Sample Category Title

As Trump Seeks Attentions With Trade Tensions Escalation, Markets are Looking Forward to Non-Farm Payrolls Instead

Trade war comes back to headline as US President Donald Trump announced his intention to triple down on the tariffs on Chinese imports. But so far, market reactions are muted. Major forex pairs are trapped in yesterday's range, just with some notable weakness in New Zealand Dollar. Swiss Franc is so far the strongest for the say with Yen trading mixed. But as the range is tight so far, the picture of who's stronger and who's weaker can change easily. In the stock markets, Nikkei is trading nearly flat at the time of writing, after fluctuating between gain and loss most of the day. Hong Kong HSI is up 1.26%. Gold is hovering slightly below 1330 as recent sideway trading continues.

Reactions to trade war news has been somewhat delayed recently. We'll have to, at least, wait for European open to gauge the response to Trump's proposal. But for the day, there are still other issues to focus on. Non-farm payroll will remain an important piece of data. And Canadian employment will be closely watched too.

Trump shows his intention to escalate trade tensions with China

In a statement release after US market close, Trump reveal his intention to escalate trade tension and actions against China. He ordered the Trade Representative to consider tariffs on additional USD 100b in Chinese imports, in addition to the USD 50b list of 1300 product lines. In his own statement, Trump condemned China's retaliation as "unfair" to "harm our farmers and manufacturers". He also ordered the Secretary of Agriculture to "implement a plan to protect our farmers and agricultural interests". USTR Robert Lighthizer supported Trump's proposal and said it's an "appropriate response" to China's recent threat of new tariffs. The statements of Trump and Lighthizer could be found here.

Here are some reports that's worth a read regarding US-China trade war:

- How Costly Would a Full-Blown Trade War Be?

- The Most Important Chapter in the Trade Saga is the Upcoming One

- China Announced Tariff on US Soybean Exports. What Next?

- Two Scenarios for the US-China Trade Conflict

Focus on wage growth again as 189k NFP growth is easily achievable

Markets are expecting NFP to show 189k growth in March, down from February's 313k. Unemployment rate is expected to drop further to 4.0%. Wage growth remains the key for Fed's tightening path. Average hourly earnings are expected to grow 0.3% mom in March. Here is a summary of preceding job data. ADP private sector jobs grew a solid 241k. ISM manufacturing employment dropped to 57.3, down fro 59.7. ISM non-manufacturing employment rose to 56.6, up from 55.0. Conference board consumer confidence dropped to 127.7, down from 130.0. The data were solid even though they don't point to that stellar 313k job growth in February. But 189k should be easy to achieve.

Here are some other NFP previews that's worth a look:

- NFP Preview: Wage Growth Remains Key Focal Point

- What To Expect From US NFP

- Dollar Looks To Jobs Data & Fed Chair Powell's Speech For Direction

Elsewhere

Japan overall household spending rose 0.1% yoy in February, below expectation of 0.3% yoy. Labor cash earnings rose 1.3% yoy in February, well above expectation of 0.50% yoy.

German industrial production, Eurozone retail PMI and Swiss foreign currency reserves will be released in European session.

Later in US session, non-farm payroll will be a major focus. Canadian employment data is equally important as markets expected 20k growth in March. Unemployment rate is expected to be unchanged at 5.8%. Canada will also release Ivey PMI.

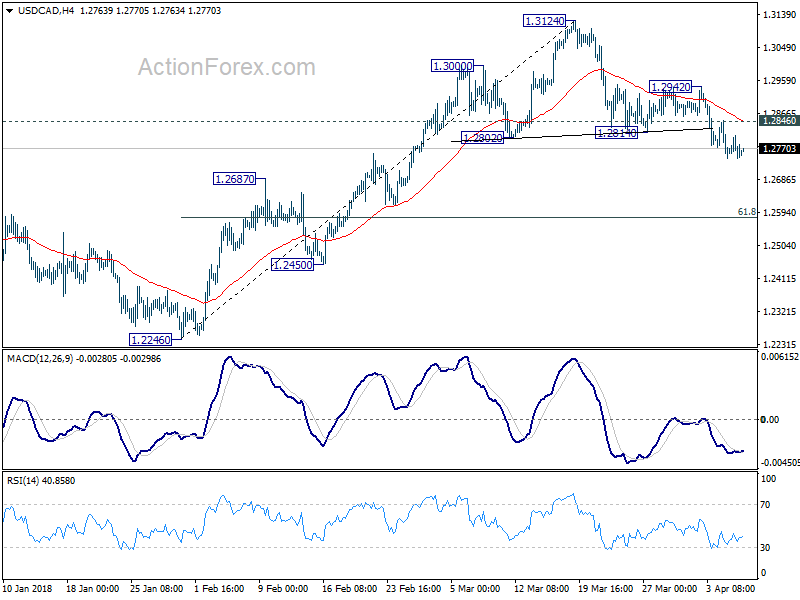

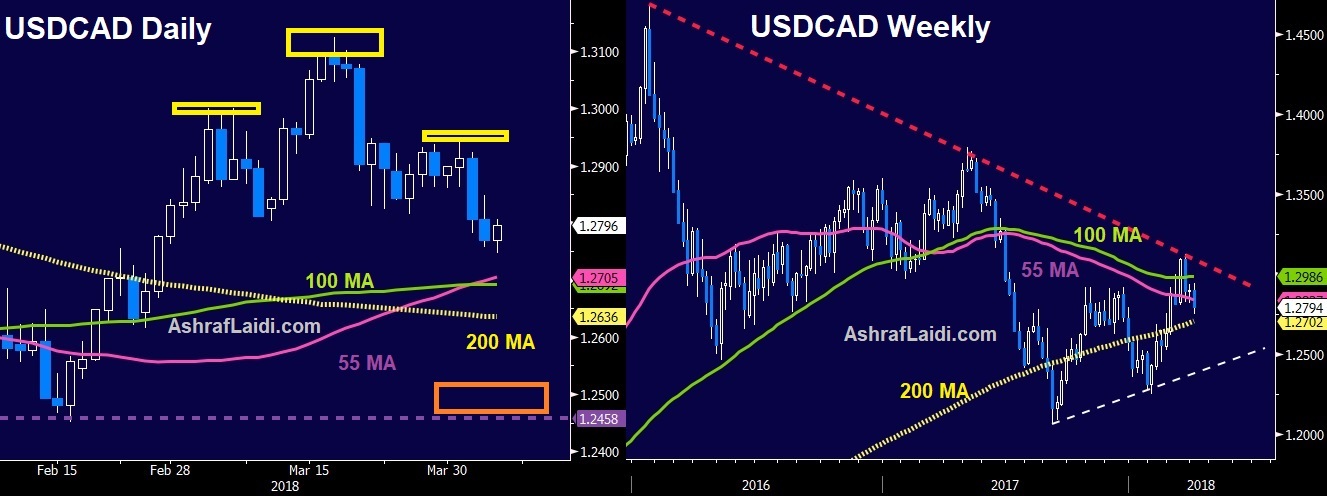

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2728; (P) 1.2767; (R1) 1.2790; More....

USD/CAD's downside momentum diminished a bit as seen in 4 hour MACD. But intraday bias stays on the downside for deeper fall. As noted before, near term trend should have reversed with head and shoulder top pattern (ls: 1.3000; h: 1.3124; rs: 1.2942). Decline from 1.3124 should target 61.8% retracement of 1.2246 to 1.3124 at 1.2581 next. Also, noted that current development suggest rejection by 1.3065 fibonacci level. And deeper decline could be seen back to 1.2246 and below eventually. On the upside, above 1.2846 minor resistance will turn bias neutral first. But break of 1.2942 is needed to confirm completion of the decline. Otherwise, outlook will stay cautiously bearish in case of recovery.

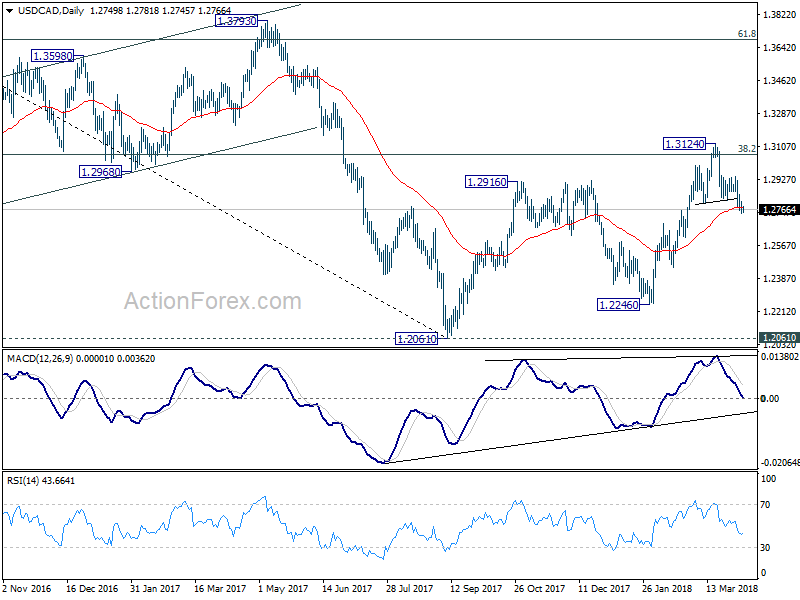

In the bigger picture, outlooks is turned a bit mixed again. Strong support was seen from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. But there was no follow through buying above 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Rejection by 1.3065 will argue that price action from 1.2061 is merely a three wave corrective pattern. And 1.2061 will be put back into focus with medium term bearishness revived.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Overall Household Spending Y/Y Feb | 0.10% | 0.30% | 2.00% | |

| 0:00 | JPY | Labor Cash Earnings Y/Y Feb | 1.30% | 0.50% | 0.70% | 1.20% |

| 5:00 | JPY | Leading Index Feb P | 105.5 | 105.6 | ||

| 6:00 | EUR | German Industrial Production M/M Feb | 0.20% | -0.10% | ||

| 7:00 | CHF | Foreign Currency Reserves (CHF) Mar | 734.5B | 732.8B | ||

| 8:10 | EUR | Eurozone Retail PMI Mar | 52.3 | |||

| 12:30 | USD | Change in Non-farm Payrolls Mar | 189K | 313K | ||

| 12:30 | USD | Unemployment Rate Mar | 4.00% | 4.10% | ||

| 12:30 | USD | Average Hourly Earnings M/M Mar | 0.30% | 0.10% | ||

| 12:30 | CAD | Net Change in Employment Mar | 20.0k | 15.4k | ||

| 12:30 | CAD | Unemployment Rate Mar | 5.80% | 5.80% | ||

| 14:00 | CAD | Ivey PMI Mar | 60.2 | 59.6 |

Elliott Wave Analysis: Further Strength In USDJPY

USDJPY short term Elliott Wave view suggests that the decline to 104.54 low on March 26 ended Intermediate wave (3). Wave (4) correction is in progress as a double three Elliott Wave Structure. A double three is a 7 swing corrective structure with WXY label. In the case of USDJPY, minor wave W of (4) ended at 107.01 and minor wave X of (4) ended at 105.62. As near term pullback stays above there, expect pair to extend higher within wave Y of (4).

Subdivision of Minor wave W of (4) in USDJPY unfolded as a zigzag Elliott Wave structure where Minute wave ((a)) ended at 105.9, Minute wave ((b)) ended at 105.29, and Minute wave ((c)) of W ended at 107.01. Subdivision of Minor wave X of (4) also unfolded as a zigzag Elliott Wave structure where Minute wave ((a)) ended at 106.09, Minute wave ((b)) ended at 106.45, and Minute wave ((c)) of X ended at 105.62.

Minor wave Y of (4) is currently in progress as a double three Elliott Wave structure where the rally from 105.62 ended at 107.49 in Minute wave ((w)). Expect pair to pullback within Minute wave ((x)) in 3, 7, or 11 swing to correct cycle from 4/3 low before the rally resumes.

USDJPY Elliott Wave 1 Hour Chart

NFP Expectation: 189k growth, unemployment to drop to 4.0%, wage growth at 0.3%

While the trade war drama continues, with intention of escalation from Trump, there are other issues that's worth a look. Non-farm payroll report is still a major focus of the day.

Markets are expecting NFP to show 189k growth in March, down from February's 313k. Unemployment rate is expected to drop further to 4.0%. Wage growth remains the key for Fed's tightening path. Average hourly earnings are expected to grow 0.3% mom in March.

Here is a summary of preceding job data:

- ADP private sector jobs grew a solid 241k

- ISM manufacturing employment dropped to 57.3, down fro 59.7

- ISM non-manufacturing employment rose to 56.6, up from 55.0

- Conference board consumer confidence dropped to 127.7, down from 130.0

The data were solid even though they don't point to that stellar 313k job growth in February. But 189k should be easy to achieve.

Here are some other NFP previews that's worth a look:

Market response to Trump: Nikkei flat, HSI up, FX in yesterday’s ranges

Market reactions to the news that Trump is trying to triple down on the tariffs on Chinese products are so far mild. Nikkei has been fluctuating between gain and loss and is trading nearly flat at the time of writing. While China is still away on holiday, Hong Kong is back with HSI trading up 1.26%.

In the current markets, major pairs and crosses are trading inside Friday's range as seen in the D heatmap.

But market reactions on the trade war issue has been somewhat delayed recently. We'll have to wait for European open, at least, to get a better idea on how serious are traders on Trump's proposal.

But market reactions on the trade war issue has been somewhat delayed recently. We'll have to wait for European open, at least, to get a better idea on how serious are traders on Trump's proposal.

Trump proposes to triple down tariffs against China to USD 150b

US President Donald Trump is now intending to triple down on his trade actions against China. He has just ordered the Trade Representative to consider tariffs on additional USD 100b in Chinese imports, in addition to the USD 50b list of 1300 product lines. In his own statement, Trump condemned China's retaliation as "unfair" to "harm our farmers and manufacturers". He also ordered the Secretary of Agriculture to "implement a plan to protect our farmers and agricultural interests". USTR Robert Lighthizer supported Trump's proposal and said it's an "appropriate response" to China's recent threat of new tariffs.

Below are the statements from Trump and Lighthizer:

Statement from President Donald J. Trump on Additional Proposed Section 301 Remedies

Following a thorough investigation under section 301 of the Trade Act of 1974, the United States Trade Representative (USTR) determined that China has repeatedly engaged in practices to unfairly obtain America's intellectual property. The practices detailed in the USTR's investigation have caused concern around the world. China's illicit trade practices − ignored for years by Washington − have destroyed thousands of American factories and millions of American jobs. On April 3, 2018, the USTR announced approximately $50 billion in proposed tariffs on imports from China as an initial means to obtain the elimination of policies and practices identified in the investigation.

Rather than remedy its misconduct, China has chosen to harm our farmers and manufacturers. In light of China's unfair retaliation, I have instructed the USTR to consider whether $100 billion of additional tariffs would be appropriate under section 301 and, if so, to identify the products upon which to impose such tariffs. I have also instructed the Secretary of Agriculture, with the support of other members of my Cabinet, to use his broad authority to implement a plan to protect our farmers and agricultural interests.

Notwithstanding these actions, the United States is still prepared to have discussions in further support of our commitment to achieving free, fair, and reciprocal trade and to protect the technology and intellectual property of American companies and American people. Trade barriers must be taken down to enhance economic growth in America and around the world. I am committed to enabling American companies and workers to compete on a level playing field around the world, and I will never allow unfair trade practices to undermine American interests.

USTR Robert Lighthizer Statement on the President's Additional Section 301 Action

"President Trump is proposing an appropriate response to China's recent threat of new tariffs. After a detailed investigation, USTR found overwhelming evidence that China's unreasonable actions are harming the U.S. economy. In the light of such evidence, the appropriate response from China should be to change its behavior, as China's government has pledged to do many times. Economies around the world – including China's own – would benefit if China would implement policies that truly reward hard work and innovation, rather than continuing its policies that distort the vital high-tech sector.

"Unfortunately, China has chosen to respond thus far with threats to impose unjustified tariffs on billions of dollars in U.S. exports, including our agricultural products. Such measures would undoubtedly cause further harm to American workers, farmers, and businesses. Under these circumstances, the President is right to ask for additional appropriate action to obtain the elimination of the unfair acts, policies, and practices identified in USTR's report."

Any additional tariffs proposed will be subject to a similar public comment process as the proposed tariffs announced on April 3, 2018. No tariffs will go into effect until the respective process is complete.

Market Morning Briefing: Euro Yen Is Respecting Resistance In The Downward Channel

STOCKS

Dow (24505.22, +0.99%) has seen a sharp bounce from levels near 23500, keeping our earlier mentioned 23500-24500 region intact. Trade region is narrowing for the coming sessions by the trendlines as indicated on the daily candles. A break on either side of the range is likely over the coming week.

After a sharp bounce from 11800 on Wednesday, Dax (12305.19, +2.90%) traded near 12200 yesterday. The daily resistance near 12300 is holding for now and while that holds, Dax is also likely to trade in the broad 12300-11700 region for the coming sessions. A fall back towards 11800-11700 is possible while below 12300. On the alternative, a sustained break above 12300 is needed to initiate a fresh rise for the medium term.

Nikkei (21679.13, +0.16%) has tried to bounce from levels near 20600 and is trading higher but it seems there is lack of upside momentum just now. If the Dollar Yen manages to break above 107.00-107.50 in the coming sessions, it could pull up Nikkei too to levels near 22200 or higher.

Nifty (10325.15, +1.94%) rose sharply to levels above 10260. There could be some upmove while the rise sustains, taking the index towards 10400-10500 in the near term. Also note interim resistance near 10370 which if holds could produce a small dip before the index rises to 10400 and higher. Sensex (33596.80, +1.75%) could attempt a rise towards 34000.

COMMODITIES

Brent (68.00) and Nymex WTI (63.18) have both come off slightly as expected. A fall towards 67-66 and 62-61 respectively looks likely in the coming sessions before the crude prices move higher afresh.

Gold (1334.90) is likely to trade sideways within the broad 1310-1360 region for the coming sessions. A break on either side is needed to get an indication of further directional course for the longer run.

Copper (3.0375) could trade in the 2.95-3.10 region for the next couple of weeks. Support near 2.95 is likely to hold in the longer run but some sideways consolidation in the 2.95-3.10 region is expected before the price rises towards 3.15-3.20 again in the longer run.

FOREX

As per our expectation, Dollar index (90.34, high of 90.59 yesterday), after having breached resistance in the downward channel (daily candles) earlier this week, has moved further up possibly targeting higher resistance (90.75-91.00 - seen on daily line chart, weekly line chart and 3 day candles). 90.75-91.00 is seen as a strong resistance level. If breached, it could lead to medium term bullishness for the Dollar.

As we had been expecting, Euro (1.2256) did test lower support on daily candles (near 1.2225) by dropping to a low of 1.2218 yesterday and is currently trading slightly above support. The 21 weeks moving average line is at 1.2150 currently and if it breaks, it could be termed as a decisive bearish turn for the Euro in the medium term. However, while above 1.2150, Euro could again move back up towards 1.25 – thereby continuing its broad ranging between 1.255-1.215 since Jan end.

Dollar Yen (107.20) has decisively breached resistance near 106.9 in the downward channel on daily, 3 day and weekly candles. Could this be an indicator of medium term bullishness? If Dollar Yen moves beyond its previous high of 107.90 (seen in Feb end), a medium term bullish view could take preference.

Euro Yen (131.37) is respecting resistance in the downward channel on 3 day and weekly candles near 131.4-131.5 and might come down from here towards 130. However, there is possibility for the Euro to rise from current support and Dollar Yen to rise towards 107.90 – if that happens, then the downward channel for Euro Yen would be breached. If we reverse the hypothesis, could resistance on Euro Yen imply that both Euro and Dollar Yen will dip further? We should get to know this in the next week.

Pound (1.4015) has broken interim support trendline on daily candles and as per our expectation has moved lower, possibly targeting important support level near 1.395 on daily and 3 day candles.

Dollar Rupee (64.96) – Dollar-Rupee could lean towards the downside, especially if it closes below 64.90 today.

INTEREST RATES

US long term yields had bounced yesterday from supports on short term charts towards channel resistances and might see a dip from there next week again. The US CPI data release next week (11th April) could be important for yields. We have been saying that US yields could continue moving in a downward channel through Apr-May.

US 10 Yr Yield (2.82%), 30 Yr (3.06%), 5 Yr (2.62%), 2 Yr (2.29%) :

The 10 Year yield had risen from support near 2.75% on the short term chart to 2.80% yesterday and is currently near 2.82%. It could move up further towards 2.85%-2.86%, which could be a resistance level in the downward channel.

The 30 yr yield instead of dipping from resistance near 3.05% has moved up further towards 3.06%. It could see a dip soon, back into the channel, or else it could move up towards 3.10%-3.12% and dip from there.

USD/JPY Poised For Further Gains, NFP Next

Key Highlights

- The US Dollar made a nice upside move and traded above the 106.50 resistance against the Japanese Yen.

- There was a break above a crucial bearish trend line with resistance at 106.70 on the 4-hours chart of USD/JPY.

- The US Initial Jobless Claims for the week ending March 31, 2018 increased from 218K (revised) to 242K.

- Today, the US Nonfarm Payrolls report for March 2018 will be released, which is forecasted to post 190K versus 313K previous.

USDJPY Technical Analysis

The US Dollar formed a support base near 105.50 against the Japanese Yen and started an upside move. The USD/JPY pair traded higher and broke a major resistance near 106.50.

During the upside move, the pair was successful in settling above the 100 (red) and 200 (green) simple moving averages (4-hour). It opened the doors for more gains and there was a break above a crucial bearish trend line with resistance at 106.70 on the 4-hours chart.

The pair also moved above the last swing high at 107.01, which means it could test the 1.236 Fib extension of the last decline from the 107.01 high to 105.65 low.

If buyers remain in action, the pair may perhaps move towards the 107.80 level. Moreover, the 1.618 Fib extension of the last decline from the 107.01 high to 105.65 low can also be tested near 107.85.

On the downside, the 106.50 support, and the 100 and 200 SMA’s are likely to act as strong barriers for declines in the near term.

Recently in the US, the Initial Jobless Claims for the week ending March 31, 2018 was released by the US Department of Labor. The market was positioned for rise from the last reading of 215K to 225K.

However, the result a bit disappointing as there was an increase in claims to 242K. Moreover, the last reading was revised up to 218K. The report added that:

The previous week’s level was revised up by 3,000 from 215,000 to 218,000. The 4-week moving average was 228,250, an increase of 3,000 from the previous week’s revised average. The previous week’s average was revised up by 750 from 224,500 to 225,250.

There was no major impact on the US Dollar. However, today’s nonfarm payrolls release could make a huge impact on pairs like EUR/USD, GBP/USD and USD/JPY in the near term.

Economic Releases to Watch Today

- US nonfarm payrolls March 2018 – Forecast 190K, versus 313K previous.

- US Unemployment Rate March 2018 – Forecast 4.0%, versus 4.1% previous.

- Canada’s employment Change payrolls March 2018 – Forecast 20K, versus 15.4K previous.

- Canada’s Unemployment Rate March 2018 – Forecast 5.8%, versus 5.8% previous.

NAFTA Theatre & USD/CAD

This article looks at international trade deficits, NAFTA and the Canadian dollar

There is far too much scepticism about a NAFTA deal. We understand it, because Trump has caught market players wrong-footed on several occasions in the past year.

There is no doubt that Trump’s action on the international trade are driven by political motives than economics. He’s wrong about how trade deficits work and he’s wrong about all kinds of numbers. The deficit with China isn’t $500 billion (it was $337 bn last year), and that with Canada is much closer to zero than the $17 billion he often mentions. But that’s all beside the point. Even if Trump’s numbers were accurate, the deficit with Canada remains a drop in the bucket and a trade war with Canada doesn’t play to his base.

A battle with Mexico might play better but NAFTA is a three-way agreement so it’s all or nothing. If there were two separate deals, Mexico would be in trouble. Mexico should be sending Canada flowers…free of any tariffs. As it is, NAFTA trade isn’t the US’s big problem, nor is the solution. Trump knows it, despite the rhetoric.

Mexico Caravan Theatre

Have you ever heard of an illegal immigrant caravan going through Mexico before? If you’re like us, the first time you ever heard of it was this week, sometime after Trump tweeted about it. Evidently this is an annual tradition that normally involves about 300 people. This year, the tally reached 1000 so it’s somewhat notable. But keep in mind that there are 11 million illegal immigrants in the US and about 42,000 enter per month, and another 20,000 attempt entry but are detained.

So all the fuss is about the 1000 is nothing but theatre. More aptly, a sham for Trump to flex his military muscles and a set-up for a NAFTA deal.

Mexico will most likely break up the caravan, especially that most riders come from Honduras, hence, there’s no big electoral pay for Mexican politicians at home.

At the same time, Mexican officials will release a few token statements about stopping illegals through Mexico, while Trump can declare victory, thus combining it with a NAFTA announcement next week.

What’s next for USD/CAD?

Things are already lining up for a bounce in the Canadian dollar (further declines in USD/CAD). A NAFTA deal appears to me as 80% done, while markets are estimating it around 50/50. Technically, there is a textbook head-and-shoulders top in USD/CAD, arguing for 1.25 as the next landmark target. The x-factors are the stock market and China. We can expect a short reprieve after the White House said it has nothing more planned at the moment, while Trump’s economic team shifted mode to damage control on Wednesday. Finally, let’s not forget that April has been the strongest month for the Canadian dollar over the last 20 years.

The Heat Is On ( Again)

The Heat is on ( Again)

Just when you thought it was safe to go back in the water, President Trump orders USTR to consider $100 in additional tariffs confirming the view that trade war rhetoric is unlikely to leave the picture anytime soon.

Equity markets held a decent bid overnight with risk sentiment bouncing higher on the back of the recent trade rhetoric suggesting both camps are incredibly motivated to contain trade tension for fear of a global market meltdown. But this morning’s headlines will question that view. But at a minimum, investors should start wondering why the US administrations soothsayers are sending out contradictory signals. I fear there are some awful actors in play on this political stage.

With the seismic shifts in sentiment this week the last thing this market needs is more confusion !! The latest in a line of bombastic Trump headlines now suggests it will take more than a kind week to sort this trade war issue out.

However, the hyper-volatility we’ve been warning about all year could be just around the corner.

We’re out of the fire and into the frying pan for stock markets as investors have forgotten about the Fed who could be the markets biggest universal foe. So besides an unlikely full-blown trade war, the real risk facing capital markets is a more aggressive Fed, and tonight’s average hourly wages data could provide that inflation fodder for reigniting the four rate hikes debate. But let’s not forget that delicate issue when QE gets pulled back, there’s no accurate roadmap to navigate that bumpy road.

.

Risk aversion plays aside, with a nudge from tonight’s payrolls data it could put the finishing touches on a remarkable week for the dollar. Of course, position squaring into NFP could be the culprit for the dollars continued revival, but economic data has topped out elsewhere including China and the Eurozone. So with the US economy expected to shine brightly in Q2 and 3, perhaps some long-held negative dollar views could fall under pressure during the next few weeks.

I’ve been fielding a lot client questions this week on how they should trade extreme sell-off followed by an equally stupendous rally. ” Carefully ” my seat is feeling every bump and bounce as trade concerns still bubble under the surface all the while President Trump’s instability alone keeps me awake at night!!

Oil Markets

Bullish signals abound to end the week, until the latest headline that is! The most recent rumblings from President Trump have seen oil prices fall convincingly, but given the supporting narrative, it should attract some dip buyers

Ths week’s US inventory data points to strong demand on the back of buoyant US exports.US oil inventories remain a volatile gauge, but they still provide a good litmus test for the short-term application.

The real surprise was Saudi Arabia lifting OIl prices for Asian buyers overnight which certainly put a significant bid in the futures markets.

Gold Markets

A few negative kickers for gold prices as US-China trade ware tension ease US 10 Year yields perked up above 2.83 strengthening the dollar and denting Gold appeal. But haven demand has only reduced and not reversed as the markets are never out of the woods with so many potential risk disruptors still in play. However, there are the usual precautionary position adjustments in the game ahead of the NFP as a substantial employment number, and wage growth would see the market quickly price in a more aggressive Fed policy ( 4 rate hikes ) and push gold prices lower.

Currency markets

The Japanese Yen

As the trade fracas diminishes, equities continue their recovery and USDJPY moves higher on risk appeal. So the opposite holds true for this morning Trump headline. But USD bears still have the NFP to navigate which could slow the re-emerging risk off USDJPY downtrend. The dollar has shown some real moxy this week, and a stronger AHE print could leave more than a few tounges wagging later tonight

The Euro

Nearing the soggy bottom 1.2220 level after the market has spent weeks building up long EURUSD inventory could be a real test of conviction.

The Malaysian Ringgit

The MYR remains quiet ahead of a pending election announcement and US NFP. Trade war rhetoric is framing regional risk sentiment, and local traders, as is so often the case heading into NFP, are increasingly nervous about a more aggressive shift from the Feds

Foreign inflows are expected to fall to a trickle as the election nears where investors will probably only trade the edges of the current MYR ranges.

With headlines risk abounding safest place appears on the sidelines today as we head into tonights NFP

Trade War Fears Make Way For US Employment Report

The US dollar surged against major pairs on Thursday. Trade war anxiety has subsided with the market awaiting the data form the U.S. non farm payrolls (NFP) to be released by the Bureau of Labor Statistics on Friday, April 6 at 8:30 am EDT. The greenback is on the rise despite a larger than expected weekly unemployment claims number due in part to the strong gain in private payrolls reported earlier in the week. The data point to watch on Friday will be the hourly wage component as it is used as an inflation indicator by the Fed. The market has priced in two to three rate hikes this year, but higher inflation could validate Fed members comments of four rate hikes in 2018.

- US forecasted to have added 188,000 jobs

- Canada expected to add 20,000 positions

- Investors to look for higher US wage growth

Dollar Caught Between Protectionism and Strong Economy

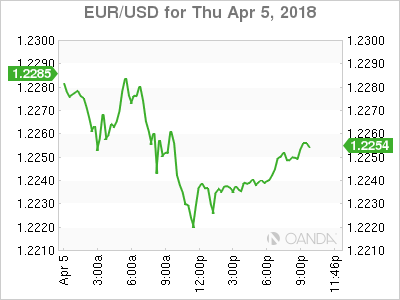

The EUR/USD fell 0.32 percent on Thursday. The single currency is trading at 1.2239 ahead of the NFP report. Employment data continues to be one of the pillars of the US economic recovery. The number of jobs has taken a backseat to the wages paid as a more telling indicator on the Fed’s next step. U.S. Federal Reserve Chair Jerome Powell chaired his first Federal Open Market Committee (FOMC) in March and announced a 25 basis points rate hike as expected. Inflation has not risen, but hawks within the central bank expect it to happen sooner rather than later which is why they want to lift rates now.

European data was uneven this week. PMIs in the EU were close to forecasts or slightly below, but it was the unexpected 0.7 fall in German retail sales that hurt the euro followed by another disappointing inflation estimate. The silver lining for the single currency has been the lack of traction of the US dollar as it struggles with trade war developments. China was on the offensive this week retaliating against US tariffs. The US has also increased its offensive by seeking the support of Europe and Japan to launch a WTO complaint on intellectual property violations against China.

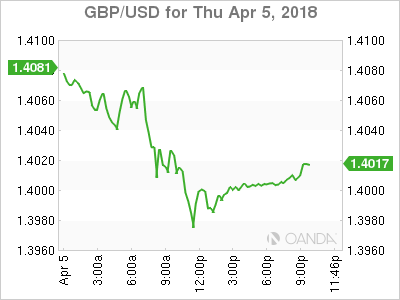

Pound Softer After Service PMI Miss

The GBP/USD fell 0.54 in the past 24 hours. The currency pair is trading at 1.40 after the UK’s Service PMI came in at 51.7. The index was below the forecasted 53.9 and shows a shrinking confidence from British purchasing managers in the Services industry. Earlier in the week the construction PMI was also below forecast and only manufacturing PMI was able to beat the estimate. Some of the drops have been suggested to be the result of bad weather.

The momentum of the dollar ahead of the biggest employment release of the month combined for a weaker pound. Interest rate hikes from the Fed are likely to come in at least twice more while the Bank of England (BoE) while not dissuaded by weather related issues could go as early as May for the second time in 10 years.

Canadian Jobs to Support Loonie

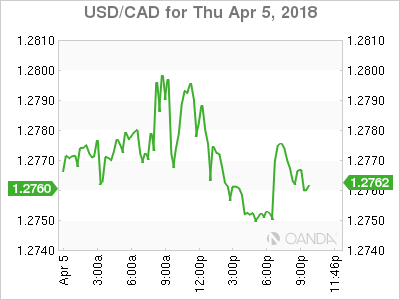

The USD/CAD lost 0.07 percent on Thursday. The currency pair is trading at 1.2756 very close to where the level seen at the Asian market open. NAFTA optimism has given the loonie a leg up. Canadian Prime Minister Justin Trudeau said on Thursday that the three nations are moving forward in a significant way. The Trump administration appears to be softening their hard ball tactics from earlier and with a deadline of May 1st to reach a deal the wheels have been greased.

Canadian and Mexican official will be in Washington meeting with trade representatives with the possibility of an unofficial meeting over the weekend potential bringing positive results.

Oil was higher despite the rise of the US dollar on Thursday. The easing of trade tensions despite the war of words between China and the US has benefited energy prices. Saudi Arabia announced a rise in prices confident there is demand for crude at that level. The phantom of increasing US shale production remains hanging over the price of crude as the Organization of the Petroleum Exporting Countries (OPEC) deal with Russia and other major producers is limiting output, giving those not part of the agreement the opportunity to increase production to capitalize on the higher prices.

Market events to watch this week:

Thursday, April 5

4:30am GBP Services PMI

8:30am CAD Trade Balance

Friday, April 6

8:30am CAD Employment Change

8:30am CAD Unemployment Rate

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change

8:30am USD Unemployment Rate