Sample Category Title

EURUSD Intraday Analysis

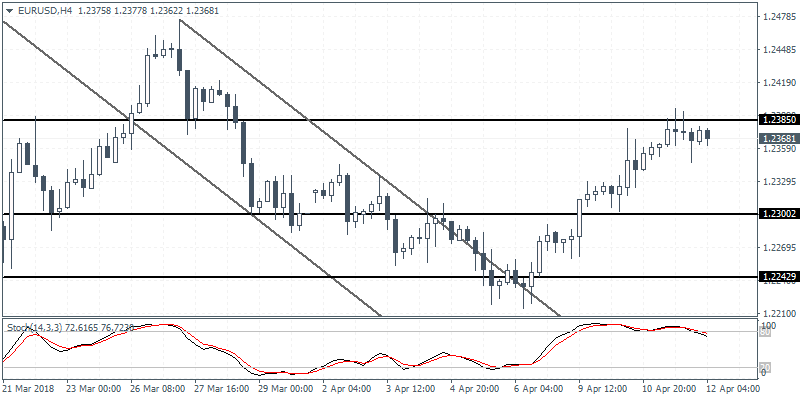

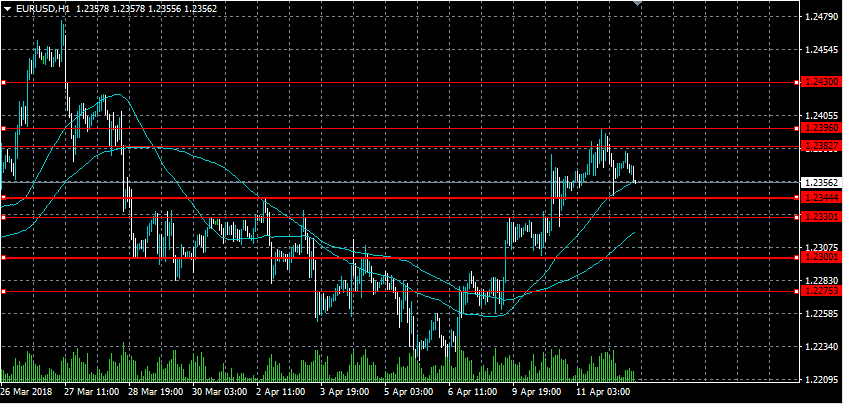

EURUSD (1.2368): The EURUSD rallied to the 1.2400 area before retracing the gains. The test towards the 1.2400 region comes after the euro currency posted gains for four consecutive days following the rebound off the 1.2241 level of support. On the 4-hour chart, the multiple retests near 1.2385 suggests that the momentum in price action might be slowing. We expect the EURUSD to ease back from the current highs and maintain a sideways range within 1.23385 and 1.2300 region.

After Fed Minutes, Investors Turn To The ECB Minutes

The FOMC meeting minutes released yesterday did not show any surprises even as the U.S. dollar weakened ahead of the meeting. However, members were seen to be hawkish as all members preferred to see higher GDP and inflation. There was also building consensus among the voting members for more rate hikes.

Investor sentiment was kept in check with developing global stories which included the U.S. President Trump threatening to take action against Russia in Syria while reports showed that Saudi Arabia had intercepted a missile over Riyadh.

On the economic front, data from the UK showed that manufacturing production fell 0.2% on the month with the previous month revised down to show an unchanged print. Construction output also declined 1.6% on the month while industrial production rose just 0.1%. The British pound however managed to maintain the gains.

Data from the U.S. showed that headline CPI fell 0.1% on the month in March but still the annual inflation rate rose to 2.4%. Core CPI which excludes the volatile food and energy prices rose 0.2% on the month as expected.

Looking ahead, the economic calendar today will see the BoE's Broadbent speaking earlier in the day. This is followed by the final inflation figures from France. The main highlight of the day will of course be the monetary policy meeting minutes which will be released by the ECB.

The NY trading session is relatively quiet with only the BoE Governor Carney expected to speak at an event later in the day.

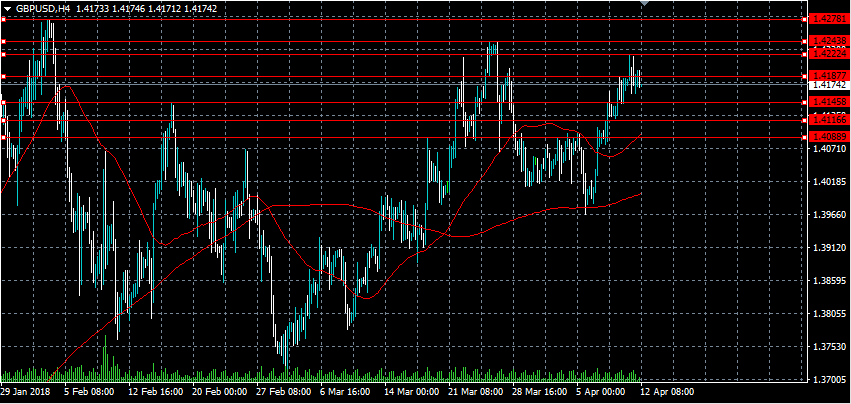

GBPUSD Only Intraday Bearish Below 1.4146 Level

The British pound has started to give back recent trading gains against the U.S dollar, after repeated technical price-failures above the key 1.4200 level on Wednesday. The GBPUSD pair currently trades around the 1.4170 level, and is currently under slight selling pressure from the bearish double-top pattern formation. Traders now look towards a scheduled speech from BOE Governor Mark Carney later today, and the 1.4146 pivotal level for directional guidance.

The GBPUSD pair only retains its intraday bullish bias while clearly trading above the 1.4146 level, key technical resistance is now found at the 1.4222 and 1.4243 levels.

Should the GBPUSD pair move below the pivotal 1.4146 level, a deeper price-correction towards the 1.4116 and 1.4088 levels appears likely.

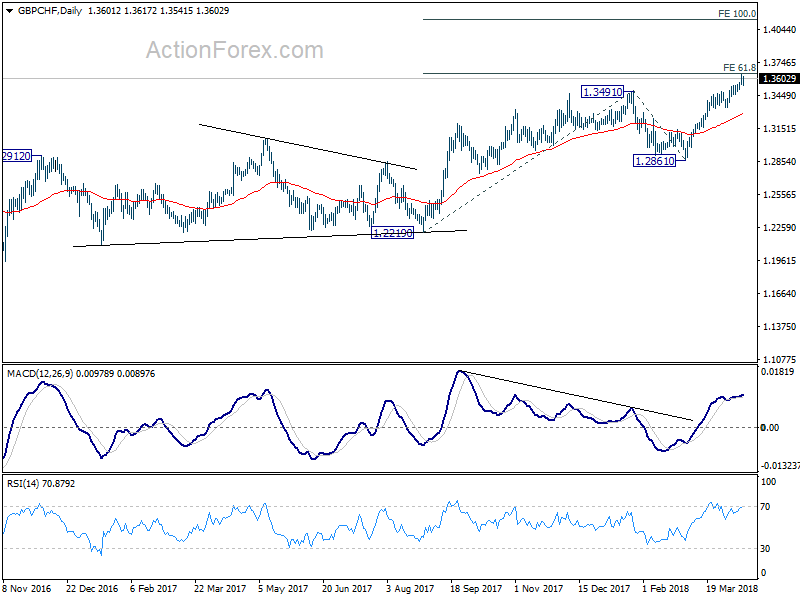

GBP/CHF building momentum for rally extension

We talked about GBP/CHF last week (here) and its rally did extend as we expected. It's so far reached as high as 1.3640, just inch below 61.8% projection of 1.2219 to 1.3419 from 1.2861 at 1.3647.

While GBP/CHF is not a big mover this week, momentum is still solid. Action Bias table is upside blue all the way with some neutral bars.

D action bias row show it's in solid rally, which is in line with the action bias chart too. The last three neutral 6H action bias bar should it was in consolidation. But H action bias bar argues that it's possibly building up momentum for a break out.

D action bias row show it's in solid rally, which is in line with the action bias chart too. The last three neutral 6H action bias bar should it was in consolidation. But H action bias bar argues that it's possibly building up momentum for a break out.

Outlook in the cross stay bullish and break of 1.3647 will pave the way to 100% projection at 1.4133.

Outlook in the cross stay bullish and break of 1.3647 will pave the way to 100% projection at 1.4133.

EURUSD Losing Bullish Momentum Below 1.2382

The euro currency has started to move lower against the U.S dollar, after the FOMC Meeting Minutes showed a more hawkish tone from U.S policy makers than expected. The EURUSD pair currently trades around the 1.2350 level, after finding strong weekly technical resistance from the 1.2396 level on Wednesday. Traders now look towards the ECB Monetary Policy Meeting Accounts, which provides a summary of the ECB’s monetary policy analysis and current monetary policy stance.

The EURUSD pair only retains its bullish intraday bias while trading above the 1.2333 level, key upside resistance remains at the 1.2382 and 1.2400 levels.

Should price-action on the EURUSD start to trade below 1.2333 level, sellers will likely test towards the 1.2300 and 1.2275 levels.

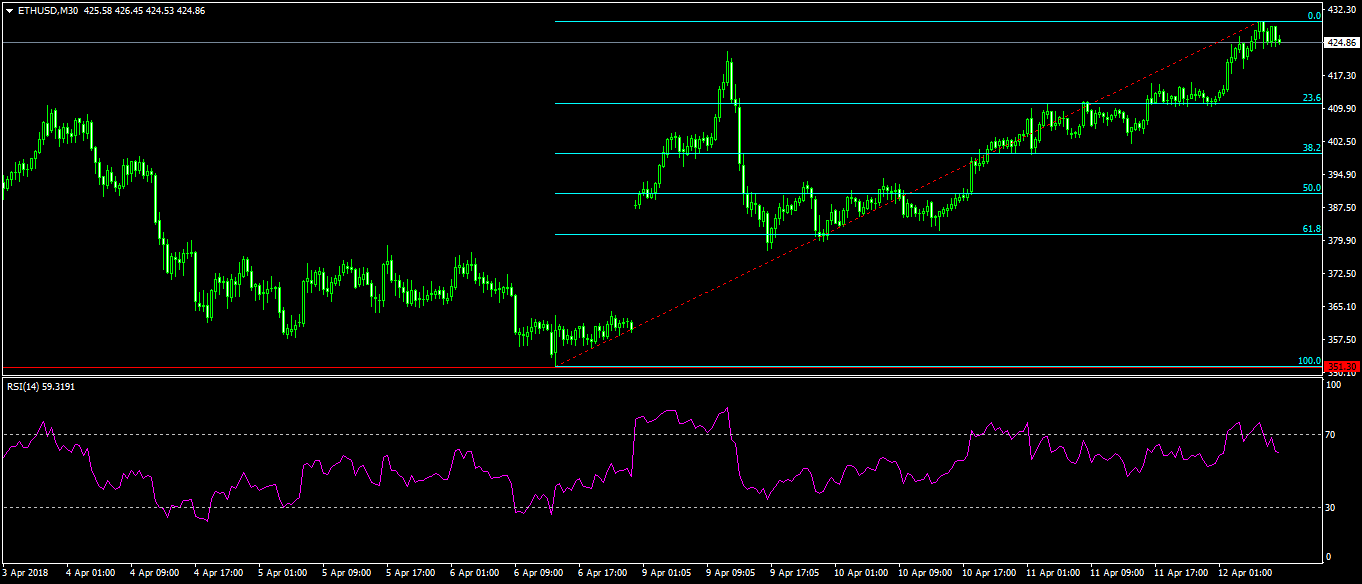

Ethereum Gains As Japan Provides Support

After weeks of declines, ethereum reached a low of $350 last Friday. After that, the ETH/USD pair has been making significant gains, soaring to a high of $426 this morning. At the same time, the price of bitcoin has formed a plateau, trading between a range of $7450 and $6400.

The surge in ethereum’s price is possibly because of Japan. A recent report by BTC Manager found that while most countries were focusing on regulations and shutting down exchanges, Japan was coming up with regulations to support the cryptocurrencies market. In addition, the country’s Financial Services Agency has been granting licenses to many cryptocurrencies exchanges. Japan is the third largest economy in the world with a GDP of almost $5 trillion.

Japanese support for the industry should not be understated. In recent months, China has banned ICOs and exchanges, South Korea has threatened the industry, and just yesterday, Australia placed major regulations on cryptocurrencies exchanges. In a statement, the Australian Transaction Reports and Analysis Center (ATRAC) said that all exchanges in the country must register immediately. At the same time, major debit and credit card providers announced that they would not allow cryptocurrencies transactions.

The rise in price may also be due to the official launch of Golem on the Ethereum Mainnet this week in beta form. The so-called ‘Airbnb for computers’ enables users to essentially ‘rent out’ idle CPU to others in exchange for cryptocurrency.

Also aiding the increase in price are the technical indicators that recently showed the ETH/USD pair being in the oversold zone. The pair is currently trading at $425. This rise could continue as the tax season in the US ends. However, in the short term, the pair could retrace to about $410 or $400 levels which are important Fibonacci Retracement levels.

ECB Meeting Minutes Drive The Headlines On Thursday

A combination of economic data and monetary policy will dominate the headlines on Thursday. The European Central Bank (ECB) tops the list when it releases the minutes of its most recent policy meeting.

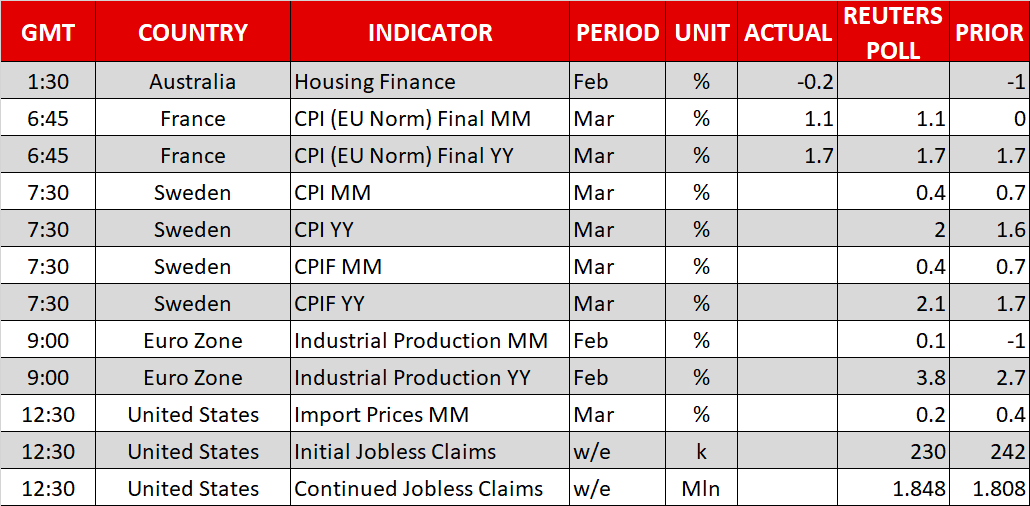

French inflation data will kick off the economic calendar on Thursday. The report, which is scheduled for 06:45 GMT, is expected to show a strong pickup in consumer price growth in March. The headline reading will likely show 1.1% growth compared with February. However, the annual rate will likely hold at 1.7%.

The European Commission's statistical agency will release the latest factory data at 09:00 GMT. Industrial production across the 19-member Eurozone is forecast to rise 0.1% in February after a 1% drop the previous month. In annualized terms, this translates into a gain of 3.8%.

The ECB will release its monetary policy meeting accounts at 11:30 GMT, giving investors more insight into the most recent interest rate decision. Officials have remained on the sidelines in recent months as the euro area recovery engine continues to pick up steam. The central bank has already shifted course on its policy trajectory by announcing cuts to its record stimulus program. In doing so, it joins the US Federal Reserve and Bank of Canada in beginning to normalize monetary policy.

ECB Executive Board member Benoit Coeure will deliver a speech at 12:15 that will be closely monitored by currency traders.

Shifting gears to North America, the Labor Department will report on initial jobless claims at 12:30 GMT. North of the border, the Canadian government will also release its latest housing price index for new properties.

Bank of England (BOE) Governor Mark Carney is scheduled to deliver a speech late on Thursday. A few hours later, Federal Open Market Committee (FOMC) member Neel Kashkari will do the same.

EUR/USD

Europe's common currency drifted lower on Wednesday after a hawkish reading of the FOMC meeting minutes emboldened the dollar. EUR/USD was last seen trading at 1.2372, having rebounded from a daily bottom of 1.2352. The pair faces immediate support at 1.2340. Resistance is located just above 1.2400.

GBP/USD

The British pound weakened in mid-week trade as investors took in the FOMC minutes. Cable bottomed out near 1.4160 before recovering around 1.4190. However, upside remains in tact, with the bulls eyeing a return to the 1.4245-1.4275 region. On the opposite side of the spectrum, immediate support is located at 1.4155.

USD/CAD

FOMC minutes couldn't save the USD/CAD from another down session. The pair fell to fresh six-week lows on Wednesday, as the Canadian dollar extended its ongoing recovery. The pair is currently trading at 1.2566, having declined 0.1% from the previous close and a whopping 550 pips since 19 March.

Geopolitical Concerns Creep Into Markets, ECB Minutes Eyed

Here are the latest developments in global markets:

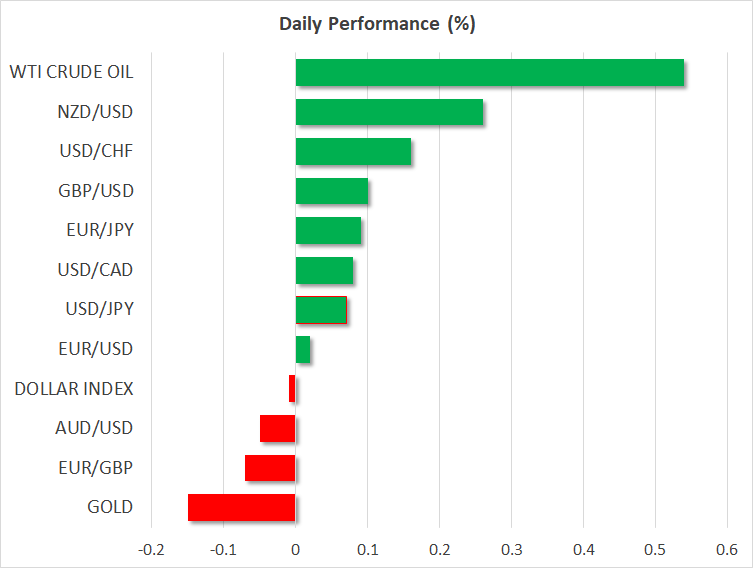

FOREX: The US dollar index traded practically unchanged on Thursday, with the currency unable to draw much support from the hawkish signals in the FOMC minutes, amid escalating tensions in the Middle East pushing US Treasury yields lower.

STOCKS: US markets closed lower yesterday, weighed on both by the optimistic tone of the FOMC minutes and rising geopolitical tensions, with the US-Russia standoff over Syria dominating headlines. The Dow Jones led the charge lower, shedding 0.9% of its value, while the S&P 500 and the Nasdaq Composite fell by 0.55% and 0.36% respectively. Nonetheless, futures tracking the Dow, S&P, and Nasdaq 100 are all pointing to a slightly higher open today. Risk aversion spread to Asia as well, with Japan’s Nikkei 225 and Topix declining by 0.1% and 0.4% correspondingly. In Hong Kong, the Hang Seng tumbled by 0.8%. In Europe, futures tracking all the major indices were flashing red as well.

COMMODITIES: Oil prices soared yesterday, with both WTI and Brent reaching fresh 3-year highs, as rising tensions in Syria were seen as threatening to disrupt oil production in the broader Middle East. Both WTI and Brent are higher today as well, by 0.55% and 0.4% respectively, with investors overlooking the larger-than-anticipated build in US crude stockpiles reported yesterday by the EIA, in the face of geopolitical risks. In precious metals, gold is 0.15% lower today, giving back some of the extraordinary gains it posted yesterday as investors sought safety. Prices surged to reach the $1365/ounce level, just shy of the 2017 high at $1366, before pulling back. Developments on the geopolitical front, particularly in Syria, will likely continue to dominate price action in the near-term.

Major movers: Geopolitical woes boost commodities, dollar rebounds after FOMC minutes

Risk appetite faltered once again yesterday, this time due to rising tensions in the Middle East. The initial wave of risk aversion was triggered by hostile rhetoric between Russia and the US, with the former threatening to shoot down any missiles the US fires into Syria, and US President Trump responding via Twitter that missiles “will be coming”.

While the US President tried to water down his remarks in subsequent tweets, the increasing risk of a standoff between two of the world’s superpowers continued to sap appetite for risk, leading investors to seek the safety of assets like gold and the yen. Gold prices in particular surged notably, coming just shy of touching their 2017 highs. Oil prices also soared reaching fresh three-year highs, seemingly on speculation that tensions could have spillover effects to other neighboring countries and disrupt oil production. Some reports of missiles flying over Saudi Arabia likely aided this narrative.

In economics, the minutes of the March FOMC meeting painted the picture of a Committee that is becoming increasingly more confident. “All” participants agreed that the economy would likely pick up steam soon and inflation will move higher in the coming months. Moreover, “several” officials judged the appropriate path for interest rates would likely be slightly steeper than they previously expected over the next years, in light of the improving backdrop. Overall, the hawkish signals helped the dollar to recover earlier losses and finish the day nearly unchanged.

In the commodity-linked currencies, kiwi/dollar is 0.25% higher today, aided by data overnight showing that consumer spending in New Zealand is picking up. Both the Aussie and the loonie were lower against the greenback, but by less than 0.1%. The loonie gained yesterday though, amid rising oil prices and media reports that the top NAFTA negotiators plan to meet this week and push for a preliminary deal.

In emerging markets, the Turkish lira touched a fresh record low against both the dollar and the euro yesterday. Besides Turkey’s large current account deficit, the lira is also pressured by speculation that the nation’s central bank is unwilling to raise rates in order to curb high inflation and defend the currency.

Day ahead: ECB minutes, eurozone industrial production and US jobless claims on the horizon

Thursday’s calendar features the release of ECB minutes, industrial production data out of the eurozone, as well as weekly jobless claims data out of the US.

Inflation numbers out of Sweden due out at 0730 GMT will bring krona pairs into the limelight.

At 1130 GMT, the attention will turn to euro pairs as the European Central Bank publishes the official record pertaining to the monetary policy meeting held on March 7-8. A hawkish tilt in policymakers’ views is anticipated to provide a lift to the common currency, with a dovish one having the opposite effect. Also of interest out of the eurozone will be industrial production figures for the month of February due earlier in the day (0900 GMT). Those are expected to reflect an improvement on both a monthly and a yearly basis.

Initial and continued jobless claims for the week ending April 7, as well as data on import & export prices for the month of March, will be generating interest out of the US; they’re all scheduled for release at 1230 GMT.

Policymakers delivering remarks include ECB Vice President Vitor Constancio who will be delivering a speech at a seminar on systemic risks and regulation commencing at 1400 GMT. Bundesbank President Jens Weidman will be talking at the same time.

Asset manager BlackRock is among companies releasing quarterly results on Thursday.

Lastly, tensions are rising in Syria and the same appears to hold true for the odds of military action by Western powers. More uncertainty in the region has the capacity to shift funds to perceived safe-haven assets, such as the yen and gold, while it also has implications for oil on the back of possible supply disruptions.

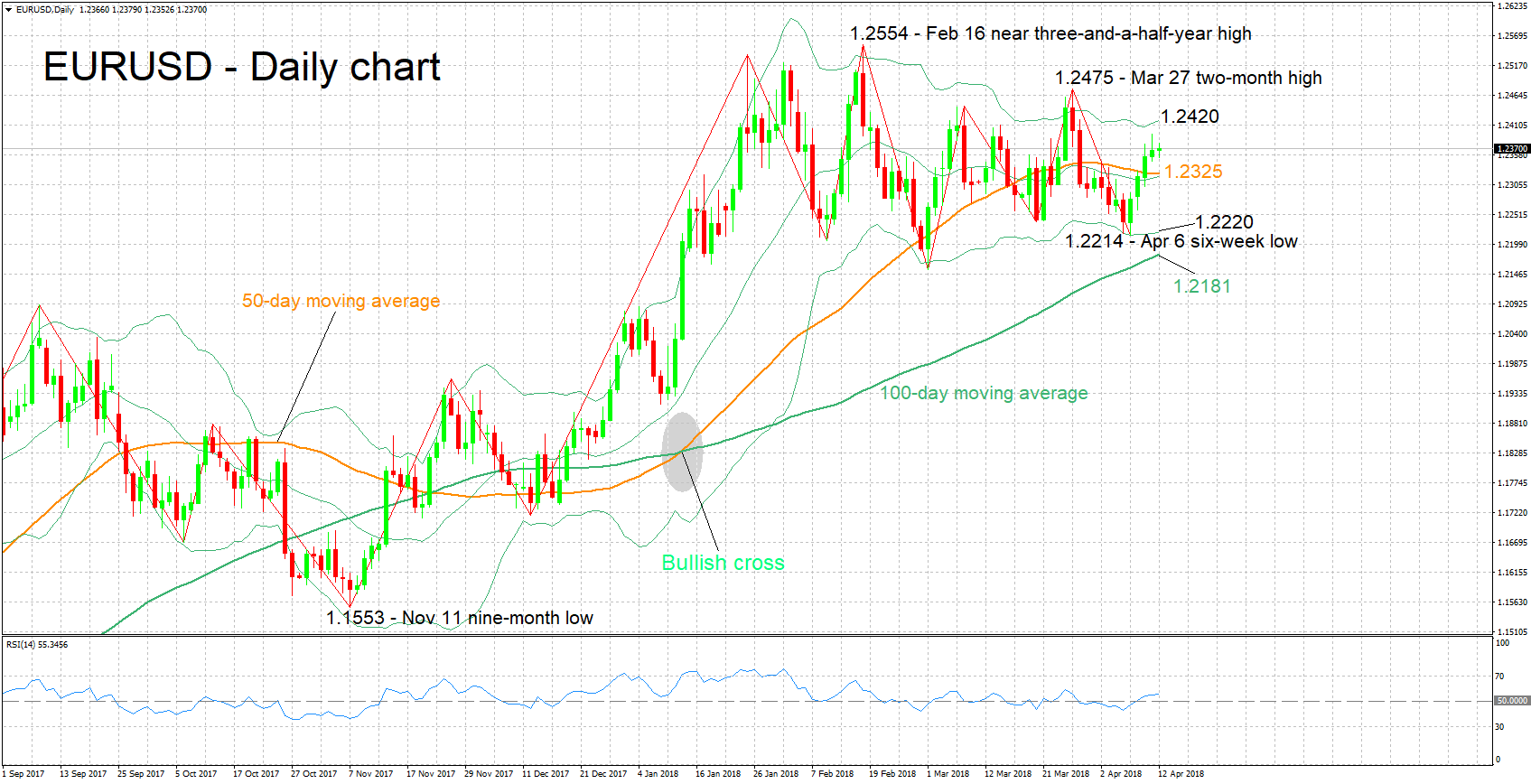

Technical Analysis: EURUSD looking mostly bullish in the short-term

EURUSD is advancing for the fifth straight day, with the pair currently trading 25 pips below yesterday’s two-week high of 1.2395. The RSI is rising in support of a positive short-term picture for the pair, though notice that its slope is not as steep at the moment; positive momentum may be fading.

Hawkish views by ECB policymakers in today’s meeting minutes are anticipated to refuel the bullish bias, with resistance to advances possibly coming around the upper Bollinger band at 1.2420. The area around this point also includes Wednesday’s two-week high of 1.2395, as well as the 1.24 round figure. Further above, the attention would turn to 1.2475, the two-month high from late March.

A dovish take by the ECB on the other hand, is expected to lead to weakness in the pair. Support to declines might come around the current level of the 50-day moving average at 1.2325 – this is where the middle Bollinger line roughly lies as well – with steeper losses shifting the focus to the range around the lower Bollinger band at 1.2220.

USDJPY Maintains Weak Bias In Near Term, Broader Trend Is Bearish

USDJPY remains under strong pressure and is looking more neutral as prices failed several times to climb above the 107.50 resistance level. This week’s upside momentum appears to have run out of steam as prices are flattening near the 107.00 psychological level. Looking at the bigger picture, the US dollar has been developing within a downward sloping channel against the Japanese yen since November 2016.

The neutral bias in the near term is also supported by the RSI indicator, which has been hovering slightly above the 50-neutral level in the past few days but failing to cross into negative territory. Also, the MACD oscillator is flattening above the zero line and is still moving with weak momentum. The 20 and 40 simple moving averages in the daily timeframe are pointing to the upside, suggesting a bullish crossover in the next few days in case of upside movement.

Should the pair manage to strengthen its positive momentum, the next resistance could come around the 108.00 psychological level. This level is the 23.6% Fibonacci retracement level of the downleg from 118.60 to 104.60. A break above the next resistance near 108.20 would shift the bias to a more bullish one and open the way towards the 38.2% Fibonacci near the 110.00 handle.

However, if prices are unable to jump above the aforementioned obstacles in the next few sessions, the risk would shift back to the downside with the 40- and next to the 20-day SMAs once again coming into focus at 106.40 and 106.30 respectively. A drop below these levels would signal a resumption of the longer-term downtrend. The next key support to watch lower down is the 105.65 level and then the more than 16-month low of 104.60.

Currencies: EUR/USD Rebound To Slow Post-Fed Minutes

Rates: Geopolitical tensions protect downside bonds short term

Risk sentiment will probably set the tone for trading. Rising geopolitical risks suggest short term downside protection for core bonds. Today's eco calendar won't move trading, but speeches by ECB Weidmann and Coeuré are wildcards. Will they follow fellow-hawk Nowotny who went off script on Tuesday, arguing in favour of a deposit rate hike soon after ending APP?

Currencies: EUR/USD rebound to slow post-Fed Minutes

Yesterday, the dollar remained in the defensive for most of the day. However, the US currency found a better bid after the publication of the Fed minutes. Is this a harbinger that the EUR/USD rally will slow? Today, the eco data will probably be only of intraday significance for USD trading. Geopolitics will remain a wildcard

The Sunrise Headlines

- US stock markets lost around 0.5% with Dow underperforming (-0.9%). Main Asian equity indices suffer a smaller setback with China underperforming.

- FOMC Minutes revealed that all participants wanted some further firming in rates because of the bullish eco outlook and optimism in inflation returning to 2%. A strong majority pointed to possible downside risks stemming from a trade war. There was also a debate on rising rates from a low level that spurs growth to being a neutral or restraining factor for economic activity.

- BoJ Kuroda stressed his resolve to maintain the central bank's massive stimulus programme, even as he offered an optimistic view on prospects for meeting his 2% inflation target.

- The Bank of Korea kept its policy rate unchanged at 1.5%. Economic growth will be consistent with the path projected in January, but CPI for the year will be “slightly below” the 1.7% forecast.

- The Hong Kong dollar fell to a fresh 33-yr low, hitting the weakest end of the monetary authority's targeted trading band amid persistent downside pressure as the interest rate gap between USD and HKD widened further. (Reuters)

- House Speaker Ryan said he would retire at the end of the term, sparking an intraparty battle to succeed him and rattling Republicans who expect a fierce struggle to maintain their majority. (WSJ)

- Today's eco calendar contains EMU industrial production and US weekly jobless claims. ECB Coeuré, Weidmann and Fed Kashkari speak. The ECB publishes Minutes of its previous meeting. Italy and the US sell bonds.

Currencies: EUR/USD Rebound To Slow Post-Fed Minutes

EUR/USD rebound to slow post Fed Minutes?

The dollar initially traded with a negative bias yesterday, in line with the price pattern early this week. Geopolitical uncertainty (Syria)/risk-off weighed slightly on the dollar, rather than on the euro (or of course the yen). US CPI was as expected and had little impact on USD trading. EUR/USD trended higher in the 1.23 big figure. Later, the Fed Minutes acknowledged uncertainty from the China-US trade dispute, but the overall tone remained slightly hawkish. The dollar regained modest ground after the Minutes. EUR/USD closed the session little changed at 1.2367. USD/JPY finished the day at 106.79 (from 107.20).

Asian equities mostly show modest losses overnight as geopolitical uncertainty lingers Even so, dollar sentiment looks slightly less negative than earlier this week. (USD supported by modestly ‘hawkish' Fed minutes?). USD/JPY hovers in the high 106 area. EUR/USD is drifting off yesterday's ST peak, trading in the 1.2360 area.

EMU production data, US import prices and jobless claims are published today. ECB's Weidmann, Coeure and Fed's Kashkari speak. EMU data recently disappointed and this might also be the case for the EMU production data. US import price are expected to rise further (3.8% Y/Y from 3.5%). Jobless claims will probably ‘normalize' back lower after last week's uptick. In theory, today's data could be marginally USD supportive. Markets will also keep a close eye at ECB speakers in the wake of Nowotny's comments earlier this week. Geopolitics remain in play. Uncertainty was dollar negative earlier this week. However, we have to impression that the dollar might be slightly better supported in the wake of yesterday's Fed minutes. Especially, the rebound in EUR/USD looks like losing momentum. EUR/JPY also struggles to regain a first important resistance. EUR/USD drifted higher in the 1.2155/1.2550 range earlier this week,. Has this correction run its course?

UK data (production, construction output and NIESR GDP estimate) all surprised on the downside yesterday. This weighed temporary on sterling, but EUR/GBP basically holds in the low 0.87 area. Overnight the RICS house prices were slightly softer than expected, with no negative impact on sterling. Sterling showed quite resillent of late. However, for now we don't see a trigger to push EUR/GBP sustainably below the 0.8668/52 range bottom

EUR/USD rebound to slow?