Sample Category Title

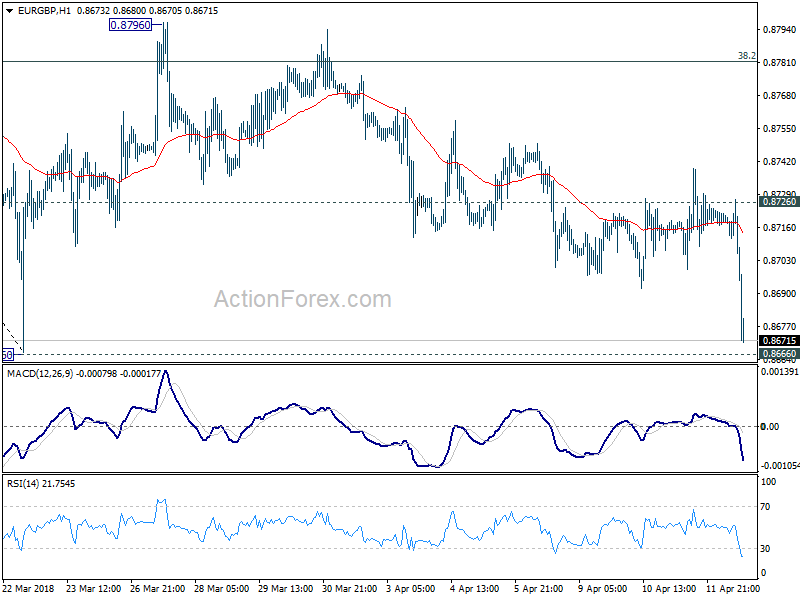

EURGBP: Vulnerable, Weakens

EURGBP - The pair faces further downside pressure leaving risk lower. Support lies at the 0.8650 level where a violation will turn focus to the 0.8600 level. A break will expose the 0.8550 level. Its daily RSI is bearish and pointing lower suggesting further weakness. Conversely, resistance resides at the 0.8800 level where a violation if seen will turn risk towards the 0.8850 level. Further up, resistance resides at 0.8900 level followed by the 0.8950 level. All in all, EURGBP remains biased to the downside on more weakness.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9555; (P) 0.9576; (R1) 0.9596; More...

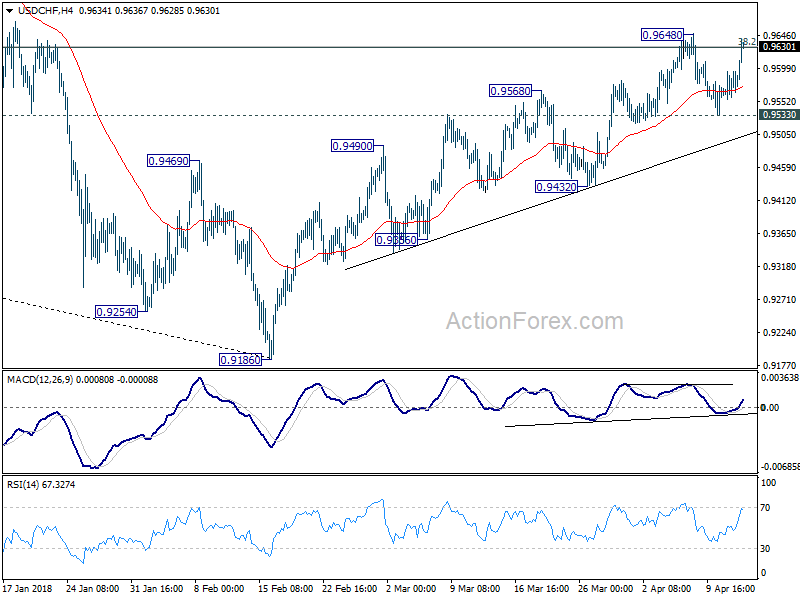

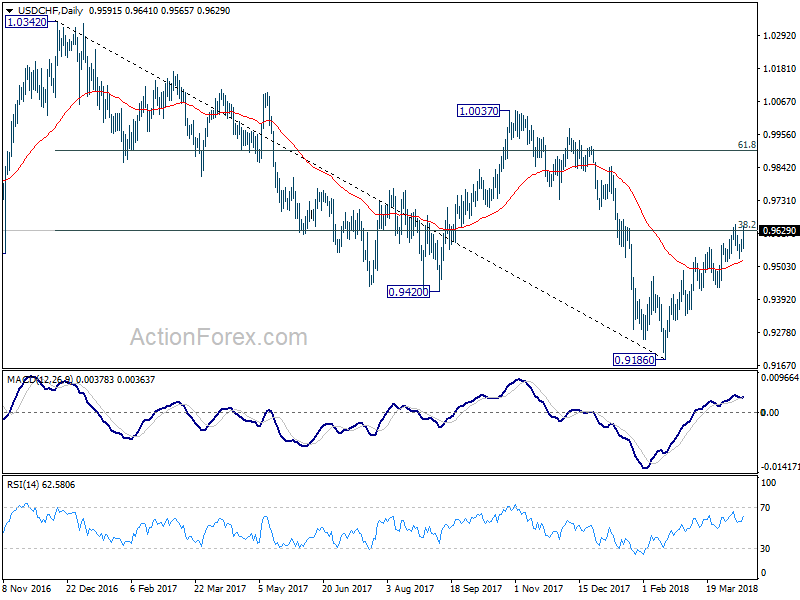

USD/CHF rebounds strongly today and focus is back on 0.9648 resistance. Break there will firstly resume whole rebound from 0.9186. Secondly, sustained trading above 0.9626 key fibonacci resistance will will be another evidence of larger reversal. In that case, further rally should be seen back to next fibonacci level at 0.9900. On the downside, though, break of 0.9533 minor support should be another indication of rejection by 0.9626. Further break of 0.9432 will turn near term outlook bearish for retesting 0.9186 low.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above. However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

Euro Tumbles after ECB Minutes, Dollar and Stocks Love Trump’s Uncertain Timing on Missile Strike

The financial markets don't always hate uncertainties. Sometimes, they embrace it. US President Donald Trump backed down from his initial tough stance on Syria, and it's now unsure when he will order firing of missiles over it. European equities cheered the newly created uncertainty with DAX turning initial loss into gain and is currently trading up 0.55%. CAC is up 0.23% while FTSE is flat. US futures now also point to higher open.

In the currency markets, Dollar welcomed Trump's tweet and surges against Euro, Swiss Franc and Yen. The greenback, nonetheless, is staying in tight range against Sterling, Canadian an Australia Dollar. One the other hand, Euro trader are clearly dissatisfied that ECB minutes provide no news. ECB Governing Council member Ewald Nowotny might have prompted some speculation of ECB rate hike earlier this week. But the minutes put everything back in place with its cautious tone that gives no hint of further action regarding the forward guidance or the asset purchase program. The ECB minutes are all very balanced and clear. But traders just don't like it and send the Euro sharply lower.

Trump backed down from his tough Syria stance

In his usual morning tweet, Trump said "Never said when an attack on Syria would take place. Could be very soon or not so soon at all!" And just yesterday, he tweeted "Russia vows to shoot down any and all missiles fired at Syria. Get ready Russia, because they will be coming, nice and new and 'smart!'". So, Trump changed is stance that from the missile are coming, to it's uncertain when, but they're coming.

Separately, Russia also tried to calm down the situation as Frants Klintsevich, a senator who's a member of the upper house's defense and security committee said warned that "if these strikes start, it could end very tragically and it's impossible to predict the outcome."

Euro dives as ECB minutes contains no hawkishness

Euro drops sharply as markets are disappointed that ECB account of March monetary policy meeting delivers no hawkishness at all. Regarding inflation, ECB noted that "measures of underlying inflation remained subdued and had yet to show convincing signs of a sustained upward trend." And, "ample degree of monetary policy accommodation remained necessary to accompany the economic expansion and for price pressures to continue to build up". Also, "remaining uncertainties and muted underlying inflation pressures called for caution and underlined the need to maintain the prevailing policy posture of prudence, patience and persistence."

The removal of easing bias on regarding the asset purchase program from the forward guidance was justified because "economic expansion had become more robust and scenarios of large negative economic surprises, leading to renewed deflationary risks, had become less likely." Still, the Governing Council members emphasized the "prudence, patience and persistence remained warranted and the key elements of the Governing Council's forward guidance on policy rates and the APP needed to be confirmed, including the open-endedness of the APP.

Regarding Euro's exchange rate, ECB noted that "recent movements in the euro exchange rate seemed to relate more to the relative monetary policy shocks, including communication, and less to improvements in the macroeconomic outlook." And, "this suggested that the exchange rate appreciation could be expected to have a more negative impact on inflation."

ECB also warned that "there was widespread concern that the risk of trade conflicts, which could be expected to have an adverse impact on activity for all countries involved, had increased." ECB added,"it was also cautioned that negative confidence effects could arise."

German Economic Ministry: Upswing continues but pace moderated slightly

Germany Federal Ministry for Economic Affairs and Energy released a monthly report today. It noted that the upswing of the German economy continues with pace moderated slightly. The global economic environment continues to be favorable. However, there are increased risks due to trade conflicts. The up trends in new orders have weakened while consumer demand has recently been less dynamic. Nonetheless, with increasing challenge for hiring, unemployment and underemployment continue to decline.

On the data front

US initial jobless claims dropped to 233k in the week ended April 7. Import price index rose 0.0% mom in March. Canada new housing price index dropped -0.2% mom in February. Eurozone industrial production dropped sharply by -0.8% mom in February. UK RICS house price balance was unchanged at 0 in March. Japan M2 rose 3.2% yoy in March. Australia consumer inflation expectation slowed to 3.6% in April. Australia home loans dropped -0.2% mom in February.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9555; (P) 0.9576; (R1) 0.9596; More...

USD/CHF rebounds strongly today and focus is back on 0.9648 resistance. Break there will firstly resume whole rebound from 0.9186. Secondly, sustained trading above 0.9626 key fibonacci resistance will will be another evidence of larger reversal. In that case, further rally should be seen back to next fibonacci level at 0.9900. On the downside, though, break of 0.9533 minor support should be another indication of rejection by 0.9626. Further break of 0.9432 will turn near term outlook bearish for retesting 0.9186 low.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above. However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS House Price Balance Mar | 0% | 2% | 0% | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Mar | 3.20% | 3.20% | 3.30% | |

| 01:00 | AUD | Consumer Inflation Expectation Apr | 3.60% | 3.70% | ||

| 01:30 | AUD | Home Loans M/M Feb | -0.20% | -0.40% | -1.10% | |

| 09:00 | EUR | Eurozone Industrial Production M/M Feb | -0.80% | 0.10% | -1.00% | |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | CAD | New Housing Price Index M/M Feb | -0.20% | 0.00% | ||

| 12:30 | USD | Import Price Index M/M Mar | 0.00% | 0.10% | 0.40% | 0.30% |

| 12:30 | USD | Initial Jobless Claims (Apr 7) | 233K | 230K | 242K | |

| 14:30 | USD | Natural Gas Storage | -11B | -29B |

Hong Kong Central Bank Intervenes as HKD Hit Weak Side of Trading Band

The Hong Kong Monetary Authority (HKMA) has just intervened in the currency market as the HK dollar (HKD) hit the weak side (7.85) of the trading band against US dollar (USD), the first time since 2005. The de facto central bank of the city has bought HK$816M Hong Kong dollars from the currency market. The intervention would lower the aggregate balance to HK$178.96 billion on April 16, when the withdrawn funds will be settled. Interbank liquidity would stay ample after the withdrawal. We do not think this would help much, if any, in narrowing the spread between HIBOR and LIBOR, the key reason causing capital to flow out of Hong Kong and hence weakness of HKD. As such, we do not feel surprised to see HKD to hit the weak side of the trading band again and this might lead to further HKMA intervention.

Canadian Dollar Trading Sideways as Middle East in Focus

The Canadian dollar is showing limited movement in the Thursday session. Currently, USD/CAD is trading at 1.2593, up 0.10% on the day. In economic news, it’s a quiet day on both sides of the border. US unemployment claims is expected to fall to 231 thousand. In Canada, the New Housing Price Index is forecast to edge up to 0.1%. On Friday, the US releases UoM Consumer Sentiment.

The Canadian dollar has flexed some muscle this week, but the minor currency could face some turbulence, as the markets are braced for a US strike against Syria. This follows an alleged chemical attack by Syrian forces against rebels, and a UN Security Council meeting ended inconclusively after Russia cast a veto on a US proposal to probe the attack. US President Trump has warned that a US response is imminent, while Russia has countered that it will respond to any US move. Matters could get very nasty if Trump makes good on his promise, as investor risk appetite could sink and drag down minor currencies such as the Canadian dollar.

There were no surprises in the Federal Reserve minutes, but the generally hawkish tone has helped support the US dollar. All of the Fed policymakers indicated that the US economy would continue to improve and that inflation would rise in the next few months. At the March meeting, the Fed unanimously voted to raise rates by a quarter-point, bringing the benchmark rate to a range between 1.50% and 1.75%. The Fed projection for rate policy in 2018 remains at three hikes, although there is speculation that the Fed could revise the forecast to four rate hikes. Last week, Fed Chair Jerome Powell said that the Fed would likely continue to raise rates in order to keep a lid on inflation, but added that the rate moves would be gradual. A new headache for the Fed is the escalating trade battle between the US and China, which could hurt the economy and raise consumer prices. As for the next two rate meetings, the markets expect Powell & Co. to sit tight in May and raise rates at the June meeting.

The Bank of Canada Business Outlook Survey was released earlier this week. The survey pointed to a generally upbeat business sector and has helped boost the Canadian dollar. The survey found widespread intention by companies to increase investment and hiring, and “forward-looking sales indicators remain positive across most regions and sectors”. Still, the report is unlikely to change the current sentiment that the BoC will not raise rates at next week’s policy meeting.

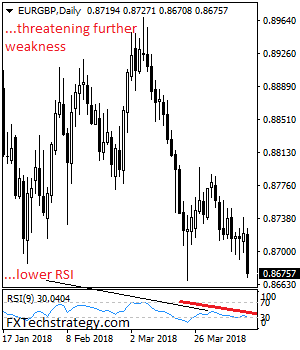

Euro dives as ECB minutes contains no hawkishness, EUR/GBP to test 0.8666

Euro drops sharply as markets are disappointed that ECB account of March monetary policy meeting delivers no hawkishness at all. EUR weakens against all but JPY and CHF as seen in the current 4H heatmap.

In particular, the sharp decline in EUR/GBP is now setting it up for a test on 0.8666 key support.

Regarding inflation, ECB noted that "measures of underlying inflation remained subdued and had yet to show convincing signs of a sustained upward trend." And, "ample degree of monetary policy accommodation remained necessary to accompany the economic expansion and for price pressures to continue to build up". Also, "remaining uncertainties and muted underlying inflation pressures called for caution and underlined the need to maintain the prevailing policy posture of prudence, patience and persistence."

The removal of easing bias on regarding the asset purchase program from the forward guidance was justified because "economic expansion had become more robust and scenarios of large negative economic surprises, leading to renewed deflationary risks, had become less likely." Still, the Governing Council members emphasized the "prudence, patience and persistence remained warranted and the key elements of the Governing Council's forward guidance on policy rates and the APP needed to be confirmed, including the open-endedness of the APP.

Regarding Euro's exchange rate, ECB noted that "recent movements in the euro exchange rate seemed to relate more to the relative monetary policy shocks, including communication, and less to improvements in the macroeconomic outlook." And, "this suggested that the exchange rate appreciation could be expected to have a more negative impact on inflation."

ECB also warned that "there was widespread concern that the risk of trade conflicts, which could be expected to have an adverse impact on activity for all countries involved, had increased." ECB added,"it was also cautioned that negative confidence effects could arise."

DAX Rebounds, ECB Minutes Next

The DAX index has posted gains in the Thursday session. Currently, the DAX is trading at 12,355 points, up 0.50% on the day. On the release front, Eurozone Industrial Production disappointed with a second straight decline. The reading of -0.8% missed the estimate of 0.1%. Later in the day, the ECB releases the minutes of its March rate meeting. On Friday, Germany releases Final CPI.

The Federal Reserve minutes were hawkish in tone, a reflection of a strong US economy. All of the Fed policymakers indicated that the US economy would continue to improve and that inflation would rise in the next few months. At the March meeting, the Fed unanimously voted to raise rates by a quarter-point, bringing the benchmark rate to a range between 1.50% and 1.75%. The Fed projection for rate policy in 2018 remains at three hikes, although there is speculation that the Fed could revise the forecast to four rate hikes. Last week, Fed Chair Jerome Powell said that the Fed would likely continue to raise rates in order to keep a lid on inflation, but added that the rate moves would be gradual. A new headache for the Fed is the escalating trade battle between the US and China, which could hurt the economy and raise consumer prices. Next on the menu? The Fed is expected to stay on the sidelines in May and raise rates at the June meeting.

It’s been a volatile week for European stock markets and investors are bracing for more movement, with tensions at a fever pitch in the Middle East. The markets reacted positively as the trade battle between the US and China took a pause. On Sunday, US officials sought to lower the temperature over the tariff spat, with Treasury Secretary Steve Mnuchin saying that he didn’t expect a trade war between the world’s largest two economies. This was followed by a conciliatory message from Chinese President Xi Jimping on Tuesday. Xi was speaking at a development conference in China, and promised to lower tariffs on vehicle imports into China. However, sentiment turned negative on Wednesday, as the rhetoric between the US and Russia has ratcheted higher. Syrian forces allegedly used chemical weapons against rebel positions last week, and a UN Security Council meeting ended inconclusively after Russia cast a veto on a US proposal to probe the attack. US President Trump has warned that a US response is on the way, and Russia has countered that it will respond to any US move. If Trump makes good on his promise, investors could lose their risk appetite and the markets could spiral downwards.

(ECB) Account of the Monetary Policy Meeting 7-8 March 2018

Account of the Monetary Policy Meeting of the Governing Council of the European Central Bank, held in Frankfurt am Main on Wednesday and Thursday, 7-8 March 2018

1. Review of financial, economic and monetary developments and policy options

Financial market developments

Mr Cœuré reviewed the latest financial market developments.

Since the Governing Council's monetary policy meeting on 24-25 January 2018, despite a short-lived and concentrated spike in market volatility, valuations across broad asset classes had remained consistent with continued optimism about the outlook for global growth.

Real long-term yields had risen by around 30 basis points in the United States and 20 basis points in the euro area since the start of the year. While part of this movement reflected adjustments in term premia, it also likely reflected investors' views on growth prospects, including the expected impact of the fiscal stimulus package adopted by the US Administration. Ten-year break-even inflation rates in the euro area had barely moved since the start of the year. By contrast, in the United States they had increased by more than 20 basis points. Markets had also reappraised the near-term monetary policy outlook in the United States, in part reflecting recent US employment and inflation data releases.

In the euro area, monetary policy expectations had changed very little since the Governing Council's January meeting. Market participants' expectations about the timing of a first 10 basis point hike in the deposit facility rate had shifted out slightly.

Turning to equity markets, two underlying forces were being exerted in opposite directions: expected earnings were continuing to push stock valuations higher, while the increase in discount rates was pulling stock prices lower on both sides of the Atlantic. Export-oriented countries and sectors seemed to have been most affected by recent concerns over trade relations. However, the turbulence in equity markets had not generated a more general sell-off of other risk assets. Looking at asset swap spreads for debt securities in Europe, only those of high-yield non-financial corporations (NFCs) had increased somewhat. When looking at sovereign yield spreads vis-à-vis Germany, the resilience had been notable considering the substantial issuance activity seen recently.

The overall limited spillovers of recent price movements in the equity markets to other markets could also be seen when looking at a comparison of implied volatility across different markets, which had remained at comparatively low levels, except in equity markets.

The observed jump in volatility in equity markets had, in turn, been exacerbated by technical flows, such as those prompted by investors following risk-parity and short volatility trading strategies. However, the VIX volatility index had fallen back from the very high levels reached in early February 2018.

As regards recent exchange rate developments, some factors had likely been supportive of an appreciation of the US dollar, such as positive inflation news, higher US yields and a surge in global uncertainty, which, given the US dollar's status as a safe haven asset, typically contributed to a strengthening of the currency. Nevertheless, other factors, which had been weighing on the US dollar in recent months, are likely to have remained at work, such as improved economic growth expectations in the rest of the world and greater borrowing needs in the United States to finance a potential increase in the current account deficit.

The global environment and economic and monetary developments in the euro area

Mr Praet reviewed the global environment and recent economic and monetary developments in the euro area.

Regarding the external environment, global activity and trade momentum remained sustained. Surveys pointed to steady and broad-based global growth momentum at the start of 2018. The global composite output Purchasing Managers' Index (PMI) had increased slightly in February.

Global trade indicators pointed to sustained growth around the turn of the year. Global goods import growth had slowed in the fourth quarter but trade indicators were relatively buoyant, with the global PMI new export orders series standing at a high level in January and above its long-term average.

Despite the global upturn, underlying price pressures had remained subdued. Annual consumer price inflation in the OECD countries had ticked down slightly in January, to 2.2%, from 2.3% in December, but core inflation had remained steady, with inflation excluding food and energy standing at 1.8% in January.

Brent crude oil prices had decreased since the January meeting but had increased slightly compared with the December projection assumptions, standing at USD 65.4 per barrel on 6 March. Over the same period, non-oil commodity prices had increased by 2.7%, largely driven by rises in food prices and, to a lesser extent, in metal prices. The euro had appreciated slightly against the US dollar and also in nominal effective terms since the January meeting.

Turning to the euro area economy, incoming data since the Governing Council's January monetary policy meeting confirmed the ongoing economic expansion. Favourable financing conditions and steady income and profit growth, together with a robust labour market, continued to be the key factors supporting aggregate demand. Risks to the growth outlook remained broadly balanced. The positive cyclical momentum pointed to some upside risks in the near term, while downside risks continued to relate to global factors, including developments in foreign exchange markets and protectionism.

According to the latest data, economic activity had remained robust in the fourth quarter of 2017. Eurostat's flash estimate had put euro area real GDP growth at 0.6%, quarter on quarter, in the fourth quarter. The expansion had been broad-based across sectors. Real value added had increased by 1.2% in the industrial sector (excluding construction), by 0.4% in the services sector and by 1.1% in the construction sector. Incoming data since the January meeting also pointed to continued expansion in the first quarter of 2018.

These positive developments were also reflected in the March 2018 ECB staff macroeconomic projections for the euro area, which projected real GDP growth at 2.5% in 2017, 2.4% in 2018 ,1.9% in 2019 and 1.7% in 2020, representing an upward revision for 2018 compared with the December 2017 Eurosystem staff projections. The favourable growth outlook was supported by a number of factors, including a continued global expansion, the ECB's very accommodative monetary policy stance, improving labour markets and diminishing deleveraging pressures for NFCs and households. Nevertheless, real GDP growth was projected to slow somewhat over the projection horizon as tailwinds were expected to fade gradually.

Turning to price developments, according to Eurostat's flash estimate, annual HICP inflation had stood at 1.2% in February 2018, down from 1.3% in January. HICP inflation excluding food and energy had been 1.0% in February, unchanged from January but slightly up from 0.9% in December. Measures of underlying inflation remained low by historical standards, although they had shown a marked improvement since the trough in 2016. Overall, these developments suggested that the strong cyclical momentum, the ongoing reduction of labour market slack and increasing capacity utilisation were translating into a steady, albeit slow, upward movement in inflationary pressures.

As regards wages, recent developments had confirmed a gradual upward trend. This increase was mainly attributable to higher contributions from wage drift, which usually reacted to cyclical developments with a shorter lag than negotiated wages. According to the March 2018 ECB staff projections, growth in compensation per employee was expected to pick up from 1.6% in 2017 to 2.7% in 2020.

In the March ECB staff projections, headline inflation was expected to reach 1.7% in 2020, driven by underlying inflation, after 1.4% in both 2018 and 2019. Compared with the December 2017 Eurosystem staff projections, the outlook for HICP inflation had been revised down slightly for 2019. The outlook for HICP inflation excluding food and energy was unchanged compared with the December 2017 Eurosystem staff projections and was expected to rise from 1.1% in 2018 to 1.5% in 2019 and 1.8% in 2020.

Inflation expectations, based on longer-term market and survey-based measures, were largely unchanged since the Governing Council's January monetary policy meeting.

Financial conditions had tightened somewhat amid volatility in equity and foreign exchange markets. At the same time, the tightening observed over recent months had to be seen in the light of improving economic conditions. The overall cost of financing for euro area firms had increased somewhat, with both the cost of equity and the cost of market-based debt having risen marginally.

Turning to money and credit developments, growth in the broad monetary aggregate M3 had remained robust and within the narrow range of 4.5-5.5% observed since the launch of the expanded asset purchase programme (APP) in early 2015. In January 2018 the annual growth rate of loans to NFCs had continued its upward trend, while the consolidated gross indebtedness of NFCs had continued to fall. The annual growth rate of loans to households had remained unchanged in January, supported by favourable borrowing conditions and the expected further improvements in labour markets. At the same time, growth in loans to households was being dampened by loan repayments. Banks' capital ratios had continued to strengthen in the third quarter of 2017, reflecting mainly an increased positive contribution from recapitalisation. Balance sheet de-risking had also continued to support capital ratios, as asset quality had been improving in line with macroeconomic fundamentals and balance sheet restructuring.

Regarding fiscal policies, the March 2018 ECB staff projections pointed to a mildly expansionary euro area fiscal stance in 2018, turning broadly neutral over 2019-20.

Monetary policy considerations and policy options

Summing up, Mr Praet remarked that financial conditions had tightened somewhat amid volatility in equity and foreign exchange markets. Nonetheless, borrowing conditions for firms and households remained very favourable, in particular in the light of the improved macroeconomic prospects.

The March ECB staff projections pointed to continued growth above potential, with an upward revision for 2018. Incoming information confirmed the strong and broad-based economic upswing. As regards inflation, the March projections confirmed the previous baseline outlook of headline inflation increasing gradually to the Governing Council's inflation aim. However, measures of underlying inflation remained subdued and had yet to show convincing signs of a sustained upward trend.

The cyclical momentum and the ongoing reduction of economic slack confirmed the confidence that euro area HICP inflation would converge towards the inflation aim. Yet inflation convergence was proceeding only gradually and remained dependent on an ample degree of monetary accommodation.

On the basis of this assessment, Mr Praet proposed to convey the Governing Council's improving confidence by removing the "easing bias" attached to the APP, i.e. the reference to increasing the asset purchase programme in terms of size and/or duration should the outlook become less favourable, or should financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation. This was a further step that followed earlier adjustments in the ECB's policy stance, namely the past reductions in the pace of purchases and the removal of the easing bias on policy rates. At the same time, patience and persistence in monetary policy remained essential for inflation pressures to build up. Accordingly, Mr Praet also proposed reconfirming the earlier decisions on asset purchases and policy rates.

Regarding communication, the Governing Council needed to reiterate its confidence that the economic expansion would eventually lead inflation to converge to its medium-term aim. It was also important to highlight prudence, patience and persistence in monetary policy for inflation pressures to build up and support the convergence of inflation to levels below, but close to, 2% over the medium term, as well as to stress that the Governing Council would continue monitoring developments in financial conditions with regard to their possible implications for the medium-term outlook for price stability.

Looking ahead, the Governing Council would continue to assess progress towards a sustained adjustment in the path of inflation. In line with its forward guidance on the APP, net asset purchases would expire once the Governing Council judged that the criteria for a sustained adjustment were met. The Governing Council's assessment would continue to be based on three criteria: first, convergence of headline inflation to the medium-term aim; second, confidence in the materialisation of the expected inflation path; and, third, resilience of inflation convergence even after the end of the net asset purchases.

Beyond the horizon of the net asset purchases, the monetary policy support still necessary for inflation to converge to the Governing Council's aim would continue to be provided by reinvestments of principal continuing for an extended period of time and by policy rates remaining at their present levels well past the end of the net asset purchases.

2. Governing Council's discussion and monetary policy decisions

Economic and monetary analyses

With regard to the economic analysis, members broadly shared the assessment of the outlook and risks for economic activity in the euro area provided by Mr Praet in his introduction. According to recent data and survey results, growth momentum, supported by very favourable financing conditions, had continued to be strong and broad-based. Looking ahead, this expansion was expected to continue in the near term at a somewhat faster pace than previously anticipated, as reflected in the March 2018 ECB staff projections, in which real GDP growth in 2018 had been revised up compared with the December 2017 Eurosystem staff projections, while the outlook for growth in 2019 and 2020 was unchanged. The risks surrounding the outlook for economic activity were assessed to have remained broadly balanced.

Regarding the outlook and risks for the external environment, the latest indicators pointed to sustained momentum in global activity and trade. The picture of a robust global economic expansion was also reflected in the March 2018 ECB staff projections, with the outlook for global activity being revised up for both 2018 and 2019. A major factor underlying the upward revision was the impact of the additional fiscal stimulus in the United States. However, the balance of risks to the global economic expansion was still assessed to be tilted to the downside, as geopolitical uncertainties and uncertainty regarding the policy outlook in some major economies – including the risk of increased trade protectionism and the uncertain impact of the United Kingdom's withdrawal from the EU – continued to constitute downside risks.

In the wake of recent statements by the US Administration, members exchanged views on the risks arising from trade protectionism, on which the Governing Council had reflected before. There was widespread concern that the risk of trade conflicts, which could be expected to have an adverse impact on activity for all countries involved, had increased. The impact on the global economy and on the euro area would ultimately depend on the scale of import tariffs imposed by the United States, as well as the scope of any retaliatory measures. However, it was also cautioned that negative confidence effects could arise. The impact of increased trade protection on inflation was seen as being more ambiguous and uncertain.

Reference was also made to the risks associated with volatility in global financial markets and foreign exchange markets. It was highlighted that, although the past appreciation of the euro had so far not had a significant negative impact on euro area external demand, developments in foreign exchange markets continued to be a significant source of uncertainty and a risk that needed monitoring.

Turning to euro area activity, members noted that recent indicators had provided further evidence that the economic expansion was strong and broad-based, and was continuing at a pace above current estimates of potential growth. Euro area real GDP growth had increased by 0.6%, quarter on quarter, in the fourth quarter of 2017, following an increase of 0.7% in the third quarter. While the latest survey data were weaker, both the European Commission's Economic Sentiment Indicator and the PMI remained at historically high levels. On the basis of developments in short-term indicators, near-term real GDP growth could turn out to be somewhat higher than previously expected.

In terms of the main components of demand, private consumption growth remained strong, supported by rising incomes and employment and by historically low household savings. Business investment was strengthening on the back of very favourable financing conditions, as well as rising corporate profitability and solid demand. Housing investment had also improved further over recent quarters. In addition, the broad-based global expansion was providing impetus to euro area exports.

Members exchanged views about the euro area's potential growth rate and the remaining degree of slack in the economy. It was noted that estimates from international institutions such as the European Commission and the OECD suggested a closing of the euro area output gap in late 2017 or early 2018, while it was also acknowledged that there were significant variations in the assessment of the output gap across countries. The view was widely shared that there was considerable measurement uncertainty about the degree of slack remaining in the labour market and in the economy as a whole.

A number of arguments were put forward suggesting that greater slack might remain in the economy than indicated in the baseline projections. It was recalled that measures of potential growth were typically derived from capital and labour inputs, as well as estimates of total factor productivity, all of which could be considered to some extent to have cyclical components. If only supply shocks were considered when estimating potential output, possibly resulting from the positive impact of past structural reforms, there could be more spare capacity in the economy than was currently implied by traditional measures.

It was also recalled that favourable revisions had already been made to estimates of both the non-accelerating inflation rate of unemployment (NAIRU) and potential output. It was noted that the assessment of slack in the labour market was in part based on broader measures of unemployment, which incorporated involuntary part-time or discouraged workers, putting additional downward pressure on wages. However, if there were significant hysteresis effects, labour market slack may be less than suggested on the basis of these broader measures. At the same time, it was remarked that crisis-induced hysteresis might be reversed in a strong economic recovery.

A further risk discussed by members was that of a more expansionary and procyclical fiscal policy over the projection horizon. Overall, the risks to the euro area growth outlook were assessed to have remained broadly balanced. On the one hand, the prevailing positive cyclical momentum could lead to stronger growth in the near term. On the other hand, downside risks continued to relate primarily to global factors, including rising protectionism and developments in foreign exchange and other financial markets.

Members emphasised that deepening Economic and Monetary Union remained a priority and stressed the need to make progress on the completion of the banking union and the capital markets union. More generally, it was recalled that other policy areas needed to contribute decisively to raising the longer-term growth potential of the euro area economy and to reducing vulnerabilities, in order to reap the full benefits from the ECB's monetary policy measures. To increase the resilience of the euro area economy, the implementation of structural reforms in euro area countries needed to be stepped up substantially and a full and consistent implementation of the Stability and Growth Pact and the macroeconomic imbalance procedure was necessary, over time and across countries.

With regard to price developments, there was broad agreement with the assessment presented by Mr Praet in his introduction. Annual euro area HICP inflation had declined to 1.2% in February 2018, compared with 1.3% in January. The decline mainly reflected negative base effects in unprocessed food price inflation. Annual rates of headline inflation were likely to hover around 1.5% for the remainder of the year, inter alia on the basis of current futures prices for oil. It was noted that in recent projection rounds the outlook for headline inflation and for measures of underlying inflation had been relatively stable, while the growth outlook had been gradually revised upwards.

Members considered that measures of underlying inflation in the euro area remained subdued, but were expected to rise gradually over the medium term, supported by the ECB's monetary policy measures, the continuing economic expansion, the corresponding absorption of economic slack and rising wage growth.

The stability of measures of underlying inflation, despite the appreciation of the euro, was again highlighted in the discussion. In this context, it was noted that non-energy industrial goods price inflation, which was considered the component most sensitive to exchange rate movements, had continued to increase despite the euro's appreciation and, at 0.7%, stood now above its long-term average. At the same time, it was remarked that recent movements in the euro exchange rate seemed to relate more to relative monetary policy shocks, including communication, and less to improvements in the macroeconomic outlook for the euro area. This suggested that the exchange rate appreciation could be expected to have a more negative impact on inflation. In addition, even though the effect of the euro's appreciation on inflation had been limited so far, the pass-through could be stronger if the shocks turned out to be permanent. Overall, there was broad agreement among members that volatility in the exchange rate of the euro continued to be a source of uncertainty, which required monitoring with regard to its possible implications for the medium-term inflation outlook.

Members observed that wage dynamics were still relatively subdued, as reflected in annual increases in compensation per employee, which stood at 1.7% in the third quarter of 2017, although it was expected that cost pressures should gradually increase as the economic expansion continued and slack in the labour market was absorbed.

As regards recent developments in inflation expectations, members noted that both market-based measures and survey-based longer-term measures remained broadly stable. Expectations of inflation five years ahead in the ECB's Survey of Professional Forecasters (SPF) for the first quarter of 2018 stood at 1.9% and the five-year forward inflation-linked swap rate five years ahead currently stood at 1.71%. While this was still higher than at the December 2017 monetary policy meeting, it was slightly lower than the level observed at the time of the Governing Council's January 2018 monetary policy meeting. It was remarked that evidence from both the SPF and option prices pointed to a shift towards higher inflation expectations since early 2015, after the start of the APP, with deflation scenarios clearly priced out.

With regard to the monetary analysis, members concurred with the assessment presented by Mr Praet in his introduction. Broad money (M3) had continued to expand at a robust pace, reflecting the impact of the ECB's monetary policy measures and the low opportunity cost of holding the most liquid components. The gradual recovery in the growth of loans to the private sector, visible since the start of 2014, was proceeding amid a further pick-up in the growth of loans to NFCs and unchanged growth in loans to households. The expansion in credit continued to be supported by very favourable borrowing costs for firms and households across euro area jurisdictions.

Monetary policy stance and policy considerations

With regard to the monetary policy stance, members widely shared the assessment provided by Mr Praet in his introduction that the incoming information, including the new staff projections, corroborated the strong and broad-based growth momentum in the euro area economy. This outlook for growth confirmed the increased confidence that inflation would converge to the Governing Council's inflation aim of below, but close to, 2% over the medium term. At the same time, measures of underlying inflation remained subdued and had yet to show convincing signs of a sustained upward trend. Overall, while the increased confidence called for a gradual adjustment in the Governing Council's communication, prudence, patience and persistence with regard to monetary policy remained warranted for underlying inflation pressures to continue to build up and support headline inflation developments over the medium term.

Members also broadly concurred with the assessment by Mr Praet that financial conditions remained very favourable but had tightened somewhat since the January monetary policy meeting on account of weaker equity markets, an appreciation of the euro and an uptick in market interest rates. It was remarked that the tightening in financial conditions also had to be seen against the background of improvements in macroeconomic conditions and, hence, may not necessarily imply a more restrictive monetary policy stance. Moreover, the pass-through of the ECB's monetary policy measures continued to provide significant support to borrowing conditions for firms and households. At the same time, some caution was voiced, as the more recent developments in the euro exchange rate and in financial conditions in part reflected changing perceptions about monetary and fiscal policies, domestically and globally, as well as rising risks of protectionism and heightened market sensitivity to communication, rather than further improvements in domestic economic fundamentals. Against this background, developments in the exchange rate and financial conditions required monitoring with regard to their possible implications for the inflation outlook.

There was broad agreement among members that the incoming information indicated ongoing progress on a sustained adjustment in the path of inflation towards the Governing Council's inflation aim. The view was put forward that the Governing Council's criteria for a sustained adjustment in the path of inflation could be assessed as close to being satisfied over a medium-term horizon. However, the broadly agreed conclusion was that the evidence for a sustained rise in inflation towards levels consistent with the Governing Council's inflation aim was still not sufficient. In this context, the point was also made that the assessment regarding the achievement of a sustained adjustment in inflation was not binary, but rather multifaceted and probabilistic in nature.

It was seen as encouraging that the latest ECB staff projections appeared to remain consistent with inflation converging to levels below, but close to, 2% over the medium term, also confirming the outlook contained in previous projection exercises. Moreover, growth rates well above current estimates of potential growth and the corresponding increase in capacity utilisation were seen as strengthening confidence in the currently expected inflation path.

At the same time, recent inflation outturns had remained some distance away from the Governing Council's inflation aim and the incoming information continued to point to muted price pressures overall. Moreover, while confidence in the inflation outlook had increased, it was still seen as subject to a number of uncertainties, related mainly to the degree of remaining economic slack and risks emanating from the global environment as well as developments in foreign exchange and other financial markets.

With regard to the criterion of resilience, which called for a self-sustaining adjustment in the path of inflation even after the end of the net asset purchases, it was widely agreed that an ample degree of monetary policy accommodation remained necessary to accompany the economic expansion and for price pressures to continue to build up and support a rise in inflation to the Governing Council's medium-term inflation aim.

All in all, remaining uncertainties and muted underlying inflation pressures called for caution and underlined the need to maintain the prevailing policy posture of prudence, patience and persistence. This suggested that the monetary policy decisions taken at the meeting in late October 2017 on net asset purchases, reinvestments and policy interest rates should be reconfirmed.

Against the backdrop of the ongoing improvements in economic prospects and the corresponding greater confidence in the inflation outlook, all members agreed with Mr Praet's proposal to remove the "easing bias" on the APP from the Governing Council's forward guidance. It was recalled that this language had been introduced at the time when net purchases had been scaled back from a monthly pace of €80 billion to €60 billion and that the economic environment had changed notably since then. In particular, its removal was seen as justified as the economic expansion had become more robust and scenarios of large negative economic surprises, leading to renewed deflationary risks, had become less likely. In this sense, the removal of the APP easing bias was consistent with the Governing Council's data-dependent approach to policy and communication.

As regards communication, there was broad agreement with Mr Praet's proposal to highlight increased confidence in the inflation outlook while reiterating the importance of patience and persistence in monetary policy to support inflation convergence towards levels below, but close to, 2% over the medium term. It was widely stressed that the Governing Council's communication needed to reflect the progressively improving economic environment and the corresponding greater confidence in the path of inflation. Accordingly, a further adjustment in communication in the form of removing the APP easing bias was seen as a natural step.

Members also agreed that alongside the elimination of the easing bias, emphasis needed to be placed on the Governing Council's firm commitment to its price stability objective, particularly as inflation had fallen short of its stated aim for a considerable period of time. Prudence, patience and persistence remained warranted and the key elements of the Governing Council's forward guidance on policy rates and the APP needed to be confirmed, including the open-endedness of the APP. In this context, it was also remarked that the removal of the easing bias should not be misunderstood as restricting the Governing Council's capacity to react to shocks and contingencies, if necessary.

At the same time, it was reiterated that the monetary policy stimulus continued to be provided by the full set of policy instruments, namely the level of policy rates, the net asset purchases, the sizeable stock of acquired assets and the current and forthcoming reinvestments, and the forward guidance on interest rates. Finally, there was broad agreement on stressing the need for continued monitoring of developments in the exchange rate and financial conditions with regard to their possible implications for the inflation outlook.

Looking ahead, there was broad agreement on the main elements put forward by Mr Praet in his introduction. The course of monetary policy would remain firmly guided by the Governing Council's continuous assessment of the progress made towards a sustained adjustment in the path of inflation based on the three criteria of convergence, confidence and resilience. In particular, once the Governing Council judged that the criteria for a sustained adjustment were met, the net asset purchases would expire in line with the conditionality expressed in the forward guidance on the APP.

It was recalled, as on previous occasions, that, beyond the horizon of the net asset purchases, the monetary policy support still necessary for inflation to converge to the inflation aim would be provided by the stock of acquired assets, by reinvestments continuing for an extended period of time, and by policy rates remaining at their present levels well past the end of the net asset purchases.

Monetary policy decisions and communication

Taking into account the foregoing discussion among the members, on a proposal from the President, the Governing Council decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility would remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council continued to expect the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases. The Governing Council confirmed that the net asset purchases, at the current monthly pace of €30 billion, were intended to run until the end of September 2018, or beyond, if necessary, and in any case until it saw a sustained adjustment in the path of inflation consistent with its inflation aim. The Eurosystem would reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of the net asset purchases, and in any case for as long as necessary. This would contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

The members of the Governing Council subsequently finalised the draft introductory statement, which the President and the Vice-President would, as usual, deliver at the press conference following the end of the current Governing Council meeting.

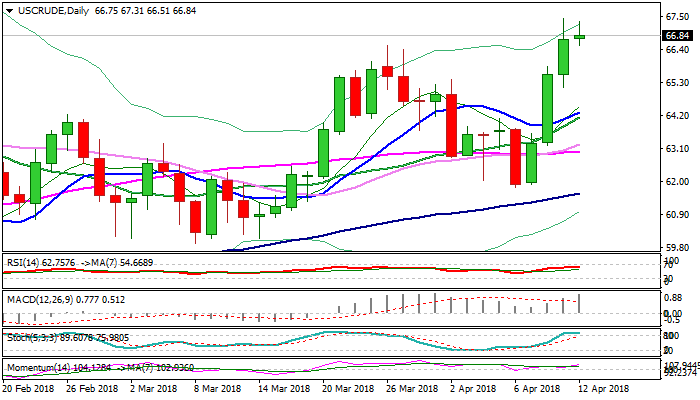

WTI OIL – Geopolitical Tensions Keep Oil Price Well Supported, Corrective Dips Seen As Positioning For Fresh Rally

Oil price is consolidating under new high at $67.43 (the highest since early Dec 2014) on Thursday, following strong rally in past three days, when oil price advanced over 7.5%.

Escalating geopolitical risk on escalation of tensions in the Middle East keeps the oil price well supported, as surprise strong build in US crude stocks (3.3 million barrels build vs 0.6 million barrels draw forecasted) had a minor impact on oil price.

Completion of $66.64/$58.06 corrective phase and close above $66.64 (25 Jan former high), generated bullish signal for extension of recovery phase from $26.04 (11 Feb 2016 low), as bulls cracked next barrier at $66.75 (Fibo 50% of $107.45/$26.04 fall).

Sustained break higher could travel towards psychological $70 barrier (also Fibo 138.2% projection of the bull-leg from $58.06).

Bullish daily techs support scenario, however, oil price may hold in extended consolidation and even dip lower on overbought conditions and profit-taking action, while situation in the Middle East stays unchanged.

Deeper pullback should be contained at $65.00 zone to keep bullish structure intact for fresh advance.

Signals of scalation of geopolitical tension would send oil price immediately higher.

Res: 67.00, 67.43, 68.63, 69.00

Sup: 66.51, 66.10, 65.28, 65.00

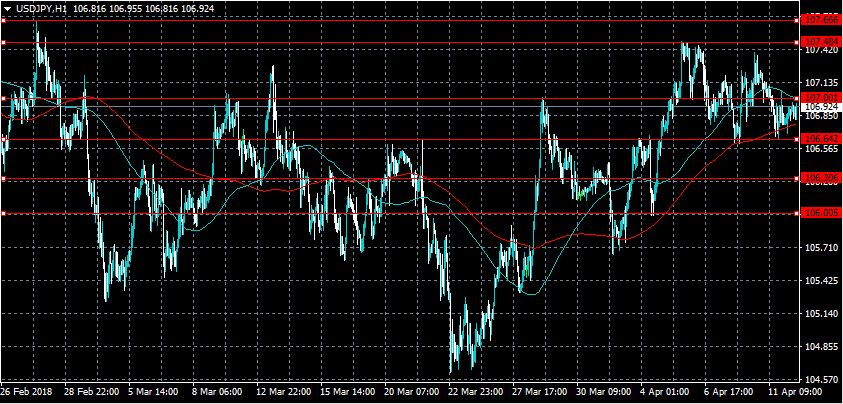

USDJPY Upside Limited On Syrian Risks

The U.S dollar is struggling to gain traction above the 107.00 handle against the Japanese yen currency, as escalating tensions between the U.S and Russia in Syria weigh on risk sentiment. The USDJPY pair currently trades around the 106.90 level, after again finding strong technical support from the 106.60 region. Heading into the U.S trading session, potential military action from the United States in Syria is likely to keep the USDJPY pairs upside fairly limited.

The USDJPY pair is only intraday bullish while trading above the 106.60 level, key upside resistance is located at the 107.48 and 107.66 levels.

Should the USDJPY pair start to trade below the 106.60 level, key technical support is then found at the 106.30 and 106.00 levels.