Sample Category Title

Economic Calendar Picks Up On Thursday

A steady stream of economic data from Europe and North America will headline the financial market newswire on Thursday.

Action picks up at 06:00 GMT when Germany releases its latest report on factory orders. The monthly reading is expected to show growth of 1.5% following a decline of nearly 4% the previous month.

The Swiss government will release its final estimate of March consumer inflation at 07:15 GMT. The consumer price index (CPI) likely rose 0.7% annually.

A steady stream of PMI data will make their way through the markets later in the morning, including the final Markit PMI Composite report for the Eurozone. The headline reading is expected to come in at 55.3, signifying steady growth for the euro area economy.

The European Commission’s statistical agency will report on producer inflation and retail sales at 09:00 GMT in two separate reports. The producer price index (PPI) likely rose 1.5% annually in February. Retail sales, which are a proxy for consumer spending, likely jumped 0.5% month-on-month.

Shifting gears to North America, the US government will report on the February trade balance at 12:30 GMT. Washington’s deficit likely ticked up to $56.8 billion from $56.6 billion the month before.

The Labor Department’s weekly jobless claims report will also make headlines at 12:30 GMT. The number of Americans filing for first-time unemployment benefits likely rose by 10,000 to a seasonally adjusted 225,000 last week.

North of the border, the Canadian government will report on international trade at the same time as the US reports. Canada’s trade deficit with the rest of the world likely rose to $2 billion in February from $1.91 billion the previous month.

On the monetary policy front, FOMC members Raphael Bostic is scheduled to deliver a speech at 17:00 GMT.

AUD/USD

The Australian dollar steadied on Thursday after government data showed a broad decline in the nation’s trade surplus. Australia’s surplus weakened to $825 million in February from $1.06 billion the month before. AUD/USD traded within a 30-pip range Thursday, eventually settling down 0.1% at 0.7706.

USD/CAD

The USD/CAD extended its downward journey on Wednesday, as prices fell below 1.2800. The currency pair was last seen trading at 1.2765, where it was down about 0.1% from the previous close. The pair faces immediate resistance at the psychological 1.2800 handle. On the flipside, support is located at 1.2730.

GBP/USD

Wednesday was another volatile session for the cable, as prices fell more than 50 pips to a low of 1.4023. Prices quickly recovered, with GBP/USD now trading at 1.4076. The pair faces stronger selling pressure at around 1.4100 but appears to have established a strong base of support near 1.4000. Latest price movements suggest that optimism surrounding the Brexit deal has largely faded.

EUR/USD

Europe’s common currency failed to recover ground north of 1.2300, leaving it exposed to further downside risk. The EUR/USD exchange rate was last seen trading at 1.2282, where it was little changed. Immediate resistance is located above 1.2300. On the downside, support is found around 1.2250.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7678; (P) 0.7699; (R1) 0.7737; More...

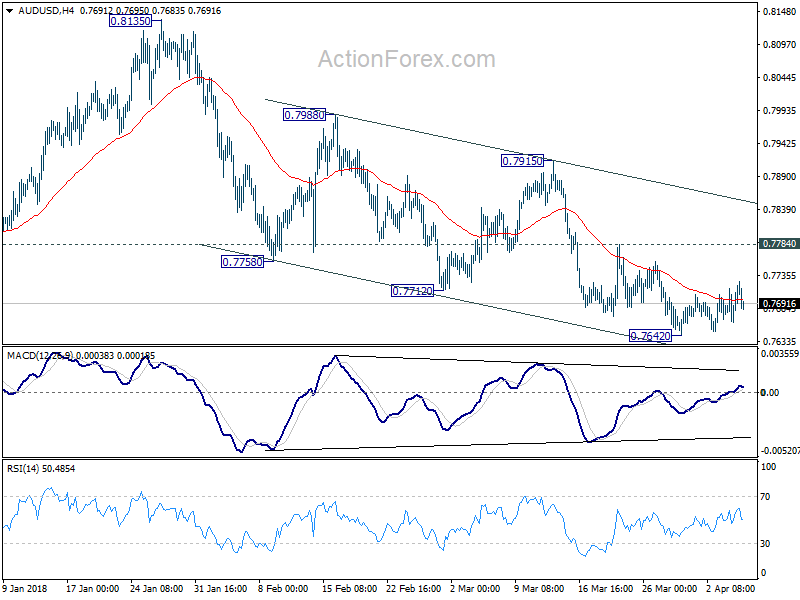

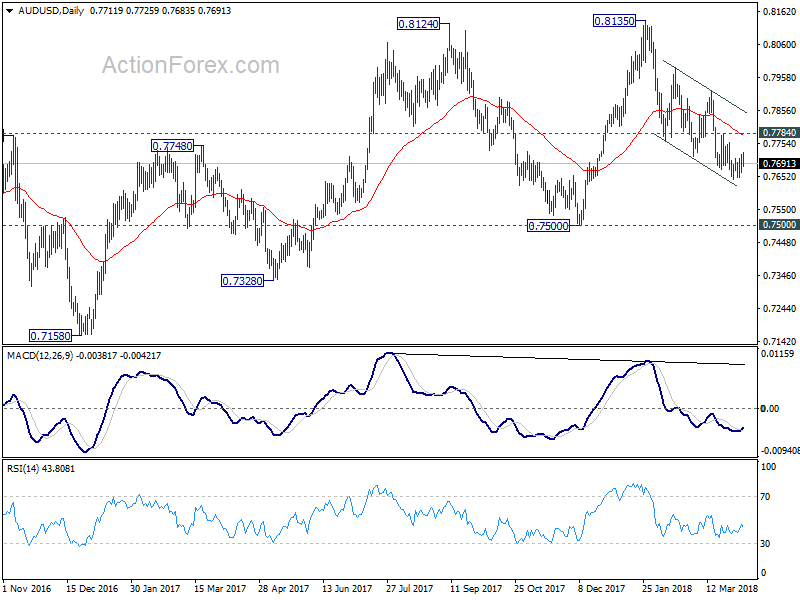

AUD/USD is still bounded in consolidation from 0.7642 temporary low and intraday bias stays neutral first. With 0.7784 resistance intact, near term outlook stays bearish and deeper decline is expected. On the downside, break of 0.7642 to will turn bias to the downside to extend recent fall from 0.8135 to retest 0.7500 key support level. On the upside, however, break of 0.7784 will suggest near term reversal and turn bias to the upside for 0.7915 resistance first.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

Services PMI Data For UK Expected To Show Further Weakness

At 07:15 GMT, Spanish Markit Services PMI (Mar) will be out with an expected headline number of 56.0 and a prior reading of 57.3. The consensus is for a further softening from the high of 58.3 created in July. However, the data has experienced a strong rebound in February and March, exceeding expectations on both occasions. The data is down from a high of 60.3 in 2015. EUR pairs may see an impact from this data release.

At 07:15 GMT, Swiss Consumer Price Index (YoY) (Mar) is expected to be 0.7% against the previous 0.6%. CHF pairs may be affected by this data.

At 07:55 GMT, German Markit Services PMI (Mar) is expected to be unchanged at 54.2. After reaching a multi-year high of 57.3 in February, this data has come back into a range under 56.0. German Markit PMI Composite (Mar) is also expected to be unchanged at 55.4. Traders will be watching for the numbers to deviate from expectations and create volatility in EUR pairs.

At 08:00 GMT, Eurozone Markit Services PMI (Mar) is expected to be unchanged at 55. This figure is expected to slip back after hitting a high of 58.0 in February. Markit PMI Composite (Mar) is also expected to be unchanged at 55.3. EUR crosses may be impacted by this data release.

At 08:30 GMT, UK Markit Services PMI (Mar) is expected to come in at 54.0 from 54.5 previously. This data is continuing to decline from a high of 62.5 in 2013 but for now, it is comfortably holding above 53.0, showing modest growth. GBP crosses may move on the results of this release.

At 12:30 GMT, US Trade Balance (Feb) is expected to be $-56.8B against $-56.6B previously. This shows a further decline to 2008 levels. Continuing Jobless Claims (Mar 23) is expected to be 1.849M against a previous 1.871M. Initial Jobless Claims (Mar 30) is expected to be 225K from 215K previously. These jobs figures indicate that Unemployment is at the lowest levels in years, with strong positive implications for the US economy. USD pairs may be moved by this data.

At 12:30 GMT, Canadian International Merchandise Trade (Mar) is expected to be $-2.00B against a previous number of $-1.91B. CAD pairs may be moved by this data.

At 17:00 GMT, US FOMC Member Bostic is due to speak about financial literacy at the University of South Florida, in Sarasota. Audience questions are expected and comments may result in moves in USD crosses.

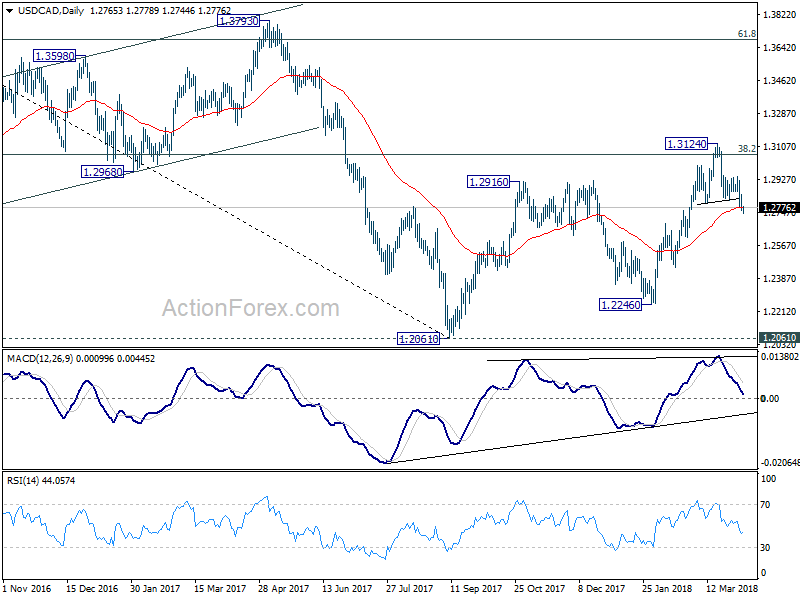

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2732; (P) 1.2789; (R1) 1.2822; More....

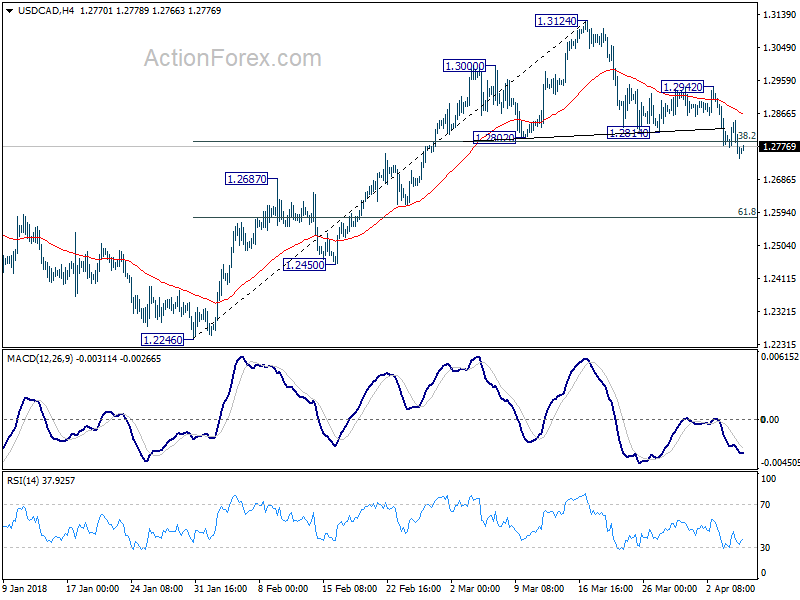

USD/CAD drops to as low as 1.2744 so far as decline from 1.3124 extends. The break of 38.2% retracement of 1.2246 to 1.3124 at 1.2789 should confirm near term reversal, with head and shoulder top pattern (ls: 1.3000; h: 1.3124; rs: 1.2942). Intraday bias stays on the downside for 61.8% retracement at 1.2581 next. Also, noted that current development suggest rejection by 1.3065 fibonacci level. And deeper decline could be seen back to 1.2246 and below eventually. On the upside, break of 1.2942 is needed to confirm completion of the decline. Otherwise, outlook will stay cautiously bearish in case of recovery.

In the bigger picture, outlooks is turned a bit mixed again. Strong support was seen from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. But there was no follow through buying above 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Rejection by 1.3065 will argue that price action from 1.2061 is merely a three wave corrective pattern. And 1.2061 will be put back into focus with medium term bearishness revived.

The US And Mexico Continue NAFTA Negotiations

US Unemployment data will be released this afternoon, ahead of NFP data on Friday. This is expected to show a slight rise in Initial Jobless Claims from the low reached last month. The trend here is for claims to continue to move lower, with the Fed highlighting concerns that the economy is running out of workers to fill positions. This will be indicated by any uptick in Average Hourly Earnings data tomorrow.

The US and Mexico are continuing NAFTA negotiations after President Trump signed a proclamation to camp US Troops on the border as part of his Border Wall Project. He is the fourth US President in a row to do this, so there is nothing new there. The Auto Content news is getting a second wind in markets and Canadian officials are positive on a “symbolic agreement in principle” showing consensus on some issues. However, the main sticking points are government procurement and dispute settlement.

Italian Unemployment (Feb) was 10.9% v an expected 11.0%, against the previous 11.1%. This dataset has fallen to levels not seen since 2012 after reaching a high of 13.4% in January 2015. The Rate is still high, comparatively speaking, but it has slid under the line this month to paint a positive picture. EURUSD moved up from 1.22877 to hit a high for the day of 1.23144 following this data release.

UK Construction PMI (Mar) came in at 47.0 against an expected headline number of 50.8, from 51.4 prior. The consensus was for a further softening from the high of 53.1 created in December but the data actually exceeded those expectations. The industry data has now slipped back under 50.0 from a high of 64.6 reached in 2014. This shows the weakness of the UK Construction sector, especially for new orders. The weather exacerbated the problem as employees were unable to attend work and materials were not delivered. Respondents were, however, positive about the coming months, with many hiring additional staff and planning expansions. GBPUSD fell from 1.40837 to 1.40282 in the hours following this data release.

Eurozone Unemployment Rate (Feb) was as expected at 8.5%, against the previous 8.6%. Consumer Price Index – Core (YoY) (Mar) was 1.0% v an expected 1.1%, from the previous 1.0%. Consumer Price Index (YoY) (Mar) was as expected at 1.4%, against the previous 1.1%. As expected, the Unemployment Rate reached a new low of 8.5%, a level not seen since April 2009. The recovery in the Euro area is still strong and growing. CPI is stabilizing around 1.2%.

US ADP Employment Change (Mar) was 241K v an expected 208K, against 235K previously, which was revised up to 246K. This data has remained above 200 for the last three months showing that the US economy is continuing to add jobs. The data series has beaten expectations for four straight months, with the strong revisions providing the icing on the cake. USDJPY recovered from its low of 106.116 to reach a high of 106.352 on this data release.

In his speech yesterday, the US Fed’s Bullard said that a trade war would be disruptive but may yield better arrangements, however, it also presents downside risks and uncertainty. He would wait and see what happens on trade before changing outlook. He sees 2.5% US GDP growth in 2018 and 2.2% in 2019. More uncertainty is likely keeping rates lower for longer. He said that it is possible the nominal yield curve will invert sometime in the next year.

US Markit Services PMI (Mar) was 54.0 v an expected 54.3, against a previous number of 54.1. This data missed on expectations after outperforming last month, but the month-on-month decline was expected. Markit PMI Composite (Mar) was 54.2 v an expected 54.1, against 54.3 previously. GBPUSD rose from 1.40725 to 1.40886, moved by this data release.

US ISM Non – Manufacturing PMI (Mar) was 58.8 v an expected 59.0, against 59.5 previously. The headline number was largely in line with expectations, albeit missing slightly to the downside. This is in the upper range of the data releases we have seen over the past seven years but off the highs of above 65.0 reached before the financial crisis. Factory Orders (MoM) (Feb) were 1.2% v an expected 1.7%, from -1.4% prior, which was revised up to -1.3%. This data missed the expected reading but the number remained in the recent range of +3.0% to -3.0%. The upward revision of the previous reading took some of the sting out of the miss. USDCAD fell from 1.28315 to 1.28146 following this data release.

In a speech about diversity in economics at Central State University, in Ohio yesterday, US FOMC Member Mester said that the diversity of views at US central bank leads to better policy.

EURUSD is down -0.06% overnight, trading around 1.22709.

USDJPY is up 0.13% in early session trading at around 106.917.

GBPUSD is down -0.10% this morning, trading around 1.40620.

USDCAD is up 0.05% in early trade at around 1.27745.

Gold is up 0.33% in early morning trading at around $1,328.70.

WTI is up 0.09% this morning, trading around $63.65

Stocks Staged Massive Rebound as Trade War Development Takes a Rest For Now

While the initial selloff in US stocks were steep, they quickly recovered and didn't look back. DOW made a massive 700 pts come back from session low at 2523.16 to close at 24264.30, up 230.94 pts or 0.96%. Nikkei followed and staged a strong 1.5% rebound. For now, the first set of the first battle of US-China trade war is done. The Donald Trump led government and China have both unveiled their cards. But no implementation date for the tariffs are set as US will need to go through the process of public input till May 22. China certainly won't have any drastic action before the US concludes the Section 301 tariffs. Hence, it's now time or the markets to focus back on other issues first.

In the currency markets, Canadian Dollar is lifted by positive NAFTA news and is trading as the strongest one for the week. The Loonie is maintaining gains throughout Asian session. Swiss Franc and the Japanese Yen are the weakest ones on flip-flop of market sentiments. While Dollar recovers today, it's staying mixed for the week.

Technically, USD/CAD's break of 1.3065 fibonacci support should confirm near term reversal and more downside should be seen ahead. EUR/USD is still on course for 1.2238 support and below despite yesterday's recovery, as it's held well below 1.2344 resistance. There are two main focuses for today. Firstly, USD/CHF is going to take on 0.9626 key fibonacci resistance. GBP/JPY will also has another test attempt on 150.92 cluster resistance too.

Fed Bullard and Bernard: Current trade policy increases uncertainty on outlook

St Louis Fed President James Bullard said yesterday that now, federal funds rate at 1.50-1.75% is closer to "neutral" than in previous years. And it's "no necessary" to raise policy rate further as "inflation is already below target". And the surprised growth in 2017 has "stalled so far in 2018". Regarding US trade policy with China, Bullard said it "increases the uncertainty around the forecast". Nonetheless, to him, it's " too early to tell what the actual impact will be on the U.S. economy."

Fed Governor Lael Brainard also said yesterday that trade policy is a "material uncertainty" to the economy outlook. She added that "it's very hard to say now, how that could evolve -- but it's certainly something that I take into account, in thinking about risks."

Dallas Fed: Steel tariffs could trim 0.25% GDP over the long run

According to research paper by the Dallas Fed, the 232 steel and aluminum tariffs would likely "trim a quarter percent" from the US GDP over the long run. While the "metal industries would likely expand", heavy industries like machines and equipment would "probably contract along with aggregate capital formation." It warned that the main risks lie in the potential for "retaliation" and the possibility of a "trade war". Full research here.

Canadian Dollar higher on good NAFTA progress

Canadian Dollar strengthens again on positive news regarding NAFTA renegotiation. It's been reported repeatedly that Trump is pushing to have a draft NAFTA agreement by next week. For now, there are so many outstanding issues that it's impossible to have a full agreement that soon. But there is a chance of a "symbolic agreement" signalling some consensus, as soon as next week.

Comments from officials were also positive. Canadian Foreign Minister Chrystia Freeland said yesterday that "we're making good progress on NAFTA … having said that, we're not there yet." And that's seen by the markets as positive comments. She will meet with US Trade Representative Robert Lighthizer today. White House top economic advisor Larry Kudlow also said that there would be "some positive news on NAFTA … and I think the stock market is going to love that."

On the data front

Australia trade surplus narrowed to AUD 0.83b in February, above expectation of AUD 0.72b. German factory orders rose 0.3% mom in February, below expectation of 1.5% mom. Swiss CPI, Eurozone Services PMI final, PPI and retail sales will be featured in European session. But main focus will be on UK services PMI.

Later in the day, Canada will release trade balance. US will release Challenger job cuts, jobless claims and trade balance.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2732; (P) 1.2789; (R1) 1.2822; More....

USD/CAD drops to as low as 1.2744 so far as decline from 1.3124 extends. The break of 38.2% retracement of 1.2246 to 1.3124 at 1.2789 should confirm near term reversal, with head and shoulder top pattern (ls: 1.3000; h: 1.3124; rs: 1.2942). Intraday bias stays on the downside for 61.8% retracement at 1.2581 next. Also, noted that current development suggest rejection by 1.3065 fibonacci level. And deeper decline could be seen back to 1.2246 and below eventually. On the upside, break of 1.2942 is needed to confirm completion of the decline. Otherwise, outlook will stay cautiously bearish in case of recovery.

In the bigger picture, outlooks is turned a bit mixed again. Strong support was seen from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. But there was no follow through buying above 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Rejection by 1.3065 will argue that price action from 1.2061 is merely a three wave corrective pattern. And 1.2061 will be put back into focus with medium term bearishness revived.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Feb | 0.83B | 0.72B | 1.06B | 0.95B |

| 06:00 | EUR | German Factory Orders M/M Feb | 0.30% | 1.50% | -3.90% | -3.50% |

| 07:15 | CHF | CPI M/M Mar | 0.30% | 0.40% | ||

| 07:15 | CHF | CPI Y/Y Mar | 0.70% | 0.60% | ||

| 07:45 | EUR | Italy Services PMI Mar | 53.9 | 55 | ||

| 07:50 | EUR | France Services PMI Mar F | 56.8 | 56.8 | ||

| 07:55 | EUR | Germany Services PMI Mar F | 54.2 | 54.2 | ||

| 08:00 | EUR | Eurozone Services PMI Mar F | 55 | 55 | ||

| 08:30 | GBP | Services PMI Mar | 54 | 54.5 | ||

| 09:00 | EUR | Eurozone PPI M/M Feb | 0.00% | 0.40% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Feb | 1.50% | 1.50% | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Feb | 0.60% | -0.10% | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Mar | -4.30% | |||

| 12:30 | CAD | International Merchandise Trade (CAD) Feb | -2.1B | -1.9B | ||

| 12:30 | USD | Initial Jobless Claims (MAR 31) | 223K | 215K | ||

| 12:30 | USD | Trade Balance Feb | -56.5B | -56.6B | ||

| 14:30 | USD | Natural Gas Storage | -63B |

US Treasuries Underperforming German Bunds

Markets

The US and China raised the stakes in their standoff on trade over the past 48 hours. Both sides sharpened their knifes by announcing lists of products possibly subject to a cumulative $50bn in tariffs. The Chinese response came only 11 hours after the US's opening gambit, taking market participants by surprise. Risk aversion reigned during yesterday's European trading hours. US stock markets opened around 1.5% weaker. Spill-over effects to other markets remained very limited, apart from small, temporary, gains for core bonds and the Japanese yen. EUR/USD is still stuck in its "comfort zone" roughly between 1.2250 and 1.2350.

Risk sentiment turned for the better as US dealers entered trading. High rank US (eg Commerce Secretary Ross and economic advisor Kudlow) and Chinese officials downplayed all the fuzz created by the proposed tariffs and emphasized that both countries will now enter a lengthy discussion period with the aim of finding a new "normal". US stock markets closed 1% to 1.5% higher with the three main indices painting a potential technical bullish engulfing signal on the charts. Core bonds ended mixed with the US Note future underperforming the German Bund. The US yield curve bear steepened with yields 1.4 bps (2-yr) to 2.7 bps (10-yr) higher. The US 10-yr yield returned north of previous support (2.8%). Changes on the German curve were limited between -0.3 bps and +0.2 bps. The dollar took the upper hand as risk sentiment improved, which was mainly visible in USD/JPY's return from 106 towards 107. A move above 107.29 (first) resistance would break the yen's momentum and would be a third technical sign that risk sentiment could improve in coming days. EUR/USD finished the day at 1.2278, nearly unchanged from the 1.2271 opening. EUR/GBP closed (0.8721) near opening levels as well, but was subject to more intraday volatility via stock markets. Strong US eco data (ADP, non-manufacturing ISM) and stubbornly low core EMU inflation were overshadowed yesterday by developments in the US/Chinese trade dispute.

Asian stock markets join WS's rebound overnight with China and Hong Kong closed. The US Note future and Japanese yen lose somewhat more ground, suggesting an improvement in risk sentiment at the start of European trading as well with a lower opening for the Bund. Today's eco calendar contains only second tier eco data with final PMI's, retail sales and PPI data in the EMU and weekly jobless claims in the US. Risk sentiment will be the key driver for trading. We think that there is room for a more sustained improvement which could weigh on core bonds with US Treasuries underperforming German Bunds. This week's US eco releases were strong and bode well for tomorrow's payrolls. Risk-on sentiment, strong US data and a rising US/German yield differential should help the dollar on FX markets, especially against the yen, but also against the euro. Sterling traditionally profits from an improvement in risk sentiment, but traders will also take today's services PMI into consideration. Consensus expects a small setback from 54.5 to 54 in March. A good outcome (like the manufacturing PMI earlier this week) could trigger a test of the key 0.8668/0.87 support area in such market conditions. We don't anticipate a break lower at this stage. An agreement on the Irish border between the EU and the UK is probably necessary to give sterling another sustained push in the back.

News Headlines

US President Trump's economic adviser Kudlow joined Commerce Secretary Ross in stressing there's still time to talk with Chinese official. "None of the tariffs have been put in place yet, these are all proposals". The Chinese ambassador to the US, who met with the acting US secretary of state, also reiterate a preference for discussion

The Trump administration has softened a key Nafta demand for more North American content in car manufacturing. It's a potential olive branch on arguably the biggest sticking point as the US pushes to reach a stopgap deal this month, according to three people familiar with the talks.

Asian Equity Markets Trade Generally Higher

General Trend:

- Financial press headline says Asia stocks rise as trade war concerns ease amid comments from US officials

- Market participation limited amid holidays in China, Taiwan, Hong Kong

- South Korean chipmakers gain as a local press report suggested direct sanction impact could be limited

- Samsung Electronics expected to report prelim Q1 figures on Friday

- Net Foreign purchases of Japanese equities rise for first time since Feb (weekly data)

- Australia Feb Trade Surplus above ests: Little initial impact on bond and currency markets

- Australia March services surveys signal further expansion

- Australia 3-month bank bill rate fixed lower for the first time since early Feb; Banks rise amid lower funding costs

- Malaysia Feb Exports to China decline

- Market closures expected on Friday include China, Taiwan and Thailand

- Philippines Central Bank chief said will evaluate appropriateness of measured policy response; March CPI data above ests

Headlines/Economic Data

Japan

- Nikkei 225 opened +1%: closed +1.5%

- TOPIX Real Estate index +2.6%

- Japanese mega-banks rise over 1%

- (JP) Former Bank of Japan (BOJ) member Hideo Hayakawa: BOJ likely to raise its yield target within a year after gains in consumer prices ex-fresh food and energy reach 1% (currently ~0.5%) - financial press

- (JP) Japan Investors Net Buying of Foreign Bonds: -¥774.3B v +¥790.1B prior week; Foreign Net Buying of Japan Stocks: +¥228.8B v -¥2.2T prior week

- (JP) Japan said to plan first step towards legalizing initial coin offerings (ICOs) - US financial press

Australia/New Zealand

- ASX 200 opened +0.2%; closed +0.5%

- ASX 200 Financials index +1.3%, REIT +0.8%, Energy +0.6%; Resources -0.5%

- Bluescope Steel [BSL.AU]: S&P raises credit rating 1 notch to BBB- (investment grade) from BB+; Outlook Stable

- (AU) AUSTRALIA FEB TRADE BALANCE (A$): 825M V 725ME

- (AU) Australia Mar CBA PMI Services: 55.6 v 54.2 prior; Composite: 55.4 v 54.3 prior

- (AU) Australia Mar AIG Performance of Services Index: 56.9 v 54.0 prior

- Constellation Brands and Champ Private Equity said to sell Accolade Wines to Carlyle Group for ~A$1.0B - US financial press

- (NZ) New Zealand sells NZ$100M in 2.5% Sept 2040 Bonds, avg yield: 2.1584%; implied bid to cover: 1.84x

China/Hong Kong

- Shanghai Composite and Hang Seng are closed for holidays

- (CN) US govt spokesperson: Chinese agricultural tariffs don't comply with WTO rules

- (CN) China govt to begin retaliatory duties on US goods whenever US implements its tariffs - Chinese press

- (CN) Financial press article comments on how China has held back from targeting US Treasuries amid trade dispute

Korea

- Kospi opened +0.8%

- (KR) South Korea chipmakers not immediately or directly impacted by US tariffs on products from China – Yonhap

- (KR) There is speculation that North Korea may have shut down a nuclear reactor - Local Media

- (KR) South Korea Finance Min Kim: Will stabilize FX markets if needed regardless of whether decides to disclose intervention details; Disclosing intervention does not mean losing FX sovereignty.

Other Asia

- (PH) Philippines Mar CPI M/M: 0.6% v 0.8% prior; Y/Y: 4.3% v 4.2%e

- (PH) Philippines Central Bank (BSP) chief Espenilla comments on March inflation data: Will carefully evaluate appropriateness of a measured policy response to firmly anchor inflation expectations

- (MY) Malaysia is seeking exemptions from the US tariffs on steel and aluminum - US financial press

- (TH) Thailand Central Bank Chief Veerathai: Thailand is 'definitely not a currency manipulator'; focusing more on impact of Baht volatility

- Looking Ahead: Reserve Bank of India (RBI) rate decision expected later today (unchanged expected)

North America

- US equity markets closed higher: Dow +1%, S&P500 +1.2%, Nasdaq +1.5%, Russell 2000 +1.3%

- S&P500 Consumer Discretionary +1.8%, Consumer Staples +1.6%

- Boeing and Apple may get 'hurt by accident in trade war' - Xinhua

- (US) President Trump tweets "We are not in a trade war with China, that war was lost many years ago by the foolish, or incompetent, people who represented the U.S. Now we have a Trade Deficit of $500B a year, with Intellectual Property Theft of another $300B. We cannot let this continue!"

- (CN) White House spokesperson: we are going through review period on China tariffs; will be a couple months before they are implemented

- (US) White House Econ Adviser Kudlow: 'It's possible' China tariffs are a negotiating tactic but 'I would take the president seriously'

- (US) Fed's Mester (FOMC voter, hawk): Does not comment on monetary policy in prepared remarks

- (US) DOE CRUDE: -4.6M V +1ME

- (BZ) Brazil Court rules that Former President Lula can be imprisoned while going through appeal process (making him unable to run again for President this Oct)

Europe

- Fidessa Group [FDSA.UK]: SS&C is one of the two unnamed parties that have made approaches to Fidessa at a premium to the standing offer from Temenos - FT

Levels as of 02:00ET

- Kospi +1.5%

- Equity Futures: S&P500 +0.4%; Nasdaq100 +0.7%, Dax +0.5%; FTSE100 +0.5%

- EUR 1.2274-1.2291 ; JPY 106.70-107.04 ; AUD 0.7685-0.7728 ;NZD 0.7288-0.7323

- Jun Gold -0.6% at $1,332/oz; May Crude Oil +0.5% at $63.66/brl; May Copper -0.1% at $3.021/lb

The US-China Trade Tensions Continue To Be The Main Theme In The Markets

Market movers today

The US-China trade tensions continue to be the main theme in the markets . Markets calmed down yesterday and rebounded during the day as focus shifted from fears of a trade war to signs of negotiations. Yesterday we published an update looking at where we expect to go from here, see Research: Two scenarios for the US-China trade conflict , 4 April 2018. The scenario we believe most in is the one in which the US and China enter negotiations and things gradually calm down and we see a kind of 'grand bargain'. The second scenario is the one in which Trump strikes back at China's retaliation and we enter a trade war. So far there are no signs of this, though, and neither of the countries have any interest in a trade war that will damage both sides and has no winners. If we are right and we move into the first scenario, we may have seen the worst in the markets and could see more relief soon.

On the data front today we have a bunch of Euro releases: German factory orders, Euro retail sales and final Euro PMI service. We expect the figures to confirm an overall picture of decent but decelerating growth.

We also get UK PMI service, US jobless claims and US trade balance.

In Scandi Norwegian house prices are due as well as the credit indicator.

Selected market news

Stock markets saw a sharp rebound yesterday and the US market rallied into the close as focus shifted to the possibility of negotiations between the US and China. Donald Trump's new economic adviser Larry Kudlow replied yes to a question on whether the tariffs might never go into effect and later in the day said: 'I don't think it's a trade war. I think there will be intense negotiations on both sides. I think we're going to come to agreements', see Reuters . Commerce Secretary Wilbur Ross has also clearly signalled that the tariffs should be seen as part of a negotiation: 'Of course, in all negotiations there are ups and downs and we are likely to see some hiccups. But ultimately we believe an agreement will be found avoiding a trade war'.

Asian markets have taken up the tone from the US yesterday with a decent rally across equity markets, see Bloomberg . Bond yields have also rebounded as the safe-haven demand has faded.

Yesterday the US ISM non-manufacturing index fell to 58.8 in March , below consensus. This is still a healthy level, but it highlights what we see in a lot of data currently, that we have likely passed the peak in the global business cycle and will see a deceleration over the coming quarters. While we expect economic as well as profit growth to stay at a decent levels, we no longer have the tailwind to risk assets from an accelerating business cycle. Deceleration in economic momentum normally provides support for fixed income markets as we have witnessed in recent months.

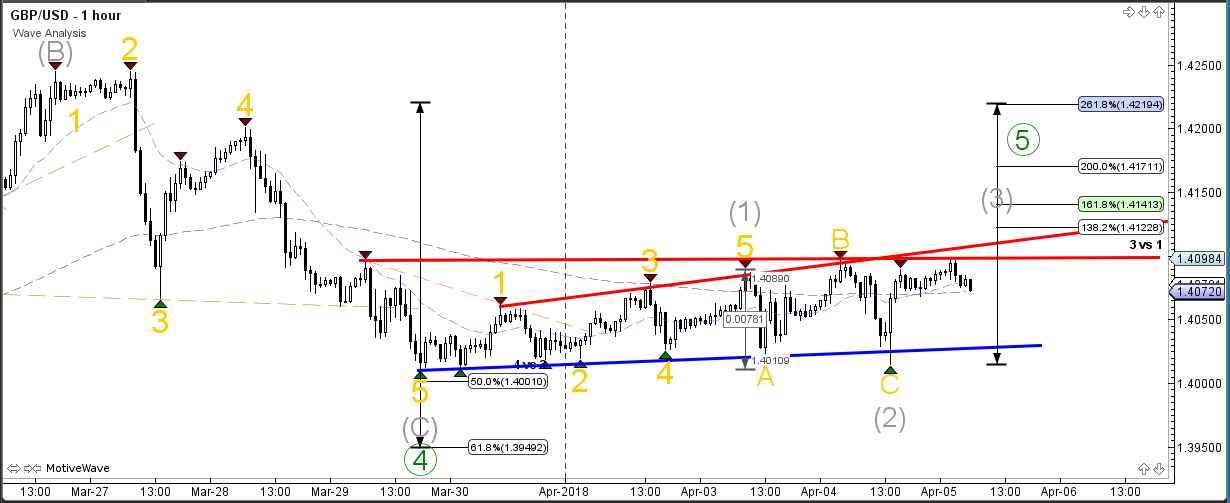

GBP/USD Lengthy Consolidation Zone Awaiting New Critical Breakout

The GBP/USDis moving sideways at the 50% Fibonacci level of potential wave 4 (green) retracement. The support and resistance level of this consolidation zone are key zones for a bullish or bearish breakout. A bearish break could indicate that the current range is a wave B or 2 and increases the chance of a bearish reversal whereas a bullish bounce could see price move up within the trend.

The GBP/USD wave pattern is fragile at this moment and will depend on the breakout direction above or below of the consolidation pattern. A break below the 50 and 61.8% Fibonacci level makes a wave 4 (green) unlikely. A bullish break, however, could perhaps start a larger bullish momentum as price might be building a wave 3 (green).