Sample Category Title

Sunset Market Commentary

Markets:

The German Bund opened lower this morning, catching up with the US Note future’s losses after Chinese President Xi Jinping reached out to the US in a market-friendly speech. Other Chinese comments later dented early optimism somewhat, suggesting difficult negotiations ahead. Core bonds hovered sideways during the first half of European trading. The Bund lost ground after noon when ECB Nowotny became the first ECB official to call for a start to policy normalization, mainly because he sees inflationary pressures building and expects inflation to hit the 2% target in the medium term. He specifically called for a 20 bps deposit rate hike in a first move after ending APP this year. The move lacked real follow-through action as Nowotny is a known hawk and doesn’t represent the (current) view of the ECB board. The US Note future held a steady range despite higher than expected US PPI data and the upcoming start of the mid-month supply operation. The German yield curve bear flattens at the time of writing (Nowotny mentioning deposit rate hike) with yield changes ranging between +1.4 bps (2-yr) and -0.8 bps (30-yr). The US yield curve shifts in similar fashion with yields up to 1.6 bps higher (2-yr). 10-yr yield spread changes vs Germany are almost unchanged with Greece underperforming (+7 bps).

Global markets entered calmer waters after comments from Chinese president Xi Jinping. USD/JPY rebounded north of 107, but there were no follow-through gains. EUR/USD didn’t go anywhere and settled in a tight range in the low 1.23 area. Early afternoon, markets were spooked by comments of ECB’s Nowotny (cf supra). Nowotny is a well-known hawk. FX markets still reacted to the fact that an ECB member re-opened the debate on the specifics of the ECB rate hike path. European yields gained marginally ground and the euro jumped higher. EUR/USD filled offers in the 1.2375 area. A bit later, the US PPI data were slightly higher than expected, but the report had hardly any impact on US yields and on the dollar. USD/JPY still struggles to hold north of 107. EUR/USD trades in the 1.2360 area. For now, the dollar still hasn’t regained the pre-payrolls positive momentum. The Nowotny comments even give the single currency the benefit of the doubt. Will tomorrow’s US CPI be able to change the balance again.

Sterling was supported by comments from BoE MPC member McCafferty this morning as he said that the BoE shouldn’t delay hiking rates as he sees upside inflation risks. EUR/GBP drifted temporary below the 0.87 handle. However, the intraday EUR/GBP decline was completely reversed after the comments from ECB’s Nowotny. EUR/GBP trades again in the 0.8720 area. Cable still preserves part of the intraday gain (currently 1.4170 area).

News Headlines:

US producer price inflation accelerated more than forecast (0.3% M/M & 3% Y/Y vs 0.1% M/M & 2.9%Y/Y consensus). Core PPI’s also beat consensus. The data reflect a broad increase in the costs of services and goods. Proposed tariffs threaten to raise costs of imported materials for US manufacturers further. NFIB Small Business Optimism unexpectedly declined from 107.6 to 104.7 (vs 107 forecast), the lowest level since October last year. The main reason for setback was the lower amount of small businesses who expect a better economy going forwards.

EUR/NOK rose from 9.60 to 9.65 following disappointing Norwegian CPI data (0.2% M/M & 1.2% Y/Y) which dented rate hike bets. The swoon in the Turkish lira continues with EUR/TRY now clearly above 5 in the wake of yesterday’s announced investment package which should, in combination with lower interest rates (despite already double digit inflation), boost the economy (risk of overheating!!). The Russian rouble still feels the sting from this weekend’s new US economic sanctions. The ministry of Finance had to pull a planned bond sale at the very last minute because of surging yields. EUR/RUB currently trades north of 78, coming from this week’s opening level of 71.

US: Small Businesses Remain Upbeat in March Despite Pullback in the Confidence Measure

After rising to the highest level since 1983 in February, the NFIB's small business optimism index fell nearly 3 points to 104.7 in March. The March print came in below market expectations, which called for only a moderate pullback to 107.

Eight of the main subcomponents fell on the month, with only two labor market indicators improving. The declines were more pronounced among those related to future performance, with expectations about an improvement in the economy, higher real sales and the belief that now is a good time to expand pulling back 11, 8 and 4 points to 32%, 20% and 28%, respectively. Still, all three remain healthy relative to historical trends.

Current conditions sub-components, such as current inventory (-3 points to -6%) and earning trends (-1 point to 4%), also pulled back, but by a lesser degree.

Hiring picked up on the month, with the average change in employment rising to 0.36 workers per firm from 0.22 previously, while hiring plans (+2 points to 20%) and job openings (+1 point to 35%) also improved. Readings from all three sub-indicators indicate some of the best performances in the survey's history.

However, the supply of labor remains a soft spot. Nearly half of businesses (47%, unchanged) reported few or no qualified workers for job openings, while quality of labor concerns remained elevated at 21% (-1 point on the month; the dominant concern for the third straight month). On the other hand, concerns regarding taxes (13%), which have fallen 9 points since November, are now at the lowest level since 1982.

Businesses continued to boost worker compensation with the share of firms doing so rising to 33% (the highest reading outside of May and November 2000). Some of the rise in labor costs are being passed on down the supply chain, with the share of firms raising prices surging to 16% – more than triple last year's level. The share of firms planning to raise worker compensation remained elevated at 19%, but is down 5 points from the nearly three-decade high of 24% in January. Meanwhile, the share of firms planning to raise prices rose 1 point to 25%.

The share of firms making capital outlay plans over the past six months fell from 66% in February to 58%, while plans to do so pulled back 3 points to 26%.

Key Implications

After rising to the highest level since 1983, some pullback in the confidence measure was likely to take place March. Still, the pullback was more acute than expected, with a part of the decline possibly related to rising trade tensions between U.S. and China – which appears to have affected expectations.

Trade tensions have led to rising uncertainty and may have resulted in a softening of recent capital expenditures as well as plans for future capital outlays. Still, we believe that a trade war is not in the cards, and tensions should ease. As they do, we expect the tightening labor market, together with the more competitive tax environment and profit repatriation to support capital investment going forward.

The fact that hiring and compensation trends continue to improve, while the willingness of businesses to hire additional workers remains intact, are all very encouraging elements. As businesses continue to grapple with worker shortages, they are expected to continue boosting worker compensation while also passing on some of the costs to other parts of the supply chain – trends evident in today's report. This bodes well for a pickup in price pressures and strengthens the case for continued monetary policy tightening.

Canada: Housing Starts Dip in March But Remain Elevated

Canadian housing starts edged lower to 225.2k (annualized) units in March, down 2.5% from February's upwardly revised figure (231k) but still an elevated pace of homebuilding. The underlying trend in starts ticked higher to 227k over the last six months.

Single-detached starts advanced 8% to 76.6k units with the gains offset by a decline in the multifamily segment, where starts were down 7% to 148.6k units.

March's drop was concentrated in Ontario (-31k to 75k units). This was expected after starts posted an unsustainable gain in February. Starts also dropped in Nova Scotia (-2.3k to 3.1k units) and Saskatchewan (-1.4k to 2.2k units). On the flip side, starts were higher in most other provinces, led by B.C. (+15.5k to 49.4k units), Newfoundland and Labrador (+5k to 6.3k units) and Alberta (+3k to 37k units). Starts were largely flat in PEI during March.

Starts were down notably in Toronto (-33k to 38.3k units), owing to a drop in the multi-family sector from an unsustainably heated pace. Starts also declined in Montreal (-6.7k to 20.3k units). Conversely, starts were higher in Vancouver (+12.2k to 32.4k units)

Key Implications

Homebuilding continues to defy gravity, with another strong print for starts in March. Over the past six months starts have averaged a solid 227k, with healthy population gains and on-going economic growth providing a boost for demand. Builders are also responding to past increases in pre-construction condo sales, a factor that should provide some support to starts going forward.

In the first quarter, starts averaged 227k, about in line with their fourth quarter level. While new housing construction is holding up, a plunge in home sales suggests that residential investment will subtract notably from Q1 growth.

Going forward, starts will likely ease from their solid Q1 pace, in light of rising interest rates, regulation, and a softer price environment. However, recent permit issuance points to only a gradual moderation.

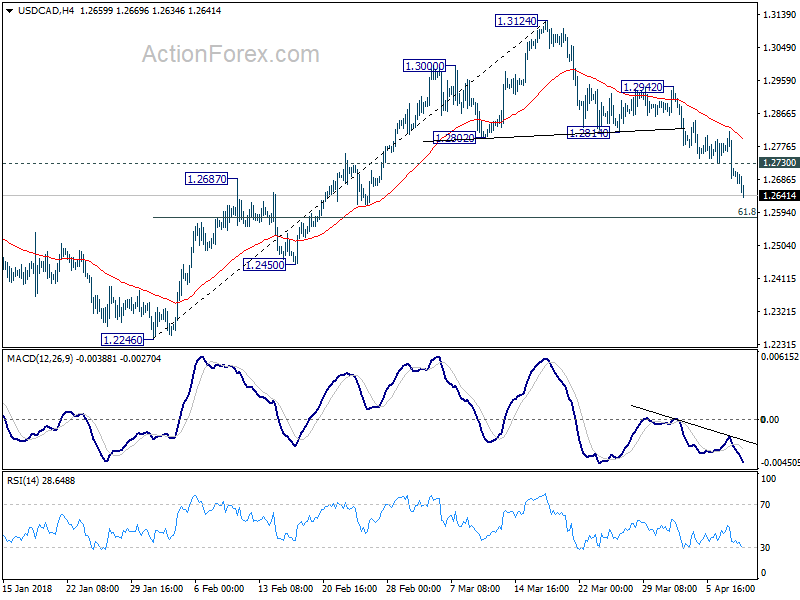

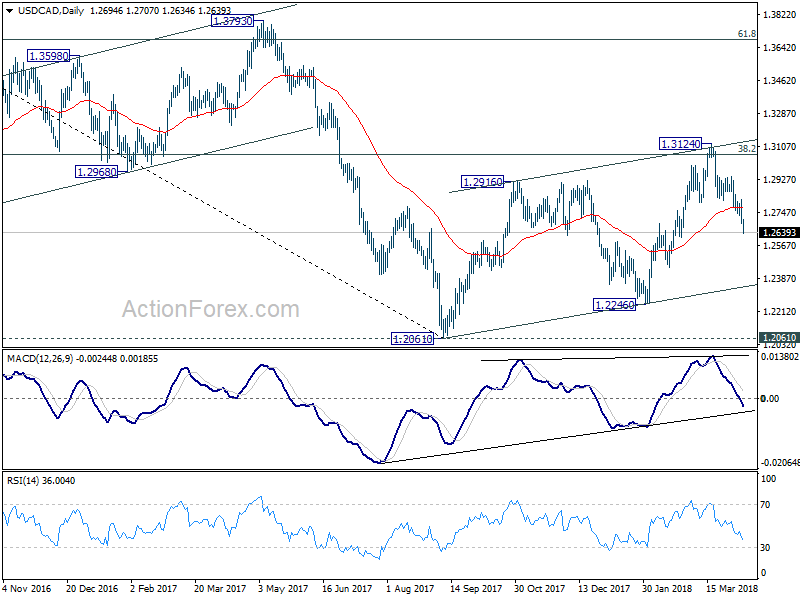

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2649; (P) 1.2733; (R1) 1.2781; More....

USD/CAD drops to as low as 1.2634 so far and intraday bias remains on the downside for 61.8% retracement of 1.2246 to 1.3124 at 1.2581 next. Firm break there will pave the way back to 1.2061/2246 support zone. On the upside, above 1.2730 minor resistance will turn intraday bias neutral first. But near term outlook will remain bearish as long as 1.2814 support turned resistance holds.

In the bigger picture, current development turns favors to the case that rise from 1.2061 is a corrective three wave pattern. It could have completed at 1.3124 after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Focus is now back on 1.2061 and 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

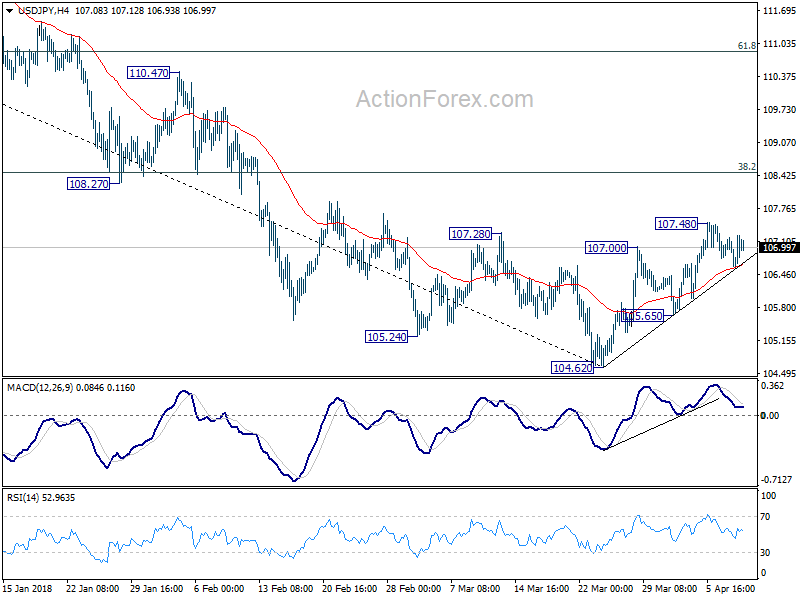

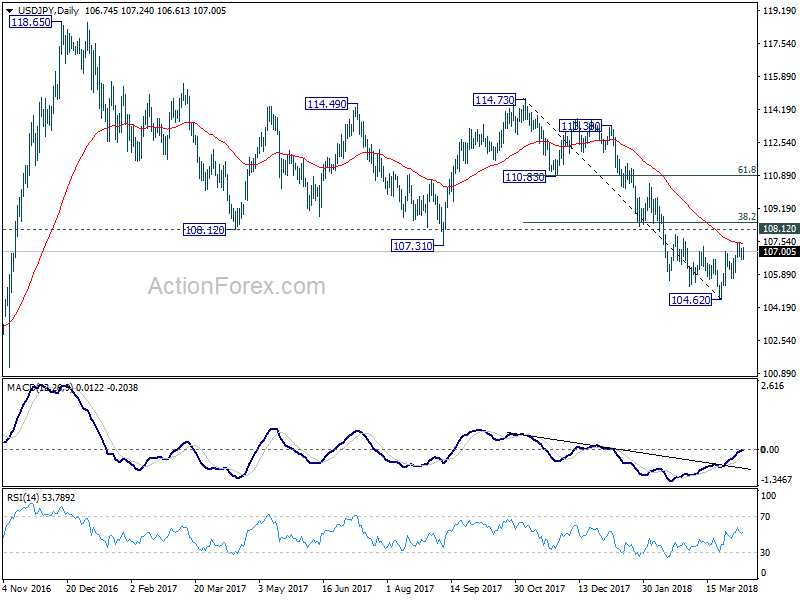

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.50; (P) 106.85; (R1) 107.09; More...

Intraday bias in USD/JPY remains neutral at this point. Above 107.48 temporary top will resume the rebound from 104.62. But reaction from 38.2% retracement of 114.73 to 104.62 at 108.48 is crucial to determine the outlook. Firm break of 108.48 will add some credence to the case of trend reversal. And USD/JPY should target 61.8% retracement at 110.86 next. Nonetheless, rejection from 108.48 (which is close to 108.12 key resistance too), will retain bearishness. Break of 105.65 support will indicate that the rebound is completed and turn bias back to the downside for 104.62 and below.

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

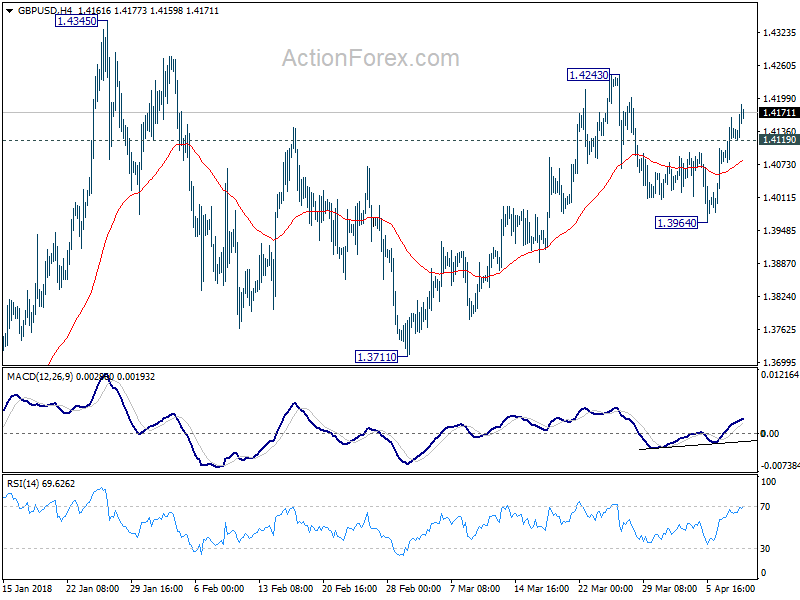

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4085; (P) 1.4124; (R1) 1.4171; More....

GBP/USD's rise continues to as high as 1.4187 so far and intraday bias remains on the upside for 1.4243 resistance first. Break will target a test on 1.4345 high next. On the downside, below 1.4119 minor support will turn intraday bias neutral first. But outlook will stay cautiously bullish as long as 1.3964 support holds.

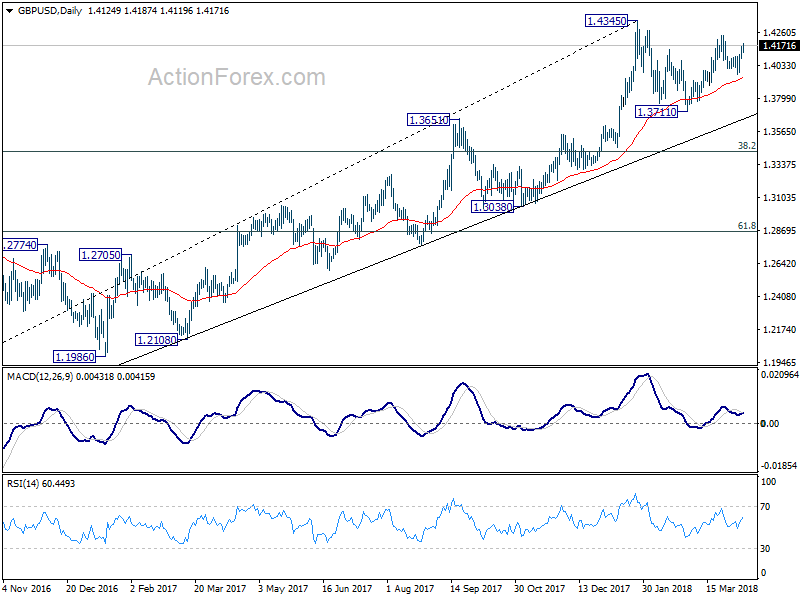

In the bigger picture, as long as 1.3651 resistance turned support holds, medium term outlook in GBP/USD will remain bullish. Rise from 1.1946 is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4267) so far. Break of 1.3651 will be the first sign of medium term reversal and turn focus to 1.3038 support for confirmation.

Yen and Dollar Broadly Lower, Markets on Risk on Mode as Trade War Fear Temporarily Relieved

Japan Yen and, to a slightly lesser extent, Dollar suffer broad based selloff today as global markets return to risk seeking mode. Major European indices are generally higher with DAX up near 1% at the time of writing. CAC is up 0.55% and FTSE is up 0.6%. That followed 0.54% rise in Nikkei earlier today. DOW opens up nearly 400 pts and is back above 24300 handle in initial trading. Generally speaking, investors are relieved that China President Xi Jinping's highly anticipated speech in Boao Forum for Asia didn't ended in escalation in trade tension with the US.

In the currency markets, commodity currencies remain the strongest ones today with New Zealand and Australian Dollar leading the way higher. Euro gets some extra push entering into US session, as boosted by hawkish comments from ECB Governing Council member Ewald Nowotny. Favor is mildly on the Euro's side based on intraday momentum. But so far, EUR/AUD and EUR/CAD are staying in tight range only.

Technically, EUR/USD's break of 1.2344 minor resistance now eliminate the trend reversal scenario. And the actions from February 1.2555 are developing into sideway consolidation pattern only. More upside is now in favor back to 1.2475 resistance and above.

China Xi pledged to open market access

To recap quickly, China Xi sounded calm and balanced in his speech in Boao. He reiterated China's commitment to multilateral framework like G20, and APEC. Xi also pledged on reforms, including lowering restrictions for foreign investment, strengthening adherence to international economic and trade rules, strengthen protection of intellectual property rights and expand imports and promote current account balances. More on Xi's pledge at China Xi Jinping in Boao Forum: Reinforces Ease of Restrictions for Foreign Investment and Protection of Intellectual Property Rights

But it should be noted the pledge to open up the markets have been delivered by various Chinese leaders for two decades but actual delivery has been relatively small. And whatever Xi said, they are still words for the moment. And more importantly, "China still have the option of opening the markets to all but those who don't commit to multilateral frameworks." The messages Xi delivered were to the world rather than the US.

Separately, Bloomberg reported citing a "person familiar with the situation" that China offered to lower its trade surplus to US by USD 50b. But the US raised the stakes by further requesting China to stop subsidizing business related to its "Made in China 2025" initiative, which China rejected. But in our view, this piece of news is more rumor than anything, obtained from unknown source. This news is dismissable.

Dollar retains dominance as world reserve currency

In IMF's latest world FX reserve report, central bank's/reserve managers' demand for US dollar remained intact in 4Q17. This has not only reinforced the greenback's dominant status as the world's reserve currency, but also signaled other currencies still failed to gain widespread confidence due to the economic and/ or financial developments of the corresponding economies. More in USD Dominance Stays Despite Twin Deficits and Threats to Sell Treasury.

Released from the US, PPI rose 0.3% mom, 3.0% yoy in March, much stronger than expectation of 0.1% mom, 2.9% yoy. PPI core rose 0.3% mom, 2.7% yoy, also stronger than expectation of 0.2% mom, 2.6%yoy. But the stronger than expected inflation reading provide no support to Dollar. From Canada, building permits dropped -2.6% mom in February.

ECB Nowotny: It's time for gradual normalization as inflation pressure will eventually materialize

ECB Governing Council member Ewald Nowotny spoke in the European Money and Finance Forum (SUERF) today. Regarding monetary policy, it reiterated that "it is time for a gradual normalization" as inflation pressure will eventually materialize. And he added that the asset purchase program could end this year. But he also emphasized that "this normalization requires a delicate balancing of measures as well as careful sequencing in time." He noted that ECB is now at an "important turning point". While the Eurozone has very strong economic expansion, it's an unequal one.

He stressed that the ECB framework is well equipped to cope with the evolving inflation debate. But still, exit is complex due to the large amount of stimulus in place. Nowotny also repeated all other central bankers have said over time. That is, tightening too soon would stifle recovery. Falling behind the curve would risk creating bubble in assets.

On the topic of trade war, Nowotny warned of the "negative effects for all involved". And, "the direct effects might be on the exchange rate side but this is difficult to see or to forecast because today we have so many linkages, we have long production chains… It might have negative effects on financial stability, but effects on monetary policy are not very clear."

BoE hawk McCafferty: Don't dally when tightening modestly

BoE known hawk Ian McCafferty urged his fellow policymakers not to "dally" when it comes to tightening policy modestly. He is seeing no labor market slack in the economy. In addition, there are modest upside risks to wage growth forecasts presented in the February Quarterly Inflation Report. He added that "It's not wages suddenly bursting away, but it gives you a modest upside risk." Also, McCafferty is concerned on whether import price inflation would fade as the central bank forecasted. On the other hand, he acknowledged that Brexit uncertainty will be a permanent feature of the economic landscape of the UK. While it may hamper long term investments, the impact on short term projects or exports would be small.

Australia NAB business condition dropped sharply from record high, confidence eased

Australia NAB business confidence dropped another 2 pts to 7 in March, down from 9. Business conditions dropped 6 pts from February's record high at 20 to 14. That's 3 points lower than January's 17. Nonetheless, the condition reading remains well above historical average at 5.5. NAB pointed out that the US announcement of tariffs on USD 50b of Chinese imports could have affected sentiments.

NAB saw that "purchase cost growth has been moving higher since late 2016" and that could be "providing a tentative sign of inflationary pressure." On the other hand, "labour cost (wage bill) growth moderated after rising the previous month", which could have offset some of the inflationary pressure.

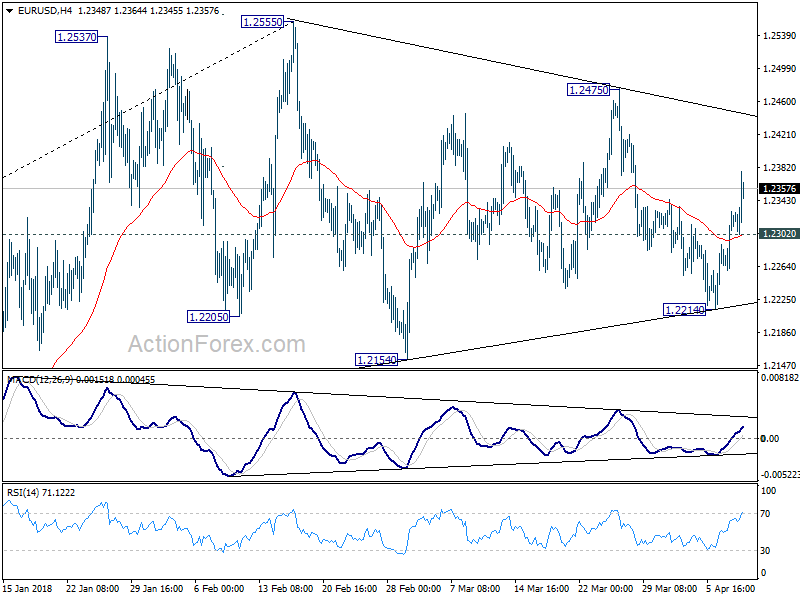

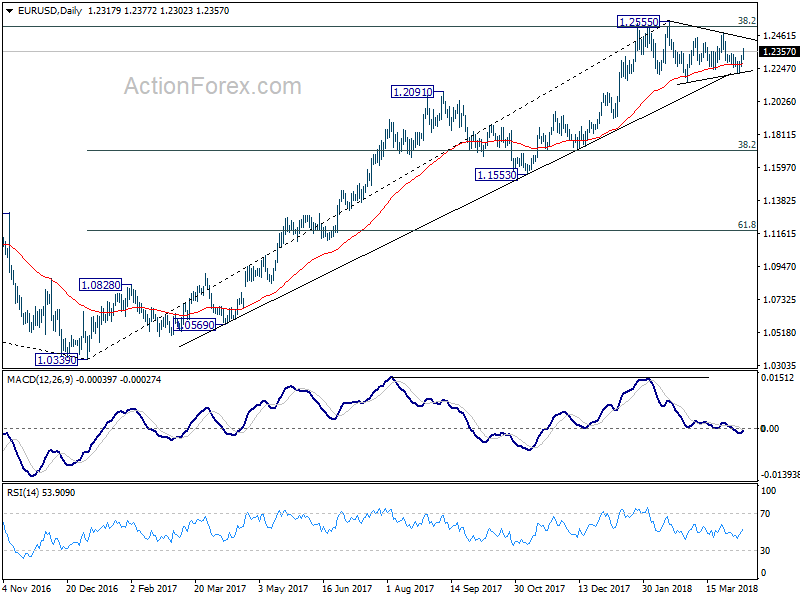

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2277; (P) 1.2303 (R1) 1.2347; More....

EUR/USD's strong rally today and break of 1.2344 resistance firstly indicates the fall from 1.2475 has completed at 1.2214 already. Secondly, it invalidated the bearish case of larger trend reversal. Instead, price actions from 1.2555 high could merely be developing into a sideway consolidation pattern. Intraday bias is back on the upside for 1.2475/2555 resistance zone. We'd be cautious on strong resistance from there to bring another fall to extend sideway trading. On the downside, below 1.2302 minor support will turn bias back to the downside for 1.2214 instead.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y Mar | 1.40% | 0.60% | ||

| 01:30 | AUD | NAB Business Conditions Mar | 14 | 17 | 21 | |

| 01:30 | AUD | NAB Business Confidence Mar | 7 | 12 | 9 | |

| 06:00 | JPY | Machine Tool Orders Y/Y Mar P | 28.10% | 39.50% | ||

| 12:30 | CAD | Building Permits M/M Feb | -2.60% | 1.30% | 5.60% | 5.20% |

| 12:30 | USD | PPI M/M Mar | 0.30% | 0.10% | 0.20% | |

| 12:30 | USD | PPI Y/Y Mar | 3.00% | 2.90% | 2.80% | |

| 12:30 | USD | PPI Core M/M Mar | 0.30% | 0.20% | 0.20% | |

| 12:30 | USD | PPI Core Y/Y Mar | 2.70% | 2.60% | 2.50% | |

| 14:00 | USD | Wholesale Inventories M/M Feb F | 0.60% | 1.10% |

Canadian March housing starts moderate slightly

Highlights:

- March housing starts dropped 2.5% to 225.2k from an upwardly revised 231.0k in February.

- The overall decline mainly reflected urban multiples dropping 7.3% to 144.6k which more than offset urban single-detached units rising 9.5% to 63.7k. Rural starts held steady at 17k.

- Regionally starts in Ontario dropped 30.4% in March to 71.6k though this only partially reversed a cumulative increase of 68.8% over the prior two months that had left February starts at a robust 102.8k.

Our Take:

Canadian housing starts moved lower in March to 225.2k from the 231.0k recorded in February. However, the average level in the first quarter of 224.3k is still representative of strong new residential investment. It is only down slightly from the 229.4k recorded in Q4 which represented the highest level of activity since 2007. This continued strong housing construction activity has persisted despite rising interest rates, more restrictive mortgage lending and poor affordability in a number of key local housing markets. These factors have started to put downward pressure on housing resales so far in 2018. Our expectation is that these factors will start to have a dampening impact on new construction going forward with starts dropping below the 200k level by the end of 2018.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2277; (P) 1.2303 (R1) 1.2347; ....

EUR/USD's strong rally today and break of 1.2344 resistance firstly indicates the fall from 1.2475 has completed at 1.2214 already. Secondly, it invalidated the bearish case of larger trend reversal. Instead, price actions from 1.2555 high could merely be developing into a sideway consolidation pattern. Intraday bias is back on the upside for 1.2475/2555 resistance zone. We'd be cautious on strong resistance from there to bring another fall to extend sideway trading. On the downside, below 1.2302 minor support will turn bias back to the downside for 1.2214 instead.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

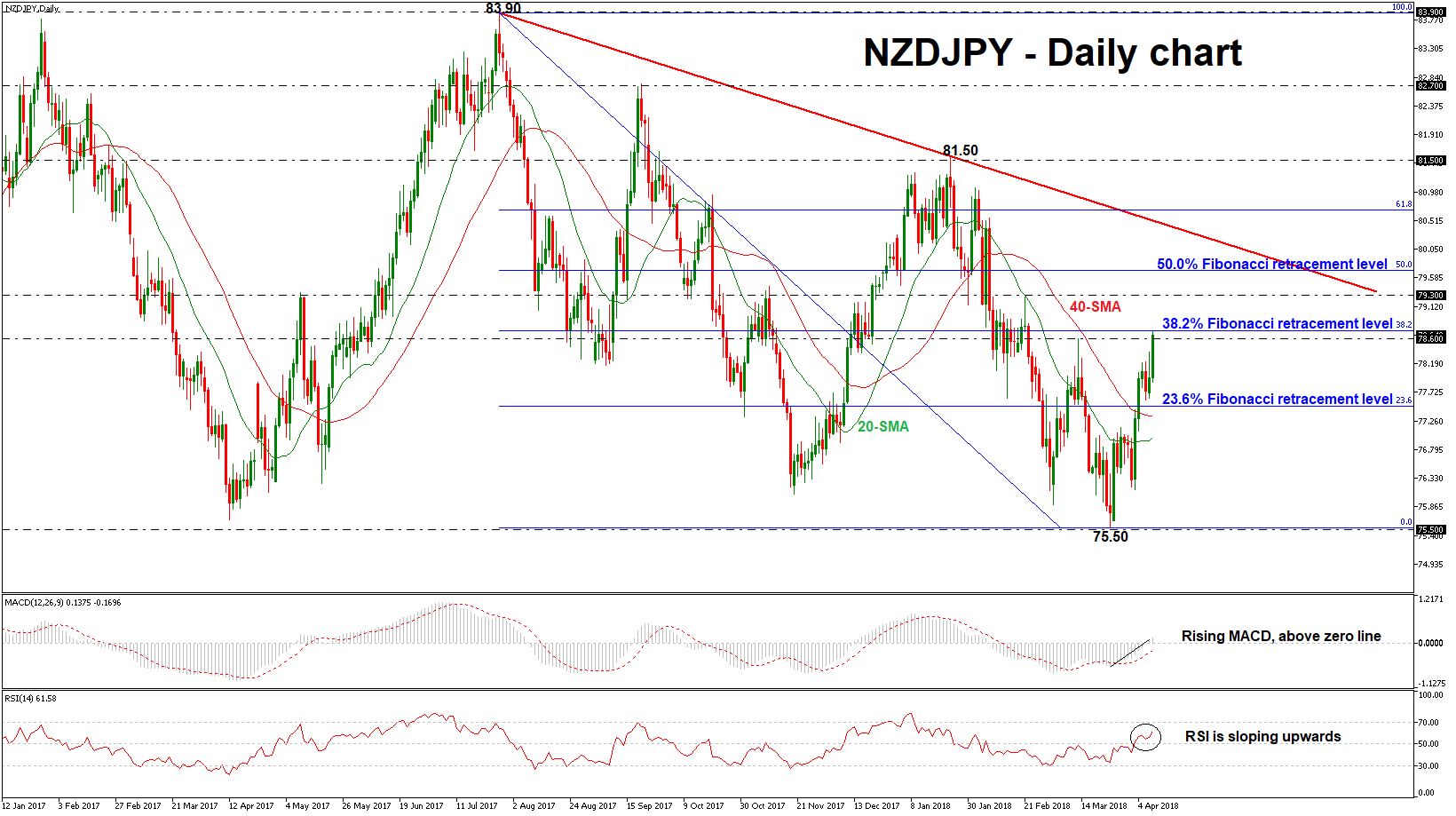

NZDJPY in Sharp Bullish Move in Near Term; Bearish Tendency in Medium Term

NZDJPY has advanced considerably over the last couple of hours and surged towards the 38.2% Fibonacci retracement level around 78.70 of the downleg from the high of 83.90 to the low of 75.50. When looking at the longer-term picture the price has been developing within a descending tendency since the end of July 2017.

Momentum indicators are pointing to a positive bias in the short-term with the MACD oscillator just above the zero line. The Relative Strength Index (RSI) is aggressively sloping to the upside and is approaching the 70 level, suggesting further gains.

In the event of an upside movement, the market could meet resistance at 79.30 in case of a climb above the 38.2% Fibonacci mark. A successful close above this level could see a retest of the 50.0% Fibonacci level near 79.70. A stronger barrier, though, could be found on the falling trend line.

In the wake of negative pressures, the market could meet support at the 23.6% Fibonacci of 77.50. The next key support to watch lower down is the 40 and then the 20 simple moving averages at 77.34 and 76.97 respectively.