Sample Category Title

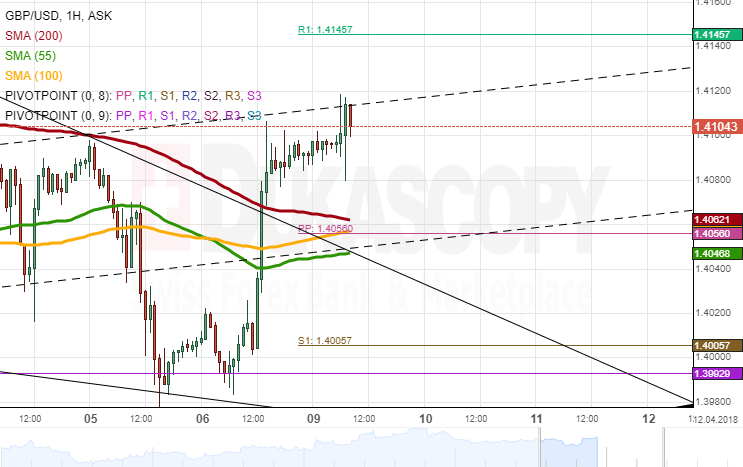

GBP/USD Analysis: Calm After Surge

The first part of Friday's trading session was spent with no massive changes to the Pound's positioning against the US Dollar, as the pair remained fluctuating slightly above the monthly PP at 1.40.

High volatility was introduced mid-session when the US released sluggish employment data. As a result, the Sterling surged 85 pips against its American counterpart within a few hours and breached the 55–, 100– and 200-hour SMAs along the way. This massive bullish momentum was followed by a narrow movement sideways during the Asian session which occurred near the upper boundary of a breached short-term channel up.

It is expected that the pair is tended south in this session just to ease the aforementioned up-move. This fall, however, is likely to be limited by the SMAs and the weekly PP at 1.4050.

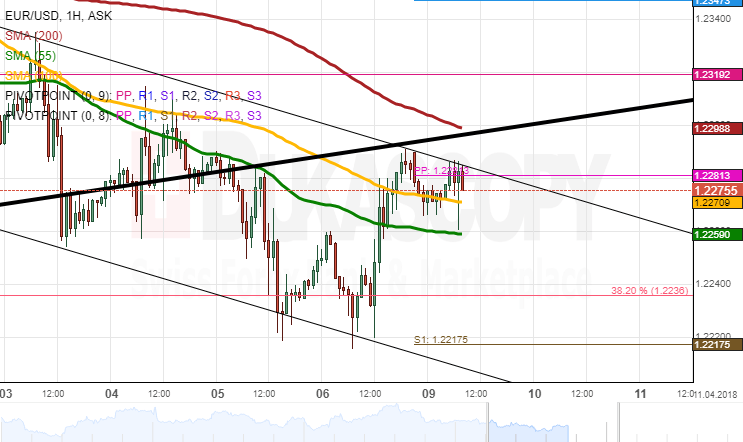

EUR/USD Analysis: Retraces From Breached Channel

EUR/USD was trading slightly above the 1.2240 mark early on Friday, being restricted by the 38.20% Fibo retracement.

This sentiment changed in favour of bulls mid-session in response to rather disappointing US employment data. Upside risks likewise prevailed during the following hours, thus sending the pair towards the upper boundary of a short-term channel and the weekly PP circa 1.2280. As a result of this upside movement, the Euro has likewise formed a retracement from the previously-breached senior channel.

Technical indicators are more bearish for today, thus suggesting that the combined support of the 55– and 100-hour SMAs near 1.2275 is more likely to be surpassed than the 200-hour SMA at 1.23. The latter is also reinforced by the monthly PP at 1.2320.

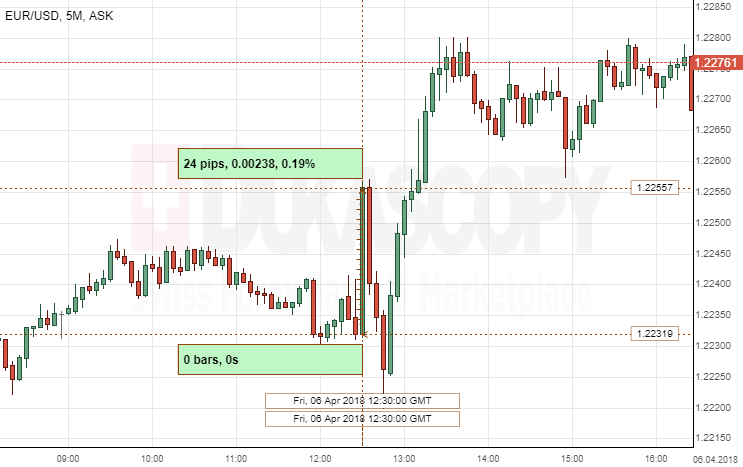

EUR/USD: US Non-Farm Employment Change

The Eurozone's single currency weakened against the Greenback, following the UK non-farm employment change data on Friday. The EUR/USD currency pair skyrocketed 24 pips, or 0.19%, to continue fluctuating in the 1.2272 area.

The Bureau of Labor Statistics revealed much lower-than-expected data in non-farm employment change in March. However, there was an employment growth of 103K, it decreased more than three times from 326K in the prior month. Without non-farm employment change, there were two more data sets that came out simultaneously. Average hourly earnings stayed in line with the forecast, however, the unemployment rate came out to be 4.1%, which was 0.1% more than expected.

China considering Yuan devaluation as trade weapon against US?

Bloomberg reported that Chinese officials are studying the impact of yuan depreciation on two fronts. Firstly, analysis was taken to look at using currency depreciation as a weapon in the trade war with the US. Secondly, it's also studied how yuan depreciation could help offset any trade deal with US that curb exports.

However, one important point to note is that the source for the information is obviously unnamed. And further than that, Bloomberg just said it's from "people familiar with the matter". So it looks unlikely that the information is from any Chinese officials.

At the same time, it's firstly seen by many that yuan devaluation could destabilize the China's own markets, and that could do more harm to itself than to the US. And more important, China has been trying to portrait itself as rule follower that complies with the WTO book. It keeps blaming the US for unilateralism and protectionism and tries to to use that to draw international support. Devaluation of the Yuan will put China up against other countries too.

President Xi Jinping probably won't mind US President Donald Trump reiterating the label that China is a currency manipulator. But he most certainly doesn't prefer other countries to jump on that bandwagon.

So, while the news is currently in Bloomberg's headline, its accuracy is suspectable.

Eurozone Sentix expectations turned negative, significant economic slowdown must now be assumed

Eurozone Sentix investor confidence dropped notably to 19.6 in April, down from 24.0 and missed expectation of 19.6. Current situation index dropped from 24.0 to 19.6, continuing the decline fro January's high of 32.9. Expectation index turned negative to -1.5, down from March's 4.3. That's also a continuation of the fall from 18.8 back in January.

Highlights from the release:

Highlights from the release:

- All regions of the world are on an economic downturn in April. Despite the still good assessment of the situation, there is no doubt that the global economy is cooling off.

- Expectations for the Euro area are negative again for the first time since July 2016. The downward dynamic for Germany is even more pronounced.

- The euphoria for the US economy is also fading noticeably. Expectations drop to a value of -7 percentage points. Trump's statements and measures on punitive tariffs raise serious concerns. The component for Expectations of the sentix Global Aggregate falls to its lowest value since February 2016.

Regarding Eurozone, the report noted that clear visible cooling. And, "after the declines in expectations had already indicated a turnaround in the previous months, a significant economic slowdown must now be assumed." And, "the customs disputes, fueled by US President Donald Trump, are leaving their traces."

Regarding the US, Sentix noted that "observers rely on the common sense of the US government and assume that the demands are merely negotiation tactics." But it warned that "Trump is consistently working through its 'America first' agenda". And, The positive effects of the tax reform have quickly evaporated, and expectations for the US economy are plummeting.

Also released in European session, German trade surplus narrowed to EUR 19.2b in February. Swiss unemployment rate was unchanged at 2.9% in March.

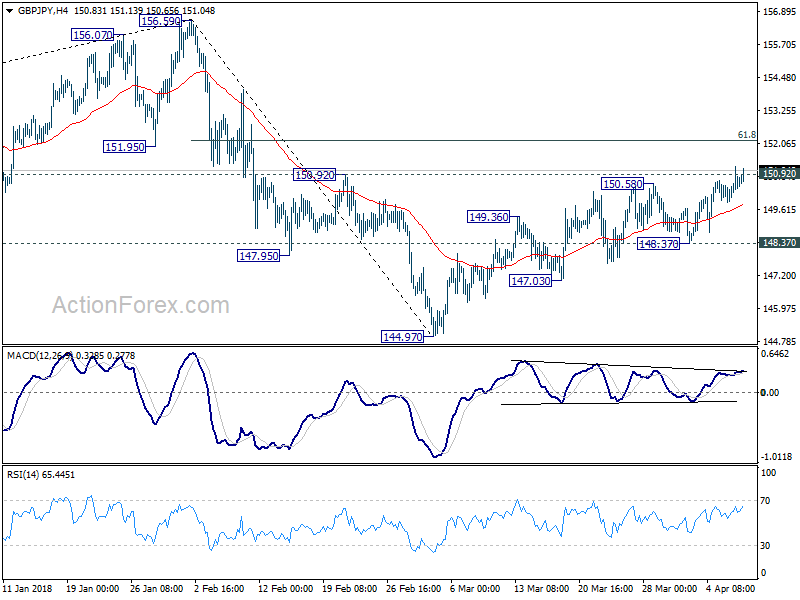

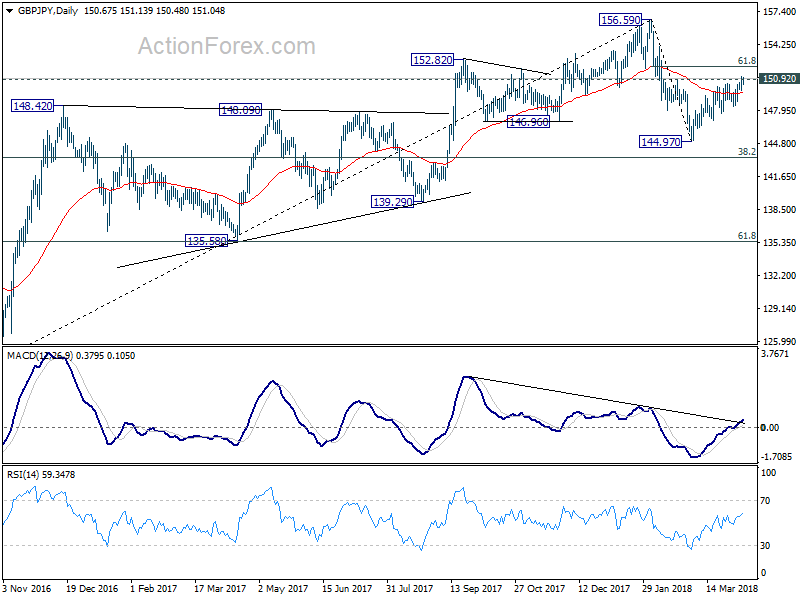

GBP/JPY Daily Outlook

Daily Pivots: (S1) 149.91; (P) 150.57; (R1) 151.25; More...

GBP/JPY's rebound from 144.97 is trying to resume today but focus stays on 150.92 resistance. Firm break there will extend the rise to 61.8% retracement of 156.59 to 144.97 at 152.15 and above. The price actions from 144.97 are still corrective looking. Hence, we'll look for sign of loss of upside momentum as it approaches 156.59 high. However, break of 148.37 minor support should confirm rejection from 150.92 resistance. In that case, deeper fall should be seen through 144.97 to resume the decline from 156.59.

In the bigger picture, the case for medium term reversal has been building up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds. However, sustained trading above 150.92 will argue that the larger rise from 122.36 might still be in progress for another high above 156.59.

USD/CAD Might Find Buyers Soon

The USD/CAD dropped within the 1.2730-40 zone and we can clearly see an inverted head and shoulders formation at support. The price is currently capped below the EMA89 and we might see few possible scenarios. The drop within 1.2730-40 POC zone could possibly be used for buyers to push the price higher towards 1.2799. If the price makes a 1h close above 1.2800, then 1.2837 should be next. 1.2837 is very important resistance. We might see short term rejections from the level towards 1.2800 but a clear 1h or 4h close above 1.2850 should provide a continuation towards 1.2894 and eventually 1.2990. However a drop below 1.2705 will probably make a bearish move towards 1.2663-1.2650.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

UK Halifax House Price Index Expected To Decline From Last Month

The UK Halifax House Price Index had recovered last month from a reading of -0.6% in January and February up to 0.4% in March. A weaker number here can be attributed in part to the recent spell of winter weather. The Year over Year figure is still robust and is expected to come in around 2.1%.

Reports over the weekend came in that North Korea is prepared to talk with the US about denuclearisation. This led to a move in the Yen of about 20 pips but the market soon settled again. There has been little market reaction to the Chemical weapons attack in Syria over the weekend but this is a potential risk given that there has been a counter strike overnight. This puts Nato and Russian forces at risk of clashing accidentally.

The ECB's Coeure made a scheduled speech with the following comments: The EU is a vehicle that brings benefits of economic openness to the greatest number of its citizens. The ECB simulations on tariffs on US imports/exports would have significant adverse effects on the global economy. Falls in equity prices and prevailing uncertainty on retaliatory measures have already contributed to tighter financial conditions. ECB rate guidance will gain in importance and will see a change in the mix of policy instruments. The market can look through the impact of the trade spat. The ECB has seen some uptick in recent inflation numbers.

US Non-Farm Payrolls (Mar) was 103K v an expected 190K, from a prior 313K, which was revised up to 326K. This measures the change in the number of employed people in March. Average Hourly Earnings (MoM) (Mar) was 0.3% v an expected 0.2%, against 0.1% previously. The Unemployment Rate (Mar) was 4.1% v an expected 4.0%, with a prior of 4.1%. This measures the percentage of the total workforce unemployed and actively seeking employment during March. Average Hourly Earnings (YoY) (Mar) was as expected at 2.7%, against 2.6% previously. Average Weekly Hours (Mar) was as expected at 34.5, against a previous 34.5. Labour Force Participation Rate (Mar) was 62.95% v an expected 63.5%, against a prior reading of 63.0%. This data showed a pickup in unemployment and a miss on the number of jobs created. The hourly earnings also picked up, indicating a rise in inflation and putting pressure on the Fed to hike sooner. USDJPY sold off from 107.411 to a low of 106.983 after these data releases.

Canadian Unemployment Rate (Mar) was as expected, unchanged from the previous reading of 5.8%. Participation Rate (Mar) was also unchanged, as expected, at 65.5%. Net Change in Employment (Mar) was 32.3K v an expected 20.0K, against a prior 15.4K. Unemployment had fallen to 5.7%, the lowest levels in ten years, in November but ticked up slightly in December with the largest drop in the Net Change in Employment data since 2009. USDCAD sold off from 1.27831 to 1.27323 from this data.

Canadian Ivey Purchasing Managers Index s.a. (Mar) was 59.8 v an expected 60.2, against a previous 59.6. Ivey Purchasing Managers Index (Mar) was 64.7 against 58.4 previously. This data missed the expected number but is still showing robust growth, continuing one of the longest positive runs, with 20 months above 50.0. USDCAD recovered its earlier losses and moved up from 1.27322 to 1.27839 after this data release.

UK BOE Governor Carney spoke at the International Climate Risk Conference for Supervisors, in Amsterdam. He said: we need to consider the financial impacts of weather-related events. “Intense hurricanes, of the type most likely to cause large insurance losses, seem to be getting more frequent and the chance of two or more intense hurricanes occurring close together may be higher than previously thought.”

Baker Hughes US Oil Rig Counts was released with a headline number of 808 against the previous week's 798. The number of rigs has moved above 800 after hovering around the level over the last few months. A firm reading above 800 next time could start to put pressure on crude prices as supply comes online.

US Fed Chairman Powel spoke about the economic outlook at the Economic Club of Chicago. He made the following comments: Further gradual rate hikes best promote growth and the US economy will require gradual hikes. The risks to the economic outlook are roughly balanced and 12-month inflation readings should move up notably this spring. Inflation could rise to unwelcome levels if the Fed waits too long and the gradual hike approach has reduced risks for the economy. The moderate wage gains show the labour market is not excessively tight.

US Consumer Credit Change (Feb) was $10.60B v an expected $15.00B, against a reading of $13.91B prior, which was revised up to $15.59B. This has been moving lower since reaching a high of $28.00B in January but there are seasonal factors that lead to a drop in the New Year. USDCAD sold off from 1.27849 to 1.27686 caused by this data release.

EURUSD is unchanged overnight, trading around 1.22840.

USDJPY is up 0.08% in early session trading at around 106.976.

GBPUSD is up 0.05% this morning, trading around 1.40979.

USDCAD is up 0.05% in early trade at around 1.27709.

Gold is unchanged in early morning trading at around $1,333.30.

WTI is up 0.53% this morning, trading around $62.30.

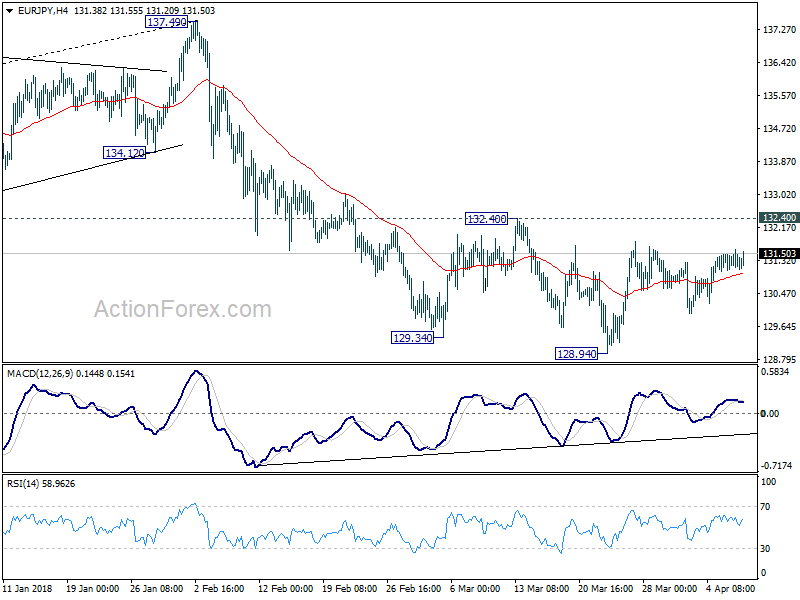

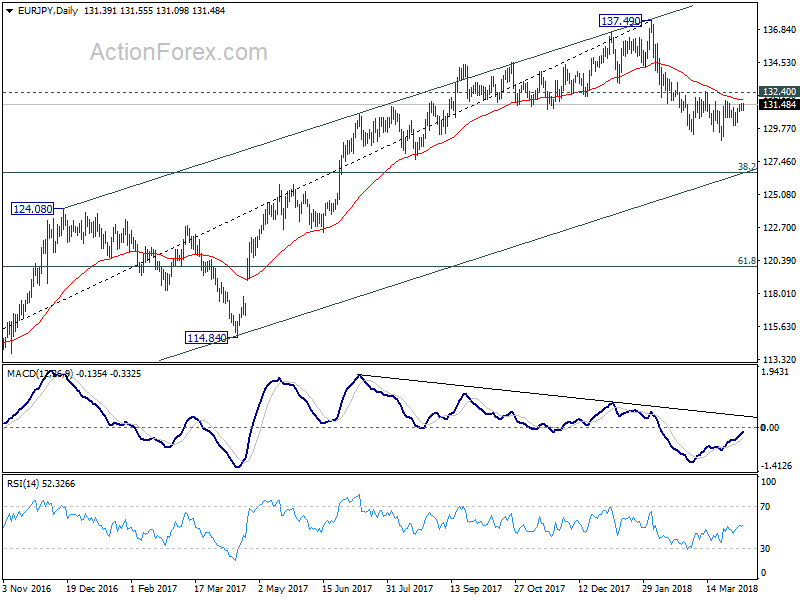

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.06; (P) 131.33; (R1) 131.59; More....

Intraday bias in EUR/JPY remains neutral as consolidation from 128.94 is still unfolding. As long as 132.40 holds, near term outlook remains bearish for deeper fall. On the downside, break of 128.94 will extend the whole fall from 137.49 to 126.61 medium term fibonacci level next. Nonetheless, break of 132.40 should confirm short term bottoming and turn bias back to the upside for stronger rebound.

In the bigger picture, current development argues that rise from 109.03 (2016 low) has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. Sustained break there would pave the way to 61.8% retracement at 119.90. On the upside, break of 132.40 resistance will indicate that the pull back is completed and bring retest of 137.49. But still, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, outlook is neutral at best for consolidations.

UK Halifax House Price Index, BoC Business Outlook & NZIER Business Confidence

At 07:30 GMT, UK Halifax House Price Index (MoM) (Mar) is expected to be 0.2% against 0.4% previously. UK Halifax House Price Index (3m/YoY) (Mar) is expected to be 2.1% against 1.8% previously. This data has been declining since hitting a high of 3.9% in June 2014. GBP crosses may be affected by this data release.

At 14:30 GMT, Bank of Canada Business Outlook Survey will be published. CAD crosses may be moved by this data release.

At 22.00 GMT, New Zealand NZIER Business Confidence (QoQ) (Q1) data will be released with the previous reading coming in at -12%.

Major data releases for this week:

On Tuesday, at 12:15 GMT, Canadian Housing Starts s.a (YoY) (Mar) will be released, with a previous reading of 229.7K. This data is showing strong performance, despite indicators that the headline number will decline this month. CAD pairs may see an increase in price movement from this data.

At 12:30 GMT, US Producer Price Index data will be released.

On Wednesday, at 05:00 GMT, Reserve Bank of Australia Governor Lowe will be speaking about recent developments in the Australian and global economies at the Australia-Israel Chamber of Commerce, in Perth.

At 12:30 GMT, US Consumer Price Index data will be released.

On Thursday, at 09:00 GMT, Eurozone Industrial Production data will be released.

At 11:30 GMT, ECB Monetary Policy Meeting Accounts will be published.

At 12:30 GMT, US Jobless Claims data will be announced.

On Friday, at 06:00 GMT, German Harmonised Index of Consumer Prices will be released.

At 14:00 GMT, US University of Michigan Consumer Sentiment Index will be released.