Sample Category Title

Forex Analysis: UK 100 And EURUSD

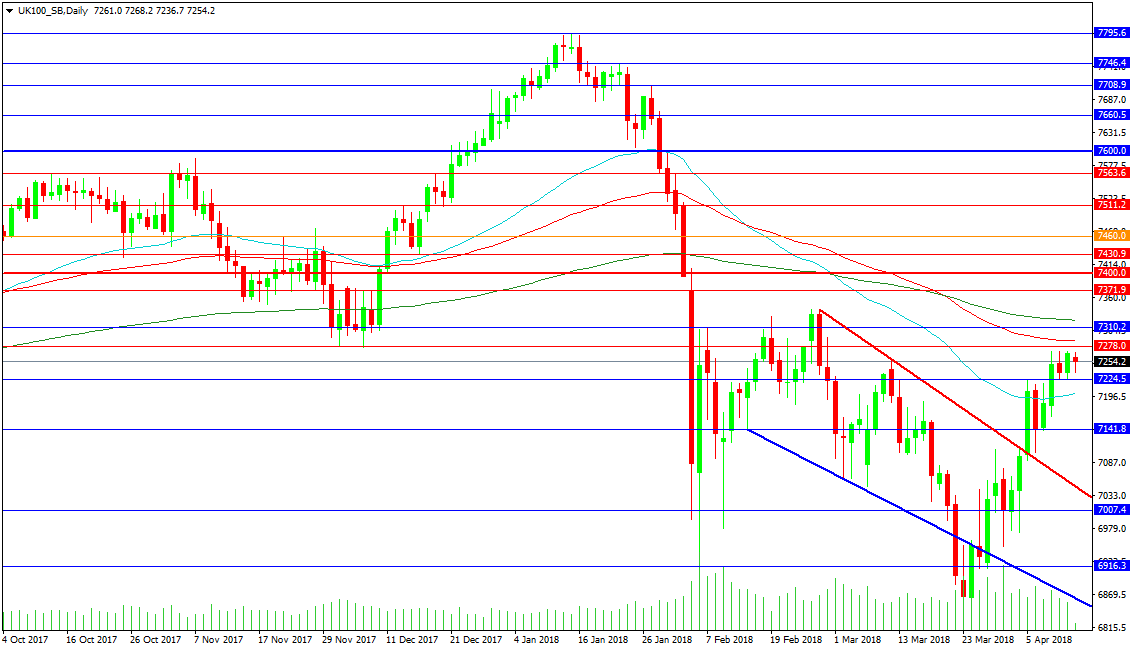

The UK 100 Index has positioned itself in a holding pattern over the last three days, after breaking above the resistance level of 7224.50 on Tuesday, with this level now becoming firm support. Further support comes from the 50 DMA at 7201.00, with a move under here handing control back to bears, who may try for a retest of the descending red trend line at 7040.00. Bulls could step in at that point to defend the breakout but a loss would target 7000.00, followed by 6916.3. The falling blue trend line comes in at 6859.00, with the March low at 6837.5.

Resistance above the current price level comes at 7278.0, supported by the 100 DMA at 7288.3. This is in the zone around the 7300.00 level, with the 7310.00 level above and the 200 DMA above that, at 7322.30. The 7340.00 level was the late February high, with 7372.00 guarding the way to 7400.00. A break above here clears a lot of resistance out of the way leaving little to prevent a run to 7500.00.

EURUSD

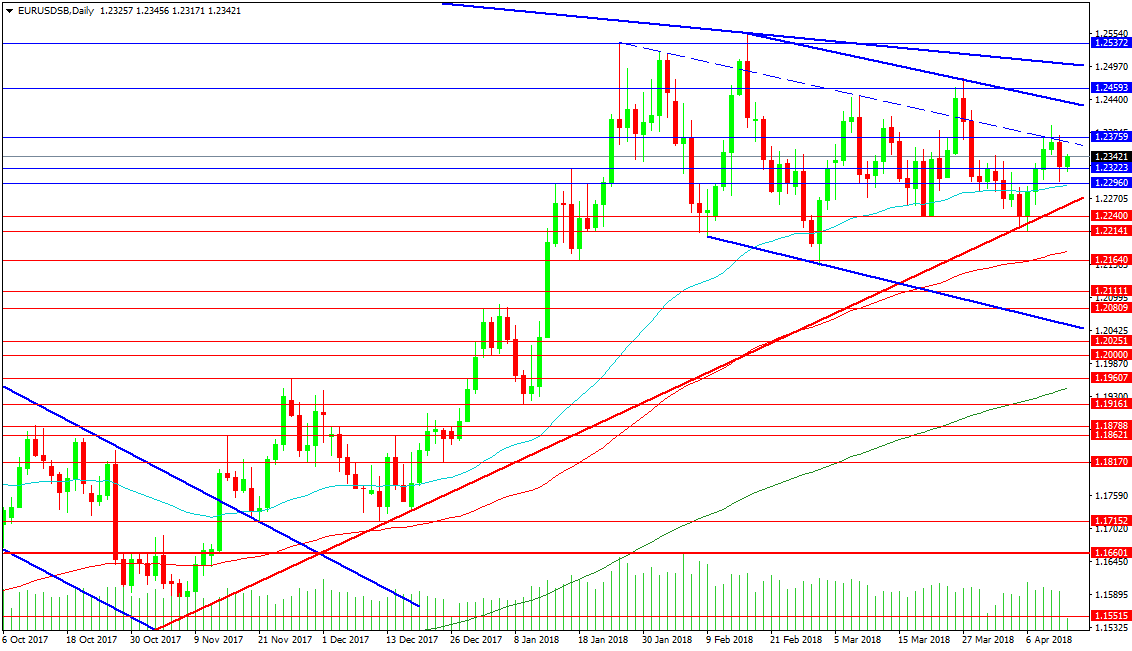

The EURUSD pair has created a sideways price action pattern with lower highs and higher lows. It is conceivable that price can reach higher from current levels but an event is needed to give the market a reason to drive price out of this sideways pattern. Resistance can be seen at the falling broken trend line at 1.23660 and the two touch blue trend line at 1.24295. The falling blue longer-term trend line is currently at 1.25000, which is a resistance level traders will pay attention to. The highs from January come in at 1.25372 and the February high is 1.25549.

Support can be seen at the 50 DMA at 1.22927 and the rising red trend line at 1.22575. The 1.22400 level represents the highest level that buyers have stepped in to buy the lows at over recent weeks. This buying zone extends down to 1.21640, which has two touches on it, but a loss of the 100 DMA at 1.21795 puts this in doubt. The 1.20809 level remains key support, with the 200 DMA at 1.19433.

WTI Oil Rallies To New 40-Month High On Bullish Signals From IEA Report

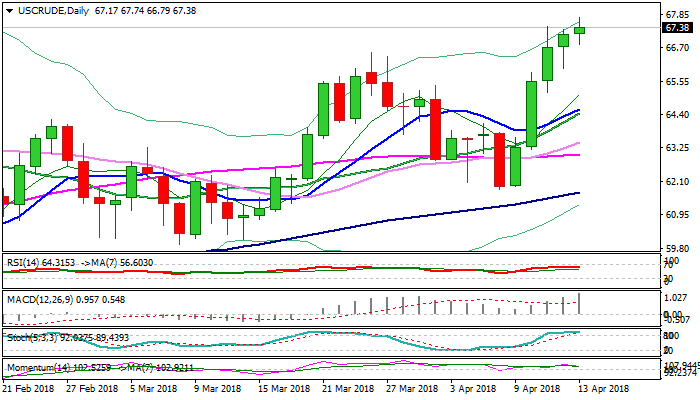

Oil price rallied to new 40-month high at $67.74 on Friday after International Energy Agency reported that global oil stocks returned to desired levels and oil glut is almost over, while demand remains unchanged. Fresh strength after oil price pulled back on easing tensions over Syria on Thursday, signals oil price may continue to rise and extend steep acceleration from last Friday's trough at $61.80. The price is on track for weekly close above cracked $66.75 barrier (Fibo 50% of $107.45/$26.04 fall) which would be bullish signal for extension towards psychological $70 barrier. Another bullish signal is developing on weekly chart as oil is on track for the strongest weekly performance since the last week of November 2016. Bullish techs add to positive fundamentals and continue to underpin oil price, however, overbought slow stochastic on daily chart warns that bulls may take a breather. Corrective dips should be ideally contained above $65.50 zone to keep bulls intact. Bearish scenario would require extension and close below converged 10/20SMA's ($64.44/$64.56) to neutralize bulls.

Res: 67.74, 68.63, 69.00, 70.00

Sup: 67.00, 66.79, 66.53, 66.00

Investors To Remain Sensitive To Market Tensions

Friday April 13: Five things the markets are talking about

Capital markets are to remain sensitive until there are clear signs that tensions are not escalating.

Ahead of the U.S open, global equities are adding to this week's advances as investors take comfort from further signs of trade tensions easing. The ‘big' dollar is steady and Treasury yields have dipped after rising above the psychological +2.80% yesterday.

President Trump hinted yesterday that the U.S might re-join the Trans-Pacific Partnership free-trade deal he pulled out of in January 2017 and this weeks oil rally take a pause as investors reassess the likelihood of direct U.S military action in Syria.

Stateside, market focus is now turning back to U.S earnings season, with some financial firms posting some of the biggest gains yesterday. JP Morgan Chase & co. and Citi are set to release theirs today.

1. Stocks mostly in the ‘black'

In Japan, the Nikkei share average rallied overnight as suggestions from U.S President Trump that a military strike on Syria may not be imminent supported investor sentiment and higher U.S bond yields helped financial stocks. The Nikkei ended +0.6% higher. For the week, the index added +1.0%, posting a third straight week of gains. The broader Topix gained +0.6%.

Down-under, Australia shares gained on Friday helped largely by materials and health care stocks, following global markets higher after fears of an imminent U.S attack on Syria eased. The S&P/ASX 200 index rose +0.2%. In S. Korea, the Kospi rallied +0.5%.

China and Hong Kong stocks slid on Friday, after data showed China's exports fell unexpectedly in March amid trade tensions with the U.S. China data showed that exports in yuan terms slid -9.8% in March. The market consensus was looking for a +8% gain. In Hong Kong, the Hang Seng index closed down -0.1%, while the China Enterprises Index lost -0.2%. In China, the CSI300 index fell -0.4%, while the Shanghai Composite Index lost -0.5.

In Europe, regional indices trade mixed following strong gains on Wall St. and mixed futures this morning as risk appetite returns now that Trump has dialed back claims on an immanent strike on Syria.

U.S stocks are set to open in the ‘black' (+0.1%).

Indices: Stoxx600 +0.2% at 379.6, FTSE flat at 7257, DAX +0.5% at 12473, CAC-40 +0.2% at 5320, IBEX-35 +0.5% at 9793, FTSE MIB +0.2% at 23358, SMI -0.1% at 8765, S&P 500 Futures +0.1%

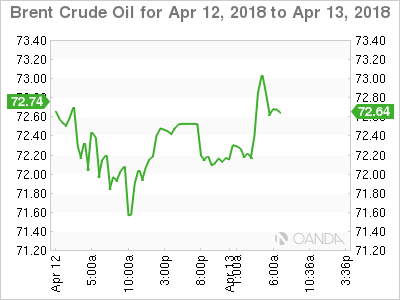

2. Oil heads for biggest weekly gain since July

Oil prices have edged a tad higher, heading for their largest weekly gain in 10-months after U.S President Trump's comments about possible military action in Syria and reports of dwindling global oil stocks.

Brent crude rose by +44c to +$72.46 a barrel, up about +8% on the week. WTI crude for May delivery gained +45c to +$67.52, putting the contract on track for a weekly jump of nearly +9%.

Note: Both benchmarks hit their highest in four years on Wednesday after Trump warned that missiles “will be coming” in response to a suspected gas attack in Syria.

Also providing a market bid was OPEC's statement yesterday, which stated “a global oil stocks surplus is close to evaporating, adding that its collective output fell to +31.96m bpd in March, down -201k bpd from February.”

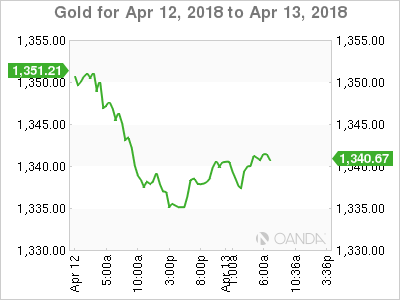

Ahead of the U.S open, gold has edged up a tad after posting its biggest percentage fall in over two-weeks yesterday and is set to post a small gain for a second consecutive week amid tensions over Syria and a U.S/China trade stand-off. Spot gold has rallied +0.2% to +$1,337.17 an ounce, and is set for a weekly gain of +0.3%.

Note: Gold prices dropped -1.3% on Thursday, the biggest one-day percentage fall since the end of March.

3. Sovereign yields climb

Borrowing costs in the euro and U.S have backed up overnight as geopolitical worries eased. On Thursday, President Trump cast doubt over the timing of a threatened strike on Syria, lifting risk appetite in world markets and in turn denting demand for safe-haven U.S and euro zone debt.

Overnight, the yield on U.S 10-year Treasuries fell less than -1 bps to +2.83%. In Germany, the 10-year Bund yield increased +1 bps to +0.52%, the highest in more than three-weeks. In the U.K, the 10-year Gilt yield gained +2 bps to +1.46%, the highest in more than three-weeks.

Note: Expect caution heading into the weekend to limit any rise in government bond yields.

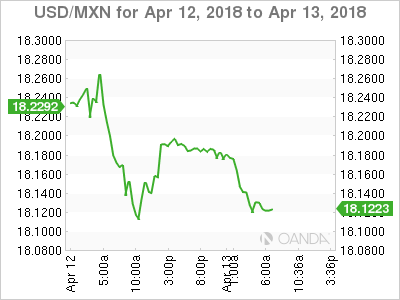

Yesterday, Mexico's Central Bank (Banxico) left the overnight rate unchanged at +7.50% (as expected). Policy makers are expected to take quick action if necessary to anchor inflation expectations and achieve convergence to target.

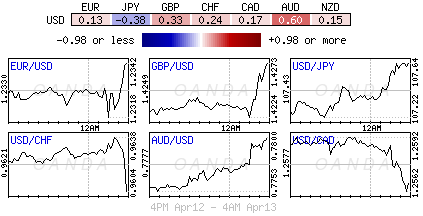

4. Dollar steady on higher yields

The USD is trading somewhat steady against G10 pairs supported by higher yields resulting from improved risk appetite.

USD/JPY (¥107.63) was at six-week highs as the pair moved above the key ¥107.50 resistance level.

The GBP/USD (£1.4284) saw its fifth straight session of gains with the pair approaching the key £1.43 level for its three month-highs on BoE rate differentials. The EUR/GBP cross was lower by -0.3% below €0.8640 as dealers noted that the recent ECB minutes showed that the debate on “normalizing” its policies appeared to be moving very slowely.

The Hong Kong Monetary Authority (HKMA) last night bought the local currency (HKD) for the first time since the current trading band was imposed 13-years ago, after the exchange rate sank to the weak end of its permitted range. The intervention is significant because the HKMA's purchases have the potential to boost borrowing costs by draining liquidity. That would signal the end of an era of ultra-cheap money.

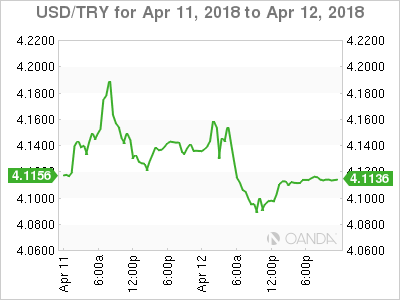

TRY ($4.0836 -0.71%) has rebounded, helped by Central Bank Statements. Bank Governor Murat Cetinkaya sais he is “closely monitoring recent lira developments with respect to their effect on the inflation outlook” and that “there may be additional tightening depending on where the lira heads next.”

5. Eurozone trade (Feb.)

Data this morning showed that in February, the euro-zone's seasonally-adjusted nominal goods trade surplus widened from January's +€20.2B to +€21.0B, beating market expectations.

Digging deeper, on the national front, Germany's trade surplus narrowed from +€21.5B to +€19.2B while France's trade deficit was little changed at -€5.2B.

Analysts note that the detail in the euro-zone release was somewhat discouraging. The surplus only widened because a -3.1% fall in imports outpaced a -2.3% fall in exports.

Euro Trading Sideways As German CPI Matches Forecast

EUR/USD has ticked higher in the Friday session. Currently, the pair is trading at 1.2339, up 0.10% on the day. On the release front, German Final CPI edged lower to 0.4%, matching the estimate. The US will release UoM Consumer Sentiment, which is expected to drop to 100.6 points.

Tensions continue to simmer in the Middle East, as Syria braces for a strike by the United States. President Trump has vowed to respond to an alleged chemical attack by Syrian forces, and a US navy task force is sailing towards Syria. Russia has promised to shoot down any US missiles, and relations between the US and Russia have nosedived. The US has received support from France and the UK, and if the US does carry out a military strike, the currency markets could respond with volatility.

The Federal Reserve minutes from the March meeting were hawkish in tone, reflective of a solid US economy. All of the Fed policymakers indicated that the US economy would continue to improve and that inflation would rise in the next few months. At the March meeting, the Fed unanimously voted to raise rates by a quarter-point, bringing the benchmark rate to a range between 1.50% and 1.75%. The Fed projection for rate policy in 2018 remains at three hikes, although there is speculation that the Fed could revise the forecast to four rate hikes. Last week, Fed Chair Jerome Powell said that the Fed would likely continue to raise rates in order to keep a lid on inflation, but added that the rate moves would be gradual. A new headache for the Fed is the escalating trade battle between the US and China, which could hurt the economy and raise consumer prices. The Fed is expected to sit tight in May and raise rates at the June meeting.

Quiet Session Heading Into Weekend

Notes/Observations

Asia:

- China Mar Trade Balance registered its first deficit in 13-months (-$5.0B v +$27.9Be). Exports YoY: -2.7% v +11.9%e; Imports YoY: +14.4% v +12.4%e

- Singapore Monetary Authority (MAS) Semi-annual Policy Statement registered its first tightening measure since April 2012 by increasing slightly the slope of the S$NEER Policy Band (prior saw a zero pct appreciation policy). MAS did maintain the width of policy band and the level at which it was centered unchanged.

- Singapore Q1 Advance GDP Q/Q: 1.4% v 1.2%e; Y/Y: 4.3% v 4.3%e

- Japan Chief Cabinet Sec Suga: To set up panel to consider ways to mitigate impact of planned Oct 2019 sales tax increase on economy

- RBA Financial Stability Review: Risks to Australia from China economy remained elevated. High household debt and riskier lending of recent years remained macro-financial risk.

Europe:

- ECB's Weidmann (Germany): price stability goal must not be weakened

- Russia UN Ambassador: 'Syria situation is very dangerous, immediate priority is to avert the danger of war'; asked if referring to war between Russia and US, says 'we cannot exclude any possibilities unfortunately'

Americas:

- US President Trump: Would only join Trans Pacific Partnership (TPP) if the deal were substantially better than deal offered to predecessor Obama. Already have bilateral deals with 6 of the 11 nations in TPP and are working to make a deal with the biggest of those nations, Japan, who has hit us hard on trade for years

- Fed's Kashkari (dove, non-voter) reiterated that had not seen much wage growth nationally but believed tax cuts and govt spending might help push inflation back to 2%

- Mexico Central Bank (Banxico) leaves Overnight Rate unchanged at 7.50% (as expected). To take quick action if necessary to anchor inflation expectations and achieve convergence to target

- US military officials said to hold high level talks with Moscow to prevent escalation between US and Russia; military strike in Syria was not coordinated action and Russia not happy about it; deconfliction line remained open

Economic Data:

- (NL) Netherlands Feb Trade Balance: €4.5B v €3.3B prior

- (NL) Netherlands Feb Retail Sales Y/Y: 2.6% v 5.1% prior

- (DE) Germany Mar Final CPI M/M: 0.4% v 0.4%e; Y/Y: 1.6% v 1.6%e

- (DE) Germany Mar Final CPI EU Harmonized M/M: 0.4% v 0.4%e; Y/Y: 1.5% v 1.5%e

- (FI) Finland Mar CPI M/M: 0.2% v 0.3% prior; Y/Y: 0.8% v 0.6% prior

- (FI) Finland Feb Current Account Balance: €0.3B v €0.4B prior - (FI) Finland Feb Final Retail Sales Volume Y/Y: 2.8% v 2.1% prelim

- (FI) Finland Feb GDP Indicator WDA Y/Y: 2.4% v 2.2% prior

- (ES) Spain Mar Final CPI M/M: 0.1% v 0.1%e; Y/Y: 1.2% v 1.2%e

- (ES) Spain Mar Final CPI EU Harmonized M/M: 1.2% v 1.2%e; Y/Y: 1.3% v 1.3%e

- (ES) Spain Mar CPI Core M/M: 0.5% v 0.5%e; Y/Y: 1.2% v 1.1%e

- (PL) Poland Mar Final CPI M/M: -0.1% v -0.1% prelim; Y/Y: 1.3% v 1.3% prelim

- (CZ) Czech Feb Current Account (CZK): 31.0B v 32.0Be

- (CN) China Mar M2 Money Supply Y/Y: 8.2% v 8.9%e; M1 Money Supply Y/Y: 7.1% v 9.5%e, M0 Y/Y: 6.0% v 7.9%e

- (CN) China Mar Aggregate Financing (CNY): 1.330T v 1.800Te

- (CN) China Mar New Yuan Loans (CNY): 1.120T v 1.176Te

- (IT) Italy Feb General Government Debt: €2.287T v €2.287T prior

- (EU) Euro Zone Feb Trade Balance (Seasonally Adj): €21.0B v €20.2Be; Trade Balance NSA (unadj): €18.9B v €3.3B prior

- (GR) Greece Mar CPI Y/Y: -0.2% v +0.1% prior; CPI EU Harmonized Y/Y: 0.2% v 0.4% prior

Fixed Income Issuance:

- (IN) India sold total INR120B vs. INR120B indicated in 2023, 2031, 2034 and 2046 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.2% at 379.6, FTSE flat at 7257, DAX +0.5% at 12473, CAC-40 +0.2% at 5320, IBEX-35 +0.5% at 9793, FTSE MIB +0.2% at 23358, SMI -0.1% at 8765, S&P 500 Futures +0.1%]

- Market Focal Points/Key Themes: European Indices trades mixed following strong gains on Wallstreet overnight and mixed futures this morning as risk appetite returns as President Trump dialed back claims on an immanent strike on Syria. On the earnings front Deutz trades sharply higher after strong earnings and revenue growth; L'Oreal trades slightly higher after LFL sales handily beat forecasts. Sage Group trades over 12% lower after cutting its FY guidance with Rocket Internet falling after its full year results. Elsewhere Hammerson is a notable faller after Kleppiere dropped its pursuit for the company. Looking ahead earnings season kicks off with major banks JP Morgan, Wells Fargo and Citigroup among some of names to report.

Movers

- Consumer Discretionary [Stora Enso [STERV.FI] +2.9% (Earnings)

- Industrials [Deutz [DEZ.DE] +7.3% (Earnings) ]

- Financial [Hammerson [HMSO.UK] -12.5% (Kleppiere drops bid), Hiscox [HSX.UK] -0.7% (Data breach) ]

- Healthcare [Galapagos [GLPG.BE] +4% (ISABELA Phase 3 program in IPF expected to start dosing in 2H18)]

- Technology [Sage[SGE.UK] -12%(most since 2001) (Cuts Rev outlook]

Speakers

- ECB's Smets (Belgium): Weak inflation remained a lingering concern. Reiterated Council view that prudence, patience and persistence were fully justified. To make policy shifts as predictable as possible

- Sweden Central Bank (Riksbank) Dep Gov Floden: Govt should wind down its bonds holdings when monetary policy was normalized. Asset purchases still might be needed in the future

- Norway Central Bank (Norges) Gov Olsen: Flexible inflation targeting couldn work counter cyclical. High household debt was amplifying effect of a rate rise

- UK Cabinet gave PM May the go-ahead for Syria strike 'to deter further use of chemical weapons by the Assad regime

- Ireland Fin Min Donohoe: GDP growth seen around 3% in coming years. No economic boom at this time

- Center-right party officials said to have told Italy President Mattarella that Salvini must be made PM

- Turkey President Chief Adviser Ertem: Treasury did not need to borrow in 2018. Central bank was displaying a decisive stance; steps to reduce FX volatility to be taken

- Draft of Russia's response to US sanctions envisaged introduction of restrictions on US goods. Russia govt could expand retaliatory measures in a 2nd reading

- Philippines Central Bank (BSP) chief Espenilla: 2018 CPI seen at the upper-end of 2-4% target range and decelerate to near 3% in 2019. Mindful of challenges of CPI target and ready to act if necessary

- China PBoC said to relax informal guidance for commercial banks' deposit ceiling

- PBoC official Ruan Jianhong stated that the money supply was moderate. Slowdown due to seasonal and short-term factors

- Japan and EU said to be signing a trade agreement in mid-July

- S&P revised Japan outlook from stable to positive; affirmed the Sovereign Rating at A+

- IEA Monthly Report maintained its 2018 global oil demand growth forecast at 1.5M bpd with global demand seen at 97.8M. Stated that it seemed OPEC/Non-OPEC members have achieved the target of reducing oil stocks to 5-year average

Currencies

- USD was steady against most pairs aided by higher yields resulting from improved risk appetite

- USD/JPY was at 6-week highs as the pair moved above the 107.50 level.

- The GBP/USD saw its 5th straight session of gains with the pair approaching the 1.43 level for 10-week highs. EUR/GBP cross was lower by 0.3% below 0.8640 as dealers noted that the recent ECB minutes should the debate on "normalizing" its policies appeared to be moving at a glacial pace

- Fixed Income

- Bund Futures trade 7 ticks lower at 159.18 as European markets trade positive. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 121.89 higher by 4 ticks off the highs the seen in early trading. Support continues stands at 121.25 then 120.85, with upside resistance at 123.35 then 123.85.

- Friday’s liquidity report showed Thursday's excess liquidity rose to €1.855T from €1.852T prior. Use of the marginal lending facility increased from €142M to €136M.

- Corporate issuance saw 1 issuer raised $0.6B in the primary market

Looking Ahead

- 05:30 (ZA) South Africa to sell ZAR600M in I/L 2025, 2029 and 2038 bonds

- 06:00 (UK) DMO to sell combined £3.0B in 1-month, 6-month and 12-month Bills (£0.5B, £1.0B and £1.5B respectively)

- 06:30 (IS) Iceland to sell 2022 and 2028 RIKB Bonds

- 06:45 (US) Daily Libor Fixing

- 07:30 (IN) India Weekly Forex Reserves

- 08:00 (PL) Poland Feb Current Account: -€0.4Be v +€2.0B prior; Trade Balance: -€0.5Be v -€0.2B prior; Exports: €16.7Be v €16.9B prior; Imports: €17.2Be v €17.1B prior

- 08:00 (IS) Iceland Mar Unemployment Rate: No est v 2.4% prior

- 08:00 (BR) Brazil Feb IBGE Services Sector Volume Y/Y: -0.6%e v -1.3% prior

- 08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming issuance

- 08:00 (IN) India announces upcoming Bill auction (held on Wed)

- 08:00 (US) Fed’s Rosengren (moderate, non-voter) on economic outlook

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Fed's Bullard (dove, non-voter) speaks at Washington University in St. Louis

- 09:00 (CA) Canada Mar Existing Home Sales M/M: No est v -6.5% prior

- 10:00 (US) Feb JOLTS Job Openings: 6.024Me v 6.312M prior

- 10:00 (US) Apr Preliminary University of Michigan Confidence: 100.5e v 101.4 prior

- 11:00 (EU) Potential sovereign ratings after European close (Poland Sovereign Debt to be rated by S&P; Ireland, Spain and USA Sovereign Debt to be rated by Moody's; Luxembourg Sovereign Debt to be rated by Fitch

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 13:00 (US) Fed’s Kaplan (dove, non-voter)

- (US) Treasury Semi-annual Currency Report

TPP member Japan, Australia, Malaysia told Trump, you’re welcomed but no renegotiation

Trump got slaps straight into his face by some members of the 11 nation Trans-Pacific Partnership today. While member countries welcomed Trump's intention to consider rejoining, they made themselves clear that there will be no renegotiation. That is, take it or leave us alone.

Australia Trade Minister Steven Ciobo said today that "we welcome the U.S. coming back to the table but I don't see any wholesale appetite for any material re-negotiation of the TPP-11."

Japan Minister Toshimitsu Motegi said the current deal is a "balanced one, like fine glassware" and it would be difficult to change.

Malaysia International Trade and Industry Minister Mustapa Mohamed also warned that renegotiation would "alter the balance of benefits for parties."

T11 include Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, Vietnam.

US withdrawn from TPP on 23 January 2017 after Trump signed a Presidential memorandum, less than a month he took office.

Earlier today, Trump tweeted, "Would only join TPP if the deal were substantially better than the deal offered to Pres. Obama. We already have BILATERAL deals with six of the eleven nations in TPP, and are working to make a deal with the biggest of those nations, Japan, who has hit us hard on trade for years!" That came after news that Trump ordered White House economic adviser Larry Kudlow and Trade Representative Robert Lighthizer to examine the benefits of re-entering TPP.

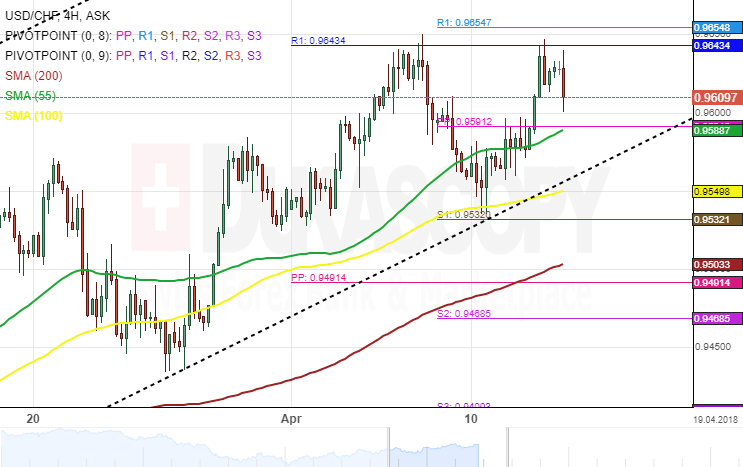

USD/CHF 4H Chart: Encounters Resistance Cluster

The US Dollar has been trading in a descending channel against the Swiss Franc since early November 2017. After reaching the lower boundary of the dominant descending pattern on February 14, the currency pair began to appreciate and has since remained bullish.

The exchange rate has been guided up by the 55– and 100-hour simple moving averages. However, the pair has encountered a resistance cluster set by the monthly R1 and the weekly R1 at the 0.9643 area.

As for near future, it is expected the currency exchange rate to breach and move past the aforementioned resistance cluster. In addition, technical indicators favour bulls to grow stronger during the following trading sessions.

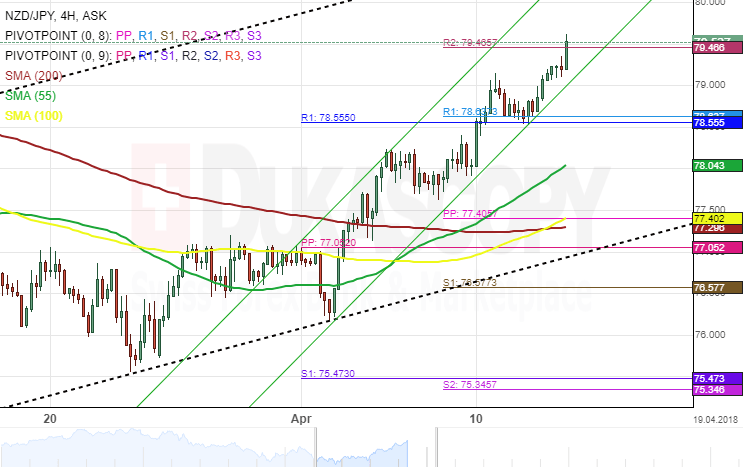

NZD/JPY 4H Chart: Junior Channel Expected To Prevails

The New Zealand Dollar has been trading in a one-month ascending channel against the Japanese Yen after the currency pair bounced off the lower boundary of a dominant channel.

The NZD/JPY exchange rate continues to maintain its ascending pattern and is gradually moving upward for a test of the upper boundary of the dominant descending channel. Meanwhile, the currency pair has moved past a strong resistance cluster formed by the combination of the weekly and the monthly pivot points near the 78.55 mark.

The overall market sentiment is bullish, therefore, the pair is likely to continue its upside movement during the following trading sessions.

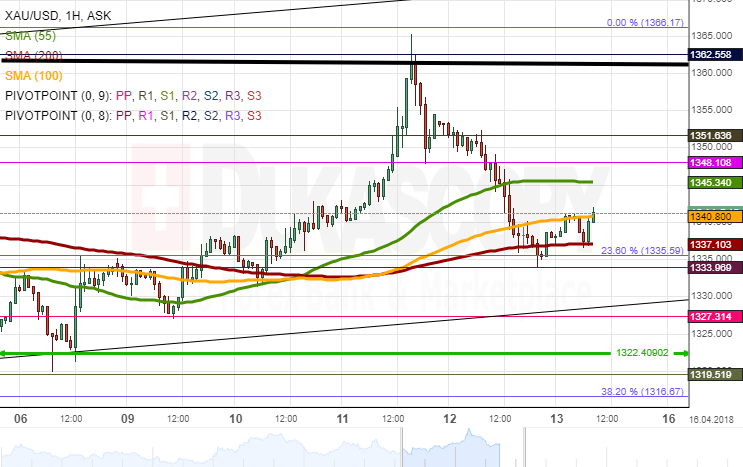

XAU/USD Analysis: Continues Its Decline

Following a massive surge earlier this week, bears have maintained their dominance in the market since late Wednesday.

The yellow metal fell 1.41% against the Greenback during the previous session and breached the 55– and 100-hour SMAs. Its subsequent support level, set by the 23.60% Fibo retracement and the 200-hour SMA, was not surpassed, thus leaving the rate near the 1,340.00 mark this morning.

Technical indicators remain bullish, suggesting that this cluster could remain intact. In addition, the pair is likely to be hindered near the 55-hour SMA and, if surpassed, no additional resistance barriers until 1,360.00 are located in between.

By and large, this session might not introduce significant volatility in the market, as no fundamental data releases are scheduled.

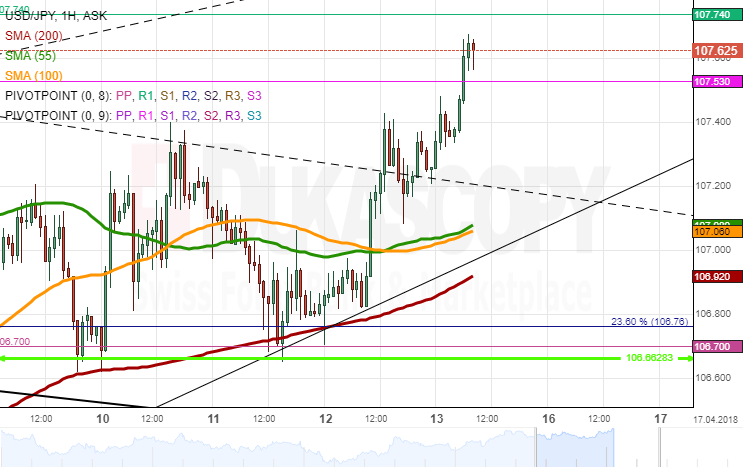

USD/JPY Analysis: Moves Toward 108.00

Being stranded by the 55-, 100– and 200-hour SMAs, USD/JPY entered a minor period of consolidation on Thursday morning. Strong bullish momentum mid-session contributed to a northern breakout and subsequently led the pair even up to the 107.50 mark where the monthly R1 is located.

It is likely that the US continues to appreciate against the Yen during the following hours. The nearest resistance is set by the weekly R1 and the 38.20% Fibo retracement at 107.75 and 108.08, respectively.

However, bulls might soon exhaust their strength and go for a minor correction during the second part of the day, as technical indicators are gradually moving towards the overbought territory. This decline is unlikely to surpass 107.00 due to several important support levels being located there.