Sample Category Title

Eco Data 4/12/18

[php_everywhere instance="1"]

Gold Surges on Syria Jitters, Weak CPI

Gold has posted sharp gains in the Wednesday session. In North American trade, the spot price for an ounce of gold is $1360.15, up 1.60% on the day. In economic news, CPI declined 0.1%, shy of the estimate of 0.0%. This marked the first decline since May. Core CPI remained unchanged at 0.2%. Later in the day, the Federal Reserve will release the minutes of the March policy meeting.

Investor sentiment turned negative on Wednesday, as the rhetoric between the US and Russia has ratcheted higher. This has sent gold prices sharply higher. Tensions in the Middle East are high, as Syrian forces allegedly used chemical weapons against rebel positions last week, and a UN Security Council meeting ended inconclusively after Russia cast a veto on a US proposal to probe the attack. US President Trump has warned that a US response is on the way, and Russia has countered that it will respond to any US move. If Trump makes good on his promise, investors could lose their risk appetite and the markets could spiral downwards.

The markets are keeping a close eye on the release of the FOMC minutes. The minutes could provide the markets with some insights regarding the Federal Reserve’s monetary policy for this year. Will the Fed press the rate trigger three times this year, or four? The current Fed forecast calls for three rate hikes, but this could be revised upwards if inflation rises. If the FOMC minutes point to a hawkish stance from policymakers,

Gold breaking out from triangle pattern, heading to 1400?

Gold surges to as high as 1365.24 so far and is attempting to break out from recent triangle consolidation. Immediate focus is now on 1366.05 high, which is nor far away. Based on current momentum, break of 1366.05 should send gold to 61.8% projection of 1236.66 to 1366.05 from 1319.82 at 1399.78, which is close to 1400 handle.

However, we'd pointed this out before, and would like to reiterate this point again. There are two resistance levels to overcome from a longer term point of view. Firstly, that's 1375.15, 2016 high. Secondly, that 38.2% retracement of 1920.94 (2011 high) to 1046.54 (2015 low) at 1380.56. This 1375/80 zone is the real test for gold ahead.

However, we'd pointed this out before, and would like to reiterate this point again. There are two resistance levels to overcome from a longer term point of view. Firstly, that's 1375.15, 2016 high. Secondly, that 38.2% retracement of 1920.94 (2011 high) to 1046.54 (2015 low) at 1380.56. This 1375/80 zone is the real test for gold ahead.

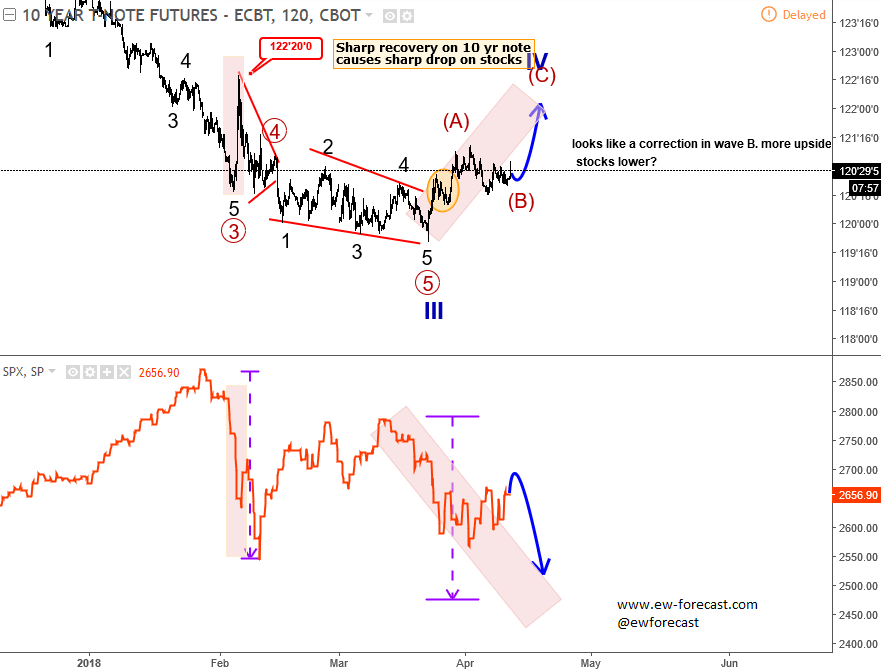

Russia-US Tensions Plus Tehchnicals Can Cause Lower Stocks

10 year US note bounced from the lows in the last two weeks while stocks accelerated to the downside, ideally within wave C which may not be over yet based on recent developments which suggests that ounce from start of April is corrective. In fact, here is also a slow price structure at the moment on 10 year, above 120'10 that looks like a wave (B) of an ongoing 3-leg recovery up to 122'00. If that is correct then stocks may see more downside, into 2500 area on S&P500 where wave C would be equal to wave A in distance. Also tensions between US and Russia are definitely not supportive for stocks either.

10 Year US Notes vs S&P500, 2h

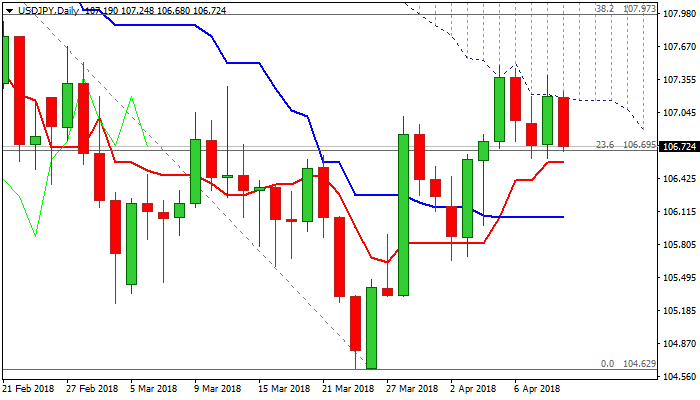

USDJPY- Bearish Bias on Fears over Syria; Thick Daily Cloud Continues to Cap

The pair holds in a steady descend from Asian high at 107.24 and dipped to 106.68 (American session low) on probe through 10SMA (currently at 106.70).

Negative bias is gaining traction as techs point lower following multiple rejections under the base of thick daily cloud and fundamentals turn focus from fading concerns about trade war towards increasing fears over the situation in Syria.

Comments of US President Trump about potential missile attack increased demand for safe haven yen, keeping near-term risk shifted lower.

Stronger bearish signal could be expected on close below 10SMA, while return below converged 20/30 SMA’s is needed to confirm reversal.

Res: 107.18; 107.50; 107.97; 108.50

Sup: 106.60; 106.40; 106.27; 106.00

Pound Rally Continues as US Consumer Inflation Sags

The British pound continues to head upwards and has posted gains for a fourth straight session. GBP/USD has gained 1.4% since Friday. In Wednesday trade, GBP/USD is trading at 1.4206, up 0.22% on the day. On the release front, British Manufacturing Production disappointed with a decline of 0.2%. This missed the estimate of a 0.2% gain. Britain’s trade deficit narrowed to GBP -10.2 billion, beating the estimate of GBP -12.0 billion. This marked the lowest deficit since October 2016. In the US, CPI declined 0.1%, shy of the estimate of 0.0%. This marked the first decline since May. Core CPI remained unchanged at 0.2%. Later in the day, the Federal Reserve will release the minutes of the March policy meeting.

The tariff spat between the US and China appears far from over, but both sides have lowered the rhetoric over the trade battle which has roiled the markets in recent weeks. Investors are breathing a sigh of relief after Chinese President Xi Jimping sent out a conciliatory message on Tuesday. Xi was speaking at a development conference in China, and promised to lower tariffs on vehicle imports into China. This has been a major sticking point between the US and China, with President Trump complaining that China has a 25% tariff on US vehicle imports, yet the US only charges 2.5% on Chinese vehicles. Xi added that China was looking to solve issues through dialogue rather than confrontation, and the markets are hoping that the US and China can avert a trade war, which could drag down the global economy.

Where is the Bank of England headed? The bank does not meet for a rate meeting until next month, but there is support for a quarter-point rate increase. On Tuesday, BoE member Ian McCafferty urged the bank not to delay in raising rates, and other policymakers support this view. One strong reason in favor of a rate hike is that inflation remains around 3%, well above the 2% target. However, the lukewarm British economy and the dark cloud of Brexit are key reasons why Governor Mark Carney has not been enthusiastic about raising rates. As things currently stand, a quarter-point rate hike seems likely at the May meeting.

Japanese Yen Gains Ground as US Consumer Inflation Contracts

USD/JPY has posted losses on Wednesday, erasing the gains seen which marked the Tuesday session. In the North American session, USD/JPY is trading at 106.72, down 0.45% on the day. On the release front, Japanese Core Machinery Orders gained 2.0%, crushing the estimate of -2.6%. Japanese PPI dropped for a fourth straight month, coming in at 2.1%. This marked the lowest gain since June. In the US, CPI declined 0.1%, shy of the estimate of 0.0%. This marked the first decline since May. Core CPI remained unchanged at 0.2%. Later in the day, the Federal Reserve will release the minutes of the March policy meeting.

As relations between the US and Russia continue to worsen, the markets are growing nervous, which could be a boon for the safe-haven Japanese currency. Syrian forces allegedly used chemical weapons on rebel-held areas last week, and a UN Security Council meeting on Tuesday ended inconclusively after Russia cast a veto on a US proposal to prove the attack. US President Trump has warned of an imminent military strike against Syria, and Russia has countered that it will respond to any US move. If Trump makes good on his promise, investor risk appetite could sink and send the Japanese yen higher.

The tariff spat between the US and China appears far from over, but both sides have lowered the flames which has roiled the markets in recent weeks. Investors are breathing a sigh of relief after Chinese President Xi Jimping sent out a conciliatory message on Tuesday. Xi was speaking at a development conference in China, and promised to lower tariffs on vehicle imports into China. This has been a major sticking point between the US and China, with President Trump complaining that China has a 25% tariff on US vehicle imports, yet the US only charges 2.5% on Chinese vehicles. Xi added that China was looking to solve issues through dialogue rather than confrontation, and the markets are hoping that the US and China can avert a trade war, which could drag down the global economy.

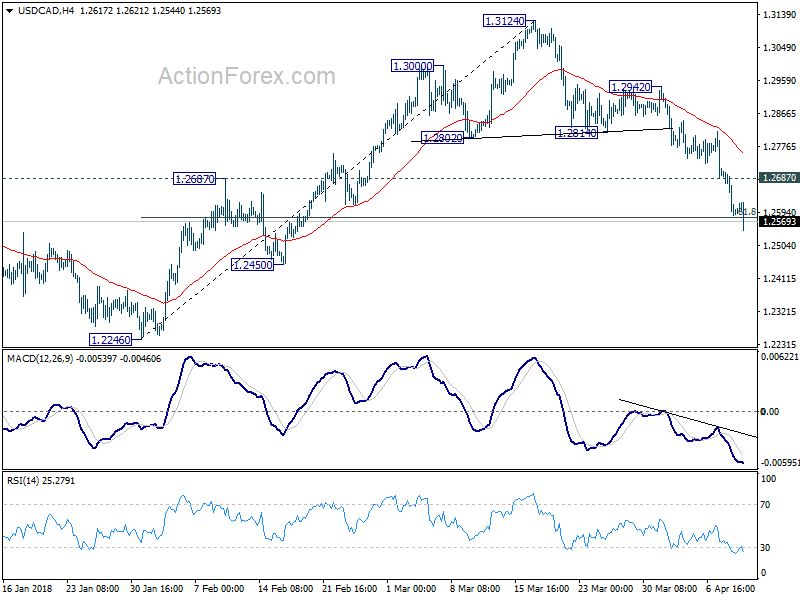

Fresh selling in USD after Saudi Arabia intercepted missiles over Riyadh, CAD follow oil higher

USD suffers another round of selloff after report that Saudi Arabia intercepted missiles over Riyadh after at least three blasts were heard in the city. WTI crude oil surges to as high as 66.82. It remains to be seen if it can sustain above key resistance level at 66.66. But momentum is promising.

Riding on the news, USD/CAD extends recent to as low as 1.2544. It's on course to next support level at 1.2450.

DOW opened lower but stabilized in initial trading. It's currently struggling around 55 H EMA, feeling heavy. Losing 24200 handle will likely prompt sellers to come out and send DOW back to 24000 handle.

DOW opened lower but stabilized in initial trading. It's currently struggling around 55 H EMA, feeling heavy. Losing 24200 handle will likely prompt sellers to come out and send DOW back to 24000 handle.

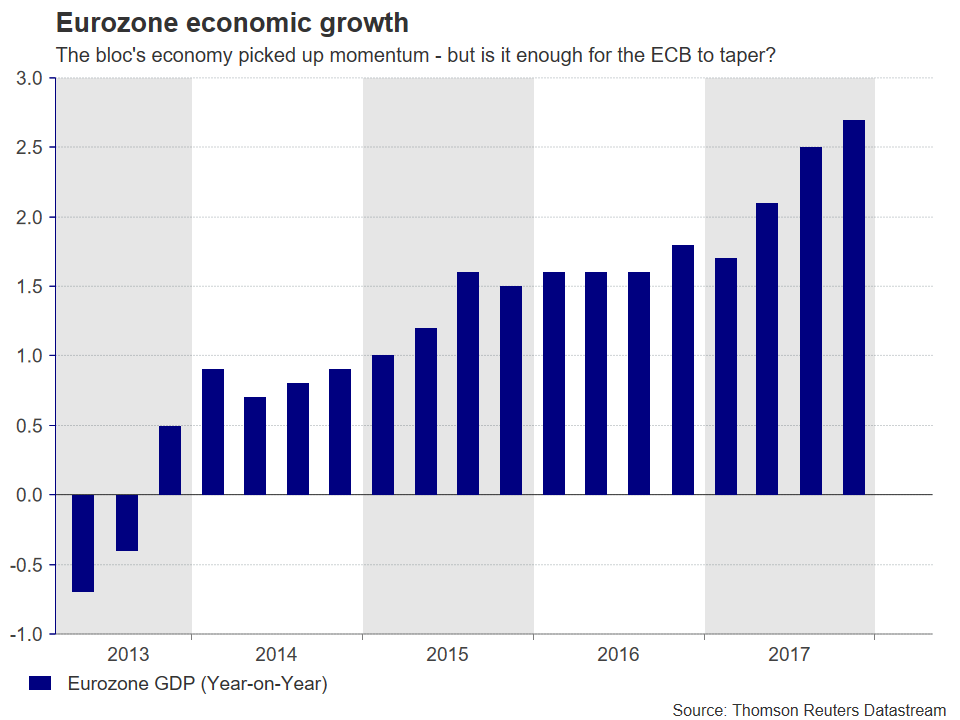

ECB Minutes Eyed for QE-Tapering Clues

The European Central Bank (ECB) will release the minutes from its March policy gathering on Thursday, at 1130 GMT. As always, investors will look for fresh clues regarding when policymakers plan to start winding down their asset purchase program, though the conversation regarding trade risks could also attract attention considering recent events.

Even though the ECB took no action in March, keeping its benchmark interest rates and asset purchase program untouched, it did tweak its forward guidance in a more hawkish direction. The Bank removed from its statement the so-called QE easing bias, the commitment that it stands ready to increase the size and/or duration of its purchases if the economic outlook becomes less favorable. This move was seen as laying the groundwork for policymakers to end their asset purchases completely later this year, triggering a spike higher in the euro.

The gains were short-lived though, with the common currency plunging to trade much lower once President Draghi started to explain the decision. The ECB chief downplayed the importance of that development, noting the Governing Council simply dropped a redundant sentence from its guidance, and that the removal does not send a signal about future decisions.

Draghi has been quite successful in “managing” market expectations, avoiding fueling too much speculation that a QE-tapering announcement is looming. Indeed, the ECB has been very careful in trying to avoid the Fed’s “taper tantrum” experience, as it heads for its own stimulus-exit door. That said, the minutes will provide an insight into the views of the entire Governing Council, not just Draghi’s. In this context, several officials have expressed their desire to end QE sooner rather than later, and the minutes could add some more color on that discussion. In particular, is the “hawkish camp” within the ECB growing larger in light of the strong growth momentum the Eurozone enjoyed recently? If so, that could work in favor of the euro.

Another area of interest will be the discussion around trade risks. Back then, only the US tariffs on steel and aluminum had been announced, so tensions had not really escalated. Still, when asked about tariffs at the press conference, Draghi said the economic impact will depend primarily on whether there is retaliation, and whether business confidence is affected, which could spill over into lower growth and inflation. Overall, his remarks suggest a conversation on the matter did take place, and investors will probably look for signals on how the Bank would respond to a further escalation in such risks.

Another area of interest will be the discussion around trade risks. Back then, only the US tariffs on steel and aluminum had been announced, so tensions had not really escalated. Still, when asked about tariffs at the press conference, Draghi said the economic impact will depend primarily on whether there is retaliation, and whether business confidence is affected, which could spill over into lower growth and inflation. Overall, his remarks suggest a conversation on the matter did take place, and investors will probably look for signals on how the Bank would respond to a further escalation in such risks.

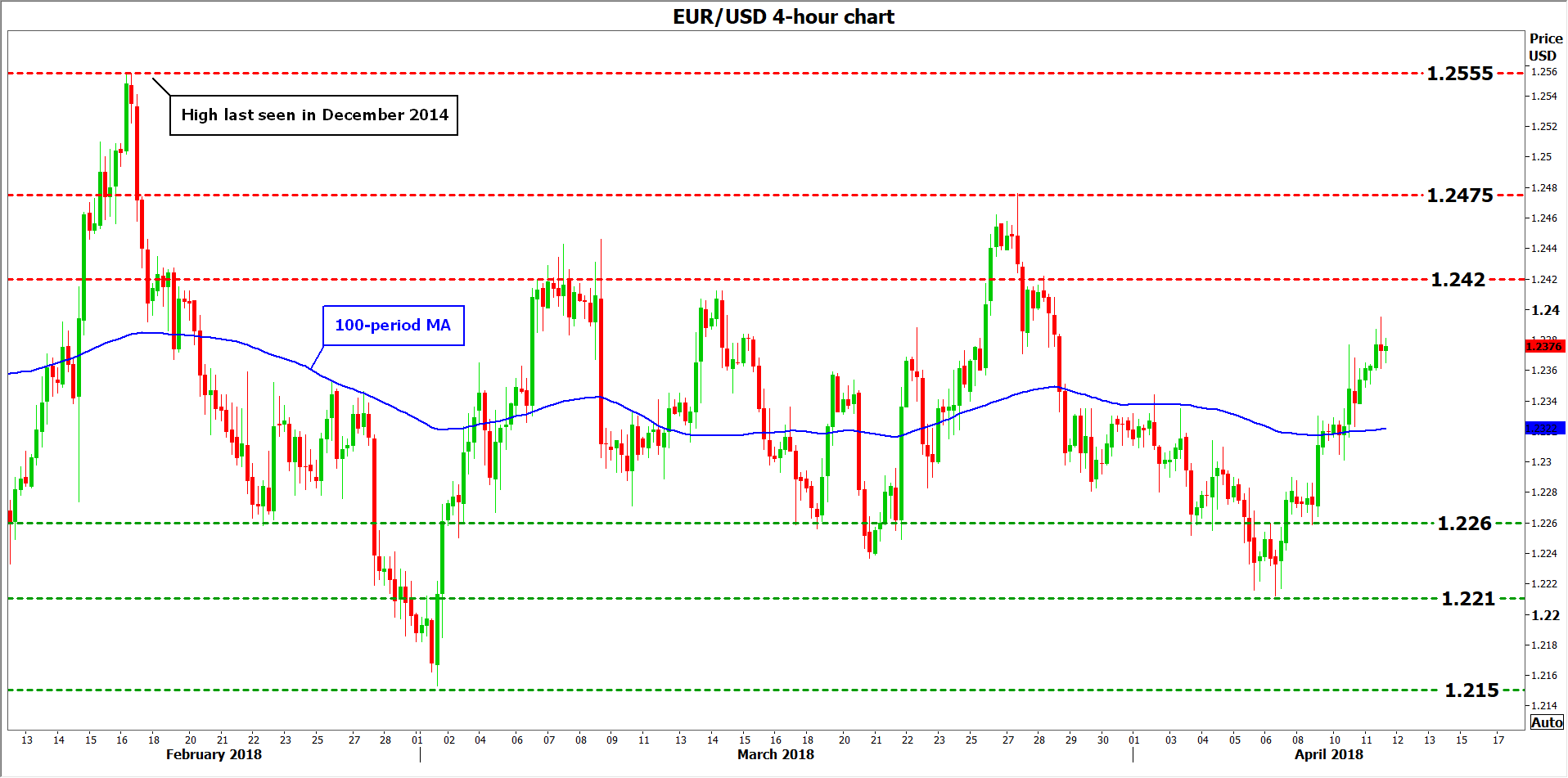

If the minutes reflect an increasing sense of optimism among officials, speculation that the Bank will begin tapering its asset purchases sooner rather than later could bring the euro under renewed buying interest. Euro/dollar could edge up and challenge the 1.2420 zone, marked by the highs of March 28, with an upside break bringing into focus the March 27 top at 1.2475. Even further advances could open the way for the pair’s three-year highs, at 1.2555.

On the flipside, if minutes paint a picture of a cautious ECB, the euro could edge lower. In this case, euro/dollar could encounter some support near the 100-period moving average on the 4-hour chart, at 1.2322. Steeper declines could initially target the 1.2260 line, defined by the lows of April 9, and subsequently the 1.2210 hurdle, marked by the trough of April 6. Even lower, support may be found at the low of March 1, at 1.2150.

US: Consumer Price Inflation Continues to Firm

The Consumer Price Index fell 0.1 percent in March amid a drop in gasoline prices. The trend is firming, however, with the core index increasing 0.2 percent and at a 2.9 percent annual rate over the past three months.

Energy Burns Consumer Price Inflation in March

CPI inflation fell 0.1 percent in March, the first monthly decline in a year. March's decline can be entirely traced to energy, where prices fell 2.8 percent. The cost of energy services dipped slightly last month, but the primary source of the pullback was a 4.9 percent drop in gasoline prices. Elsewhere, however, price gains were stronger and point to inflation continuing to firm. Prices for food at home rose 0.1 percent, which was above the average monthly gain over the past year.

Core Remains Strong

After what had been the strongest three-month run in 10 years, the core index increased 0.2 percent (0.18 percent). Although on the surface the gain looked similar to February, when the index also rose 0.18 percent, the components tell a different story.

Core services strengthened 0.3 percent, led by a rebound in shelter costs. Primary rent and owners' equivalent rent last month posted the smallest gains in more than three years, so the 0.4 percent increase in shelter costs looks due to some payback for last month's below-trend reading. It is worth noting, however, that rent growth has been slowing more generally, leading to the smallest 12-month gain since late 2015 as the flood of new apartments is finally beginning to weigh on prices. Prices for medical services also strengthened notably (up 0.5 percent) after being flat last month.

Snapping a three-month string of gains, core goods prices edged down 0.1 percent. Apparel prices led the decline (down 0.6 percent) after what had been the strongest two months of increases since the early 1990s. Used vehicle prices fell for a second straight month, down 0.3 percent.

Wireless Services No Longer a Hang Up

It was this time last year that core inflation posted a surprising decline due to the now-infamous drop in wireless services. The index fell 0.1 percent—a rare event outside of a recession. With the drop now a full year behind us, the 12-month rate of core inflation jumped from 1.8 percent to 2.1 percent. While the 12-month change has been helped by an easy base comparison, we believe there is more strength to come even without such a favorable comparison over the next few months. Core CPI has increased at a 2.9 percent annual rate over the past three months, which points to the year-ago rate of core CPI climbing a bit further in the months to come. We look for the core index to increase 2.2 percent year-over-year in the second quarter.

FOMC Chair Powell and other members have been aware of the favorable arithmetic surrounding the year-ago rate of core inflation, so the jump in March is unlikely to alter their view of inflation. What we believe is likely to be more influential in the Fed's thinking is the strength that has prevailed since late last year, as well as broadening indications of higher input costs for labor and raw materials.