Sample Category Title

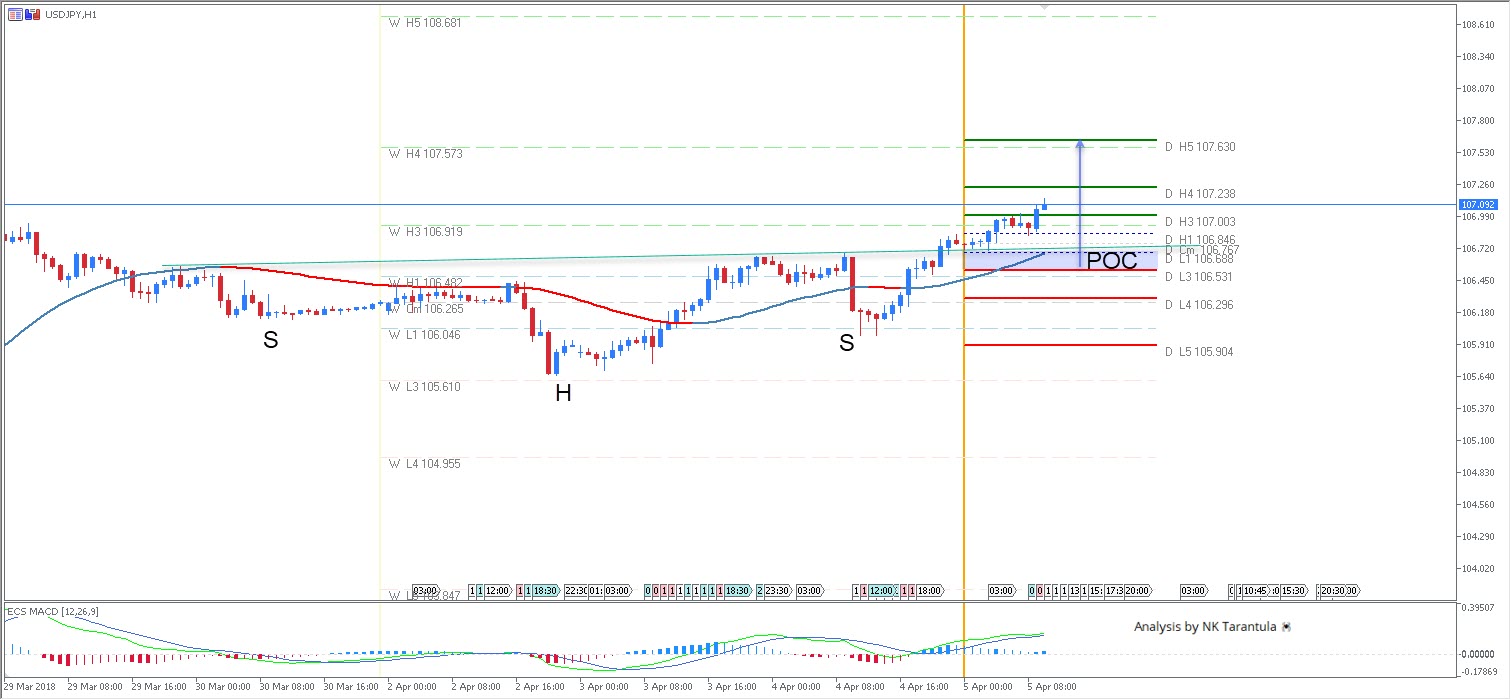

USD/JPY 106.75 Is Support Now

The USD/JPY has formed a bullish head and shoulders pattern and we might see a further bullish continuation. At this point the price has closed above D H3 107.00. A dip towards the POC zone could be used for buying into the dip. Better than expected NFP is giving a boost to USD so we might see the USD strength carry-over to Friday too. Targets are 107.32 and 107.63. Break of 107.63 might target 108.000 zone. As long as the pair is kept above 105.90, bull will have the upper hand.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

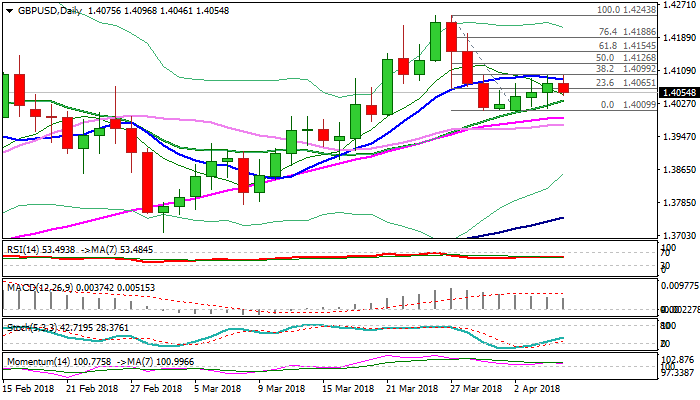

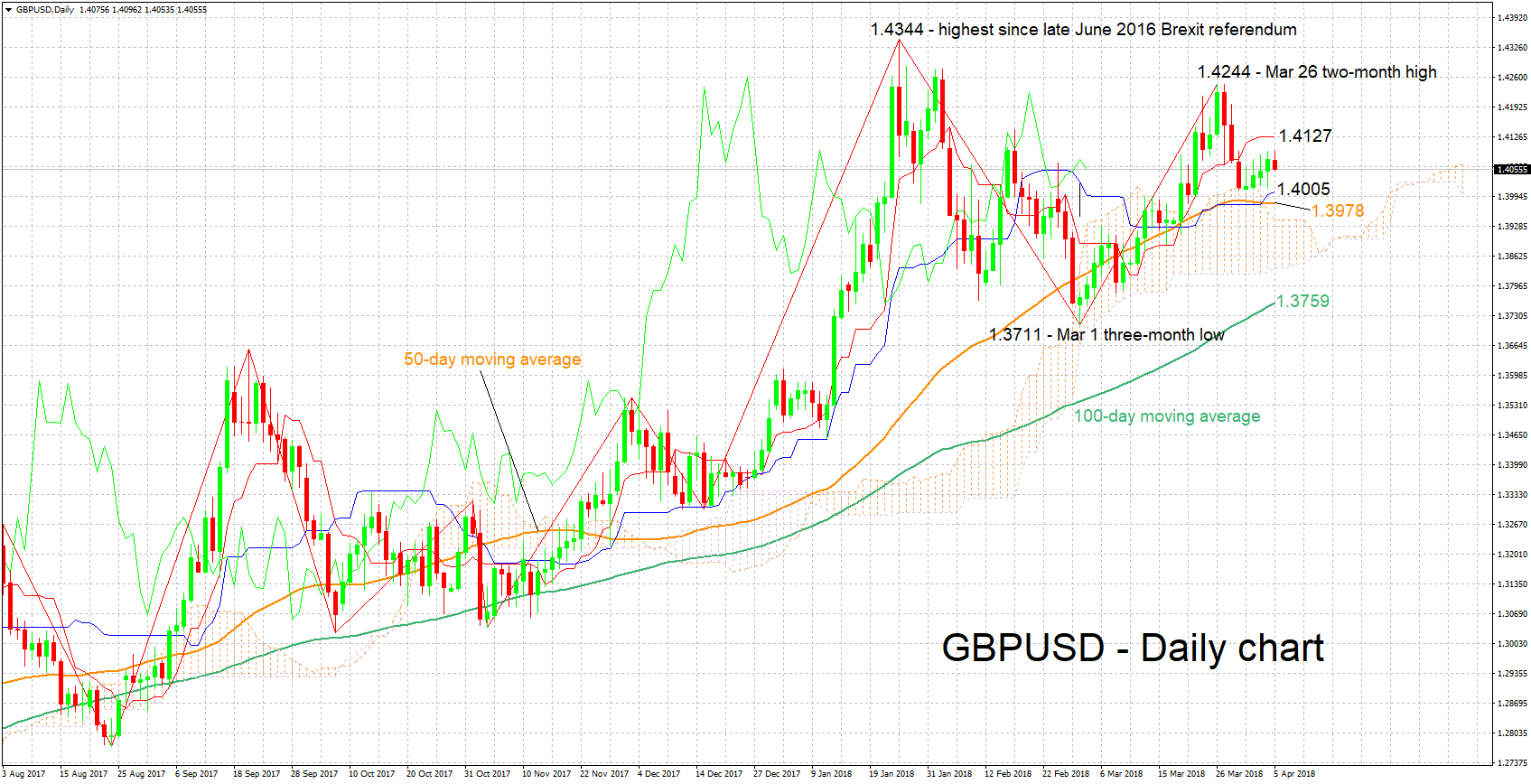

GBPUSD Is Trading Between Converging 20&10SMA’s And Looking For Directional Signal

Cable managed to regain traction after Wednesday's dip to 1.4014 which dented key supports (rising 20SMA/daily cloud top), where losses were contained. Subsequent recovery was again capped by 10SMA (1.4087) which marks key near-term barrier. Near-term action is moving within narrowing range, defined by 20&10SMA's and looking for a catalyst for fresh direction. Daily techs are bullishly aligned and supportive, but lacking momentum for final break through pivots at 1.408t (10SMA) and 1.4099 (Fibo 38.2% of 1.4243/1.4010) to resume recovery leg from 1.4010 higher base. On the other side, daily cloud is narrowing and twists in mid-April, which could attract for fresh weakness. Release of UK Services PMI is in focus today (Mar f/c 53.9 vs Feb 54.5), with better than expected outcome to trigger final push through 1.41 zone pivots. Conversely, downbeat figure could soften near-term tone and risk retest of key supports at 1.4010/00 zone.

Res: 1.4086, 1.4099, 1.4126, 1.4154

Sup: 1.4046, 1.4034, 1.4010, 1.3993

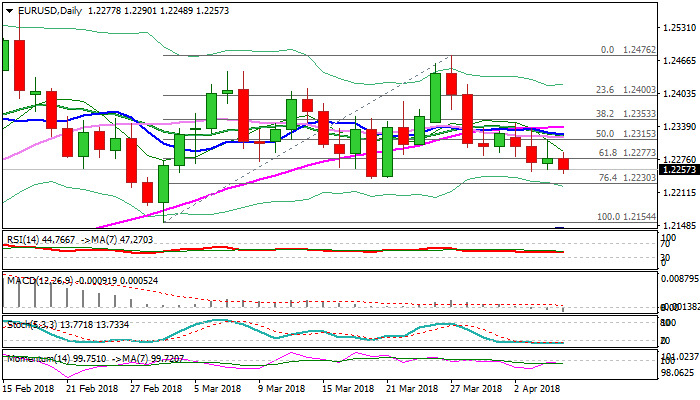

EURUSD – Negative Outlook Below 30SMA

The Euro holds in red in early European trading on Thursday and pressures Tuesday's low at 1.2253, following limited upside action in Asia (capped at 1.2290). Strong upside rejection on Wednesday, when upside attempts stalled just under 30 SMA which capped the action in past five days, maintains negative near-term tone. Also, Wednesday's close below 1.2277 (Fibo 61.8% of 1.2154/1.2476 ascend) was negative signal. Near-term bears eye targets at 1.2240/30 (20/21 Mar higher base/Fibo 76.4%), to open way towards key supports at 1.2154/45 (01 Mar trough/daily cloud base, reinforced by rising 100SMA). Hourly cloud (spanned between 1.2285 and 1.2300) capped overnight's upside attempts, guarding pivotal 30SMA (1.2317), break above which would sideline immediate downside risk. Releases of EU Services PMI and retail sales are key events of the European session. Services PMI is forecasted unchanged in March (55.0), while retail sales are expected to regain traction in Feb after negative figures in previous two months (Feb f/c 0.6% m/m vs -0.1% in Jan).

Res: 1.2290, 1.2317, 1.2337, 1.2362

Sup: 1.2240, 1.2230, 1.2200, 1.2154

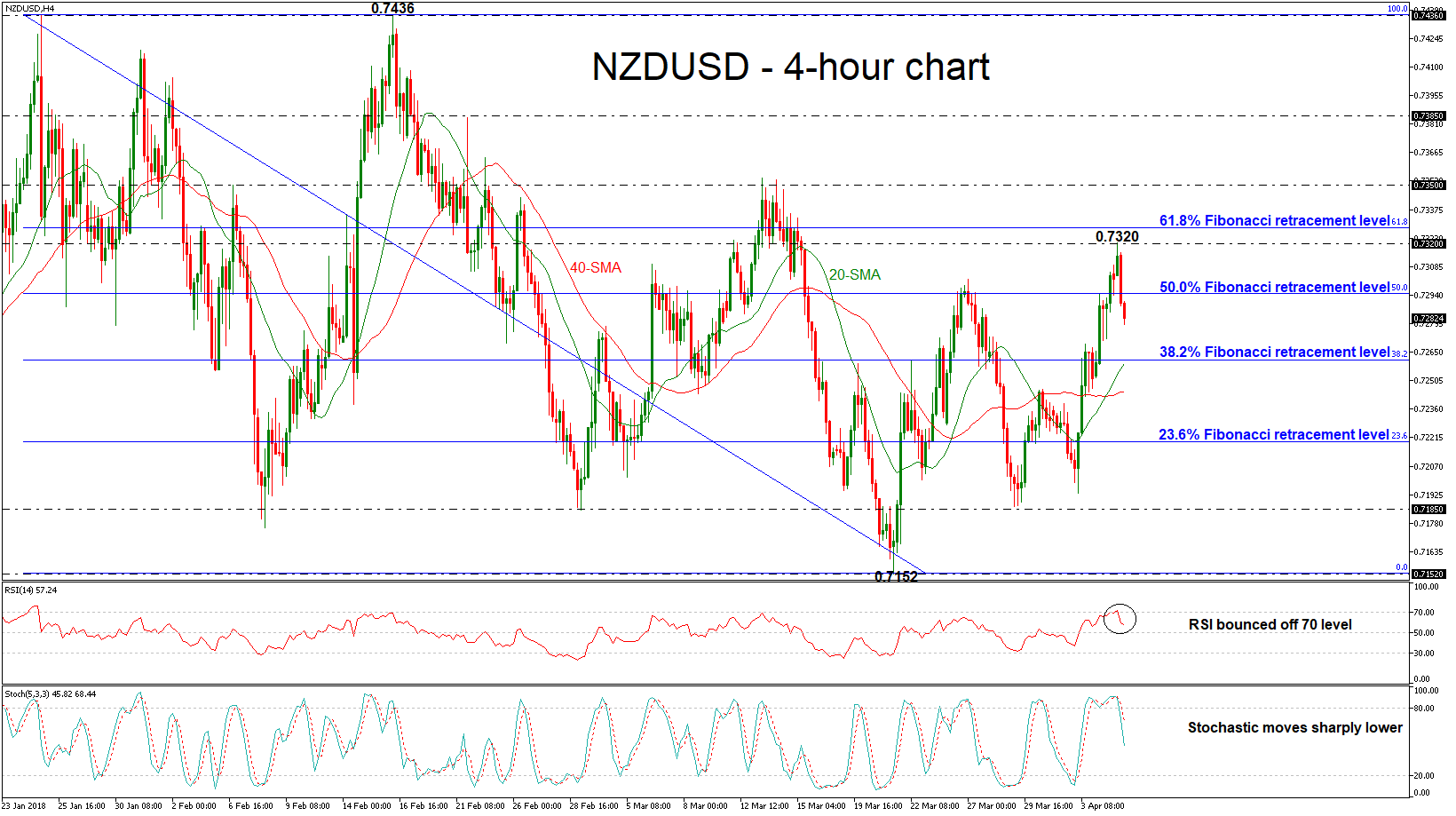

NZDUSD Remains Below 3-Week High, Next Level To Watch 38.2% Fibonacci Of 0.7260

NZDUSD has reversed back down again after finding resistance at the 3-week high of 0.7320 achieved during today’s Asian session. This top is just below the 61.8% Fibonacci retracement level of the downleg from the high of 0.7436 to the low of 0.7152.

Momentum indicators in the 4-hour chart, are pointing to a bearish bias with the RSI indicator bouncing off the overbought zone and approaching the 50 level in an aggressive manner. Moreover, the stochastics have overstretched and posted a bearish cross above the 80 level and turned into negative.

Further losses should see the 38.2% Fibonacci of 0.7260 acting as a major support as this is also where the 20-simple moving average (SMA) is currently standing. A drop below the 20-SMA would reinforce the bearish structure in the short-term and open the way towards the next key level of 40-SMA around 0.7245 at the time of writing.

In the event of an upside reversal, the 61.8% Fibonacci near 0.7330 could act as a barrier before being able to re-challenge the 0.7350 resistance zone. A break above this level would shift the short-term outlook to a more bullish one as it would take the pair towards the 0.7385 barrier.

To sum up, a bearish movement is predicted in the short-term as the technical indicators and the current market price action confirm the negative scenario.

Eurozone PMI Composite: Economy growing at 0.6% quarterly rate, down from unsustainably rapid 0.8-0.9%

Eurozone PMI Services Business Activity Index was finalized at 54.9 in March, revised down from 55.0. That compares to February reading at 56.2. Final PMI Eurozone Composite index wars revised down to 55.2, from 55.3. February's reading was at 57.1.

Quote from there lease by Chris Williamson, Chief Business Economist at IHS

Quote from there lease by Chris Williamson, Chief Business Economist at IHS

Markit:

- "The eurozone economy came off the boil in March, though continued to run hot. Although the final PMI numbers showed the weakest rise in business activity since the start of last year, adding to signs that the growth spurt has peaked, the surveys are still indicative of the economy growing at an impressive 0.6% quarterly rate in March, down from a clearly unsustainably rapid 0.8-0.9% rate around the start of the year.

- "Some pull-back from the elevated level of the PMI at the start of the year was always highly likely, and it's important to note that the slowdown generally represents a reduction in the number of companies reporting month-on-month improvements in business activity, as opposed to a rise in the number of companies reporting a deterioration in business conditions.

- "Some of the loss in growth momentum also appears to have been the result of temporary factors, such as bad weather and short-term capacity constraints, notably shortages of supplies and labour. Some reversal of these impediments should therefore hopefully help boost growth in April.

- "Gauging the true extent of any slowdown is consequently difficult due to the disruptions to business from bad weather in recent months. April's PMI data will therefore be particularly important in ascertaining true underlying growth momentum and in providing a steer on the likely timing of any ECB policy changes."

Markets Recover On Hopes For Trade Negotiations, UK Services PMI And US Trade Data Due

Here are the latest developments in global markets:

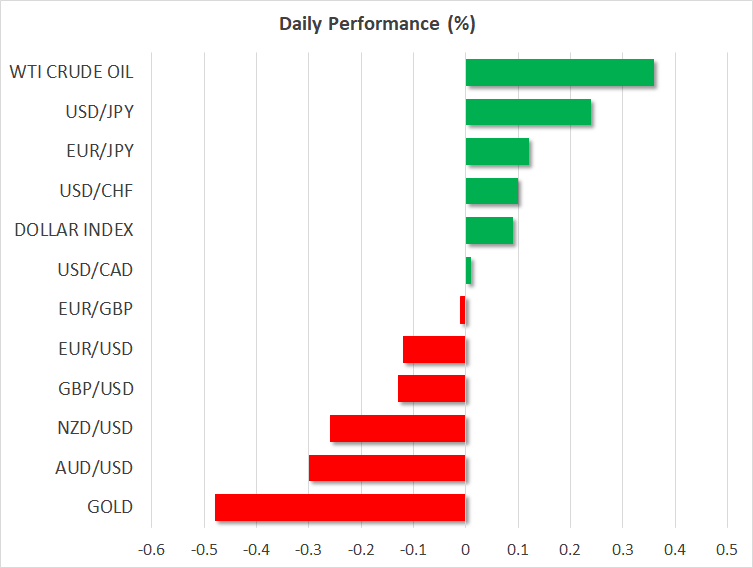

FOREX: The US dollar index traded 0.1% higher on Thursday. Against the yen, the dollar was up nearly 0.25% as concerns of an imminent trade war subsided, diverting flows out of the Japanese currency, which is considered a safe-haven asset.

STOCKS: US markets closed higher yesterday, managing to recoup earlier losses following comments from US National Economic Advisor Larry Kudlow that helped to calm the nerves of investors worried about a potential trade skirmish with China (see below). The Nasdaq Composite led the pack, climbing by 1.45%, while the S&P 500 and the Dow Jones gained 1.16% and 0.96% respectively. The recovery looks set to continue, as futures tracking the S&P, Dow, and Nasdaq 100 are all flashing green currently, pointing to a higher open today. The positive sentiment rolled over into Asia as well. In Japan, the Nikkei 225 surged by 1.5%, while the Topix rose 1.1%. Markets in China and Hong Kong remained closed for a public holiday. Meanwhile in Europe, futures tracking all the major benchmarks were a sea of green.

COMMODITIES: In energy markets, oil prices are higher today, with WTI and Brent rising by 0.35% and 0.45% correspondingly. The recovery in risk appetite, combined with a surprising drawdown in the weekly EIA inventory data released yesterday, helped prices to rebound. In precious metals, gold is nearly 0.5% lower today, extending its losses from yesterday. The safe haven metal sold off amid the broader risk-on environment in markets. It’s currently trading near the $1326/ounce level and looks to be headed for a test of the March 29 lows, at $1321

Major movers: Risk assets bounce as focus shifts to potential trade negotiations

Volatility was heightened across financial markets yesterday. Moves began after China unveiled its countermeasures to the US tariffs on technology products. The Chinese levies will target 106 US goods, among which are soybeans and aircrafts. The news triggered an immediate risk-off reaction, with US stock futures sliding alongside commodity-currencies like the aussie and the loonie, as well as the US dollar. Meanwhile, safe haven assets such as the yen and gold spiked higher.

However, the above reactions remained relatively short-lived. By the time US markets opened, sentiment started to recover, aided by some comments from the US National Economic Advisor Larry Kudlow. Asked whether the US tariffs against China may never go into effect, Kudlow replied yes, adding he expects intense negotiations. Previous market moves reversed soon thereafter, with US stocks finishing the day in the green and safe havens giving back prior gains to end the day lower.

What happens next is by far the most important chapter in the trade saga. If the two sides enter into negotiations, that would enhance the narrative that all this was only posturing ahead of tough talks, and that the situation won’t escalate further. Risk sentiment could recover, boosting stocks and commodity-currencies. Conversely, fresh countermeasures could reinforce concerns for an imminent trade war, pushing risk assets lower and safe havens higher. On balance, the scenario for negotiations appears more realistic. Neither side wants a real trade war, and by now, the US may have done enough for China to make some concessions in their trading relationship, which is probably all it wanted to achieve in the first place.

The dollar index is 0.1% higher today. Reflecting this, euro/dollar and sterling/dollar are both 0.1% lower. Note that the UK construction PMI unexpectedly fell into contractionary territory yesterday, and it will be interesting to see whether such a weakness is reflected in today’s all-important services PMI. The probability for a BoE rate hike in May still hovers around 70%.

Elsewhere, aussie/dollar and kiwi/dollar are lower by 0.3% and 0.25% respectively, giving back some of the gains they posted yesterday on the back of diminishing trade worries.

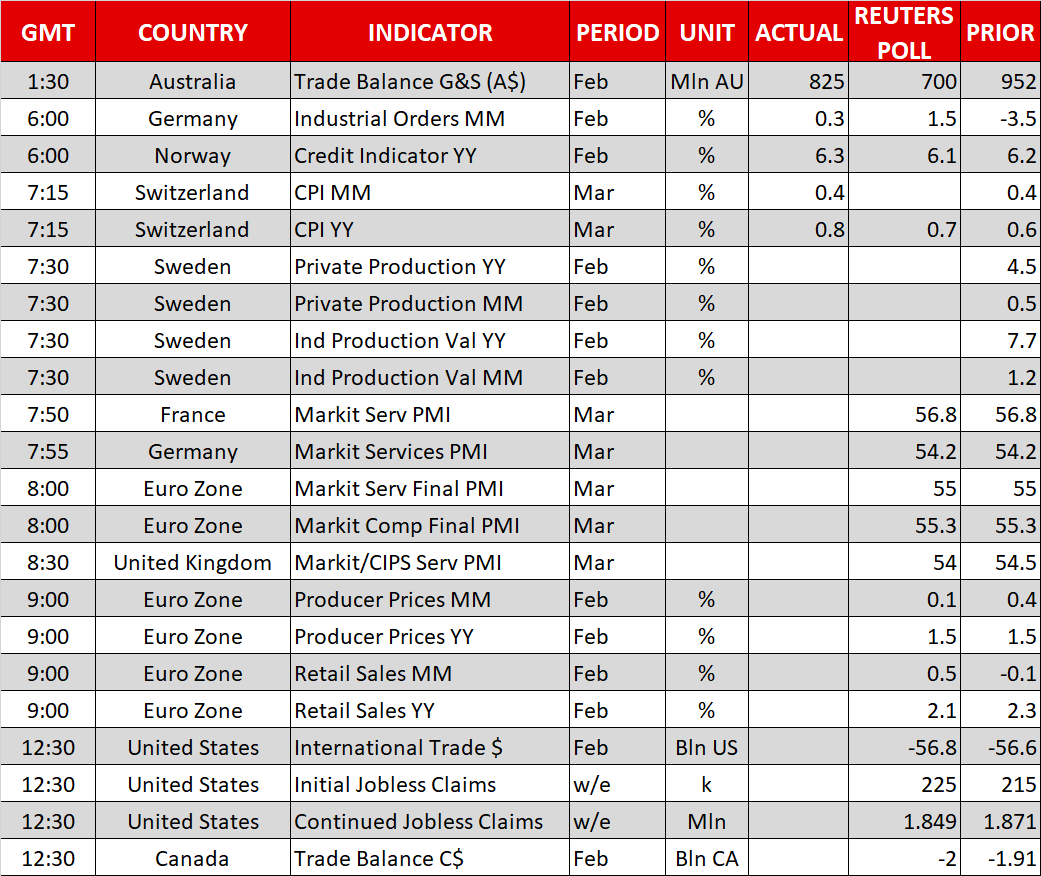

Day ahead: UK services PMI, eurozone producer prices & retail sales, and US trade data on the horizon

Thursday’s economic calendar features the services PMI print out of the UK, producer prices and retail sales out of the eurozone, as well as trade data out of the US.

At 0830 GMT, the UK’s services PMI for the month of March will be made public. The services sector dominates the UK economy, making up around 80% of GDP, and thus the reading could lead to positioning on sterling pairs, especially if it is seen as altering the odds for a rate hike by the Bank of England during its May meeting.

Earlier (0800 GMT), the eurozone will see the release of its PMI figures for the month of March for the services sector, as well as the composite measure that blends the manufacturing and services industries. However, the fact that the releases will pertain to the final prints rather than the preliminary estimates, renders considerable movements in euro pairs not that likely. Germany and France, the eurozone’s two largest economies, will also see the release of their respective services PMI numbers a little earlier (at 0755 GMT and 0750 GMT correspondingly).

Also attracting interest out of the eurozone and having the capacity to spur positioning in euro pairs are February’s producer prices and retail sales due at 0900 GMT.

The focus will next turn to North America. International trade data out of the US slated for release at 1230 GMT will be of significance, especially in light of recent developments on the trade front. In January, the US trade deficit rose to a more than nine-year high, with the Chinese-related shortfall steeply increasing. Also at 1230 GMT, initial and continued jobless claims for the week ending March 31 out of the world’s largest economy are scheduled for release, while at the same time Canadian trade data – February’s trade balance – will be made public.

Trade-related developments and their effects on currencies, but also asset classes such as equities, will yet again be on the forefront. After the Chinese retaliatory move to US tariffs, the latest “chapter” of the trade story was more calming to markets, with the US leaving the door open for negotiations with China. This move also acted as the catalyst behind the rebound in US equities on Wednesday.

Atlanta Fed President Raphael Bostic (voter) will be giving a speech at 1700 GMT, thought the topic of discussion renders any comments on monetary policy unlikely.

Technical Analysis: GBPUSD cautiously bullish in the short-term

GBPUSD has advanced in the four preceding trading days, in support of a positive short-term picture for the pair. This view is also supported by the positively aligned Tenkan- and Kijun-sen lines. The gains in previous days have not been considerable though, on balance pointing to a cautiously bullish bias.

A stronger-than-anticipated services PMI reading out of the UK could boost GBPUSD, with resistance potentially coming around the current level of the Tenkan-sen at 1.4127.

A data miss on the other hand, might exert selling pressure on the pair. Support in this case might be met around the Kijun-sen, which is currently located at 1.4005. The area around this point also includes the 50-day moving average at 1.3978 and the 1.40 handle that may hold psychological significance.

US releases due later on the day can also steer GBPUSD in either direction.

Swiss CPI rose 0.4% mom, 0.8% yoy in March

Swiss CPI rose 0.4% mom in March, above expectation of 0.3% mom. Annual rate rose to 0.8% yoy, up from 0.6% yoy in February and beat expectation of 0.7% yoy.

Swiss Federal Statistical Office (FSO) noted that "various factors contributed to the 0.4% rise compared with the previous month, such as an increase in the price of international package holidays, air transport and hotel accommodation. However, prices fell for medicines and fuel."

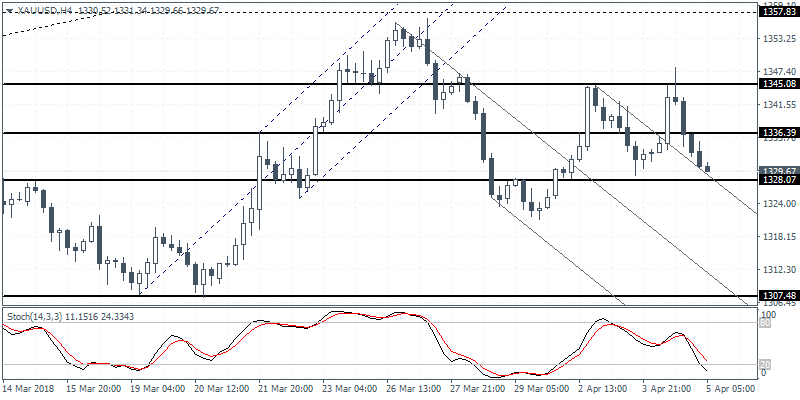

XAUUSD Intraday Analysis

XAUUSD (1329.67): Gold prices once again rallied to the 1345 level of resistance before giving up the gains to close flat on the day. The declines continue to extend lower with price breaking down below the 1336 level of support. Gold prices are now just a few points away from testing the 1328 handle. A breakdown below this level could signal further downside with the potential to test the 1307 region in the medium term.

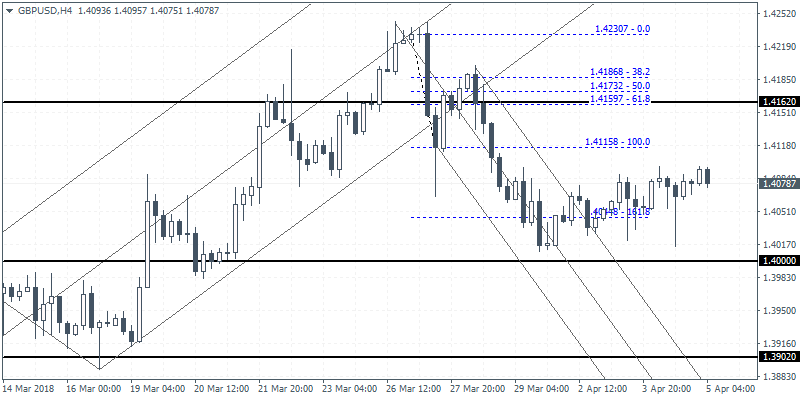

GBPUSD Intraday Analysis

GBPUSD (1.4078): The British pound extended modest gains on the day on Wednesday. The gains came despite the fact that the construction PMI fell into contraction in March. Price action remains well below the upside target at 1.4116 where resistance is most likely to be established. To the downside, the support level at 1.4065 could be tested in the near term. A close below this level could however put the upside bias in question with the possibility that the declines could extend toward 1.4000 handle.

EURUSD Intraday Analysis

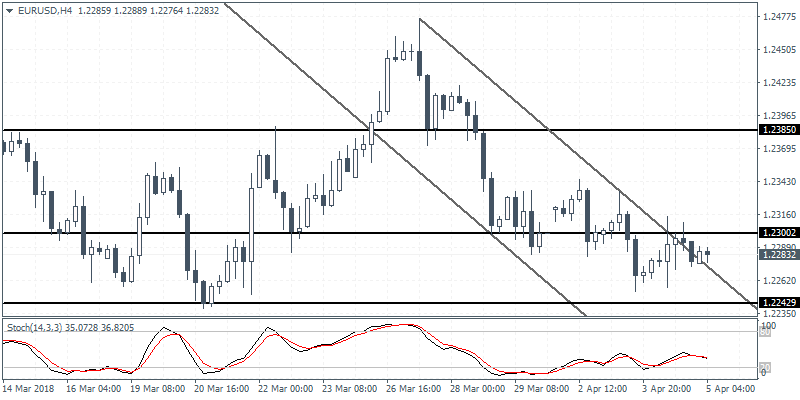

EURUSD (1.2283): The EURUSD was seen trading within the range established from Tuesday forming an inside bar as a result on the daily chart. A breakout from this range could potentially establish a short term direction. With the resistance level at 1.2300 formed, we expect a breakout to the downside as price action is likely to test the lower support level at 1.2250. In the event that the euro breaks out higher, then watch for a close above 1.2300. Price action could be seen then testing the next resistance level at 1.2385.