Sample Category Title

US Markets Fall After Hours As Trump Proposes More Tariffs

Friday's session is expected to be volatile, with Non-Farm Payrolls (13:30 UK Time) ahead and President Trump's proposal for an additional $100B of trade tariffs for China affecting markets. The President instructed Treasury to consider the move, which would bring tariffs against China to $150B. This sent US stock markets lower and USDJPY from 107.430 to the 107.000 area before it rebounded higher to erase the loss. This is partially to do with positioning ahead of the NFP, which is expected to show an additional 190K jobs added after a stellar 313K last month. Average Hourly Earnings are expected to tick up to 0.3% from 0.1%. The move up to 0.3% caused a selloff in February on fears of inflation. With the US 500 Futures Index down -1.16%, disagreeable jobs data could deepen the selloff.

The response from China to the US tariff proposal has been swift, with Japan's chief cabinet secretary, Suga, saying it is important for China and the US to build a relationship that leads to stable growth and development of the global economy. The Chinese have responded saying that the US is recklessly wielding the stick of protectionism and they will only miss an opportunity to resolve the problem. China's resolve to protect global trading rules is strong and if the US insists on acting willfully, China will fight until the end. This was tempered by the comment that China's door for trade negotiation is still open. China's Commerce Ministry said that the trade war is caused by the US and that China does not want a trade war.

In a move that shows the potential damage this course of action could have on the domestic US economy, US Department of Agriculture Undersecretary Northey said that the department is “going to find ways to attempt to hold harmless the agriculture sector” from trade conflict with China. Soyabeans have been targeted in China's response and if the US has to subsidise its farmers, the negative impacts of the trade war will only grow.

Spanish Markit Services PMI (Mar) came out at 56.2 against an expected headline number of 56.0, from 57.3 prior. The consensus was for a further softening from the high created in July at 58.3 and the data was as expected. However, the data has shown a strong rebound in February and March, exceeding expectations on both occasions. The data is down from its 2015 high of 60.3. EURUSD moved higher from 1.22505 to 1.22705 after this data release.

Swiss Consumer Price Index (YoY) (Mar) was 0.8% v an expected 0.7%, against the previous 0.6%. This shows a continued move higher in inflation. GBPCHF fell from 1.35289 to 1.34939 led by this data.

German Markit Services PMI (Mar) came out at 53.9 against an expected headline number of 54.2, from 54.2 previously. After reaching a multi-year high of 57.3 in February, this data has come back into its range under 56.0. German Markit PMI Composite (Mar) was 55.1 v an expected 55.4, from a prior number of 55.4. The weather is being partly blamed for the drop in these numbers, alongside a particularly bad Flu season. EURUSD moved higher from 1.22532 to 1.22832 as a result.

Eurozone Markit Services PMI (Mar) came out with a headline number of 54.9 v a consensus of 55.0, against 55.0 previously. This figure was expected to slip back after hitting a high of 58.0 in February, but the fall was only marginal and still in line with expectations. Markit PMI Composite (Mar) was 55.2 v an expected 55.3, from a prior number of 55.3. EURGBP moved higher from 0.87191 to 0.87372 after this data release.

UK Markit Services PMI (Mar) was 51.7 v an expected 54.0, from 54.5 previously. This data is continuing to decline from its 2013 high of 62.5 and fell below the 53.0 level with this release, showing modest growth but putting the 50.0 level in focus. It is hoped that the data for April will show improvement as the weather picks up. GBPUSD moved up from 1.40300 to 1.40673 after this release.

US Trade Balance (Feb) was $-57.6B v an expected $-56.8B, against $-56.6B previously, which was revised down to $-57.7B. This shows a further decline to 2008 levels. Continuing Jobless Claims (Mar 23) were 1.808M v an expected 1.849M, against a previous 1.871M, which was revised up to 1.872M. Initial Jobless Claims (Mar 30) were 242K v an expected 225K, from 215K previously, which was revised up to 218K. These jobs figures indicate that Unemployment is at the lowest levels in years, with strong positive implications for the US economy. The move up in Initial Jobless Claims is being attributed to the Easter holidays and Spring breaks. GBPUSD moved higher from 1.40046 to 1.40292.

Canadian International Merchandise Trade (Mar) was $-2.69B v an expected $-2.00B, against a previous number of $-1.91B, which was revised down to $-1.94B. This fall was down to a record drop in Agricultural Exports. USDCAD fell from 1.28001 to 1.27826.

US FOMC Member Bostic spoke about financial literacy at the University of South Florida, in Sarasota. He said that he sees financial stimulus having a robust impact in the short run. He sees inflation hitting 2% in the next quarter or two and is comfortable going over 2% inflation by some amount. He sees the natural rate in the 2.25% to 2.75% range. Trade protectionism tends to be difficult for economic growth.

EURUSD is unchanged overnight, trading around 1.22377.

USDJPY is down -0.06% in early session trading at around 107.311.

GBPUSD is down -0.07% this morning, trading around 1.39924.

USDCAD is up 0.19% in early trade at around 1.27721.

Gold is up 0.15% in early morning trading at around $1,328.31.

WTI is down -1.13% this morning, trading around $63.03.

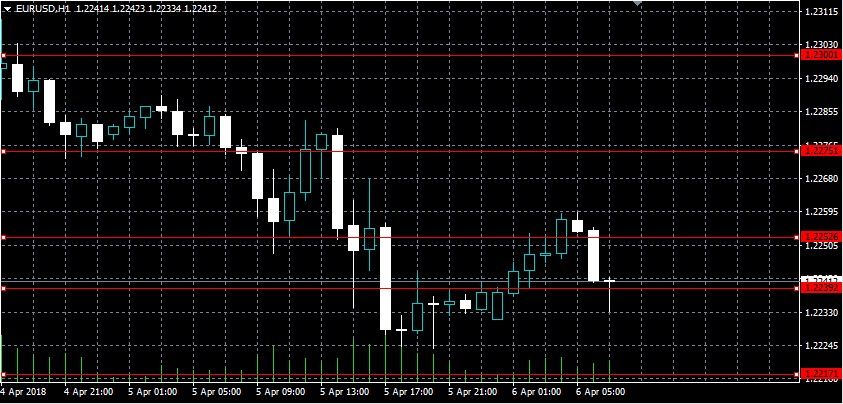

EURUSD Under Presure Below 1.2252 Level

The euro has moved to its lowest trading level against the greenback since March 1st, as fears over a slowdown in eurozone economic activity weigh on the single currency. The EURUSD pair currently trades around the 1.2239 level, after finding interim technical support from the 1.2217 level. Traders now look towards the release of German Industrial production data, with downside pressures likely to intensify while price-action trades below the 1.2252 level.

The EURUSD pair is under pressure while trading below the 1.2252 level, key support is found at the 1.2205 and 1.2160 level.

If the EURUSD pair moves above the 1.2252 level, buyers may look to test towards the 1.2275 and 1.2300 resistance levels.

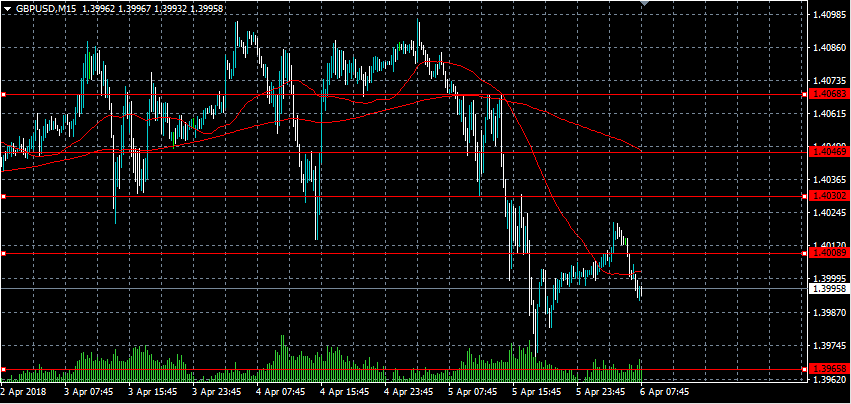

GBPUSD Bearish While Below 1.4008 Level

The British pound has moved sharply lower against the U.S dollar, hitting 1.3965, after the U.S dollar index climbed to a new five-week trading high. The GBPUSD pair also came under pressure, after the UK released much weaker than expected macroeconomic data for the second consecutive day. Downside pressure are likely to remain on sterling while price trades below the 1.4008 level, with the 1.3965 level remaining the gateway for further losses.

The GBPUSD pair remains bearish whilst trading below the 1.4008 level, key technical support is now found at the 1.3960 and 1.3890 levels.

If price-action on the GBPUSD pair moves back above the 1.4008 level, key intraday resistance is found at the 1.4030 and 1.4068 levels.

Optimism As A Wall Street Veteran Sees Porential Gains In Cryptocurrencies

In the past few weeks, the price of Ethereum has been on a free fall. The ETH/USD pair has reached a multi-monthly low of $360. The decline was caused by the continuation of bad news in the cryptocurrencies space.

However, there might be some of hope if Wall Street veteran, Tom Lee is to be believed. Yesterday, Tom Lee, the founder of Fundstrat released a report that showed that cryptocurrencies would rebound after 15th April. His thesis was that most Americans who own cryptocurrencies have been forced to sell the currencies as they filed their tax returns.

The report predicted that Americans had capital gains on cryptocurrencies worth more than $92 billion. As such, they will be forced to pay more than $25 billion in capital gains taxes. As you recall, cryptocurrencies were the best performing asset class of last year with most of them rising by more than 1000%.

Fundstrat is one of the leading Wall Street advisory firms with clients in the hedge fund and money management industry. Tom is also a favorite for major financial broadcasters like CNBC, Fox Business, and Bloomberg.

From a technical perspective, there is a likelihood that Ethereum has found a floor. This year, the ETH/USD pair reached the all-time high price of $1375, where it established a double top position. From the end of January, it started a sharp decline, ultimately reaching the current lows. However, if Lee’s sentiments are correct, there is a likelihood that the pair could see some gains. As shown below, the MACD, the RSI, and other oscillator indicators show that the pair is currently oversold.

Nonfarm Payrolls Take Centre Stage On Friday

Friday is US nonfarm payrolls day, which means currency traders, stock investors and other market participants will be glued to the economic calendar at 12:30 GMT. Luckily for them, the session will also feature other headline reports from around the world.

Action begins at 06:00 GMT with a report on German industrial production. The monthly reading is expected to show a 0.3% increase in February, compared with a 0.1% drop the month before. In annualized terms, this translates into growth of 4.3%.

About 45 minutes later, the French government will report on trade for the month of February. Paris’ trade deficit is forecast to narrow to €5.15 billion from €5.56 billion.

Other European data releases scheduled for Friday include Spanish industrial output and Swiss foreign currency reserves. Both releases will apply to the month of February.

Nonfarm payrolls will hit the news wire at the start of New York trading. The report is expected to show a gain of 190,000 jobs for the month of March, following a gain of 313,000 in February that was much higher than expected.

Average hourly earnings, an important proxy for wage inflation, likely grew 2.7% annually compared with 2.6% the month before.

The jobless rate is also forecast to improve to 4% from 4.1% as workforce participation also increases sharply to 63.5% from 63%.

Earlier in the week, the ADP Institute said private sector payrolls grew by 241,000 in March, compared with 246,000 the month before. The increase was much higher than expected.

North of the border, the Canadian government will also release its headline employment numbers on Friday. Canada’s economy is forecast to have added 20,000 jobs for the month, compared with 15,400 the previous month. The unemployment rate likely held steady at 5.8%.

EUR/USD

After being rangebound for much of the week, Europe’s common currency edged lower on Thursday as currency traders turned their attention to nonfarm payrolls. EUR/USD touched a low of 1.2231, putting it on track for its lowest level since early March. The pair was last seen trading at 1.2256, where it had gained 0.2% from the previous close. Overall, the euro is stuck in a sideways range going back many months, with upside limited to 1.25 and downside contained at 1.22.

USD/CAD

The USD/CAD extended its downward correction on Thursday, as the Canadian dollar remained buoyed by NAFTA optimism. The pair was last seen trading around 1.2755, its lowest level since February. Jobs data will likely determine the pair’s next move.

GBP/USD

Cable’s slide accelerated on Thursday, as the pair briefly traded below 1.4000. At the time of writing, GBP/USD was back above that crucial level to trade at 1.4015. According to a recent analysis by Westpac, the year-end target for the pair remains 1.4245.

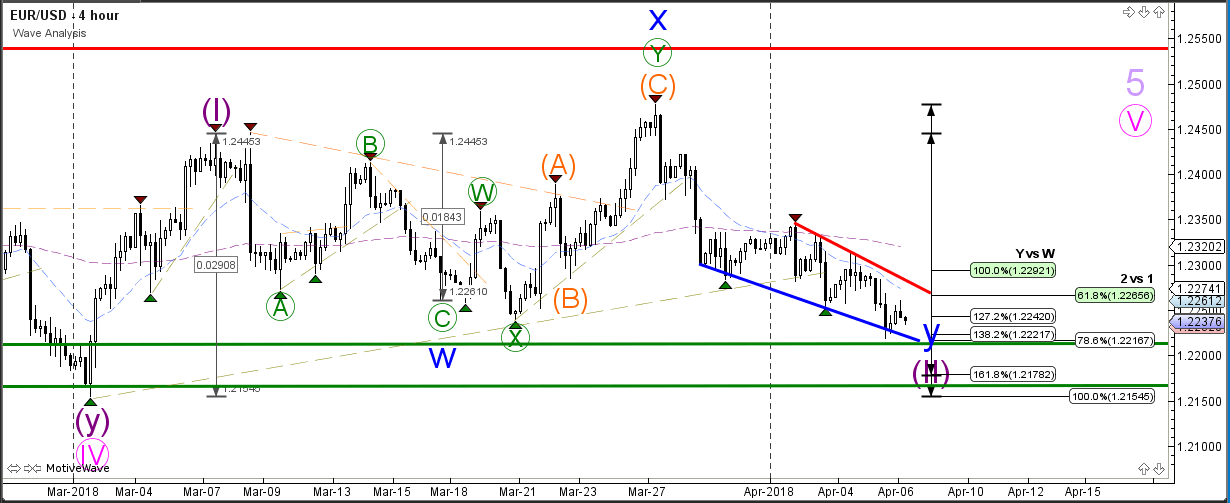

EUR/USD Market Structure After Completing 5 Bearish Waves

The EUR/USD bearish channel is choppy and corrective and is now approaching a key support zone between 1.2150 and 1.22.The bearish retracement could be completing a wave 2 (purple) or starting a new down trend. Price will need to break above the support (green) or resistance (red) levels before a new trend can be expected.

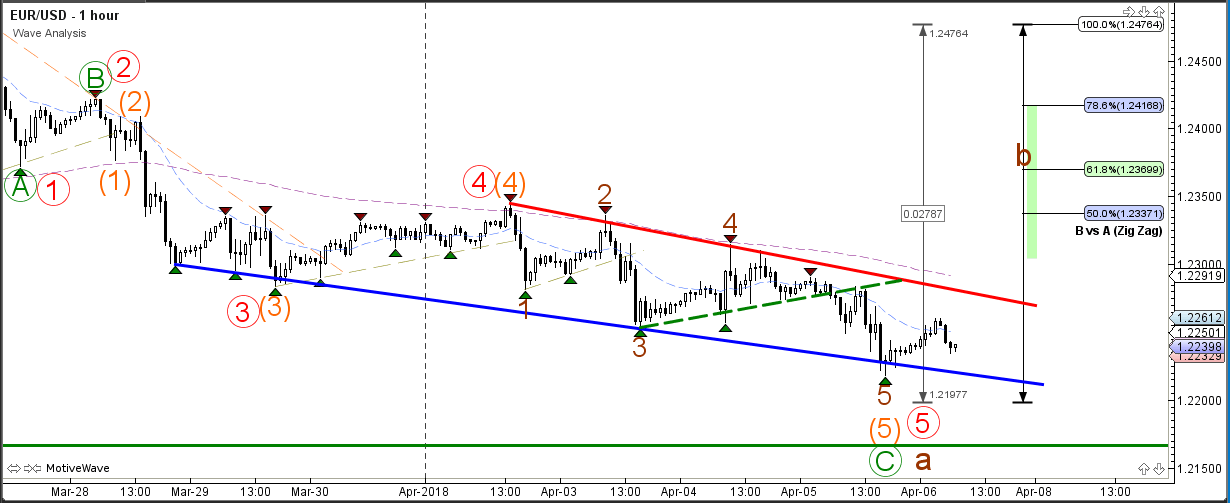

The EUR/USD is building 5 bearish waves which could either complete a wave c (green) within the wave 2 mentioned on the 4 hour chart. The bearish 5 waves could also be a wave A of a bigger ABC (brown) or start a new downtrend and become a bearish wave 1. For the moment however, price is at a strong support zone and a bullish bounce could become more likely here or at 1.2150. A break below the support zone would decrease the chance of a bullish bounce.

The US Note Future And Minor Losses For The Dollar

Markets

Yesterday, European stock markets joined the rally which started on WS on Wednesday after high rank US and Chinese officials indicated the start of a negotiating period after placing hawkish opening bets in the trade conflict. Main indices ended 2% to 3% higher. US stock markets extended gains, booking another +0.5% to +1%. Core bonds grinded gradually lower throughout the session on the improvement in risk sentiment. Both the US and German yield curves bear steepened. German yields increased by 1.1 bp (2-yr) to 3.1 bps (30-yr). US yields added 1.1 bp (2-yr) to 3.8 bps (30-yr). Traded volumes were lower than on the previous two days with some investors side-lined ahead of today's payrolls and a speech by Fed-governor Powell. The dollar gained momentum with EUR/USD (1.2240), USD/JPY (107.29) and the trade weighted dollar (90.45) all testing first support/resistance levels.

US President Trump surprised markets overnight just when trade dust seemed to have settled. He ordered his administration to consider tariffs on an additional $100 bn in Chinese imports, initially causing a new collapse in US stock market futures (-2%), an uptick in the US Note future and minor losses for the dollar. While Beijing condemned the move, it remains in favour of turning to the negotiation table. Proposing to slap the US by a similar amount of measures, the strategy used earlier this week, would more than cover all US exports to China.

We aren't convinced that the overnight move will trigger a new full-blown risk-off session. US equity futures partly recovered losses, main Asian indices trade mixed, the US Note future is topping off and the dollar reversed all minor losses. Focus turns to the US payrolls report and speeches by Fed chairman Powell and future NY Fed governor Williams who both speak on the economic outlook. Consensus expects net job growth of 185k in March. Employment indices in ISM's, the ADP employment report and weekly jobless claims continue to point to a very healthy US labour market, suggesting that the payrolls should at least be able to match this level. The unemployment rate is expected to decline from 4.1% to 4% which would be the lowest level since the end of 2000. Consensus forecasts wage growth of 0.3% M/M and 2.7% Y/Y increase. The latter was key in previous months to determine the market reaction. Matching the outcome should be sufficient to exert more upward pressure on the dollar and on US yields even if the reaction might be muted with the Powell speech in mind. We think that the key element will be whether or not the Fed chairman flags possible risks to growth stemming from the trade conflict. US stock markets might struggle in both cases (via the normalization narrative or via the weaker growth narrative). We see limited downside for the dollar and US rates though, given their recent resilience to the trade theme and as Powell certainly won't step away from this year's current consensus view of 2 more rate hikes this year.

News Headlines

US President Trump threatened a major escalation in trade tensions with Beijing, saying he was considering imposing tariffs on an additional $100 bn in imports from China. China left the door open for talks though, even as state media said the US is "recklessly wielding the stick of protectionism."

Atlanta Fed Bostic, voting FOMC member this year, sees a buoyant US economy lifting inflation to the central bank's 2% target "sometime in the next quarter or two", but said he doesn't think this should prompt the central bank to choke off the expansion (2% is not a ceiling!). Bostic is in favour of two additional rate hikes this year. He suggested that the Fed should pause its tightening cycle once it reaches neutral and then see how the economy evolves.

Japanese eco data were mixed. Labor cash earnings rose at the fastest pace since 2016 in February (1.3% Y/Y) and beat 0.5% Y/Y consensus. However, inflation-adjusted real wages fell for a third straight month (-0.5% Y/Y), undercutting household buying power. February household spending data disappointed, rising only 0.1% Y/Y.

German Industrial Production Is Due For Release This Morning

Market movers today

The US-China trade dispute continues to be on the radar.

Focus will revert to economic key figures, as the US employment report is due for release today. Wage growth will take centre stage. A drop in the hourly earnings growth in February to 2.6% y/y from 2.8% y/y eased inflation concerns, but they might flare up again if wage growth moves back up. Also keep an eye on the unemployment rate, which is expected by consensus to drop to an 18-year low of 4.0%. On the payroll number, consensus expects a rise of 185k following a strong 313k print in February.

German industrial production is due for release this morning. Yesterday German factory orders disappointed somewhat, rising only 0.3% m/m (consensus 1.5% m/m), which suggests there is some downside risk to the industrial production number as well. The softer orders generally confirm the picture of decelerating euro area growth.

Selected market news

The positive risk sentiment continued yesterday in global financial markets amid signs that we have reached a negotiation stage in the US-China conflict, which has helped ease fears over a trade war. Although we see signs that we have passed the peak in terms of tensions between US and China, we should expect ebbs and flows in the trade negotiations to drive continued market volatility. Overnight, risk sentiment in global financial markets turned around after Trump ordered his administration to consider tariffs on an additional USD100bn worth of Chinese imports (see Bloomberg ). For more on where we expect to go from here, see Research: Two scenarios for the US-China trade conflict , 4 April 2018.

This week's euro area data releases have been undershooting expectations with weak euro area core and headline inflation on Wednesday and German factory orders, euro area retail sales and final euro area PMI service yesterday. This confirms the overall picture of a deceleration in euro area growth. A drop in momentum could push the ECB to maintain a dovish tone (see also Bloomberg ).

In Norway house prices increased 0.2 % m/m in March (Danske: 0.3 % m/m, no consensus). Also, inventory-to-sales came down again. This implies a further stabilisation of the Norwegian housing market. Decreasing downside risks from the housing market support a Norges Bank rate hike over the summer (although not our base case).

US Employment Data, Powell Coming Up

General Trend:

- US President Trump threatens additional $100B in tariffs on China (Follows plans to already target $50B in Chinese goods)

- China Commerce Min (MOFCOM) implies further countermeasures

- Nasdaq Futures trade lower by over 1.5%

- Samsung Electronics declines after reporting record Q1 Op profit, sales below ests: Shares had gained over 3% ahead of the earnings

- US-based Japan stock funds continued to face outflows (weekly Lipper data)

- Market participation limited by continuing holiday in China

- Japan Feb Household Spending unexpectedly declines; Gov’t cites weather conditions, but adopts more cautious stance

- Japan Feb wages hit highest since 2016, but inflation-adjusted figure continues to decline

- Some analysts speculate BoJ may cut inflation forecasts

- Australia sells Dec 2021 bonds at over 7x bid to cover

- Traders to now look ahead to upcoming US employment data and comments from Fed Chair Powell

Headlines/Economic Data

Australia/New Zealand

- ASX 200 opened -0.1%; closed flat

- ASX 200 Financials index -0.2%; Energy +0.8%, REIT +0.5%

- (AU) Australia sells A$400M v A$400M indicated in Dec 2021 bonds, avg yield 2.2152% v 2.2960% prior, bid to cover 7.69x v 5.03x prior

- (AU) Morgan Stanley sees the end of 'super-cycle' for Australia banking industry - US financial press

China/Hong Kong

- Hang Seng opened +0.8%, Shanghai closed for holiday

- Hang Seng Energy index +1.3%, Telecom +1.1%, Info Tech +0.9%, Property/Construction +0.9%, Materials +0.7%, Financials +0.7%

- (CN) US PRESIDENT TRUMP ORDERS USTR TO CONSIDER $100B IN ADDITIONAL CHINA TARIFFS

- (US) President Trump: China's retaliation is 'unfair'

- (CN) China Commerce Ministry (MOFCOM) comments after Trump’s $100B tariff call: To take ‘new comprehensive’ measures to safeguard interests

- (CN) US $100B tariff proposal is violation of international trade rules, vows to defend its interests against US actions – Xinhua

- (HK) Hong Kong Mar PMI: 50.6 v 51.7 prior (5-month low)

Japan

- Nikkei 225 opened -0.1%; closed -0.4%

- TOPIX Real Estate index -0.9%, Electric Appliances -0.4%; Retail Trade +1.1%, Securities +0.4%

- Seven & I [3382.JP]: Shares gain over 3% after FY earnings and guidance

- Familymart [8028.JP]: Rises over 2% amid earnings speculation

- Monex [8698.JP] Rallies over 15% after agreeing to pay ¥3.6B for Japanese cryptocurrency exchange Coincheck

- Softbank announces C$99.1M investment in lithium company

- (JP) Japan Feb Household Spending Y/Y: -0.9% v +0.4%e (largest decline since April 2017)

- (JP) Japan Feb Labor Cash Earnings Y/Y: 1.3% v 0.5%e (highest reading since 2016); Real Cash Earnings Y/Y: -0.5% v -1.2%e (3rd straight decline)

- (JP) There is speculation among some analysts that the BoJ may have to cut its inflation forecasts at April 26-27 policy meeting – financial press

- (JP) Japan Mar Official Reserve Assets: $1.27T v $1.26T prior

- (JP) Japan Fin Min Aso: Share US thinking on intellectual property enforcement; to announce results of crypto probe at 3:30 PM local time (2:30 am EST)

- (JP) Japan METI: Sees April-June quarter crude steel production: 26.3M tons, +0.9% y/y and -0.9% q/q; April-June steel product demand (including exports) may rise 1.8% y/y to 23.3M tons

- (JP) Japan Foreign Min to create division focused on North Korea - Japanese Press

- (JP) Japan Ruling LDP Official Ishiba: Have to be prepared as no administration lasts forever; bad for LDP if leadership election is again uncontested

Korea

- Kospi opened -0.7%

- (KR) North Korea leader Kim Jong Un reportedly told China Premier Xi of intent to rejoin 6 party talks - Nikkei

Other

- (SG) Singapore Monetary Authority (MAS): To issue semiannual monetary policy statement and Q1 Advance GDP data on Friday, April 13th

- (MY) Malaysia PM Najib confirms to dissolve parliament and begin election process; dissolution is effective on Saturday (as rumored)

North America

- US stocks ended broadly higher: Dow +1%, S&P500 +0.7%, Nasdaq +0.5%, Russell 2000 +0.7%

- S&P500 Materials +1.9%, Energy +1.8%

- Wynn Resorts [WYNN]: MGM Resorts said to show interest in Wynn - NY Post

- (US) Fed's Bostic (FOMC voter, dove): dot plot does not lock Fed into policy path; not critical to signal whose dot belongs to whom; Should pause once neutral is reached; sees inflation hitting 2% in next quarter or two

- (US) Fitch affirms US AAA rating; outlook stable

Europe

- (EU) Reportedly EU and Japan to join US trade complaint against China regarding licensing rules – press

- Mothercare [MTC.UK]: Reportedly Sainsbury considered making a takeover approach for Mothercare - press

- Dufry [DUFN.CH]: Announces up to CHF400M buyback; proposes cash dividend of CHF3.75/share

Levels as of 02:00ET

- Hang Seng +0.7%; Kospi -0.6%

- Equity Futures: S&P500 -1%; Nasdaq100 -1.1%, Dax -0.6%; FTSE100 -0.7%

- EUR 1.2234-1.2260 ; JPY 106.99-107.46 ; AUD 0.7657-0.7695 ;NZD 0.7255-0.7278

- Jun Gold +0.1% at $1,331/oz; May Crude Oil -0.8% at $63.02/brl; May Copper -1.2% at $3.029 /lb

China pledges to figh US unilateralism and protectionism “to the end, and at any cost”

The Ministry of Commerce issued a quick response to Trump's intention to add tariffs to additional USD 100b of Chinese imports, while they're on holiday.

In a statement, China pledged to fight US unilateralism and protectionism "to the end, and at any cost". And China will "firmly attack, using new comprehensive countermeasures, to firmly defend the interest of the nation and its people."

The MOFCOM blamed that the the US "single-handedly started the trade conflicts". And it added that it's "provocation of unilateralism of the US to global free trade".

This is sort of the expected response from China.