Sample Category Title

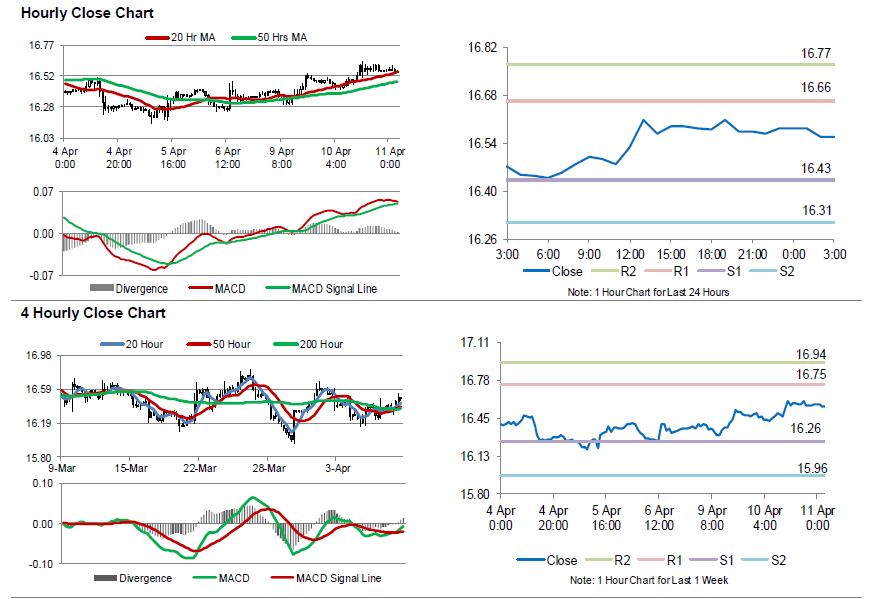

Silver: White Metal Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, Silver rose 0.67% against the USD and closed at USD16.58 per ounce, tracking gains in gold prices.

In the Asian session, at GMT0300, the pair is trading at 16.56, with silver trading 0.15% lower against the USD from yesterday’s close.

The pair is expected to find support at 16.43, and a fall through could take it to the next support level of 16.31. The pair is expected to find its first resistance at 16.66, and a rise through could take it to the next resistance level of 16.77.

The white metal is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

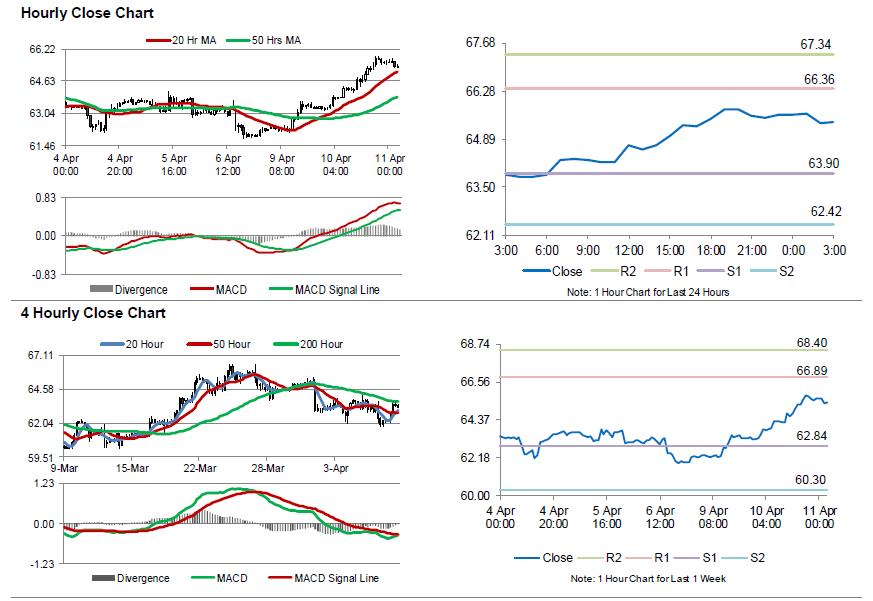

Crude Oil: Oil Trading Lower, Ahead Of EIA’s Weekly Crude Oil Stockpiles Data

For the 24 hours to 23:00 GMT, Crude Oil rose 3.70% against the USD and closed at USD65.59 per barrel, as tensions surrounding Syria stoked concerns over disruptions to Middle East crude output.

Separately, the American Petroleum Institute (API) indicated that US crude oil inventories rose by 1.8 million barrels to 429.1 million barrels in the week to 06 April.

In the Asian session, at GMT0300, the pair is trading at 65.38, with oil trading 0.32% lower against the USD from yesterday's close.

The pair is expected to find support at 63.90, and a fall through could take it to the next support level of 62.42. The pair is expected to find its first resistance at 66.36, and a rise through could take it to the next resistance level of 67.34.

Crude oil is trading above its 20 Hr and 50 Hr moving averages.

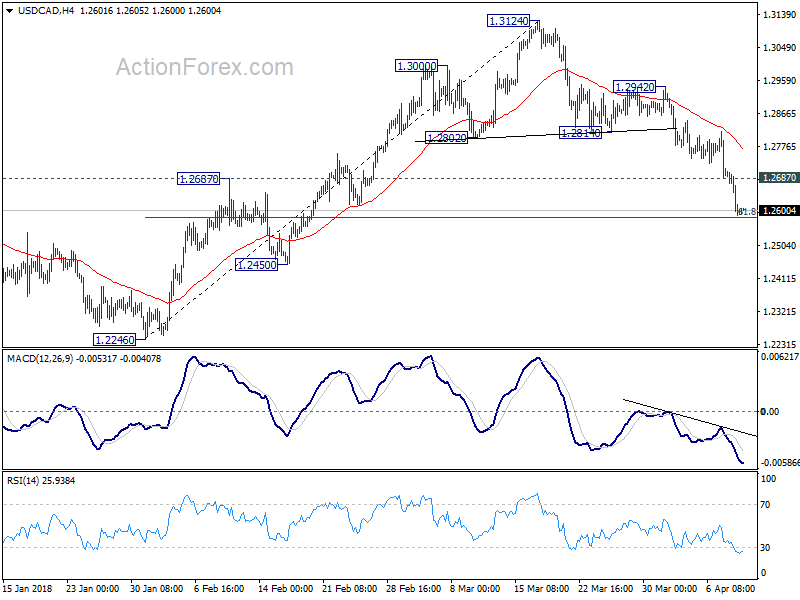

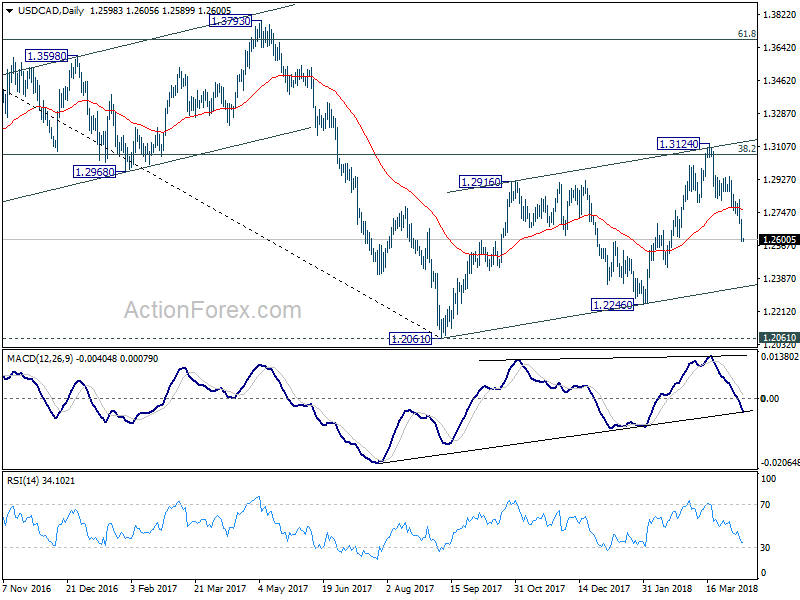

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2554; (P) 1.2631; (R1) 1.2674; More....

USD/CAD's decline from 1.3124 accelerated to as low as 1.2587 so far, just ahead of 61.8% retracement of 1.2246 to 1.3124 at 1.2581. Intraday bias remains on the downside for deeper decline. The corrective rise from 1.2061 should have completed with three waves up to 1.3124. Break of 1.2581 will pave the way back to 1.2061/2246 support zone. On the upside, above 1.2687 minor resistance will turn intraday bias neutral first. But near term outlook will remain bearish as long as 1.2814 support turned resistance holds.

In the bigger picture, current development turns favors to the case that rise from 1.2061 is a corrective three wave pattern. It could have completed at 1.3124 after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Focus is now back on 1.2061 and 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Decisive break there will resume larger down trend from 1.4689 (2016 high) to 61.8% retracement of 0.9406 to 1.4689 at 1.1424.

Dollar Stays Weak as Focus Turns to US CPI and FOMC Minutes

Risk appetite stays strong so far with receding fear of full-blown trade war between US and China. Major US indices closed up overnight with DOW gaining 1.79%, S&P 500% risen 1.67% and NASDAQ up 2.07%. Hong Kong HSI is lifted further by more specific details regarding China opening up financial market access and is trading up 0.75% at the time of writing. But Nikkei gives up initial gain and is trading down -0.3%.

In the currency markets, Canadian Dollar, Australian Dollar and New Zealand Dollar remain the strongest one for the week even though they are paring some gains in Asian session. Canadian Dollar outshines the others with the help of surge in oil prices. Dollar and Yen remain the weakest two for the week.

For today, focus will now turn to UK production data in European session first. US CPI and FOMC minutes will take center stage later in the day.

Markets to scrutinize FOMC minutes for chance of four hikes this year

US CPI release and FOMC meeting minutes will be the main focuses of today. Headline CPI is expected to accelerate from 2.2% yoy to 2.4% yoy in March. Core CPI is also expected to accelerate from 1.8% yoy to 2.1% yoy. After March Fed hike, there are still a lot of questions regarding Fed's rate path. In particular, back then, traders were quite disappointed that Fed kept the projection of three hikes in total in 2018 unchanged. Among the 15 top Fed policymakers, 8 had two or fewer hikes for this year in the famous dot-plot. On the other hand, 7 had three or more. This showed quite a divergence between Fed hawks and doves. And the minutes could reveal more about the debates inside FOMC, thus, giving some hints on the chance of a total of four hikes this year.

The markets, without a doubt, would want to read more into Fed policymakers' minds regarding inflation outlook. But in addition to that, their views on flattening yield curve will catch a lot of attentions. This could be a factor that prompt some cautions for doves to turn hawkish. Another point to scrutinize is Fed officials view on where the neutral rate is. The key is that when interest rates surpasses the neutral rate, policy will become restrictive. For now, it looks like even the hawks wouldn't commit to turn monetary policy restrictive yet. And the neutral rate could be seen as a ceiling in the current tightening cycle.

Nonetheless, it should be noted that with easing concerns over trade war, traders are back putting their bets on a June hike. As indicated by fed funds futures, chance of a 25bps June hike surged sharply this week to 95%. But that provides little support to Dollar so far. Hence, while the CPI and FOMC minutes are important events, the market reactions could be another story.

China PBoC Yi outlines specifics on opening financial market access at Boao

China PBoC Yi outlines specifics on opening financial market access at Boao

New People's Bank of China Governor Yi Gang pledged to further open the financial markets in the Boao Forum for Asian in China. And some specifics were offered by Yi too. Firstly, the government will remove foreign ownership caps on Chinese banks by the end of June. Secondly, foreign securities and life insurance companies will be allowed to hold majority stakes in their Chinese counterparts. That is, ownership could be raised from 49% to 51%. And such restriction will also be abolished in three years. Thirdly, by the end of June, the permitted business scope for foreign insurance agents will be expanded. Fourthly, the daily quota for foreign investors to buy Chinese stocks and for Chinese investors to buy Hong Kong traded stocks will be quadrupled. In addition, by the end of 2018, China will launch a trading link between Shanghai stock markets to London's. Separately, Yi also said that China won't devalue Yuan as part of the moves of trade war with the US.

UK CBI: Don't diverge from EU rules after Brexit

The Confederation of British Industry published a report showing that UK business overwhelming prefer to stay with EU rules after Brexit. Carolyn Fairbairn, CBI Director-General said that for the majority of businesses, "diverging from EU rules and regulations will make them less globally competitive, and so should only be done where the evidence is clear that the benefits outweigh the costs." She emphasized that the report comes from "heart of British business" and it provides "unparalleled evidence to inform good decisions that will protect jobs, investment and living standards across the UK." Additionally, she urged "major acceleration" in the partnership between businesses and the government to deal with Brexit issues. Here is the 114-paged reported titled "Smooth operations: An A-Z of the EU rules that matter for the economy".

On the data front

Japan machine orders rose 2.1% mom in February. Japan Domestic CGPI rose 2.1% yoy in March. Australia Westpac consumer confidence dropped -0.6% in April. China CPI slowed to 2.1% yoy in March, down sharply from 2.9% yoy. PPI also slowed to 3.1% yoy, down from 3.7% yoy.

Looking ahead, UK industrial production, manufacturing production and trade balance will be the main focus of European session. US will release CPI and FOMC minutes later today.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2554; (P) 1.2631; (R1) 1.2674; More....

USD/CAD's decline from 1.3124 accelerated to as low as 1.2587 so far, just ahead of 61.8% retracement of 1.2246 to 1.3124 at 1.2581. Intraday bias remains on the downside for deeper decline. The corrective rise from 1.2061 should have completed with three waves up to 1.3124. Break of 1.2581 will pave the way back to 1.2061/2246 support zone. On the upside, above 1.2687 minor resistance will turn intraday bias neutral first. But near term outlook will remain bearish as long as 1.2814 support turned resistance holds.

In the bigger picture, current development turns favors to the case that rise from 1.2061 is a corrective three wave pattern. It could have completed at 1.3124 after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Focus is now back on 1.2061 and 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Decisive break there will resume larger down trend from 1.4689 (2016 high) to 61.8% retracement of 0.9406 to 1.4689 at 1.1424.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machine Orders M/M Feb | 2.10% | -2.50% | 8.20% | |

| 23:50 | JPY | Domestic CGPI Y/Y Mar | 2.10% | 2.00% | 2.50% | |

| 0:30 | AUD | Westpac Consumer Confidence Apr | -0.60% | 0.20% | ||

| 1:30 | CNY | CPI Y/Y Mar | 2.10% | 2.60% | 2.90% | |

| 1:30 | CNY | PPI Y/Y Mar | 3.10% | 3.30% | 3.70% | |

| 8:30 | GBP | Visible Trade Balance (GBP) Feb | -11.9B | -12.3B | ||

| 8:30 | GBP | Industrial Production M/M Feb | 0.40% | 1.30% | ||

| 8:30 | GBP | Industrial Production Y/Y Feb | 2.90% | 1.60% | ||

| 8:30 | GBP | Manufacturing Production M/M Feb | 0.20% | 0.10% | ||

| 8:30 | GBP | Manufacturing Production Y/Y Feb | 3.30% | 2.70% | ||

| 8:30 | GBP | Construction Output M/M Feb | 0.70% | -3.40% | ||

| 11:00 | GBP | NIESR GDP Estimate Mar | 0.30% | 0.30% | ||

| 12:30 | USD | CPI M/M Mar | 0.00% | 0.20% | ||

| 12:30 | USD | CPI Y/Y Mar | 2.40% | 2.20% | ||

| 12:30 | USD | CPI Core M/M Mar | 0.20% | 0.20% | ||

| 12:30 | USD | CPI Core Y/Y Mar | 2.10% | 1.80% | ||

| 14:30 | USD | Crude Oil Inventories | -4.6M | |||

| 18:00 | USD | Monthly Budget Statement Mar | -175.0B | -215.2B | ||

| 18:00 | USD | FOMC Meeting Minutes |

Oil Price Jumped to 4 Years’ High before Profit-taking

Brent crude oil price jumped to a fresh 4- year high of US$ 71.34/bbl before settling at US$ 71.04/bbl, up +3.48%. WTI crude oil price also gained +3.3%, ending the day at US$ 65.51/bbl. The rally was driven by the broadly based improvement in risk appetite as Chinese President Xi Jinping's speech in Boao appeared to have eased US-China trade tensions. Meanwhile, Saudi Arabia's Energy Ministry indicated that the Kingdom would keep exports below 7M bpd and restore its inventories to "normal" level.

Profit-taking in both oil benchmarks on Wednesday was facilitated by the inventory report released after US market close. The industry- sponsored API estimated that crude oil inventory surprisingly increased +1.56 mmb in the week ended April 6. For refined oil products, gasoline stockpile added +2.01 mmb while distillate fell -3.85 mmb for the week. EIA, the US governmental agency, today probably reports a -0.19 mmb draw in crude oil inventory. Gasoline and distillate stockpiles might have dropped -1.43 mmb and -0.03 mmb respectively.

UK CBI: Don’t diverge from EU rules after Brexit

The Confederation of British Industry published a report showing that UK business overwhelming prefer to stay with EU rules after Brexit. Carolyn Fairbairn, CBI Director-General, said the report comes from "heart of British business" and it provides "unparalleled evidence to inform good decisions that will protect jobs, investment and living standards across the UK." She urged "major acceleration" in the partnership between businesses and the government to deal with Brexit issues.

She warned that "it's vitally important that negotiators understand the complexity of rules and the effects that even the smallest of changes can have. Deviation from rules in one sector will have a knock-on effect on businesses in others, and divergence from rules in one part of a production process will have consequences for market access throughout entire supply chains."

Fairbairn added that "it's hard to overstate the importance of the decisions that will be taken over the next six months. Put simply, for the majority of businesses, diverging from EU rules and regulations will make them less globally competitive, and so should only be done where the evidence is clear that the benefits outweigh the costs."

CBI devised three principles for further Brexit negotiations:

- Where rules are fundamental to the trade or transport of goods, the UK and EU must negotiate ongoing convergence.

- In the negotiation of the new relationship, both sides should look to set a new international precedent in the trade of services and digital products.

- Alignment will need to come with mechanisms for influence and enforcement that benefit both sides.

Here is the 114-paged reported titled "Smooth operations: An A-Z of the EU rules that matter for the economy".

China PBoC Yi outlines specifics on opening financial market access at Boao

New People's Bank of China Governor Yi Gang pledged to further open the financial markets in the Boao Forum for Asian in China. And some specifics were offered by Yi too.

Firstly, the government will remove foreign ownership caps on Chinese banks by the end of June.

Secondly, foreign securities and life insurance companies will be allowed to hold majority stakes in their Chinese counterparts. That is, ownership could be raised from 49% to 51%. And such restriction will also be abolished in three years.

Thirdly, by the end of June, the permitted business scope for foreign insurance agents will be expanded.

Fourthly, the daily quota for foreign investors to buy Chinese stocks and for Chinese investors to buy Hong Kong traded stocks will be quadrupled.

In addition, by the end of 2018, China will launch a trading link between Shanghai stock markets to London's.

Separately, Yi also said that China won't devalue Yuan as part of the moves of trade war with the US.

Market Morning Briefing: Euro Yen Has Moved Up

STOCKS

Global stock indices could see some up move in the coming sessions after trading low and sideways for quite sometime now.

Dow (24408, +1.79%) fell sharply to close almost near the intra-day lows. Sideways consolidation is likely to continue for some more sessions with a possible test of 23500 over today or tomorrow. Near term looks bearish within the 23500-245000 range trade.

Dax (12397.32, +1.11%) tried to move up but remained stable near 12400 levels. As mentioned yeaterday, we need to watch price action near important resistance at 12500. While 12500 holds, Dax is likely to move down in the coming sessions.

Nikkei (21750.43, -0.20%) is stable just below 21800. A sustained break above 21800 is needed to push the index higher in the near term; else a fall from here could again take it lower towards 21500-21400 levels.

Shanghai (3206.64, +0.51%) finally showed some strength to move up contrary to our expectation mentioned yesterday. It has moved above 3200 almost after 9-10 sessions and if the momentum continues, it could move up towards 3250 and higher in the coming sessions. Near term looks bullish while above 3200.

Nifty (10402.25, +0.22%) and Sensex (33880.25, +0.27%) are trading below our mentioned resistance levels near 10500 and 34000 respectively. While these levels hold, the indices could see a short dip before rising again; else a break above 10500 and 34000 respectively could trigger an upmove in the near term.

COMMODITIES

Brent (70.81) has sharply moved up to test immediate resistance near 71 as mentioned yesterday while Nymex WTI (65.38) has some more scope on the upside and looks bullish towards 67 before seeing a short dip. Brent could remain stable while resistance at 71 holds. Note that the WTI has strong 3-day trend support which if holds could eventually take the price higher towards 68 in the longer run as visible on the weekly charts. Brent does not look that strong just now but as both prices move together, WTI may influence a rise in Brent too.

Gold (1340.40) has moved up a bit and could re-test 1350-1360 in the coming sessions. Failure to break below 1320 would indicate some upside momentum to trigger in the medium term eventually helping the price to move towards 1360-1380 levels.

Copper (3.1260) has moved up sharply breaking above the immediate resistance near 3.10. Higher resistance near 3.20 on the 3-day candles is the next target for Copper in the coming sessions. Near to medium term looks bullish while above 3.10.

FOREX

Dollar index (89.6) didn't get any support from 13 days or 21 days moving averages on the daily line chart and has broken below them. It is now likely to test support on daily candles and weekly line chart near 89.25 by this week's end / early next week. The US CPI data release (due later today) is unlikely to have any positive effect on Dollar strength (since analysts expect moderation in inflation which should thereby not raise bond yields).

Euro (1.2358) tested support near 1.2225 last week and has been rising from support for the past 2 days, breaching the 21 days moving average line on the daily line chart. It should now target immediate resistance on daily line chart near 1.2425-1.245 by this week's end / early next week. We have been saying that: A decisive breach above 1.25-1.26 would imply medium term bullishness for the Euro. While it stays below 1.25-1.26, it could continue its ranging between 1.215-1.255 of the past 2 months.

Dollar Yen (107.12) got support from earlier resistance trendline on daily candles near 106.9 yesterday and could now rise towards 107.4 again. If it rises beyond 107.4, it could target 107.9 which is the previous high seen in Feb end. However, we prefer a dip back towards 107 rather than a rise past 107.4 immediately. We have been saying that 107.9-108.0 is a crucial level for the Dollar Yen. A breach of this level could imply medium term bullishness.

Euro Yen (132.39) has moved up further after breaching resistance line in downward channel on 3 day and weekly candles. The 21 week moving average line on the weekly line chart at 133 could provide some resistance to it. Euro @ 1.2425 and Dollar Yen @ 107 gives us 132.95; which is a likely scenario as per our above forecasts.

As per expectation, Pound (1.4178) is trading just below 1.42 (seen as resistance on daily and 3 day candles).If 1.42 is breached, there could be some interim resistance near 1.43 on 3 day line chart. In the medium term, a breach of 1.430-1.435 could imply bullishness 1.46 (seen as resistance on weekly line chart).

Dollar Rupee (64.99) is likely to remain stable in the 64.80-65.00 region today as well. We prefer an eventual break on the downside. Let us see how that goes.

INTEREST RATES

Repeating yesterday's comment: US long term yields have been moving in a downward channel since the Fed rate hike last month. The US CPI data release is due later today - analysts expect some moderation in monthly gain figures; however the year-on-year gain figures could reflect higher inflation (which could be slightly misleading considering last year's low figures in March).

High year on year figures could take yields higher temporarily but a moderation in monthly gains could mean that yields will continue moving down through Apr-May.

US 10 Yr Yield (2.7954%), 30 Yr (3.0150%), 5 Yr (2.62%), 2 Yr (2.2988%) :

The 10 Year could test resistance near 2.83%-2.85% on downward channel in short term charts if markets react to a higher year-on-year figure for US CPI; otherwise we expect it to dip back towards 2.75% or lower.

The 30 yr yield as expected has dipped lower after testing channel resistance and could stay near 3% for the coming sessions.

Oil price surges as Syria decision imminent

Brent crude oil surged above 70 yesterday partly as USD depreciated. But more importantly, Trump's decision on Syria in imminent as geopolitical tensions in the Middle East escalates.

Similar picture is seen in WTI crude oil. As seen in the continuation chart, WTI drew strong support from 55 day EMA and rebounded, closing at 65.51 yesterday. 66.66 high is now back in radar. Based on current momentum, this resistance could be taken out very soon.

More importantly, 66.66 is close to long term fibonacci resistance of 50% retracement of 107.68 to 26.05 at 66.87. A strong break of the level will pave the way to 61.8% retracement at 76.50 and above. And that might give USD/CAD another push down towards 1.2 handle.

DOW, S&P 500, NASDAQ not out of the woods yet despite relief rally

Major US equity indices followed other global indices and rebounded strongly overnight on easing trade war fear. DOW closed up 428.90 pts or 1.79% at 24408.00. S&P 500 rose 43.71 pts or 1.67% to 2656.87. NASDAQ also gained 143.96 pts or 2.07% to 7094.30.

However, we'd like to note that all three indices are bounded in recent consolidative pattern started last March/early April.

DOW, despite yesterday's rise, is staying below last week's high at 24622.26, below 55 day EMA at 24591.41. It's also limited below near term falling trendline at around 24722.90. This 24600/700 zone is the key resistance zone to overcome for the near term. As long as it holds, current rebound is seen as part of a consolidation pattern from 23344.52. Once this consolidation completes, there will be another decline through 23344.52 to resume the fall from 26616.71. Firm of the 24600/700 zone will delay the immediate bearish case and bring stronger rebound back towards 25800.35 first.

Similarly, S&P 500 also stays below last week's high at 2672.08, as well ass 55 day EMA at 2685.16.

Similarly, S&P 500 also stays below last week's high at 2672.08, as well ass 55 day EMA at 2685.16.

NASDAQ breached last week's high of 7112.38 but didn't close above. It's also limited below 55 day EMA at 7159.69.

NASDAQ breached last week's high of 7112.38 but didn't close above. It's also limited below 55 day EMA at 7159.69.

While US stocks rebounded, they're not out of the woods yet.

While US stocks rebounded, they're not out of the woods yet.