Sample Category Title

FOMC Minutes In Focus, Trade War Worries Ease

The markets were buoyant yesterday after the speech by Chinese Premier Xi struck a positive tone among investors. Xi promised to reform China's markets including opening the automobile and insurance sector for foreign investors who could claim a majority stake. Xi's speech eased concerns about a looming trade war.

On the economic front, data included the French industrial production figures which rose just 1.2% on the month, missing estimates of 1.5%. In the U.S. the producer prices index saw a better than expected print. Both headline and core PPI rise 0.3% on the month beating estimates.

Looking ahead, investors will be focusing on the FOMC meeting minutes that will be released today. The minutes cover the Fed's central bank monetary policy meeting held in March where interest rates were hiked by 25 basis points.

Ahead of the FOMC meeting minutes, the U.S. monthly consumer price index data will be coming out. Economists forecast that the headline CPI was unchanged on the month in March while core CPI picked up 0.2%, rising at the same pace as the month before.

The UK's manufacturing production data will be coming out today where estimates show a 0.2% increase on the month, slightly higher from 0.1% previously. Construction output and industrial production figures are also expected to be released today.

EURO Bullish Ahead Of Draghi Speech

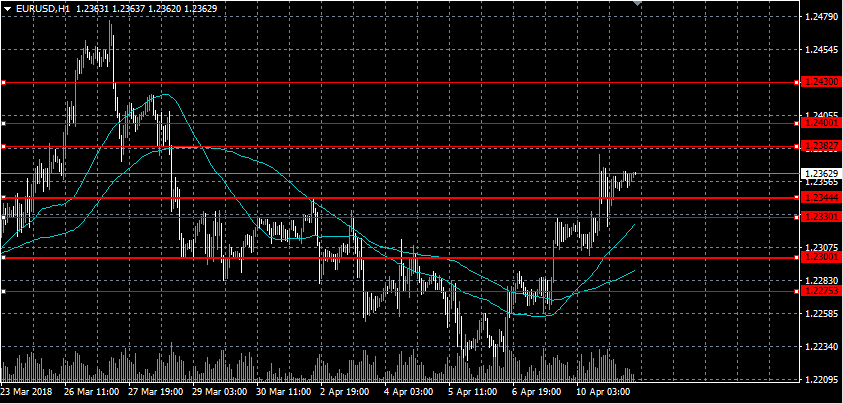

The euro continues to make bullish higher daily price-highs against the U.S dollar, with price-action so far finding weekly technical resistance from the 1.2378 level. The EURUSD pair currently trades around the 1.2360 region, and retains an intraday bullish bias whilst clearly trading above the 1.2333 level. Euro traders now await European Central Bank President Mario Draghi, who is scheduled to speak during today’s European trading session.

The EURUSD pair retains its bullish bias while trading above the 1.2333 level, key intraday resistance is currently located at the 1.2382,1.2400 and 1.2430 levels.

If price-action on the EURUSD pair falls below the key 1.2333 level for a sustained basis, a decline towards the 1.2300 and 1.2275 levels seem likely.

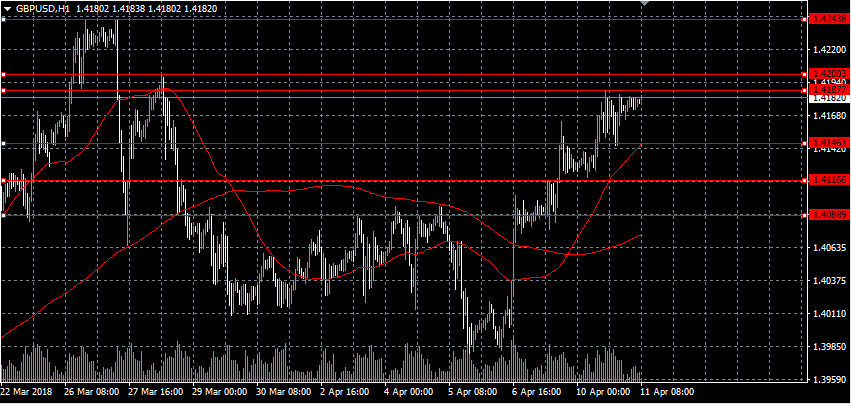

GBPUSD Intraday Bullish Above 1.4146 Level

The British pound continues to press towards the 1.4200 resistance level against the greenback, as the U.S dollar index comes under further selling pressure. The GBPUSD pair has so far reached a weekly price-high of 1.4187, with pound dip-buyers still prevalent on pullbacks towards the key 1.4146 technical level. Sterling traders now look towards a raft of economic data points from the United Kingdom this morning, with monthly UK Manufacturing and Industrial Productions in focus.

The GBPUSD pair retains its bullish bias while price-action trades above the 1.4146 level, key upside technical resistance is located at the 1.4200 and 1.4243 levels.

If price-action on the GBPUSD pair holds below the 1.4146 level for a sustained basis, sellers may test back towards the 1.4116 and 1.4088 levels

FED Watchers Await US CPI Data On Wednesday

Wednesday will be another active day for global finance, with headline data releases and monetary policy speculation high on the agenda.

European trading is expected to pick up around 08:00 GMT with a report on Italian retail sales. Half an hour later, the United Kingdom will dominate the headlines with data on industrial production, manufacturing production and the goods trade balance. Each figure is expected to show a notable improvement for the month of March.

European Central Bank (ECB) Governor Mario Draghi is set to deliver a speech at 11:00 GMT that could have monetary policy implications. The ECB is gradually unwinding its record stimulus program thanks to a broad pickup in the euro region's economy.

The US Department of Labor will kick off the North American session with a report on consumer inflation scheduled for 12:30 GMT. The consumer price index (CPI) is expected to have flat-lined in March after climbing 0.2% the month before. In annual terms, however, CPI likely expanded 2.4% from a 2.2% pace.

So-called core inflation, which strips away volatile goods such as food and energy, likely rose 2.1% year-over-year.

Federal Reserve officials target inflation at 2% annually but relies on the core PCE index to gauge changes in consumer prices. That said, the monthly CPI report is seen as a good gauge of long-term inflation trends, which can have a direct impact on Fed policy.

The Fed on Wednesday will release the minutes of the March Federal Open Market Committee (FOMC) meeting, where officials voted to raise interest rates by a quarter point.

Energy traders will also be monitoring weekly inventory data courtesy of the US Energy Information Administration (EIA). Weekly crude stockpiles are forecast to have risen by 220,000 in the latest week.

EUR/USD

Europe's common currency marched higher on Tuesday, hitting 1.2373 US in intraday trade. At the time of writing, EUR/USD was trading around 1.2360 for a gain of 0.1%. The pair faces stiff resistance at the 1.2370 handle. A breakout from this level would target the recent swing high north of 1.2400.

GBP/USD

Cable extended its multi-day run on Tuesday, as prices once again came close to breaching the 1.4200 level. GBP/USD would later consolidate around 1.4180, where it was last trading. The bulls are finding support above 1.4100 levels, which could see prices extend further into positive territory.

USD/JPY

Improved risk sentiment failed to propel the USD/JPY forward on Tuesday, as the pair touched an intraday low of 106.66. It would later recover north of 107.00, although downside pressure remains the focus. Immediate support is located at the 106.60 swing low region, with upside likely capped by the 107.50 resistance band.

Currencies: Will US CPI Be Able To Unlock USD Stalemate

- Rates: US CPI and FOMC Minutes take center stage

Risk sentiment turned more cautious overnight on rising geopolitical risks. Today's US events (CPI and FOMC Minutes) could weigh on US Treasuries, underperforming the Bund. On the European side, we eye a Q&A session by ECB President Draghi who will probably further downplay yesterday's Nowotny comments. - Currencies: Will US CPI be able to unlock USD stalemate

The dollar ignored a higher than expected US PPI yesterday. The euro was supported by hawkish comments from ECB's Nowotny. The focus turns to US inflation data today. Both core and headline CPI are expected north of 2.0%. However, will it be enough to give the dollar additional interest rate support?

The Sunrise Headlines

- US stock markets managed to slightly add to opening gains, resulting in a 1.5% to 2% profit on a daily basis. Asian stock markets are mixed overnight with China outperforming (+0.75%).

- The ECB disowned comments by governor Nowotny who said the central bank could lift its deposit rate alone when it starts tightening policy. “Nowotny's views are his own,” an ECB spokesperson said in a emailed statement.

- China's factory inflation slowed for a fifth month, from 3.7% Y/Y to 3.1% Y/Y (vs 3.3% Y/Y forecast), while the consumer prices retreated from a 4-yr high (2.9% Y/Y) to 2.1% Y/Y (vs 2.6% Y/Y consensus).

- China will allow domestic and foreign financial firms to compete on an equal footing and "sharply" expand the business scope for foreign banks, central bank governor Yi Gang said. (Reuters)

- The US worked to rally international support for a possible military strike against Syrian President al-Assad for an alleged chemical-weapons attack, drawing initial backing from France, the UK and Saudi Arabia (WSJ).

- Oil prices temporary traded above $71/barrel, the highest level since the end of 2014. Mounting concerns about Syria and rounds of sanctions against Russia and Iran are at play. The US also trimmed its 2018 production forecast.

- Today's eco calendar contains UK industrial production and US CPI. ECB Draghi, Hakkarainen and Angeloni are scheduled to speak. The Fed publishes Minutes of its previous meeting. Germany, Portugal and the US tap the bond market.

Currencies: Will US CPI Be Able To Unlock USD Stalemate

Will US CPI be able to unlock USD stalemate?

Yesterday, market tensions eased after soft comments from the Chinese president on trade. Still, it didn't provide a clear guide for USD trading. US PPI was stronger than expected but was largely ignored by FX and bond markets. On the other hand, the euro was supported by hawkish comments from ECB's Nowotny. He re-opened the debate on ECB policy normalization and suggested that a hike in the deposit rate was possible relatively soon after ending APP. USD/JPY ended the session at 107.20 (from 106.77). EUR/USD finished the day at 1.2356 (from 1.2321).

Overnight, headlines from Chinese officials on trade issues remain soft, but markets apparently want more concrete progress in the US-China trade dispute. Asian equities are trading mixed to modestly higher. The dollar keeps a tentative negative bias. USD/JPY is drifting back south to the 107 area. EUR/USD (1.2360 area) is holding near yesterday's top.

Today, the US February CPI and the Minutes of the March Fed meeting will be published. Headline CPI is expected at 0.0% M/M and 2.4% Y/Y (from 2.2%). Core inflation is expected at 2.1% Y/Y (from 1.8%). One is inclined to expect higher inflation to provide additional interest rate support for the USD. However, US yields recently settled in a wait-and-see modus, mainly due the uncertainty on the impact of the US-China trade dispute. We look out whether a rise in US inflation (especially in case of an upside surprise) will be able to unlock the stalemate on bond markets and in the dollar. Yesterday's reaction on the PPI suggests that a substantial positive surprise is needed to provide USD interest rate support. Last week, EUR/USD drifted lower in the 1.2555/1.2155 range. However, a downside test was blocked after disappointing US payrolls. EUR/USD rebounded in the established range. A sustained break of the range bottom will probably remain difficult as long as Fed rate hike expectations are clouded by uncertainty on trade. At the same time, the Nowotny comments helped to solidify the euro downside.

Yesterday, EUR/GBP temporary revisited the 0.87 area on hawkish comments from BoE's McCafferty, but the move was reversed after the Nowotny comments. Today, the UK trade balance, production data and the NIESR GDP estimate will be published. Markets will look out whether the data will confirm the case for a May BoE rate hike. We doubt that today's data will be strong enough to trigger further sustained GBP gains, especially against the euro.

EUR/USD rebounding higher in the established range both due to USD softness and ’euro strength’

RBA Lowe: No strong case for near term adjustment in interest rate

RBA Governor Philip Lowe devoted a section on monetary policy is his address to Australia-Israel Chamber of Commerce (WA) today. And, he brought out four broad points.

1. He expects a "further pick-up" in the Australian economy, with increased investment, hiring and exports. Inflation is also expected to "gradually pick up" with wages growth too. But there are uncertainties "lying in the international arena". Lowe warned that "a serious escalation of trade tensions would put the health of the global economy at risk and damage the Australian economy". And, "we also have a lot riding on the Chinese authorities successfully managing the build-up of risk in their financial system." Domestically, the level "high level of household debt remains a source of vulnerability".

2. The next interest rate move will likely be "up, not down". And that might "come as a shock to some people".

3. Inflation returning to midpoint of target zone is expected to be "only gradual". And, "it is still some time before we are likely to be at conventional estimates of full employment.

4. "Reserve Bank Board does not see a strong case for a near-term adjustment in monetary policy." Lowe reiterated that other global central banks have lower policy rates than Australia "over the past decade". So, the situations are different.

US CPI Data Expected To Decline In March

At 07:00 GMT, The ECB's Non-Monetary Policy Minutes will be released, and EUR crosses may be affected.

At 08:30 GMT, UK Industrial Production (YoY) (Feb) is expected to be 2.9% against a previous 1.6%. Industrial Production (MoM) (Feb) is expected to be 0.4% against 1.3% previously. Seasonally, there is generally a downturn in this figure, with a drop early in the New Year, usually seen in February and followed by a strong rebound in March. Manufacturing Production (YoY) (Feb) is expected to be 3.3% against 2.7% previously. Manufacturing Production (MoM) (Feb) is expected to be 0.2% against 0.1% previously. This figure had been less volatile during much of 2017, with readings staying positive but close to zero. The expectation is for a slight improvement after last month's marginal miss. GBP pairs may move because of this data release.

At 11:00 GMT, ECB President Draghi is due to speak at the Generation Euro Students' Award Ceremony, in Frankfurt. Audience questions are expected and comments may result in movement in EUR crosses.

At 12:30 GMT, US Consumer Price Index (YoY) (Mar) data will be released with an expected reading of 2.4% against 2.2% previously. Consumer Price Index Ex-Food & Energy (YoY) (Mar) data will be released with an expected reading of 2.1% against 1.8% previously. Consumer Price Index Ex-Food & Energy (MoM) (Mar) data will be released and is expected to be unchanged at 0.2%. Consumer Price Index (MoM) (Mar) data will be released with an expected reading of 0.0% against 0.2% previously. Consumer Price Index Core s.a. (Mar) data will be released with an expected reading of 256.200 against 255.751 previously. These data points will allow for an updated measure of the effect of inflation on consumers. Inflation is one of the main drivers of market sentiment in the US currently. The expectation is for an increase in consumer prices year-on-year but for the monthly reading to show a drop. The higher reading shocked the market in January but can be partly explained as an increase in demand for winter items due to the cold weather. This can be seen in the February number, which showed a correction, one which is expected to continue today. USD pairs and US assets may experience a pickup in volatility due to this data.

At 18:00 GMT, The FOMC Minutes will be released, along with the US Monthly Budget Statement (Mar), which is expected to show a balance of $-194B against $-215B previously. The FOMC Minutes are expected to focus on rate hikes and inflation, giving traders an insight into the Fed's thinking on the path of rates for the coming months. The trade war with China may not be mentioned in these minutes because the meeting occurred before the situation escalated last month.

IMF Lagarde: Sun is still shining but we have to “steer clear of protectionism”

In a speech at the University of Hong Kong, IMF Managing Director Christine Lagarde expressed her optimism on the global economy. She said the "economic picture is "mostly bright" and "the sun is still shining". Global momentum is driven by "stronger investment", "rebound in trade" and "favorable financial conditions". She said the forecast to be release next week will "continue to be optimistic".

Regarding advanced economies, Lagarde said Eurozone's upswing is "now more widely spread across the region". US growth will "likely accelerate further due to expansionary fiscal policy". In Asian emerging markets, China and India lead by "rising exports and higher domestic consumption. But she also warned of "darker clouds looming". Momentum in 2018 and 2019 will eventually slow because of "fading fiscal stimulus" in the US China, rising interest rates and tighter financial conditions.

Lagarde emphasized three priorities for the global economy, including 1. Steering clear of Protectionism, 2. Guard against Fiscal and Financial Risk, 3. Foster Long-term Growth that Benefits Everyone.

Airlines Warned Of Possible Strikes On Syria Over The Next 72 Hours

As we await the FOMC minutes this evening, which will give an indication of the Fed's thinking on the path of hikes going forward, UK Industrial Production is expected to decline from 1.3% to 0.4% (MoM) today, which puts it back in line with the January reading. The Trade tensions between the US and China have eased as the geopolitical situation in Syria takes centre stage. Coalition forces are expected to retaliate against the Assad regime for an alleged chemical weapons attack, with Eurocontrol warning airlines flying over the area that military traffic is expected to build up and it is likely missiles will be deployed in the next 72 hours. The markets may react to any strike with a move to risk-off sentiment.

FOMC Member Kaplan spoke in Beijing and made the following comments: The US economy in 2018 will be relatively strong. He expects growth of 2.50% to 2.75% this year. Inflation will firm in 2018 and move towards the 2% target. Business investment should be stronger on tax reforms. 2019 growth will be a little weaker and will trend down to 1.75% by 2020. He said that globalisation and trade is an opportunity to boost US economic growth. The base case is still for the Fed to increase rates three times this year. On US/China relations, he said that it is clearly in the interests of both countries to have a constructive trading relationship.

MPC Member Haldane spoke about the role of central banks and societal inequality at the David Finch Public Lecture, in Melbourne. He made the following comments: with few exceptions, the impact of looser monetary policy on different cohorts of society has been positive and significant in income and wealth terms. Policy loosening since 2007 has had a significant positive effect.

Canadian Housing Starts s.a (YoY) (Mar) were released coming in at 225.0K against an expected 218.0K, from 229.7K last month, which was revised up to 231.0K. This data is performing strongly, with a beat on expectations, despite the headline number declining from last month's reading. EURCAD fell from 1.56456 to 1.55458 in the hours after the release.

US Producer Price Index Ex-Food and Energy (YoY) (Mar) was 2.7% v an expected 2.6%, against a previous reading of 2.5%. Producer Price Index (MoM) Mar) was 0.3% v an expected 0.1%, from 0.2% previously. Producer Price Index Ex-Food and Energy (MoM) (Mar) was 0.3% v an expected 0.2% against a previous reading of 0.2%. Producer Price Index (YoY) Mar) was 3.0% v an expected 2.9%, from 2.8% previously. This data came in largely as expected, with all of the readings ticking up slightly. This can feed into the inflation forecast, as consumers are inevitably left with the burden of increased prices. USDJPY halted its decline and moved higher from 1.26522 up to 1.26691 but then resumed its fall.

EURUSD is up 0.08% overnight, trading around 1.23648.

USDJPY is down -0.11% in early session trading at around 107.060.

GBPUSD is up 0.09% this morning, trading around 1.41862.

USDCAD is unchanged in early trade at around 1.26015.

Gold is up 0.20% in early morning trading at around $1,342.06.

WTI is down -0.49% this morning, trading around $65.27.

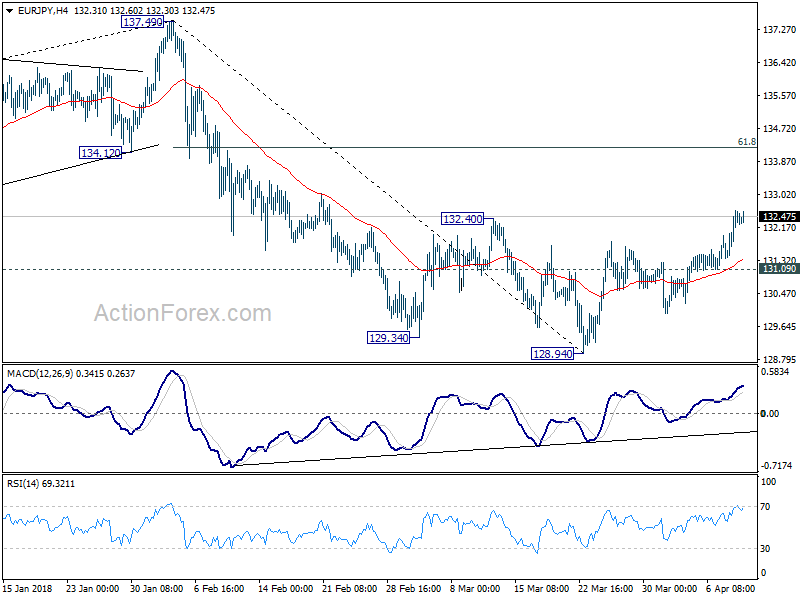

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.70; (P) 132.16; (R1) 132.89; More....

EUR/JPY's rally continues to as high as 132.61 so far. Breach of 132.40 resistance with solid upside momentum suggests decline from 137.49 has completed at 128.94 already. Intraday bias is now on the upside for 61.8% retracement of 137.49 to 128.94 at 134.22 and above. On the downside, break of 131.09 support is needed to indicate completion of the rebound. Otherwise, further rebound will remain in favor in case of retreat.

In the bigger picture, price action from 137.49 medium term top are developing into a corrective pattern. Strong support from 55 EMA (now at 129.91) suggests that the first leg has completed at 128.94 already. Nonetheless, break of 137.49 is needed to confirm resumption of the rise from 109.03 (2016 low). Otherwise, we'd expect more corrective range trading another, with risk of another fall to 38.2% retracement of 109.03 to 137.49 at 126.61 before completion.