Sample Category Title

BoE hawk McCafferty: Don’t dally when tightening modestly

BoE known hawk Ian McCafferty urged his fellow policymakers not to "dally" when it comes to tightening policy modestly.

He is seeing no labor market slack in the economy. In addition, there are modest upside risks to wage growth forecasts presented in the February Quarterly Inflation Report. He added that "It's not wages suddenly bursting away, but it gives you a modest upside risk." Also, McCafferty is concerned on whether import price inflation would fade as the central bank forecasted.

On the other hand, he acknowledged that Brexit uncertainty will be a permanent feature of the economic landscape of the UK. While it may hamper long term investments, the impact on short term projects or exports would be small.

Stocks Rise As China’s President Xi’s Speech Eases Trade Tensions

Notes/Observations

- China President Xi strikes conciliatory tone on trade; makes no reference to possible countermeasures on trade (helped to diffuse tensions)

- European inflation data remains subdued

- US Congressional Budget Office forecasting stronger growth but also significantly wider deficits

Asia:

- China President Xi remarked at Boao conference that China to lower auto and auto product import tariff later this year and open sector to higher foreign ownership; China reform and opening would definitely succeed, world should push for free trade. Cold war mentality was out of place and a zero sum game, isolationism would hit walls

Europe:

- ECB's Coeure (France): growth outlook did not warrant change in monetary policy stance. Growth in the euro zone was not slowing. Interest rates to remain at their current level for a long time even after asset purchases end. We'll do what's needed to bring inflation back to 2%; no need to change the stance now

- ECB's Praet (Belgium, chief economist): inflation developments have stayed subdued - UK Mar BRC Sales LFL Y/Y: +1.4% v -0.3%e (Note: Easter holiday sales took place in March rather than April)

Americas:

- Fed’s Kaplan (dove, non-voter) reiterated view that base case was three interest rate increases in 2018. Interest rate path likely a little bit flatter in 2019.

- Congressional Budget Office (CBO) Budget and Economic Outlook: US Federal budget deficits will grow substantially over the next few years, then stabilize in 2023. Forecasted $1T budget deficit in 2020 (2 years earlier than previously anticipated)

- President Trump meeting with North Korea Leader Kim to be held in May or early June, hoped to reach a denuclearization deal. US has been in touch with North Korea govt. - President Trump: to make major decisions on Syria in the next 24-48 hours

Economic Data:

- (NL) Netherlands Mar CPI M/M: 0.2% v 0.5% prior; Y/Y: 1.0% v 1.2% prior

- (NL) Netherlands Mar CPI EU Harmonized M/M: 0.2% v 1.1%e; Y/Y: 1.0% v 1.8%e

- DK) Denmark Mar CPI M/M: 0.0% v 0.3%e; Y/Y: 0.5% v 0.8%e

- (DK) Denmark Mar CPI EU Harmonized M/M: 0.0% v 0.3%e; Y/Y: 0.4% v 0.7%e

- (NO) Norway Mar CPI M/M: 0.3% v 0.6%e; Y/Y: 2.2% v 2.4%e

- (NO) Norway Mar CPI Underlying M/M: 0.2% v 0.6%e; Y/Y: 1.2% v 1.4%e

- (NO) Norway Mar PPI including Oil M/M: +0.5% v -2.6% prior; Y/Y: 6.4% v 4.7% prior

- (FI) Finland Feb Industrial Production M/M: -1.2% v +0.1% prior; Y/Y: 3.4% v 4.8% prior

- (JP) Japan Mar Preliminary Machine Tool Orders Y/Y: 28.1% v 39.5% prior

- (FR) France Feb Industrial Production M/M: 1.2% v 1.4%e; Y/Y: 4.0% v 4.3%e

- (FR) France Feb Manufacturing Production M/M: -0.6% v +0.7%e; Y/Y: 2.4% v 4.3%e

- (CZ) Czech Mar CPI M/M: -0.1% v 0.0%e; Y/Y: 1.7% v 1.7%e

- (CZ) Czech Mar Unemployment Rate: 3.5% v 3.5%e

- (HU) Hungary Mar CPI M/M: 0.1% v 0.1%e; Y/Y: 2.0% v 2.1%e

- (SE) Sweden Feb Household Consumption M/M: 0.5% v 0.1% prior; Y/Y: 1.7% v 1.2 % prior

- (IT) Italy Feb Industrial Production M/M: -0.5% v +0.8%e; Y/Y: 2.4% v 7.6% prior; Industrial Production WDA Y/Y: 2.5% v 4.7%e

- (TW) Taiwan Mar CPI Y/Y: 1.6% v 1.7%e; CPI Core Y/Y: 1.5% v 1.3%e, WPI Y/Y: +0.5% v -0.2% prior

Fixed Income Issuance:

- (IE) Ireland Debt Agency (NTMA) opened its book to sell EUR-denominated 15-year bond; guidance seen +5bps to mid-swaps

- (EU) EFSF opened its book to sell €3.0B in 8-year notes; guidance seen -17bps to mid-swaps

- (NL) Netherlands Debt Agency (DSTA) sold €2.005B vs. €1.5-2.5B indicated range in 0% Jan 2024 DSL Bond; Avg Yield: 0.087% v 0.052% prior

- (ID) Indonesia sold total IDR21.85T vs. IDR17T target in 3-month, 12-month Bills, 5-year, 10-year and 15-year Bonds

- (ES) Spain Debt Agency (Tesoro) sold total €1.295B vs. €1.0-2.0B indicated range in 3-month and 9-month Bills

- (AT) Austria Debt Agency (AFFA) sold total €1.0B vs. €1.0B indicated in 2028 and 2037 RAGB bond

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.6% at 377.6, FTSE +0.4% at 7221, DAX +1.0% at 12387, CAC-40 +0.7% at 5300, IBEX-35 +0.3% at 9767, FTSE MIB +0.3% at 23120, SMI +0.5% at 8730, S&P 500 Futures +1.1%]

- Market Focal Points/Key Themes: European Indices trade higher across the board being led by the Dax on gains from Bayer and Auto names, as Indices trade higher on higher US futures. Overall sentiment has been helped by comments from China's President Xi paving the way for China to lower auto and auto product import tariff later this year. On the earnings front Christian Dior and LVMH trade sharply higher after strong results, while Givaudan trades lower after reporting inline results. Sequana is another notable faller after declining profits and a suspension of its dividend, whilst Air France trades over 1% lower after their March metrics and warning on full year profits following the recent strike action. Looking ahead earnings include MSM Industrial and Simply Good Foods.

Movers

- Consumer Discretionary [Givaudan [GIVN.CH] -4.2% (Earnings), Christian Dior [C.FR] +3.8% (Earnings), LVMH [MC.FR] +5.2% (Earnings), Air France [AF.FR] -1.6% (Mar Metrics)]

- Industrials [ Sequana [SEQ.FR] -7% (Earnings), Daimler [DAI.DE] +1.7%,BMW [BMW.DE] +2.5%, Volkswagon [VOW3.DE] +1.9% (China President Xi comments regarding auto tariffs)]

- Healthcare [Bayer [BAYN.DE] +4.1% (Reportedly the US set to approve deal with Monsanto with consessions)]

- Energy [TGS-Nopec Geophsical Company [TGS.NO] +13% (Prelim results)]

Speakers

- BOE's McCafferty (dissenter): Brexit uncertainty hampering longer-term investment; uncertainty would be a permanent feature in the economic landscape. Must not dilly dally over the next rate hike and saw no labor market slack. He saw modest upside risk to BOE's Feb wage growth forecasts

- BOE’s Haldane: Policy had not worsened income inequality. No clear shift in wealth

- ECB’s Nowotny (Austria): At an important turning point in monetary policy; must normalize policy not too soon nor too late. Expansion has been strong but unequal one

- ECB's Villeroy (France) stated that France must address the high level of spending by the govt; French level was higher than average in Euro region

- ECB’s Nouy (SSM member): Still room for improvement in risk appetite framework

- ECB bank supervision official Donnery: NPL loan sale can be part of the solution

- Bank of France maintained its 2018 GDP growth forecast at 1.9%. Domestic economy still needed to increase its growth potential but saw no risk to growth from trade tensions

- Czech Central Bank Gov Rusnok reiterated view that would continue with its tightening

- Russia Central Bank (CBR) Gov Nabiullina: Ready to reduce the RUB currency (Ruble) effect on inflation. Sanctions did effect Russia and needed to adopt to external changes. Took time for markets and economy to get use to sanctions but Russia had a wide range of tools to address the situation

- China-US talks said to have stalled over high-tech issues. US asked China to stop subsidizing high-tech industry. US rejected offer from China to reduce trade deficit by $50B. China said to be considering trade concessions for Europe and Mexico

- IEA's Atkinson: 2018 oil demand growth seen between 1.4-1.5M bpd. Believed that US was not at peak oil production

- Fed’s Kaplan (dove, non-voter) commented from Beijing that the US economy 2018 GDP growth was seen between 2.50-2.75% and 2019 a tad softer. Business investment should be stronger on tax reform. Had to be gradual and patient in raising rates in light of headwinds

Currencies

- European inflation and growth data both continued to be subdued in the session. CPI data from Netherlands, Hungary and Czech Republic came in below expectations while French Feb Industrial Production missed its consensus view. EUR/USD remains steady in its price action and hold above the 1.23 level and in the mid-range of its 2018 overall trading band.

- GBP was firmer in the session as BOE's McCafferty (dissenter) saw saw modest upside risk to BOE's Feb wage growth forecasts. GBP/USD higher by 0.3% at 1.4175 just ahead of the NY morning.

- NOK currency (Krona) was softer after Norway Mar CPI missed expectations. Norges has been stated that the 1st potential rate hike could come after the summer but today inflation data took some momentum from that view.

- Safe haven flows saw some unwind after China President Xi struck a conciliatory tone on trade and made no reference to possible countermeasures on US tariffs. Cyclical currencies like AUD and NZD werer firm as Xi’s remarks helped to reduce trade tensions.

- The RUB currency (Ruble) continued its plunge in the aftermath of fresh US sanctions. The Ruble has lost approx. 7% this week. USD/RUB trading around the mid-62 area

Fixed Income

- Bund Futures trade 12 ticks lower at 159.34 as Xi speech eases trade tension. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 122.21 lower by 15 ticks continuing the respect of the 123 handle. Support continues stands at 121.25 then 120.85, with upside resistance at 123.35 then 123.85.

- Tuesday’s liquidity report showed Monday's excess liquidity rose to €1.865T from €1.864T prior. Use of the marginal lending facility rose from €0M to €404M.

- Corporate issuance saw 5 issuers raised $5.08B in the primary market

Looking Ahead

- (PT) Bank of Portugal Reports Mar ECB financing to Portuguese Banks: No est v €22.0B prior

- (UR) Ukraine Mar CPI M/M: 0.9%e v 0.9% prior; Y/Y: 13.2%e v 14.0% prior

- (AR) Argentina Central Bank (BCRA) Interest Rate Decision: Expected to leave 7-Day Repo Reference rate unchanged at 27.25%

- (MX) Mexico Mar ANTAD Same-store Sales Y/Y: No est v 4.8% prior

- (MX) Mexico Mar Nominal Wages: No est v 5.6% prior

- (SI) Slovenia Debt Agency to sell Bills

- 05.30 (UK) Weekly John Lewis LFL sales data - 05:30 (UK) BOE’s Haldane in Melbourne

- 05:30 (EU) ECB allotment in 7-day Main Financing Tender

- 05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

- 05:30 (DE) Germany to sell €500M in 0.1% inflation-linked 2026 bonds (Bundei)

- 05:30 (UK) DMO to sell £2.0B in 1.75% July 2057 Gilts

- 05:30 (BE) Belgium Debt Agency (BDA) to sell €1.4-1.8B in 6-month and 12-month Bills

- 05:30 (ZA) South Africa to sell combined ZAR2.4B in 2030, 2035 and 2048 bonds

- 06:00 (US) Mar NFIB Small Business Optimism: 107.0e v 107.6 prior

- 06:00 (IE) Ireland Feb Industrial Production M/M: No est v -2.6% prior; Y/Y: No est v -2.8% prior

- 06:45 (US) Daily Libor Fixing

- 07:00 (ZA) South Africa Feb Manufacturing Production M/M: +0.5%e v -1.6% prior; Y/Y: 2.1%e v +2.5% prior

- 07:00 (CZ) Czech Central Bank to comment on CPI data

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:00 (HU) Hungary Central bank (NBH) Mar Minutes

- 08:00 (BR) Brazil Mar IBGE Inflation IPCA M/M: 0.1%e v 0.3% prior; Y/Y: 2.7%e v 2.8% prior

- 08:00 (BR) Brazil CONAB Crop Report

- 08:00 (RU) Russia announces weekly OFZ bond auction

- 08:05 (UK) Baltic Dry Bulk Index

- 08:15 (CA) Canada Mar Housing Starts: 218.0Ke v 229.7K prior

- 08:30 (US) Mar PPI Final Demand M/M: 0.1%e v 0.2% prior; Y/Y: 2.9%e v 2.8% prior

- 08:30 (US) Mar PPI Ex Food and Energy M/M: 0.2%e v 0.2% prior; Y/Y: 2.6%e v 2.5% prior

- 08:30 (US) Mar PPI Ex Food, Energy, Trade M/M: 0.2%e v 0.4% prior; Y/Y: No est v 2.7% prior

- 08:30 (CA) Canada Feb Building Permits M/M: No est v 5.6% prior

- 08:55 (US) Weekly Redbook Sales

- 09:00 (EU) Weekly ECB Forex Reserves

- 09:00 (RU) Russia Q1 Preliminary Current Account: $29.5Be v $13.7B prior

- 09:45 (UK) BOE to buy £1.22B in in APF Gilt purchase operation (over 15-years)

- 10:00 (US) Feb Final Wholesale Inventories M/M: 0.8%e v 1.1% prelim, Wholesale Trade Sales M/M: No est v -1.1% prior

- 11:30 (IT) ECB’s Visco (Italy) in Rome

- 11:30 (US) Treasury to sell 4-Week Bills

- 12:00 (US) DOE Short-Term Crude Outlook

- 12:00 (US) USDA World Agricultural Supply and Demand Estimate (WASDE) Crop Report

- 13:00 (US) Treasury to sell 3-Year Notes

- 16:30 (US) Weekly API Oil Inventories

ECB Nowotny: It’s time for gradual normalization as inflation pressure will eventually materialize

European Central Bank (ECB) Governing Council member Ewald Nowotny spoke in the European Money and Finance Forum (SUERF) today. .

Regarding monetary policy, it reiterated that "it is time for a gradual normalization" as inflation pressure will eventually materialize. But he also emphasized that "this normalization requires a delicate balancing of measures as well as careful sequencing in time." He noted that ECB is now at an "important turning point". While the Eurozone has very strong economic expansion, it's an unequal one.

He stressed that the ECB framework is well equipped to cope with the evolving inflation debate. But still, exit is complex due to the large amount of stimulus in place. Nowotny also repeated all other central bankers have said over time. That is, tightening too soon would stifle recovery. Falling behind the curve would risk creating bubble in assets.

On the topic of trade war, Nowotny warned of the "negative effects for all involved". And, "the direct effects might be on the exchange rate side but this is difficult to see or to forecast because today we have so many linkages, we have long production chains... It might have negative effects on financial stability, but effects on monetary policy are not very clear."

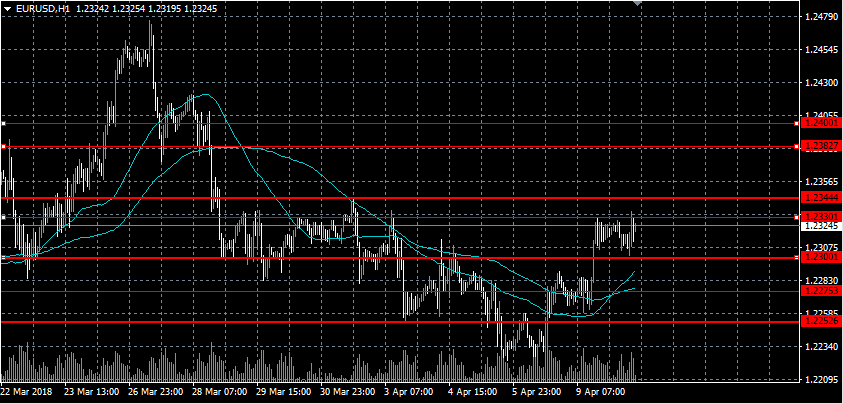

Next Euro Upmove Above 1.2344 Level

The euro continues to maintain upside pressure against the U.S dollar, with price-action still well support above the 1.2300 handle and creating bullish higher daily price-highs. The EURUSD has yet to move above the 1.2344 resistance level, despite other major currencies pairs breaking above key short-term trading ranges. Traders now look toward the release of monthly PPI inflation figures from the U.S economy, with the 1.2382 level the key EURUSD resistance level to watch.

The EURUSD pair retains a bullish trading bias while trading above the 1.2300 level, the 1.2344 and 1.2382 levels remain the key top-side resistance levels to watch.

Should the EURUSD pair decline below the 1.2300 level, price-action will turn bearish, with short-term support then found at the 1.2275 and 1.2252 levels.

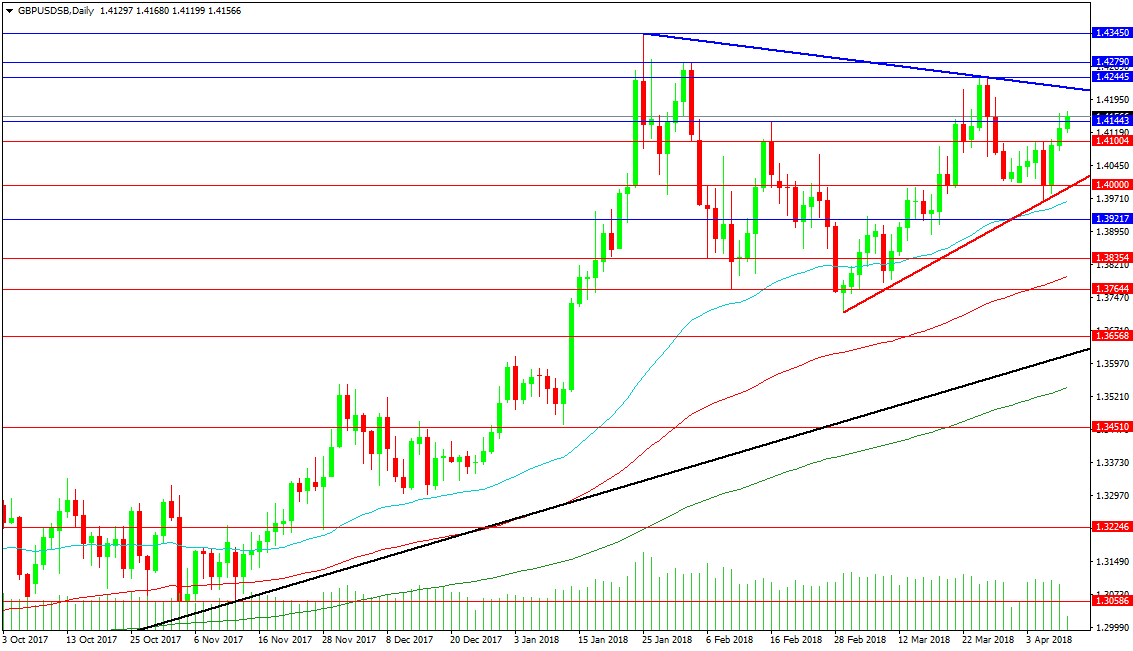

GBPUSD Buyers Looking To Test 1.4200 Level

The British pound continues to trade sharply higher against the U.S dollar, with price-action hitting 1.4175, as buyers edge ever closer to the key 1.4200 resistance level. The move higher in the GBPUSD pair has been sparked by overall U.S dollar weakness, and bullish comments on future rate hikes by BOE voting member McCafferty this morning. Moving into the U.S session, traders look towards the release of U.S PPI inflation data and rising tensions between western and Russian governments.

The GBPUSD pair is strongly bullish while trading above the 1.4146 level, further upside towards the 1.4200 and 1.4243 levels seems possible.

Should price-action on the GBPUSD pair trade below the 1.4146 level, a correction towards the 1.4116 and 1.4088 levels seems possible.

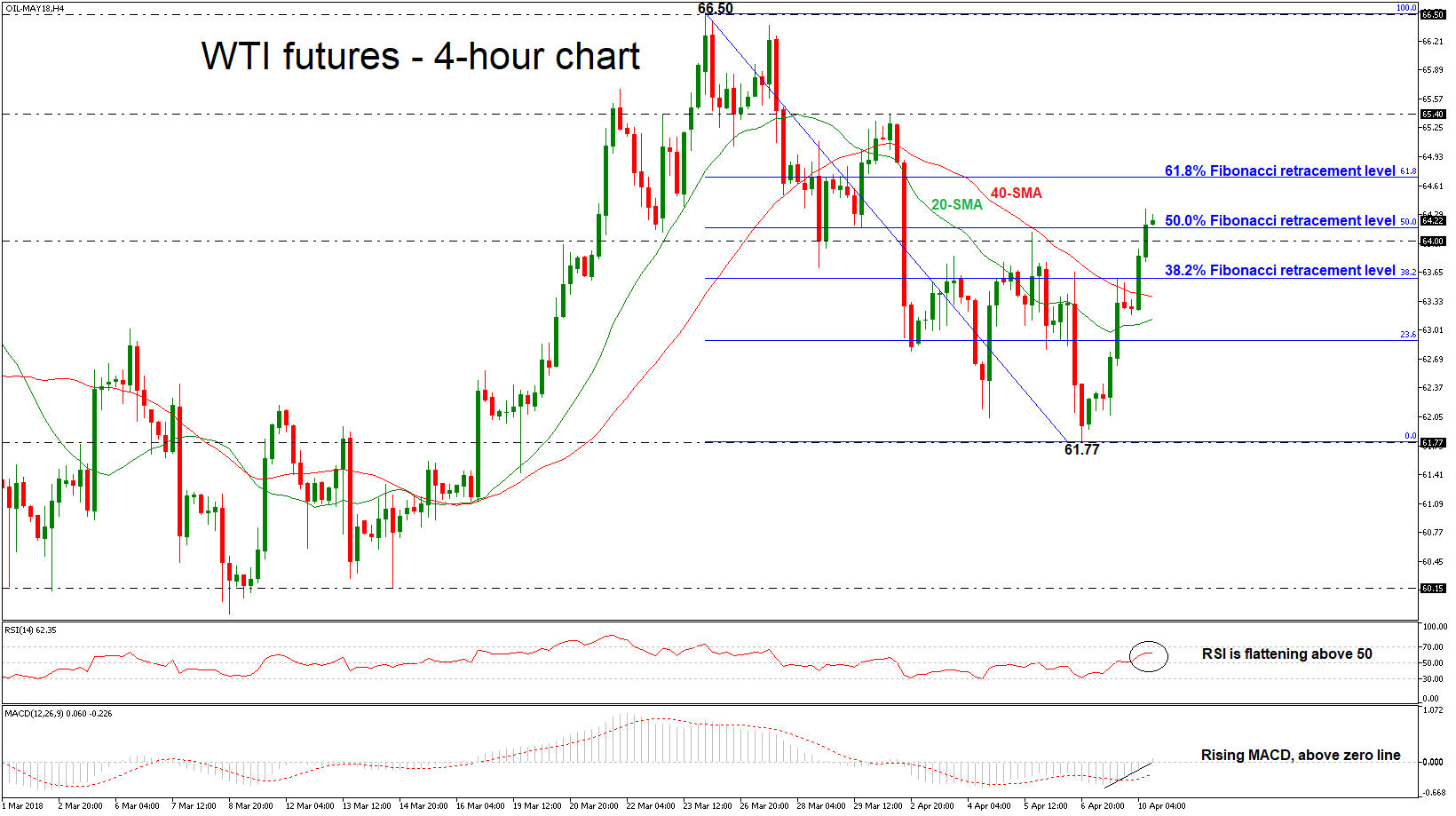

WTI Crude Oil Futures In Strong Upside Movement After Rebound On 61.77

WTI crude oil futures have come under renewed buying interest, rising back above the 64.00 strong psychological level. After the significant rebound on the 61.77 support, the price reversed and is trying to pare some of the previous week’s losses. Oil prices jumped to a new one-week high and challenged the 64.35 price level during today’s European session.

Looking at momentum oscillators in the 4-hour chart, they suggest further bullish movements may be on the cards in the short-term. The Relative Strength Index (RSI) is above its neutral 50 line, detecting positive momentum, but is flattening. The MACD oscillator has just entered positive ground as it was rising from the bearish territory.

In case of further upside pressure, immediate resistance may be found near the 61.8% Fibonacci retracement level around 64.70 of the downleg from 66.50 to 61.77. If buyers manage to push the price above that hurdle, that would mark a higher intraday high in the 4-hour chart, increasing the probability for further bullish extensions. Resistance may be found initially at 65.40, identified by the April 2 top.

Conversely, if the bears retake control, prices advances may stall and slip below the 64.00 handle. The next support level to have in mind is the 38.2% Fibonacci mark near 63.58. A drop below the aforementioned obstacle could open the way towards the 40 and 20 simple moving averages at 63.37 and 63.14 respectively.

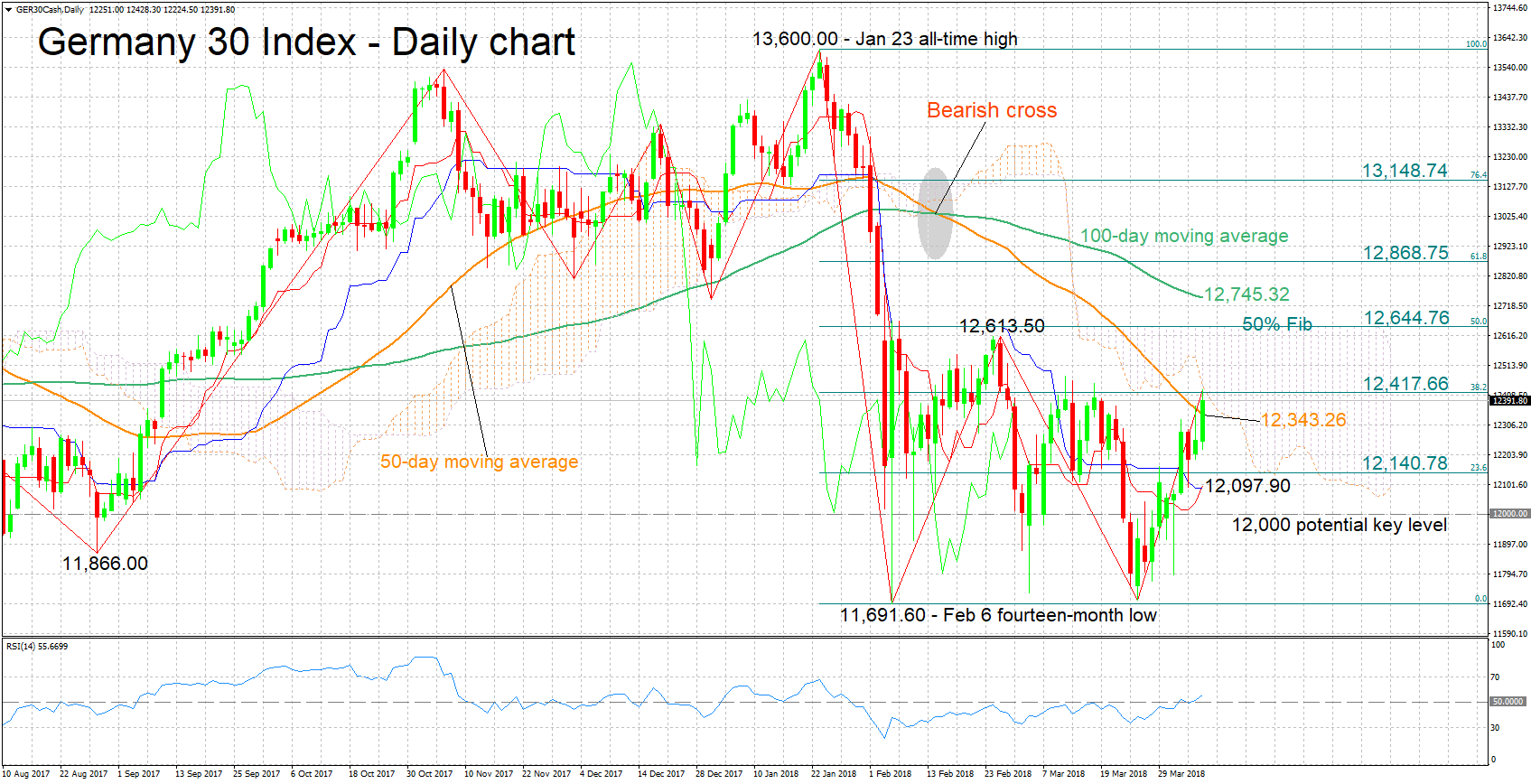

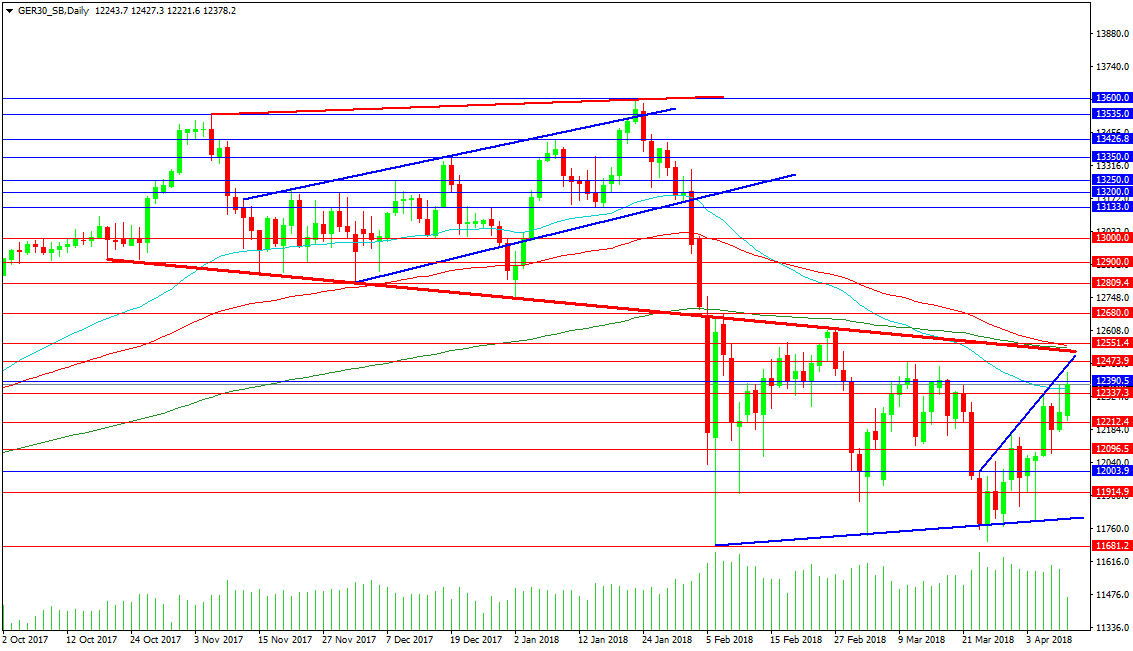

GER 30 Index Crosses Above 50-Day MA To Record 4-Week High, Challenges Ichimoku Cloud Bottom

The Germany 30 index has advanced considerably after hitting a two-month low of 11,703.80 on March 26 and coming close to the more than one-year trough of 11,691.60 recorded in early February. Earlier on Tuesday, the index posted a near four-week high of 12,428.30.

In terms of the short-term picture, the Tenkan-sen line has just crossed above the Kijun-sen, this being a positive alignment that supports a bullish bias. The RSI lends credence to this view: the indicator continues to rise, having moved above the 50 neutral-perceived level.

Resistance might be taking place at the moment around the 38.2% Fibonacci retracement level of the January 23 to February 6 downleg at 12,417.66. The area around this level encapsulates the Ichimoku cloud bottom (12,440.48), while it was somewhat congested in recent months. An upside break from this area would shift the attention to the range around the 50% Fibonacci mark at 12,644.76.

On the downside, support could come around the current level of the 50-day moving average at 12,343.26 which failed to act as resistance earlier in the day and might instead provide support. In case of steeper declines, the focus would start to turn increasingly to the 23.6% Fibonacci level at 12,140.78.

The medium-term picture is looking mostly bearish, with trading taking place below the Ichimoku cloud and the 50- and 100-day MA lines maintaining a negative slope – a bearish cross has been in place since mid-February when the 50-day MA moved below the 100-day one as well. However, a more decisive break above the 50-day MA, one that sends price action inside the Ichimoku cloud, would be indicative of a neutral outlook for the index.

Overall, the short-term picture is positive, with the medium-term being negative for the most part though with a neutral tilt as well.

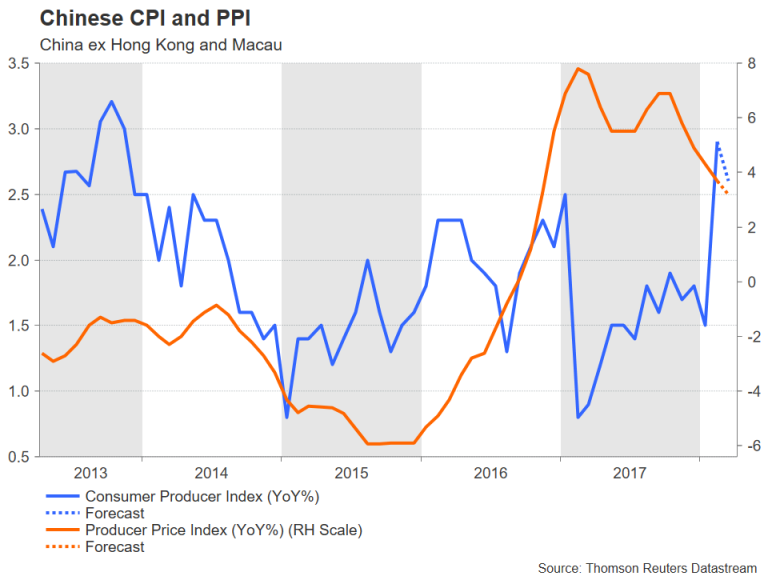

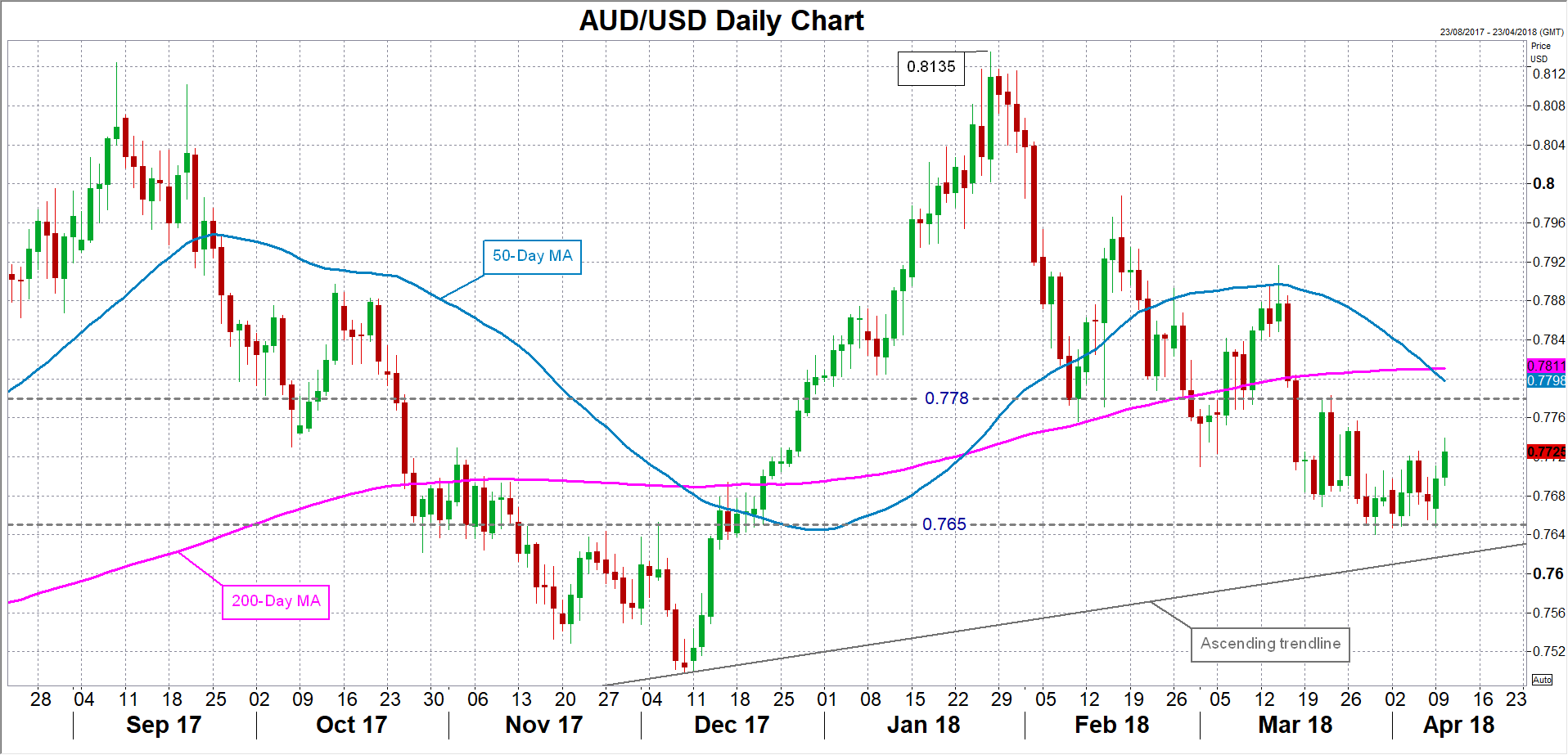

China Prices To Ease In March After Lunar New Year Distortion, Yuan Firmer Amid Trade Friction

China's National Bureau of Statistics will publish inflation data on Wednesday consisting of the consumer and producer price indices. While both the CPI and PPI rates are expected to moderate in March, investors will be wary of any unexpected weakness in price pressures in the world's second largest economy amid an escalating trade spat with the United States.

The annual rate of CPI is forecast to ease by 0.3 percentage points to 2.6% in March, remaining below the People's Bank of China's (PBOC) target of around 3%. Inflation had jumped from 1.5% to 2.9% in February, mainly due to the effects of the Lunar New Year, which caused a one-off bump in food and travel costs. However, apart from the holiday distortion, there are few upside pressures on consumer prices on the horizon, especially as the economy is expected to slow this year, and inflation looks set to remain below the central bank's target for a while longer. The 12-month CPI rate has been below 3% since late 2013.

The more closely watched item in tomorrow's data will be producer prices, which are seen as a good indicator of demand for commodities and the profitability of China's industrial sector. Factory inflation surged in late 2016/early 2017, fuelling the global reflation trade and alleviating deflationary pressures around the world. However, PPI is forecast to moderate for the fifth straight month in March to 3.2% year-on-year from 3.7%.

A bigger-than-expected fall in the PPI rate would raise concerns of weakening demand for Chinese imports of commodities and signal softer prices for Chinese manufactured goods exported to the rest of the world, boding negatively for global inflation. The Australian dollar is the most sensitive to any surprises in tomorrow's inflation indicators as Australia is a major exporter of commodities to China.

Disappointing numbers could see the aussie re-testing recent support around the $0.7650 level and heading back towards its longer-term ascending trend line. However, stronger-than-expected readings could lift the aussie towards the $0.7780 resistance level.

The yuan could also see some volatility from the inflation data, having come into focus this week after a Bloomberg report said China was considering the possibility of a gradual depreciation of its currency to use as a tool in its trade stand-off with the US. The US dollar spiked to 6.3168 yuan in onshore trading from an earlier low of 6.2940 after the report emerged, but later fell back to close lower on the day. The yuan is even firmer today, last trading around 6.2920 per dollar, possibly on intervention by the PBOC to counter speculative trade.

A speech by China's President Xi Jingping earlier on Tuesday also probably contributed to the yuan extending its gains. Speaking at the Boao Forum for Asia, President Xi promised to increase access for foreign investors to the Chinese market as well as lower import tariffs for key sectors such as automobiles. Xi also pledged to improve legislation on protecting ownership of intellectual property – a big cause of conflict with US President Trump. His proposals, while lacking much detail, calmed market fears of an imminent trade war between the US and China and raised hopes of a negotiated solution.

China looks set to remain in the headlines until the end of the week as March trade figures are released on Friday, which will include monthly export and import performance.

Forex Analysis: GBPUSD And GER30

The GBPUSD pair is breaking higher today, after managing to close above the 1.41000 level yesterday. This move gives long positions a bit of confidence, with the falling blue trend line at 1.42162 the main obstacle on the way to the high of 1.43450. There is also a band of resistance between the 1.42445 and 1.42790 levels but a solid break of the trend line could be enough to carry the price higher regardless.

Support comes at the previously mentioned 1.41000 level, which is acting as a point of control. Should price fall below this level, the rising trend line at 1.40000 comes into focus. The 50 DMA is positioned to provide support at 1.39640, with the 1.39217 level below that. The 100 DMA is at 1.37940 with support at 1.38354. A strong level of support is found at 1.37644 and, should this be broken, a retest of the rising black trend line support at 1.36140 may occur.

GER30 Index

Price remains below the descending red trend line that has dominated the chart for the last few months. This trend line is supported by the 100 and 200 DMAs and the 12550.00 level. A move back above this area, in conjunction with the risk-on sentiment in the broader market, would be a bullish development for this index. In the meantime, the 12390.00 level is acting as resistance, with price testing the area this morning on a strong rebound after yesterday’s late selloff in the US session. The 12473.9 level is providing short-term resistance as the high from early March.

Support comes from the 50 DMA at 12357.80, with the 12337.30 level close by. This is followed by 12212.40 and the 12100.00 area, with further support at 12000.00 and 11915.00. The supporting blue trend line is located at 11800.00 with the 11681.20 level holding the way to 11500.00.

CRUDE OIL Trading Above 64

Crude oil recovery phase started at 61.81 continues, approaching the 64.35 range. The bullish pattern started in November 2017 is somewhat weakened since recent decline started at the end of March. Crude oil is contained between hourly support and resistance at 61.34 (08/01/2018 low) and 64.67 (30/01/2018 high). The technical structure suggests short-term increase.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading above its 200 DMA.