Sample Category Title

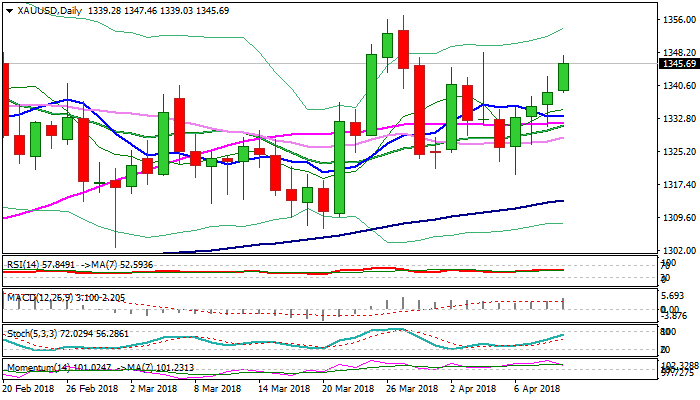

XAUUSD – Bulls Remain Firmly In Play On Geopolitical / Trade Tension

Gold price continues to trend higher and extends advance into fourth straight day on Wednesday, driven by rising safe-haven demand on geopolitical concerns and continuous trade tensions between the US and China.

The yellow metal gained around 1% on rally from last week’s spike low at $1319, as fresh bullish acceleration today broke through pivotal $1342 barrier (Fibo 61.8% of $1356/$1319 bear-leg) and pressuring next barrier at $1348 (Fibo 76.4% / 04 Apr spike high and strong upside rejection).

Bullish setup of daily techs maintains support but geopolitical factor is expected to be the key driver.

US CPI data and FOMC minutes are also eyed for fresh signals about Fed’s next steps.

Broken Fibo 61.8% marks solid support at $1342, which is expected to keep the downside protected.

Res: 1348, 1356, 1361, 1366

Sup: 1342, 1339, 1333, 1331

Euro Edges Higher, Markets Eye US Inflation, Fed Minutes

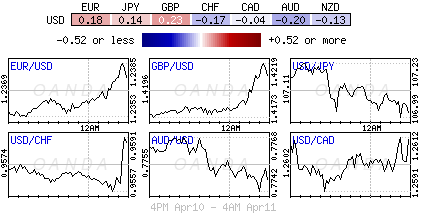

EUR/USD continues to post slow but steady gains. In the Wednesday session, the pair is trading at 1.2384, up 0.22% on the day. On the release front, there are no major German or eurozone events this week. ECB President Mario Draghi will speak at an event in Frankfurt. In the US, today’s highlight is consumer inflation. CPI is expected to dip to 0.0%, and Core CPI is forecast to remain at 0.2%. As well, the FOMC releases the minutes of its March rate meeting. On Thursday, the ECB releases the minutes of its March rate meeting and the US publishes unemployment claims.

The markets are keeping a close eye on Wednesday’s key releases – CPI and the FOMC minutes. Both events could provide clues regarding the Federal Reserve’s monetary policy for 2018. Will the Fed press the rate trigger three times this year, or four? The current Fed forecast calls for three rate hikes, but this could be revised upwards if inflation rises. If the FOMC minutes point to a hawkish stance from policymakers, the US dollar could respond with gains.

The tariff spat between the US and China appears far from over, but both sides have lowered the flames which ahs roiled the markets in recent weeks. Investors are breathing a sigh of relief after Chinese President Xi Jimping sent out a conciliatory message on Tuesday. Xi was speaking at a development conference in China, and promised to lower tariffs on vehicle imports into China. This has been a major sticking point between the US and China, with President Trump complaining that China has a 25% tariff on US vehicle imports, yet the US only charges 2.5% on Chinese vehicles. Xi added that China was looking to solve issues through dialogue rather than confrontation, and the markets are hoping that the US and China can avert a trade war, which could drag down the global economy.

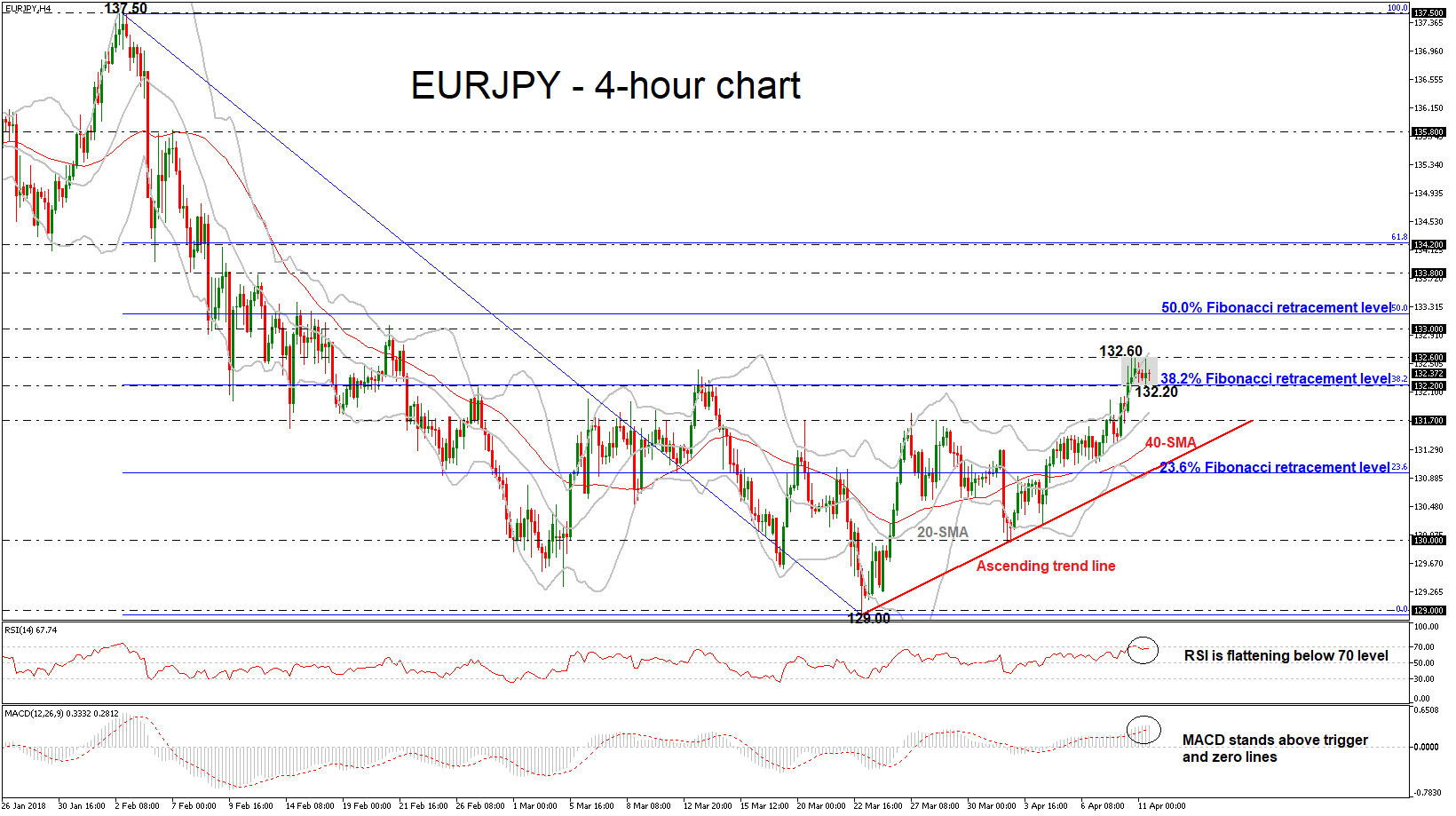

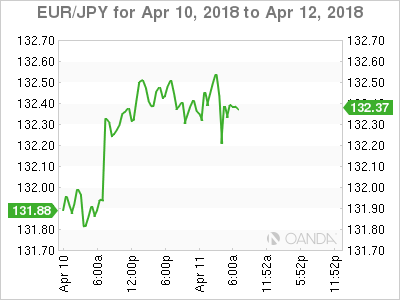

EURJPY Creates Weak Sessions Within Narrow Range Between 132.20 – 132.60

EURJPY reached a 7-week high of 132.60 during Tuesday’s trading session as the pair extended its bullish rally for the second day in a row. In the short-term, prices are capped by the 132.60 resistance level and the upper Bollinger Band. In addition, the 38.2% Fibonacci retracement level of 132.50 of the downleg from 137.50 to 129.00 acts as strong support barrier for the price.

In the 4-hour chart, momentum indicators seem to be in confusion. The RSI indicator is flattening slightly below the overbought level, while the MACD oscillator stands above its trigger and zero lines but with weak momentum.

Should prices reverse lower, immediate support should come at 132.20. A successful close below the aforementioned obstacle would take the pair closer to the 131.70 support level and towards the ascending two-week trend line. In case of a slip below the diagonal line would reinforce the bearish structure again and re-challenge the 23.6% Fibonacci near 131.00, which coincides with the lower Bollinger band.

To the upside, there is immediate resistance at 132.60, while above that, the next major resistance to watch is at 133.00. A break above this zone could push EURJPY until the 50.0% Fibonacci mark of 133.20.

Syria Risks Offset Trade Truce

Wednesday April 11: Five things the markets are talking about

Ahead of the U.S open, Euro equities are under pressure following a mixed Asian session as capital markets weigh easing global trade tensions against the prospect of Euro/U.S military action in Syria.

The ‘big’ dollar continues to drift, while U.S debt prices edge a tad higher before this morning’s U.S inflation data and this afternoon’s FOMC (02:00 pm EDT) minutes.

Stateside, inflation pressures appear to be building according to yesterday’s producer-price report, a trend that could also be visible in today’s U.S consumer-price data (08:30 am EDT).

U.S PPI rose +3% last month from a year earlier, matching the largest increase since prices grew +3% last November. Ex-food and energy, the volatile trade services category grew +2.9%, the strongest y/y increase in nearly four-years.

The markets focus has now officially shifted towards geopolitical stress around Syria.

1. Stocks mixed session

In Japan, stocks fell for the first time in three-days overnight, following a strong rally Tuesday, but index-heavy SoftBank rose on rumours that Sprint is in new talks to merge with T-Mobile. The Nikkei ended -0.5% lower, while the broader Topix declined -0.4%.

Down-under, Aussie shares ended lower overnight as investors switched from the defensive sector to resource plays on strength in commodities after China spoke of further opening their economy and lowering tariffs. The S&P/ASX 200 index slipped -0.5%. In S. Korea, the Kospi was -0.2% lower.

Shares in China and Hong Kong posted the biggest gains as PBoC Governor Yi Gang offered more details on pledges to open the Chinese economy. In Hong Kong, equities rallied for a fourth consecutive session. The Hang Seng index rose +0.6%, while the China Enterprises Index was unchanged. In China, stocks also ended higher. The blue-chip CSI300 index rose +0.3%, while the Shanghai Composite Index gained +0.6%.

In Europe, regional bourses are trading mostly lower across the board, consolidating some of their recent gains and tracking U.S futures lower following yesterday’s strong session.

U.S stocks are set to open in the ‘red’ (-0.5%).

Indices: Stoxx600 -0.2% at 377.6, FTSE -0.1% at 7261, DAX -0.3% at 12359, CAC-40 -0.3% at 5294, IBEX-35 +0.1% at 9777, FTSE MIB flat at 23182, SMI -0.2% at 8736, S&P 500 Futures -0.5%

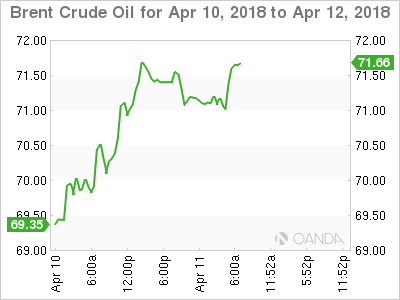

2. Oil hovers atop of 2014 peak as geopolitics vie with supply, gold higher

Oil prices trade atop of their four-year highs, supported by geopolitical tension in the Middle East, although higher U.S inventory reports are capping price gains.

Brent crude has gained +5.7% this week, rising to +$71.34 a barrel on Tuesday, although the price has since fallen back and was +$70.98 a barrel, down -6c. U.S crude futures are at +$65.55 a barrel, up +4c.

The U.S and its Euro allies are considering air strikes against Syrian forces following a suspected poison gas attack last weekend.

Note: Syria is not a significant oil producer, but any sign of conflict in the region would trigger concern about potential disruption to crude flows across out of the Middle East.

Earlier today, the Saudi energy Minister Khalid al-Falih said his country would “not sit by and let another supply glut surface,” implying that the OPEC would continue to withhold supply.

Capping price are U.S inventory reports. Yesterday’s U.S API data showed that crude inventories rose by +1.8m barrels in the week to April 6 to +429.1m, compared with market expectations for a decrease of -189k barrels.

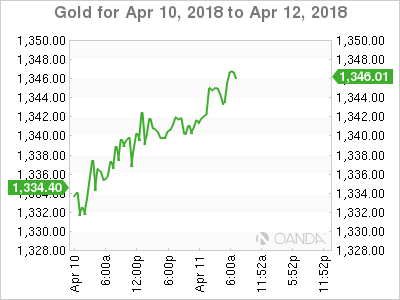

Ahead of the U.S open, gold prices have touched a one-week high, as the dollar falls to a two-week low and as a host of geopolitical factors stoked demand for the safe-haven metal. Spot gold has rallied + 0.4% to +$1,344.16 an ounce, its fourth straight session of gains. U.S gold futures have gained +0.2% at +$1,348 an ounce.

3. E.U yields drop as ECB plays down Nowotny’s comments

E.U sovereign yields eased back towards their multi-month lows after the ECB distanced itself from one Nowotny’s comments of a move away from deeply negative deposit rates yesterday.

Note: Nowotny indicated yesterday that there was a possibility of a +20 bps hike in the deposit rate as part of ECB’s efforts to normalise policy.

The yield on Germany’s 10-year Bund is -1 bps lower at +0.505% while other sovereign yields across the bloc saw yields drop -1 to -2 bps.

Elsewhere, the yield on U.S 10-year Treasuries dipped -1 bps to +2.79%, while in the U.K, the 10-year Gilt yield decreased -1 bps to +1.402%.

4. Dollar feels the pressure

The USD remains on soft footing, somewhat pressured by a number of Euro central bankers commenting on their future rate outlook.

Bank of England’s (BoE) McCafferty (dissenter) noted the U.K policy makers should not delay its next rate hike, while European Central Bank’s (ECB) Nowotny stated, “a good place to start on its normalization would be a +20 bps hike in the discount rate.”

EUR/USD (€1.2374) is making an attempt to penetrate the psychological € 1.24 handle despite the ECB playing down Nowotny hike comments.

EUR/CHF (€1.1853) has crossed its highest level since the Swiss National Bank (SNB) removed the $1.20 floor back in January 2015.

Sterling (£1.4195) fell slightly on this morning’s IP news (see below), given that further data showed the U.K trade deficit shrank to £10.2B in February. EUR/GBP has rallied to €0.8718.

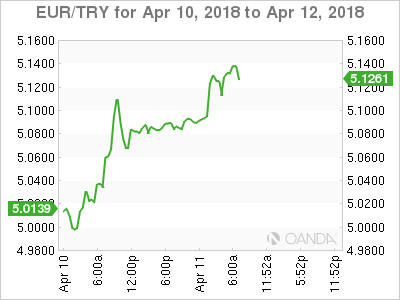

Russia’s rouble (RUB) extended it recent losses to hit its weakest since November 2016 as selling continued in the wake of new U.S. sanctions and as geopolitical tensions over Syria rose, with Turkey’s lira (TRY) also falling another record low atop of $4.1502).

5. U.K factory output fell in February

Data this morning showed that U.K. factory output declined in February, the latest sign the U.K economy slowed in Q1.

Manufacturing output fell -0.2%, though overall industrial production recorded a +0.1% gain, thanks largely to higher energy generation as U.K citizens consumed more energy during this past winter’s deep cold snap.

Market expectations were for the U.K to lag its peers for a second consecutive year as uncertainty over the country’s future ties to the E.U weigh on activity.

Bitcoin: Back In Green But Not Cream (The Cream Of The Crop)

There is an optimism in the market

Cryptos still recovering from the recent sell-off

China's state electricity firm eyes blockchain

Bitcoin back in green, but still below the key of $7000. It has been a win for the cryptos yesterday. Bitcoin rose from 6.7k to 6.8k, whilst Ethereum rose from 396 to around 410. Ethereum's 200 MA matched with its 50 MA, hitting the death cross, which normally ends up with huge selling off. However, the cross symbolized more about the selling-off reaching a lifespan of 3 months, rather than indicating future sell-offs. The huge slide from all-time highs supports this argument.

There is an optimism in the market as Gemini rolled out Bitcoin and Ether Block Trading, allowing institutional investors to place large trades without driving the prices of cryptos up and down, significantly reducing the possible volatility (a deterrent to small traders), in the market. Confidence in cryptos increase. Such news matched with the Intercontinental Exchange's decision to not rule out crypto futures launch, saying that different products could be on the table one day. Once again, showing optimism over crypto-products - a boost to the crypto-space. The combination of these news sent cryptos soaring.

As the market was still recovering from the recent sell-off, it appeared that the sell-off, by no means, showed a lack of enthusiasm amongst the public. Argentina's Bitcoin Day was matched with support and participation, proving that the country is one of the leading forces in the technology, showing at the same time how countries and their people haven't given up on cryptos. This is a boost to the cryptos.

In China, more positive news are coming out, turning the tide. China's state electricity firm eyes blockchain for its Internet of Energy plan, following China's 1billion-funded blockchain launch yesterday. The tide is turning, and cryptos get a massive boost from China's support. Again, sending prices higher.

Negativity is also present in today's market, but didn't stop the cryptos from rising. Ledger Wallet users can't access their bitcoin cash. Such news matches with previous news related to crypto exchanges, where investors find it hard to get back their holdings and gains, showing despite confidence in the community, small investors will find it hard to actually invest in it. The pessimism, however, was completely counteracted my general positivity today

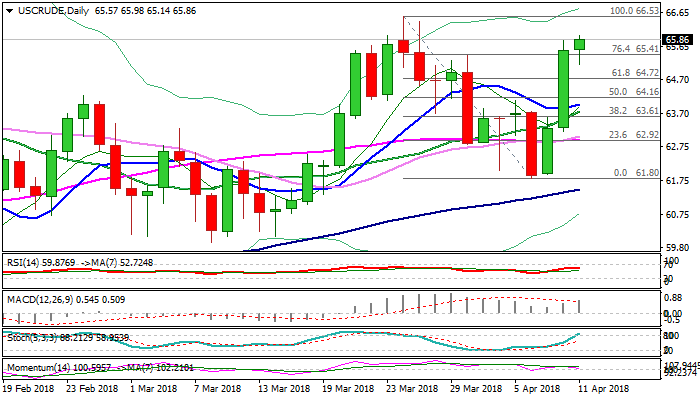

WTI OIL Maintains Firm Bull Tone Ahead Of EIA Report / US CPI Data

Oil price regained traction and hit new marginally higher two-week high at $65.89 on Wednesday, after brief pullback found footstep at $65.14.

Oil price surged on Monday and Tuesday, gaining nearly 6%, on rally from $61.80 through which threatens to fully retrace $66.53/$61.80 pullback.

WTI rose on weaker dollar and geopolitical tensions in the Middle East, as well as concerns about trade war between US and China.

Much stronger than expected build of crude stocks (API report showed build of 1.75 million barrels vs 0.100 million barrels forecast and 3.2 million barrels draw of last week) did not show stronger impact on oil bulls.

Daily techs in bullish setup continue to underpin, however, weaker momentum and overbought slow stochastic warn of hesitation on approach to key barrier at $66.53 (26 Mar peak).

Oil price remains supported by geopolitical tensions over Syria and signals that the US could renew sanctions against Iran, which could further complicate the situation and boost oil price.

EIA weekly crude stocks report and US CPI data are in focus today. Crude inventories are forecasted for a minor draw of 0.18 million barrels, compared to last week's strong 4.61 million barrels draw.

indicate oil's near-term direction.

Psychological $65 level marks initial support, followed by more significant $64.29 support (top of 4-hr cloud) which should contain stronger dips and keep bulls intact.

Res: 66.00, 66.28, 66.53, 66.64

Sup: 65.14, 65.00, 64.72, 64.29

GBPUSD Still Bullish Despite More Weak UK Data

The British pound has moved to a fresh monthly trading high against the greenback, with price-action breaking above the key 1.4200 level, hitting 1.4222, during the European trading session. The GBPUSD pair currently trades around the 1.4190 level, after pulling back on weaker than expected Manufacturing and Industrial production data from the UK economy. Sterling traders now look towards the release of U.S CPI data, with the pairs strong bullish momentum intact while price-holds above the 1.4187 level.

The GBPUSD pair retains a strong bullish bias while price-action trades above the 1.4187 level, key resistance is currently located at the 1.4243 and 1.4300 levels.

Should the GBPUSD pair move below the 1.4187 level, price-action may correct back towards the 1.4146 and 1.4116 levels.

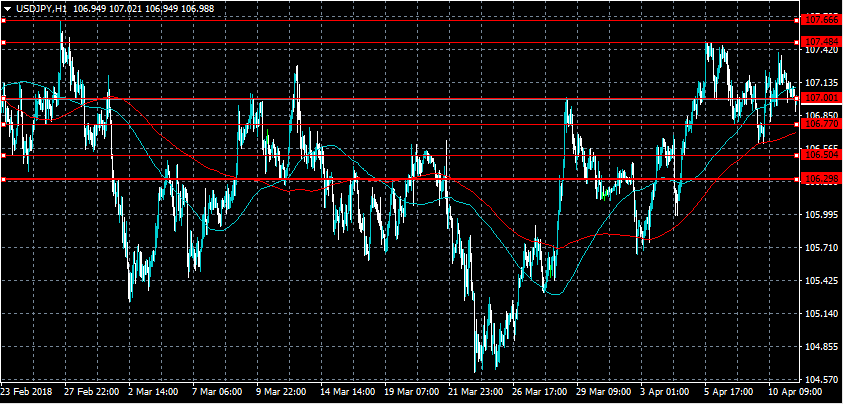

USDJPY Likely To Break Range After U.S CPI Data

The U.S dollar continues to consolidate around the 107.00 handle against the Japanese yen, as traders await key CPI inflation data from the United States economy. The USDJPY pair retains its intraday bullish bias while trading above the 106.77 level, with traders now looking for a definitive range-break this afternoon. A better than expected U.S CPI number will likely cause the U.S dollar to firm, as traders price-in more rate hikes from the Federal Reserve.

The USDJPY pair retains its intraday bullish bias while trading above the 106.77 level, key resistance is found at the 107.66 and 108.10 levels.

If the USDJPY pair moves below the 106.77 level, sellers will likely attempt to test the 106.50 and 106.30 support levels.

CRUDE OIL Profit Taking

Crude oil recovery phase stops after breaking hourly resistance at 64.67 (30/01/2018) and reaching 65.86. Heading along the 65.15 range. The bullish pattern started in November 2017 is somewhat weakened since recent decline started at the end of March. Crude oil is contained between hourly support and resistance at 61.34 (08/01/2018 low) and 66.66 (25/01/2018 high). The technical structure suggests short-term decrease.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading above its 200 DMA.

SILVER Selling Pressures

Silver is weakening following recent rise at 16.64, heading along the 16.54 range. Silver is contained between hourly support and resistance given at 16.03 (18/12/2017 low) and 16.98 (15/02/2018 high). The short-term technical structure suggests short-term downward moves.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. The pair is trading below its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).