Sample Category Title

USD/JPY Daily Outlook

Daily Pivots: (S1) 106.53; (P) 106.89; (R1) 107.13; More...

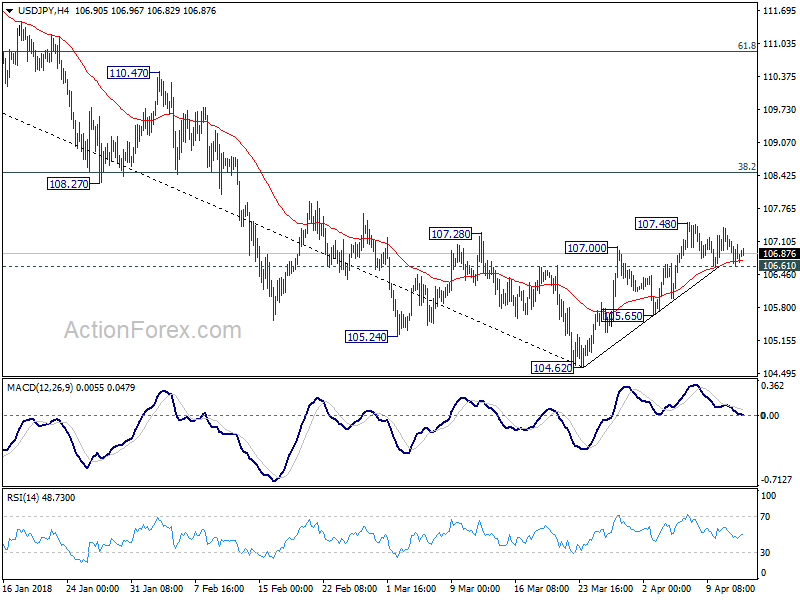

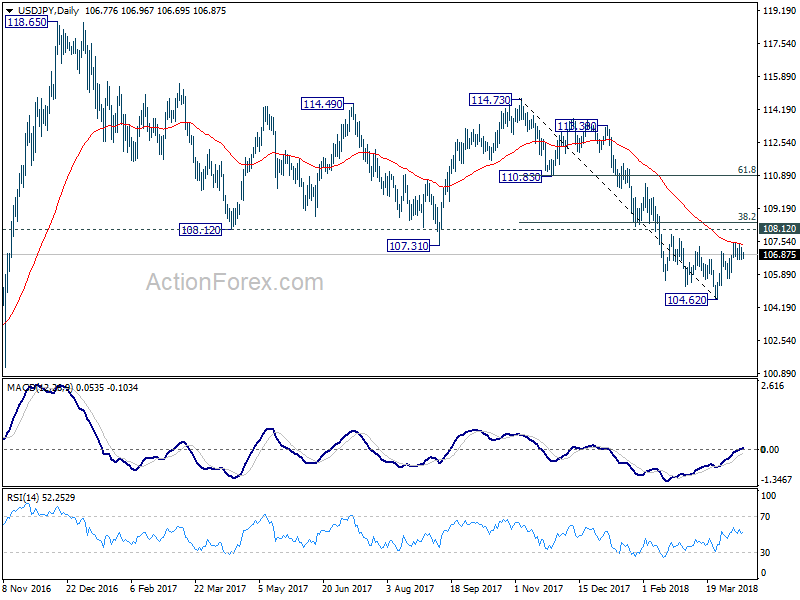

USD/JPY is still staying in range below 107.48 and intraday bias remains neutral. On the downside, below 106.61 minor support will bring deeper fall to 105.65. Break of 105.65 support will indicate that the rebound from 104.62 is completed and target a test on 104.62 low. This will also retain medium term bearishness for down trend resumption later. On the upside, above 107.48 will extend the rebound to 38.2% retracement of 114.73 to 104.62 at 108.48 9 which is close to 108.12 and is crucial to determine the medium term outlook.

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

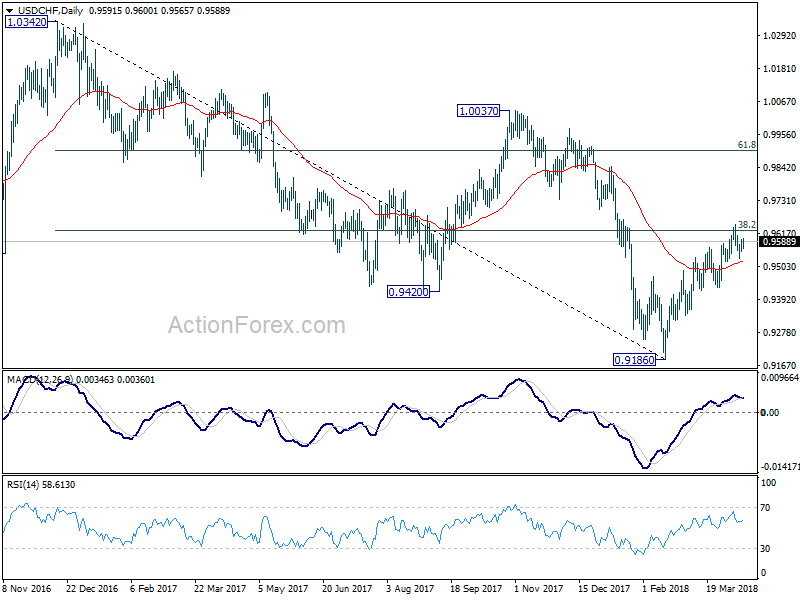

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9555; (P) 0.9576; (R1) 0.9596; More...

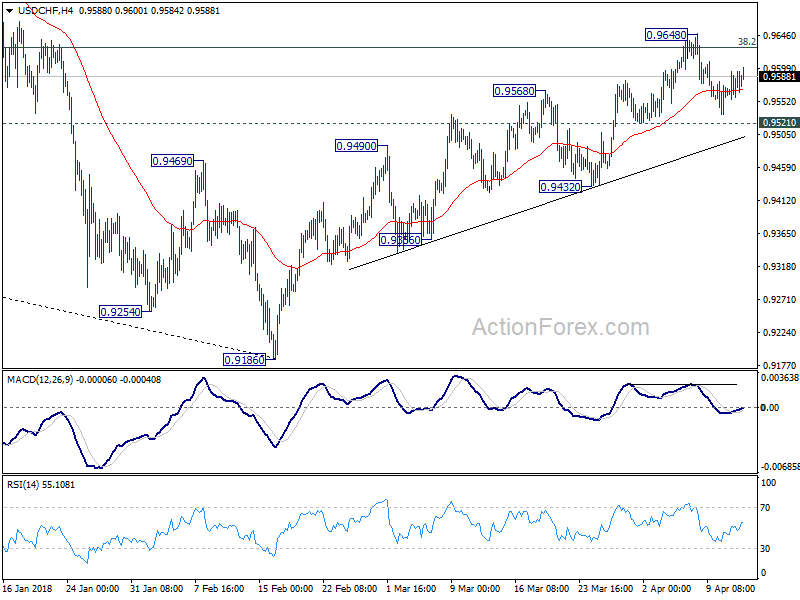

No change in USD/CHF's outlook as it's still bounded in range of 0.9521/9648. Intraday bias remains neutral for the moment. On the downside, firm break of 0.9521 minor support will indicate rejection by 0.9626 key fibonacci resistance. Intraday bias would then be turned back to the downside for 0.9432 support first. Break there will also confirm completion of rebound from 0.9186 and turn outlook bearish. On the upside, sustained break of 0.9626 will be another evidence of larger reversal. In this case, further rise would be seen to next fibonacci level at 0.9900.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above. However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

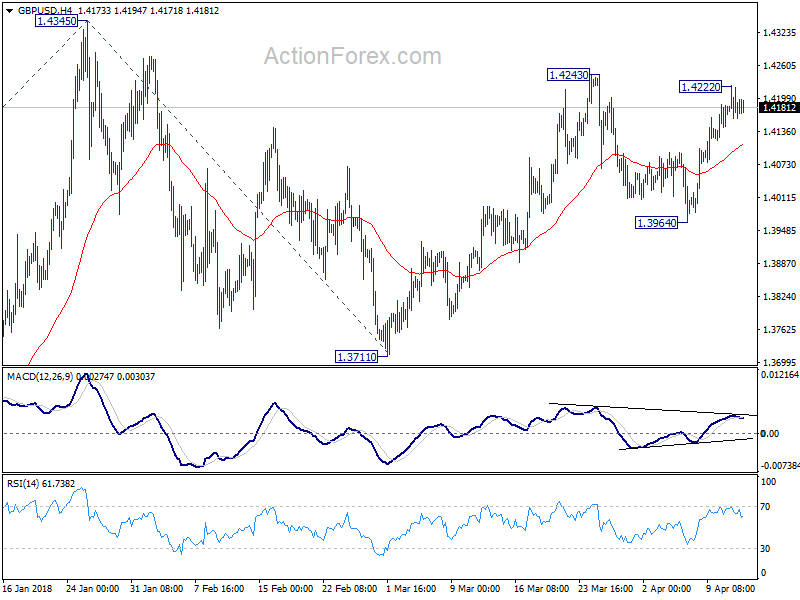

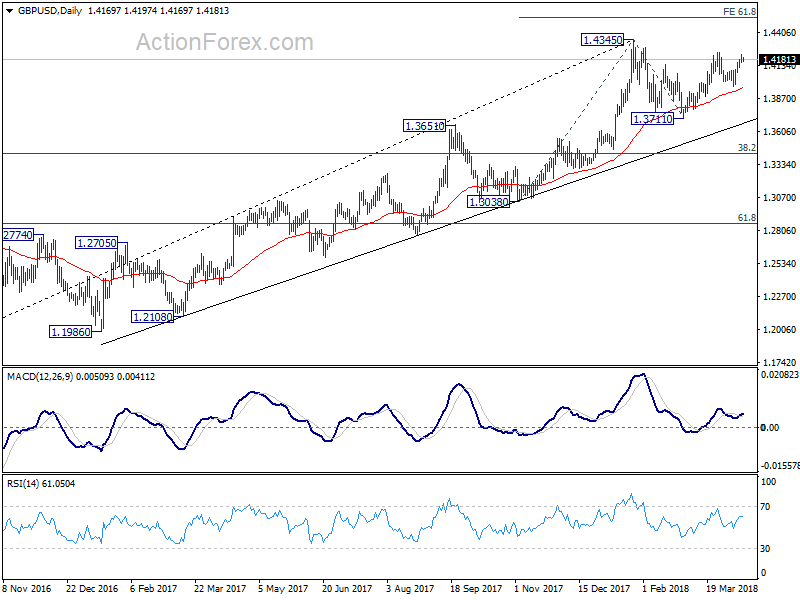

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4151; (P) 1.4187; (R1) 1.4214; More....

GBP/USD lost momentum after hitting 1.4222, ahead of 1.4243 resistance, as seen in 4 hour MACD. Intraday bias is turned neutral first. Another rise is expected as long as 1.3964 support holds. Above 1.4222/43 will target 1.4345 high. Firm break of 1.4345 will resume medium term rally and target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 next.

In the bigger picture, as long as 1.3651 resistance turned support holds, medium term outlook in GBP/USD will remain bullish. Rise from 1.1946 is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4267) so far. Break of 1.3651 will be the first sign of medium term reversal and turn focus to 1.3038 support for confirmation.

EUR/USD Bullish Momentum Running Out Of Steam

The EUR/USD uptrend channel is running into a key resistance zone between 1.24 and 1.25. The bullish price action could struggle to continue higher and a break below the support trend line (blue) could complete this bullish swing, which could be a wave 1 (green) of the uptrend or a bearish correction within a larger ABC (brown).

The EUR/USD bullish momentum seems to be running out of momentum, which could indicate either the end of a wave 1 (green) or wave A (red) of a larger wave B (brown). A break below the support (blue) trend line could create a bearish reversal whereas a break above resistance (red) could extend the 5th wave (orange)

The USD/JPYis testing the support trend line (blue), which is a break or bounce spot.A break above the shallow 38.2-50% Fib levels makes such a wave 4 unlikely whereas a bearish break below support (blue) could indicate a continuation of the downtrend.

The USD/JPY is building a lengthy sideways correction between support and resistance trend lines.A bearish breakout could start a reversal but a bullish breakout could be limited due to other resistance levels nearby.

US CPI Figures Yesterday Rose At The Fastest Pace During The Past Year

Market movers today

In terms of global data releases, today is quite boring. We get the ECB minutes from the March meeting but we doubt it will provide new insight about the timing of the next step in the normalisation process.

In Sweden, we get CPIF inflation data today, see page 2 for details.

Selected market news

Risk sentiment turned sour yesterday driven by geopolitics. Potential US action in Syria in Russian supported areas adds tensions to an already tough dilemma following last week's sanctions on Russia. Oil surged yesterday and now stands at USD66.7 per barrel.

As expected, there was no major news in the FOMC minutes released last night. There are a few things worth highlighting: (1) The Fed says trade policy poses a downside risk to the US economy, (2) the Fed thinks the expansionary policy will boost growth over the next years but thinks it is difficult to estimate the magnitude, as the output gap is already nearly closed, (3) 'several' Fed members think it is likely necessary to increase the Fed funds rate above the natural/neutral rate over the next couple of years to avoid overheating the economy and (4) the Fed will continue to shrink its balance sheet despite the USD liquidity situation. We still expect two more hikes this year with risk skewed towards three more hikes. The next hike will most likely come at the June meeting.

US CPI figures yesterday rose at the fastest pace during the past year, in line with expectations.

Overnight, sentiment from a joint PBoC/IMF conference suggested that China will 'unquestionably' retaliate if the US introduces more measures in the trade war. China also said that it already has a detailed plan if needed.

Oil Prices Gained for Three Days in a Row, Despite Inventory Build

The report from the US Energy Information Administration (EIA) shows that total crude oil and petroleum products stocks soared +5.97 mmb to 1191.55 mmb in the week ended April 6. Crude oil inventory gained +3.31 mmb to 428.64 mmb, amidst increases in 4 out of 5 PADDs. Stockpile in PADD 3 alone added +2.63 mmb for the week. Cushing stock added +1.13 mmb to 36.02 mmb. Utilization rate increased +0.5% to 93.5%. Meanwhile, crude production increased +0.62M bpd to 10.53M bpd for the week.

For refined oil products, gasoline inventory added +0.19 mmb to 238.94 mmb although demand increased +0.76% to 9.27M bpd. Production rose +0.35% to 10.15M bpd while imports plunged -13.93% to 0.66M bpd during the week. Distillate inventory reduced -0.81 mmb to 128.45 mmb as demand soared +7.28% to 4.17M bpd. Production added +4.79% to 5.26M bpd while imports jumped +26.3% to 0.13M bpd during the week.

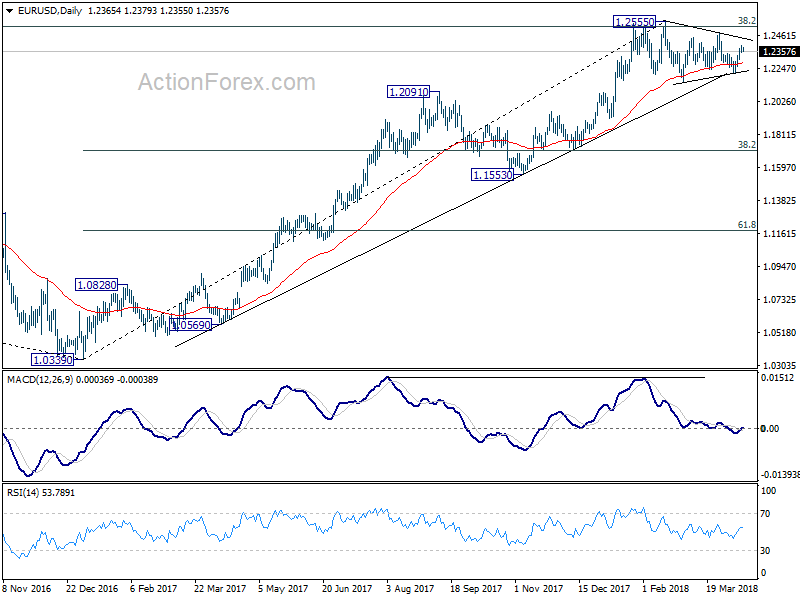

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2344; (P) 1.2369 (R1) 1.2393; More....

EUR/USD lost momentum after hitting 1.2396, as seen in 4 hour MACD. Intraday bias is turned neutral first. As long as 1.2302 minor support holds, further rise is in favor. Above 1.2396 will target 1.2475 first. Break will target key resistance level at 1.2555 high. However, as EUR/USD is still bounded in range trading pattern from 1.2555, break of 1.2302 minor support will turn bias back to the downside for 1.2214 instead.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

Euro to Look into ECB Minutes for Guidance, Markets Steady in Asia

The Asian markets are relatively steady today as for now, there is no escalation in the situation in Syria. At the time of writing Nikkei is trading down -0.26% only while HK HSI is down -0.17%. Performance of US indices overnight were not too bad. DOW closed down 0.9% at 24189.45 as there was no follow through selling below 24200 handle. In other markets, Syria tension continued to boost oil price with WTI breaching 67 handle, hitting the highest level since 2014. Gold also attempted to rally, hitting as high as 1365.24 but failed to push through 1366.95 resistance. Gold is back below 1350 at the time of writing, settling back into established range.

In the currency markets, Dollar is recovering broadly today, digesting recent loss. March FOMC minutes were seen as hawkish, yet they're not more hawkish than expected. Fed fund futures continued to price in over 95% chance of a June hike. But there is little support to the greenback. Dollar remains the second weakest one for the week, following Japanese Yen. Elsewhere in the currency markets are rather quite today. Focus will now turn to ECB monetary policy meeting accounts to be released in European session.

ECB minutes as the focus of today

Euro was shot up earlier this week by comments from outspoken ECB Governing Council member Ewald Nowotny. He firstly said the EUR 30b per month asset purchase could ended this year. Secondly, he called on ECB to start the process of raising interest rates. He noted he had no problem with moving deposit rate from -0.4% to 0.2% as first step. However, ECB was quick to clarify as a spokesman said Nowotny's view didn't represent the central banks. And Euro's rally lost steam since then.

For the March ECB meeting accounts, the markets would, as usual, like to know more on the central bank's plans on altering its language and forward guidance. Also, questions will remain on whether ECB would stop the asset purchase program after September, or it would taper it. In addition, while it's still admittedly still early, the markets would like to know if there is any discussion about raising interest rates, just as what Nowotny said.

Dollar gets no support from hawkish FOMC minutes

The minutes of the March FOMC meeting revealed nothing surprising. Almost all policymakers supported a rate hike even though there were a couple of them pointed to benefits of waiting a bit longer. All policymakers expected inflation to rise in the coming months, showing receding worry on the inflation outlook. Nonetheless, the pick-up in inflation is not enough to alter the projected rate path yet. Regarding the economy, it's a consensus view that outlook has strengthened in recent month. Meanwhile, a strong majority of the members viewed escalation in trade tension and retaliation by other countries as downside risks for the economy. The minutes are seen as hawkish in general, but not more hawkish than expected.

More on FOMC minutes:

- FOMC Minutes: Fiscal Stimulus During Full Employment Facilitates Inflation to Reach +2%

- FOMC Minutes: Chair Powell's First Meeting Confirms a Smooth Transition

High-level NAFTA talks to continue as sideline of Summit of the Americas in Lima

High-level NAFTA negotiation talks will resume this week on the sidelines of the Summit of the Americas in Lima, Peru this weekend. U.S. Trade Representative Robert Lighthizer will be present in the occasion even though President Donald Trump cancelled is trip. Canadian Foreign Minister Chrystia Freeland and Mexican Economy Minister Ildefonso Guajardo will be there too.

It's believed that Trump is still seeking to close the NAFTA deal quickly and offered a concession regarding car contents. The timing is important as securing the deal by May should meet all the necessary deadlines to have the revised NAFTA agreement approved by Republican-controlled Congress, before mid-term elections. Another key milestone is Mexican elections on July 1.

BoJ Kuroda and Maeda: Medium- and long-term inflation expectations improving

BoJ Governor Haruhiko Kuroda spoke at a branch manager meeting today. He expressed the an upbeat view on inflation. Kuroda noted improving output gap as well as heightening medium- to long-term inflation expectations. Thus, He expected "inflation accelerate as a trend and head toward 2 percent." Also, "Japan's economy is expected to continue expanding moderately". Nonetheless, Kuroda maintained that the ultra loose monetary policy needs to be maintained "until needed to stably and sustainably achieve" its target.

Separately, BOJ Executive Director Eiji Maeda told the parliament that "medium- and long-term inflation expectations are recently emerging from weaknesses. Also "wages and inflation are rising moderately." Maeda also said that "Japan's economy is making steady progress toward achieving the BOJ's 2 percent inflation target".

RBNZ McDermott: Entering into next stag of evolution

RBNZ Assistant Governor and Head of Economics John McDermott discussed "evolution in inflation targeting" in a speech delivered to the RBA conference on central bank frameworks in Sydney today. He noted that the New Zealand "framework has changed significantly over thirty years, reflecting lessons learned and the changing economic and political environment" And, the central bank is " about to enter the next stage of that evolution."

A key recent change to RBNZ's framework is duel mandates of inflation and employment. The exact wordings to be put on the Reserve Bank Act are not finalized yet. But putting a qualitative target like "maximum sustainable employment" would be a better choice rather than a numerical target. He pointed out that "focusing too narrowly on one indicator, such as the unemployment rate, can be misleading. For example, a fall in the unemployment rate could be the result of an increased demand for labour – typically reflecting a strong economy – or the result of people dropping out of the labour force altogether because they are unable to find a job and have become discouraged."

World Bank raised East Asia and Pacific growth forecast

The World Bank raised its growth forecast for East Asia and Pacific (EAP) in it's update today. 2018 growth for EAP is now projected to be 6.3%, revised up from October projection of 6.2%. China's growth forecast was also revised to 6.5%, up from October forecast of 6.4%.

Overall outlook of EAP was supported by "prospects for a continued broad-based global recovery and robust domestic demand". However, faster than expected monetary policy tightening in advanced economies and threat of escalation in trade tensions posted some risks to the region.

The World Bank urged that "to address risks to macroeconomic stability, countries will need to consider tightening monetary policies and further strengthening macroprudential regulations." Also, "improving competitiveness will also be important for countries in the region as they seek to adjust to the ongoing changes in the manufacturing landscape with the evolution of technology."

IMF Lagarde warned of two challenges of China's Belt and Road

IMF Managing Director Christine Lagarde talked about China's "One Belt, One Road" initiative at a conference in Beijing today. She acknowledged the potential of the initiative as a "platform for international cooperation" and there were already "signs of progress". Nonetheless, Lagarde also warned of two challenges.

Firstly, she urged that Belt and Road "Only travels where it is needed". She pointed to global experience of "failed projects" and "misuse of funds". Also, Chinese and other companies involved in construction overseas may face "new political, legal, and environmental obstacles". Secondly, she warned that the Belt and Road ventures can "problematic increase in debt". And that could potentially limit other spending as debt service rises and create "balance of payment challenges".

On the data front

UK RICS house price balance was unchanged at 0 in March. Japan M2 rose 3.2% yoy in March. Australia consumer inflation expectation slowed to 3.6% in April. Australia home loans dropped -0.2% mom in February.

Looking ahead, Eurozone will release industrial production and ECB minutes. Canada will release new housing price index. US will release import price index and jobless claims.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2344; (P) 1.2369 (R1) 1.2393; More....

EUR/USD lost momentum after hitting 1.2396, as seen in 4 hour MACD. Intraday bias is turned neutral first. As long as 1.2302 minor support holds, further rise is in favor. Above 1.2396 will target 1.2475 first. Break will target key resistance level at 1.2555 high. However, as EUR/USD is still bounded in range trading pattern from 1.2555, break of 1.2302 minor support will turn bias back to the downside for 1.2214 instead.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS House Price Balance Mar | 0% | 2% | 0% | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Mar | 3.20% | 3.20% | 3.30% | |

| 1:00 | AUD | Consumer Inflation Expectation Apr | 3.60% | 3.70% | ||

| 1:30 | AUD | Home Loans M/M Feb | -0.20% | -0.40% | -1.10% | |

| 9:00 | EUR | Eurozone Industrial Production M/M Feb | 0.10% | -1.00% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | CAD | New Housing Price Index M/M Feb | 0.00% | |||

| 12:30 | USD | Import Price Index M/M Mar | 0.10% | 0.40% | ||

| 12:30 | USD | Initial Jobless Claims (Apr 7) | 230K | 242K | ||

| 14:30 | USD | Natural Gas Storage | -29B |

Elliott Wave Analysis: USDCAD Moving In Impulsive Structure

USDCAD Short Term Elliott Wave view suggests that the decline from 3/19 high (1.313) is unfolding as a 5 waves impulse Elliott Wave structure. Down from 1.313, Minor wave 1 ended at 1.2819, Minor wave 2 ended at 1.2943, and Minor wave 3 is in progress. Internal of Minor wave 3 also unfolded as an impulse with a nest. Minute wave ((i)) of 3 ended at 1.2771, Minute wave ((ii)) of 3 ended at 1.2847, and Minute wave (((iii)) is unfolding as a 5 waves of lesser degree.

Down from Minute wave ((ii)) at 1.2847, Minutte wave (i) of ((iii)) ended at 1.274, Minutte wave (ii) of ((iii)) ended at 1.2819, and Minutte wave (iii) of ((iii)) should complete with 1 more leg lower. Afterwards, expect pair to do minor bounce in Minutte wave (iv) of ((iii)) before turning lower again. While Minor wave 2 pivot at 4/2 high (1.2943) stays intact, expect pair to extend lower a few more legs before ending the entire 5 waves structure from 3/19 high. We don’t like buying the pair.

USDCAD Elliott Wave 1 Hour Chart

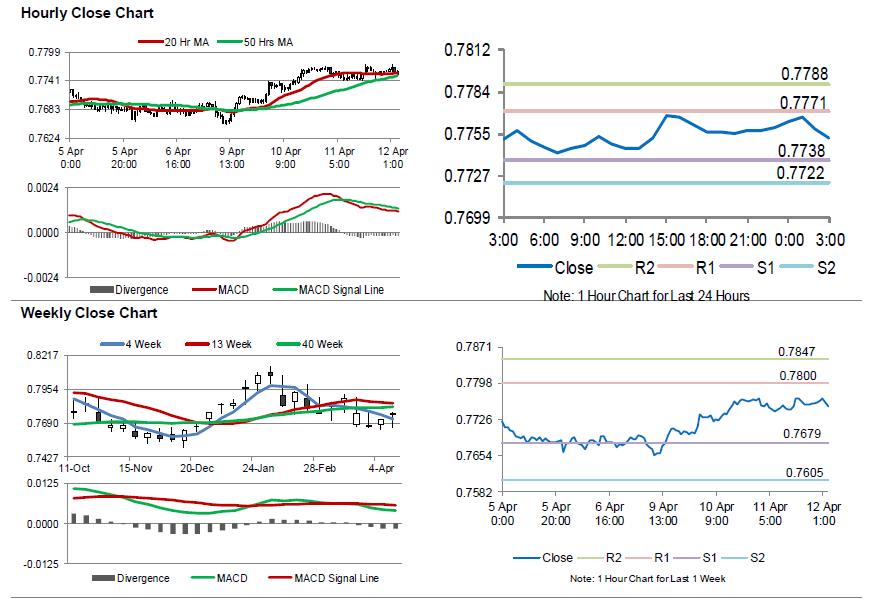

Australia’s Consumer Inflation Expectations Dropped In April

For the 24 hours to 23:00 GMT, the AUD declined 0.08% against the USD and closed at 0.7760.

LME Copper prices rose 0.62% or $42.5/MT to $6930.5/MT. Aluminium prices rose 3.75% or $81.5/MT to $2253.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7753, with the AUD trading 0.09% lower against the USD from yesterday's close.

In economic news, Australia's consumer inflation expectations eased to 3.6% in April, after recording a reading of 3.7% in the prior month.

The pair is expected to find support at 0.7738, and a fall through could take it to the next support level of 0.7722. The pair is expected to find its first resistance at 0.7771, and a rise through could take it to the next resistance level of 0.7788.

Looking ahead, market participants would focus on the Reserve Bank of Australia's (RBA) financial stability review, due to release tomorrow.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.