Sample Category Title

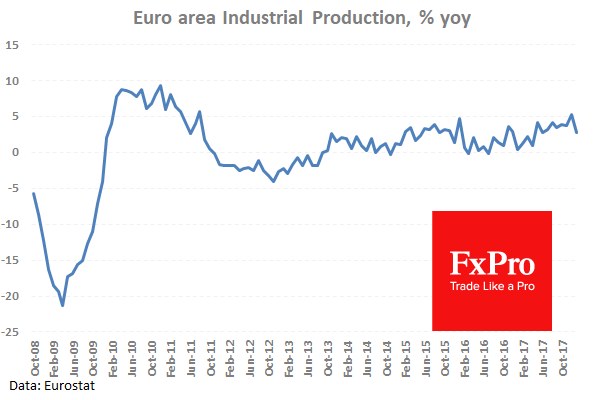

Eurozone Industrial Production Expected To Rebound From Last Month’s Decline

At 08:30 GMT, the BOE Credit Conditions Survey will be published. This is a survey of lenders which asks respondents to rate the level of credit conditions, including secured and unsecured loans to households, small businesses, non-financial corporations and non-bank firms. GBP pairs could move because of this data release.

At 09:00 GMT, Eurozone Industrial Production w.d.a. (YoY) (Feb) will be released with a consensus of 3.8% from a prior of 2.7%. Industrial Production s.a. (MoM) (Feb) is expected at 0.1% from -1.0% previously. The monthly figure dipped to -1.0% last month, with a further decline creating a headwind for the Eurozone economy. This data was compiled during the cold snap that gripped the continent so there is still hope for a rebound in the coming months. The EUR may be moved by this data.

At 11:30 GMT, the ECB Monetary Policy Meeting Accounts will be released. This is a detailed record of the ECB Governing Board’s most recent meeting, providing in-depth insights into the economic conditions that influenced their decision on where to set interest rates. EUR traders will pay attention to this release.

At 12:15 GMT, the ECB’s Coeure is due to deliver a scheduled speech. Comments made may result in movement in EUR crosses.

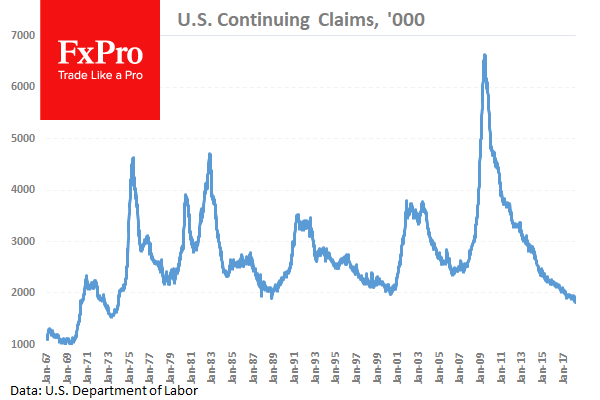

At 12:30 GMT, US Continuing Jobless Claims (Mar 30) is expected to be 1.848M against a previous 1.808M. Initial Jobless Claims (Apr 6) is expected to be 230K from 242K previously. The Initial Claims ticked up last week, with this week’s data expected to show a rise in continuing claims after a decade-low number was recorded. USD pairs could be moved by this data.

At 16:00 GMT, German BUBA President Weidmann is due to deliver a speech titled “A spirit of optimism in Europe – guidelines for a crisis-proof monetary union” at the Ludwig Erhard Lecture, in Berlin. Comments may cause moves in EUR pairs.

At 19:00 GMT, BOE Governor Carney is due to deliver closing remarks at the Public Policy Forum’s Canada growth summit, in Toronto. His comments may result in volatility in GBP crosses.

At 21:00 GMT, FOMC Member Kaskari is due to make a scheduled speech. Comments may affect USD pairs.

At 22:30 GMT, Business NZ PMI (Mar) will be released, with a previous reading of 53.4. This data has been declining since its December reading of 57.7. A reading above 50.0 indicates growth. NZD crosses may be moved by this data release.

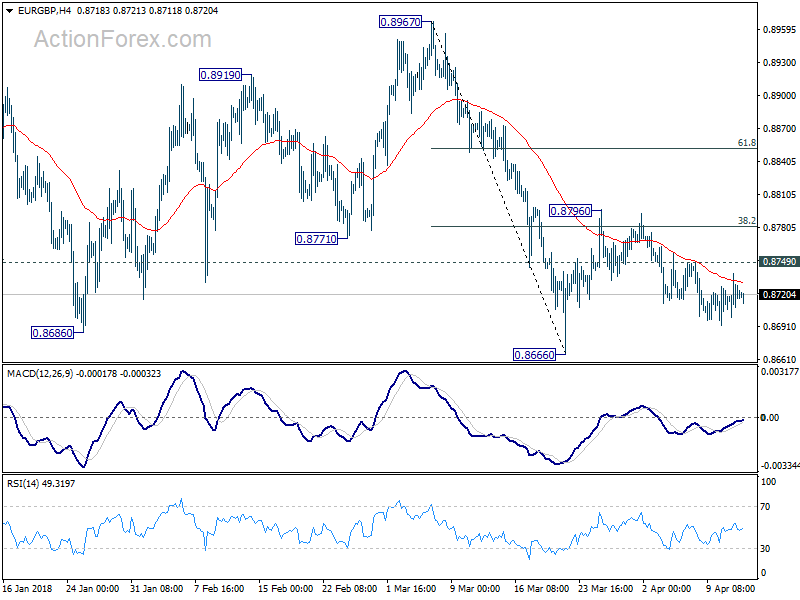

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8700; (P) 0.8719; (R1) 0.8741; More...

Intraday bias in EUR/GBP is neutral for now as it's lacking a direction. On the upside, above 0.8749 will reaffirm the strong support from 0.8686 and turn bias to the upside for 0.8796. Break there will target 61.8% retracement of 0.8967 to 0.8666 at 0.8852 and above. On the downside, decisive break of 0.8666 will resume whole fall from 0.9305. In that case, EUR/GBP should target 0.8303 key support next. On the upside, above 0.8749 will reaffirm the strong support from 0.8686 and turn bias to the upside for 0.8796. Break there will target 61.8% retracement of 0.8967 to 0.8666 at 0.8852 and above.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

ECB Monetary Policy Meeting Accounts To Be Released Today

The main economic event today will be the publication of the ECB Monetary Policy Meeting Accounts, which will give an insight into the thinking of the ECB on economic conditions that influence their decisions. The reaction to the data events over the past couple of months will be of particular interest.

Syria dominated headlines overnight, as Nato members prepare for strikes against the country. There were reports of British Subs moving to the Eastern Mediterranean and Italian fighter jets seen in the same area. Commercial airlines have ceased flights in the region, particularly to Lebanon, which is on the route from the Med to Syria that sub-launched cruise missiles would fly over. There was also a report that UK PM May would seek cabinet approval to strike.

Trade tensions between the US and China increased, as the Chinese Ministry of Commerce said that they would fight back without hesitation if the US escalates tariffs. They hope that the US will understand the world situation and not blindly walk down its own path. It said that US actions so far were typical trade protectionism and unilateralism. It said that China will carry out measures announced by President Xi in regard to opening up the country to trade and investment.

UK Industrial Production (YoY) (Feb) was 2.2% v an expected 2.9%, against a previous 1.6%, which was revised down to 1.2%. Industrial Production (MoM) (Feb) was 0.1% v an expected 0.4%, against 1.3% previously. Seasonally, there is generally a downturn in this figure, with a drop early in the New Year, something which can be seen in the February reading, with a strong rebound expected in March. As was the case last month, the reading came in lower than expected. The downward revision for the yearly figure is also a worry. Manufacturing Production (YoY) (Feb) was 2.5% v an expected 3.3%, against 2.7% previously, which was revised down to 2.2%. Manufacturing Production (MoM) (Feb) was -0.2% v an expected 0.2%, against 0.1% previously, which was revised down to 0.0%. This figure fell below the 0% level, matching the July number of -0.2%. Both monthly and yearly figures were revised down and the traders will await this data next time out to see if this downward trend accelerates. EURGBP moved higher from 0.87013 to 0.87243 because of this data release.

ECB President Draghi spoke at the Generation Euro Students’ Award Ceremony, in Frankfurt. Some of the comments made were: more integration allows the EU to face the economy’s challenges. The EU can’t solve its problems just at national levels. Wages and inflation will rise as the economy improves and there is confidence that inflation will rise to the ECB’s goal. The direct impact of the US trade tariffs announcement has not been big, the key issue is retaliation. The confidence effect of the trade spat can be very important.

US Consumer Price Index (YoY) (Mar) came in as expected at 2.4% against 2.2% previously. Consumer Price Index Ex-Food & Energy (YoY) (Mar) also came in as expected at 2.1% against 1.8% previously. Consumer Price Index Ex-Food & Energy (MoM) (Mar) was as expected, unchanged at 0.2%. Consumer Price Index (MoM) (Mar) came in at -0.1% v an expected reading of 0.0%, against 0.2% previously. Consumer Price Index Core s.a. (Mar) came in as expected at 256.200 against 255.751 previously. These data points will allow for an updated measure of the effect of inflation on consumers. Inflation is currently one of the main drivers of market sentiment in the US. The higher reading shocked the market in January but can be partly explained as an increase in demand for winter items due to the cold weather. This can be seen in the February number, which showed a correction which continued with the present release. Despite the fall in monthly data, the yearly data increased from last month. USDJPY found support at 106.677 and advanced higher from there to 106.956 due to this data.

The FOMC Minutes were released along with the US Monthly Budget Statement (Mar) which showed a balance of $-209B v an expected $-194B, against $-215B previously. The FOMC Minutes revealed that all the members expected 12-month inflation to rise in the next few months. Almost all agreed that gradual rate hikes were appropriate and the economic outlook had strengthened in recent months. A strong majority agreed that the prospect of retaliatory trade actions by other countries is a downside risk for the US economy. Despite expectations for rising YoY inflation, policymakers agreed that this alone would not justify a change in projected rate hike path. Many said the Fed funds rate will likely need to be above the normal long-term rate for a time. A few said future Fed statements might need to signal that policy will shift to being a neutral or restraining factor for the economy. The Fed sees a ‘significant’ fiscal policy growth boost over the next few years. Participants noted slow recent household spending and investment but expect it to be transitory, pointing to factors including delayed payment of personal tax refunds and residual seasonality in data. No one saw balance of risks to the downside for inflation.

EURUSD is down -0.10% overnight, trading around 1.23553.

USDJPY is up 0.13% in early session trading at around 106.920.

GBPUSD is up 0.03% this morning, trading around 1.41792.

Gold is down -0.17% in early morning trading at around $1,350.55.

WTI is up 0.34% this morning, trading around $66.93.

China MOFCOM Issues Strong Comments On Trade War

General Trend:

- Asian equities trade generally lower, in line with US trading

- Markets still waiting for next move by US regarding Syria

- Energy companies track advance in oil prices

- Japan retail earnings in focus: Aeon and Ryokin Keikaku gain after earnings and guidance, Lawson Inc declines

- Nikkei-weighed Fast Retailing scheduled to report earnings after the close

- PBoC Gov says Q1 data has been a bit better than expected ahead of GDP figures expected on April 17th

- China Commerce Ministry plays down recent comments from President Xi on trade

- Bank of Korea (BOK) votes unanimously to leave rates unchanged; 3-year bond yields decline

- RBNZ official says the central bank plans to start publishing accounts of policy meetings

- Hong Kong Monetary Authority (HKMA) declines to enter market, as HKD hits weak end of trading band

- Singapore Monetary Authority (central bank) expected to issue semiannual monetary policy statement and Q1 advance GDP data on Friday

- China Trade Balance is scheduled to be released April 12-13th; March bank lending data may be released later today

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.1%; closed -0.1%

- TOPIX Electric Appliances index -0.8%, Iron & Steel -0.6%, Securities -0.4%

- Takata, 7312.JP To be acquired by Joyson & Pag fund KSS for $1.59B in equity and debt; to be rebranded Joyson Safety Systems

- (JP) Bank of Japan (BOJ Gov Kuroda: Reiterates economy is expected to continue expanding moderately; CPI moving around 1%; affirms to maintain QQE with yield curve control for as long as needed to reach 2% inflation in stable manner

- Toshiba, 6502.JP Likely to miss deadline for China chip sale approval; planning to go ahead with sale to Bain

- (JP) BoJ Executive Dir Maeda: BOJ is moving steadily toward CPI goal; will continue monetary easing persistently, still distant from price target - Parliament

- (JP) Japan MoF sells ¥565B v ¥700B indicated in 0.8% (0.8% prior) 30-yr bonds; Avg yield: 0.714% v 0.75% prior; Bid to cover: 4.34x v 4.24x prior

- (JP) Japan govt said to be looking at new budget balancing goal by mid-2020 - financial press

- (JP) Bank of Japan (BOJ) Regional Report: Cuts assessment for 1 of 9 regions; Raises view in 2 of 9 regions

Korea

- Kospi opened +0.3%

- (KR) South Korea Finance Min Kim: Reiterates South Korea is NOT fx manipulator; spoke with US Treasury Sec Mnuchin over the phone regarding FX policy

- (KR) BANK OF KOREA (BOK) LEAVES 7-DAY REPO RATE UNCHANGED AT 1.50%; AS EXPECTED

- (KR) BOK Gov Lee: A stronger won could reduce room for policy rate increase; FX rate not the only factor for monetary policy

China/Hong Kong

- Hang Seng opened +0.6%, Shanghai Composite -0.2%

- Hang Seng Info Tech index -1%, Materials -0.8%, Services -0.7%, Property/Construction -0.5%, Financials -0.4%; Energy +2%

- (CN) China may raise Qualified Domestic Limited Partnership (QDLP) quota at the appropriate time - Chinese press

- (CN) China FX Regulator SAFE said to study Qualified Domestic Institutional Investor (QDII) reform

- HK$ touched key HK$7.85 level (low end of band) for the first time since band was implemented in 2005

- (HK) Hong Kong Monetary Authority Comments after HKD hit weak end of trading band: Has not been asked by a bank to purchase HKD at $7.85/USD

- (CN) China PBoC sets yuan reference rate at 6.2834 v 6.2911 prior

- (CN) China PBoC Open Market Operation (OMO): Skips reverse repo operations for 3rd consecutive day; Net: CNY20B drain v CNY20B drain prior

- (CN) PBoC Gov Yi Gang: Q1 data has been a bit better than expected; Belt-Road initiative needs to involve private and sustainable finance - PBOC-IMF Belt and Road Forum

- (CN) China YTD Foreign Direct Investment (FDI): CNY227.5B v CNY139.4B prior; y/y: +0.5% v 0.5% prior

- (CN) China MOFCOM's Gao: China's opening is not relevant to US/China trade spat, hope the US does not misjudge the situation. Not a matter of if China willing to negotiate with US, its about US not showing sincerity. US actions so far are typical trade protectionism unilateralism.

- Rusal, [+5.8%], 486.HK Russia ready to provide temporary liquidity to co if needed

- (CN) China said to be planning to raise fuel prices Friday; Gasoline by CNY55/ton; Diesel by CNY50/t - Chinese press

Australia/New Zealand

- ASX 200 opened +0.1%

- ASX 200 REIT index -0.7%, Financials -0.5%; Resources +0.7%, Consumer Discretionary +0.6%, Energy +0.3%

- (NZ) New Zealand Mar Card Spending Retail m/m: 1.0% v 0.5%e; Total m/m: 0.7% v 0.1% prior

- (NZ) New Zealand Govt bans oil exploration; effective immediately - NZ press

- (NZ) RBNZ Assistant Gov McDermott: Including employment into mandate will help flexibility of inflation targeting

- (AU) Australia Apr Consumer Inflation Expectation: 3.6% v 3.7% prior

- (AU) AUSTRALIA FEB HOME LOANS M/M: -0.2% V -0.4%E; INVESTMENT LENDING: 0.5% V 1.4% PRIOR

- (NZ) New Zealand sells NZ$200M in 2.75% 2025 bonds; avg yield 2.6218%; bid to cover 3.02x

Other Asia

- (SG) Singapore Feb Retail Sales M/M: -1.7% v +4.2%e; Y/Y: 8.6% v 4.9%e

North America

- US equity markets ended mostly lower: Dow -0.9%, S&P500 -0.6%, Nasdaq -0.4%, Russell 2000 +0.2%

- S&P500 Financials -1.2%, Health Care -0.8%; Energy +1%

- Costco [CSCO] March US SSS above ests

- (US) FOMC MINUTES FROM MAR 21 MEETING: ALL POLICYMAKERS SAID FURTHER TIGHTENING POLICY LIKELY WARRANTED, ALMOST ALL AGREED GRADUAL APPROACH IS APPROPRIATE

- (US) President Trump tweets " Russia vows to shoot down any and all missiles fired at Syria. Get ready Russia, because they will be coming, nice and new and “smart!” You shouldn’t be partners with a Gas Killing Animal who kills his people and enjoys it!"

- (US) White House Press Sec Sanders: there are a number of options remaining on the table over Syria attack; no final decisions have been made

- (US) TREASURY'S $21B 10-YEAR NOTE REOPENING DRAWS 2.795%; BID-TO-COVER RATIO: 2.46 V 2.50 PRIOR AND 2.48 OVER THE LAST 8

- (US) DOE CRUDE: +3.3M V -0.5ME

- (SY) Bashar Aide: Syria does not fear strike threats by US

- (RU) Russia said to be expecting info on US Syria targets; Russia said to be getting countermeasures on Syria - Russian press

- (MX) Moody's raises Mexico sovereign outlook to stable from negative; Affirms A3 rating

Europe

- (DE) Germany said to advocate ECB place tougher bad loan standards on banks – press

- (IT) Italy Northern League leader Salvini (euro-skeptic) reportedly may be asked to form a govt next week - press

- (IE) Ireland Central Bank makes 'small' upward revisions to 2018 and 2019 GDP growth forecasts - Quarterly Bulletin

- (UK) Mar RICS House Price Balance: 0% v 2%e (ties the lowest since Feb 2013)

- (UK) British Chambers of Commerce (BCC): Domestic demand remains muted, growth being driven by global environment - Quarterly Economic Survey

- Shire [SHP.UK] Takeda Pharam said to be shopping for several trillion yen in loans from banks to acquire Shire - Japan press

- First Group [FGP.UK]: Rejected takeover approach from private equity firm Apollo

- Carrefour [CA.FR]: Reports Q1 Rev €20.8B v €20.9Be

Levels as of 02:00ET

- Hang Seng -0.2%; Shanghai Composite -0.4%; Kospi +0.2%; ASX 200 -0.3%

- Equity Futures: S&P500 +0.2%; Nasdaq100 +0.3%, Dax +0.1%; FTSE100 +0.1%

- EUR 1.2379-1.2356; JPY 106.97-106.70; AUD 0.7772-0.7745;NZD 0.7376-0.7354

- Jun Gold -0.5% at $1,353/oz; May Crude Oil +0.4% at $67.06/brl; May Copper -0.8% at $3.09/lb

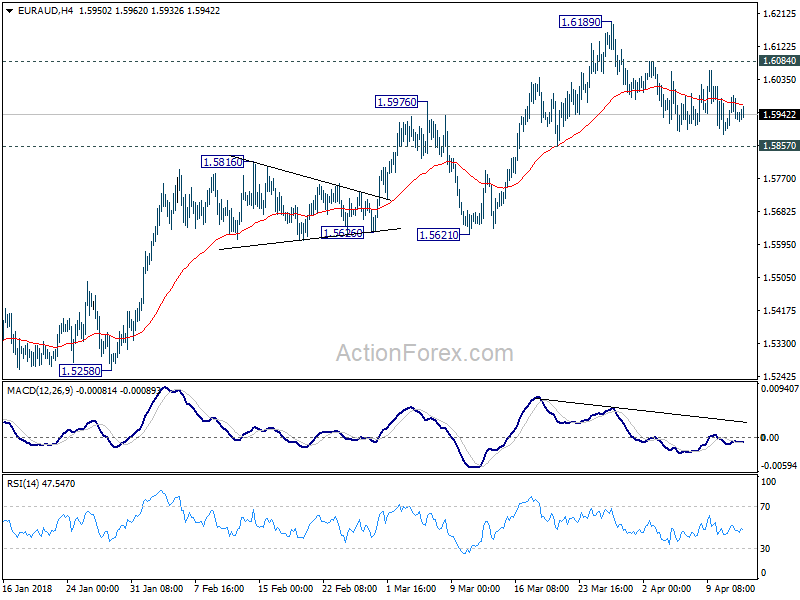

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5899; (P) 1.5947; (R1) 1.5988; More....

Intraday bias in EUR/AUD remains neutral as sideway trading continues, in range of 1.1.5852/6084. As long as 1.5857 minor support holds, further rally is expected in the cross. On the upside, above 1.6084 minor resistance will turn bias to the upside for retesting 1.6189 first. Break will resume larger rally towards 1.6587 key resistance. However, break of 1.5857 will be an early sign of trend reversal and turn bias to the downside for 1.5621 support to confirm.

In the bigger picture,rise from 1.3624 is not completed yet. And it's still in progress for 1.6587 key resistance level. We'd be cautious on strong resistance from there to limit upside, on bearish divergence condition in daily MACD. But for now, break of 1.5621 support is needed to be the first sign of medium term reversal. Otherwise, outlook will stays bullish even in case of deep pull back.

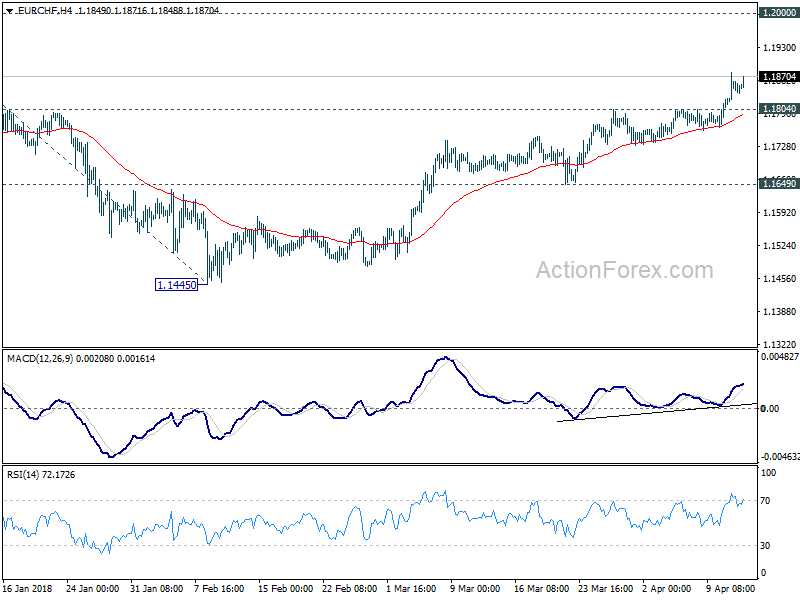

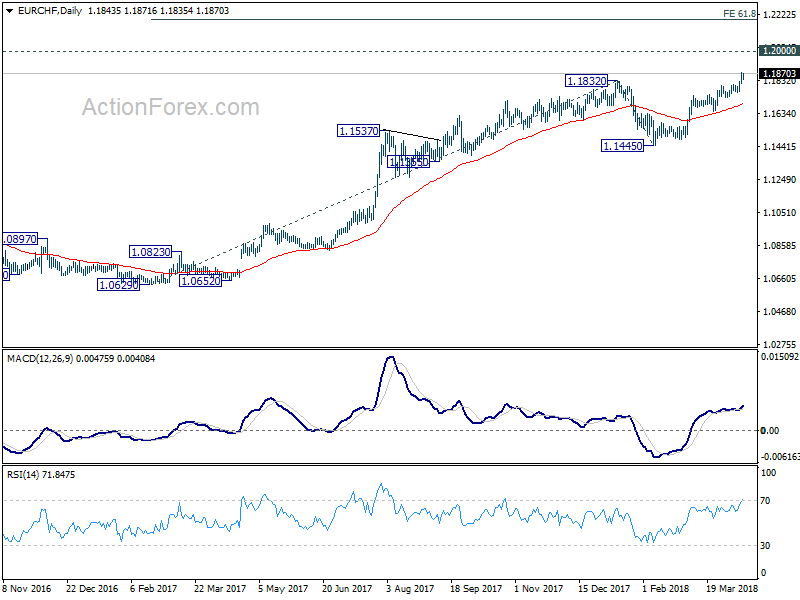

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1810; (P) 1.1845; (R1) 1.1878; More...

Intraday bias in EUR/CHF remains on the upside for the moment. Medium term up trend has just resumed and further rise should be seen to 1.2 handle first. Break will target 61.8% projection of 1.0629 to 1.1832 from 1.1445 at 1.2188 next. On the downside, below 1.1804 minor support will turn intraday bias neutral first. But retreat should be contained well above 1.1649 support to bring another rise.

In the bigger picture, decisive break of 1.1832 should now extend the medium term up trend through prior SNB imposed floor at 1.2000. 2013 high at 1.2649should be the next target. Outlook will remain bullish as long as 1.1445 support holds, even in case of deep pull back.

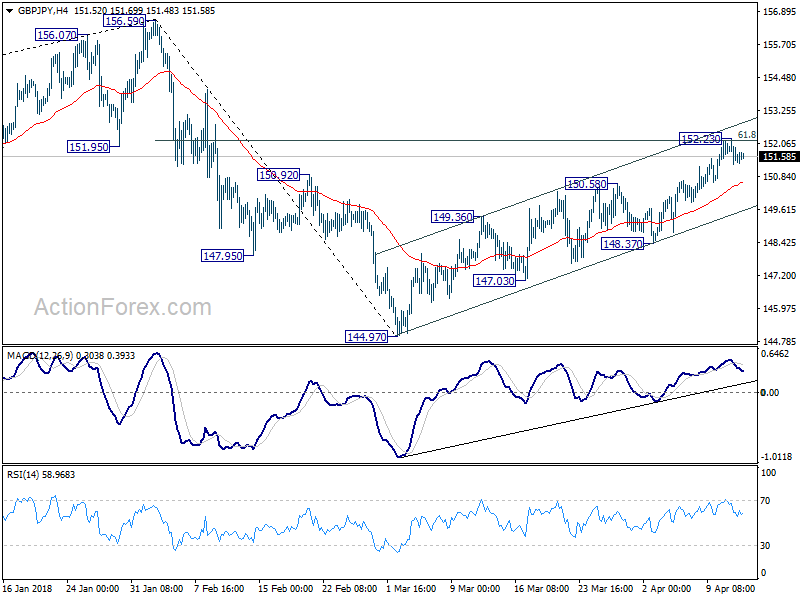

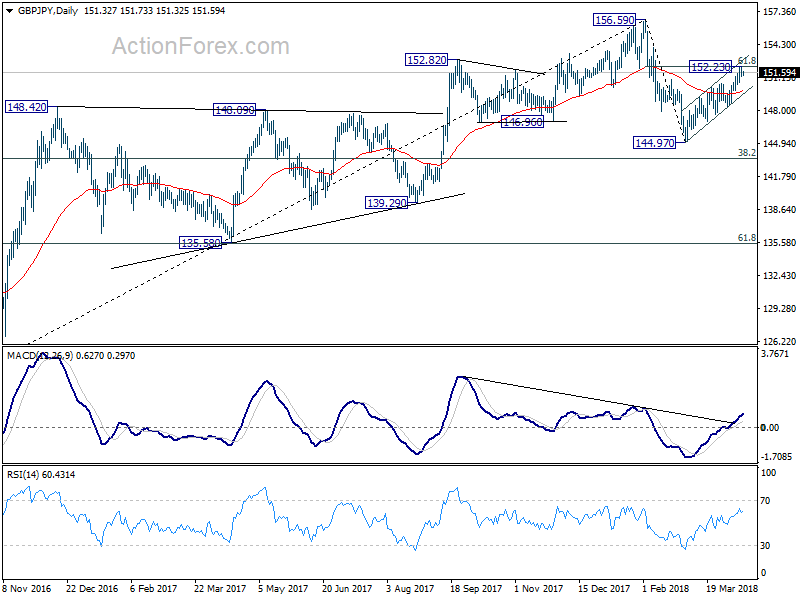

GBP/JPY Daily Outlook

Daily Pivots: (S1) 151.06; (P) 151.59; (R1) 152.49; More...

GBP/JPY lost upside momentum after meeting 61.8% retracement of 156.59 to 144.97 at 152.15. A temporary top is in place at 152.23 and intraday bias is turned neutral. Another rise is in favor as long as 148.37 minor support holds. But again, price actions from 144.97 are still seen as corrective looking. Hence, we'll look for sign of loss of upside momentum as it approaches 156.59 high. Meanwhile, break of 148.37 will indicate completion of the rebound from 144.97 and bring retest of this low.

In the bigger picture, the outlook is turning mixed again. On the one hand, the cross was rejected by 55 month EMA (now at 154.20) after breaching it briefing. On the other hand, there was no sustainable selling pushing it through 38.2% retracement of 122.36 to 156.59 at 143.51. The most likely scenario is that GBP/JPY is turning into a sideway pattern between 143.51 and 156.59. And more range trading would now be seen before a breakout, possibly on the upside.

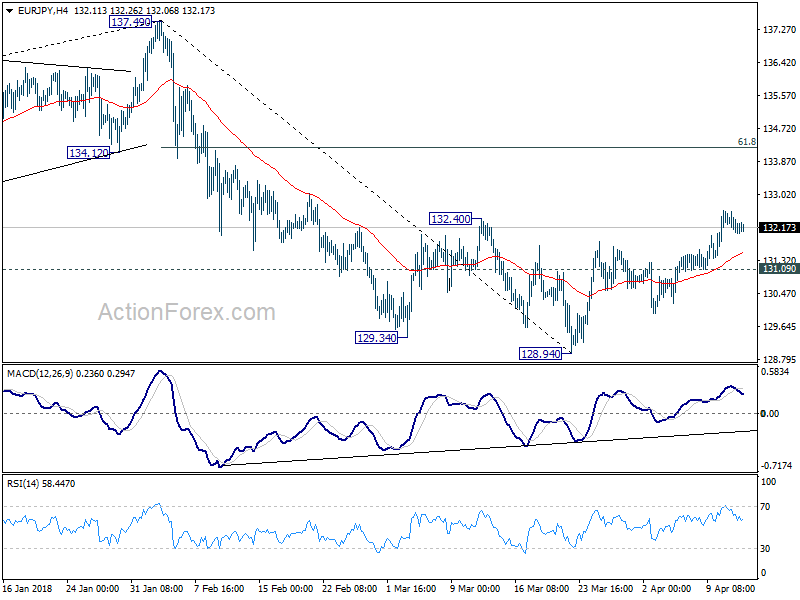

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.86; (P) 132.23; (R1) 132.44; More....

EUR/JPY reaches as high as 132.61 but lost momentum since then. For now, further rally is in favor as long as 131.09 minor support holds. Rebound from 128.94 would extend to 61.8% retracement of 137.49 to 128.94 at 134.22 and above. However, break of 131.09 will indicate completion of the rebound and bring retest of 128.94 low instead.

In the bigger picture, price action from 137.49 medium term top are developing into a corrective pattern. Strong support from 55 EMA (now at 129.91) suggests that the first leg has completed at 128.94 already. Nonetheless, break of 137.49 is needed to confirm resumption of the rise from 109.03 (2016 low). Otherwise, we'd expect more corrective range trading another, with risk of another fall to 38.2% retracement of 109.03 to 137.49 at 126.61 before completion.

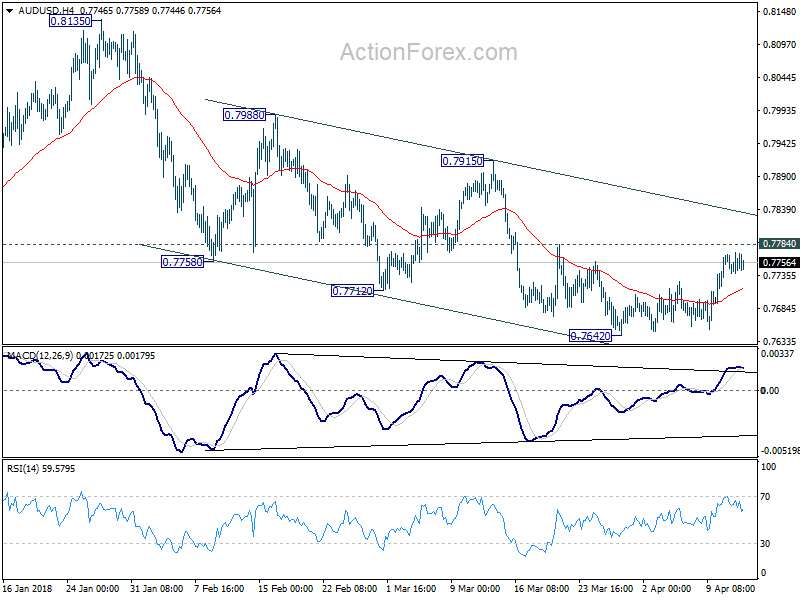

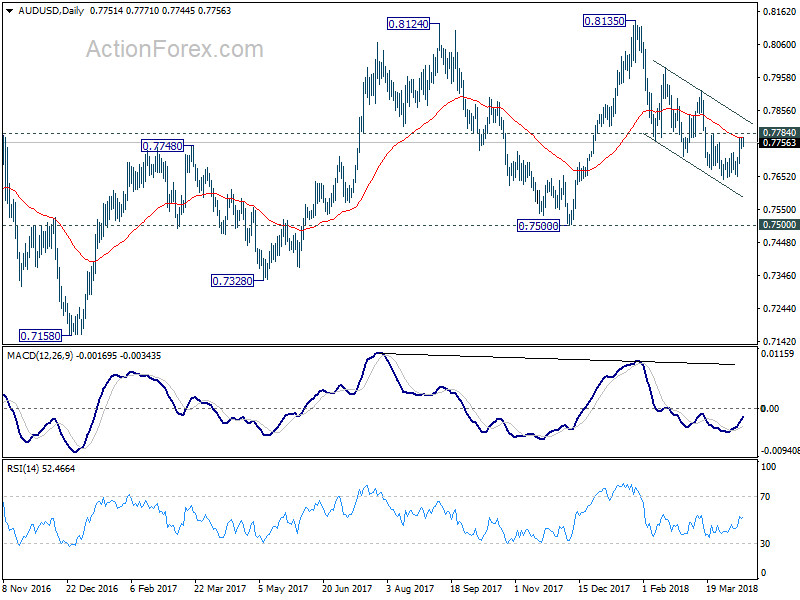

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7739; (P) 0.7755; (R1) 0.7772; More...

At this point, AUD/USD is still bounded in range of 0.7642/7784. Intraday bias remains neutral first. Also, with 0.7784 minor resistance intact, deeper fall is in favor. On the downside, break of 0.7642 will resume the decline from 0.8135 to retest 0.7500 key support level. On the upside, however, firm break of 0.7784 will suggest near term reversal and turn bias to the upside for 0.7915 resistance first.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

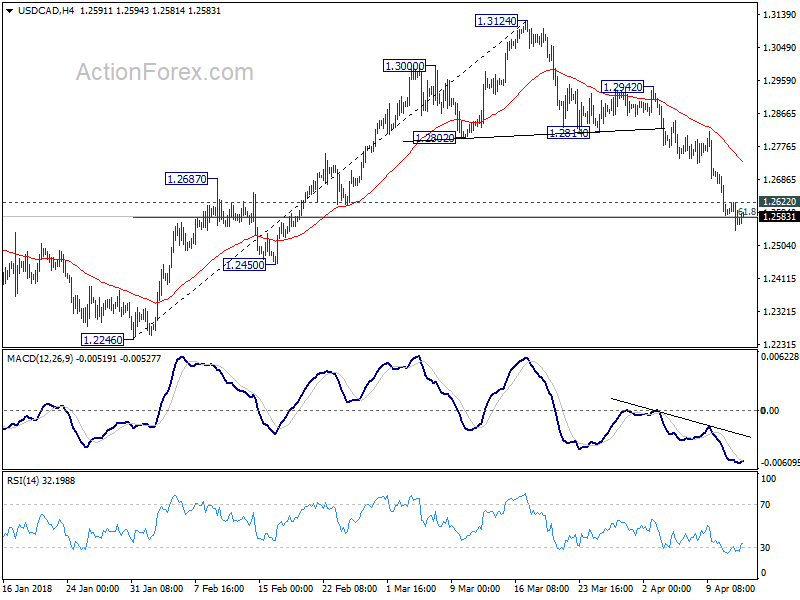

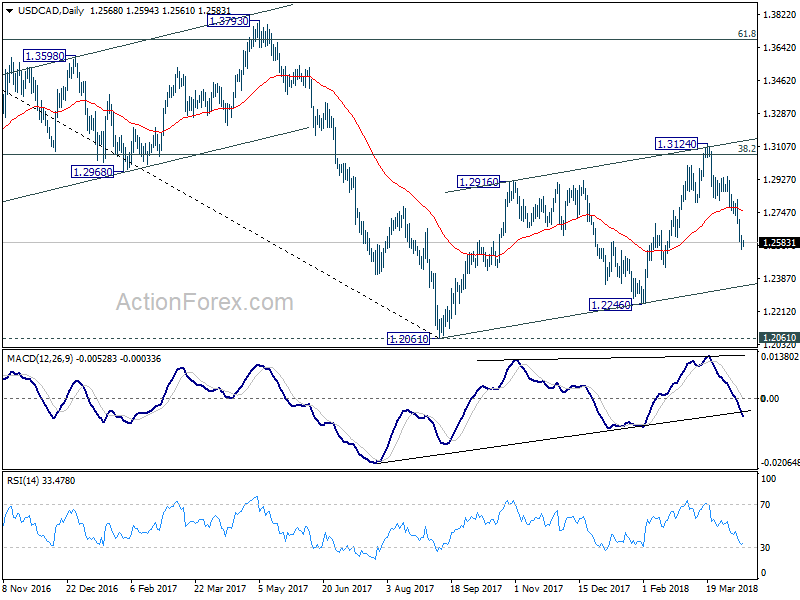

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2540; (P) 1.2581; (R1) 1.2619; More....

USD/CAD lost some downside momentum as it's pressing 61.8% retracement of 1.2246 to 1.3124 at 1.2581. But intraday bias stays on the downside as long as 1.2622 minor support holds. Sustained break of 1.2581 will pave the way to 1.2061/2246 support zone. On the upside, above 1.2622 will turn intraday bias neutral and bring recovery. But upside should be limited below 1.2814 support turned resistance and bring another fall.

In the bigger picture, current development turns favors to the case that rise from 1.2061 is a corrective three wave pattern. It could have completed at 1.3124 after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Focus is now back on 1.2061 and 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Decisive break there will resume larger down trend from 1.4689 (2016 high) to 61.8% retracement of 0.9406 to 1.4689 at 1.1424.