Sample Category Title

Dollar rebounds as Trump tweaks the meaing of his own tweet

Dollar rebounds after Trump backed down from his initial tough/high pressure position again. This time is about Syria. In his usual morning tweet, Trump said: "Never said when an attack on Syria would take place. Could be very soon or not so soon at all! In any event, the United States, under my Administration, has done a great job of ridding the region of ISIS. Where is our 'Thank you America?'"

At around the same time just yesterday, Trump tweeted "Russia vows to shoot down any and all missiles fired at Syria. Get ready Russia, because they will be coming, nice and new and 'smart!' You shouldn't be partners with a Gas Killing Animal who kills his people and enjoys it!"

These tweets reminded me of an old friend. We're supposed to meet at a certain time but he's not around past 30 mins or so. I called and asked, "hey are you coming?" And he said "yeah, I'm coming!". After waiting for an hour, I called again and asked "hey you said you're coming, didn't you?" Then he answered, "yeah I'm coming. But I could come soon or not so soon at all!" Well, we're never friends again since then.

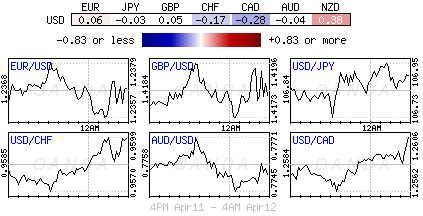

Anyway, from the 4H heatmap, USD's strength is centered against EUR, JPY and, CHF and NZD. EUR/USD looks safe for the momentum as it's holding well above 1.2303 minor support. USD/JPY is at around the mid-point of range of 106.61/107.48. The more imminent move could be find in USD/CHF considering that EUR/CHF also resumed the medium term up trend yesterday.

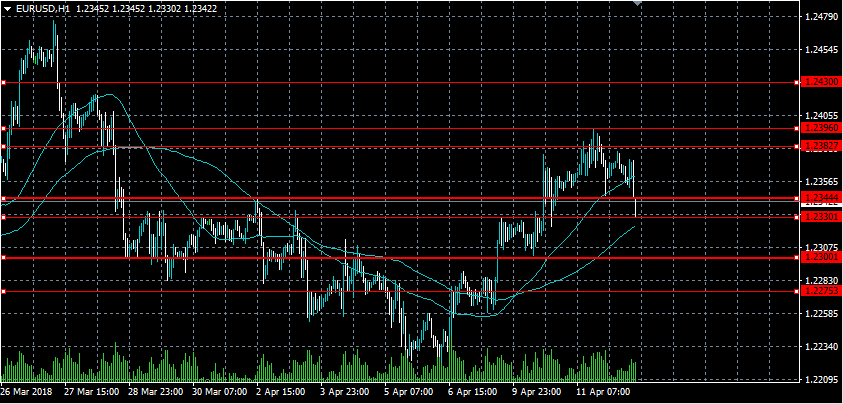

EURO Testing Key Daily Support

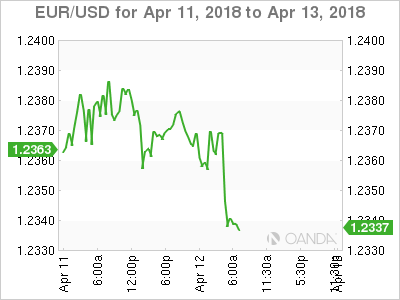

The euro has moved lower against the U.S dollar during the European trading session, following weaker than expected eurozone data and a rebound higher in the U.S dollar index. The EURUSD pair has seen dip buying demand from lower levels, with the key 1.2333 level surviving its first technical test, although downside pressures continue to build. Traders now look towards weekly jobs data from the United States, with the 1.2333 to 1.2382 price-range in focus.

The EURUSD pair will turn intraday bearish below the 1.2333 level, key support is located at the 1.2300 and 1.2275 regions.

Should price-action on the EURUSD pair managed to hold above the 1.2333 level, buyers will likely test back towards the 1.2382 and 1.2396 levels.

Dollar Sees Some Gains As Kremlin Calms War Tensions, ECB Meeting Minutes Next

Here are the latest developments in global markets:

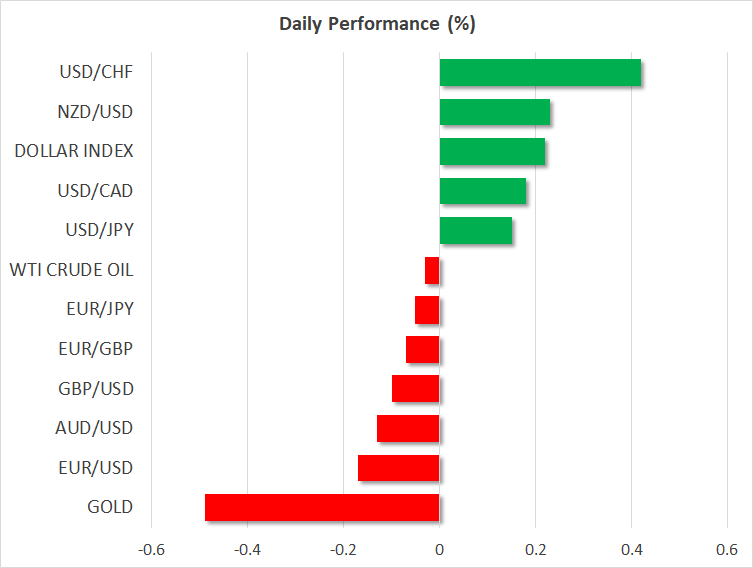

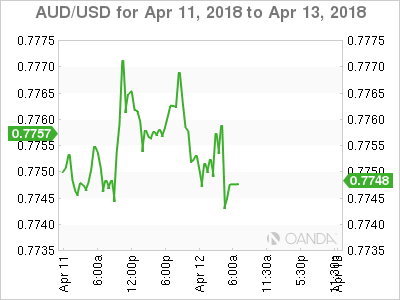

FOREX: An exchange of war words between the two nuclear-armed powers, the US and Russia yesterday regarding strikes in Syria continued to weigh on the dollar during early European afternoon despite the FOMC minutes from the March meeting embracing a positive outlook on the economy. Still, comments by the Kremlin today, supporting that further tensions in Syria should be avoided, eased somewhat the risk-off sentiment. The dollar index rose to 89.77 but remained near two-week lows (+0.23%), while dollar/yen climbed to 106.94 (+0.14%). Euro/dollar inched down to 1.2339 (-0.20%) ahead of the ECB meeting minutes due later today, pressured by worse-than-expected industrial figures out of the Eurozone, which slowed down for the third consecutive month, reaching the lowest yearly growth since August 2017. Pound/dollar was also on the backfoot, changing hands lower at 1.4147 (-0.22%) despite the UK Brexit Minister saying that the financial sector will face fewer job losses after the exit from the EU than previously thought. Aussie/dollar retreated further to 0.7742 (-0.14%) in contrast to its cousin kiwi/dollar which moved higher to 0.7373 (+0.24%) after RBNZ assistant governor John McDermott expressed on Thursday that the addition of the employment goal to the RBNZ’s mandate reinforces inflation flexibility. Dollar/loonie climbed to 1.2606 (+0.22%). Swedish krona tumbled after CPI readings out of Sweden missed forecasts, with dollar/krona surging to a one-week high of 8.4097 (+0.97%).

STOCKS: European equities opened weaker on Thursday as risk aversion persisted given rising concerns over a war in the Middle-East and the hawkish tone of the FOMC meeting minutes. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.09% and 0.20% respectively at 0830 GMT, with all sectors being in the red except financials, energy and utilities. The German DAX 30 declined by 0.13%, the French CAC 40 fell by 0.16% and the British FTSE 100 inched down by 0.03%. The Italian FTSE MIB, though, managed to jump by 0.31% after news that Playtech, a gambling software developing company, agreed to buy the Italian betting firm Snaitech. Asian stocks closed mixed, while indices tracking US stock futures were in the red, pointing to a negative open.

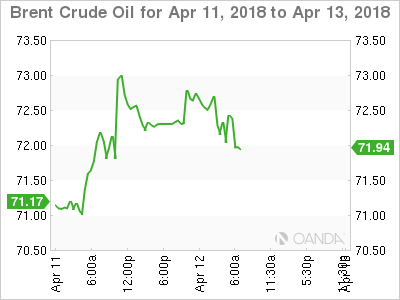

COMMODITIES: Oil paused yesterday’s rally which took prices to three-year highs, with WTI crude standing flat at $66.82 (+0.01%) per barrel and the London-based Brent slipping to $71.93 (-0.17%). Geopolitical risks, though, continued to underpin the market. Early today Saudi Arabian air forces reported that they had intercepted missiles in Riyadh fired by Yemen a day after Trump warned to take military actions against the Syrian government which is backed by Russia and Iran.

Day Ahead: ECB meeting minutes pending; US releases jobless claims

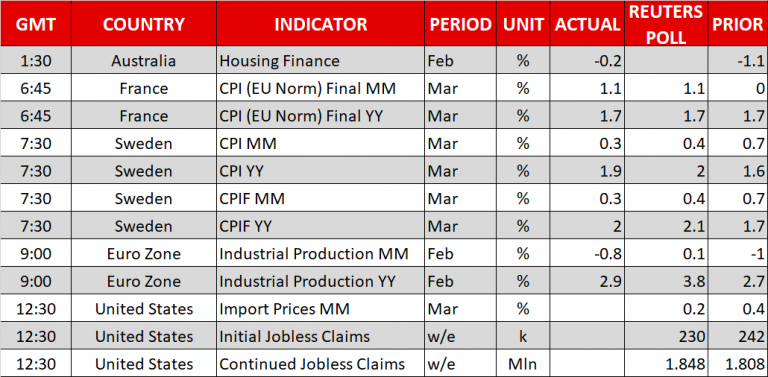

The main economic event later today will be the release of the European Central Bank (ECB) monetary policy accounts from the March 7-8 meeting (1130 GMT). At that meeting, the central bank kept its monetary strategy unchanged as was widely anticipated but dropped out of the statement its easing bias that officials stand ready to increase QE in terms of size and duration if the outlook becomes less favorable. The central bank has already taken some steps to reduce record stimulus by lowering the amount of monthly asset purchases, while recent headlines indicated that policymakers have shifted focus to interest rates as well, with ECB council member Ewald Nowotny saying a few days ago that the ECB could raise deposit rates by as much as 20bps when the rate hike process starts. However, an ECB spokesman played down this view afterwards. In forex markets, the euro could take a boost if the minutes prove hawkish, but if they disappoint the common currency could head lower.

Out of the US, initial jobless claims will come out at 1230 GMT and expectations are for the measure to drop to 231k in the week ending April 6 from 242k in the preceding week. Moreover, data on import and export prices for March will be published at the same time.

In Canada, investors will take a look at the new housing price index for the month of February at 1230 GMT.

As of today’s public appearances, ECB Executive Board member Benoit Coeure will be delivering remarks at 1215 GMT that will be closely monitored by investors after the release of meeting minutes. Comments by ECB Vice President Vitor Constancio and Bundesbank President Jens Weidman will follow at 1400 GMT.

Asset manager BlackRock is among companies releasing quarterly results on Thursday.

Moreover, any developments on global trade can spur positioning in equity markets; China’s commerce ministry said today that trade talks would be impossible as Washington’s attempts at dialogue were not sincere.

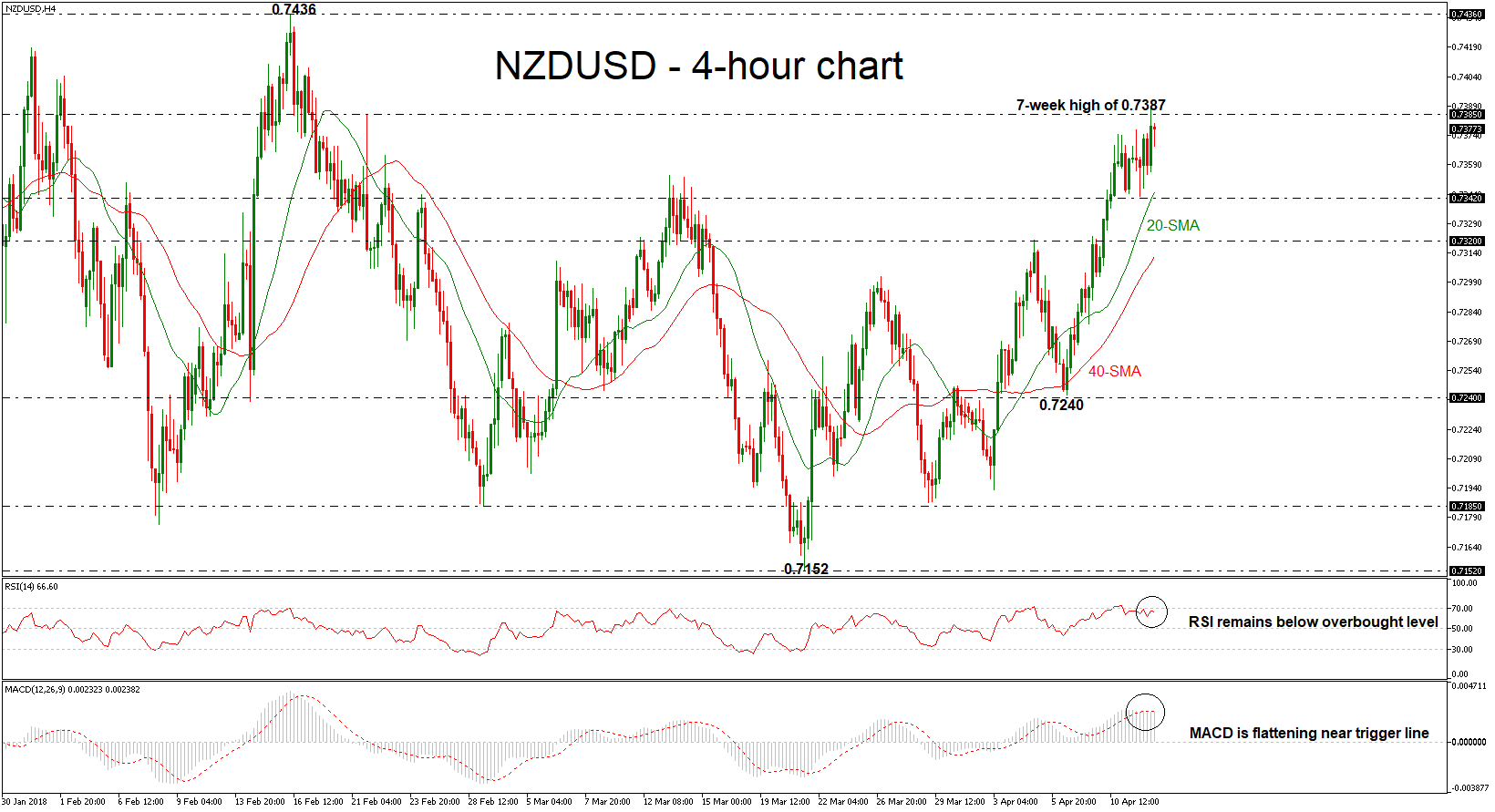

NZDUSD Holds Near 7-Week High, Momentum Indicators Look Neutral

NZDUSD surged to a 7-week high of 0.7387 during today’s European session following the aggressive buying interest that started after the rebound on the 40-day simple moving average of 0.7240 last Friday. The technical indicators, though, are sending neutral to bearish signals, suggesting that the strengthening of the market is weakening.

In the 4-hour chart, the Relative Strength Index (RSI) has flattened near overbought levels, indicating that the market could weaken a little bit in the short-term until the index jumps above that threshold. The MACD oscillator supports a neutral picture, as well, as the index,continues to flatten near its red-trigger line.

If the market manages to pick up speed and jumps above the 0.7385 resistance level, it could open the door towards the 0.7436 strong barrier. A significant run above the aforementioned obstacle could extend gains until the 0.7560 peak, taken from the high of July 2017.

Should prices decline, immediate support could be found around 0.7342 support, which holds near the 20-day simple moving average (SMA). A close below this level could slip the pair until the next support at 0.7320, raising chances for further losses. In case of further downside pressure, prices could slip towards the 0.7240 support.

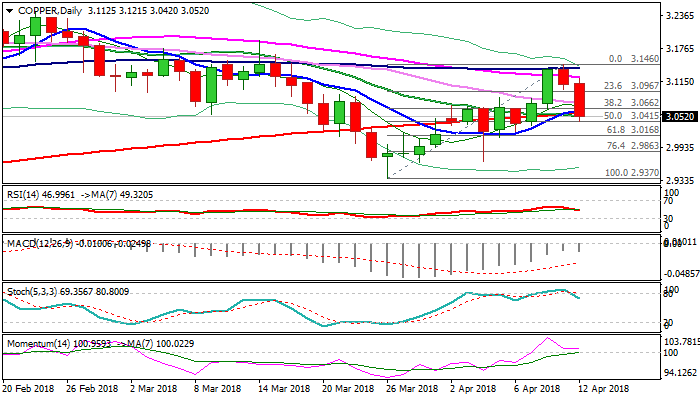

COPPER Extends Weakness On Thursday, Down Nearly 2% As Traders Took Profits On Fears Of Escalation Of Tensions In...

Copper was sharply lower on Thursday, extending pullback Wednesday’s one-month high at $3.1460, being down nearly 2% for the day so far.

Investors fear from situation in Syria which could escalate and took profit from 2 ½ week rally from $2.9370 which stalled at strong barrier at $3.1434 (Fibo 61.8% of $3.2710/$2.9370 descend), also failing to clearly break above 100SMA ($3.1392).

Fresh bearish acceleration turned near-term studies into bearish mode, while daily picture also weakened as MA’s are back to negative setup and slow stochastic is heading south after reversal from overbought zone and showing a plenty of room at the downside.

Fresh weakness so far retraced 50% of $2.9370/$3.1460 rally, where temporary footstep was found, but could extend further to test $3.0168 (Fibo 61.8%) and psychological $3.00 support.

Close below cracked 200SMA ($3.0578) is needed to confirm scenario, while upticks should be capped by falling 30SMA ($3.0768) to keep fresh bears intact.

Res: 3.0578, 3.0768, 3.0817, 3.0940

Sup: 3.0420, 3.0345, 3.0168, 3.0000

Markets Pare Losses After Trump’s Syria Tweets

- Caution Remains Even as Initial Concern Passes;

- Fed Minutes Confirm More Hawkish Stance;

- ECB Minutes, Carney Speech and US Jobless Claims on the Agenda Today.

'With a possible trade war and conflict with Russia over Syria on the horizon, it’s no wonder investors aren’t feeling particularly bullish right now'

Financial markets have settled down again on Thursday following another flare up a day earlier when US President Donald Trump threatened retaliation against Syrian use of chemical weapons.

Markets were already in slight risk averse mode ahead of the Tweet from the US President, with the trade conflict with China continue to drag on risk appetite, but the announcement triggered another drop which indices only marginally managed to recover from. Ahead of the open on Wall Street, futures are posting gains over around one tenth of one percent, only a small percentage of the losses suffered on Wednesday.

With a possible trade war and conflict with Russia over Syria on the horizon, it’s no wonder investors aren’t feeling particularly bullish right now. That said, I still believe the chances of either – yet alone both – actually materialising are relatively slim which may stop the sell-off in equities getting out of hand.

'It would appear the central bank has laid the groundwork for another rate hike in June'

The Federal Reserve minutes on Wednesday offered relatively new of note although they do appear to have given some support to the dollar in the near-term. It’s not surprising to see that policy makers were feeling increasingly hawkish, given the revisions to rate, inflation and growth forecasts, or that they were cautious about the impact a trade war could have on the economy.

It would appear the central bank has laid the groundwork for another rate hike in June which would leave them six months to implement the third that is forecast and also leave room for a fourth if it’s deemed necessary by the data in the interim. That may be providing some relief for the greenback in the near-term but it’s really struggling to gather any upward momentum, although at least the sell-off has temporarily stalled in recent months.

We have one of the quieter agenda’s on the cards today, with the only economic release in the US being the weekly jobless claims report. We will also get the minutes from the recent ECB meeting, although I don’t expect much to come from these that we don’t already know, with the central bank likely using one of the upcoming meetings to hint at what to expect post-September. Bank of England Governor Mark Carney will speak later on which will be of interest given the expectation that they will raise interest rates in May.

Euro Edges Lower, Investors Eye ECB Minutes

EUR/USD continues to post slow but steady gains. In the Thursday session, the pair is trading at 1.2341, down 0.22% on the day. On the release front, Eurozone Industrial Production disappointed with a second straight decline. The reading of -0.8% fell short of the estimate of 0.1%. Later in the day, the ECB releases the minutes of its March rate meeting. In the US, the key event of the day is unemployment claims, which is expected to drop to 231 thousand. On Friday, Germany releases Final CPI and the US publishes UoM Consumer Sentiment.

Investors are casting a wary eye on developments in Syria. Last week, Syrian forces allegedly used chemical weapons against rebel positions, and a UN Security Council meeting on Tuesday ended inconclusively after Russia cast a veto on a US proposal to probe the attack. US President Trump has warned that a US response is imminent, and Russia has countered that it will respond to any US move. If Trump makes good on his promise, investor risk appetite could sink and impact on the currency markets.

The Federal Reserve minutes were hawkish in tone, a reflection of a strong US economy. All of the Fed policymakers indicated that the US economy would continue to improve and that inflation would rise in the next few months. At the March meeting, the Fed unanimously voted to raise rates by a quarter-point, bringing the benchmark rate to a range between 1.50% and 1.75%. The Fed projection for rate policy in 2018 remains at three hikes, although there is speculation that the Fed could revise the forecast to four rate hikes. Last week, Fed Chair Jerome Powell said that the Fed would likely continue to raise rates in order to keep a lid on inflation, but added that the rate moves would be gradual. A new headache for the Fed is the escalating trade battle between the US and China, which could hurt the economy and raise consumer prices. Next on the menu? The Fed is expected to sit tight in May and raise rates at the June meeting.

Dollar Gains Limited By Geopolitical Risks

Capital markets remain uneasy as growing geopolitical tensions rattle equities and commodities. Adding fuel to the fire is yesterday’s FOMC’s March meeting minutes showing that most officials are leaning towards a faster pace of tightening as their growth outlook and confidence in hitting inflation targets strengthened.

“The appropriate path for the federal funds rate over the next few years would likely be slightly steeper than they had previously expected,” the FOMC said in its March minutes. Most Fed officials penciled in two or three more moves this year, and didn’t see a significant effect from steel and aluminum tariffs.

Fed officials expect the Republican tax plan to deliver “a significant boost” to the economy over coming years, though some expressed wariness about its fiscal sustainability – higher budget deficits could eventually drive up interest rates and pose a threat to the U.S economic outlook.

Elsewhere, U.K ministers are planned to gather later this morning to discuss whether to join the U.S and France in a possible military attack on Syria that threatens to bring the west and Russian forces into direct confrontation.

1. Global equities see red

Euro equities are drifting after Asian shares declined as investors digested the latest signals from the U.S Fed on monetary policy and escalating tensions in the Middle East.

In Japan, stocks pulled back overnight as worries about possible U.S military action against Syria curbed investor risk appetite, while earnings reports kept the retail sector in the spotlight. The Nikkei share average ended down -0.1% while the broader Topix lost -0.4%.

Down-under, the Aussie’s shares slid overnight on the threat of an imminent U.S attack on Syria and China’s commerce ministry saying that trade negotiations with the U.S would be impossible. The S&P/ASX 200 index slipped -0.2%, while in S. Korea, the Kospi fell -0.06%.

In Hong Kong, stocks shed early gains to end lower on Thursday, as caution prevailed amid rising tensions in the Middle East. The Hang Seng index closed down -0.2%, while the China Enterprises Index ended -0.3% lower.

In China, stocks ended lower on Thursday, weakened by financial and transport stocks, as investors were rattled about possible U.S military action in the Middle East. The blue-chip CSI300 index ended down -1%, while the Shanghai Composite Index closed -0.9% lower.

In Europe, regional indices trade flat to slightly lower, with a bout of M&A news offsetting Middle Eastern tensions.

U.S stocks are set to open in the ‘red’ (-0.1%).

Indices: Stoxx600 -0.2% at 375.7, FTSE -0.1% at 7249, DAX -0.1% at 12277, CAC-40 -0.2% at 5270.3, IBEX-35 -0.2% at 9713, FTSE MIB +0.3 at 23069, SMI flat at 8707, S&P 500 Futures -0.1%.

2. Oil retreats from three-year highs

Oil prices trade atop of their three-year highs, with U.S futures jumping as much as +3%yesterday amid the geopolitical turmoil.

Brent crude futures are at +$71.70 a barrel, down -36c from their last close. U.S WTI crude futures are down -20c at +$66.62.

Note: Both Brent and WTI on Wednesday hit their highest since late 2014 at +$73.09 and +$67.45 a barrel respectively after the Saudi’s said it intercepted missiles over Riyadh and President Trump warned Russia of imminent military action in Syria.

Technically, geopolitical fears continue to push crude oil fundamentals aside.

Data this week showed that U.S crude oil inventories rose by +3.3m barrels to +428.64m barrels, while U.S crude production last week hit a record +10.53m bpd. The U.S now produces more crude oil than top exporter Saudi Arabia. Only Russia, at nearly +11m bpd, pumps more.

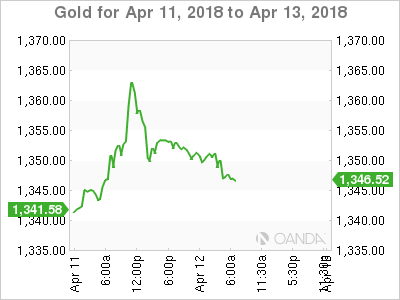

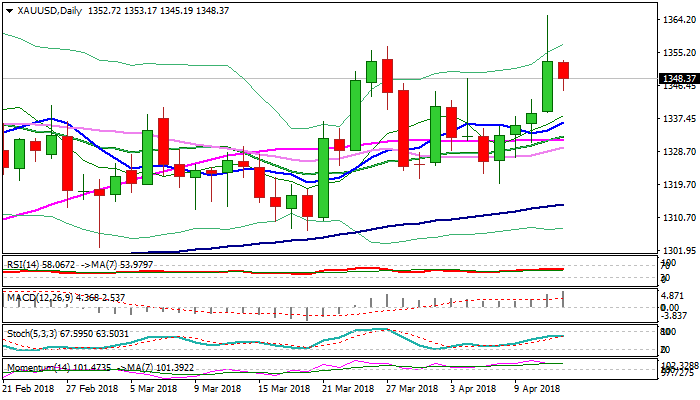

Ahead of the U.S open, gold prices have eased off their multi-week highs overnight as yesterday’s FOMC minutes have raised expectations for a faster pace of U.S rate hikes. Spot gold is down -0.1% at +$1,351.48 an ounce, while U.S gold futures fell -0.4% to +$1,355 an ounce.

3. U.S yield curve flattens

FOMC minutes yesterday showed officials leaning towards a slightly faster pace of tightening at their March meeting as their growth outlook and confidence in hitting inflation targets strengthened.

The yield on U.S 10-year Treasuries dipped -1 bps to +2.78%, while the yield on U.S two-year Treasuries fell less-1 bps to +2.30%. The spread, at +48 bps is the tightest in over a decade.

Elsewhere, Germany’s 10-year Bund yield declined -1 bps to +0.50%, the lowest in more than three-months.

Down-under, the Reserve Bank of Australia (RBA) plays it straight with its own rate outlook. In his speech yesterday, RBA Gov. Lowe’s said that the economy is likely to improve, the next rate move is probably up, and only a gradual pickup in wages and prices is expected. On top of that, Lowe said the RBA board does not see a strong case for a near-term adjustment in monetary policy.

4. Dollar pares Fed gains

EUR/USD (€1.2336) trades relatively flat ahead of the U.S open, in a quiet market overnight, with the U.S still weighing its options on Syria.

The USD rallied immediately after the Fed minutes were published on Wednesday, given that quite a few members seemed in favour of higher interest rates.

Since then, the EUR/USD has nearly recovered its level prior to the minutes. The USD/JPY is also flat, at ¥106.84. Later this morning, the ECB minutes are published and market is anxious to see whether any early discussions on rates took place.

Elsewhere, GBP/USD is steady at £1.4170, while the EUR/SEK (€10.3860) hit a nine-year high after Sweden’s March CPI came in below expectations. Many are beginning to push back their view for the first potential rate hike by Sweden Riksbank from Sept to Dec.

In Russia, the RUB rout continues – triggered by the most punitive U.S penalties to date. The currency has slumped to a 16-month low and yields on local debt surged to the highest level this year.

5. Eurozone industrial production declines again

Data this morning showed that industrial production (IP) in the eurozone fell for a third consecutive month in February, an indication that economic growth may be slowing as the ECB faces key decisions over its stimulus programs.

Euro stats showed that the output of factories, mines and utilities was -0.8% lower than in January, the largest m/m drop in two years. The markets expectations were for a +0.2% increase.

Note: In December, IP fell by -0.1%, and in January by -0.6% – the three-month stretch of declines was the longest since September through November 2012.

Some of the weakness in IP reflects temporary factors that should not act as a drag on growth in the months to come. A spell of unusually cold weather across Europe has been a hindrance to activity.

Signs of weaker growth supports ECB Draghi’s view that the central bank needs to move cautiously as its phases out QE.

Spot Gold Pulls Back On Easing Geopolitical Tensions But Keeps Bullish Bias

Gold price holds in red on Thursday and eases from new high at $1365 (the highest since 25 Jan), posted on Wednesday in strong safe-haven rally. Traders booked profits of strong four-day rally, as immediate threats of escalation of Syria conflict eased. The pullback is seen as corrective and positioning for fresh upside action, however, could extend lower as pivotal support at $1348 (Fibo 38.2% of $1319/$1365 rally has been broken. Extended dips should ideally find footstep at $1342 (Fibo 50%/10 Apr high) to keep bulls intact. Renewed attempt higher need to clearly break $1354 pivot which kept upside attempts in past few months limited, as several probes failed to close above. Strong bullish signal would be generated on eventual close above $1354 for probe through multi-month congestion ceiling at $1366 and attack at July 2016 peak at $1375. Bullish techs support scenario, however geopolitical situation is expected to be the main driver.

Res: 1350, 1354, 1361, 1365

Sup: 1345, 1342, 1337, 1333

Euro Zone Data Continues To Miss Expectations

Notes/Observations

- Markets wrestling with positive tone struck with regards to US-China trade negotiations and the escalation of rhetoric between the US and Russia

- European economic data continues to miss expectations and further off cycle highs

- Miss in Sweden CPI data pushes off expectations of a potential summer rate hike

Asia:

- Bank of Korea (BOK) left its 7-Day Repo Rate unchanged at 1.50% (as expected). A stronger won currency could reduce room for policy rate increase; FX rate not the only factor for monetary policy

- Bank of Japan (BOJ Gov Kuroda reiterated that to maintain QQE with yield curve control for as long as needed to reach 2% inflation in stable manner

- BoJ Executive Dir Maeda: BOJ was moving steadily toward CPI goal; reiterated to continue monetary easing persistently as was still distant from price target. Medium and long-term inflation expectations were emerging from weakness.

- Japan govt said to be looking at new budget balancing goal by mid-2020 (Reminder: In late Jan, Japan Cabinet confirmed that the government would push back its forecast for achieving a primary budget surplus by two years to FY26/27)

- China Commerce Ministry (MOFCOM) official Gao stated that was misleading to say Tuesday’s speech by President Xi was a concession to the US on trade issue. China to retaliate without doubt if US escalated disputes

- PBoC Gov Yi Gang: Q1 data has been a bit better than expected (Note: China Q1 GDP release expected Apr 17th)

- World bank raises 2018 China GDP forecast to 6.5% from 6.4%

Europe:

- Germany said to advocate ECB place tougher bad loan standards on banks

Americas:

- FOMC Minutes from Mar 21st policy meeting showed that All policymakers believed that further tightening policy likely warranted, almost all agreed gradual approach appropriate

- White House econ adviser Kudlow stated that China Pres Xi's speech this week was very important; was first time that China made a positive statement about trade. US economic growth may be “soft” in Q1 but should rebound of the rest of the year

Economic Data:

- (RO) Romania Mar CPI M/M: 0.3% v 0.2%e; Y/Y: 5.0% v 4.9%e

- (FR) France Mar Final CPI M/M: 1.0% v 1.0%e; Y/Y: 1.6% v 1.5%e

- (FR) France Mar Final CPI EU Harmonized M/M: 1.1% v 1.1%e; Y/Y: 1.7% v 1.7%e, CPI Ex-Tobacco Index: 102.42 v 102.40e

- (SE) Sweden Mar CPI M/M: 0.3% v 0.3%e; Y/Y: 1.9% v 2.0%e

- (SE) Sweden Mar CPIF M/M: 0.3% v 0.4%e; Y/Y: 2.0% v 2.1%e, CPI Level: 325.76 v 326.10e

- (SE) Sweden Mar Average House Prices (SEK): 3.033M v 3.164M prior

- (GR) Greece Jan Unemployment Rate: 20.6% v 20.8% prior

- (EU) Euro Zone Feb Industrial Production M/M: -0.8% v +0.1%e; Y/Y: 2.9% v 3.5%e

Fixed Income Issuance:

- (SE) Sweden sold SEK500M in I/L 2032 bonds; Avg Yield: -0.7603% v -0.4304% prior; Bid-to-cover: 3.14x v 3.74x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.2% at 375.7, FTSE -0.1% at 7249, DAX -0.1% at 12277, CAC-40 -0.2% at 5270.3, IBEX-35 -0.2% at 9713, FTSE MIB +0.3 at 23069, SMI flat at 8707, S&P 500 Futures flat]

- Market Focal Points/Key Themes: European Indices trade flat to slightly lower, with a bout of M&A news offsetting Middle Eastern tensions. On the M&A front Playtech trades higher after acquiring Snaitech, FirstGroup rises after rejecting a proposal from Apollo, DFDS is another notable gainer after acquiring UN Ro-Ro and raising their outlook, with Countrywide another gainer after acquiring Westleigh Group. On the earnings front French Supermarket giant Carrefour drops over 5% after a slight miss in Q1 results, while GEA and Gerresheimer are other notable fallers. Man Group, Dunelm and Stolt Nielson are among the gainers following results. In Switzerland Sulzer rises after Renova's stake dropped below 50% and as a result no long blocked by US sanctions. Looking ahead notable earners include Airline giant Delta, Blackrock and Rite Aid.

Movers

- Consumer Discretionary [Carrefour [CA.FR] -5.6% (Earnings), Carpetright [CPR.UK] -4% (CVA Proposal and Equity capital raise update), Dunelm [DNLM.UK] +10.8% (Earnings), Sodexo [SW.FR] -1.5% (Earnings), Stolt Nielsen [SNI.NO] +2.2% (Earnings)]

- Industrials [Sulzer [SUN.CH] +12% (Renova (Russian oligarch) ownership is below 50%; No longer blocked party by US sanctions), DFDS [DFDS.DK] +6.1% (Acquisition, raised outlook), GEA Group -7% (prelim earnings), Gerresheimer [GXI.DE] -4.7% (Earnings)]]

- Financial [Man Group [EMG.UK] +6.5% (FUM update)]

- Technology [ Playtech [PTEC.UK] +8.6% (Acquistion)]

Speakers

- German Economic Ministry Monthly Report: Domestic economy continued with a solid upturn but at a slightly weaker pace. Exporters were less upbeat to due strong Euro currency. Trade conflict brought heightened risks

- Bank of England (BOE) Q1 Credit Conditions & Bank Liabilities Surveys. Total cost of bank funding increased a little in 2018 Q1 but remained low by historic standards. Availability of unsecured credit to consumers declined in quarter

- Norway Central Bank (Norges) Gov Olsen reiterated view that 1st potential rate hike was drawing closer (seen after summer) as inflation was on the way to gradual improvement.

- UK Brexit Min Davis: Virtually nothing will change for business during the transition period. Expected a lot of detail in a negotiated deal later this year. Parliament would not accept a Brexit deal without a vision for the future. Believed that a possibility of a no deal Brexit was a tiny percentage. Trade argument with EU will be about regulation, not tariffs. Aimed for invisible border on Ireland, not no border

- German CDU member Brinkhaus: EU Commission and Germany were far apart on Euro reforms

- ECB again lowered the emergency liquidity assistance (ELA) cap for Greece banks from €16.6B to €14.7B

- European Council said to extend sanctions on Iran by another year. Extended the travel ban and assets freeze against 82 people

- Russia Central Bank official Lipion: All options were on the table for rate decisions. Higher RUB currency (Ruble) might increase inflation expectations. No risk of not meeting monthly FX purchase plan

- China State Council guideline on implementing work Report reiterated its prudent but neutral monetary policy stance and proactive fiscal policy. Reiterated stance to keep reasonable growth of M2 money supply and credit

- Japan rating agency JCR raised South Korea sovereign rating from A+ to AA-; outlook stable

- India Finance Ministry official: To track yield for additional time before acting (**Note: Yields have been rising). Sudden spurt in yields had been a surprise and due to State bank issuance. Could not ask State banks for more active market participation

Currencies

- FX price action was subdued during the session. Markets wrestling with positive tone struck with regards to US-China trade negotiations and the escalation of rhetoric between the US and Russia.

- EUR/USD was lower 0.2% after more European data missed expectations. The pair at 1.2335 area after Euro Zone IP data came in below expectations. Analysts also noted that the Fed Minutes had a hawkish tilt which helped the greenback offset recent weakness on geopolitical concerns

- GBP/USD steady at 1.4170 while USD/JPY was little changed at 106.85 just ahead of the NY morning.

- The SEK currency was softer after Sweden Mar CPI came in below expectations. EUR/SEK cross hit a 9-year high just under the 10.38 area. Some analysts pushed back their view for 1st potential rate hike by Sweden Central Bank (Riksbank) from Sept to Dec

Fixed Income

- Bund Futures trade 8 ticks higher at 159.44 as European markets trade mixed amid Middle East tensions. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 122.49 lower by 2 ticks off the highs the seen in early trading. Support continues stands at 121.25 then 120.85, with upside resistance at 123.35 then 123.85.

- Thursday’s liquidity report showed Wednesday's excess liquidity fell to €1.852T from €1.858T prior. Use of the marginal lending facility increased from €53M to €136M.

- Corporate issuance saw no deals priced in the primary market

Looking Ahead

- (IT) Italy Debt Agency (Tesoro) to sell €7.25-9.25B in 2021, 2025, 2038 and 2048 BTP Bonds

- 05:30 (ZA) South Africa Feb Total Mining Production M/M: No est v 1.0% prior; Y/Y: No est v 2.4% prior; Gold Production Y/Y: No est v -7.7% prior; Platinum Production Y/Y: No est v -13.6% prior

- 05:30 (HU) Hungary Debt Agency (AKK) to sell bonds (3 tranches)

- 06:00 (IE) Ireland Mar CPI M/M: No est v 0.9% prior; Y/Y: No est v 0.5% prior

- 06:00 (IE) Ireland Mar CPI EU Harmonized M/M: No est v 0.9% prior; Y/Y: No est v 0.7% prior

- 06:00 (IE) Ireland Feb Property Prices M/M: No est v 0.9% prior; Y/Y: No est v 12.5% prior

- 07:00 (UR) Ukraine Central Bank Rate Decision: Expected to keep Key Rate unchanged at 17.00%

- 07:10 OPEC Monthly Report

- 07:30 ECB Account of March Policy Meeting

- 08:00 (BR) Brazil Feb Retail Sales M/M: 0.7%e v 0.9% prior; Y/Y: 3.5%e v 3.2% prior

- 08:00 (BR) Brazil Feb Broad Retail Sales M/M: +0.5%e v -0.1% prior; Y/Y: 6.1%e v 6.5% prior

- 08:00 (IN) India Mar CPI Y/Y: 4.2%e v 4.4% prior

- 08:00 (IN) India Feb Industrial Production Y/Y: 6.8%e v 7.5% prior - 08:05 (UK) Baltic Dry Bulk Index

- 08:15 (FR) ECB's Coure (France) in Paris

- 08:30 (US) Initial Jobless Claims: 230Ke v 242K prior; Continuing Claims: 1.84Me v 1.808M prior

- 08:30 (US) Mar Import Price Index M/M: 0.1%e v 0.4% prior; Y/Y: 3.8%e v 3.5% prior; Import Price Index ex Petroleum M/M: 0.2%e v 0.5% prior

- 08:30 (US) Mar Export Price Index M/M: 0.2%e v 0.2% prior; Y/Y: No est v 3.3% prior

- 08:30 (CA) Canada Mar Teranet/National Bank HPI M/M: No est v -0.1% prior; Y/Y: No est v 7.5% prior, HPI Index: No est v 218.90 prior

- 08:30 (CA) Canada Feb New Housing Price Index M/M: 0.1%e v 0.0% prior; Y/Y: 3.0%e v 3.2% prior

- 08:30 (US) Weekly USDA Net Export Sales

- 09:00 (RU) Russia Gold and Forex Reserve w/e Apr 6th: No est v $457.7B prior

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 11:30 (NO) Norway Central Bank (Norges) Dep Gov Nicolaisen in Oslo

- 12:00 (DE) ECB's Weidmann (Germany) in Berlin on strengthening Euro

- 13:00 (US) Treasury to sell 30-Year Bonds Reopening

- 14:00 (MX) Mexico Central Bank (Banxico) Interest Rate Decision: Expected to leave Overnight Rate unchanged at 7.50%

- 15:00 (AR) Argentina Mar National CPI M/M: 2.1%e v 2.4% prior; Y/Y: No est v 25.5% prior

- 15:00 (UK) BOE Gov Carney speaks at Canada Growth Summit in Toronto