Sample Category Title

GBP/CHF resuming medium term up trend quietly as traders focus on trade war

NZD and AUD are trading among the strongest ones today, with the help of recovery in US stocks. While DOW did suffer at initial trading, there ain't no crash. CAD, however doesn't share the same fortune as markets are back in concern over NAFTA renegotiation. CHF follows as the second weakest one.

A quick glance at the action bias tables for each currency reveals that CHF is trading with rather broad based downside bias.

A quick glance at the action bias tables for each currency reveals that CHF is trading with rather broad based downside bias.

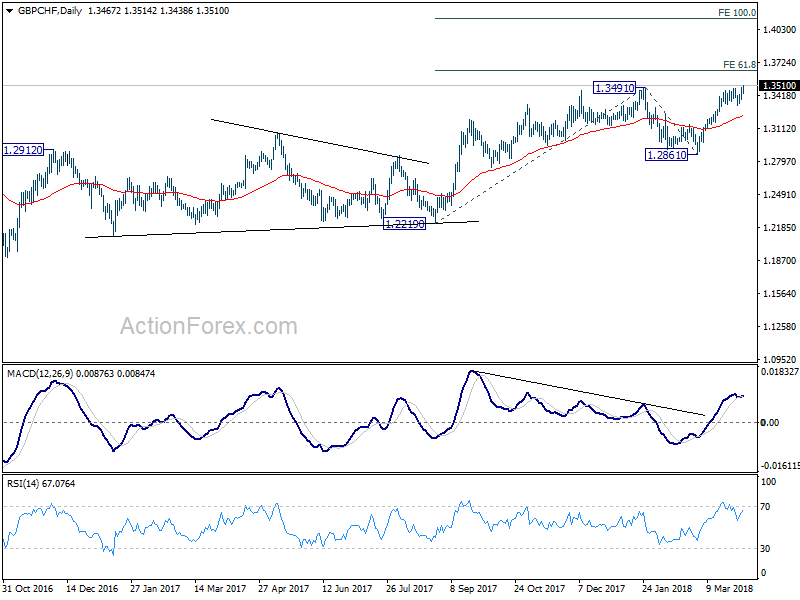

GBP/CHF is a clear example with upside Action Bias across time frames. The patterns suggests that it has just finished a near term consolidation and is ready for further rally.

GBP/CHF is a clear example with upside Action Bias across time frames. The patterns suggests that it has just finished a near term consolidation and is ready for further rally.

GBP/CHF has indeed taken out 1.3194 key near term resistance today and is resuming the medium term up trend. Next target will now be 61.8% projection of 1.2219 to 1.3419 from 1.2861 at 1.3647.

GBP/CHF has indeed taken out 1.3194 key near term resistance today and is resuming the medium term up trend. Next target will now be 61.8% projection of 1.2219 to 1.3419 from 1.2861 at 1.3647.

DOW lost 510 pts at initial trading, but quickly halved it on recovery

DOW opened sharply lower and dived to as low as 23523.16 in the first hour. That's 510 pts of decline. But it quickly found footing and recovered. At the time of writing, it's down only around -1.1%, with loss halved.

Technically it's, for now, holding on to 2336.029 key near term support. But rebound has been getting weaker and weaker. This is so far in-line with our view that current fall is the third leg of the corrective pattern from 26616.71.

Volatility aside, near term outlook will remain bearish as long as 24314.30 resistance holds. And a decisive break of 23360.29 support should be seen in the near term.

Volatility aside, near term outlook will remain bearish as long as 24314.30 resistance holds. And a decisive break of 23360.29 support should be seen in the near term.

For, we're seeing the fall from 26617 as correcting the up trend from 2016 low at 15450.56. Such correction would try to hit 38.2% retracement of 15450.56 to 26616.71 at 22351.24 before completion.

Yen Edges Lower, Japanese Household Spending Next

USD/JPY has posted losses in the Wednesday session, after posting gains on Tuesday. In the North American session, USD/JPY is trading at 106.25, down 0.33% on the day. On the release front, there are no Japanese events on the schedule. In the US, employment indicators kicked off with ADP Nonfarm Payrolls, and the news was good. The indicator defied expectations and rose in March, climbing to 241 thousand, well above the forecast of 208 thousand. On the services front, ISM Non-manufacturing PMI dropped to 58.8, shy of the estimate of 58.8 points. On Thursday, the US releases unemployment claims and Japan publishes a key consumer indicator, Household Spending.

The tariff spat between China and the US continues, and the growing possibility of a global trade war has the markets seeing red. The Chinese government has fired the latest salvo, announcing 25% tariffs on 106 American products, including soy beans, wheat and some motor vehicles. The value of these US exports amounts to some $50 billion – the same value as Chinese exports which have been slapped with tariffs by President Trump. This represents a significant raising of the stakes, and has the markets worried. China’s deputy finance minister has said that a trade war between the two sides would be a ‘lose-lose’, and few investors would disagree with his diagnosis. However, neither Trump nor Chinese President Xi Jinping has blinked so far, and the crisis shows no signs of being resolved anytime soon. As one US analyst wrote this week, “trade wars are easy to start but hard to stop.” The Japanese yen is a key safe-haven asset, and nervous investors could snap up the Japanese currency if there is no quick resolution to the tariff spat unleashed by US President Trump.

Japanese Prime Minister Shinzo Abe will meet with Prime Minister Trump later this month in Florida, and Japanese officials are bracing for what could be difficult trade talks. Trump signed a free-trade deal with South Korea in March, and the agreement included a side deal to prevent currency devaluation, and the US could demand similar provisions with the Abe government, which has adopted an ultra-accommodative monetary policy that has kept the yen at low levels. Trump may also demand a bilateral free-trade agreement between the two countries, rather than the multilateral approach favored by Tokyo.

Sunset Market Commentary

Markets:

The pace of China’s retaliatory measures against last night’s detailed list by the US administration of import tariffs against Chinese products took markets by surprise. China slapped 106 products with tariffs of up to 25%, matching the US’s $50bn package. An eye for an eye and a tooth for a tooth. The measures send US equity futures tumbling, registering losses to the tune of 2%. The spill-over to European stock markets amounts to about 1%. Commodity markets lost significant ground as well with investors fearing a backlash to global growth. The key driver during the remainder of today’s trading session will of course be stock market sentiment, with main indices fighting back after the official opening. Medium term, we eye the February low in the S&P 500 (2532). A move lower would steadily install a technical pattern of lower highs and lower lows and suggest and end to the bullish stock market, suggesting consolidation ahead.

FX markets again managed to withstand the new escalation in the US/Chinese trade conflict. The trade-weighted dollar overcame initial weakness and trades currently close to opening levels. EUR/USD spiked temporary above the 1.23 mark, but faces difficulties to stay north of that level. The Japanese yen is the only one who really profits from the safe haven status with USD/JPY currently around 106.25 compared to a 106.60 opening. Sterling reversed yesterday’s gains as it faced exactly opposite forces. Risk aversion instead of a risk-on climate and a very weak construction PMI instead of yesterday’s good manufacturing PMI. EUR/GBP rose from 0.8715 to 0.8740 currently.

Core bonds eked out relatively small gains given the new US stock market swoon. US Treasuries slightly outperformed German Bunds. The German yield curve bull flattens at the time of writing with yields 0.4 bps (2-yr) to 1.1 bp (30-yr) lower. US yields decline by 1 bp (30-yr) to 1.7 bps (5-yr). We argued before that equity weakness because of an escalation in the trade conflict shouldn’t necessarily result in lower yields via safe haven flows as China might consider a reallocation of its FX reserves away from US Treasuries. The discrepancy between strong US (labour) market data and disappointing EMU (inflation) data failed to trigger any significant market action on core bond or FX markets.

News Headlines:

China hit back quickly against the Trump administration's plans to slap tariffs on $50 bn in Chinese goods, retaliating with a list of similar duties on key US imports including soybeans, planes, cars, beef and chemicals. US Commerce Secretary Ross responded that he isn’t surprised by the Chinese reaction and predicted that both countries might end up negotiating. US President Trump tweeted that the US is not in a trade war with China.

The US ADP employment report showed a net job creation of 241k in March, beating 210k consensus, confirming ongoing strength on the US labour market and boding well for Friday’s payrolls. ADP upwardly revised the March outcome from 235k to 246k. The US non-manufacturing ISM remained strong in March, declining from 59.5 to 58.8.

The Eurozone unemployment rate fell as expected from 8.6% to 8.5% in February, the lowest level since December 2008. Labour market strength doesn’t really translate into upward wage/inflationary pressure though. The EMU core CPI stabilized at 1% Y/Y in March, printing below 1.1% consensus. The headline inflation figure rose from a downwardly revised 1.1% Y/Y to 1.4% Y/Y, mainly driven by a surge in food, alcohol and tobacco prices (2.2% Y/Y).

The UK construction PMI unexpectedly dropped below the 50 boom/bust mark in March. The decline from 51.4 to 47 was the sharpest since July 2016 and caused by a snowstorm that hit the UK in late February and early March.

ISM non-manufacturing composite dropped to 58.8 in March

ISM non-manufacturing composite dropped to 58.8 in March, down from 59.5 slightly below expectation of 59.0. Sub components are mixed with improvements seen in employment, suppliers deliveries prices, backlog of orders and imports. Deteriorations are seen in business activity, new orders, new export orders and inventory sentiment.

Here are some quotes from responents:

Here are some quotes from responents:

- "The unbelievable amount of market volatility in construction-related materials that started with lumber continues with the tariffs on steel and aluminum. Accurate, long-term planning has become incredibly difficult, as distributors that historically held costs for at least 30 days are now, in some cases, committing to only seven days, as prices can change drastically in that time." (Construction)

- "Interest rate hike [and] tariffs are likely to impact cost and price of goods and services." (Finance & Insurance)

- "Still feeling effects of plants in Puerto Rico being down, or not back to full capacity of IV solutions and plastic tubing sets." (Health Care & Social Assistance)

- "Business is stronger than forecast in March. Strategic sales continue to exceed forecast in March, as they have all quarter." (Management of Companies & Support Services)

- "Increased level of activity and pricing overall." (Mining)

- "As the first quarter end approaches, business outlook is steady, but not nearing growth forecast in Q4 2017." (Professional, Scientific & Technical Services)

- "Housing market [is] still strong, despite a shortage of construction workers." (Public Administration)

- "Q1 was positive, despite weather conditions that affected operations on the East Coast. The outlook remains positive going into Q2." (Transportation & Warehousing)

- "Overall, business has been slower than [the] previous quarter; however, we expect it to increase in the second quarter of 2018." (Wholesale Trade)

Fed Bullard: Not necessary for more rate hike

St. Louis Fed President James Bullard spoke in a speech to a meeting of the Arkansas Bankers Association meeting in Little Rock, Ark.

He said monetary policy, with federal funds rate at 1.50-1.75%, is now closer to "neutral" than in previous years. And it is "not necessary" to " raise the policy rate further in order to put downward pressure on inflation". And "inflation is already below target".

He also pointed to the "surprise" growth in the economy in 2017 and said it has "stalled so far in 2018". To him, Q1 GDP growth looks "uncertain". And markets are concerned with US trade policy as well as tech sector regulation.

Regarding the flattening of yield curve and the indication of recession, Bullard sounded much relaxed on it. He said, "it is possible that the nominal yield curve will invert sometime in the next year, but recently the 10-year yield has increased enough to keep pace with the FOMC's rate increases."

Below is St louis Fed's regarding the discussions. With a link to the presentation.

St. Louis Fed's Bullard Discusses the U.S. Economy Three Months into 2018

LITTLE ROCK, Ark. — Federal Reserve Bank of St. Louis President James Bullard discussed "The U.S. Economy Three Months into 2018" Wednesday at the Arkansas Bankers Association and Arkansas State Bank Department's Day with the Commissioner.

Reflecting on U.S. macroeconomic developments so far this year, Bullard discussed real GDP growth, inflation and the yield curve, as well as the current stance of monetary policy.

On growth, Bullard noted that global real GDP growth surprised to the upside during 2017, driving global financial market developments last year. "The effects of the surprise seem to have abated during the first months of 2018 in the face of uncertain first-quarter U.S. real GDP growth along with other factors," he said.

On inflation, Bullard noted that while it remains low, it is expected to move somewhat higher during 2018. Regarding other macroeconomic developments, he noted that yield curve inversion remains a possibility later this year, and that monetary policy is close to neutral today.

"Current monetary policy settings are close to neutral, which is appropriate for the current macroeconomic situation," he said.

Growth

Bullard noted that the U.S. and other large economies had better-than-expected growth in 2017, which fed into the profits of U.S. multinationals and helped U.S. equity prices rally last year. For instance, U.S. real GDP growth in 2017 was 0.4 percentage points higher than what the International Monetary Fund projected in October 2016.

However, he explained, the effects from the surprise in growth have stalled this year. He cited the following: The growth rate of U.S. real GDP looks uncertain in the first quarter, possibly due to residual seasonal effects; markets are trying to discern the direction of U.S. trade policy; U.S. interest rates are higher; and markets are contemplating possible tech sector regulation.

Inflation

Turning to the low inflation readings in 2017, Bullard explained why they were so surprising. He noted that they occurred against a backdrop of relatively good labor market performance and a still historically low policy rate (i.e., the federal funds rate target). However, he said, "Special factors are expected to drop out of the year-over-year comparisons soon, likely suggesting that inflation is somewhat closer to target."

He also discussed inflation expectations, which may give a signal of future inflation. He noted that market-based measures of inflation compensation have increased recently. "The measures today are closer to being in line with the FOMC's 2 percent inflation target, but remain a bit low," he said.

Yield curve

Bullard then discussed the flattening of the U.S. nominal yield curve since 2014, which is the result of short-term rates rising while long-term rates have remained relatively stable. To quantify the flattening, he noted that the spread between the 10-year and one-year Treasury yields declined from about 300 basis points at the beginning of 2014 to 70 basis points during the week of March 28.

"It is possible that the nominal yield curve will invert sometime in the next year, but recently the 10-year yield has increased enough to keep pace with the FOMC's rate increases," he said.

Monetary policy

Turning to the stance of U.S. monetary policy, Bullard noted that the FOMC has begun to gradually reduce the size of the Fed's balance sheet. In addition, the range for the policy rate has been increased gradually and is currently 1.50 to 1.75 percent.

He also noted that current estimates of the neutral real rate (or r*) are near zero, and that core PCE inflation (measured as the year-over-year percentage change in the core personal consumption expenditures price index) is 1.6 percent. Therefore, the current policy rate setting minus core PCE inflation is near r*, which suggests that "the current policy setting is closer to neutral than in previous years," Bullard said.

He explained that the neutral setting for the policy rate puts neither upward nor downward pressure on inflation, given everything else that is occurring in the economy. "This is appropriate for the current situation, in which inflation is not far below target and is expected to rise," he said, adding that "it is not necessary in this circumstance to raise the policy rate further in order to put downward pressure on inflation, since inflation is already below target."

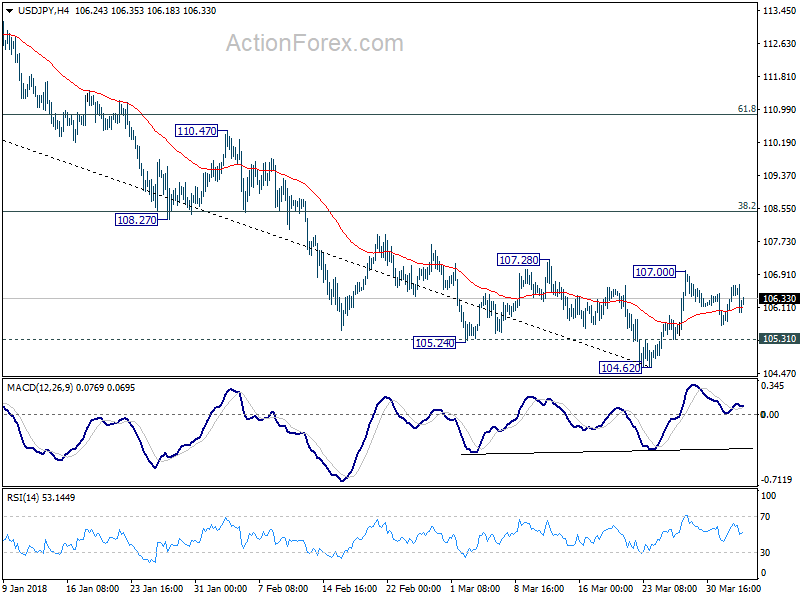

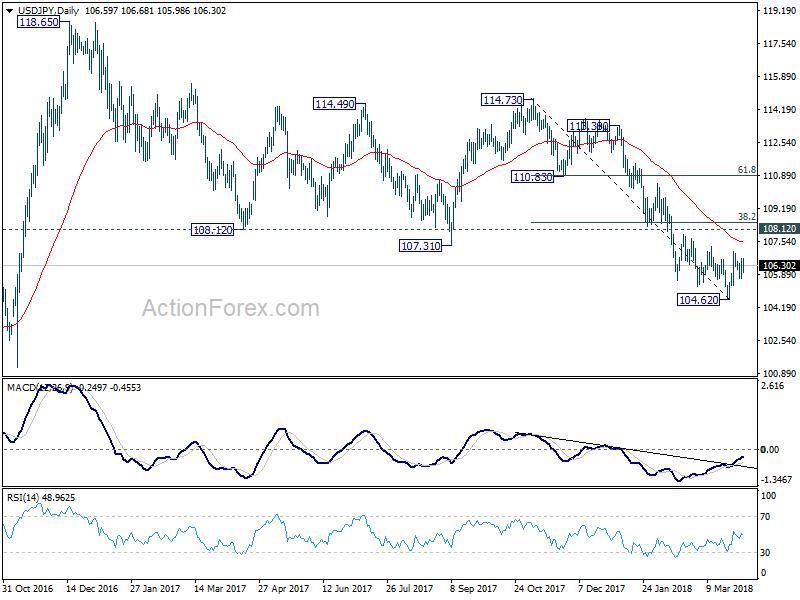

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.98; (P) 106.31; (R1) 106.94; More...

Intraday bias in USD/JPY stays neutral first. With 105.31 minor support intact, further rise is mildly in favor. Above 107.00 will target 38.2% retracement of 114.73 to 104.62 at 108.48. At this point, there is no confirmation of trend reversal yet. Hence, we'll look at the reaction from 108.48 (which is close to 108.12 too) to assess the chance. On the downside, below 105.31 minor support will indicate that the rebound is completed and turn bias back to the downside for 104.62 and below.

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

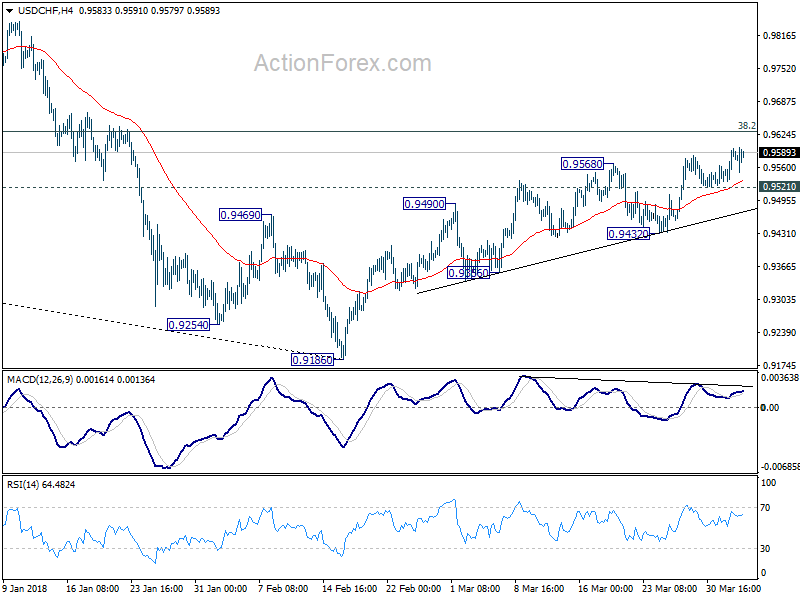

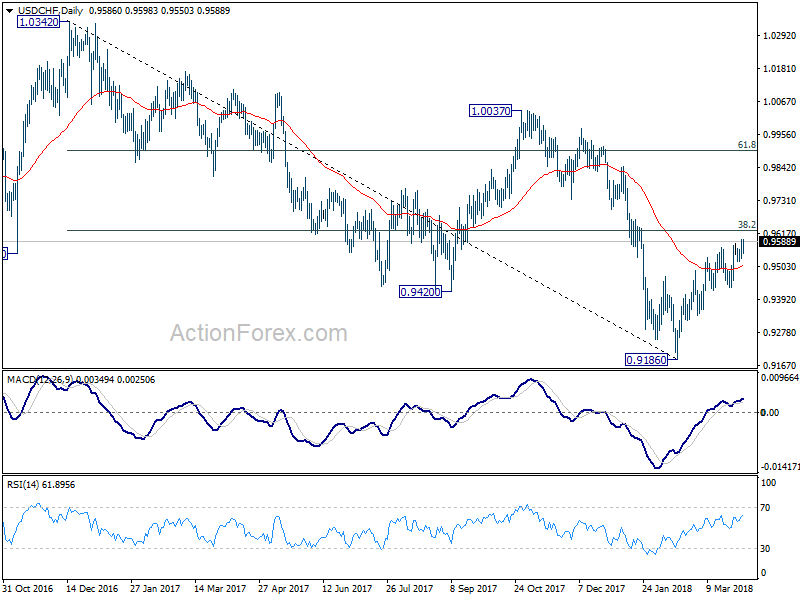

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9547; (P) 0.9572; (R1) 0.9611; More...

USD/CHF's corrective rebound from 0.9186 might extend higher. Still, we'd be cautious on strong resistance from 0.9626 key fibonacci level to limit upside. On the downside, below 0.9521 will turn intraday bias back to the downside for 0.9432 support. Break there will indicate near term reversal and completion of rebound from 0.9186. However, sustained break of 0.9626 will be another evidence of larger reversal. In this case, further rise would be seen to next fibonacci level at 0.9900.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

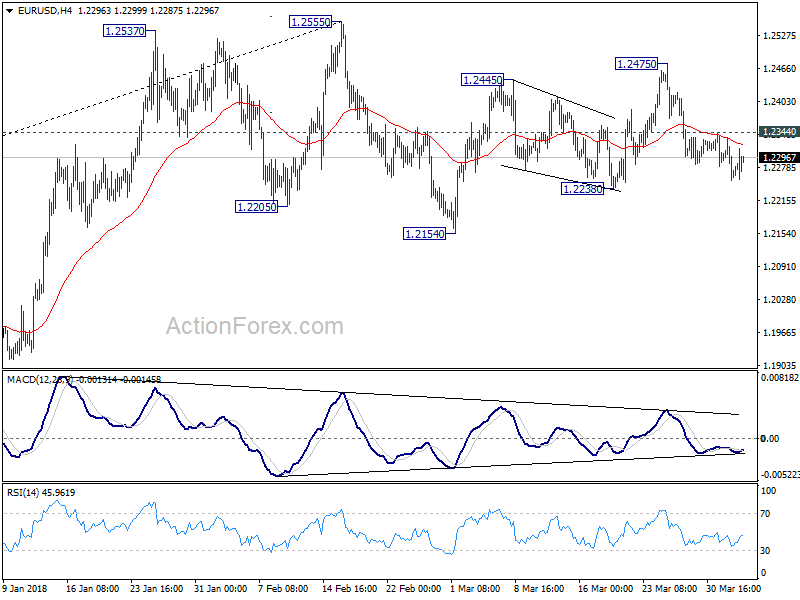

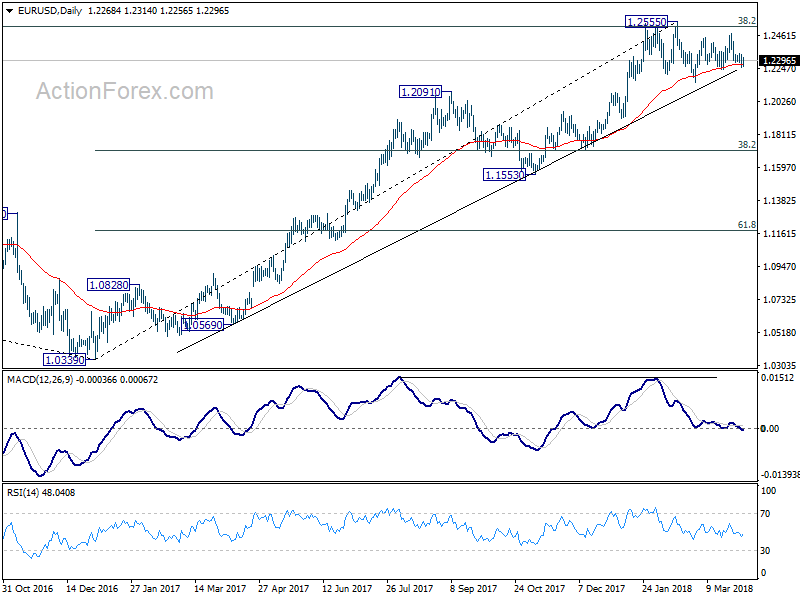

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2236; (P) 1.2285 (R1) 1.2318; More....

No change in EUR/USD's outlook. With 1.2344 minor resistance intact, deeper fall should be seen to 1.2238 first. Break will target 1.2154 and below. Such development would confirm the rejection by 1.2516 key fibonacci resistance and pave the way to 38.2% retracement of 1.0339 to 1.2555 at 1.1708. However, break of 1.2344 minor resistance will dampen this bearish case and turn bias back to the upside for 1.2475 resistance instead.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

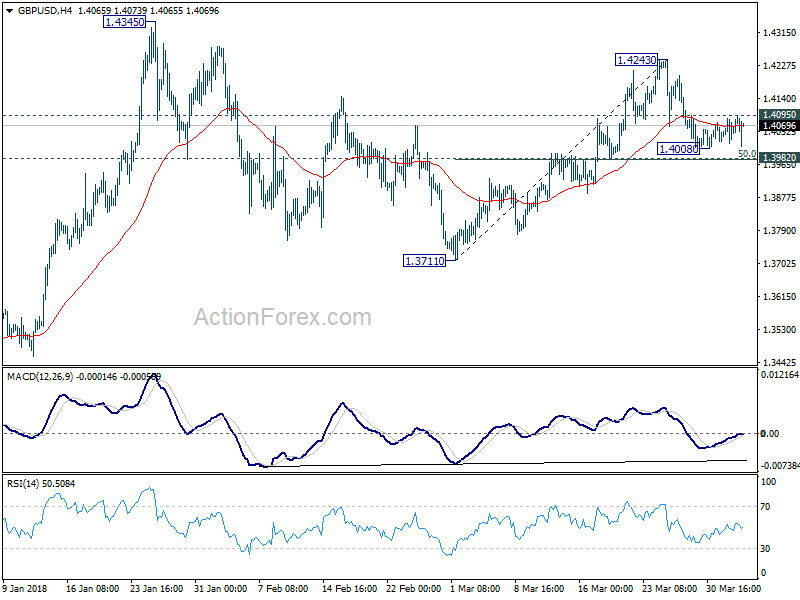

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4023; (P) 1.4056; (R1) 1.4091; More....

Much volatility is seen in GBP/USD today but it's, after all, bounded in tight range above 1.4008 temporary low. Intraday bias stays neutral first. On the downside, firm break of 1.3982 support will indicate completion of the rise from 1.3711. In that case, intraday bias will be turned back to the downside for retesting 1.3711. Nonetheless, strong rebound from 1.3982, followed by break of 1.4095 minor resistance will turn bias to the upside for 1.4243. Break will resume the rally from 1.3711 for 1.4345 high first.

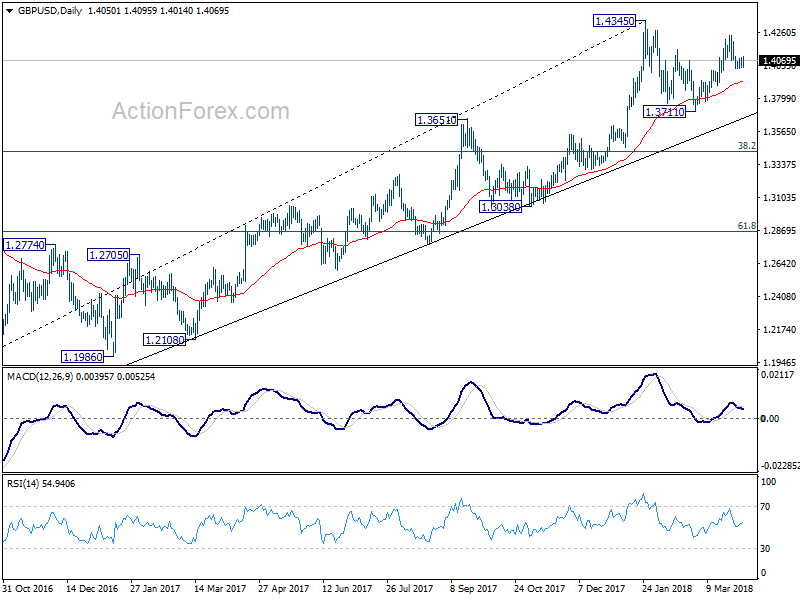

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.