At 13:15 GMT, US Industrial Production (MoM) (Mar) will be released. The consensus is for 0.4% from 0.9% previously, which was revised down from 1.1%. This measure rebounded strongly to reach the highest reading since December 2014, after slipping below the zero line in the previous reading. Capacity Utilization (Mar) will also be released at this time, with an expectation for 77.9% v 77.7% prior, which was revised down from 78.1%. The expectation is for the number to match the two-year high in December. USD crosses may be impacted.

At 14:00 GMT, Fed Member Quarles is due to testify on supervision and regulation before the House Financial Services Committee, in Washington DC. USD crosses may be impacted by any comments made.

At 15:00 GMT, FOMC Member Harker is due to give a scheduled speech. USD pairs may move on the back of statements made.

At 21:40 GMT, FOMC Member Bostic is due to discuss the economic outlook in an interview conducted by Bloomberg at an executive workshop, in Atlanta. USD pairs may be affected by comments made during this interview or during audience question after.

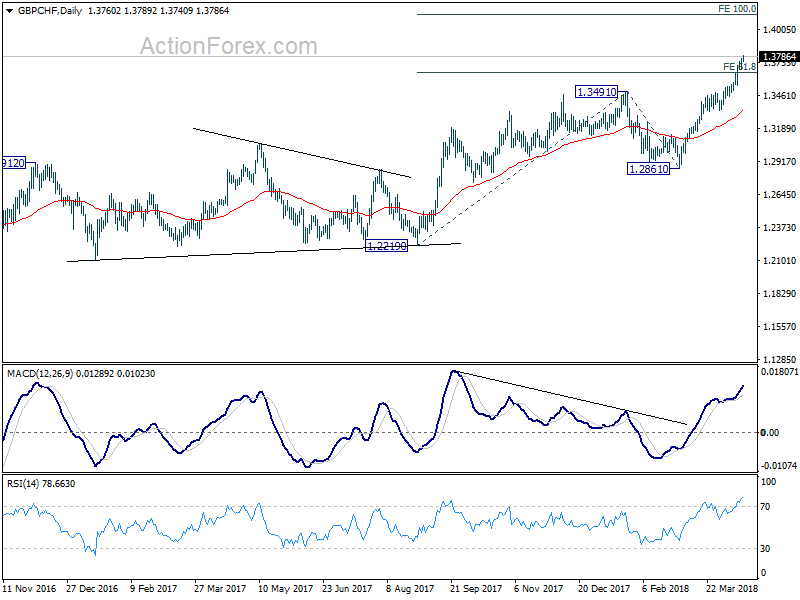

GBPCHF in solid up trend as UK wage growth awaited

Revisiting GBP/CHF that we covered here last week. The strong up trend continues as seen in the action bias table.

It's also apparent in the D action bias chart that momentum is very solid.

It's also apparent in the D action bias chart that momentum is very solid.

Now that 61.8% projection of 1.2219 to 1.3419 from 1.2861 at 1.3647 is firmly taken out, next upside target will be 100% projection at 1.4133.

Now that 61.8% projection of 1.2219 to 1.3419 from 1.2861 at 1.3647 is firmly taken out, next upside target will be 100% projection at 1.4133.

The path will be subject to the job and inflation data to be released today and tomorrow. Market expect today's data to show average weekly earnings growth accelerating from 2.8% 3moy to 3.0% 3moy. Headline CPI to be released tomorrow is expected to be unchanged at 2.7% yoy, while core CPI is expected to accelerate to 2.5% yoy.

The path will be subject to the job and inflation data to be released today and tomorrow. Market expect today's data to show average weekly earnings growth accelerating from 2.8% 3moy to 3.0% 3moy. Headline CPI to be released tomorrow is expected to be unchanged at 2.7% yoy, while core CPI is expected to accelerate to 2.5% yoy.

Meeting these expectations will solidify the case for BoE to raise the Bank rate again in May. And the chance of another hike in November would increased too. Missing these expectation might trigger some rethink of the BoE expectations. That could trigger a setback in GBP/CHF's rally. But the setback should be temporary even in that case, as BoE is still on it's tightening path. It's just about the pace.