Sample Category Title

Risk Aversion Comes Back on Syria Tension, Dollar Gets No Help from CPI

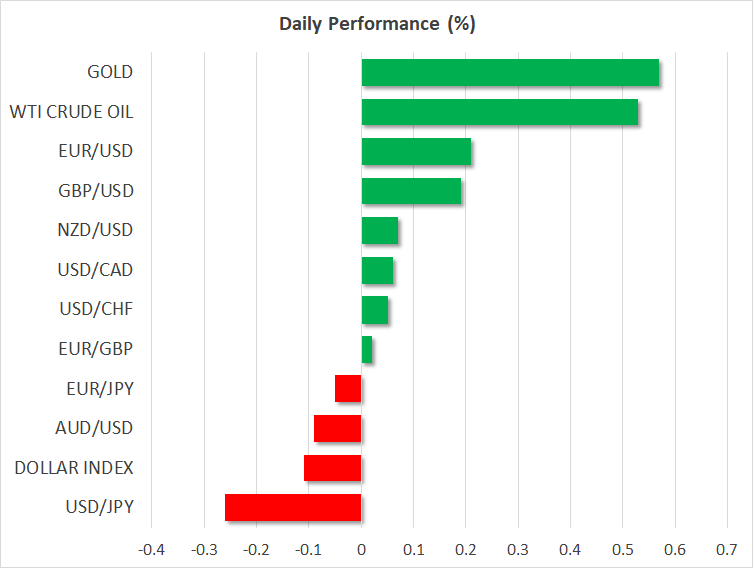

Risk aversion comes back to the markets today. Syria tension comes into spotlight and US-China trade war leaves the stage temporarily. DAX turned south at initial trading and never looked back. It's currently trading down -1% at the time of writing. CAC id down -0.67% while FTSE is down -0.22%. US futures also point to lower open, with DOW likely heading back towards 24000 handle. In the currency markets, Yen and Swiss Franc are trading as the strongest one entering into US session. Sterling suffered some selling after data misses. For the day so far, Yen is the strongest one followed by Euro. Australia Dollar and Canadian Dollar are the weakest.

US President Donald Trump is a master in escalating tensions with his tweets, no one can beat that. The financial markets are rocked again after Trump said in his usual morning tweet that "Russia vows to shoot down any and all missiles fired at Syria. Get ready Russia, because they will be coming, nice and new and 'smart!' You shouldn't be partners with a Gas Killing Animal who kills his people and enjoys it!" The tweet triggered concerns that if, intentionally or unintentionally, any US strike causes Russian casualties, there would be an escalatory cycle that worsen the situation in Syria further.

US CPI and core CPI accelerated in March, FOMC minutes next

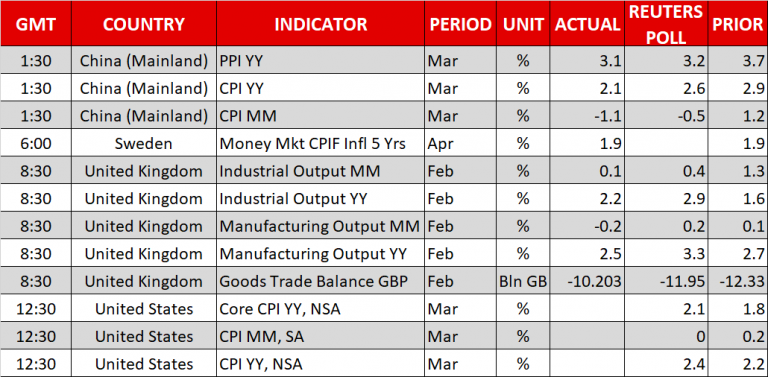

Released from the US, headline CPI dropped -0.1% mom in March, below expectation of 0.0% mom. But annual rate accelerated to 2.4% yoy, up fro 2.2% yoy and met expectation. Core CPI rose 0.2% mom, 2.1% yoy, up from 1.8% yoy in February, and met expectations. The set of data should ease some inflation worries of Fed policymakers. But they are providing no support to Dollar. Focus will turn to FOMC minutes next.

The main question in reading the FOMC minutes is whether Fed is more likely to stick with its projection of having three hikes in total this year. Or, it's more likely to hike four times. During the March meeting, among the 15 top Fed policymakers, 8 had two or fewer hikes for this year in the famous dot-plot. On the other hand, 7 had three or more. This showed quite a divergence between Fed hawks and doves. And the minutes could reveal more about the debates inside FOMC.

But after all, it should be noted that with easing concerns over trade war, traders are back putting their bets on a June hike. As indicated by fed funds futures, chance of a 25bps June hike surged sharply this week to 95%. But that provides little support to Dollar so far. The greenback might not get any sustainable boost even it the Fed minutes turn out to be more hawkish than expected.

ECB Draghi: EU cannot solve problems just at national levels

ECB President Mario Draghi spoke at the Generation €uro Students' Award today. He said that EU cannot solve its problem just at national levels. And, more integration will allow EU to face economic challengers more effectively. Draghi also sounded easy regarding recent escalation in trade tension between US and China. In his view, the impact of the tariffs "announced" is small. Nonetheless, this could still hurt investor confidence. And Draghi emphasized that while "the direct effects are not big… in the end the key issue is retaliation."

Separately, ECB governing council member Ardo Hansson said recent low inflation in the euro area has been the result of "a combination of factors." And, most of these factors are "temporary in nature". Therefore, impact from these factors will "weaken over time". Therefore, Hansson said "we need to be more patient in achieving our price stability goal." Nonetheless, ECB still has to monitor the side effects of policy carefully.

Sterling pares gains after data disappointment

GBP/USD pares some of earlier against after disappointing data. Industrial production rose 0.1% mom, 2.2% yoy in February, below expectation of 0.4% mom, 2.9% yoy. Manufacturing production dropped -0.2% mom, rose 2.5% yoy, below expectation of 0.2% mom, 3.3% yoy. Construction output dropped -1.6% mom in February versus expectation of 0.7% mom. Visible trade deficit narrowed to USD -10.2b in February versus expectation of GBP -11.9b. NIESR GDP estimate rose 0.2% in March, below expectation of 0.3%.

UK CBI: Don't diverge from EU rules after Brexit

The Confederation of British Industry published a report showing that UK business overwhelming prefer to stay with EU rules after Brexit. Carolyn Fairbairn, CBI Director-General said that for the majority of businesses, "diverging from EU rules and regulations will make them less globally competitive, and so should only be done where the evidence is clear that the benefits outweigh the costs." She emphasized that the report comes from "heart of British business" and it provides "unparalleled evidence to inform good decisions that will protect jobs, investment and living standards across the UK." Additionally, she urged "major acceleration" in the partnership between businesses and the government to deal with Brexit issues.

RBA Lowe: No strong case for near term adjustment in interest rate

BA Governor Philip Lowe devoted a section on monetary policy is his address to Australia-Israel Chamber of Commerce (WA) today. And, he brought out four broad points.

Firstly, he expects a "further pick-up" in the Australian economy, with increased investment, hiring and exports. Inflation is also expected to "gradually pick up" with wages growth too. But there are uncertainties "lying in the international arena". Lowe warned that "a serious escalation of trade tensions would put the health of the global economy at risk and damage the Australian economy". And, "we also have a lot riding on the Chinese authorities successfully managing the build-up of risk in their financial system." Domestically, the level "high level of household debt remains a source of vulnerability".

Secondly, the next interest rate move will likely be "up, not down". And that might "come as a shock to some people". Thirdly, inflation returning to midpoint of target zone is expected to be "only gradual". And, "it is still some time before we are likely to be at conventional estimates of full employment. Fourthly, and most important to the markets, "Reserve Bank Board does not see a strong case for a near-term adjustment in monetary policy." Lowe reiterated that other global central banks have lower policy rates than Australia "over the past decade". So, the situations are different.

IMF Lagarde: Sun is still shining but we have to "steer clear of protectionism"

In a speech at the University of Hong Kong, IMF Managing Director Christine Lagarde expressed her optimism on the global economy. She said the "economic picture is "mostly bright" and "the sun is still shining". Global momentum is driven by "stronger investment", "rebound in trade" and "favorable financial conditions". She said the forecast to be release next week will "continue to be optimistic".

Regarding advanced economies, Lagarde said Eurozone's upswing is "now more widely spread across the region". US growth will "likely accelerate further due to expansionary fiscal policy". In Asian emerging markets, China and India lead by "rising exports and higher domestic consumption. But she also warned of "darker clouds looming". Momentum in 2018 and 2019 will eventually slow because of "fading fiscal stimulus" in the US China, rising interest rates and tighter financial conditions.

Lagarde emphasized three priorities for the global economy, including 1. Steering clear of Protectionism, 2. Guard against Fiscal and Financial Risk, 3. Foster Long-term Growth that Benefits Everyone.

China PBoC Yi outlines specifics on opening financial market access at Boao

New People's Bank of China Governor Yi Gang pledged to further open the financial markets in the Boao Forum for Asian in China. And some specifics were offered by Yi too. Firstly, the government will remove foreign ownership caps on Chinese banks by the end of June. Secondly, foreign securities and life insurance companies will be allowed to hold majority stakes in their Chinese counterparts. That is, ownership could be raised from 49% to 51%. And such restriction will also be abolished in three years. Thirdly, by the end of June, the permitted business scope for foreign insurance agents will be expanded. Fourthly, the daily quota for foreign investors to buy Chinese stocks and for Chinese investors to buy Hong Kong traded stocks will be quadrupled. In addition, by the end of 2018, China will launch a trading link between Shanghai stock markets to London's. Separately, Yi also said that China won't devalue Yuan as part of the moves of trade war with the US.

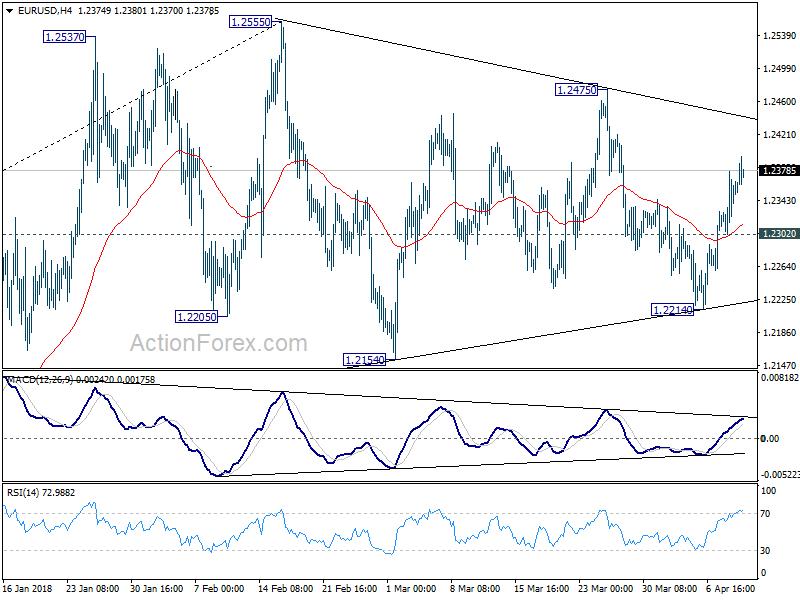

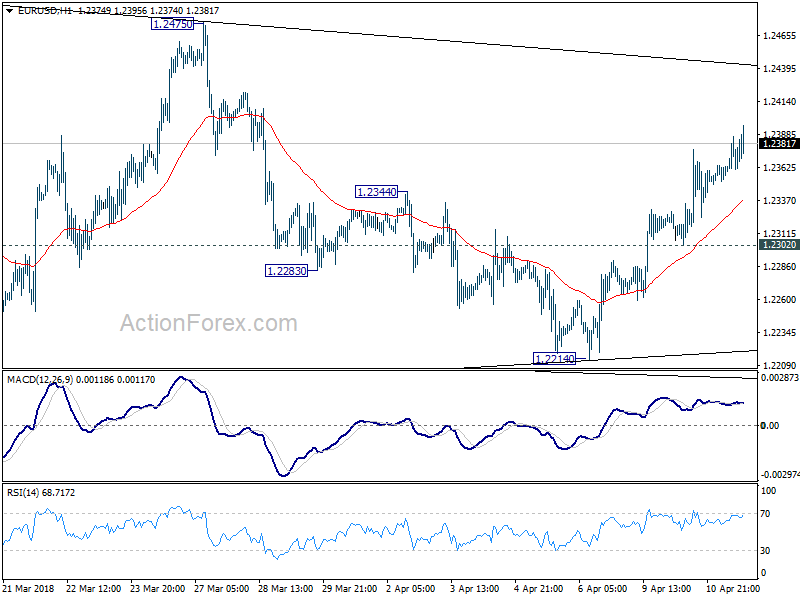

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2312; (P) 1.2345 (R1) 1.2387; More....

Intraday bias in EUR/USD remains on the upside as rise from 1.2214 is in progress, hitting 1.2395 so far. Further rally should be seen for 1.2475 first. Break will target key resistance level at 1.2555 high. For now, as EUR/USD is bounded in range trading pattern from 1.2555, break of 1.2302 minor support will turn bias back to the downside for 1.2214 instead.

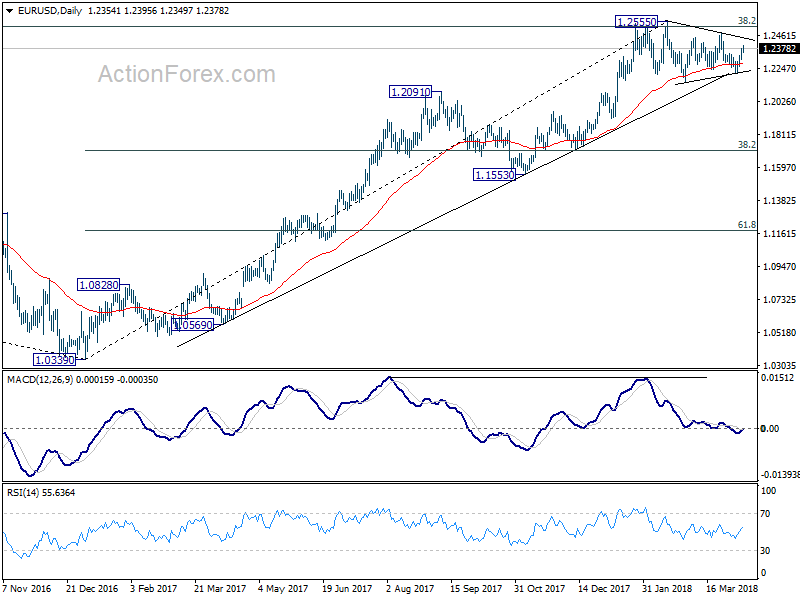

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machine Orders M/M Feb | 2.10% | -2.50% | 8.20% | |

| 23:50 | JPY | Domestic CGPI Y/Y Mar | 2.10% | 2.00% | 2.50% | |

| 00:30 | AUD | Westpac Consumer Confidence Apr | -0.60% | 0.20% | ||

| 01:30 | CNY | CPI Y/Y Mar | 2.10% | 2.60% | 2.90% | |

| 01:30 | CNY | PPI Y/Y Mar | 3.10% | 3.30% | 3.70% | |

| 08:30 | GBP | Visible Trade Balance (GBP) Feb | -10.2B | -11.9B | -12.3B | |

| 08:30 | GBP | Industrial Production M/M Feb | 0.10% | 0.40% | 1.30% | |

| 08:30 | GBP | Industrial Production Y/Y Feb | 2.20% | 2.90% | 1.60% | 1.20% |

| 08:30 | GBP | Manufacturing Production M/M Feb | -0.20% | 0.20% | 0.10% | |

| 08:30 | GBP | Manufacturing Production Y/Y Feb | 2.50% | 3.30% | 2.70% | 2.20% |

| 08:30 | GBP | Construction Output M/M Feb | -1.60% | 0.70% | -3.40% | -3.10% |

| 11:00 | GBP | NIESR GDP Estimate Mar | 0.20% | 0.30% | 0.30% | |

| 12:30 | USD | CPI M/M Mar | -0.10% | 0.00% | 0.20% | |

| 12:30 | USD | CPI Y/Y Mar | 2.40% | 2.40% | 2.20% | |

| 12:30 | USD | CPI Core M/M Mar | 0.20% | 0.20% | 0.20% | |

| 12:30 | USD | CPI Core Y/Y Mar | 2.10% | 2.10% | 1.80% | |

| 14:30 | USD | Crude Oil Inventories | -0.6M | -4.6M | ||

| 18:00 | USD | Monthly Budget Statement Mar | -175.0B | -215.2B | ||

| 18:00 | USD | FOMC Meeting Minutes |

US CPI and Core CPI accelerated, But USD weak against Euro and Yen

US headline CPI dropped -0.1% mom in March, below expectation of 0.0% mom. But annual rate accelerated to 2.4% yoy, up fro 2.2% yoy and met expectation. Core CPI rose 0.2% mom, 2.1% yoy, up from 1.8% yoy in February, and met expectations.

CPI provides little support the USD. Rising geopolitical tension in Syria is weighing market sentiments and the greenback. Trump's attention is now temporary away from China and back to Russia, with his tweeted to warn Russia of missiles in Syria.

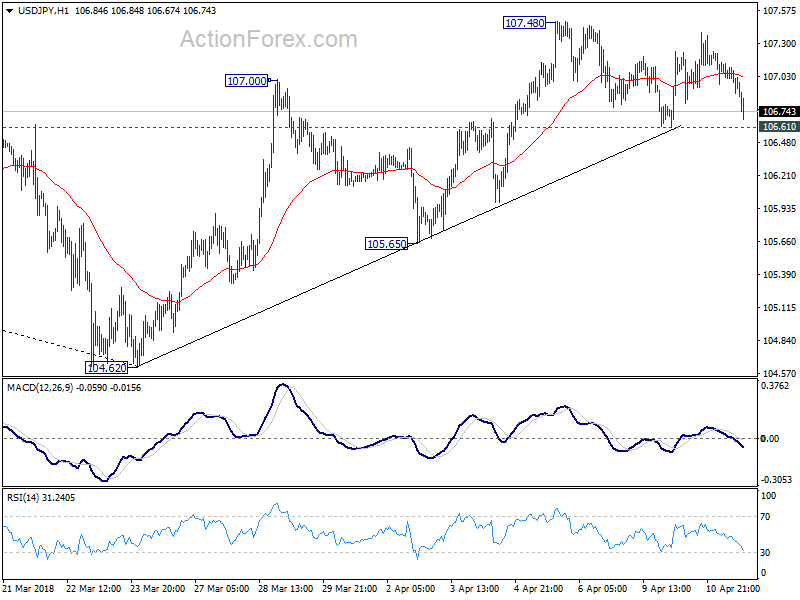

USDJPY's immediate focus in now on 106.61 minor support in early US session. Break will put 105.65 into focus.

EURUSD doesn't bother much about the Syira news and is on track for 1.2475.

EURUSD doesn't bother much about the Syira news and is on track for 1.2475.

FOMC minutes will be the next major focus in US session. But even something hawkish there is unlikely to give USD a lift.

ECB Draghi: EU cannot solve problems just at national levels

ECB President Mario Draghi spoke at the Generation €uro Students' Award today. He said that EU cannot solve its problem just at national levels. And, more integration will allow EU to face economic challengers more effectively. Draghi also sounded easy regarding recent escalation in trade tension between US and China. In his view, the impact of the tariffs "announced" is small. Nonetheless, this could still hurt investor confidence. And Draghi emphasized that while "the direct effects are not big... in the end the key issue is retaliation."

Separately, ECB released a paper titled "Completing the Banking Union with a European Deposit Insurance Scheme: who is afraid of cross-subsidisation?" The paper noted that study results indicated that a " fully-funded DIF (Deposit Insurance Fund) would be sufficient to cover payouts even in very severe crises - even more severe than the 2007-2009 global financial crisis." And, "EDIS (European Deposit Insurance Scheme) would offer major benefits in terms of depositor protection while posing limited risks...since the probability and magnitude of interventions are likely to be low."

Canadian Dollar Rally Continues, US Consumer Inflation Next

The Canadian dollar has posted strong gains this week, gaining 1.2 percent. In the Wednesday session, USD/CAD has risen 0.14% on the day. In economic news, there are no Canadian events on the schedule. It’s a busy day in the US, with the release of the FOMC minutes and consumer inflation indicators. CPI is expected to dip to 0.0%, and Core CPI is forecast to remain at 0.2%. As well, the FOMC releases the minutes of its March rate meeting. On Thursday, the US publishes unemployment claims.

The Canadian dollar has flexed some muscle, but some serious headwinds could be around the corner. Syrian forces allegedly used chemical weapons against rebel positions last week, and a UN Security Council meeting ended inconclusively after Russia cast a veto on a US proposal to prove the attack. US President Trump has warned that a US response is on the way, and Russia has countered that it will respond to any US move. If Trump makes good on his promise, investor risk appetite could sink and drag down minor currencies such as the Canadian dollar.

The Bank of Canada Business Outlook Survey was released earlier this week. The survey pointed to a generally upbeat business sector and has helped boost the Canadian dollar. The survey found widespread intention by companies to increase investment and hiring, and “forward-looking sales indicators remain positive across most regions and sectors”. Still, the report is unlikely to change the current sentiment that the BoC will not raise rates at next week’s policy meeting.

The tariff spat between the US and China appears far from over, but both sides have lowered the flames which ahs roiled the markets in recent weeks. Investors are breathing a sigh of relief after Chinese President Xi Jimping sent out a conciliatory message on Tuesday. Xi was speaking at a development conference in China, and promised to lower tariffs on vehicle imports into China. This has been a major sticking point between the US and China, with President Trump complaining that China has a 25% tariff on US vehicle imports, yet the US only charges 2.5% on Chinese vehicles. Xi added that China was looking to solve issues through dialogue rather than confrontation, and the markets are hoping that the US and China can avert a trade war, which could drag down the global economy.

Risk Appetite Fizzles On Syria Tensions, While Oil Jumps

A touch of risk aversion crept into financial markets on Wednesday, as the sense of relief over easing U.S-China trade tensions was overshadowed by the rising geopolitical risk surrounding Syria.

Asian stocks closed mostly mixed due to market caution, with European equities sinking lower as investors adopted a guarded approach. Although Wall Street ended higher on Tuesday as trade fears eased, geopolitical tensions could pressure U.S equity bulls this afternoon.

The wild movements witnessed across global equity markets in recent weeks continue to highlight how fragile market sentiment remains amid the ongoing U.S-China trade developments. Although conciliatory remarks from President Xi Jinping have soothed concerns over a global trade war, will this be enough to support equity bulls in the long term? Stock markets still remain vulnerable to downside losses, especially if escalating tensions in Syria prompt investors to scatter away from riskier assets to safe-haven investments.

Sterling supported by Dollar weakness

Sterling surrendered some gains but remained firm on Wednesday, after British manufacturing output fell unexpectedly in February.

The U.K’s manufacturing output fell 0.2%, its first drop since March 2017. Today’s soft economic data could fuel concerns that economic growth cooled in the first quarter of 2018. However, Sterling is likely to remain supported by ongoing Dollar weakness. Market expectations over the Bank of England raising U.K interest rates in May remain high, while a vulnerable Dollar is likely to continue supporting the GBPUSD’s upside.

Focusing purely on the technical picture, the GBPUSD is turning increasingly bullish on the daily charts. Prices are trading above the 50 Simple Moving Average while the MACD has crossed to the upside. Bulls could attack the 1.4230 level, as long as prices remain above 1.4100.

U.S inflation and FOMC minutes in focus

The Dollar extended losses against a basket of major currencies as lingering trade war fears and political uncertainty in Washington weighed heavily on the currency.

Much focus will be directed towards the U.S CPI data reading today and anticipated FOMC minutes from the meeting in March, which could determine the Dollar’s near-term direction. An upside surprise in U.S inflation, coupled with a more hawkish tone in the FOMC minutes, could throw the Dollar a lifeline.

Taking a look at the technical picture, the Dollar Index remains under noticeable pressure on the daily charts. A breakdown below 89.50 could encourage a decline towards 89.00.

Commodity spotlight – WTI Oil

Escalating tensions in the Middle East have stimulated concerns over potential supply disruptions; this is likely the main culprit behind oil’s recent aggressive appreciation.

While oil is likely to remain supported by geopolitical risk and a vulnerable U.S Dollar for the moment, soaring U.S Shale production has the ability to cap upside gains. The fundamentals behind oil are likely to remain shaky in the longer-term as increasing U.S output complicates OPEC’s efforts to prop prices higher and rebalance markets. Taking a look at the technical picture, WTI Crude has scope to reach $68.00 if bulls can break above $66.50. A scenario where prices are unable to breach the $66.50 resistance level could encourage a decline back towards $64.00.

JPY rebounds as Trump tells Russia to get ready for missiles

European stocks dive while JPY rebound strongly after Trump's Syria warning.

In his usual morning tweet, Trump wrote "Russia vows to shoot down any and all missiles fired at Syria. Get ready Russia, because they will be coming, nice and new and "smart!" You shouldn't be partners with a Gas Killing Animal who kills his people and enjoys it!

In the current 4H heatmap, JPY and CHF are the clear winners. GBP started to pare back recent gains after weaker than expected industrial and manufacturing production released earlier today. Commodity currencies, AUD, CAD and NZD are also pressured as risk aversion resurfaces.

Dollar Faces Headwinds As Geopolitical Risks Weigh, FOMC Minutes & US CPI Figures In Focus

Here are the latest developments in global markets:

FOREX: While trade concerns seemed to ease following an encouraging speech by the Chinese President yesterday, who promised to improve the business environment for foreign companies, a pledge later outlined in more detail by the People’s Bank of China Governor, geopolitical fears appeared in the horizon. Particularly investors turned cautious after Western countries including the US and France were considering taking military action against Syria’s government in response to last week’s chemical attack in the region, with Russia warning Washington that it would shoot down any US missiles. The dollar index edged down to a two-week low of 89.44 (-0.08%) ahead of the US CPI figures and the FOMC meeting minutes due today, while dollar/yen almost reversed yesterday’s gains, falling to 106.93 (-0.24%). On the other hand, pound/dollar was on the rise today reaching a two-week high of 1.4222, but worse-than-expected industrial figures pushed the pair down to 1.4193 afterwards (+0.14%). Euro/dollar was also enjoying some gains, crawling up to a fresh two-week peak of 1.2386 (+0.19%) on the back of a weaker dollar despite an ECB spokesman playing down ECB Nowotny’s rate hike comments. In antipodean currencies, aussie/dollar inched down to 0.7754 (-0.05%), while kiwi/dollar managed to reverse today’s losses, rising slowly to 0.7365 (+0.08%). Dollar/loonie was flat at 1.2607 (+0.03%). The Turkish lira hit a fresh record low against the greenback at 4.1552 per dollar.

STOCKS: European stocks retreated moderately during early European session affected by rising tensions in Syria, with the European air control warning airlines over airstrikes on Syria over the next 72 hours. The pan-European STOXX 600 was down by 0.22% at 0900 GMT, with the British supermarket Tesco being the best performer after the company reported a 28% growth in full-year profits. The blue-chip Euro STOXX 50 fell by 0.33%, the German DAX 30 declined by 0.26%, the French CAC 40 retreated by 0.25%, while UK’s FTSE 100 moved lower by 0.07%. Asian equities closed mixed, while indices tracking US stock futures were in the green, pointing to a positive open.

COMMODITIES: Geopolitical risks also affected oil prices negatively early on Wednesday as the Middle East is considered one of the largest world crude exporters and any military activities in the region could disrupt oil markets. However, the market shrugged off those risks afterwards, following comments by the Saudi Arabian energy minister who expressed his satisfaction regarding the current market conditions and said that Saudi Arabia would not let another supply glut to develop. WTI crude and Brent were last seen at $65.81/barrel (+0.46%) and $71.19/barrel (+0.21%) respectively. In precious metals, gold hit a one-week high of $1346.40 (+0.53%).

Day Ahead: US CPI & FOMC meeting minutes gather attention

The dollar will be in the spotlight later in the day as FOMC meeting minutes and US CPI figures could bring fresh volatility to the currency.

At 1230 GMT, the US Bureau of Labour Statistics will release CPI figures for the month of March. According to forecasts, the index is expected to gain 0.2 percentage points, rising to 2.4% y/y, while the core equivalent is anticipated to inch up 0.3 percentage points to 2.1% y/y. While this is not the Fed’s preferred inflation measure – this is the core PCE index –, an upside surprise in the CPI numbers could increase speculation that inflation is probably running to the upside. Note that on Tuesday the core PPI came in at 2.9% y/y in the 12 months through March, printing the biggest increase since August 2014, after climbing by 2.7% y/y in February.

Later at 1800 GMT, the Federal Open Market Committee will publish minutes from its latest meeting on March 20-21 which was chaired for the first time by Jerome Powell. At that meeting, policymakers raised interest rates as was widely expected and the closely-watched dot plot signaled two more rate hikes for 2018, which was already priced in by the markets. The latter was interpreted as a dovish sign since speculation was in the air that the Fed could deliver four rate hikes in total in 2018 instead of three. Policymakers, though, appeared more optimistic about this year’s rate path as the number of officials backing a steeper monetary tightening increased despite the median “dot” remaining unchanged at three hikes. The minutes could also reveal the Fed’s view on Trump’s trade policy, another spot that could add some volatility to the dollar. It should be also noted that with easing concerns over trade war, traders are widely expecting a rate hike in June. As indicated by the Fed funds futures, chances of a 25bps hike in June surged this week to 95%.

Also, on the agenda today, investors will look through the EIA report on US crude oil inventories. Crude inventories are anticipated to drop by 0.189 million barrels in the week ending April 6 compared to a fall of 4.617mn in the preceding week.

During early Asian session, New Zealand electronic card retail sales for the month of March are scheduled to be released at 2245 GMT, with forecasts supporting a growth of 0.5% y/y compared to a contraction of 0.3% y/y seen previously. A few minutes later at 2300 GMT, RICS house price balance will come into view in the UK.

As for today’s public appearances, ECB President, Mario Draghi will be speaking in Frankfurt at 1100 GMT, while ECB members Pentti Hakkarainen and Ignazio Angeloni are scheduled to deliver remarks at 1300 GMT and 1440 GMT respectively. In the US, Facebook’s chief executive, Mark Zuckerberg, will be in the hot seat for the second day, testifying before the House Energy and Commerce Committee regarding the sharing of private information with the London-based data mining firm Cambridge Analytica which had connections with Trump’s campaign in 2016.

ECB Hansson: Low inflation in Euro area due to temporary factors

ECB governing council member Ardo Hansson said recent low inflation in the euro area has been the result of "a combination of factors." And, most of these factors are "temporary in nature". Therefore, impact from these factors will "weaken over time". Therefore, Hansson said "we need to be more patient in achieving our price stability goal." Nonetheless, ECB still has to monitor the side effects of policy carefuly.

US Futures Lower Ahead Of FOMC Minutes

- Trade War Fears Continue to Weigh Despite Recent Gains;

- US Inflation Seen Ticking Higher After PPI Beat;

- Safe Havens Sought in Risk Averse Trade.

US futures are back in negative territory ahead of the open on Wednesday, as stocks continue to fluctuate against the backdrop of a potential trade war.

Investors are also awaiting the release of the FOMC minutes from the March meeting, at which the central bank raised interest rates by 25 basis points a released new economic forecasts containing upward revisions to rate, inflation and growth forecasts. The change was largely attributable to tax reform which was passed at the end of 2017 but many expected the Fed to go further and forecast a fourth hike this year rather than next.

While it wasn't far from doing so, traders will be curious about how likely that is to change in June, especially if inflationary pressures grow in the meantime, as we're expecting from the CPI releases today. Yesterday's PPI release showed an uptick in March to 3% which is expected to be reflected in today's data, with CPI seen rising to 2.4% from 2.2% and core CPI to 2.1% from 1.8%, compared to a year ago.

While this may not be the Fed's preferred measure of inflation, it is released a few weeks earlier and so gives us the earliest indication of price pressures in the previous month. Anything above expectations could lift expectations ahead of the June meeting and lift yields on US debt in the process. The 10-year continues to trade well below 3%, with the trade conflict with China being the latest development to weigh on it.

Aside from the safe haven flows that US Treasuries naturally attract, a full blown trade war would likely have negative implications for the country and therefore impact the pace at which the Fed can raise interest rates, which may explain why the yield on the 10-year is still struggling to break 3%.

With stock markets in Europe trading in the red and US futures on course to do the same, we're seeing some typically risk averse trading on Wednesday. As is typically the case, this is favouring save havens such as Gold and the yen, with the former close to 1% higher and trading near the top end of its range this year. The yen is making gains against the dollar, euro and pound, with the latter having also been negatively impacted by the manufacturing and industrial production figures this morning, all of which were shy of expectations.

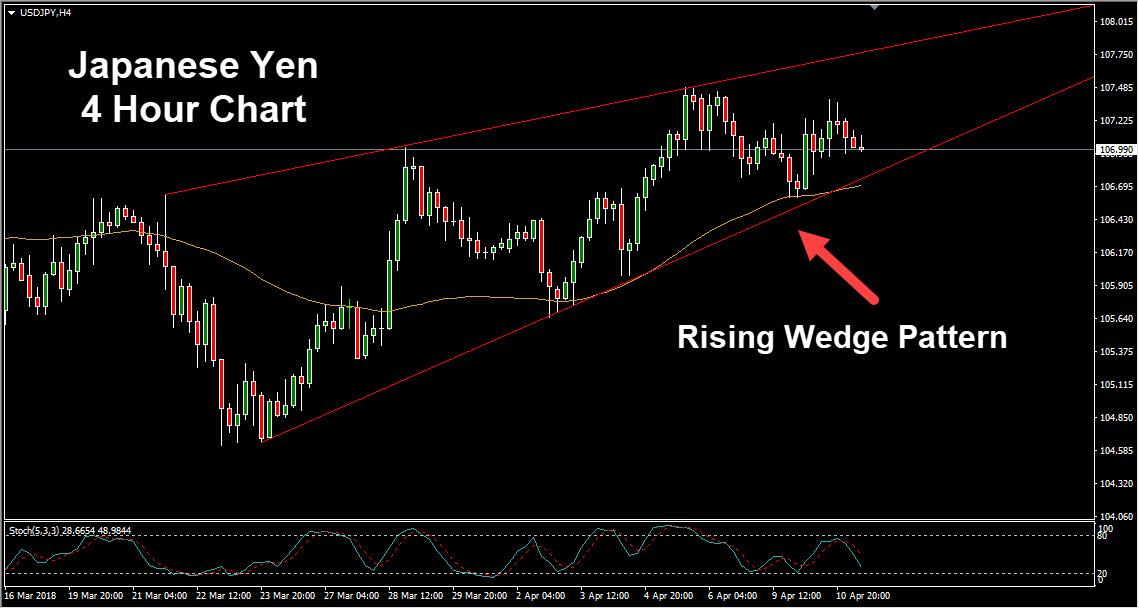

Chart Of The Day: Pressure Building Within USD/JPY Wedge Pattern

The safe haven Japanese Yen weakened on Tuesday after the Chinese president adopted conciliatory stance in his speech on trade. Risk appetite was revived as Xi Jinping said his government would "significantly lower" tariffs on vehicle imports this year in an effort to further open China’s economy to the world.

Meanwhile, the US dollar was pressured by a disappointing jobs report on Friday. The data dampened expectations for four rate hikes from the Fed in 2018. Political unrest within the US and lingering trade war concerns continue to keep a lid on the greenback.

Gold prices have surged amid the possibility of a US military response in Syria and a weaker US dollar. Geopolitical uncertainty related to the conflict in Syria could also boost the Japanese Yen.

Looking at the 4 Hour USD/JPY chart we can see the price is confined within a well defined rising wedge pattern. The pattern appears in the context of a downtrend that began in November of 2017.

Major data ahead for the US dollar on Wednesday could provide the impetus for a breakout of the wedge pattern. The US Consumer Price Index (CPI) and FOMC Meeting Minutes are both due for release later on Wednesday.