Sample Category Title

Risk Aversion Returns As China Announces Tariffs

- Dow Futures Slip More Than 500 Points Ahead of the Open;

- Trade Wars May Not Be as Easy to Win as Trump Promised;

- US Employment, Services Surveys and Fed Speakers Still to Come.

Dow Futures Slip More Than 500 Points Ahead of the Open

We’re back in risk aversion mode on Wednesday, after Beijing announced new tariffs in retaliation to those planned by the White House in a direct attack on Chinese exports.

With still a few hours to go until the open on Wall Street, Dow futures are posting losses of more than 500 points which makes for a rather bleak start to trading. The losses more than wipe out Tuesday’s rebound and set us on course for another worrying session driven by fears that a trade war between the world’s two largest economies is heating up with neither side showing any sign of backing down.

The Dow has found support around 23,350 the last two times we’ve traded at these levels so this could be critical again today, with a break below here potentially signalling more severe losses ahead. This would require a drop of 3% or more today so may not happen straight away but the way markets are trading prior to the open, it’s not looking good.

Trade Wars May Not Be as Easy to Win as Trump Promised

The Chinese tariffs will target $50 billion of US products including soy beans, cars and whisky, a sign that Beijing is up to the fight and that if US President Donald Trump wants to prove that trade wars are in fact easy to win, he’ll have to back it up with actions. Ultimately, the response we’re seeing in the markets suggest investors are not on board with the actions being taken by both countries and see them as a real threat to what has been a good period of global growth.

US 10-year Treasury yields are edging lower again, with investors potentially looking to longer term bonds as a safe haven play in these markets. Naturally, this will likely trigger more concerns about what a flattening of the yield curve means and whether it’s a reflection of increasing recession worries. I don’t think this is the case currently, with low inflation and safe haven demand, among other things suppressing longer term yields.

US Employment, Services Surveys and Fed Speakers Still to Come

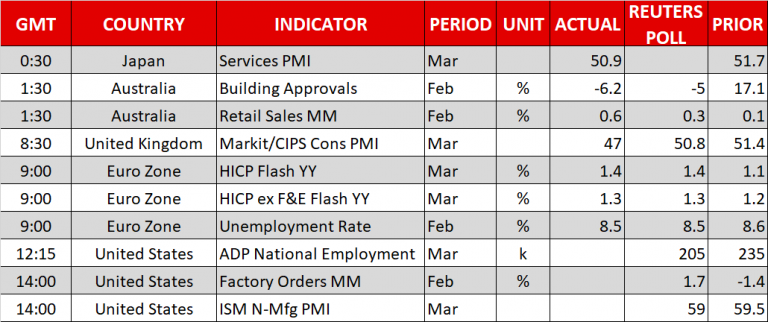

There is plenty of economic data being released throughout the day on Wednesday, although naturally this is being overshadowed by the latest tariff announcement. While not the most accurate indicator of job growth – as measured by Friday’s NFP – the ADP non-farm employment number is always looked to for an indication of how employers hired last month, with it being released two days before the official reading. Although, as has become the case, the earnings numbers are perceived to be of more importance now that job growth, with unemployment having fallen close to 4% and inflation lacking.

Also to come today we’ll get services and non-manufacturing surveys, factory orders and crude oil inventories. We’ll also hear from Loretta Mester – an FOMC voter this year and typically a hawk – and James Bullard – an FOMC voter next year and typically one of the more dovish members of the committee.

GBPUSD – Key Support Zone Under Pressure As Pound Eases After Downbeat UK Data

Cable fell to session low at 1.4041, unaffected by turmoil in the markets on China’s retaliation on US tariffs plan but came under pressure on weak UK construction data (Construction PMI fell to 47 in Mar the lowest since July 2016 vs 50.9 f/c and 51.4 in Feb).

Fresh weakness after recovery attempts were repeatedly capped by 10SMA, which turn s lower today, makes the downside vulnerable.

Initial support at 1.4020 (rising 20SMA) came under pressure, with risk of testing key support zone between 1.4010 (higher base), psychological 1.40 support (also top of thinning daily cloud) and 1.3090 (55SMA), loss of which would generate stronger bearish signal.

Res: 1.4065, 1.4099, 1.4126, 1.4154

Sup: 1.4020, 1.4010, 1.3990, 1.3978

Yen Rallies As China Unleashes New Tariffs On US

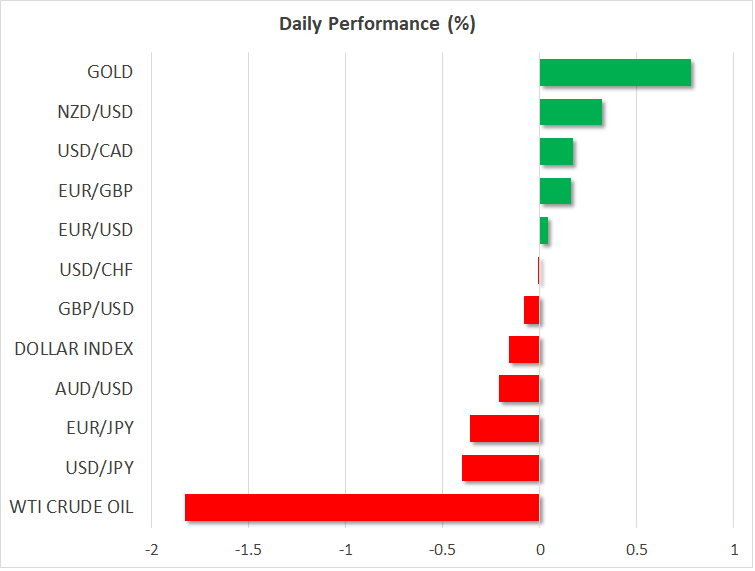

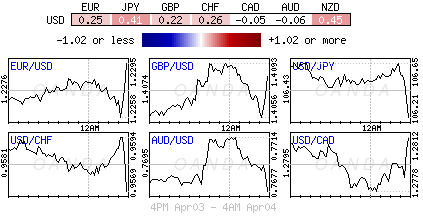

FOREX: The US dollar index – which measures the greenback’s performance against six major currencies – dipped by 0.17% on Wednesday and safe-havens jumped once again after China took further trade retaliatory measures against the US today, imposing a 25% import tariff on key US products. Dollar/yen dropped to a session low of 105.98 before it inched up to 106.09, losing 0.43% on the day. Euro/dollar was trading higher by 0.08% during today’s European session and was last seen slightly below the 1.2300 psychological level. Eurozone’s headline CPI released earlier today matched expectations, rising from 1.1% y/y to 1.4% y/y in February. The core measure, though, remained unchanged at 1.0%, below the 1.1% forecast. Pound/dollar slipped by 0.04% to 1.4050 and was on track to post the fourth green day in a row. Aussie/dollar fell by 0.20% to 0.7668, while kiwi/dollar moved higher by 0.37% to 0.7284. Dollar/loonie pared some of Tuesday’s losses after it touched a more than a one-month low of 1.2774 today, being up by 0.19%.

STOCKS: European stocks dipped sharply on Wednesday. The benchmark European STOXX 600 tumbled by 0.78% for the second day in a row. The blue-chip Euro STOXX 50 was down by 0.87%, while the German DAX 30 tumbled by 1.23%, the largest fall in more than a week. The French CAC 40 dived by 0.59%, the Spanish IBEX 35 slipped by 0.82% and the British FTSE 100 declined by 0.41%. In Asia, Japan’s Nikkei 225 and Topix edged marginally higher by 0.13% and 0.14% respectively. In the US, even though the S&P, Dow Jones and the Nasdaq all surged yesterday, futures tracking these indices are currently in the red, pointing to a lower open today.

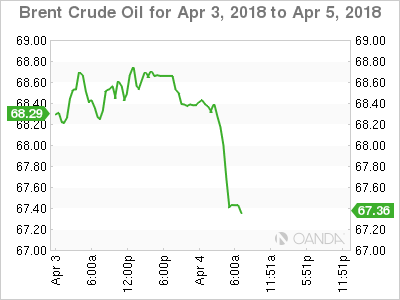

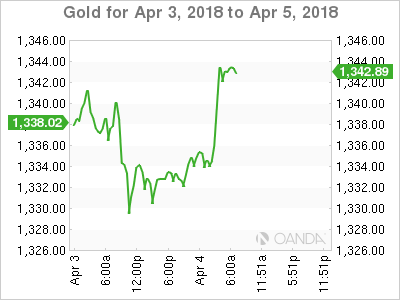

COMMODITIES: Oil prices slipped on Wednesday as the trade dispute between the US and China escalated, while investors were also concerned about rising US oil production. WTI crude oil plummeted by 1.83%, reaching a new two-week low of $62.35/barrel, while Brent crude plunged by 1.73% below $67.00/barrel. In precious metals, gold prices rebounded from one-week lows touched today, rising by 0.79% to $1,343.6/ounce.

Day ahead: US ADP employment report, factory orders eyed; trade risks intensify

Later in the day, US data will be in focus, with investors keeping a close eye on the ADP national employment report (1215 GMT) which tends to give an early indication of employment trends in the US ahead of the government’s nonfarm payrolls report (NFP) due on Friday. Particularly, the print is expected to show that positions in the private sector grew by 205,000 in March compared to 235,000 seen in February.

Separately, US factory orders due at 1400 GMT are anticipated to return to growth in February, rising by 1.7% in monthly terms after falling by 1.4% in the previous month, while at the same time, the US non-manufacturing PMI for the month of March is said to slow down by 0.5 points to 59.0. Note that, on Monday the ISM manufacturing PMI missed forecasts, retreating from 60.8 to 59.3.

In energy markets, the Energy Information Administration will publish its report on US oil inventories for the week ending March 30, with analysts expecting crude oil inventories to grow for the second straight week. Yesterday, the American Petroleum Institute indicated a drop in US oil stocks, surprising analysts who believed that the measure will continue to increase.

As for today’s, public appearances, St. Louis Fed President James Bullard (non-voter) will be making comments at 1345 GMT before a speech by FOMC board member and Cleveland Fed President Loretta Mester at 1500 GMT.

Trade headlines during the day will be of greater interest as China and the US continue the tit-for-tat game bringing more headaches to investors. A few hours ago, China decided to levy a 25% import tariff on 106 US products amounting to $50 billion per year – the products include soybeans, automobiles, and chemicals. This came just a day after the US unveiled a set of tariffs on Chinese imports.

U.S At War: China Retaliates To Trumps Tariffs

Sino-U.S Trade fears

Investors trade fears are back with a bang as trade tension is again the markets central focus, with Asian and European equity bourses turning lower amid an escalation of protectionist rhetoric and action between China and the U.S.

Ahead of the U.S open, investors have piled into safe-haven assets (¥, Au, and Ag) as China unveiled retaliatory measures against U.S tariffs.

Beijing plans to levy a +25% tariff on soybeans, auto, and chemical products among +106 products.

Stateside, equities will open deep in the red, down close to -2%, while the ‘big’ dollar drifts with Treasury prices.

On Tap: Up next is U.S ADP non-farm employment change at 08:15 am EDT and U.S ISM non-manufacturing PMI at 10:00 am EDT and DoE crude oil inventories at 10:30 am EDT.

1. Stocks see red on retaliation to tariffs

Ahead of China’s tariff retaliation announcement, Japanese stocks edged higher on Wednesday in choppy trade as some automakers rose after they reported strong U.S sales numbers, helping to offset the impact of a stronger yen (¥106.19). The Nikkei added +0.1%, while the broader Topix rallied just shy of +0.1%.

Down-under, the Aussies S&P/ASX 200 added +0.2% on stronger than expected retail sales data (March +0.6% vs. +0.3% m/m), while in S. Korea, stocks hit a week’s low with the Kospi down -1.4%. Tech giant, Samsung, dropped -2.5% to hit a fresh four-week low.

In China, stocks, which started steadily, ended, lower with benchmarks in Shanghai and Shenzhen down -0.2% and -0.6% respectively after Beijing said it would levy tariffs on soybeans, autos and chemical products.

In Hong-Kong, the Hang Seng declined late in the session and was last down -1.8% at a seven-week low.

In Europe, regional indices trade lower across the board tracking sharp declines in U.S futures as China’s levies reciprocal tariffs on U.S goods totaling +$50B.

U.S stocks are set to open deep in the ‘red’ (-2%)

Indices: Stoxx600 -0.7% at 366.4, FTSE -0.5% at 6998, DAX -1.2% at 11859, CAC-40 -0.6% at 5123, IBEX-35 -0.8% at 9480, FTSE MIB -0.8% at 22336, SMI -0.9% at 8558, S&P 500 Futures -2%

2. Oil inches lower on U.S crude stock build, gold higher

Oil prices have slipped a tad on market expectations for a build in U.S crude inventories. However, Russian comments on prospects for stepping up cooperation with OPEC to coordinate output cuts broke steeper declines.

Brent crude have eased to +$67.94 per barrel, down -18c, or -0.26%, after it rallied +0.7% yesterday. U.S WTI crude futures were at +$63.36 a barrel, down -15c, or -0.24%, from Tuesday’s close.

Investors are expected to take their cues from this morning’s DoE data at 10:30 am EDT. Market consensus is looking for a U.S crude inventory build for the second straight week, while refined product stockpiles are forecasted to have declined last week.

Earlier this morning, Russian Energy Minister Alexander Novak said that a joint organization between OPEC and non-OPEC countries may be set up after the current deal on production cuts expires at the end of this year.

Note: Russia’s oil output rose last month to +10.97m bpd, up from +10.95m bpd in February.

The markets trade risk-off nature has pushed gold prices higher ahead of the open stateside. Spot gold has climbed +0.2% to +$1,336.04 an ounce.

3. Sovereign yields mixed results

U.S. Treasury yields initially rallied overnight as stock markets firmed and as investors looked ahead to Friday’s closely watched U.S employment report for March. However, news that China would retaliate against Trumps tariffs initiative has changed the landscape with investors applying ‘risk-off’ trading strategies and buying short-term product.

The yield on 10-year Treasuries declined -2 bps to +2.77%. In Germany, the 10-year Bund yield has dipped -1 bps to +0.50%, the lowest in 12-weeks, while in the U.K, the 10-year Gilt yield fell -1 bps to +1.359%, the lowest in almost 11-weeks.

In Japan, longer-dated JGB’s prices gained overnight on steady investor demand for debt at the start of the new domestic fiscal year. Super-long (30-years+) JGB yields fell to a new 16-month low amid demand from life insurers and pension funds who were purchasing product to balance their portfolios at the start of the fiscal year, which began April 1. The 30-year yield fell -0.5%.

4. Dollar rallies vs. EM pairs

The ‘big’ dollar has added to its earlier gains versus currencies of big Asian exporting nations after China unveiled plans to levy tariffs on several U.S. products.

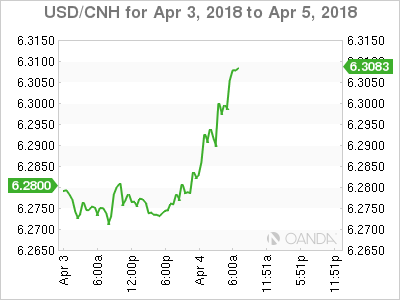

USD has rallied as much as +0.8% vs. KRW following the move compared with its earlier gain of +0.4%. The dollar is up as much as +0.3% vs. CNH vs. its earlier advance of +0.2%. Meanwhile, the yen (¥106.13) – a safe haven asset – strengthened outright. For the yen, ¥105.50 remains a key level on the dollar downside.

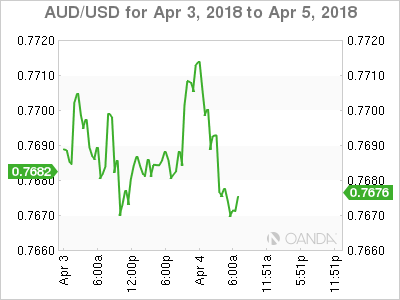

AUD too could not escape China’s retaliatory trade measures despite Aussie March retail sales beating expectations (+0.6% vs. +0.3%). The AUD is down -0.4% vs. EUR and -0.6% vs. JPY after China’s move to impose a tariff on 106 U.S products. AUD to remain under pressure as risk-off takes a firmer grip.

In Europe, EUR/USD began the session below the psychological €1.23 level as dealers noted that the EMU data had been disappointing recently. However, the escalation of trade tension is now weighing somewhat upon the greenback vs. G7 pairs. EUR gains were slightly eroded after the E.U flash CPI (see below) came in-line, while core registered a miss.

GBP/USD (£1.4053) continues to lag in price action as March construction PMI contracted (see below) for the first time in six-months.

5. E.U inflation ticks up, U.K construction PMI falls

Data this morning showed that Eurozone consumer prices picked up in March for the first time in four-months. The headline print should reinforce the ECB’s belief that they are on track to meet its inflation target over coming years.

Consumer prices for March were +1.4% higher than a year earlier, an increase from the +1.1% rate of inflation recorded in February. The less volatile core measure of inflation is expected to record a slower, but more encouraging climb. The measure has not been higher than +1.2% over the last five-years – the core rate of inflation was unchanged at +1.0% in March.

Note: Analysts expect today’s headline print to mark the start of a steady climb higher over coming months, and inflation may touch the ECB’s target later this year.

U.K construction PMI falls sharply

U.K data this morning showed that business activity in the U.K.’s construction sector dropped in March following five-months of marginal growth.

IHS Markit construction PMI fell to 47.0 in March, down from 51.4 a month earlier.

Digging deeper, the fastest pace decline in two-years was driven by the sharpest reduction in civil-engineering activity for five-years and a renewed fall in commercial work.

DAX Slide Continues As China Fires Back At Trump

The DAX index has posted strong losses in the Wednesday session. Currently, the DAX is trading at 11,813 points, down 1.57% on the day. On the release front, it’s another busy day. In the eurozone, inflation indicators were within expectations. CPI Flash Estimate rose to 1.4%, matching the forecast. Core CPI Flash Estimate remained unchanged at 1.0%, just shy of the estimate of 1.1%. Eurozone unemployment ticked lower to 8.5%, matching the forecast. On Thursday, Germany releases Factory Orders and Final Services PMI, and the eurozone will publish PPI and Retail Sales.

With the eurozone economy continuing to perform well, and unemployment levels have been steadily falling. The rate dipped to 8.5% in February, compared to 9.5% in February 2017. This marked the lowest unemployment rate since December 2008. Inflation levels remain slightly above 1 percent, well below the ECB target of around 2 percent. This means that the ECB is unlikely to change its monetary policy, although Germany wants to see a tighter policy, which would be better suited to its robust economy. In January, the ECB tapered its stimulus program, from EUR 60 billion to 30 billion per month. The stimulus is scheduled to wind up in September, and it remains an open question as to whether Mario Draghi will extend the scheme. If the eurozone economy remains on track and inflation moves higher, there is a strong likelihood that the ECB will adopt a policy of normalization, after years of stimulus.

After a break for Easter, European stock markets are seeing red over fears of a trade war between the US and China. The Chinese government fired the latest salvo on Wednesday. China announced 25% tariffs on 106 American products, including soy beans, wheat, aircraft and motor vehicles. The value of these US exports amounts to some $50 billion – the same value as Chinese exports which have been slapped with tariffs by President Trump. This represents a significant escalation of the tariff battle, and understandably has the markets worried. China’s deputy finance minister has said that a trade war between the two sides would be a ‘lose-lose’, and few investors would disagree with his diagnosis. However, neither Trump nor Chinese President Xi Jinping has blinked so far, and the crisis shows no signs of being resolved anytime soon. As one US analyst wrote this week, “trade wars are easy to start but hard to stop.” If the trade dispute drags on, traders should be prepared for the market’s downward spiral to continue.

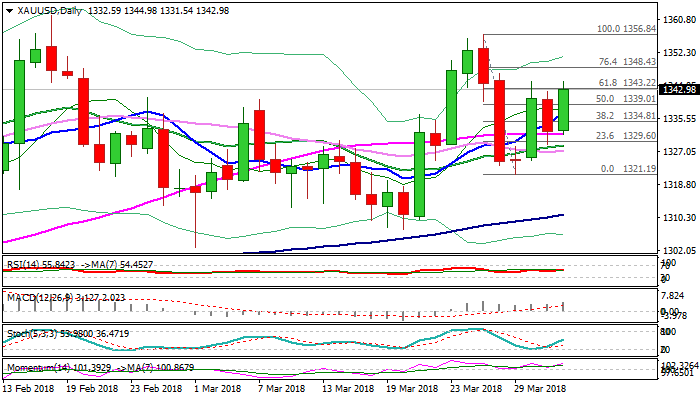

Spot Gold Rallies Strongly On Fresh Safe Haven Demand

Gold price surged on Wednesday on renewed safe haven demand after China announced tariffs on imported US goods, which shook the markets and increased uncertainty.

The yellow metal peaked at $1344, retesting Monday's high, as fresh bullish acceleration emerged above daily cloud and probed again above next pivotal barrier at #1343 (Fibo 61.8% of $1356/$1321 fall).

Bulls need close above the latter (after initial attempt on Monday failed) to confirm bullish continuation of recovery leg from $1321 (29 Mar low).

Daily MA's returned to full bullish configuration, with fresh bullish momentum building and being supportive for further advance.

Broken daily cloud top ($1337) is expected to keep the downside protected.

Res: 1344, 1348, 1351, 1356

Sup: 1339, 1337, 1334, 1331

CRUDE OIL Testing Support At 62.33

Crude oil is falling from 63.86 high, approaching hourly support at 62.33 (23/02/2018 low). The bullish pattern started in November 2017 is weakened. Silver is currently contained between hourly support and resistance at 62.33 (23/02/2018 low) and 66.66 (25/01/2018 high). The technical structure suggests short-term decrease.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

SILVER Rising

Silver is starting a recovery phase, bouncing off from 16.36 low and rising along the 16.55 range. Silver is contained between hourly support and resistance given at 16.03 (18/12/2017 low) and 16.98 (15/02/2018 high). The short-term technical structure suggests upward moves.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. The pair is trading below its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Approaching Resistance At 1349

Gold is bullish trend continues, bouncing off from 1329 low and currently trading above 1340. Expected to approach the 1345 range. Hourly support and resistance are given at 1318 (14/02/2018 low) and 1349 (30/01/2018 high) The technical structure suggests short-term increase.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1'392 (17/03/2014) is required to confirm it. A major support can be found at 1'045 (05/02/2010 low).

BITCOIN Continued Bearish Consolidation

Bitcoin continues its bearish consolidation, trading along 7300. Bitcoin bearish pattern started in March 2018 continues. The pair is contained between hourly support and resistance given at 6306 (13/11/2017 low) and 10232 (01/02/2018 high). The technical structure suggests short-term sideways trading moves.

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 7'000 - 12'000 in 2018. Bitcoin is trading below its 200 DMA (7500 range).