Sample Category Title

Weekly Focus: More to Worry About

Market movers ahead

- In a week with few important data releases and scheduled events, we expect markets to remain focused on global politics – there have been encouraging signs on trade policy lately but increasing worries over Syria and the US-Russia relationship.

- US retail sales should be interesting, as they have been weak lately but the underlying case for consumption growth remains strong.

- UK data is likely to show increasing wage growth and core inflation, supporting the case for a rate hike next month.

- We expect a lot of attention on Swedish house prices for March – our indicator shows that the decline in Stockholm apartment prices continued and there was a very large decline in trading activity.

Global macro and market themes

- Geopolitical risk has resurfaced but despite the heightened uncertainty from a weakening growth cycle and the trade issue, volatility has stayed subdued and market moves have generally been muted with the RUB a key exception.

- We still expect equities to rebound, while rate and FX markets are taking a breather from recent ECB and Riksbank repricing and the USD decline.

- Norwegian inflation was much lower than expected in March, but that was only due to temporary factors, and the new wage agreement actually points clearly towards higher inflation.

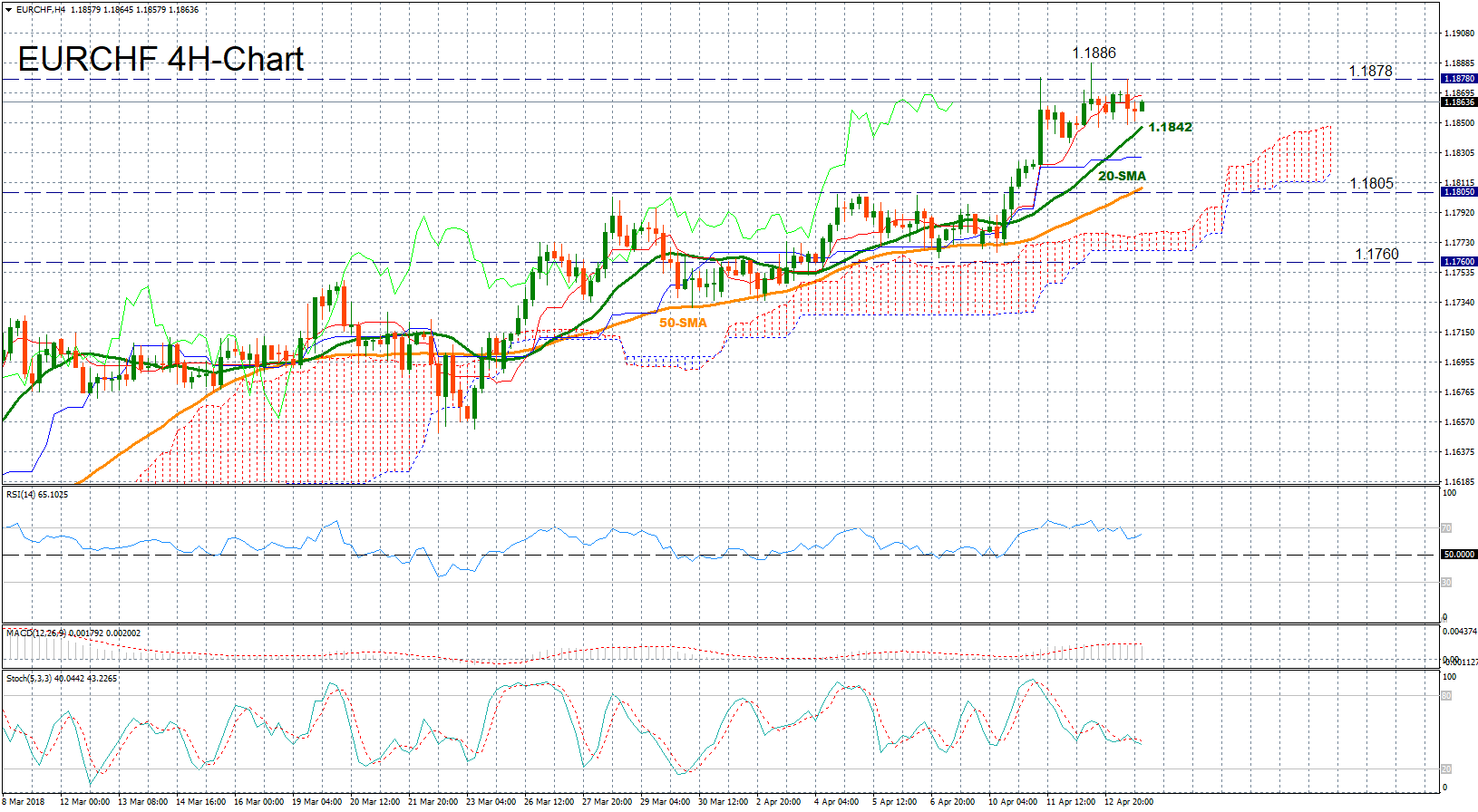

EURCHF Hovers at Three-Year Highs but Could Lose Steam

EURCHF spiked higher on Thursday, stretching its upleg started at the beginning of March to a fresh three-year high of 1.1886. While the sentiment remains positive, with prices continuing to trend above the Ichimoku cloud and all the simple moving average lines, momentum could fade in the short-term according to technical indicators.

The RSI is holding in bullish territory above 50, but the index looks weaker now after It left overbought levels earlier today. The MACD has also slowed down, falling below its red signal line, while Stochastics are moving downwards, with the green %K line set to post a bearish cross with the red %D once again.

In the event of declines, the 20-day SMA at 1.1842 could provide nearby support. Should the pair fail to hold above this level, a stronger obstacle could be met at 1.1805 where the 50-day SMA currently stands. Breaking this previous resistance area, negative pressures could strengthen with scope to retest the 1.1760 mark, another frequently visited level.

On the upside, the area encapsulated by this week’s peaks of 1.1878 and 1.1886 could be in focus since any decisive close above from this area could energize bulls, opening the door to the 1.1900 and 1.2000 key-marks.

Sunset Market Commentary

Markets:

Global core bonds lost marginally ground today with easing geopolitical tensions still at play. Interestingly, the US yield curve bear flattens (+1.6 bps for 2-yr and flat for 30-yr) while the German one bear steepens (flat for 2-yr and +1.3 bps for 30-yr). The widening of the short term US/GE spread accelerated this week following the mix of hawkish FOMC Minutes and dovish ECB Minutes. The spread reaches a new multiyear high of 294 bps. The US 2-yr yield set a cycle high at 2.37%. Boston Fed Rosengren, a hawk in favour of more rate hikes this year than the current median (2), warned of the risk of overheating and slightly added to the move. EUR/USD held remarkably strong around 1.2330 throughout the session despite this mix of strong equities and a rising spread differential. The dollar did gain the upper hand against the yen, overtaking first intermediate resistance (107.49) and heading towards strong technical resistance at 108.28/43 (previous low/38% retracement).

Sterling took a strong start to trading with GBP/USD attacking 1.43 and EUR/GBP dropping below 0.8650. However, the UK currency couldn’t hold on to those positive vibes and the rally gradually choked. The test of key EUR/GBP 0.87/0.8650 support remains ongoing though. We hold this morning’s line that a break will be difficult ahead of next week’s events. The EU and UK will for the first time look into the post-brexit trade relationship. The negotiations will also cover the unresolved issue of the Irish border and other parts of the divorce agreement that remain to be settled. It could break sterling’s momentum given that both parties’ official views remain wide apart. The UK labour market report, CPI and retail sales are also on the agenda next week.

News Headlines:

OPEC and its allies appear to have accomplished their mission of bringing global oil stocks to desired levels, the International Energy Agency said, signaling that the markets could become too tight if supply remains restrained. Brent crude hovers around $72/barrel as geopolitical concerns keep oil prices underpinned.

S&P raised the outlook from the Japanese A+ rating to positive from stable. The rating agency expects Japan’s relative debt burden to stabilize sooner than previously anticipated due to negative effective real interest rates and the country’s nominal economic growth exceeding 2%, according to the statement. Japan is rated at a similar level at Moody’s (A1, stable) and one notch weaker at Fitch (A, stable).

Headline earnings (EPS) topped expectations for JP Morgan, Wells Fargo and Citi who kicked off the real Q1 earnings season. JP Morgan’s quarterly profit fell short of expectations though as lower revenue from investment banking ate into gains from US corporate tax changes and higher interest rates. Wells Fargo’s earnings were subject to change as a $1bn penalty over mis-sold car insurance and mortgage fees looms.

Italian President Mattarella said he will decide how to break the political deadlock in a few days’ time, after a second round of talks with party leaders failed to make progress in the search for a new government.

• Turkish President Erdogan’s senior advisor Ertem told local media that they are able to quickly defeat exchange rate volatility, hinting at interventions. EUR/TRY decline from 5.08 to 5.03 after hitting an all-time high earlier this week following the launch of a new economic incentive plan which is rumoured to be complemented by lower interest rates. That’s a rather bizarre policy week given the country’s already strong growth and double digit inflation.

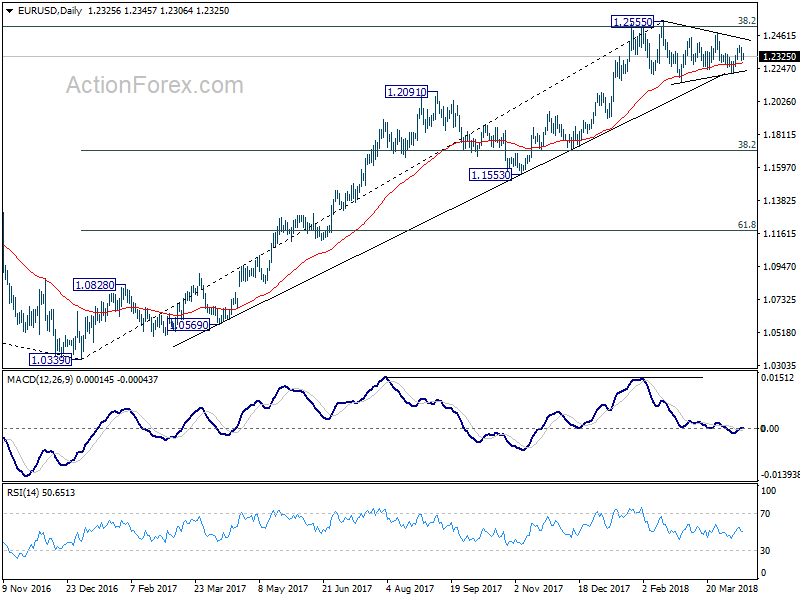

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2290; (P) 1.2334 (R1) 1.2370; More....

EUR/USD is holding inside tight range above 1.2302 minor support. Intraday bias stays neutral first. On the upside, above 1.2396 will extend the rise from 1.2214 to 1.2475 and then 1.2555. 1.2516/55 is the key resistance zone to determine larger outlook. On the downside, below 1.2302 will turn bias to the downside for 1.2214 support first. And firm break there will revive the case of rejection by 1.2516 key fibonacci level and turn outlook bearish.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

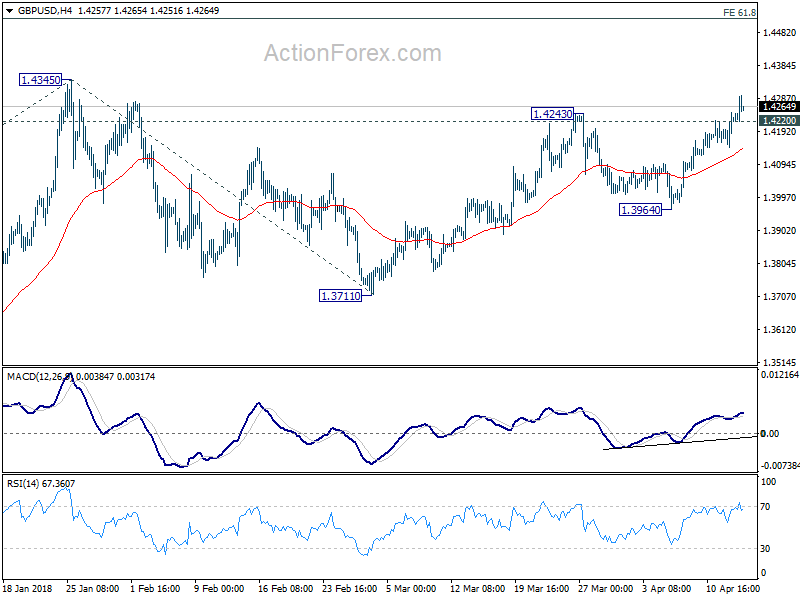

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4165; (P) 1.4206; (R1) 1.4266; More....

Intraday bias in GBP/USD remains on the upside for 1.4345 high. Firm break there will resume medium term rally and target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 next. On the downside, below 1.4220 minor support will turn intraday bias neutral again. But retreat should be contained well above 1.3964 support to bring another rally.

In the bigger picture, as long as 1.3651 resistance turned support holds, medium term outlook in GBP/USD will remain bullish. Rise from 1.1946 is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4267) so far. Break of 1.3651 will be the first sign of medium term reversal and turn focus to 1.3038 support for confirmation.

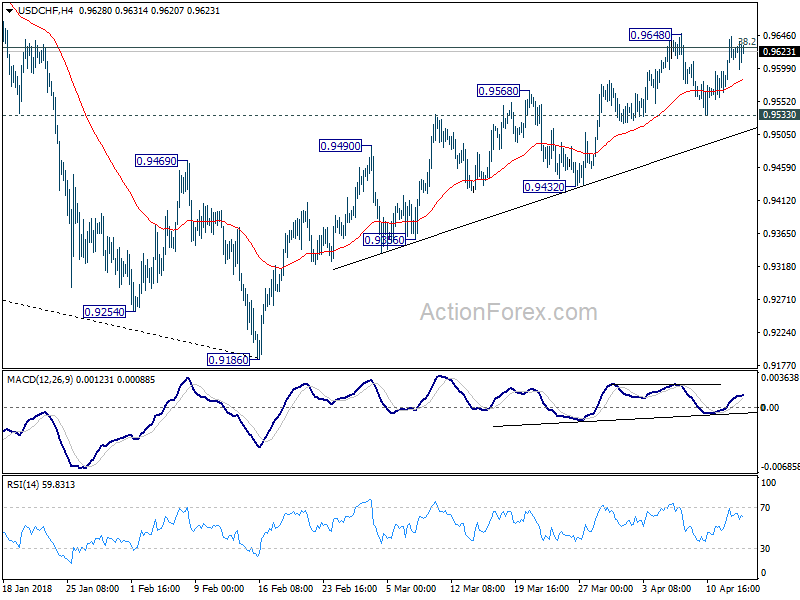

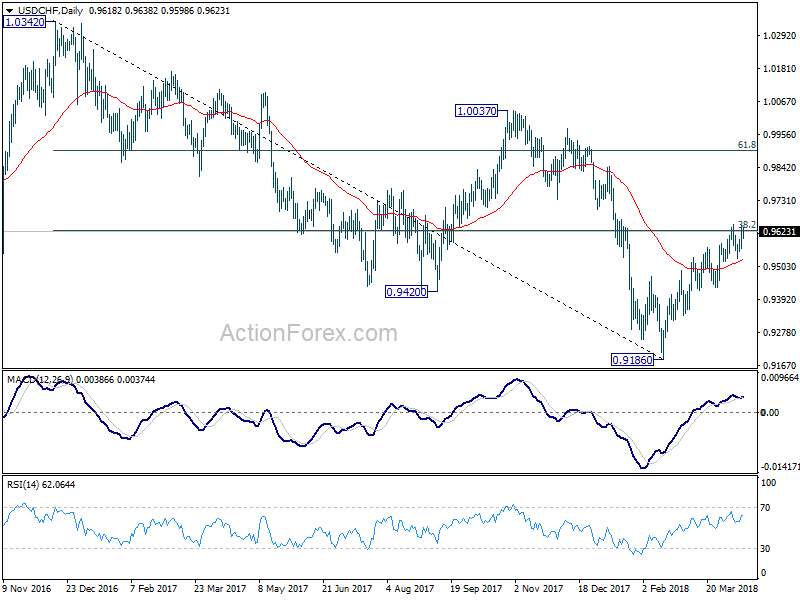

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9575; (P) 0.9610; (R1) 0.9659; More...

USD/CHF is still bounded in range of 0.9533/9648 and intraday bias remains neutral. Focus stays on 0.9626 key fibonacci resistance. Sustained trading above this level will be another evidence of larger reversal. In that case, further rally should be seen back to next fibonacci level at 0.9900. On the downside, though, break of 0.9533 minor support should indicate rejection by 0.9626. Further break of 0.9432 will turn near term outlook bearish for retesting 0.9186 low.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above. However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

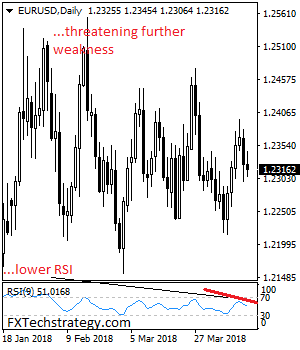

EURUSD: Weakens, Eyes Key Support

EURUSD: The pair faces further downside pressure as it looks to extend downside pressure. On the upside, resistance comes in at 1.2350 level with a cut through here opening the door for more upside towards the 1.2400 level. Further up, resistance lies at the 1.2500 level where a break will expose the 1.2550 level. Conversely, support lies at the 1.2300 level where a violation will aim at the 1.2250 level. A break of here will aim at the 1.2200 level. Below here will open the door for more weakness towards the 1.2150. All in all, EURUSD faces further downside threats.

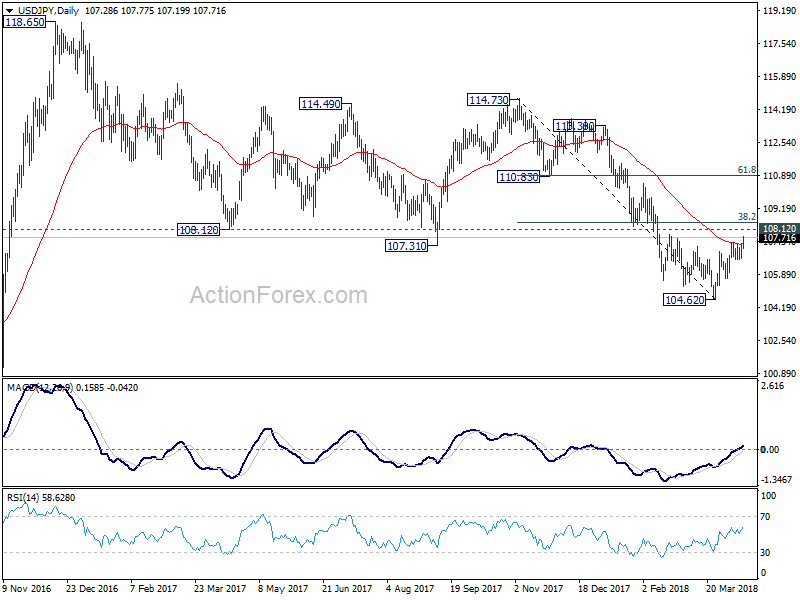

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.88; (P) 107.15; (R1) 107.61; More...

USD/JPY's rally extends to as high as 107.77 so far. Intraday bias remains on the upside for 38.2% retracement of 114.73 to 104.62 at 108.48 9 which is close to 108.12. This resistance zone will be crucial in determining the medium outlook. On the downside, break of 106.64 minor support is needed to indicate completion of the rebound. Otherwise, further rise will remain in favor even in case of retreat.

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

Yen Selling Intensified, Dollar Supported by Hawkish Fed Rosengren

Yen continues to be the weakest one today as selloff intensifies in European session. Relieves from immediate risks are still as the major reason driving the Japanese currency down. Australian Dollar continues to be the strongest one with AUD/USD and EUR/AUD taking out key near term levels. Dollar was under some pressure earlier today but is supported by Fed Rosengren's comments and turned mix entering into US session.

Boston Fed Rosengren: Somewhat more tightening may end up being needed

Boston Fed President Eric Rosengren sounded hawkish in his comments today. Referring to Fed's projection of two more hikes this year, Rosengren said that "somewhat more tightening may end up being needed". He expected a "somewhat stronger" economy ahead than the already "quite positive" FOMC projections. He also pointed to solid performance in job creation, falling unemployment and inflation close to Fed's 2% target. However, Rosengren also pointed out short-run and long-run risks to the positive outlook. Short run risks include trade tensions and overheated "boom-bust" scenario. Long run risks included insufficient fiscal and monetary buffers.

TPP member Japan, Australia, Malaysia told Trump, you're welcomed but no renegotiation

Ministers of three of TPP-11 members responded to news that Trump is considering to rejoin TPP. While all of the welcomed the news, they also said there will be no renegotiation on what were signed. Australia Trade Minister Steven Ciobo said today that "we welcome the U.S. coming back to the table but I don't see any wholesale appetite for any material re-negotiation of the TPP-11."Japan Minister Toshimitsu Motegi said the current deal is a "balanced one, like fine glassware" and it would be difficult to change. Malaysia International Trade and Industry Minister Mustapa Mohamed also warned that renegotiation would "alter the balance of benefits for parties." These were in response to Trump's tweet that "would only join TPP if the deal were substantially better than the deal offered to Pres. Obama."

S&P upgrades Japan's A+ rating outlook to "positive"

S&P Global Ratings upgraded Japan's A+ outlook from "stable" to "positive". S&P noted stronger economy should set the stage for fiscal improvement in Japan. The positive outlook reflects healthier growth prospect, in both real and nominal terms. The current rating also reflect Japan's formidable external position, diversified economy, political stability and financial system stability. Nonetheless, it also pointed out that While Japan's external balance sheet is strong, Government finances are weak. And that is a significant constraint of its creditworthiness.

China reported rare trade deficit in March, Q1 imports from EU surged

China reported a rate trade deficit of USD -5b in March versus expectation of USD 27.8b surplus. That's also the first monthly trade deficit since last February. Imports rose 5.9% yoy while exports dropped -2.7% yoy. Trade surplus with US dropped to USD 15.3b. In CNY terms trade balance came in at CNY -30b deficit versus expectation of CNY 160b surplus. Imports dropped -9.8% yoy while exports also dropped -9.8% yoy.

For the quarter from January to March, 2018, China's trade surplus came in at USD 49.1b, dropped -23.2% yoy from Q1 of 2017. Exports rose 14.1% yoy. But import grew even stronger by 18.9% yoy. In CNY terms, Q1 trade surplus rose came in at CNY 326.2b with exports increased by 7.4% yoy and imports jumped even stronger by 11.7% yoy.

Also for Q1, export to US rose 14.8% yoy to USD 99.9b while imports from US rose 8.9% yoy to USD 41.7b. Exports to EU rose 13.2% yoy to USD 90.2b while imports from EU rose 17.5% yoy to USD 63.5b.

New Zealand manufacturing PMI signed slower expansion

New Zealand BusinessNZ Performance of Manufacturing Index (PMI) dropped -1.1 to 52.2 in March. That's also the second consecutive decline in 2018 even though it still signaled expansion. Nonetheless, BusinessNZ's executive director for manufacturing Catherine Beard noted a positive point that the proportion of positive comments in March (55.1%) picked up from both February (51.4%) and January (50.7%). BNZ Senior Economist, Craig Ebert said that the weak spot in March's PMI was its production index.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.88; (P) 107.15; (R1) 107.61; More...

USD/JPY's rally extends to as high as 107.77 so far. Intraday bias remains on the upside for 38.2% retracement of 114.73 to 104.62 at 108.48 9 which is close to 108.12. This resistance zone will be crucial in determining the medium outlook. On the downside, break of 106.64 minor support is needed to indicate completion of the rebound. Otherwise, further rise will remain in favor even in case of retreat.

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | RBA Financial Stability Review | ||||

| 3:10 | CNY | Trade Balance (USD) Mar | -5.0B | 27.8B | 33.7B | |

| 3:10 | CNY | Trade Balance (CNY) Mar | -30B | 160B | 225B | |

| 6:00 | EUR | German CPI M/M Mar F | 0.40% | 0.40% | 0.40% | |

| 6:00 | EUR | German CPI Y/Y Mar F | 1.60% | 1.60% | 1.60% | |

| 9:00 | EUR | Eurozone Trade Balance (EUR) Feb | 21.0B | 20.1B | 19.9B | 20.2B |

| 14:00 | USD | U. of Mich. Sentiment Apr P | 100.6 | 101.4 |

Markets Sensitive to Geopolitical Tensions, Gold Dips

It has certainly been another volatile and unpredictable trading week for financial markets, as heightened geopolitical tensions have left investors on edge. President Donald Trump’s market shaking tweets have not helped matters, with global equity markets violently whipsawing in recent days. As the trading month progresses, global risk appetite is poised to remain extremely fragile and highly sensitive to the Russia-U.S tensions over Syria.

Asian stock markets were cautiously higher this morning, after U.S President Trump appeared to soften his approach to Syria and made a U-turn on protectionist policies. In Europe shares were somewhat supported, as concerns over the conflict in Syria eased. Although U.S stocks could extend gains this afternoon on strong earnings optimism, market anxiety is likely to create headwinds for equity bulls down the road.

With geopolitical tensions and heightened political uncertainty still weighing on sentiment and silently eroding risk appetite, stock markets remain vulnerable to heavy losses.

Gold bruised but continues to shine

This has been a rollercoaster trading week for Gold, with the metal displaying high levels of sensitivity to geopolitics and U.S interest rate hike expectations.

While heightened political tensions between the U.S and Russia have supported the yellow metal, expectations that the Fed will adopt a more aggressive approach over U.S interest rate hikes this year has capped upside gains. With uncertainty still a major market theme and investors clearly on edge, Gold is likely to remain buoyed in the medium term.

Taking a look at the technical picture, the metal is under pressure on the daily charts. Although prices have secured a daily close below the $1340 support level, the candlesticks remain above the 50 Simple Moving Average. Sustained weakness below the $1340 level could encourage a decline towards $1324. Alternatively, a breakout above $1340 may result in an appreciation back towards $1360.

Commodity spotlight – WTI Oil

Commodity spotlight – WTI Oil

Oil prices were incredibly bullish this week, as escalating tensions in the Middle East fueled concerns of potential supply disruptions.

The upside was complemented by encouraging statements made by the IEA (Institute of Economic Affairs) saying that OPEC was on the verge of clearing the global oil glut. Price action suggests that oil prices could edge higher near-term amid geopolitical tensions and optimism over OPEC supply cut rebalancing markets. However, rising production from U.S Shale could create obstacles for oil bulls down the road. From a technical standpoint, WTI Crude has scope to test $68.00 if bulls maintain control above $66.50. A scenario where prices are unable to stabilize above $66.50 could result in a decline back towards $64.00.