Sample Category Title

Boston Fed Rosengren: Somewhat more tightening may end up being needed

Boston Fed President Eric Rosengren sounded hawkish in his comments today. Referring to Fed's projection of two more hikes this year, Rosengren said that "somewhat more tightening may end up being needed". He expected a "somewhat stronger" economy ahead than the already "quite positive" FOMC projections. He also pointed to solid performance in job creation, falling unemployment and inflation close to Fed's 2% target.

However, Rosengren also pointed out short-run and long-run risks to the positive outlook.

For the short run risks, he pointed to trade tension. He noted that "it would take a significantly broader set of trade actions than those reported to date to materially reduce the roughly $2.4 trillion in annual U.S. exports." But still "spillover effects are possible."

Another run risk is an overheated "boom-bust" scenario. Particularly, "periods in which unemployment dipped significantly and persistently below the estimated natural rate historically have tended to generate conditions that resulted in a recession."

In the long run, he expressed his concern regarding the narrowing of fiscal and monetary buffers. He said "by using up so much fiscal capacity now – by which I mean the ability to lower tax rates or boost federal spending to offset economic weakness – the country risks not having sufficient fiscal capacity in the future when it might be needed."

There would be also be little room for monetary policy to respond to a large adverse shocks considering the median forecast among FOMC members for longer-run interest rates is 2.9 percent – "quite low" by historical standards

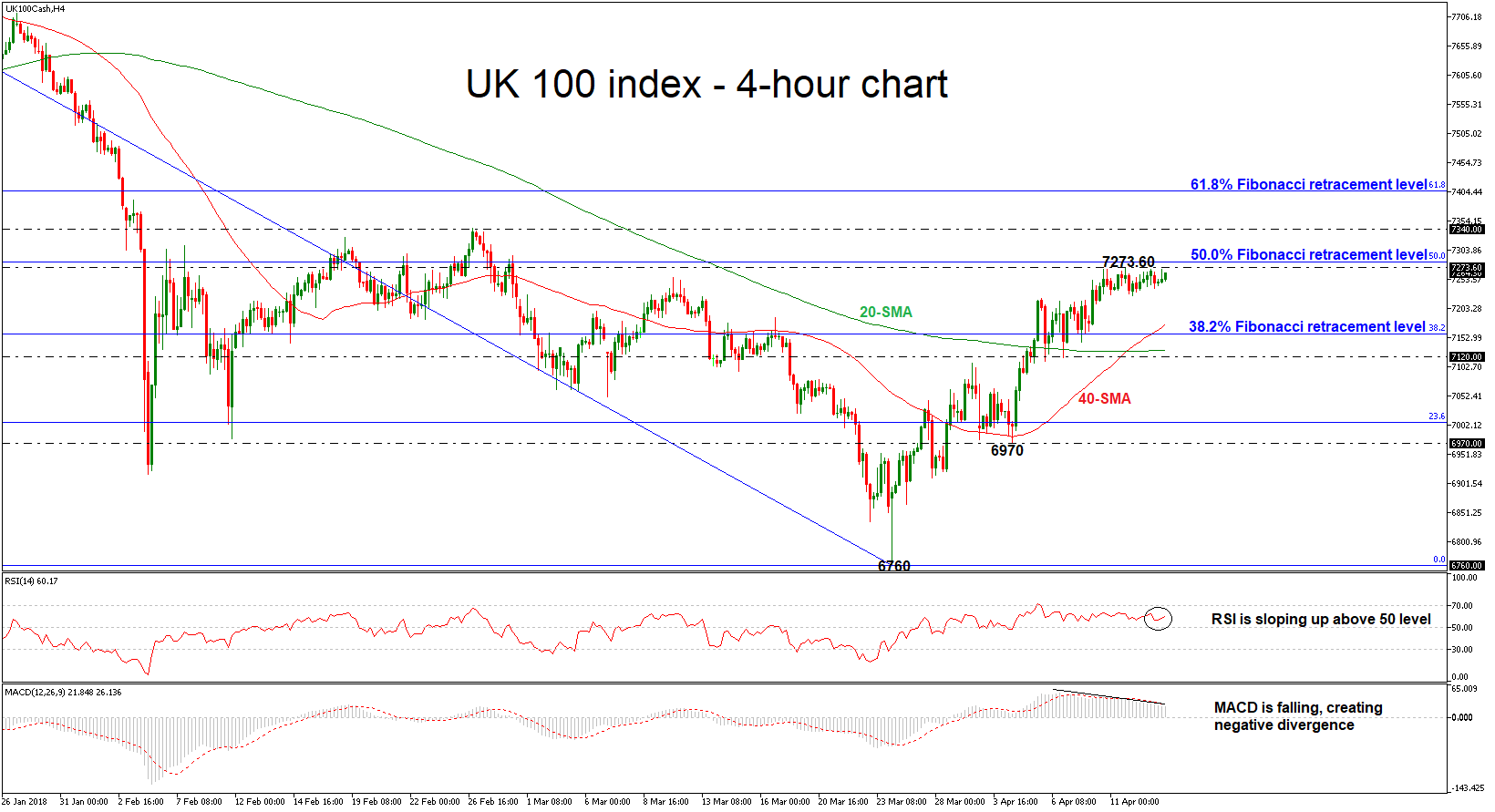

UK 100 Index is Stuck Below 50.0% Fibonacci Level Following Bullish Rally from 6760

UK 100 index has reversed back up again after finding support at the 16-month low of 6760. The index is on track to record a third green week, however, looking at the 4-hour chart, the price is stuck below the 50.0% Fibonacci retracement level of the downleg from 7806 to 6760. The technical picture supports that the range bound is likely to continue in the short-term.

Technically, the momentum indicators are holding in the positive territory with weak momentum. The RSI indicator is moving slightly to the upside, however, the MACD oscillator is falling below its trigger line, creating negative divergence and signaling for a possible downside correction.

If the price surpasses the 7273.60 resistance level and jumps above the 50.0% Fibonacci, this would reinforce the bullish view and open the way towards the 7340 barrier. Above this level, the next target could come at the 61.8% Fibonacci mark of 7406, posting a new two-month high.

On the flip side, if the bears take back control, the bullish rally may stall initially near the latest highs and turn negative. In such a case, the next immediate support comes from the 38.2% Fibonacci near 7160, which stands near the 40-simple moving average (SMA) in the 4-hour chart. A potential downside violation of this barrier would raise the likelihood of more declines towards 7120 taken from the lows on April 6.

Gold Pauses After Plunge, Consumer Confidence Ahead

Gold has edged higher in the Friday session, after sharp losses in Thursday trade. In the North American session, the spot price for an ounce of gold is $1338.02, up 0.22% on the day. In economic news, the US releases UoM Consumer Sentiment, which is expected to soften to 100.6 points. On the employment front, JOLTS Jobs Openings is expected to fall to 6.11 million.

It’s been a roller-coaster ride for gold over the past two days. Gold prices slumped 1.3% on Thursday, after gains of 1.0% on Wednesday. The volatility is closely connected to escalating tensions in the Middle East. The US has threatened to attack Syria for an alleged chemical attack on the weekend, but Russia has promised it will shoot down any US missiles aimed at Syria. President Trump had vowed that a strike was imminent, but has since backtracked, to the relief of the markets. Still, Trump is unpredictable, and if the US carries out a military strike, panicky investors could snap up safe-haven gold. Meanwhile, a fact-finding team from the Organization for the Prohibition of Chemical Weapons has arrived in Syria to attempt to verify if a chemical attack did indeed take place.

The Federal Reserve minutes had a generally hawkish tone, reflective of a solid US economy. All of the Fed policymakers indicated that the US economy would continue to improve and that inflation would rise in the next few months. At the March meeting, the Fed unanimously voted to raise rates by a quarter-point, bringing the benchmark rate to a range between 1.50% and 1.75%. The Fed projection for rate policy in 2018 remains at three hikes, although there is speculation that the Fed could revise the forecast to four rate hikes. Last week, Fed Chair Jerome Powell said that the Fed would likely continue to raise rates in order to keep a lid on inflation, but added that the rate moves would be gradual. A new headache for the Fed is the escalating trade battle between the US and China, which could hurt the economy and raise consumer prices. As for the next two rate meetings, the markets expect Powell & Co. to sit tight in May and raise rates at the June meeting.

Canadian Dollar Edges Higher, US Consumer Confidence Next

The Canadian dollar continues to trade quietly. Currently, USD/CAD is trading at 1.2563, down 0.22% on the day. In economic news, it’s a quiet end to the week. The US releases UoM Consumer Sentiment, which is expected to soften to 100.6 points. We’ll also get a look at JOLTS Jobs Openings, which is forecast to fall to 6.11 million. There are no Canadian events on the schedule.

The Canadian dollar has looked sharp in the month of April, posting gains of 2.5 percent. However, there could be some headwinds around the corner, as the US has threatened to attack Syria for an alleged chemical attack on the weekend. The situation has become further complicated as Russia has promised it will shoot down any US missiles aimed at Syria. President Trump had vowed that a strike was imminent, but has since backtracked, to the relief of the markets. Still, Trump is unpredictable, and if the US carries out a military strike, panicky investors could dump minor currencies such as the Canadian dollar. Meanwhile, a fact-finding team from the Organization for the Prohibition of Chemical Weapons has arrived in Syria to attempt to verify if a chemical attack did indeed take place.

The Federal Reserve minutes had a generally hawkish tone, reflective of a solid US economy. All of the Fed policymakers indicated that the US economy would continue to improve and that inflation would rise in the next few months. At the March meeting, the Fed unanimously voted to raise rates by a quarter-point, bringing the benchmark rate to a range between 1.50% and 1.75%. The Fed projection for rate policy in 2018 remains at three hikes, although there is speculation that the Fed could revise the forecast to four rate hikes. Last week, Fed Chair Jerome Powell said that the Fed would likely continue to raise rates in order to keep a lid on inflation, but added that the rate moves would be gradual. A new headache for the Fed is the escalating trade battle between the US and China, which could hurt the economy and raise consumer prices. As for the next two rate meetings, the markets expect Powell & Co. to sit tight in May and raise rates at the June meeting.

Risk Appetite Resumes, Oil At Fresh Three-Year Highs

Here are the latest developments in global markets:

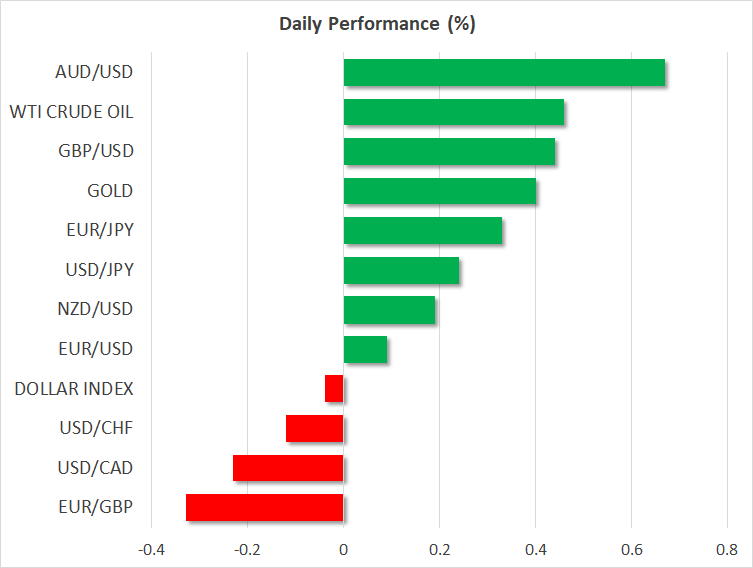

FOREX: While war and trade risks have not fully faded, Trump’s tweets on Thursday showed that the US president is considering to rejoin the Trans-Pacific free trade partnership, which he pulled out in his first months in the role. His remarks also indicated that he wanted to avoid tit-for-tat tariffs with China. In the wake of the comments, investors turned focus to riskier investments, sending safe havens lower, with dollar/yen crawling up to a fresh six-week high of 107.66 (+0.22%) today. The dollar index, though, was struggling to gain ground as the pound was on the forefoot. The pound hit a new 10-week high of 1.4284 (+0.40%) versus the greenback, while against the euro it broke a six-month range, with euro/dollar falling to a 10-month trough of 0.8627 (-0.33%). While optimism on Brexit and expectations of a rate hike in May seemed to support the currency, the rally could be also a technical correction. Note that EU-UK trade negotiations will start next week. Euro/dollar inched up to 1.2331 (+0.06%) after a deep fall yesterday triggered by somewhat dovish ECB meeting minutes, which expressed concerns about trade risks and the euro strength. Aussie/dollar moved rapidly up to 0.7805 (+0.66%), kiwi/dollar climbed to 0.7380 (+0.22%), while dollar/loonie retreated to 1.2554 (-0.25%).

STOCKS: European equities managed to close in the green yesterday and today opened slightly higher after trade and war concerns calmed down. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.14% and 0.05% respectively at 0830 GMT, on track to post gains for the third consecutive week. The German DAX 30 jumped by 0.42% driven by financials and consumer cyclicals, while basic materials and industrials were leading the Spanish IBEX 35 (+0.39%) and the French CAC 40 (+0.22%) after sanctions imposed to the Russian aluminum firm Rusal. On the other hand, the British FTSE 100 moved down by 0.11, weighed by losses in the technology sector arising after the UK’s second largest software company Sage reported worse-than-expected Q1 2018 earnings. Sage shares are now set to post their largest daily decline in 25 years. Asian equities closed mixed, while most of the indices tracking US stock futures were pointing to a positive open ahead of key earnings releases from the banking industry,

COMMODITIES: Oil prices were set to recover losses made the previous two weeks, with WTI crude and Brent surging to fresh three-year highs during the early European afternoon, peaking at $67.69/barrel (+0.92%) and $72.64 (+0.86%) respectively at 0900 GMT. Fears over a war in the Middle-East were still hanging on the background but the rally picked up speed on the release of a monthly report by the Paris-based International Energy Agency which stated that OPEC and its allies look to have accomplished their mission to bring oil stocks into desired levels. Note that recent headlines showed that OPEC is poised to extend supply cuts into 2019. In metals, gold continued to pare yesterday’s losses, climbing to 1340.76 (+0.44%).

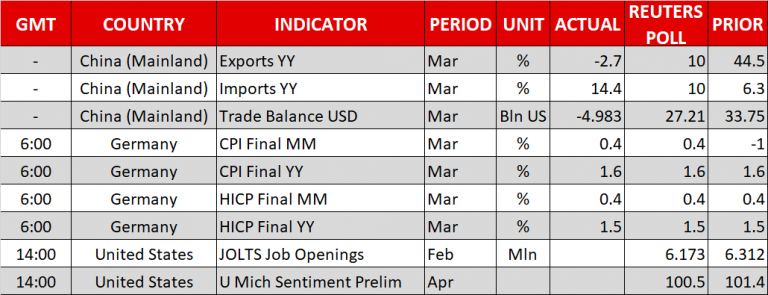

Day Ahead: US JOLTs job openings & University of Michigan consumer sentiment awaited

The economic calendar will be thin in the remainder of the day and in the absence of important figures, investors may turn their focus on developments on the geopolitical and trade fronts.

US JOLTs job openings will attract the most interest later today at 1400 GMT. Particularly, the report published by the Bureau of Labor Statistics is expected to show that 6,110 million positions opened in February compared to 6,312mn seen in the previous month.

At the same time, the University of Michigan will be delivering flash estimates on the US consumer sentiment. The index is forecast to inch down to 100.6 in April compared to 101.4 in the preceding month.

Later in the day, at 1700 GMT, Baker Hughes will publish its US oil rig count report, probably adding further volatility to oil prices which peaked at new three-year highs during the European session.

Turning to public appearances, several speeches by Fed members are scheduled later today. At 1130 GMT, Boston’s Fed President Eric Rosengren will be delivering comments ahead of a speech by St. Louis’s Fed President James Bullard at 1330 GMT. Remarks by Dallas Fed President Robert Kaplan will also attract attention at 1700 GMT.

In stock markets, earnings releases will continue to attract attention, with JPMorgan Chase, Citigroup, and Wells Fargo being among companies to reveal Q1 2018 results.

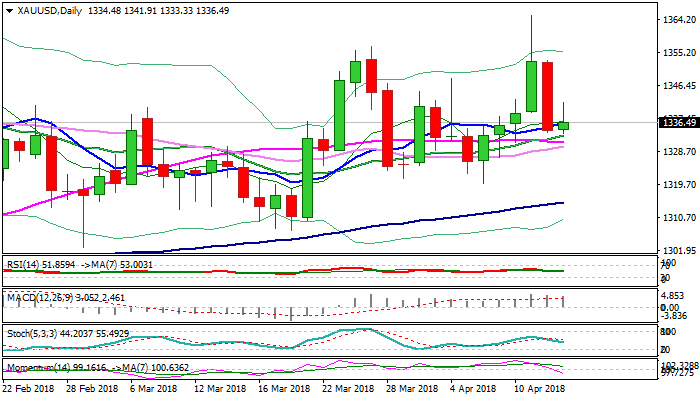

Spot Gold – The Downside Remains Vulnerable On Risk Sentiment/Weak Techs, Geopolitical Situation Remains In Focus For Fresh Signals

Gold price moved slightly higher on Friday and hit session high at $1341 but remains at the back foot following sharp fall on Thursday, when the yellow metal fell $20 on renewed risk sentiment after geopolitical tensions eased. Daily techs lost momentum, with today's limited recovery keeping the downside vulnerable. Thursday's long bearish candle (the biggest one-day fall since 28 Mar) weighs, as bears on Thursday closed below $1337 (Fibo 61.8% of $1319/$1365 upleg) and generated bearish signal. Weekly close below $1337 would reinforce negative signal and maintain bearish near-term bias for test of $1330 support zone, loss of which could open way towards thin daily cloud which twists next week and could attract and key support at $1319 (06 Apr trough). However, situation in Syria remains the key driver of gold and will remain in focus. Rising tensions could revive safe-haven demand and yellow metal price could surge on such scenario.

Res: 1341, 1343, 1348, 1353

Sup: 1333, 1330, 1326, 1319

Traders Remain Cautious Heading Into The Weekend

- Heightened Geopolitical Risk May Weigh on Gains into End of the Week;

- Earnings Season to Provide Timely Distraction;

- Is This Another False Dawn For Bitcoin?

'Given the backdrop of a trade conflict with China and rising tensions with Russia over Syria, any rallies may be somewhat gradual'

The end of the week is looking a little quieter in some respects and yet, with geopolitical risk heightening in recent days and first quarter earnings season getting under way, it's unlikely to be entirely peaceful.

The open in Europe and trade in Asia was broadly mixed with investors clearly adopting more of a cautious tone. US futures are a little higher but again, given the backdrop of a trade conflict with China and rising tensions with Russia over Syria, any rallies may be somewhat gradual and dependent on the situations not deteriorating further. We are seeing small signs of encouragement but the unpredictable nature of all concerned doesn't provide much confidence.

With Donald Trump being so active on Twitter, it's unlikely the day will pass without at least some mention of one or both of the above, the question is whether his comments will act to calm or inflame the situation. Any indication that strikes in Syria are likely over the weekend could trigger risk aversion into the close in case of a negative fallout in the markets at the open next week.

'Expectations for the quarter and year as a whole have grown in recent months following the passing of tax reforms at the back end of last year and this comes on the back of already improving and impressive numbers'

Something that may provide some distraction over the coming weeks is earnings season, with JP Morgan, Wells Fargo and Citigroup kicking things off today. Expectations for the quarter and year as a whole have grown in recent months following the passing of tax reforms at the back end of last year and this comes on the back of already improving and impressive numbers.

Lower taxes will likely play a big role in the improved earnings numbers and outlook but higher interest rates on the horizon will likely also have an impact. On the flipside, the prospect of a trade war may also feature in some reports and the impact that could have on the outlook for the coming year.

'We've had good days on numerous times this year and they turned out to be false dawns, this could be another'

Bitcoin has sprung back to life in the last 24 hours and while numerous people have tried to explain the sudden surge as being a short squeeze or numerous other things, it's at least brought the cryptocurrency space back to life having become somewhat lifeless by its own standard. In terms of where it goes from here, the move yesterday was certainly encouraging for the bulls and came amid a clear lack of selling appetite in the weeks previous but I remain unconvinced this is the end of the sell-off as some are already claiming.

For one, every time we've seen a resurgence in prices over the last four months, cryptocurrency enthusiasts have claimed the good times are back and we'll be back at $20,000 before you know it. While I'm not saying we won't get back there, I think we need a little more evidence that the bulls are back in force before I believe it's happening and one day of sudden gains just doesn't cut it. Let's see what the weekend brings but we've not even touched the last peak in March. We've had good days on numerous times this year and they turned out to be false dawns, this could be another.

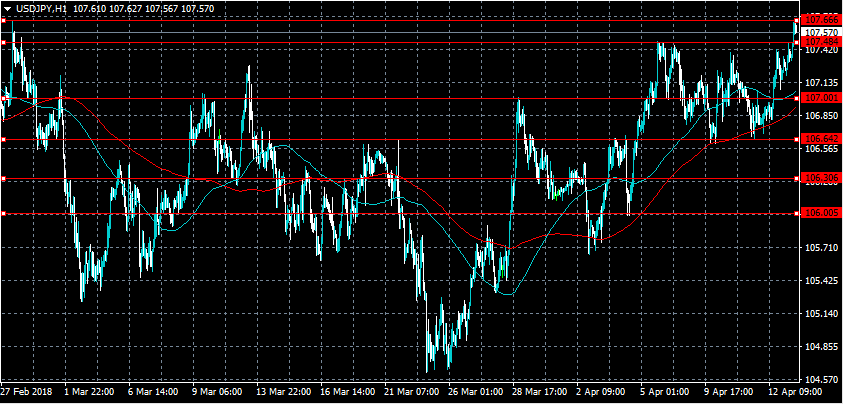

USDJPY Probing Topside Of Medium-Term Range

The U.S dollar has moved to the top-side of its recent medium-term trading range against the Japanese yen, as financial markets look past potential military action from the United States against Syria. The USDJPY pair is currently trading around the 107.50 region, after earlier finding strong weekly resistance from the key 107.66 level. Traders now look towards Jobs and Consumer Confidence data from the United States economy, with risk-sentiment finely balanced heading into the weekend.

The USDJPY pair remains bullish while trading above the 107.00 level, intraday resistance is located at the 107.66 and 108.00 levels.

Should the USDJPY pair move below the 107.00 level, key intraday support is located at the 106.60 and 106.00 levels.

GBPUSD Buyers Eye 1.4300 Level

The British pound has moved to a fresh monthly trading high against the U.S dollar, with price-action hitting 1.4295, during the European trading session. The GBPUSD pair currently trades around the 1.4275 level, as traders buy the British pound on expectations of an upcoming rate hike from the Bank of England. Moving into the U.S trading session, a bullish weekly close above the pairs 200-week moving average, at 1.4245, may signal further medium-term upside in sterling.

The GBPUSD pair is strongly bullish while trading above the 1.4245 level, key resistance is now found at the 1.4300 and 1.4347 levels.

Should the GBPUSD pair decline below the 1.4245 level, the 1.4200 and 1.4146 levels currently offer strong intraday support.

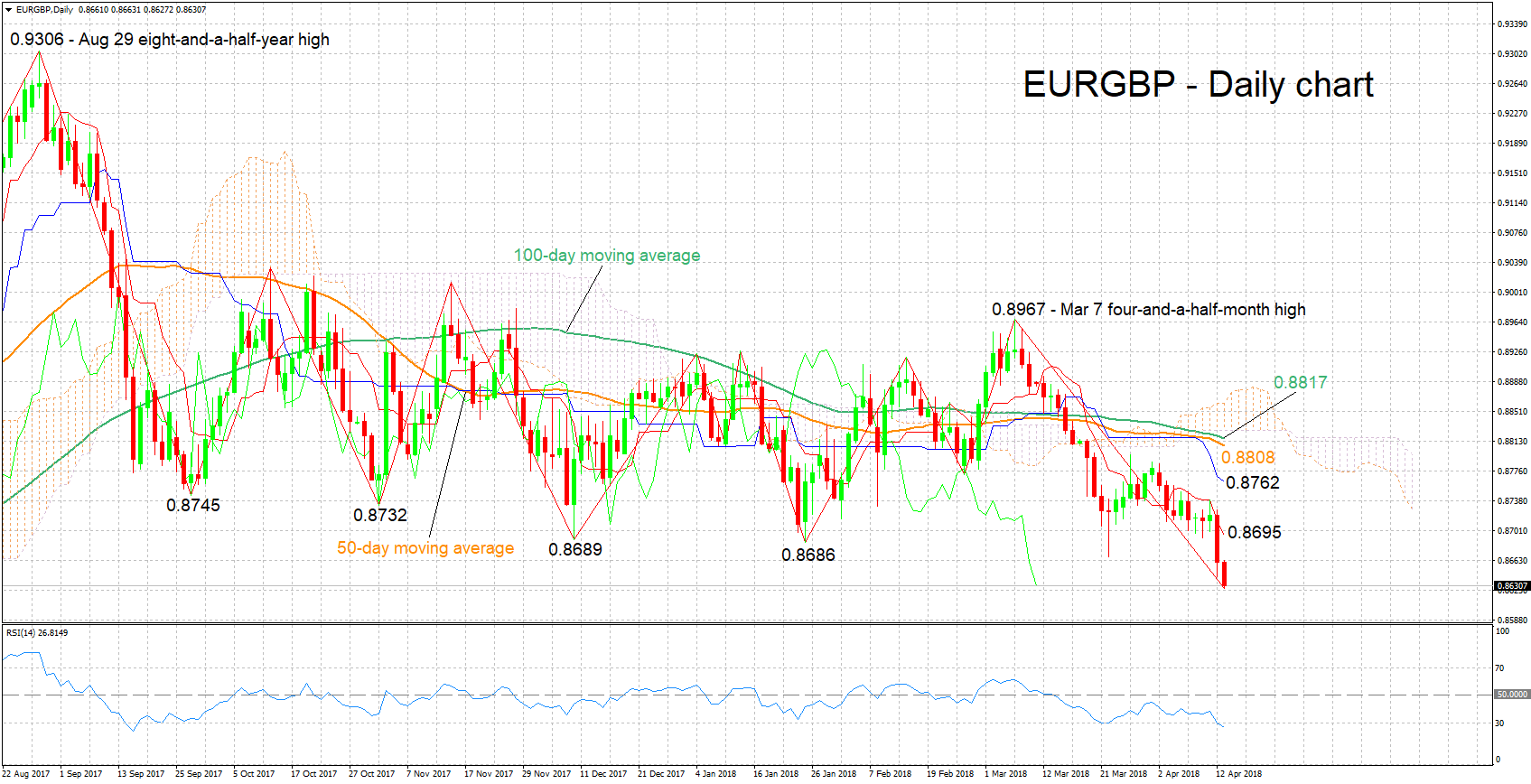

EURGBP Hits Near 11-Month Low, Looking Bearish In The Medium-Term

EURGBP has declined considerably after recording a four-and-a-half-month high of 0.8967 in early March. Earlier in Friday’s trading it touched 0.8627, this being its lowest since May 24 of last year, while it is currently trading not far above this trough.

The Tenkan- and Kijun-sen lines are negatively aligned and the RSI is heading lower, both being supportive of a negative short-term momentum for the pair. However, the RSI has entered oversold territory below 30 and the Chikou Span also seems to provide evidence of an overstretched selloff; a reversal in the short-term should thus not be ruled out.

Further declines could meet support around the round figures of 0.86 and 0.85 that may hold psychological significance.

On the upside, resistance could come around the current level of the Tenkan-sen at 0.8695. The area around this includes a few bottoms from previous months as well as the 0.87 handle that may also be of psychological importance. Stronger bullish movement would turn the attention to the range around the Kijun-sen at 0.8762.

The medium-term picture is looking mostly bearish, with trading taking place below the 50- and 100-day moving average lines, as well as below the Ichimoku cloud. Notice also that a broader range between roughly 0.87-0.90 that held since mid-September was violated to the downside.

Overall, the short-term outlook is bearish – with some signs of an oversold market though – and the medium-term picture is looking predominantly negative.