Sample Category Title

EUR/USD: US Producer Price Index

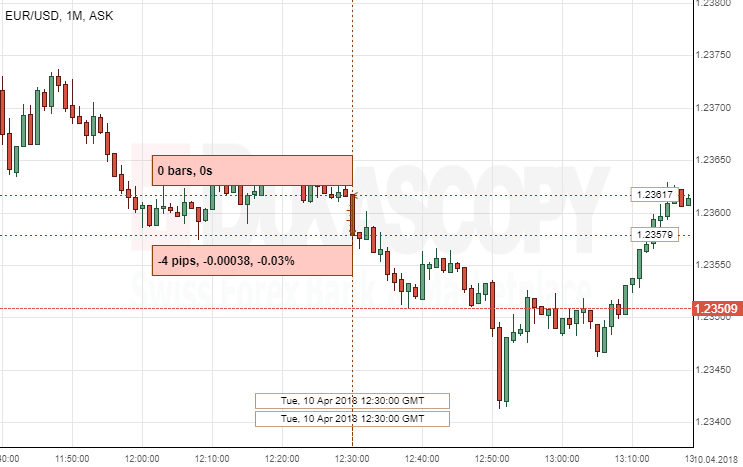

The Greenback strengthened against the Eurozone's single currency, following the US producer price index data on Tuesday. The EUR/USD currency lost only four pips, or 0.03%, to continue fluctuating in the 1.2359 area.

The Bureau of Labor Statistics revealed better-than-expected data in producer price index in March. It was mainly led by the increase in costs of an airline and healthcare services, pointing out to the wholesale inflation pressures. Economists give their opinion about inflation being pushed towards the Fed's two percent target at the end of this year in a form of the weak dollar, tight labor market and fiscal stimulus.

CAD/JPY 4H Chart: Bullish Sentiment

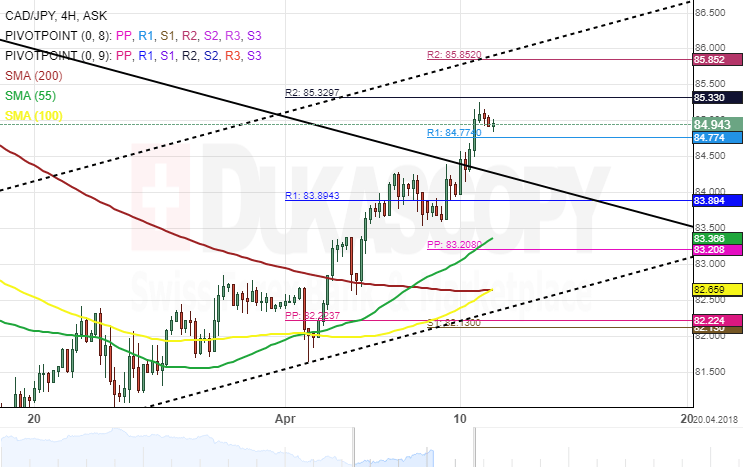

The Canadian Dollar has been trading in a dominant descending channel against the Japanese Yen since early January. The currency pair smooth journey in this pattern was interrupted in March when a reverse north occurred after hitting a support cluster set by the combination of the weekly and the monthly PPs near the 80.78 area.

The CAD/JPY exchange rate has since been moving in a junior ascending channel. Meanwhile, a breakout has occurred through the upper boundary of the dominant channel.

The overall market sentiment is bullish; therefore, the currency exchange rate is likely to continue moving north during the following trading sessions.

EUR/AUD 4H Chart: Possible Reverse To The Upside

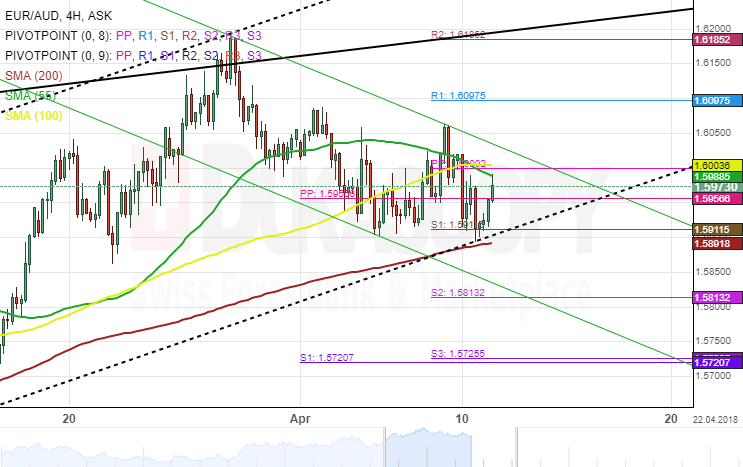

After reaching the monthly pivot point at 1.5151 on early January, the single European currency began appreciating against the Australian Dollar. The movement has been steered by a junior ascending channel. The most recent test of its lower boundary was April 10.

The EUR/AUD currency pair was being supported by the 200– hour simple moving average at 1.5891, and the Euro was able to breach the monthly PP at the 1.5956 mark.

On the four hour time-frame, technical indicators suggest a sell signal, while on the weekly time-frame, its advice to go long. By and large, it is likely the currency exchange rate could move upward during this week until it breaches the up border of the junior pattern.

Forex Analysis: EURCAD And Silver

The EURCAD pair has fallen back under the red supporting trend line, leading to a down move to the 1.55500 support area. The low reached 1.55458 but there is support close by at 1.55325. Price action is now back to the 1.56000 level. Resistance comes in the form of the 50 DMA at 1.56860, with the 1.58134 level an important low from late March. An upward move through this area targets the red ascending trend line at 1.59617, followed by the 1.60000 level and the high for 2018 at 1.61490.

Support at the 100 DMA is found at 1.54876, with the 1.53712 level of resistance from late 2017 coming in as support, which was tested in February. The 200 DMA was used in early January as support and there is no reason to think that it won’t be used again if price drops that far. A loss of this area can see a determined sell-off target the 1.50000 area, followed by 1.47365 and 1.45000.

Silver

The metal has formed an unusual but common enough double trend line pattern over the last few weeks. The most recent touch on the lower of the two blue trend lines was earlier today, with the area representing strong resistance around 16.650. A break above here targets 16.750, followed by 16.800. This would lead to a retest of the 17.000 level, and higher to 17.500.

Support can be seen at the 200-period MA at 16.489, with the rising black trend line at 16.460 supported by the 100 and 50 MA at 16.440. A loss of this area would see price move to test 16.300, followed by 16.137 and 16.076. The 16.000 area represents strong psychological support, a loss of which could see 15.610 tested, followed by 15.000.

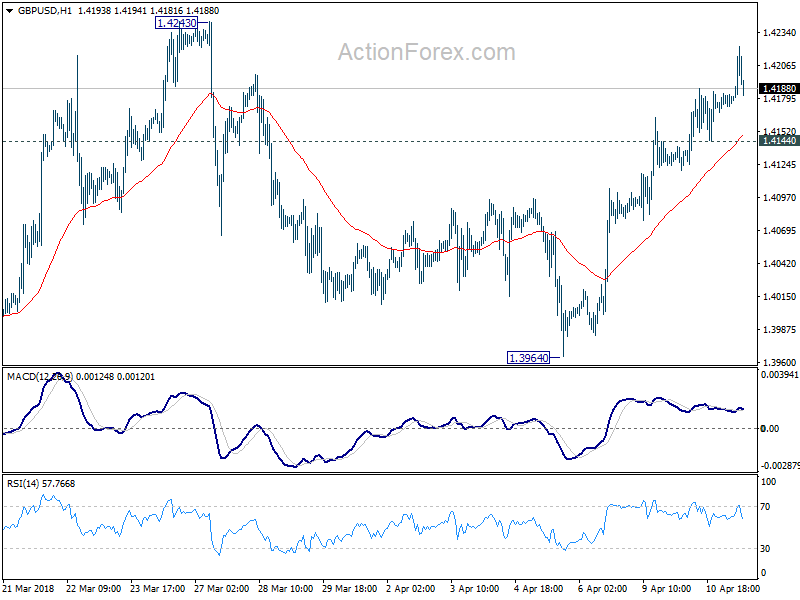

GBP pares gain as industrial and manufacturing production missed expectation

GBP/USD pares some of earlier against after disappointing data.

- Industrial production rose 0.1% mom, 2.2% yoy in February, below expectation of 0.4% mom, 2.9% yoy.

- Manufacturing production dropped -0.2% mom, rose 2.5% yoy, below expectation of 0.2% mom, 3.3% yoy.

- Construction output dropped -1.6% mom in February versus expectation of 0.7% mom.

- Visible trade deficit narrowed to USD -10.2b in February versus expectation of GBP -11.9b.

While GBP/USD retreats after hitting 1.4222, it's still on track to 1.4243 as long as 1.4144 minor support holds.

AUDUSD Has Significant Bullish Day Before Touching Upper Bollinger Band

AUDUSD has reversed back up again after four bearish weekly sessions, following the strong rebound on the 38.2% Fibonacci retracement level near 0.7640 of the upleg from the low on January 2016 (0.6820) and the high on January 2018 (0.8135). In the short-term, the pair posted an aggressive positive rally during yesterday's session, approaching the 40-day simple moving average around 0.7765, which overlaps with the upper Bollinger Band.

In the daily timeframe, prices bounced off the latter level during today's early European session and based on the technical indicators, momentum is weak to provide a sustained move higher. RSI is above the threshold of 50 but is pointing to the downside, while the MACD oscillator is slightly rising above its trigger line.

If price action jumps above the intraday high of 0.7768 and surpasses the aforementioned obstacles (40-day SMA and upper Bollinger Band), there is scope to test the 23.6% Fibonacci mark of 0.7826. Rising above it would see prices re-test the 0.7920 peak, taken from the high on March 14.

In case of further correction, then the focus could shift to the downside towards the 38.2% Fibonacci level around 0.7640, which holds near the medium-term ascending trend line. If this level is breached, it would increase the bearish pressure and bring about a strong reversal of the trend. From here, AUDUSD would be on the path towards the 0.7500 psychological level.

Abating Trade Woes Support Risk, Dollar Eyes FOMC Minutes & CPIs

Here are the latest developments in global markets:

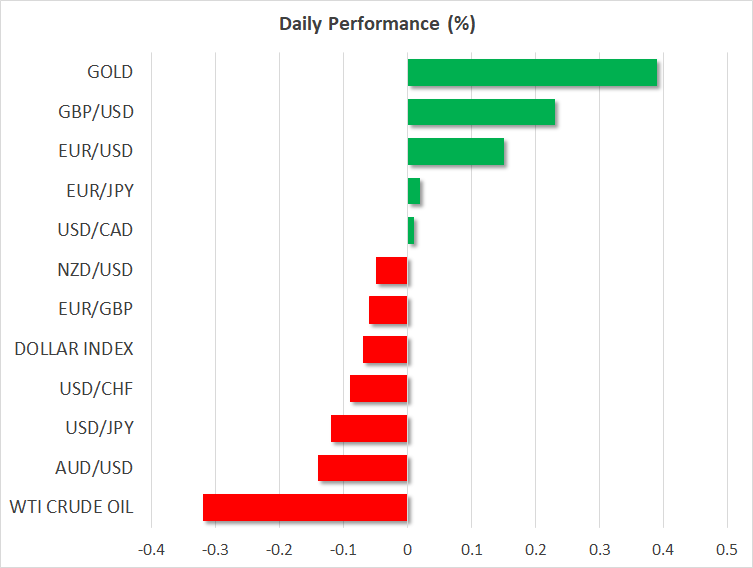

FOREX: The US dollar index traded nearly 0.1% lower on Wednesday, touching a fresh 2-week low ahead of the release of US CPI data and the minutes from the latest FOMC meeting. Both the euro and the pound gained yesterday, amid hawkish remarks from ECB and BoE officials respectively. Commodity currencies such as the aussie, kiwi, and loonie, were all a touch softer today, giving back some of the notable gains they posted yesterday as trade concerns abated.

STOCKS: US markets closed higher on Tuesday, buoyed by diminishing trade worries following the diplomatic tone in the Chinese President's remarks. The Congressional testimony of Facebook CEO Zuckerberg likely played a role too, as the tech sector rallied in the aftermath. The tech-heavy Nasdaq Composite surged almost 2.1%, while the Dow Jones and S&P 500 gained 1.8% and 1.7% respectively. However, futures tracking the S&P, Dow, and Nasdaq 100 are all pointing to a lower open today, which may be related to expectations that a US military action in Syria is imminent. In Japan, the Nikkei 225 and the Topix closed lower by 0.5% and 0.4% correspondingly, though in Hong Kong, the Hang Seng gained 0.56%. In Europe, futures tracking all the major indices were a sea of red.

COMMODITIES: Oil prices corrected a little lower today, giving back some of the significant gains they posted yesterday. The catalyst for the gains were reports Saudi Arabia is aiming for $80/barrel oil prices, to boost the valuation of Saudi Aramco ahead of its planned IPO. Today, oil traders will turn their sights to the weekly EIA crude inventory data, for an update on US production. In precious metals, gold prices are 0.4% higher today, currently hovering near the $1344/ounce barrier. The gains seem to be related to geopolitical concerns, and specifically to the prospect of US military action in Syria that further jeopardizes US-Russian relations. The tumble in the dollar likely contributed as well.

Major movers: Euro gyrates on ECB speculation, commodity currencies bid amid abating trade risks

The euro went for a ride yesterday. The common currency surged initially following hawkish remarks from ECB Governing Council member Ewald Nowotny, who said that the ECB will wind down its QE program this year, and that the first deposit rate hike could be as large as 20bps. However, the ECB soon “intervened”. A spokesperson for the Bank noted Nowotny's views are his own and don't represent the Governing Council, backpedaling on the hawkish rhetoric and sending the euro back down. Still, the currency managed to rise again after that and finish the day higher overall, especially versus the yen that was on the back foot amid a risk-on environment.

In the big picture, even though investors already knew QE was most likely going to end this year, Nowotny confidence likely enhanced that narrative. Despite some softness in recent data, the ECB still looks set to taper its asset purchases in the autumn, with some signaling of that likely to come at the summer meetings.

The US dollar index traded nearly 0.1% lower on Wednesday, extending the losses it posted so far this week amid political and geopolitical uncertainties. At home, the Mueller investigation into Russian election-meddling is heating up, while overseas, the US is contemplating military action against Syria, risking further tensions with Russia. Not to mention trade risks, which although having subsided a little, are still present. Still, the dollar may get some reprieve from key economic releases today, which include the US CPIs for March and the minutes from the March FOMC meeting (see below).

Pound/dollar is 0.2% higher today, building on its gains from yesterday. The surge followed comments from BoE MPC member and notorious policy-hawk Ian McCafferty, who said the Bank should not wait to raise rates, amplifying expectations for a May hike.

Elsewhere, commodity-linked currencies enjoyed the reduction in trade uncertainties yesterday. The aussie, kiwi, and loonie all surged as investors sought riskier assets and diverted funds out of safe havens, like the yen.

Day ahead: FOMC meeting minutes & US CPI take the center stage

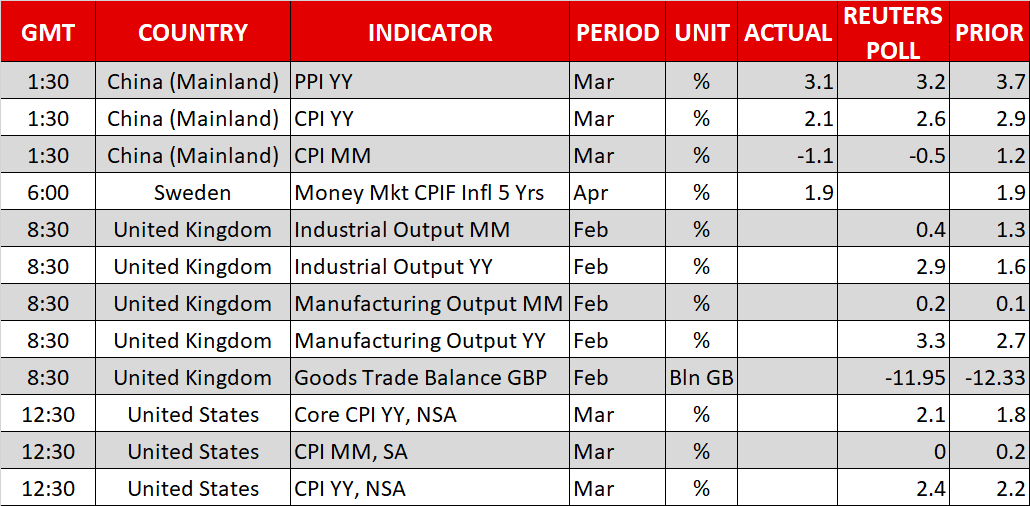

On Wednesday the FOMC meeting minutes due at 1800 GMT will be the highlight of the day as investors are eagerly waiting to identify details behind the Committee's decision to raise interest rates at Jerome Powell's first policy gathering as Fed Chairman. On March 20-21, policymakers raised interest rates as was widely expected and the closely-watched dot plot signalled two more rate hikes for 2018, which was already priced in by the markets. The latter was interpreted as a dovish sign since speculations were in the air that the Fed could deliver four rate hikes in total in 2018 instead of three. Policymakers, though, appeared more optimistic about this year's rate path as the number of officials backing a steeper monetary tightening increased despite the median “dot” remaining unchanged at three hikes. The minutes will also reveal the Fed's view on Trump's trade policy, another spot that could add some volatility to the dollar.

Staying in the US, the Bureau of Labor Statistics will publish readings on consumer prices for the month of March at 1230 GMT. According to forecasts, the headline CPI is expected to edge up by 0.2 percentage points to 2.4% on a yearly basis, while the core measure, which excludes food and energy, is projected to increase to 2.1% y/y from 1.8% in February. This would be the highest growth recorded in a year.

In the UK, stats on manufacturing output and goods trade balance will attract attention, with analysts projecting an improvement in both measures. Particularly, production by manufactures is said to have grown by 3.3% y/y in February compared to 2.7% in the preceding month, while the trade deficit in goods is anticipated to have narrowed from 12.33 billion pounds to 11.95bn in February. Should the data surprise to the upside the pound could extend yesterday's gains, that emerged after BoE MPC member Ian McCafferty stressed the need to raise rates as wage growth could appear stronger than policymakers believe.

In energy markets, the Energy Information Administration (EIA) will report on US oil inventories for the week ending April 6 at 1430 GMT. Oil prices jumped to two-week highs yesterday amid easing tensions between the two largest oil consumers, the US and China, despite the American Petroleum Institute indicating on Tuesday a larger-than-expected increase in US crude oil stocks for the aforementioned week and the EIA saying that crude oil production could rise more than previously thought.

As for today's public appearances, the ECB President, Mario Draghi will be speaking in Frankfurt at 1100 GMT, while the ECB members Pentti Hakkarainen and Ignazio Angeloni are scheduled to deliver remarks at 1300 GMT and 1440 GMT respectively. In the US, Facebook's chief executive, Mark Zuckerberg, will be in the hot seat for the second day, testifying before the House Energy and Commerce Committee regarding the sharing of private information with the London-based data mining firm Cambridge Analytica which had connections with Trump's campaign in 2016.

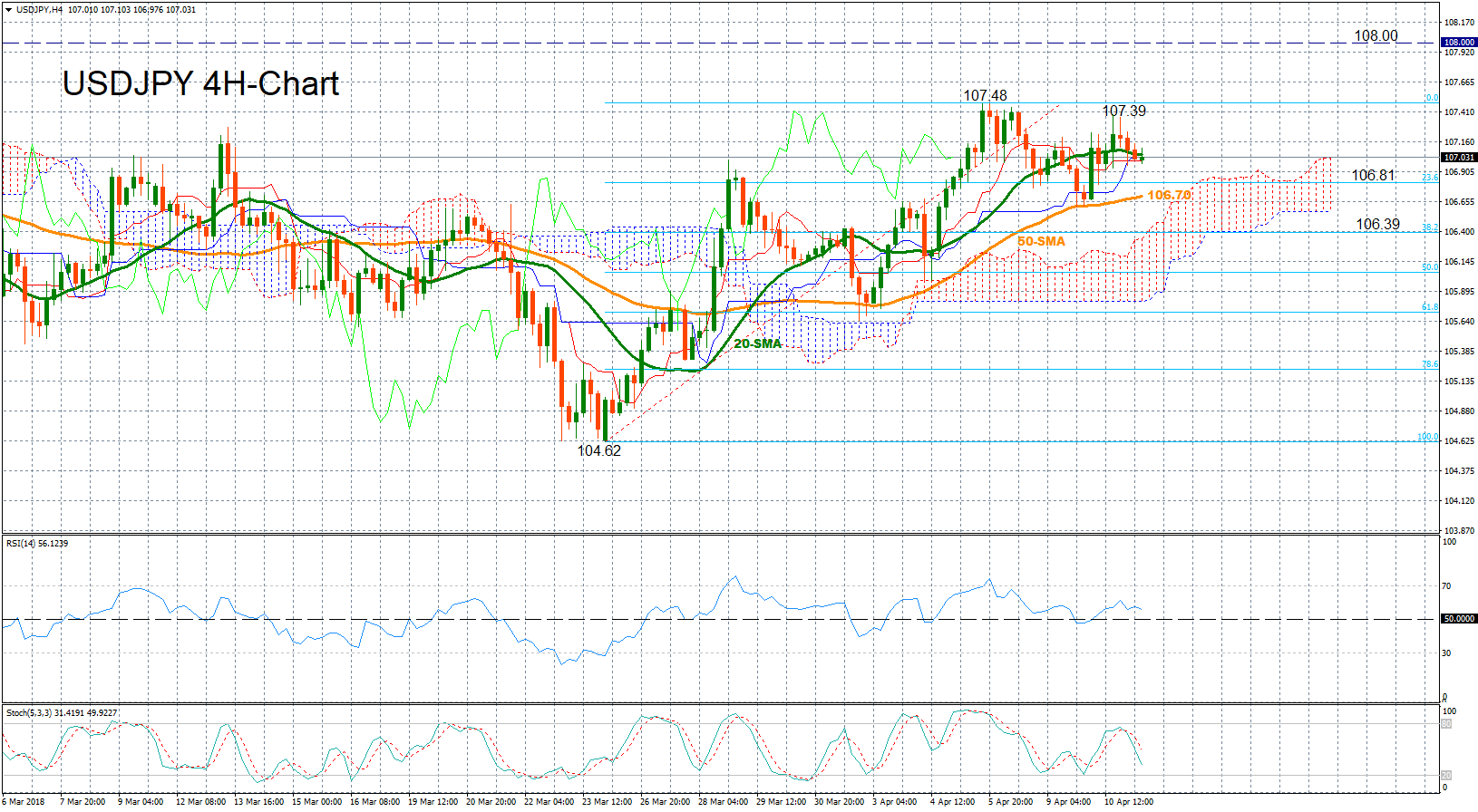

Technical Analysis: USDJPY sends bearish signals for the short-term

USDJPY rebounded adequately yesterday after it found support at the 50-period simple moving average line (SMA) in the four-hour chart. But today the market is turning lower and the technical indicators suggest that weakness might persist in the near term as the RSI is heading lower towards its neutral threshold of 50 and Stochastics are moving downwards after posting a bearish cross.

The pair, though, will be waiting for the US CPI figures and the FOMC meeting minutes today in hopes to regain its strength. In case the CPI numbers beat expectations and the minutes prove hawkish, increasing the odds for further monetary tightening this year, dollar/yen could bounce back to yesterday's high of 107.39 before it tests the more-than-a-one-month high of 107.48 printed last week. Any break above from there could open the door to the 108 handle.

In the alternative scenario, dovish headlines could extend losses towards 106.81, the 23.6% Fibonacci of the upleg from 104.62 to 107.48, while in the event of steeper declines, the 50-period SMA currently at 106.70 could provide support ahead of the 38.2% Fibonacci of 106.39.

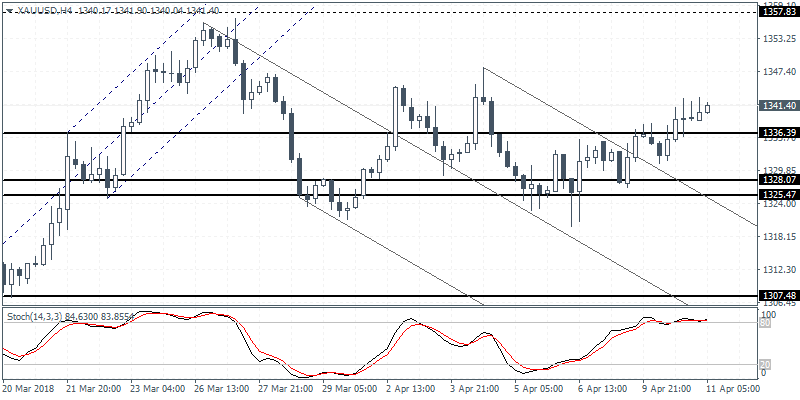

XAUUSD Intraday Analysis

XAUUSD (1341.40): Gold prices edged higher on the day breaking above the 1336 handle. We expect the upside momentum to continue with the risk of gold prices falling back to 1336 handle to establish support. A rebound off this level will confirm the upside bias in gold prices. The next target comes in at 1344 level and in the near-term gold prices could pull back from the current highs and maintain a sideways range.

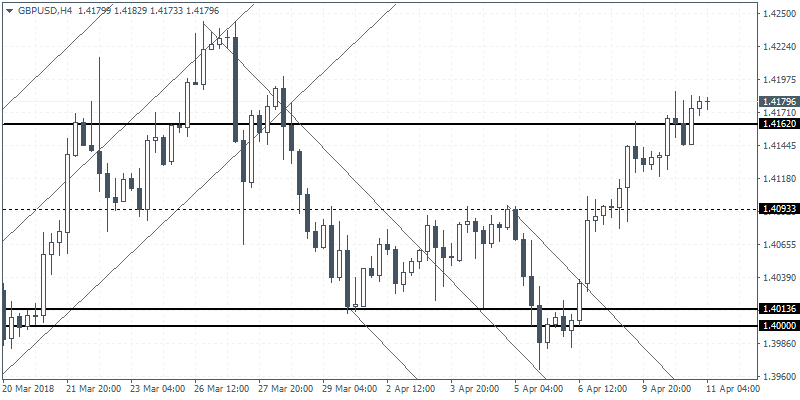

GBPUSD Intraday Analysis

GBPUSD (1.4179): The GBPUSD was seen breaking past the resistance level at 1.4162. Further gains are likely to test the March 28 highs of around 1.4191. There is a risk for GBPUSD to give up the gains in the near term and price action is likely to slip back below the 1.4162 level. The lower support at 1.4093 could stem the declines in the near term. To the upside, price action will need to establish strong support at the 1.4162 level to confirm further upside in price.

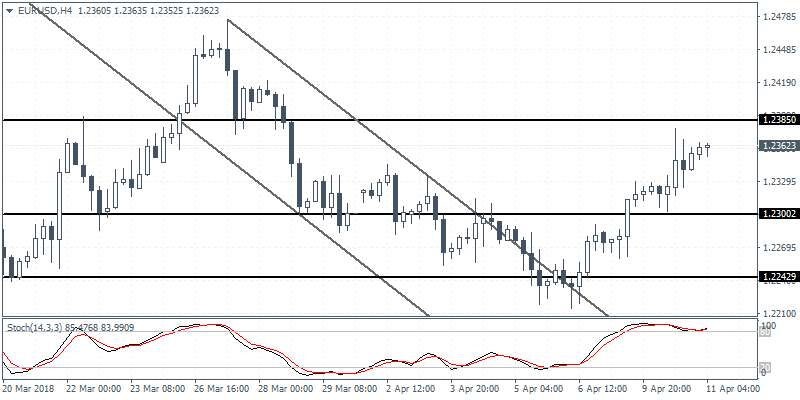

EURUSD Intraday Analysis

EURUSD (1.2362): The EURUSD currency pair extended gains for the third consecutive day, rising to a fresh two week high. Price action is likely to continue to the upside extending the gains toward the resistance level seen at 1.2385. A retest of this resistance level is likely to keep price action range bound within the lower support level of 1.2300. We therefore expect to see the EURUSD maintain a sideways range in the near term.