Sample Category Title

CAD surges on BoC Business Outlook Survey, CADJPY resuming rebound

Canadian Dollar surges as BoC's Business Outlook Survey painted a positive picture. In particular, business sentiments were supported by "healthy" sales prospects. Capacity and labor pressures are "evident" in most regions due to strong demand.

Here are highlights of the survey:

- Forward-looking sales indicators remain positive across most regions and sectors. Some firms expect a moderation in sales activity from high levels in the past year or a gradual slowing of the pace of the recovery in the energy sector.

- While firms' expectations for US economic growth have strengthened further, some cited rising protectionism and reduced competitiveness as factors limiting the impact on their sales.

- Although less so than in recent surveys, intentions to increase investment continue to be widespread. Employment intentions are solidly positive, based on firms' plans for hiring to support expected sales growth or to expand operations.

- Indicators of capacity pressures and labour shortages edged down but are still close to recent high levels. Remaining economic slack appears to be mostly concentrated in the energy-producing regions.

- Despite expectations for faster input price growth overall, on balance, firms continue to anticipate only modest acceleration in the growth of their output prices due to competitive pressures. Partly driven by rising labour costs, inflation expectations picked up but are still well within the Bank's inflation-control range of 1 to 3 per cent.

- While credit conditions were unchanged for most firms, the indicator points to a slight tightening.

- The Business Outlook Survey indicator continues to be high, signalling positive business sentiment.

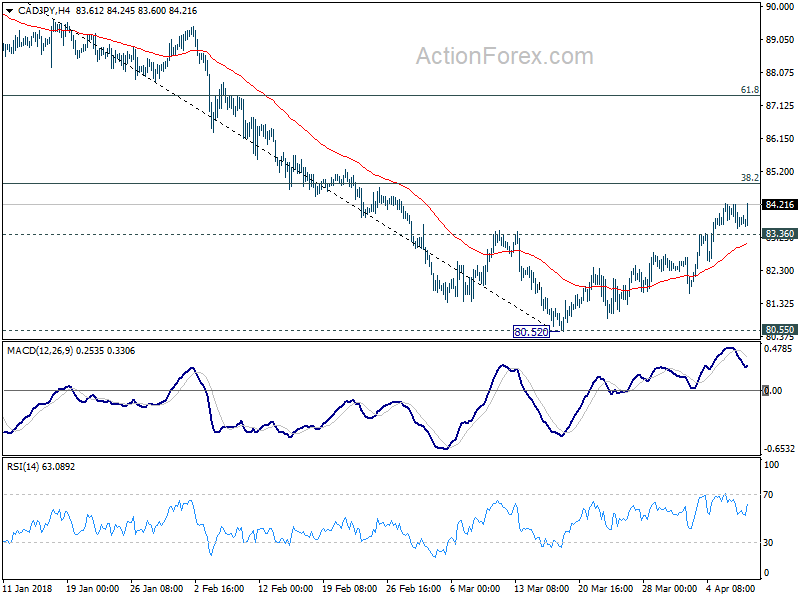

CAD is now the second strongest for the day while JPY remains the weakest one.

H action bias in CADJPY turned positive again.

H action bias in CADJPY turned positive again.

CADJPY's retreat was contained above 83.36 support, maintaining near term bullishness. The rebound from 80.52 is likely ready to resume for 38.2% retracement of 91.56 to 80.52 at 84.73.

CADJPY's retreat was contained above 83.36 support, maintaining near term bullishness. The rebound from 80.52 is likely ready to resume for 38.2% retracement of 91.56 to 80.52 at 84.73.

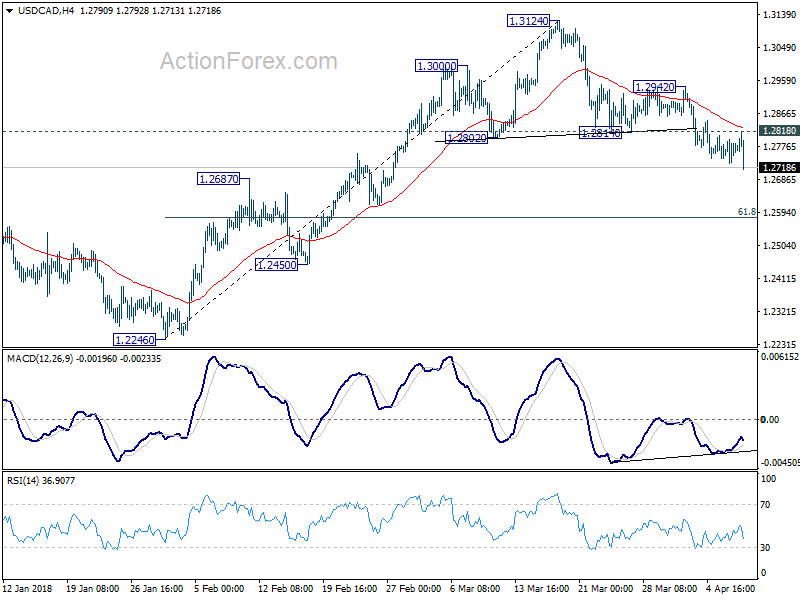

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2740; (P) 1.2767; (R1) 1.2806; More....

USD/CAD's fall resumed after brief consolidation and reaches as low as 1.2713 so far. Intraday bias is back on the downside. Fall from 1.3124 short term top should target 61.8% retracement of 1.2246 to 1.3124 at 1.2581 next. On the upside, above 1.2818 minor resistance will turn intraday bias neutral again. But near term outlook will remain bearish as long as 1.2942 resistance holds.

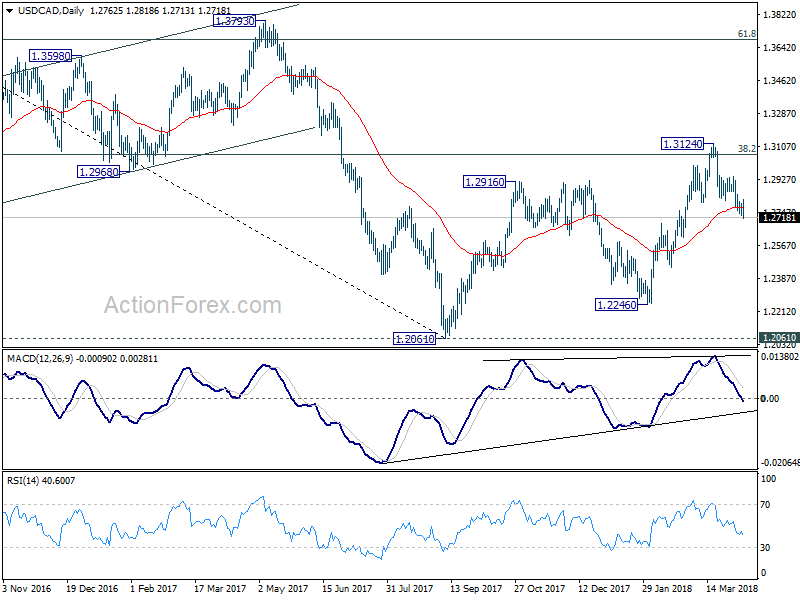

In the bigger picture, current development turns favors to the case that rise from 1.2061 is a corrective three wave pattern. It could have completed at 1.3124 after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Focus is now back on 1.2061 and 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

US CPI Preview: Monthly Moderation, Soaring Year-Ago Comps

CPI inflation is likely to moderate in March, with an overall gain of 0.1 percent and "low" 0.2 percent rise for core. A year after the now-infamous drop in wireless costs, core CPI should vault back above 2 percent yr/yr.

Monthly Gains to Moderate, but Year-Ago Inflation to Soar

CPI inflation has gotten off to a solid start this year. After a 0.5 percent increase in January—largely on the back of the biggest increase in core inflation in almost 12 years—there were few signs of payback in February. Both headline and core CPI rose 0.2 percent last month. The year-over-year rate of headline CPI rose to 2.2 percent, while the year-ago change in core CPI held steady at 1.8 percent.

For March, we expect monthly gains to moderate again. We forecast that headline CPI rose 0.1 percent amid an unusually small gain in energy prices for this time of year. We expect that core CPI will come in at a "low" 0.2 percent (0.15 percent), while the non-seasonally adjusted index should rise to 249.35.

The most eye-catching part of the March report is likely to be the leap in year-over-year inflation. March was the low point of last year's inflation slowdown. Core CPI posted a rare drop (down 0.07 percent) on the back of the now-infamous decline in wireless services. That makes for an easy base comparison in March. We expect core CPI to jump to 2.1 percent on a yearago basis and for headline inflation to rise to 2.5 percent.

What We'll Be Watching...

Cell-shock Lingers: Last year's cell-shock may reverberate through more flattering seasonal adjustment (SA) effects this March. The latest seasonal factors now shave off less from the NSA March figures than in prior years, having taken last year's drop as a regular change for this time of year, rather than the one-off we believe it to be (middle chart).

Core Goods—Four in a Row? The 7 percent decline in the broad trade weighted dollar since the start of 2017 has offered some modest support to core goods prices. While we expect this trend to continue, we are skeptical that core goods can string together a fourth consecutive increase. Apparel prices again looked unusually strong (up 1.5 percent after a 1.7 percent rise in January), while vehicle prices are under renewed pressure now that replacement demand following last year's natural disasters has faded.

Shelter: Core services inflation softened in February, in part due to the smallest gains in both primary rent and owners' equivalent rent in more than three years. While this might just be noise, we will be watching for signs that there may be more to it. Industry data show that apartment rent growth rolled over in 2016 amid a torrent of new units, but home prices have shown no such slowing as inventories remain exceptionally lean (bottom chart).

Energy: We expect that energy prices will be a slight drag this month. According to AAA, gasoline prices barely budged in March. With prices typically rising more prominently this time of year, the energy component is likely to decline after seasonal factors are applied.

Sunset Market Commentary

Markets:

The German Bund opened lower in line with improving risk sentiment and the US Note future’s losses in Asian trading. Comments from US top officials in favour of negotiation in the US/Chinese trade conflict provided the main argument. European dealings were characterized by one stretched yawn. Trading ranges of the Bund and the US Note future were extremely narrow and volumes low amid an empty eco calendar. European equity indices held on to opening losses, but are drifting away as the US trading session gets started. Contradicting Chinese comments on the negotiation phase negatively affect stocks and the dollar. Core bonds can’t profit at the moment, but moves on other markets suggest, if any, some support during the remainder of US dealings. US yields add 1.5 bps to 2 bps at the time of writing with the belly of the curve underperforming the wings. Changes on the German yield curve are limited between +0.2 bps and +0.5 bps. Peripheral yield spread changes vs Germany are almost unchanged.

(Currency) markets remain mainly focused on the trade saga between the US and China. This morning, markets considered comments from US officials during the weekend as a sign that tensions could ease. This ‘optimism’ was mainly visible on the equity markets. The impact on FX was limited. During the day, rumours swirled that China was studying the potential consequences of using a yuan devaluation in the trade conflict. Initially, the debate had little impact on the dollar. Later there were again other indications that in depth negotiations between the US and China (with concrete results) were still quite some way off. The dollar again proved to be the weakest link among the majors. EUR/USD rebounded north of 1.23. USD/JPY dropped back below 107. In a broader perspective, the US currency holds an indecisive trading pattern as a cautious bid was blocked after last week’s disappointing US payrolls.

There was no high profile news to inspire sterling trading. It was mainly driven by technical consideration and by the broader moves in the dollar. The afternoon decline of the dollar was also visible in cable. The pair rebounded to the mid 1.41 area. EUR/GBP is holding a tight range close to, but mostly slightly north of 0.87. The absence of negative headlines on Brexit and the expectations for a May BoE rate hike remain marginally sterling supportive.

News Headlines:

The Turkish lira felt more selling pressure with EUR/TRY touching a new all-time high, north of 5, as President Erdogan presented a new economic incentive package to boost the economy into the world top 10 ranking economies. His senior aide added that the package will be followed by steps to reduce interest rates.

The Russian ruble is the worst performer in the emerging markets specter after the US slapped new sanctions against the Russian business sector. EUR/RUB surged from 71.5 to 74, the highest level since the end of 2016. US President Trump also criticized Russian President Putin over the weekend for supporting the Syrian government.

German trade data disappointed this morning with exports declining by 3.2% M/M in February, below 0.4% M/M consensus and the biggest monthly drop in two years. It adds to fears that we’ve reached the German growth peak in Q4 2017. Imports decreased by 1.3% M/M compared to 0.5% M/M expectations. The trade balance rose less than forecast, from 17.3bn to 18.4bn.

Bloomberg reports that China is evaluating the potential impact of a gradual yuan depreciation, according to people familiar with the matter, as the country’s leaders weigh their options in a trade spat with US President Trump that has roiled financial markets worldwide. Official added that it’s impossible to negotiate under “current circumstances”. Investors now eye tomorrow’s speech by Chinese president Xi Jinping at the Boao Forum for Asia.

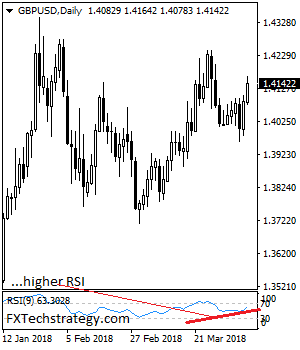

GBPUSD: Faces Further Corrective Recovery Higher

GBPUSD: The pair saw a follow through higher on the back of its Friday gain during Monday trading session today. Support lies at the 1.4100 level where a break will turn attention to the 1.4050 level. Further down, support lies at the 1.4000 level. Below here will set the stage for more weakness towards the 1.3950 level. Conversely, resistance stands at the 1.4200 levels with a turn above here allowing more strength to build up towards the 1.4250 level. Further out, resistance resides at the 1.4300 level followed by the 1.4350 level. On the whole, GBPUSD remains biased to upside on more strength.

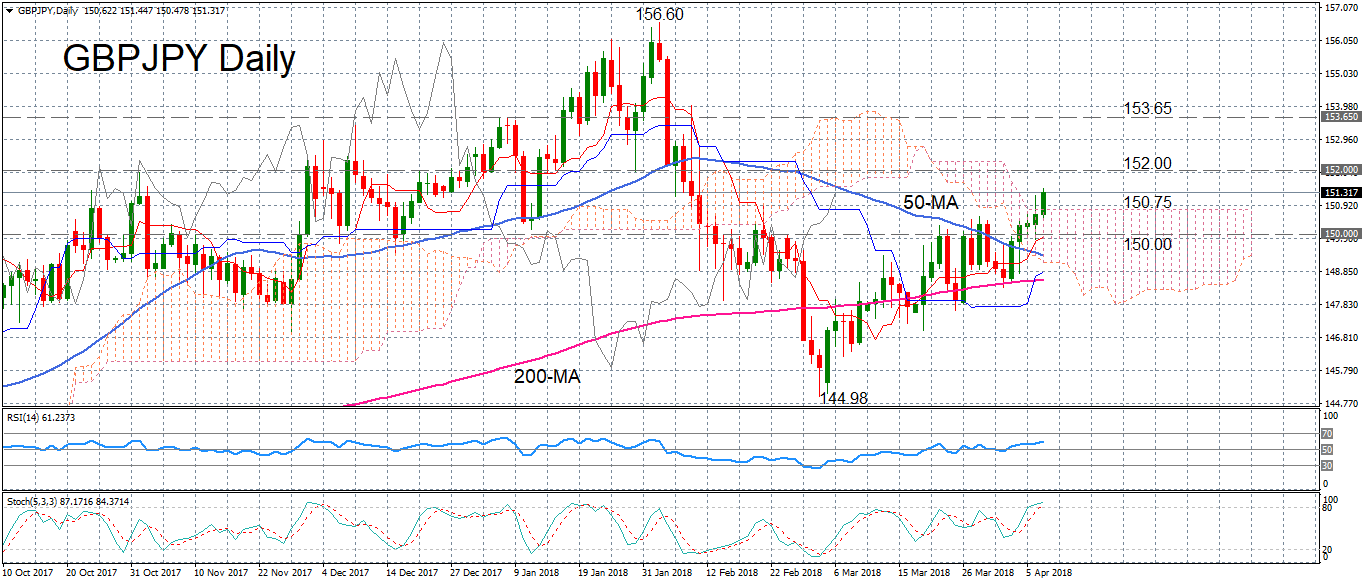

GBPJPY Attempting Cloud Breakout; Outlook More Bullish

GBPJPY is looking more bullish in the short to medium term as it extends its gains from March’s 5-month low of 144.98 to above the 151 handle. The pair has been trying to break above the Ichimoku cloud during the past two sessions but failed on Friday to close above it. Prices are back above the cloud today, rising to 2-month highs.

A successful daily close above the cloud top is possible given the bullish short-term indicators and would strengthen the current upside momentum. The RSI is trending upwards in positive territory but has yet to reach overbought levels, suggesting there is scope for additional gains in the near term. However, there is a risk of a downside correction according to the stochastic oscillator as the %K line is already in overbought territory and could be about to record a bearish cross with the %D line.

In case of a downwards reversal, immediate support is likely to come from the top of the cloud at 150.75. Not too far down, another support point to watch is the psychological 150 level, which also coincides with the Tenkan-sen line, and further below is the 50-day moving average (MA). A breach of the 50-day MA (currently around 149.35) would weaken the positive momentum and shift the focus back to the downside.

However, should the pair stick to its current uptrend, resistance could come at the 152 level, while further up, 153.65 could be the next major obstacle. A break above 153.65 could clear the way towards February’s 19-month top of 156.60.

ECB Draghi and Constancio struck cautious tones

ECB President Mario Draghi sounded cautious as usual in today's comments. Here are some highlights:

- "While we remain confident that inflation will converge towards our aim over the medium term, there are still uncertainties about the degree of slack in the economy,"

- "A patient, persistent and prudent monetary policy therefore remains necessary to ensure that inflation will return to our objective,"

Regarding recent stock market volatility, Draghi sounded calm though as he noted:

- "These risks materialized in global equity markets in early 2018, although to date without significant spillovers to euro area credit markets and hence broader financial conditions."

ECB Vice President Vitor Constancio also spoke today:

- "Inflation, which is our objective, has not yet responded completely to what we wish to see."

- "We have confidence that inflation will continue to evolve...(but) we should be cautious in order to avoid that some early, strongly restrictive policy could derail this development," he added.

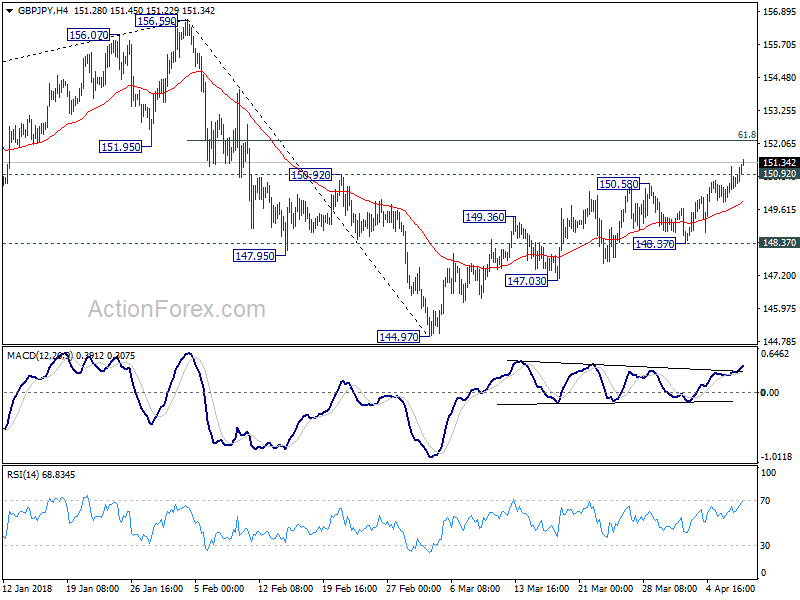

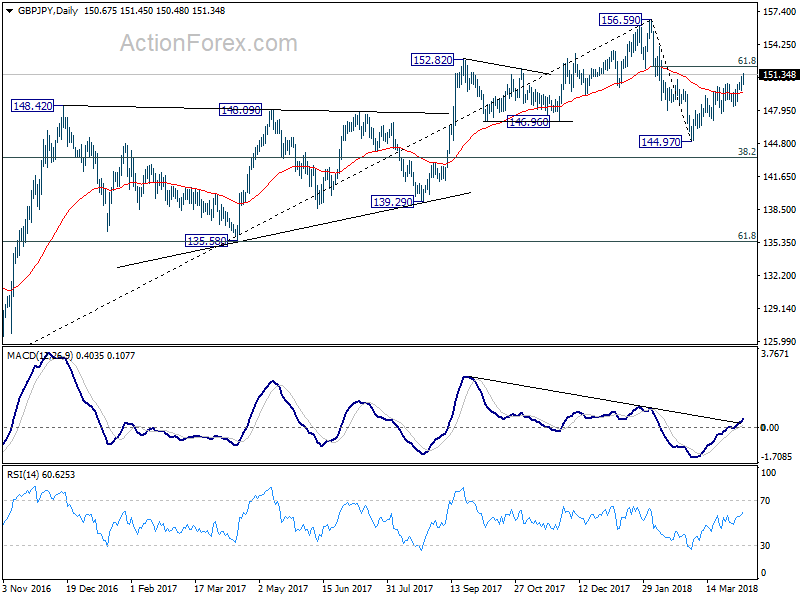

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.91; (P) 150.57; (R1) 151.25; More...

GBP/JPY's rise from 144.97 gathers further upside momentum as seen in 4 hour MACD. And it reaches as high as 151.45 so far. With 150.92 resistance taken out, intraday bias is on the upside for 61.8% retracement of 156.59 to 144.97 at 152.15 and above. For now, price actions from 144.97 are still seen as corrective looking. Hence, we'll look for sign of loss of upside momentum as it approaches 156.59 high. However, break of 148.37 is now needed to confirm completion of the rebound. Otherwise, near term outlook will remain cautiously bearish in case of retreat.

In the bigger picture, the outlook is turning mixed again. On the one hand, the cross was rejected by 55 month EMA (now at 154.20) after breaching it briefing. On the other hand, there was no sustainable selling pushing it through 38.2% retracement of 122.36 to 156.59 at 143.51. The most likely scenario is that GBP/JPY is turning into a sideway pattern between 143.51 and 156.59. And more range trading would now be seen before a breakout, possibly on the upside.

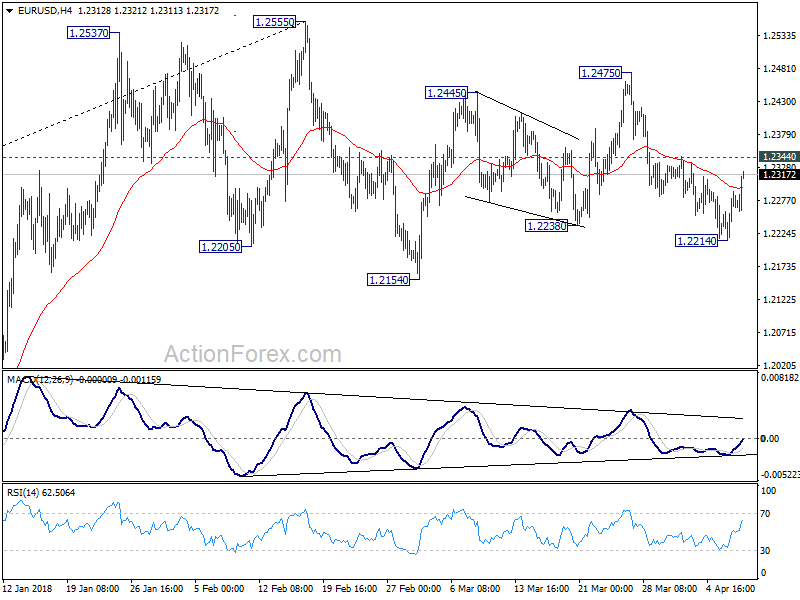

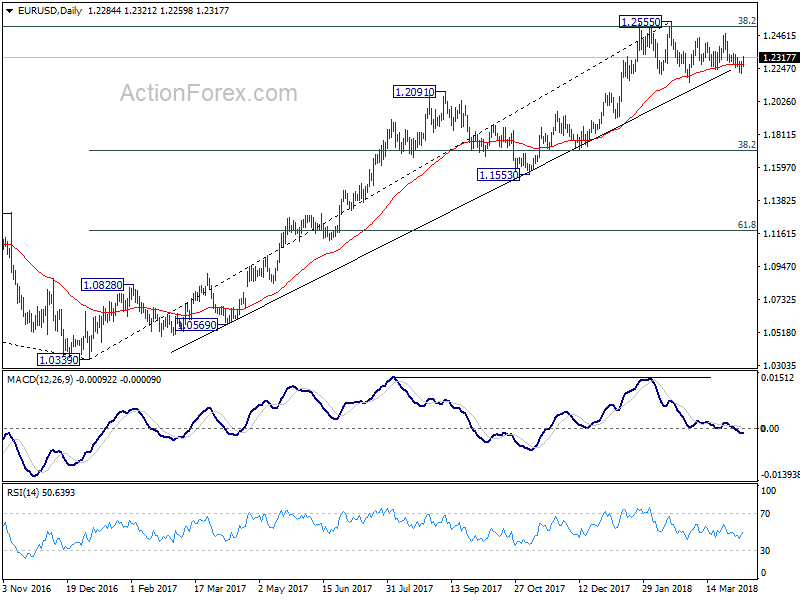

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2232; (P) 1.2261 (R1) 1.2308; More....

EUR/USD's rebound from 1.2214 extends to as high as 1.2321 so far today. The upside acceleration dampens the immediate bearish case. Focus is back on 1.2344 minor resistance. Break there will indicate that the decline from 1.2475 has completed and turn bias back to the upside for this resistance. Break will target a test on 1.2555 high. On the downside, below 1.2214 will target 1.2154 key support first. Firm break there should confirm rejection by 1.2516 key fibonacci resistance.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

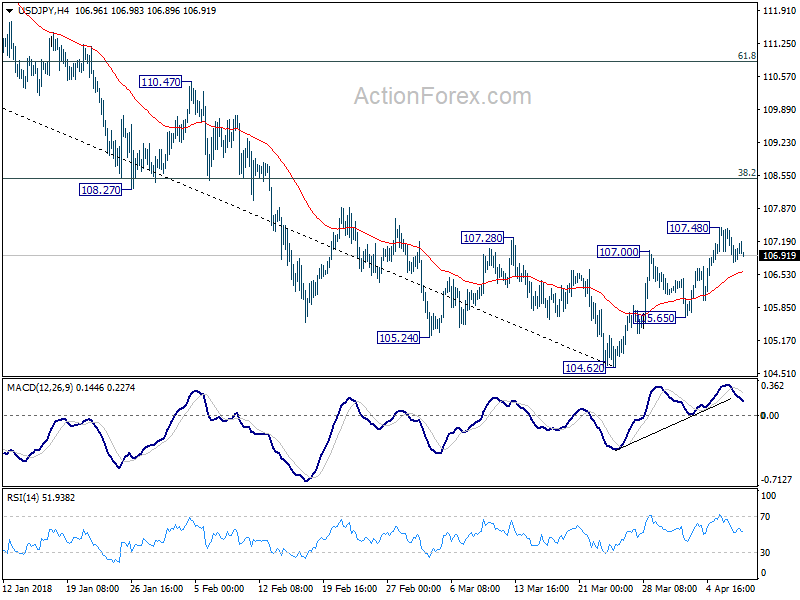

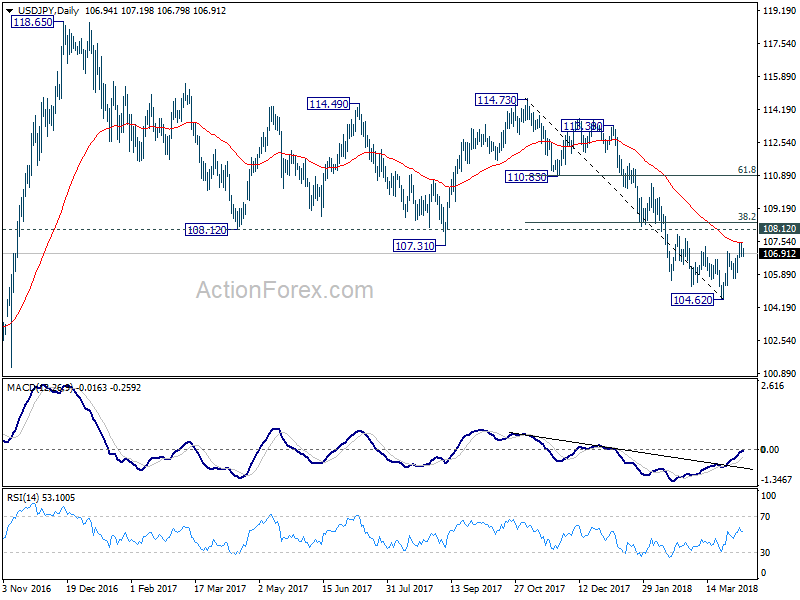

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.64; (P) 107.04; (R1) 107.32; More...

USD/JPY is staying in tight range below 107.48 temporary top and intraday bias remains neutral. On the upside, above 107.48 will resume the rebound from 104.62. But reaction from 38.2% retracement of 114.73 to 104.62 at 108.48 is crucial to determine the outlook. Firm break of 108.48 will add some credence to the case of trend reversal. And USD/JPY should target 61.8% retracement at 110.86 next. Nonetheless, rejection from 108.48 (which is close to 108.12 key resistance too), will retain bearishness. Break of 105.65 support will indicate that the rebound is completed and turn bias back to the downside for 104.62 and below.

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.