Sample Category Title

EURUSD: Strengthens, Extends Bull Pressure

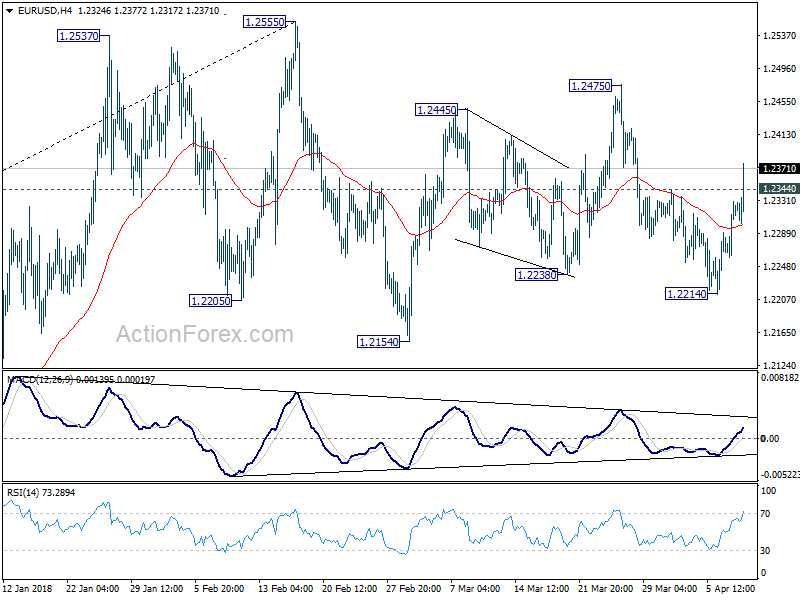

EURUSD: The pair faces further recovery higher as it was seen following through higher on the back of Monday gain on Tuesday. On the upside, resistance comes in at 1.2400 level with a cut through here opening the door for more upside towards the 1.2450 level. Further up, resistance lies at the 1.2500 level where a break will expose the 1.2550 level. Its daily RSI is bullish and pointing higher suggesting further strength. Conversely, support lies at the 1.2300 level where a violation will aim at the 1.2250 level. A break of here will aim at the 1.2200 level. Below here will open the door for more weakness towards the 1.2150. All in all, EURUSD faces further upside threats.

Canadian Dollar at 6-Week High as Risk Appetite Improves

The Canadian dollar continues to post gains in the Tuesday session, after starting the week with strong gains. Currently, USD/CAD is trading at 1.2665, down 0.27% on the day. On the release front, Canadian construction indicators are in focus, with the markets braced for soft data. Building Permits is forecast to decline 1.5%, after two straight gains. Housing Starts are expected to drop sharply to 219 thousand. In the US, PPI is expected to edge lower to 0.1%, and Core PPI is forecast to remain unchanged at 0.2%. On Wednesday, the US releases consumer inflation reports and the Federal Reserve will publish the minutes of its March rate meeting.

The Bank of Canada Business Outlook Survey pointed to a generally upbeat business sector, and this helped boost the Canadian dollar on Monday. The survey found widespread intention by companies to increase investment and hiring, and “forward-looking sales indicators remain positive across most regions and sectors”. Still, the report is unlikely to change the current sentiment that the BoC will maintain rates at next week’s policy meeting.

Investors are breathing a sigh of relief after Chinese President Xi Jimping sent out a conciliatory message earlier on Tuesday. Xi was speaking at a development conference in China, and promised to lower tariffs on vehicle imports into China. This has been a major sticking point between the US and China, with President Trump complaining that China has a 25% tariff on US vehicle imports, yet the US only charges 2.5% on Chinese vehicles. Although China has previously declared that it would reduce the tariffs on vehicles, the markets were looking for some positive news, as the trade battle between the two largest economies in the world has shaken the markets in recent weeks. Xi added that China was looking to solve issues through dialogue rather than confrontation, and the markets are hoping that the US and China can avert a trade war, which could drag down the global economy.

On Friday, the US released a very soft nonfarm payroll report. The indicator fell to 103 thousand, well off the forecast of 188 thousand. Still, the markets do not appear overly concerned, as payroll reports often sag in March. On a more positive note, wage growth improved to 0.3%, up from 0.1% a month earlier. This release matched the estimate. The improvement is likely to reinforce sentiment that the Fed could press the rate trigger four times in 2018, which could push the US dollar higher.

AUD & NZD strong on risk appetite, but EUR overtaking

The financial markets are generally on risk on mode today as Chinese President Xi Jinping's speech in Boao eased the fear of immediately escalation of trade tension with the US. Nikkei closed up 0.54%, HSI closed up 1.65%. At the time of writing, DAX is up 0.8%, CAC up 0.5% and FTSE up 0.55%. US futures also point to higher open.

In the forex markets, it's typical in such risk on mode that Aussie and Kiwi are strong while Yen is weak, as seen in the D heatmap. But it also revealed that USD is getting no support from investors' optimism. And the USD is somewhat dragging down CAD too.

The top movers table revealed pretty much the same picture. In particular, NZDJPY is the among the top 10 across time frame. Both AUDJPY and NZDUSD have their top 10 places in 4H bar overtaken by EUR pairs.

The top movers table revealed pretty much the same picture. In particular, NZDJPY is the among the top 10 across time frame. Both AUDJPY and NZDUSD have their top 10 places in 4H bar overtaken by EUR pairs.

Pound Hits Two-Week Highs, European Stocks Gain As Risk-On Appetite Returns

Here are the latest developments in global markets:

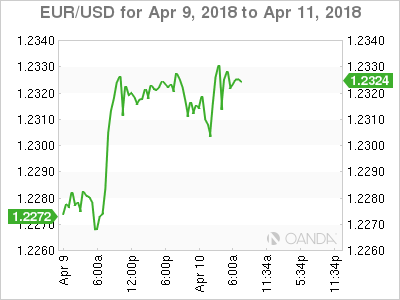

FOREX: Investors continued to digest encouraging comments by the Chinese President, Xi Jinping, during the early European afternoon, driving the Chinese-linked currencies the kiwi and the aussie even higher. The gains appeared after Jinping backed free trade and pledged to limit import tariffs, while his remarks also somewhat eased concerns over a yuan devaluation. However, a report by Bloomberg today saying that US-China talks regarding the high-tech industry have stalled last week pushed dollar/yen lower to 106.79 before it inched up to 106.97 (+0.22%). The dollar index gave back earlier gains, falling to 89.80 (-0.04%) as the pound and the euro strengthened even further. Pound/dollar advanced to a two-week high of 1.4178 after the BoE and MPC member Ian McCafferty told Reuters today that monetary tightening should not be delayed as wage growth might pick up faster than expected, pushing inflation above the BoE target. Euro/dollar stretched upwards to 1.2334 before it fell back to 1.2320 after the ECB member Ewald Nowotny reiterated that the ECB must reduce stimulus not too soon but neither too late. The Turkish lira tumbled to record lows against the dollar and the euro amid rising tensions in Syria as well as worries about the countries inflation and current account outlook.

STOCKS: European stocks opened higher after the Chinese President promised to improve the business environment for foreign investors, including a reduction in import tariffs in the auto industry this year. The pan-European STOXX 600 was up by 0.58% at 0900 GMT near one-month highs, while the blue-chip Euro STOXX 50 gained 0.75%, crawling up to six-week highs. The German DAX 30 surged 0.97%, with automakers leading the index, the French CAC 40 jumped by 0.69%, the Italian FTSE MIB rose by 0.31% and the British FTSE 100 increased by 0.38%. In Asia, equities closed higher, while in the US stock futures were in the green, pointing to a positive open.

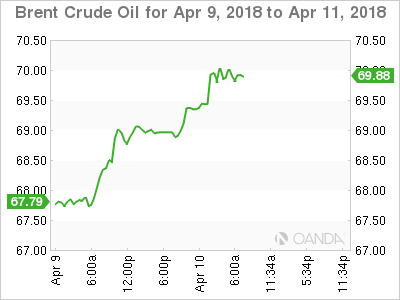

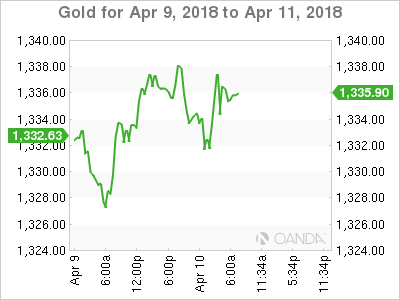

COMMODITIES: Oil prices extended yesterday's gains to one-week highs as trade tensions between the two biggest oil consumers, China and the US, continued to ease on Tuesday. WTI crude oil and the London-based Brent rallied by 1.34% to $64.27/barrel and $69.56/barrel respectively at 0900 GMT. In precious metals, gold was flat on the day at $1,336.13/ounce.

Day Ahead: US delivers PPI data; Canadian housing starts pending as well

Next on the day's agenda, the US Bureau of Labor Statistics will release figures on producer prices at 1230 GMT. The headline PPI is expected to inch up by 0.1% percentage points to 2.9% y/y from 2.8% in the previous month, while the core measure which excludes food and energy is also predicted to rise by an equivalent percentage to 2.6% y/y. On a monthly basis, the headline index is forecasted to tick slightly lower from 0.2% to 0.1%, whilst the core PPI is predicted to remain unchanged to 0.2%. In case the numbers come in stronger than expected, the dollar could enjoy some gains. This could also raise speculation that March CPI's due on Wednesday may rise as well. Forecasts are for the headline CPI to have risen to 2.4% y/y versus 2.2% the preceding month.

In other data releases, the Canada Mortgage and Housing Corporation will deliver figures on housing starts for the month of November at 1215GMT. The number of new constructions is anticipated to slow down by 10,700 to 219,000. Moreover, Canadian building permits for the month of February will be available at 1230GMT, with analysts predicting the gauge to turn negative to -1.5% m/m from 5.6% m/m previously.

In energy markets, investors will be waiting for the API weekly report to indicate the change in US crude oil stocks at 2030 GMT.

Early in the Asian session, corporate goods prices and machinery orders out of Japan at 2350 GMT will likely show some weakness.

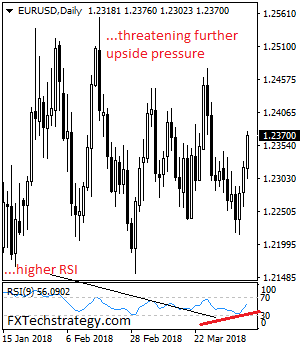

EURUSD powers through 1.2344 resistance heading into US session

EUR/USD soars sharply as markets are heading into US session. While some might point to sluggishness in USD/JPY as argue that risk appetite is not but. But they missed the point that USD/JPY is usually not the best pair that correlates with risk sentiment. Just like today, JPY and USD are the two weakest ones.

Back to EUR/USD, the break of 1.2344 minor resistance now invalidate the case of medium tem reversal in the pair. It's too early to judge whether rise from 1.2214 is resuming the larger up trend or it's another leg in the sideway pattern from 1.2555. But in either case, further rise should be seen back to 1.2475 and above in near term.

China Xi Jinping in Boao Forum: Reinforces Ease of Restrictions for Foreign Investment and Protection of Intellectual Property Rights

Speaking at the Boao Forum, sometimes known as "Asian Davos", Chinese President Xi Jinping announced four major areas of reform in opening up the market. First, the government would “significantly” ease market access, lowering restrictions for foreign investment in a number of Chinese sectors. In the financial industry, Xi reinforced the measures announced in late last year to liberalize the ratio of foreign-capital shares in banking, securities, and insurance industries. The government would also reduce restrictions automobile, shipping and aviation industries, among which restrictions on foreign investment in the automobile industry would be lowered as soon as possible

Second, China would create a better investment environment, strengthening adherence to international economic and trade rules, increasing transparency and opposing monopoly, so as to attract foreign capital. More importantly, it aims to complete the revision to the negative list for foreign investors in the first half of the year.

Third, through reorganization of the State Intellectual Property Office, the authority strives to strengthen protection of intellectual property rights though stricter enforcement of law.

Fourth, Xi stressed that China does not aim at pursuing a trade surplus. Instead, it plans to expand imports and promote current account balances. To achieve this, the government would reduce tariffs on autos and some other products. It would also accelerate the process of joining the WTO’s “Government Procurement Agreement”.

The abovementioned measures are nothing new. Indeed, since the 19th Party Congress, the government has in various occasions pledged to ease restriction on the establishment if foreign financial institutions, encourage technological exchanges between Chinese and foreign corporate and improve protection of intellectual property rights, and expand imports. The government has announced in January the organization of the first “China International Import Expo” this November. At the Boao speech, Xi mainly reinforced the importance and urgency of implementing these reforms. However, he has still refrained from offering the timeline of them. We believe his speech aims mainly at cooling down the intensified tensions with the US on trade.

Xi Warms Up Global Equity Markets

- Words are not deeds so be careful

- Geopolitical uncertainties are still very much in the background

- Michael Cohen's office was raided by the FBI, more threat for Trump

Despite the disappointing French Industrial economic, European markets are trading higher. Traders are taking a cue from President Xi Jinping’s speech who was successful in calming the markets and not escalating the tensions further on the US and China trade war issue. However, it is important to keep in mind as an investors that these are only words and if deeds are backed, the turmoil would continue.

Nonetheless, for now, the president sent the message that he is willing to open the economy further and lower taxes on the auto industry. Traders have taken this as a more positive outcome because for them the Chinese president understands that the trade war would not benefit any country.

One could say that perhaps president Trump’s strategy has yielded some results, especially when Xi Jinping confirmed that he is also determined to improve the environment for foreign companies. But one needs to be careful because improving environment for foreign companies doesn’t necessarily mean American companies.

His subtle message for Trump was clear that unfair tax penalties will not be welcomed. Overall, I think the markets have focused more on the positive tone of the president Xi Jinping and his remarks that China will remain open for the global trade.

No matter what the president Xi Jinping said, the geopolitical uncertainties are still very much in the background. We think it is important for investors to keep in mind what happened in Syria (a horrific chemical attack) and Trump's comments "big price to pay". The US has imposed a fresh set of new sanctions on Russia and the tit for tat reaction is still due.

Moreover, the US equity market lost its mojo yesterday when the news broke out that Trump's lawyer, Michael Cohen's office was raided by the FBI. He is under investigation for bank fraud & campaign finance violations. These raids clearly present a threat for president Trump because the FBI will not only be interested in finding the source of the money paid to Daniel (real name Stephanie Clifford) but patterns of other payments as well.

DAX Surges After Chinese President Offers Olive Branch

European markets are higher in the Tuesday session. Currently, the DAX is trading at 12,397 points, up 1.10% on the day. The CAC is also higher, posting gains of 0.69% on the day. On the release front, there are no German or eurozone indicators on the schedule. On Wednesday, ECB President Mario Draghi speaks at an event in Frankfurt. As well, the Federal Reserve will publish the minutes of its March rate meeting.

After weeks of escalating rhetoric in the trade battle between the US and China, there is a lull in the action, and the markets have reacted positively. On Sunday, US officials sought to lower the temperature on the Sunday television programs, and Treasury Secretary Steve Mnuchin said that he doesn’t “expect there will be a trade war.” This was followed by a calm message from Chinese President Xi Jimping on Tuesday. Xi was speaking at a development conference in China, and promised to lower tariffs on vehicle imports into China. This has been a major sticking point between the US and China, with President Trump complaining that China has a 25% tariff on US vehicle imports, yet the US only charges 2.5% on Chinese vehicles. Although China has previously declared that it would reduce the tariffs on vehicles, the markets were looking for some positive news, as the trade battle between the two largest economies in the world has shaken the markets in recent weeks. Xi added that China was looking to solve issues through dialogue rather than confrontation, and the markets are hoping that the US and China can avert a trade war, which could drag down the global economy.

German industrial numbers disappointed last week. Factory Orders posted a weak gain of 0.3%, well off the forecast of 1.6%. On Friday, Industrial Production declined 1.6%, compared to an estimate of 0.2%. This marked the fifth decline in the past six months. Earlier in the week, German Manufacturing PMI softened to 58.2, missing the estimate of 58.4. Although the reading indicated expansion, there is cause for concern as it marked an 8-month low.

Euro Unchanged Ahead Of US Inflation Reports

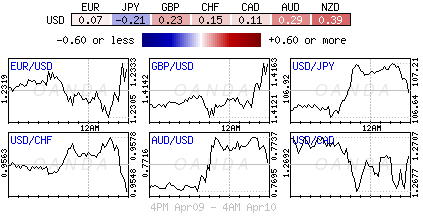

EUR/USD continues to have an uneventful week. Currently, the pair is trading at 1.2319, down 0.01% on the day. On the release front, there are no major eurozone events. In the US, the focus is on inflation indicators. PPI is expected to edge lower to 0.1%, and Core PPI is forecast to remain unchanged at 0.2%. On Wednesday, ECB President Mario Draghi speaks at an event in Frankfurt. The US releases consumer inflation reports, and the Federal Reserve will publish the minutes of its March rate meeting.

Investors are breathing a sigh of relief after Chinese President Xi Jimping sent out a conciliatory message earlier on Tuesday. Xi was speaking at a development conference in China, and promised to lower tariffs on vehicle imports into China. This has been a major sticking point between the US and China, with President Trump complaining that China has a 25% tariff on US vehicle imports, yet the US only charges 2.5% on Chinese vehicles. Although China has previously declared that it would reduce the tariffs on vehicles, the markets were looking for some positive news, as the trade battle between the two largest economies in the world has shaken the markets in recent weeks. Xi added that China was looking to solve issues through dialogue rather than confrontation, and the markets are hoping that the US and China can avert a trade war, which could drag down the global economy.

US employment numbers ended the week on a mixed note, and the euro gained ground on Friday. US nonfarm payrolls, one of the most important economic indicators, plunged to just 103 thousand, well off the forecast of 188 thousand. Still, the markets do not appear overly concerned, as payroll reports often sag in March. On a more positive note, wage growth improved to 0.3%, matching the forecast. This improvement is likely to reinforce sentiment that the Federal Reserve could press the rate trigger four times in 2018. The Fed has maintained its forecast of three rate increases this year, and an upwards revision could boost the US dollar against the euro and other rivals.

Xi Speech Constructive, Positive For Risk Assets

In his highly anticipated speech overnight, Chinese President Xi Jinping, speaking at the Boao Forum, sent an appeasing note on trade tensions with the U.S, giving markets a lift.

Xi vows to broaden market access, ease restrictions on foreign ownership in the auto sector and protect intellectual property. His comments seem aimed at “negotiation rather than confrontation” with the U.S.

Xi’s cool-headed approach toward the U.S/Sino trade dispute would suggest that the spat would probably end with concessions from China.

Risk assets – including equities and commodities – have rallied.

Stateside, inflation is the markets focus for the coming week, starting today with the producer price report (08:30 am EDT) which may offer the first hard evidence on price effects tied to steel and aluminum tariffs.

Tomorrow, U.S consumer prices (08:30 am EDT) will offer the latest on whether tariff or wage pressures are beginning to be passed through, while on Thursday, import prices (8:30 am EDT) will update the inflationary effects of ‘big’ dollar depreciation.

Also tomorrow will be the FOMC minutes (2:00 pm EDT) and with them details on the inflation debate inside the Fed.

1. Stocks given a leg up

Overnight, Japanese stocks rallied to a one-month high, led by automakers after Chinese President Xi promised to lower import tariffs on products including cars. The Nikkei rose +0.5%, while the broader Topix rallied +0.4%.

Down-under, Australia shares rose on Tuesday as a combination of higher metal prices and comments from China’s president Xi, calmed investors fears over trade tensions with the U.S and China. Both resource stocks and financials found support. The S&P/ASX 200 index gained +0.8%. In S. Korea, the Kospi was little changed at +0.27%.

In Hong Kong, stocks rally the most in a month on China reform pledge. The Hang Seng index rose +1.7%, while the China Enterprises Index gained +2.1%.

In China, stocks had their best day in seven-weeks as Xi’s speech eases trade war fears. The blue-chip CSI300 index rose +1.9%, while the Shanghai Composite Index gained +1.7%.

In Europe, regional indices trade higher across the board being led by the DAX on gains from Bayer and Auto names. Market sentiment has been helped by comments from President Xi overnight. Investors will now focus on earnings season.

In the U.S, stocks are set to open deep in the ‘black’ (+1.1%).

Indices: Stoxx600 +0.6% at 377.6, FTSE +0.4% at 7221, DAX +1.0% at 12387, CAC-40 +0.7% at 5300, IBEX-35 +0.3% at 9767, FTSE MIB +0.3% at 23120, SMI +0.5% at 8730, S&P 500 Futures +1.1%

2. Oil prices rise on Xi pro-trade comments, gold lower

Ahead of the U.S open, oil markets have rallied by more than +1%, extending yesterday’s strong gains, on hopes a trade dispute between the U.S and China may be resolved without too much damage to the global economy.

Brent crude futures are at +$69.62 per barrel, up +96c, or +1.4%, from yesterday’s close. U.S West Texas Intermediate crude futures are at +$64.31 a barrel, up +89c, or +1.4%.

Note: The gains followed a more than +2% rally on Monday, but that was a rebound from a -2% decline last Friday.

Despite this, prices remain confined within recent ranges as oil markets still face an abundance of supply that puts pressure on producers to keep their prices competitive.

Beyond the U.S/China trade dispute, oil markets are also concerned about the potential of renewed U.S sanctions against some significant oil producers.

Expect investors to take their cues from this week’s U.S inventory reports.

Gold prices have erased their early gains to trade lower on Tuesday after Chinese President Xi promised to lower import tariffs on certain products. Spot gold is down -0.1% at +$1,334.70 an ounce, after having risen to a near one-week intraday high of +$1,338.12 earlier in the session.

3. Sovereign yields remain in a tight range

To many, German Bunds are the most expensive and overbought sovereign asset along the fixed income curve.

The 10-year German Bund yield is trading at +0.51%, up +0.4 bps ahead of significant government bond supply from core eurozone countries on Tuesday.

Note: The Netherlands, Austria and Germany line up for bond auctions, while Ireland is likely to go ahead with the syndication of a new 15-year debt on Tuesday.

The 10-year German-Portuguese government bond-yield spread is currently +118 bps. On the same day in 2017 it was around +360 bps.

Net result would suggest that Portugal and the whole eurozone periphery is clearly benefitting from the broadening economic recovery and the ECB’s asset purchases, but the spread also reflects an amount of optimism around the next stage of European integration.

Elsewhere, the yield on U.S 10-year Treasuries gained +2 bps to +2.80%, while in the U.K, the 10-year Gilt yield decreased less than -1 bps to +1.407%.

4. Dollar loses some appeal

European inflation and growth data both continued to be subdued in the session. CPI data from Netherlands, Hungary and Czech Republic came in below expectations, while French February Industrial Production (IP) missed its consensus view (see below).

EUR/USD (€1.2321) remains steady and continues to hold above key support at €1.23 level and in the mid-range of its 2018 overall trading band.

GBP (£1.4167) is a tad firmer as BoE’s McCafferty (dissenter) saw “modest upside risk” to the BoE’s February wage growth forecasts.

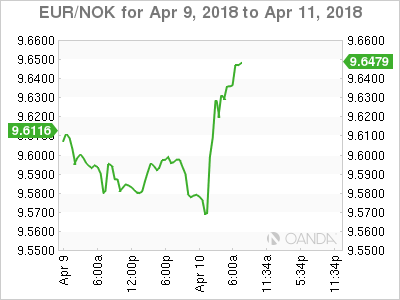

NOK (€9.6293 up +0.54%) is a tad softer after Norway’s Mar CPI missed expectations. Norges Bank rhetoric has suggested that their first potential rate hike could come after the summer, but todays disappointing inflation data is pushing the timing further out the curve.

Safe haven flows saw some unwind after China’s President Xi struck a conciliatory tone on trade – both the AUD ($0.7722) and NZD ($0.7340) both rallied in the overnight session.

The Russian rouble (RUB) continues to sell off Tuesday (down -8.1% in two day’s), falling to its lowest level outright in around 16-months as geopolitical pressure on Moscow intensifies. Over the weekend, the U.S. government announced sanctions against Russian government officials and business magnates, and issued harsher criticism against the Russian government for its support of Syrian President Assad.

5. French & Italian industrial production

E.U national data this morning suggests that the euro-zone’s industrial sector fared poorly in February, despite a rise in energy production as a result of the unseasonably cold weather.

Digging deeper, the headline production figure for France was fairly positive. French production rose by +1.2%, m/m, and January’s decline was revised to -1.8%, slightly smaller than previously estimated. But, the breakdowns were much less encouraging. The headline increases were largely reliant on substantial pick-ups in energy production due to the exceptionally cold weather, while non-durable consumer goods production fell.

Elsewhere, Italian headline industrial production fell by -0.5% on the month, much weaker than the consensus forecast for a +0.8% rise. Again, energy production picked up sharply, but this was more than offset by weakness in manufacturing.