Sample Category Title

USD/JPY Edging Higher

USD/JPY bullish momentum continues, trading at 107.10 and approaching the 107.15 range. Hourly support and resistance are given at 104.30 (08/11/2016 low) and 107.90 (14/02/2018 high). The bearish pattern started in January 2018 is maintained. The short-term technical structure suggests further short-term increase.

We favor a long-term bearish bias. Support remains at 101.20 (09/11/2016 low). A gradual rise toward the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 101.20 (09/11/2016 low). The pair trades largely below its 200 DMA.

GBP/USD Strong Recovery

GBP/USD continues its recovery phase, approaching the March highs and heading along the 1.4118 range. Hourly support and resistance are given at 1.3905 (23/02/2018 low) and 1.4278 (02/02/2018 high). The technical structure suggests further short-term increase.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

EUR/USD Bearish Consolidation

EUR/USD is starting a consolidation phase, trading at 1.2280 and heading along the 1.2265 range. The pair is currently maintained between hourly support and resistance given at 1.2165 (17/01/2018 low) and 1.2506 (25/01/2018 high). The technical structure suggests sideways trading moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

The Greenback Consolidates After Disappointing NFPs

Swiss unemployment fell to 2.9%

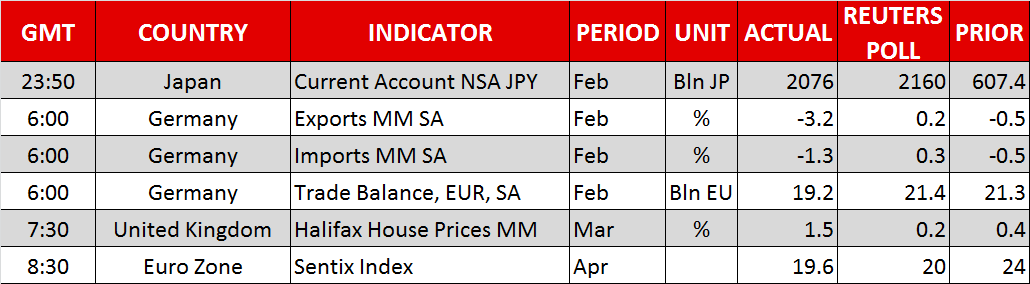

According to the latest report from the State Secretariat for Economic Affairs (SECO), the Swiss labour market continued to improve in March and this in spite of still overvalued Swiss franc. The unemployment rate beat median forecast of 3.0% as it printed at 2.9% (3.2% in February. When adjusted for seasonal factors the gauge stood at 2.9%, unchanged from the previous month and in-line with expectations.

In the FX market, the news went mostly unnoticed as market participants focus on the trade tariff argument between the US and China. After Friday’s sharp moves, the volatility was relatively low on Monday morning. Traders are still trying to interpret the last US job report. Indeed, Nonfarm payrolls came in well below estimates, printing at 103k versus 185k median forecast, while previous month reading was upwardly revised to 326k from 313k. The unemployment rate stood at 4.1%, while economists were looking for 4.0%.

Since mid-March, the US 2-year Treasury yield has been trading between 2.25% and 2.35%. However, over the same period, inflation expectations have decreased significantly, falling from 2% to 1.78%, as investors desperately wait for a significant increase in wage pressure. Despite the sustained positive developments in the job market, the lack of reaction on the wage side suggests that there is room for further improvement.

After testing 0.9649 last Friday, USD/CHF stabilised around 0.9595 this morning. Despite failing at breaking the key 0.9630-60 resistance area, the pair is still trading within its monthly uptrend channel. We believe that the greenback has just only gone back to take a better jump forward against the Swissie. On the upside, the following resistance lies at 0.9766 (Fibo 50% on December-February debasement). On the downside, a support can be found at 0.9420-35 (previous low and 50dma).

France imports and exports decelerate

Supported by lower inflation for the month of February (February consumer price index +0.20%), France February trade balance remains strongly in deficit, below its 5 years average of EUR -4.64 billion and slightly higher than previous month, given at EUR -5.19 billion (previous: EUR -5.42 billion). Over 12 months period, the deficit reaches EUR -60.2 billion (2017: EUR -62.5 billion), backed by a slowdown in imports for the month of February, estimated at EUR 44.90 billion (-1.40%). Exports are stabilizing, valued at EUR 39.7 billion (-0.90%), put under pressure by chemicals, electric materials and telephony exporting sectors while contributors such as aerospace and transportation remain. Accordingly, we remain positive as to the French economic recovery outlook, waiting for Tuesday’s February industrial production monthly data that are expected to deliver positive numbers.

French equity index CAC 40 shows signs of robustness, ending previous week in positive numbers (+1.76%) and providing higher performance than its European counterparts on a year to date basis, currently given at -1.02% (Euro Stoxx 50: -2.74%, DAX: -5.24%, Ibex 35: -3.08%, SMI -7.58%), confirming its favorable defensive bias in the context of higher volatility.

EUR/USD bearish pattern started in mid-February continues (-1.87%), the pair is currently trading at 1.2270, heading along the 1.2265 range in the short-term.

Dollar Steadier After NFP Miss But Trade And Syria Tensions Weigh On Sentiment

Here are the latest developments in global markets:

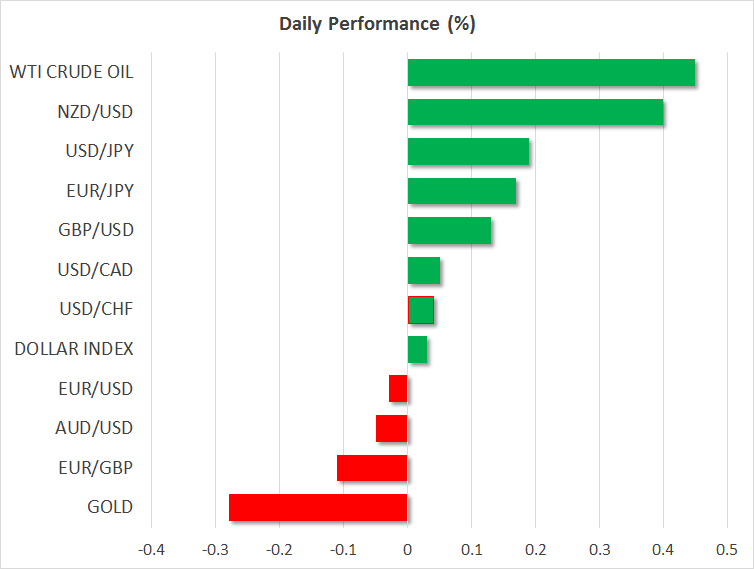

FOREX: The US dollar was attempting a rebound on Monday, climbing back above the 107 level against the Japanese yen after twice coming under pressure on Friday. A smaller-than-expected increase in March nonfarm payrolls out of the US followed heated exchanges between the US and China on trade, causing the dollar to undo its prior day's gains when it rose to 5-week highs. However, comments by US President Donald Trump over the weekend helped ease some of the fears about the prospect of a Sino-US trade war, with the dollar index edging up slightly to 90.16 at the start of European trading today. The euro and the pound benefited from the dollar weakness to recover from last week's multi-week lows. The single currency was last trading flat at $1.2277, but sterling extended Friday's gains to reclaim the $1.41 level to a 1½-week high. The Australian and New Zealand dollar were also firmer, rising by 0.2% and 0.6% to $0.7690 and $0.7301 respectively. The Canadian dollar was slightly down versus its US counterpart but stuck close to Friday's 5-week high of C$1.2729 per US dollar.

STOCKS: Asian stocks turned green on Monday and European bourses were also poised to open higher despite losses of more than 2% on Wall Street on Friday. Sentiment in equity markets tracked US stock futures higher, which were lifted by a slightly more conciliatory tone on trade with China by President Trump over the weekend. Hong Kong was the biggest gainer, with the Hang Seng index surging 1.5% as Chinese and other regional markets reopened after a long holiday weekend. Japan's Nikkei 225 index was also positive, rising by 0.5%. In Europe, future for London's FTSE, the German DAX and the French CAC were pointing to gains of around 0.5%.

COMMODITIES: Gold prices seemed unmoved by reports of an airstrike at a Syrian air base on Monday. Syria says the missile strikes were likely carried out by the US in response to a suspected chemical attack by Syrian forces on civilians on Saturday. But the Pentagon has denied any involvement. However, news that North Korea has reportedly told the United States that it is prepared to discuss denuclearization when leaders of the two nations meet next month offset the latest tensions in the Middle East. The precious metal was last trading marginally lower at $1331 an ounce. Oil prices shrugged off an increase in the US oil rig count last week to head higher on Monday. Both WTI and Brent crude were up 0.45% at $62.33 and $67.42 a barrel respectively.

Major movers: Dollar fights off selling pressure to hold near 107 yen

There was relative calm in forex markets on Monday as the week's trading got underway. While a disappointing US jobs report and an escalation of trade tensions between the US and China put a dent in risk sentiment on Friday, the dollar sell-off was limited and traders were more focused on the first quarter earnings season, which has just begun and will fully kick off next week. The dollar found support at 106.76 yen on Friday and is currently hovering around the 107-yen level.

Also weighing on the greenback last week was a speech by Fed Chair Jerome Powell. In his first big speech on the economy since becoming chair, Powell stuck to familiar language. He reiterated that 'further gradual increases' in interest rates are needed while remaining cautious about wage inflation, saying 'The absence of a sharper acceleration in wages suggests that the labor market is not excessively tight'.

Earlier, economic data showed the US economy added just 103k jobs in March, versus forecasts of 193k, though there was a small upward revision to the prior month's figure. There was relief however, that there were no surprises in wages, which grew by 2.7% year-on-year as expected.

Renewed dollar weakness on Friday helped other majors bounce back. The euro moved away from a 5-week low of $1.2212 but appears to have met resistance at $1.2290, with an unexpected drop in German exports in February not doing the single currency any favours on Monday. The pound recorded a stronger rebound, managing to rise back above $1.41 and the New Zealand dollar also recovered sharply to re-test the $0.73 level.

There was some boost to risk appetite following remarks by President Trump and his officials at the weekend where they sought to downplay talks of 'trade war' and were hopeful of a solution. President Trump tweeted 'China will take down its trade barriers because it is the right thing to do. Taxes will become reciprocal and a deal will be made on intellectual property.'

However, the Trump administration may need some tough persuading to do as a spokesman for China's Ministry of Commerce said late on Friday that 'It's impossible for both sides to engage in any negotiation'.

The US was having better luck in updating its trading relations with its neighbours though. Hopes are high that a deal on NAFTA can be reached with Canada and Mexico. The optimism drove the Canadian dollar to a 5-week high of C$1.2729 to the greenback on Friday but eased to C$1.2780 on reports that a preliminary deal is unlikely this month.

Day Ahead: ECB speeches eyed

With little in terms of data releases for the rest of the day apart from the Eurozone sentix index, focus will be on possible remarks by European Central Bank officials in planned speeches. ECB Vice President Vitor Constancio will present the Bank's annual report at the European Parliament at 13:00 CET, while Governing Council member Peter Praet will participate in the European Finance Forum in Germany at 16:45 GMT.

With the euro losing steam since the end of March, investors will be watching for policymakers' views on the Eurozone economy given recent indications of moderating growth at the start of 2018, and the implications of any slowdown on monetary policy. Hawkish comments could help the euro break above $1.23 but signs of concerns about growth could push the single currency below $1.22.

Trade relations between the US and China look set to remain at the forefront of traders' attention this week with nerves high for another potential escalation in the trade dispute. Investors will be hoping that President Xi of China will use his address at the Boao Forum for Asia on Tuesday to ease tensions by announcing more access for US firms in China's domestic market.

Should China go far enough in making concessions to the US, it could provide a major boost to risk assets and as well as the US dollar.

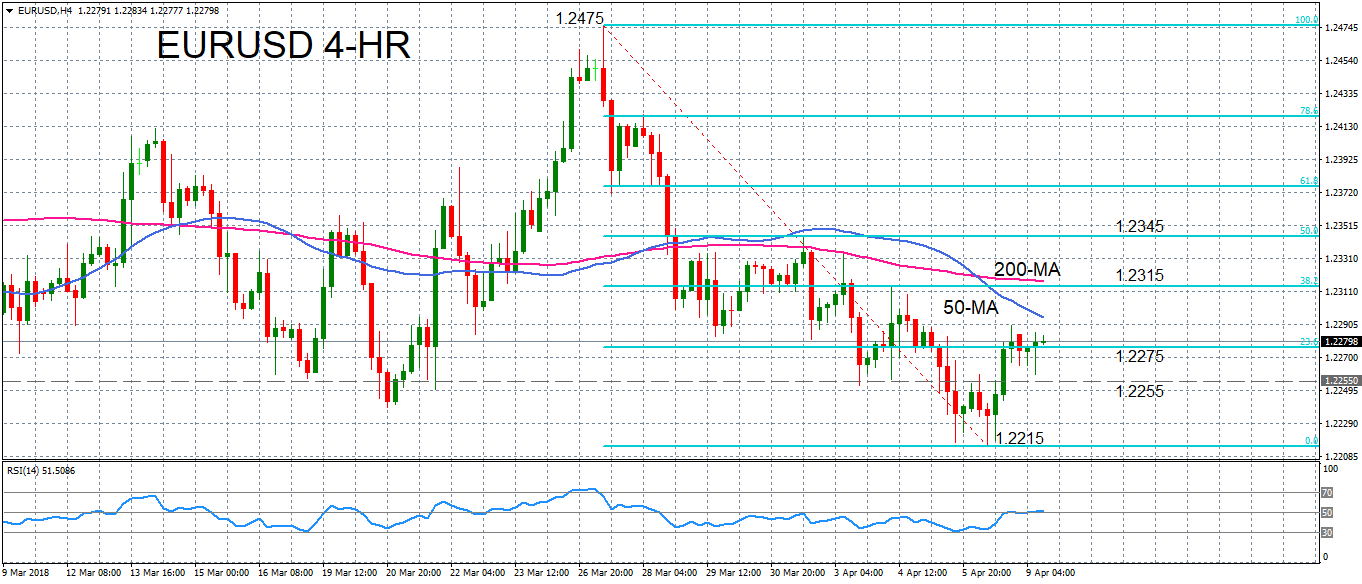

EURUSD Bearish In Short Term, Looking Neutral In Medium Term

EURUSD remains on a downtrend in the short term despite an upwards correction, which now appears to be fizzling out. The rebound from Friday’s 5-week low of 1.2215 has been halted at the 23.6% Fibonacci retracement of the downleg from 1.2475 to 1.2215. This level is around 1.2275.

Prices are struggling to overcome this resistance region as the RSI has turned neutral around 50 in the 4-hour chart, suggesting little immediate upside momentum. Should the pair overcome this hurdle, another resistance could be met at the 50-period moving average (MA), just under the 1.23 level. A break above the 1.23 mark would open the way towards the 38.2% Fibonacci retracement level of 1.2315. However, without a successful challenge of the 50% Fibonacci around 1.2345, EURUSD will find it difficult to break out of its current bearish phase, which was recently confirmed by the bearish crossover of the 50-MA with the 200-MA.

If price movement turns lower again, immediate support is likely to come from around 1.2255, a previous congestion area. A drop below this region would bring last week’s low of 1.2215 back into scope and open the way towards the near 2-month low of 1.2154 from March 1.

In the medium term, the picture is increasingly of a neutral one, as the pair has been trading sideways since late January.

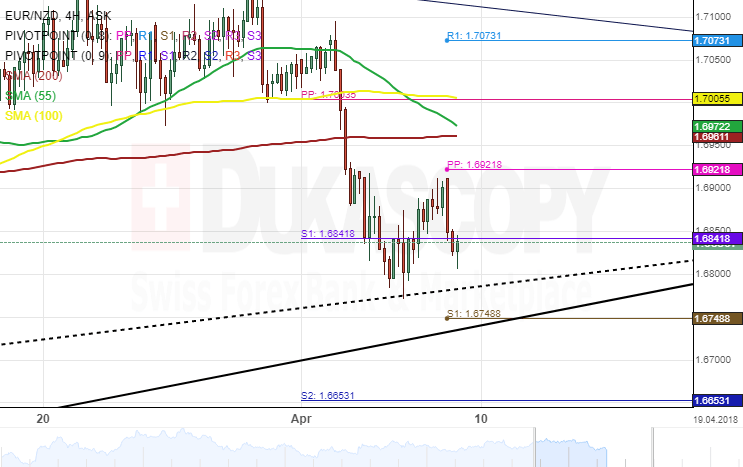

EUR/NZD 4H Chart: Breakout Is Expected

The single European currency has been trading in a four-month descending channel against the New Zealand Dollar. The currency pair tested the upper boundary of a junior pattern on December 1 followed with a new wave down.

The Euro has since been moving in a slight uptrend, however, a resistance cluster set by the weekly pivot point and the combination of the 55-, 100, and the 200– hour SMAs near the 1.7005 area continues to pressurized the price movement south.

Everything being equal, the EUR/NZD currency exchange rate is likely to decline further until it breaches the bottom border of a dominant channel during the following trading sessions.

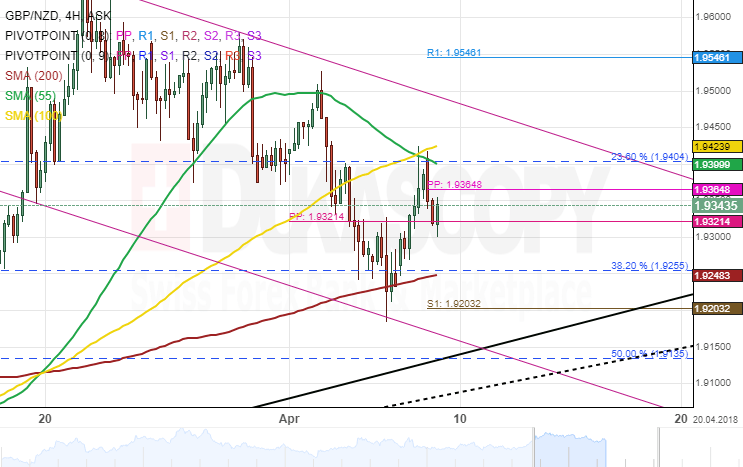

GBP/NZD 4H Chart: Reaches Resistance Cluster

The British Pound continues to strengthen against the New Zealand Dollar. However, a new downtrend channel has been spotted and it is believed to be a corrective movement south as it can be observed on the chart.

After piercing both the 38.20% Fibonacci retracement level and the 200– hour simple moving average, the GBP/NZD exchange rate began to appreciate, nonetheless, a resistance cluster set by the 55– and 100– hour SMAs has restricted the pair from making any further gains. This retracement can be measured by connecting the low at 128.96 and the high at 132.27.

Technical indicators suggest that a short period of consolidation is likely during the following trading session.

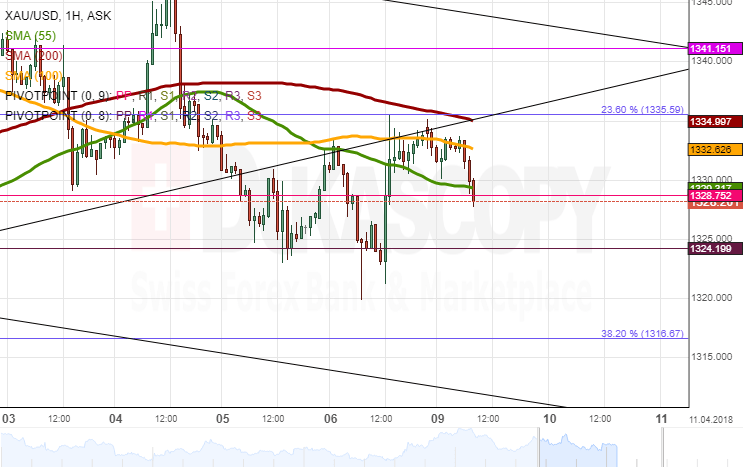

Gold Analysis: Pressured By Strong Resistance

Gold was trading along a breached trend-line against the US Dollar during Friday's session. Further advances were restricted by this line and the 100-hour SMA, while a fall below the 1,324.00 was stopped by the weekly PP.

On Monday, the northern barrier is likewise reinforced by the 200-hour SMA and the 23.60% Fibo. This factor is likely to either pressure the yellow metal lower or result in a minor period of consolidation today. In case the 55-hour SMA and the monthly PP at 1,328.00 is breached, a possible fall is restricted solely by the 38.20% Fibo retracement line at 1,316.67.

The prevailing patterns suggest that the pair is likely to push lower in both short– and medium-term. The bottom boundary of a two-week channel is located at 1,310.00.

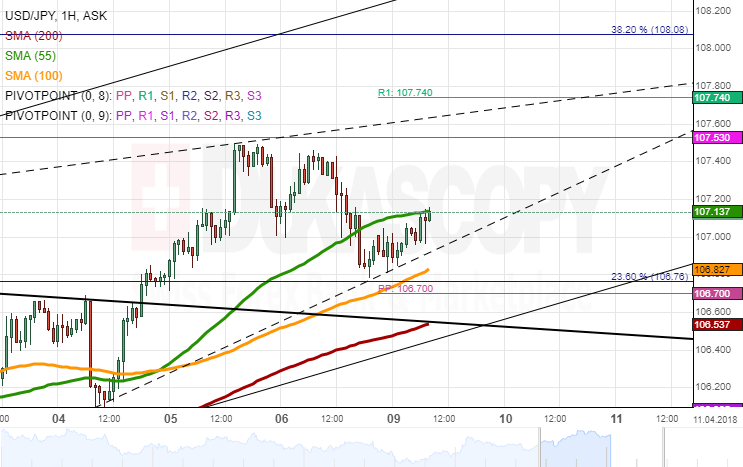

USD/JPY Analysis: Confined By Two Moving Averages

After trading at its March high of 107.50 early on Friday, downside risks took over the market and pushed the pair down to the support of the 100-hour SMA, the 23.60% Fibo retracement and the weekly PP.

The pair remained near this level on Monday morning as well, thus being stranded between the 55– and 100-hour SMAs during the Asian session. Technical indicators suggest that the rate is more likely to push higher in this session towards the upper boundary of a three-week channel. This line, however, is unlikely to be reached today. In case of a strong bullish sentiment, the US Dollar could test the weekly R1 and the 38.20% Fibo at 108.00.

Meanwhile, the downside target for today is the 200-hour SMA and a breached channel line at 106.00 which might be used to form a retracement.