Sample Category Title

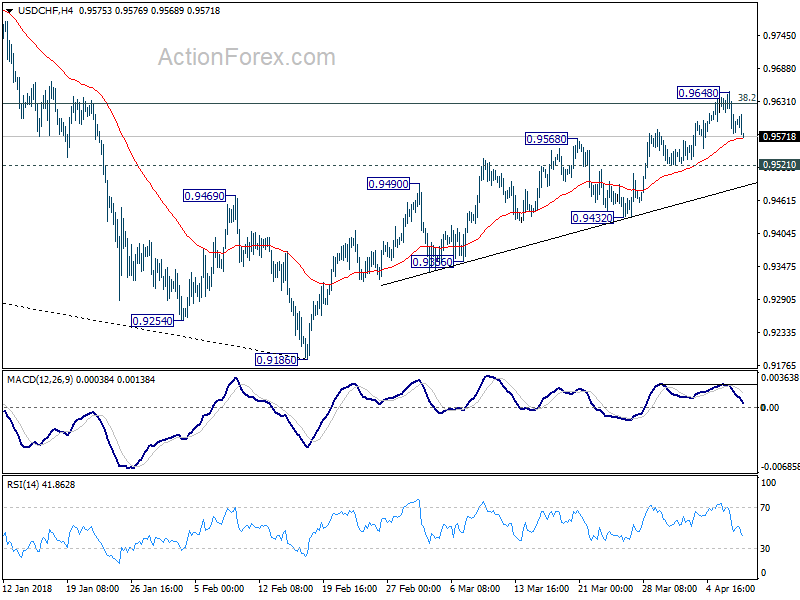

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9563; (P) 0.9605; (R1) 0.9634; More...

USD/CHF's decline from 0.9648 extends lower today. But it's still staying above 09521 minor support. Intraday bias remains neutral at this point. On the downside, break of 0.9521 minor support will indicate rejection by 0.9626 key fibonacci resistance. Intraday bias would then be turned back to the downside for 0.9432 support first. Break there will also confirm completion of rebound from 0.9186 and turn outlook bearish. On the upside, sustained break of 0.9626 will be another evidence of larger reversal. In this case, further rise would be seen to next fibonacci level at 0.9900.

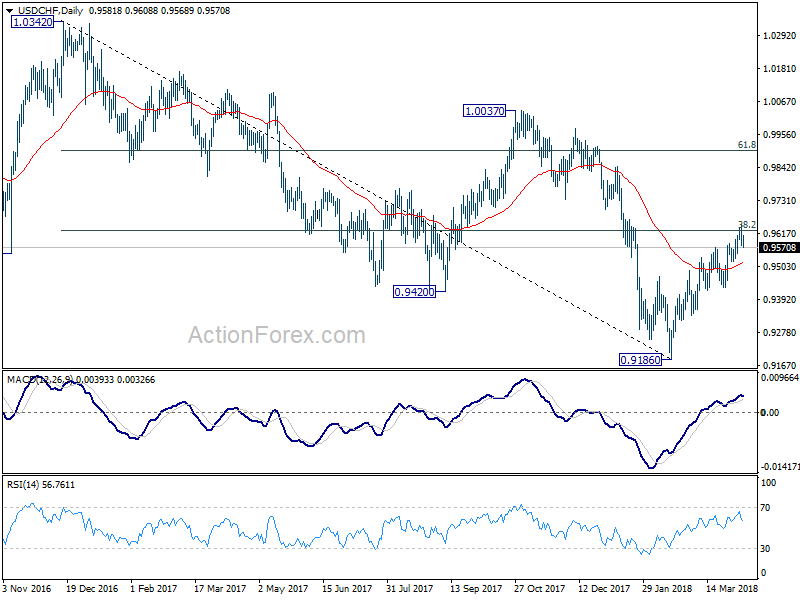

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above. However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

Stocks Rebound Eases after China Devaluation Talk but Dollar Edges Up

Here are the latest developments in global markets:

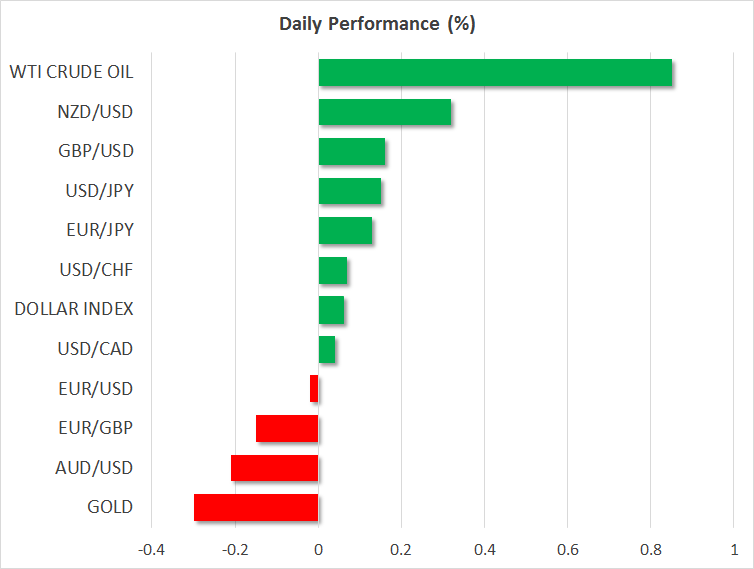

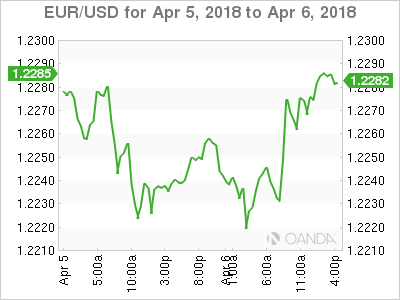

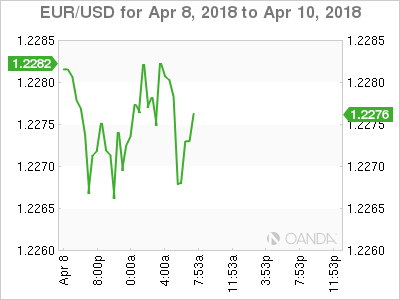

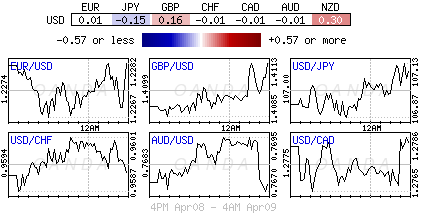

FOREX: Trade tensions continued to dominate the market theme as the US open approached. A tweet by President Trump on Sunday about the trade dispute with China went some way in lifting risk appetite in Asian trading on Monday. However, a report by Bloomberg that China is considering a gradual depreciation of the yuan knocked back the Australian dollar in European trading, as well as the Chinese currency. The aussie was hit hard, as Australian exports to China could suffer significantly from a weaker yuan, and slid to a one-week low of $0.7649. The yuan meanwhile tumbled to a 2-week low of 6.3168 per dollar from around 6.2950 in onshore trading. The euro also lost some ground, slipping to $1.2267 after the Eurozone sentix index decline sharply in April, missing expectations. Sterling was flat around $1.41, showing little reaction to a surprise monthly jump in UK house prices in March, according to figures from Halifax. The US dollar remained unfazed however by the China devaluation story, as the greenback extended its overnight gains. Dollar/yen was last trading higher 0.2% at 107.14 and the dollar index was up a similar amount to 90.24.

STOCKS: European stocks gave back some of their earlier advances as the risk of another currency devaluation by China hurt sentiment for risk assets. However, major indices in the region remained in positive territory, with the Euro Stoxx 50 index last trading 0.5% higher. UK shares were the exception though as the FTSE 100 was flat on the day. In the US, expectations of strong corporate earnings results for the first quarter, as well as some easing of trade tensions since Friday led the e-mini futures for the Dow Jones, S&P500 and the Nasdaq Composite between 0.7% and 1% higher.

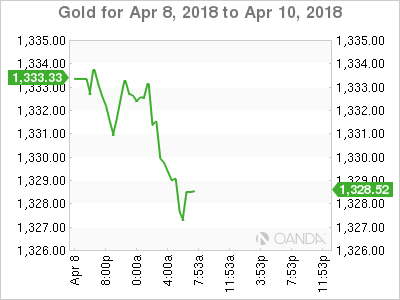

COMMODITIES: Major commodities enjoyed a bounce on Monday along with equities. A heated war of words between the US and China on Friday had driven oil prices to closer lower by 2%. Another rise in the Baker Hughes oil rig count in the US last week also weighed on the commodity. But prices turned higher today, with WTI oil holding on to 0.2% gains at $62.21 a barrel, and Brent crude up 0.5% at $67.41 ahead of the US open. Gold retreated however, finding little safe-haven support from reports that Israel had allegedly carried out missile strikes on a Syrian airbase. The US had earlier been suspected of carrying out the strikes, which was denied by the Pentagon. The yellow metal was last down 0.4% at $1328 an ounce.

Day Ahead: Quiet start but Xi speech, US inflation and earnings season coming up later this week

While there seemed to be no let-up in the trade stand-off between the US and China, many investors remained hopeful that a full-blown trade war can still be averted and chose instead to focus on the week’s upcoming risk events. The first of which comes on Tuesday when President Xi of China makes a keynote address at the Boao Forum for Asia. The speech could be significant if President Xi uses the event to deescalate the trade dispute between the two nations. The Chinese leader will likely announce economic reforms and offer the US more market access, appeasing the US side. But if the proposals don’t go far enough, the US may continue to play hardball.

On Wednesday, all eyes will be on the US CPI figures for March, and on Friday, US corporate giants, including JP Morgan, Well Fargo and Citigroup will report their latest quarterly earnings.

Ahead of all that though, speeches by European Central Bank policymakers will be eyed. ECB Vice President Vitor Constancio will present the Bank’s annual report at the European Parliament at 13:00 CET, while Governing Council member Peter Praet will participate in the European Finance Forum in Germany at 16:45 GMT.

The euro has come under negative pressure recently following disappointing business confidence gauges for the Eurozone. A deep slowdown could hamper the ECB’s efforts to pull the plug on its stimulus program. Investors will therefore be paying special attention to policymakers’ views on the economic outlook. Hawkish comments could spur the euro above immediate resistance at $1.2290 handle, but any signs of a more cautious tone could push the single currency below $1.22.

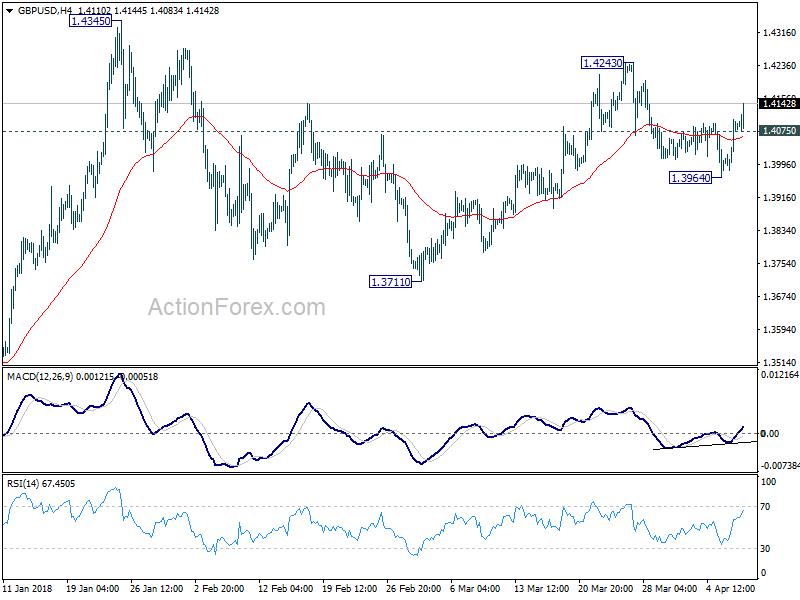

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4011; (P) 1.4058; (R1) 1.4134; More....

GBP/USD's rally from 1.3964 continues today and reaches as high as 1.4139 so far. Intraday bias remains on the upside for 1.4243 resistance first. Break will target a test on 1.4345 high next. On the downside, below 1.4075 minor support will turn intraday bias neutral first. But outlook will stay cautiously bullish as long as 1.3964 support holds.

In the bigger picture, as long as 1.3651 resistance turned support holds, medium term outlook in GBP/USD will remain bullish. Rise from 1.1946 is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4267) so far. Break of 1.3651 will be the first sign of medium term reversal and turn focus to 1.3038 support for confirmation.

Sterling Surges Broadly, Taking Europeans Higher; Dollar Selling Emerges into US Session

Sterling surges broadly today and is so far trading as the strongest one. Some point to solid housing data as a trigger for the buying. Mortgage lender Halifax house price rose more than expected by 2.7% in Q1. And that should be something welcomed by BoE hawks on their push for May rate hike. Nonetheless, to us, the Pound's rally today is more technical than fundamental. In particular, UK seems to have turned quiet after Brexit transition deal, while trade war drums are beating elsewhere in the world. As pointed out earlier in the Daily Report, GBP/USD does extend it's rebound from 1.3964 and affirm it's near term bullish news. GBP/JPY's break of 150.92 resistance should now align the bullish outlook together.

Elsewhere, in the currency markets, Dollar is under heavy selling right into US session, especially against European majors. But for the day, Yen is trading as the weakest one. Canadian Dollar followed as the second weakest as it's getting more unlikely for even a symbolic NAFTA deal to be signed this week. Mexican Economy Minister Ildefonso Guajardo was quoted that there aren't conditions right now for NAFTA deal to be reached this week. He believed that is 80% chance of a symbolic, principle agreement by the first week of May, as the US would like to push for it.

China said to consider currency devaluation as a weapon in trade spat

Ahead of China President Xi Jinping's address in the Boao Forum for Asia on Tuesday, there are rumors that China is considering currency devaluation as a weapon in the trade spat with the US. Bloomberg reported that Chinese officials are studying the impact of yuan depreciation on two fronts. Firstly, analysis was taken to look at using currency depreciation as a weapon in the trade war with the US. Secondly, it's also studied how yuan depreciation could help offset any trade deal with US that curb exports.

However, the accuracy of the news is suspectable as there was no named source, and Bloomberg just said it's from "people familiar with the matter", not even an government officials. Also, Yuan devaluation could destabilize the China's own markets, and that could do more harm to itself than to the US. Politically, it's against what China is portraiting. That is, China sees itself as following WTO rules and is trying to draw support from other countries against US unilateralism and protectionism. Devaluating Yuan would only alien China from those whom it could ally against the US on trade.

Meanwhile, there were expectations that Xi would make use of the Boao Forum fight back against the US. Or, there were expectations that Xi would say something that eventually launch trade negotiations. But it should be noted that Xi's leadership and communication style is clearly very different from Trump's. It's somewhat unrealistic to expect him to say something over the top.

Meanwhile, China is so far adopting a passive but quick in response tactic. That is, it wouldn't anything until the US make a step. Such tactics give China a ground to claiming that the US started the problems. Hence, it's expected that is the US doesn't initial a discussion, there won't be negotiations. So far, we only see Trump raising the threats to China. We saw Trump ordering Trade Representative to study tariffs on another USD 100b of Chinese imports. But we haven't seen Trump ordering anyone to start the negotiation quickly. No matter what Xi says tomorrow, the ball would still be in Trump's court.

Eurozone Sentix: Significant economic slowdown must now be assumed

Eurozone Sentix investor confidence dropped notably to 19.6 in April, down from 24.0 and missed expectation of 19.6. Current situation index dropped from 24.0 to 19.6, continuing the decline from January's high of 32.9. Expectation index turned negative to -1.5, down from March's 4.3. That's also a continuation of the fall from 18.8 started back in January. Sentix noted in the released that the global economy is "cooling off" And negative expectation for Eurozone for indicated "a turnaround in the previous months" and "a significant economic slowdown must now be assumed." In particular, the customs dispute fueled by US President Donald Trump are "leaving their traces".

Regarding the US, Sentix warned that "common sense" would assume the US demands on trade were "merely negotiation tactics". But Trump is consistent working through its "America first" agenda, thus, the threats could become implementations. The "positive effects of the tax reform have quickly evaporated, and expectations for the US economy are plummeting."

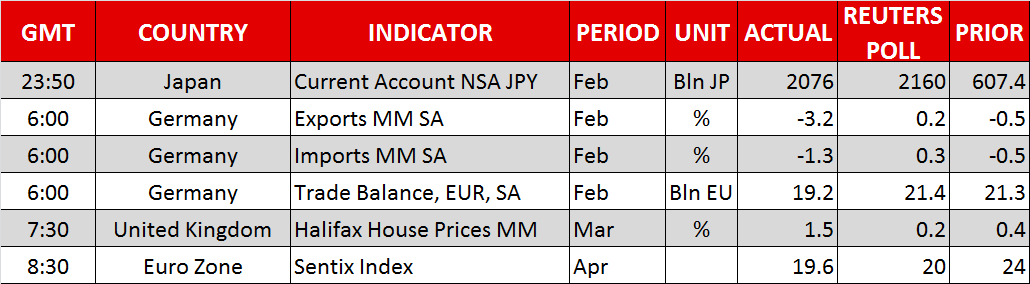

Also released in European session, German trade surplus narrowed to EUR 19.2b in February. Swiss unemployment rate was unchanged at 2.9% in March.

BoJ Kuroda reiterated there's some distance to 2% inflation

BoJ Governor Haruhiko Kuroda held his inaugural press confidence today. There he repeated familiar comments. Kuroda said that while the "economy and prices are doing quite well now", there is still "some distance" to achieving the 2% inflation target. And therefore, it's "inappropriate to tighten policy or diminish monetary support" for the sake of creating "policy room to cope with a future downturn:. And, he emphasized that any monetary policy shift would be cautious and gradual" just what what Fed and ECB are doing.

Released from Japan today, current account surplus narrowed to JPY 2.02% in February. Consumer confidence was unchanged at 44.3 in March.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4011; (P) 1.4058; (R1) 1.4134; More....

GBP/USD's rally from 1.3964 continues today and reaches as high as 1.4139 so far. Intraday bias remains on the upside for 1.4243 resistance first. Break will target a test on 1.4345 high next. On the downside, below 1.4075 minor support will turn intraday bias neutral first. But outlook will stay cautiously bullish as long as 1.3964 support holds.

In the bigger picture, as long as 1.3651 resistance turned support holds, medium term outlook in GBP/USD will remain bullish. Rise from 1.1946 is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4267) so far. Break of 1.3651 will be the first sign of medium term reversal and turn focus to 1.3038 support for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Construction Index Mar | 57.2 | 56 | ||

| 23:50 | JPY | Current Account (JPY) Feb | 1.02T | 1.39T | 2.02T | |

| 05:00 | JPY | Consumer Confidence Mar | 44.3 | 44.5 | 44.3 | |

| 05:45 | CHF | Unemployment Rate Mar | 2.90% | 2.90% | 2.90% | |

| 06:00 | EUR | German Trade Balance Feb | 19.2B | 23.1B | 21.3B | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Apr | 19.6 | 20.8 | 24 | |

| 14:30 | CAD | BoC Overall Business Outlook Survey Q1 |

BoJ Kuroda: Inappropriate to tighten policy or diminish monetary support

BoJ Governor Haruhiko Kuroda held his inaugural press confidence today. Here are some comments:

- "I think the process of any shift (from easy policy) would be cautious and gradual, as with U.S. and European central banks,"

- "The economy and prices are doing quite well now but there's some distance to achieving 2 percent inflation,"

- "It's inappropriate to tighten policy or diminish monetary support to create policy room to cope with a future downturn"

The comments are basically the same as what we heard from Kuroda repeatedly.

Trade Spat Fallout To Direct Markets

Monday April 9: Five things the markets are talking about

This week, the Fed and the European Central Bank (ECB) release minutes of their latest meetings, and China reports import, export (Friday) and inflation data (Tuesday).

Last Friday, Fed Chair Powell reaffirmed the central bank's slow and steady path of raising interest rates. The March meeting minutes likely will reflect plans to continue this pace. U.S CPI data and FOMC minutes are due Wednesday.

China's consumer inflation likely retreated in March from a more than four-year high in February as the Lunar New Year holiday effects waned. The market expects CPI to rise by about +2.6% in March y/y, compared with February's +2.9%. The country's PPI probably rose about +3.2%, easing from February's +3.7%.

On Thursday, the Bank of Mexico releases a policy statement on the heels of a strengthening MXN – in late March, the peso was the best amongst the G20 pairs. In its last policy statement, the bank left the door ajar for an additional rate increase. The ECB will release minutes of its March 7-8 meeting, when it signalled a shift toward tighter monetary policy by dropping a long-held pledge to accelerate its bond-buying program if the region's economy deteriorates.

Note: Attention now turns to China's Boao Forum (Tuesday), where President Xi is among senior officials scheduled to speak. Markets waits for any reference to trade.

1. Stocks in the black

Despite continued sabre-rattling on trade over the weekend between Washington and Beijing, Asia and Europe's major bourses rallied again overnight as we head into Q1's U.S earnings season.

In Japan, stocks recovered from the previous session's drop and edged a tad higher, lifted by defensive shares. Despite ongoing concerns about an U.S/China trade spat, a rise in U.S stock futures has helped calm sentiment for now. The Nikkei ended the day up +0.5%, while the broader Topix rallied +0.35%.

Down-under, Aussie stocks rallied on Monday, with the health care sector and consumer staples helping to cool nervousness over an escalating U.S/China trade spat. The S&P/ASX 200 index gained +0.4%, its third gain in four sessions. It was little changed on Friday. In S. Korea, the Kospi was up + Kospi was up +0.6%.

In Hong Kong, stocks rallied on hopes that the U.S and China can reach a deal to avoid trade war. The Hang Seng index rose +1.3%, while the China Enterprises Index gained +0.9%.

In China, stocks were tepid as investors pondered global trade developments. At the close, the Shanghai Composite index was up +0.3%, while the blue-chip CSI300 index was down -0.1%.

In Europe, regional indices trade higher across the board extending its two-week rally as worries over a potential global trade war fade.

U.S stocks are set to open in the ‘black' (+0.7%).

Indices: Stoxx600 +0.5% at 376.6, FTSE +0.1% at 7192, DAX +0.9% at 12352, CAC-40 +0.4% at 5280, IBEX-35 +0.9% at 9770, FTSE MIB +0.6% at 23070, SMI +0.8% at 8739, S&P 500 Futures +0.7%

2. Oil prices firm, but trade worries and Syria keep market on edge

Oil markets have steadied ahead of the U.S open after slumping around -2% last Friday on concerns over a Sino/U.S trade dispute, as well as increased U.S drilling activity.

Investors are also eyeing the situation in Syria after reports – denied by the U.S – that U.S forces had struck a major air base there.

Brent crude futures are at +$67.42 per barrel, up +31c, or +0.5%. U.S WTI crude futures are at +$62.31 a barrel, up +25c, or +0.4%, from Friday's close.

Note: With Chinese markets closed last Thursday and Friday, Shanghai crude futures played catch-up overnight, dropping -0.2% to around +¥401.4 yuan ($63.73) per barrel.

Stateside, Baker Hughes data on Friday showed that drillers added +11 rigs looking for new production in the week to April 6, bringing the total count to 808, the highest level since March 2015.

Gold prices are little changed ahead of the U.S open as the market awaits for any new developments on the simmering trade spat between the U.S and China. Spot gold is steady at +$1,332.75 an ounce.

Note: On Friday, prices hit a two-week low of +$1,321.16 an ounce, before closing +0.5% higher. U.S gold futures are unchanged at +$1,335.80 an ounce.

3. Sovereign yields little changed

Sovereign yields are expected to trade in a tight range as you go out the curve.

Yields continue to hover atop of their recent levels as investors are less anxious to sell amid heightened macro uncertainty and are reluctant to buy as Fed and ECB stay broadly on course.

With President Trump having raised the stakes in the trade stand-off, the near-term upside in 10-year Treasuries, Bunds and Gilts yields seems even more capped.

The yield on U.S 10-year Treasuries has gained +2 bps to +2.79%. In the U.K, the 10-year Gilt yield has increased less than +1 bps to +1.396%, while in Germany; the 10-year Bund yield was unchanged at +0.50%, the lowest in almost three-months.

4. Dollar maintains firm tone

The ‘mighty' USD has maintained a firm tone ahead of the open stateside as the global trade concerns continued to simmer. The buck is looking to continue its gains for the second consecutive week with market concerns over trade continuing to pivot from NAFTA to China.

The EUR/USD has eased by -0.2% at €1.2275, while USD/JPY was a tad firmer by +0.2% at ¥107.15 area.

Consensus expects the EUR to trade within its €1.22 to €1.25 range for the medium term. On Wednesday, U.S CPI is expected to show an uptick in core inflation, but the base effect is not expected to provide enough support to the USD to drive EUR/USD sustainably below current levels.

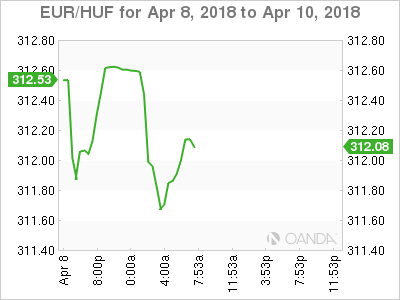

Hungarian assets rallied overnight after Prime Minister Viktor Orban won a third term in yesterday's election, eliminating the risk of unpredictable policy changes. USD/HUF, is trading at $253.92, down -0.3%.

5. Eurozone Sentix investor confidence declines

Data from the think tank Sentix this morning showed that Eurozone investor confidence declined notably in last month on fears of trade war.

The investor sentiment index fell to 19.6 in April from 24.0 in March. Market expectations for the score were forecast to remain unchanged at 24.0.

The third consecutive decline was due to a significant deterioration in economic expectations.

Digging deeper, the current situation index came in at 43.0, down from 45.8 a month ago. Even though the current situation was still rated as excellent, the prospects for the future have become much gloomier.

The expectations index turned negative for the first time in nearly 24-months. The score was -1.5 vs. 4.3 in March.

Data showed that the investor confidence index for Germany declined to 24.4 in April from 29.1 in March.

US Futures Pare Losses As Trade Conflict Rumbles On

- Will Xi Jinping's Speech Aid or Inflame Tensions Between US and China?

- Earnings Season and FOMC Minutes Key This Week.

'There is a hope that Tuesday's speech may contain some commitments that will help kick start negotiations between the world's two largest economies'

US equity markets are expected to open almost 1% higher on Monday, paring another substantial day of losses on Friday as the trade conflict between the US and China ramped up.

Whether the moves we're seeing at the start of the week in Asia and Europe – and in US futures – reflect optimism that a solution will be found or are simply a case of profit taking on Friday's moves isn't clear but a speech from Chinese President Xi Jinping scheduled for Tuesday may point towards the former. China has been gradually opening up its markets for a long time now and there is a hope that Tuesday's speech may contain some commitments that will help kick start negotiations between the world's two largest economies.

The message from Larry Kudlow and Peter Navarro – White House Senior Economic Advisor and Director of the White House National Trade Council, respectively – in recent days has been that, while US President Donald Trump is willing to embark on tariffs, he is open to negotiations in order to avoid this. This very much supports the view that this is simply a tactic to get China to the negotiating table and perhaps we can start to see less confrontational talk and more willingness to find a diplomatic solution.

This makes Xi's speech on Tuesday one of, if not the, most important event for markets this week. Many expect announcements on further opening of the Chinese economy, the question is how far he'll go and whether it will be enough to satisfy the US administration, at least to the point that it takes on a less provocative approach. Any indication that this is the case could provide some reprieve for markets and lift investor sentiment.

'It will be interesting to get a sense of how close policy makers were to bringing forward an extra rate hike to this year and what it will take for this to change in June.'

The start of the week at least is likely to centre around trade in the absence of any other events. First quarter earnings season kicks off later in the week which will be of keen interest to investors as we get insight into what impact tax reforms have had on the bottom line, as well as how companies have fared at the start of the year.

The other event of note this week will be the Federal Reserve minutes on Wednesday. The central bank released new economic projections in March which including upward revisions to growth this year and next, slightly higher inflation and, most importantly, an additional rate hike next year and higher again in 2020. The revision comes in response to Trump's tax reforms which passed at the end of 2017 and will provide an additional stimulus for an economy that is already performing quite well. It will be interesting to get a sense of how close policy makers were to bringing forward an extra rate hike to this year and what it will take for this to change in June.

Strong Start For Markets | Deutsche Bank And Novartis Under Focus

- Investors shaking off all those concerns

- A more friendly solution could be the outcome

- Q2 earning seasons is going to start this week

Investors have been nervous and remained over the edge due to the heightened tensions around the trade war between the US and China. If a trade war does actually break out between the US and China, both counties are going to lose from this in terms of their economic growth. At the same time, corporate profits would also see the adverse impact.

Having said this, the only silver lining in this entire situation would be that it is another tactic deployed by Mr Trump. A man who knows how to bring the opponents to the negotiating table. The equity markets over in Asia has kicked off the week on a positive note by shaking off all those concerns. The US markets on Friday also closed higher and they are back above the critical 200-day moving average.

Similarly, the European markets also closed strong last week and traders are picking up the moment where they left off. Markets have seen a massive surge in volatility and there is no shortage of up and down swings in the markets. The main reason behind any optimism (when it comes to the US and China trade war) is that it is only a strategic tactic, deployed by President to pressure China in order to get a deal what he desires. However, if this tactic becomes a reality, the sentiment in the market would be highly negative.

Over the weekend, Mr Trump has used his favourite media channel, Twitter, to communicate more signs of optimism that perhaps a more friendly solution could be the outcome when it comes to the trade war.

The Q2 earning seasons is going to start this week. The focus among investors isn’t going to be the impact of the past changes in the US tax system, which was seen as a positive sign for the US corporates, but rather it would be on the impact of the trade war.

In terms of currencies, the dollar index is trading flat after a more disappointing US NFP data. The Fed chairman had a more upbeat tone during his speech on Friday after the US NFP however. It doesn’t seem like traders believe that the Fed is going to be any more aggressive, especially not under the current situation.

As the New CEO takes charge of the Deutsche Bank, looking at the analyst rating on the stock, the ratio is firmly skewed in favour of bears. The stock recomendation ratio among analyst is almost 3-to-1, which means sell recommendations are a lot higher. One thing which is optimistic about the new CEO is that he has plenty of inside knowledge about the bank among the new top leadership. The biggest challenge for Mr Sweing is to change the landscape for the bank's plunging revenue which is hitting multi-year low. We expect him to pull the bank out of many operations which are not profitable-get ready buyers. Overall, investors are a lot more optimistic about the new CEO and this is the reason that the stock is trading higher.

Gene therapy is one of the biggest areas of growth among healthcare and pharmaceutical companies. If you do not have a strong position in this area, the strategy is to acquire a firm which is playing a leading role and this is what really happened between Novartis AG and AveXis. The $8.7 billion dollar deal under which Novartis decided to buy AveXis is going to make Novartis's position more firm in gene therapy position- an area which is not only revolutionary but also classified as a game changer. AveXis product called AVXS-101 (to treat spinal muscular atrophy) is the jewel which Novartis wanted to acquire. The premium of 88% on Friday's AveXis close price paid by Novartis is still a bargain given the potential the product has.

Focus Remains On Trade

Notes/Observations

Asia:

- Market concerns over trade continue to pivot from NAFTA to China

- High expectations ahead of 1Q earnings season

Asia:

- China Mar Foreign Reserves: $3.143T v $3.147Te (FX Reserve data has registered increases in 13 of the past 14 months (declined in Feb 2018)

- North Korea confirmed Leader Kim Jong Un prepared to discuss denuclearization of the Korean Peninsula

Europe:

- Italy’s center-right alliance to present a united stance to President Mattarella during a second round of talks with party leaders this week. Move would be viewed as reducing chances of a pact between the League and the fellow-populist Five Star Movement

- S&P affirmed France sovereign rating at AA; outlook Stable

- Canadian ratings agency DBRS raised Spain sovereign rating to A from A (low), Stable trend

Americas:

- Fed Chair Powell: he and colleagues believed US economy would require further gradual interest rate increases. Inflation could rise to unwelcome levels if Fed waited for inflation and employment to hit goals

- Fed's Williams (moderate, voter): three to four rate hikes in 2018 remained appropriate; gradual rate rises help economy from overheating

- Fed's Evans (non-voter, dove): US economy was very strong; optimistic about hitting 2% inflation target. Need for accommodative monetary policy was less than it was before

- The reworking of NAFTA said not to be advanced enough to announce a deal in principle this month at the summit in Lima (April 13-14). Officials were still debating issues related to the auto sector.

- Senior Mexican Economy Ministry official: very convinced that new NAFTA trade agreement will be reached very soon

- Canada Foreign Min Freeland: NAFTA teams will continue to work intensively in days to come; have had some good conversations; have entered a new more intensive phase, had some constructive talks

- Treasury Sec Mnuchin: Did not expect there will be a trade war’, reiterated that the US’ intention is to continue to have talks with China

- White House Econ Adviser Kudlow: Believes solution to trade dispute with China is possible within three months but tariffs are not a bluff

- White House and certain Republicans in Congress said to be seeking to revise some of the federal spending measures approved under the $1.3T spending bill (Reminder: President Trump previously expressed dissatisfaction with some of the spending in the $1.3T package)

- President Trump tweeted China will take down its trade barriers because it is the right thing to do, taxes will become reciprocal and a deal will be made on intellectual property’

Economic Data:

- (NL) Netherlands Feb Manufacturing Production M/M: -0.2% v -0.6% prior; Y/Y: 4.2 v +7.1% prior, Industrial Sales Y/Y: 6.9 v 5.1% prior

- (JP) Japan Mar Consumer Confidence: 44.3 v 44.5e

- (CH) Swiss Mar Unemployment Rate: 2.9% v 3.0%e, Unemployment Rate (Seasonally Adj): 2.9% v 2.9%e

- (DE) Germany Feb Current Account Balance: €20.7B v €22.9Be; Trade Balance: €18,4B v €20.1B; Exports MoM: -3.2% v +0.4%e; Imports M/M: -1.3% v +0.5%e

- (NO) Norway Feb Industrial Production M/M: -0.3% v +3.3% prior; Y/Y: 1.8% v 1.8% prior

- (NO) Norway Feb Manufacturing Production M/M: 0.2% v 1.0%e; Y/Y: +0.2% v -0.4% prior

- (DK) Denmark Feb Current Account Balance (DKK): 13.5B v 9.4B prior; Trade Balance: 7.0B v 6.0B prior

- (ZA) South Africa Mar Gross Reserves: $50.0B v $50.0Be; Net Reserves: $43.4B v $43.4Be

- (FI) Finland Feb Preliminary Trade Balance: -€0.3B v -€0.2B prior

- (JP) Japan Mar Eco Watchers Current Survey: 48.9 v 48.0e; Outlook Survey: 49.6 v 51.0e

- (AU) Australia Mar Foreign Reserves: A$76.6B v A$70.8B prior

- (SE) Sweden Apr SEB Housing Price Indicator: 7 v 4 prior

- (CZ) Czech Feb National Trade Balance (CZK): 18.0B v 16.0Be

- (HU) Hungary Feb Preliminary Trade Balance: €0.8B v €0.7Be

- (UK) Mar Halifax House Prices M/M: 1.5% v 0.1%e; 3M/Y: 2.7% v 2.0%e

- (SE) Sweden Mar Budget Balance (SEK): 6.4 v 49.9B prior

- (CH) SNB Total Sight Deposits for Week Ended Apr 6th(CHF): 574.9B v 575.4B prior

- (TW) Taiwan Mar Trade Balance: $6.0B v $3.9Be; Exports Y/Y: +16.7% v +7.1%e; Imports Y/Y: 10.4% v 9.1%e

- (EU) Euro Zone Apr Sentix Investor Confidence: 19.6 v 20.8e

Fixed Income Issuance:

- (EG) Egypt to sell EUR-denominated 8-year and 12-year notes

- (NO) Norway sold NOK4.0B vs. NOK4.0B indicated in 6-month bills; Avg Yield: 0.61% v 0.46% prior; Bid-to-cover: 1.61x v 2.39x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.5% at 376.6, FTSE +0.1% at 7192, DAX +0.9% at 12352, CAC-40 +0.4% at 5280, IBEX-35 +0.9% at 9770, FTSE MIB +0.6% at 23070, SMI +0.8% at 8739, S&P 500 Futures +0.7%]

Market Focal Points/Key Themes:

- European Indices trade higher across the board extending a 2 week rally as the pan-European benchmark remains on track to close at a 2 week high as worries over a potential global trade war fade.

- The Dax trades higher helped by share of Deutsche Bank following the announcement of Christian Sewing as the new CEO; Sulzer trader lower after buying back 5M shares, French Connection trades over 10% higher after divesting Toast, while Mothercare trades lower after reports of store closures.

- Healthcare giant Novartis announced the acquisition of AveXis in an $8.7B deal, elsewhere Oerilkon and Schmolz + Birkenback trade lower after holder Victor Vekselberg is said to be affected by the US sanctions.

Movers

- Consumer Discretionary [Mothercare [MTC.UK] -9.0% (Reports of possible store closures), Hollywood Bowl [BOWL.UK] +1% (Earnings), French Connection [FCCN.UK] +19% (Divestment)]

- Industrials [Sulzer [SUN.CH] -9% (Repurchases stock from Renova to avoid US sanctions)]

- Financials [Deutsche Bank [DBK.DE] +4.2% (Names new CEO)]

- Healthcare [EKF diagnostics [EKF.UK] +7% (FDA approval of Diaspect Tm)]

Speakers

- Turkey Presidential advisor Bulut: Steps to reduce interest rates to following govt package. Govt incentive package in response to cool down economy

- South Africa Fin Min Nene: Some domestic cities on the verge of collapse, cannot be allowed to occur

- China govt said to study a potential CNY currency (Yuan) devaluation as a tool in the current trade spat

- China Premier Li reiterated view that needed to oppose unilateralism and trade protectionism

- China Foreign Ministry reiterated that have not conducted negotiations with US on trade and saw the talks as impossible under current conditions

- Thailand Central Bank reiterated view that policy to remain accommodative; Had no policy of FX intervention for trade

- US and India official said to hold trade talks on Wed, Apr 10th

Currencies

- USD maintained a firm tone as the global trade concerns continued to simmer. The greenback looking to continue its gains for the 2nd straight week with market concerns over trade continuing to pivot from NAFTA to China. Dealers noted that we are moving in the window where the next semi-annual Treasury report would be published amidst of backdrop of rising trade tensions and could name countries that were considered to be manipulating their currency

- EUR/USD softer by 0.2% at 1.2275 while USD/JPY was firmer by 0.2% at 107.15 area.

Fixed Income

- Bund Futures trade 22 ticks lower at 159.35 after Euro zone Investor confidence for April declines. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 122.27 lower by 15 ticks continuing the respect of the 123 handle. Support continues stands at 121.25 then 120.85, with upside resistance at 123.35 then 123.85.

- Monday’s liquidity report showed Friday's excess liquidity fell to €1.864T from €1.868T prior. Use of the marginal lending facility fell from €40M to €0M.

- Corporate issuance saw the primary market finish with over $25B sold

Looking Ahead

- 05:30 (DE) Germany to sell €3.0B in 6-Month BuBills

- 06:00 (PT) Portugal Feb Trade Balance: No est v -€1.2B prior

- 06:00 (JP) BOJ Gov Kuroda press conference to mark his 2nd term

- 06:45 (US) Daily Libor Fixing

- 07:00 (BR) Brazil Mar FGV Inflation IGP-DI M/M: 0.7%e v 0.2% prior; Y/Y: +0.9%e v -0.2% prior

- 07:25 (BR) Brazil Central Bank Weekly Economists Survey

- 07:30 (CL) Chile Central Bank Traders Survey

- 07:30 (CL) Chile Mar Trade Balance: $0.9Be v $1.3B prior; Total Exports: $6.4Be v $6.4B prior; Total Imports: $5.5Be v $5.1B prior

- 07:30 (CL) Chile Mar International Reserves: No est v $38.4B prior

- 08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming actions in week

- 08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

- 08:05 (UK) Baltic Dry Bulk Index

- 08:15 (CA) Canada Mar Housing Starts: 218.0Ke v 229.7K prior

- 08:55 (FR) France Debt Agency(AFT) to sell combined €4.7-5.9B in 3-month, 6-month and 12-month BTF Bills

- 09:00 (MX) Mexico Mar CPI M/M: 0.4%e v 0.4% prior; Y/Y: 5.1%e v 5.3% prior, CPI Core M/M: 0.4%e v 0.5% prior

- 09:30 (EU) ECB announces Covered-Bond Purchases

- 09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

- 10:30 (CA) Bank of Canada (BOC) Q1 Loan Officer Survey: No est v -6.4 prior, Business Outlook Future Sales: No est v 8 prior

- 11:30 (US) Treasury to sell 3-Month and 6-Month bills

- 16:00 (US) Weekly Crop Progress Report

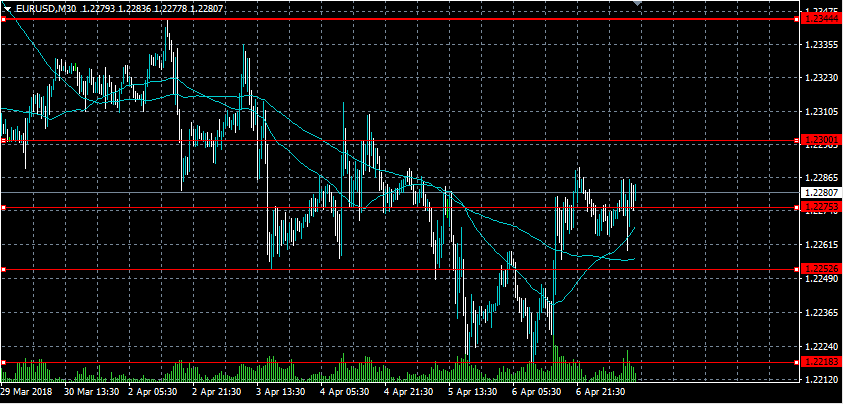

EURUSD Only Bullish Above 1.2275 Level

The euro continues to trade towards the top-end of its short-term trading range against the U.S dollar, with price-action now trading above the key 1.2275 level. The EURUSD pair has so far found intraday technical resistance from the 1.2290 level, with the 1.2300 level the next key upside hurdle for euro buyers. Moving into the U.S session, traders continue to look to the U.S dollar index for guidance, with the pivotal 1.2275 level on the EURUSD coming into focus yet again.

The EURUSD pair retains an intraday bullish bias while trading above the 1.2275 level, key upside resistance is currently found at the 1.2300 and 1.2344 levels.

If the EURUSD pair trades below the 1.2275 level for a sustained period, price-action will turn bearish. Key intraday support is then found at the 1.2252 and 1.2218 levels.