Sample Category Title

Fed’s Ideal Inflation Measure Rises, Claims at 45 Year Low

The personal consumption expenditures price index rose +1.8% in February from a year earlier, an increase last matched 12-months ago.

The rise in annual inflation, which comes after the inflation rate held at 1.4% for several months last summer, is the latest sign of strengthening inflation pressures that could encourage the Fed to continue raising interest rates this year.

The core-version (ex-food and energy) also strengthened, increasing +1.6% y/y.

Despite evidence of firming inflation stateside, the headline PCE price index remains below the Fed’s +2% target for annual inflation.

U.S jobless claims decline to its lowest level in 45-years

U.S filings for unemployment benefits unexpectedly fell last week to the lowest level since January 1973, further evidence that the labor market remains tight, Labor Department figures showed Thursday.

Highlights of Jobless Claims (Week ended March 24)

- Jobless claims decreased by -12k to +215k vs. +230k (e)

- Continuing claims rose by +35k to +1.87m in week ended March 17

- Four-week average of initial claims fell to +224.5k from the prior week’s +225k.

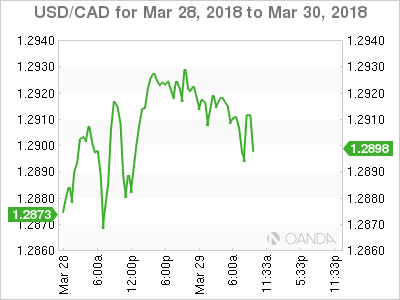

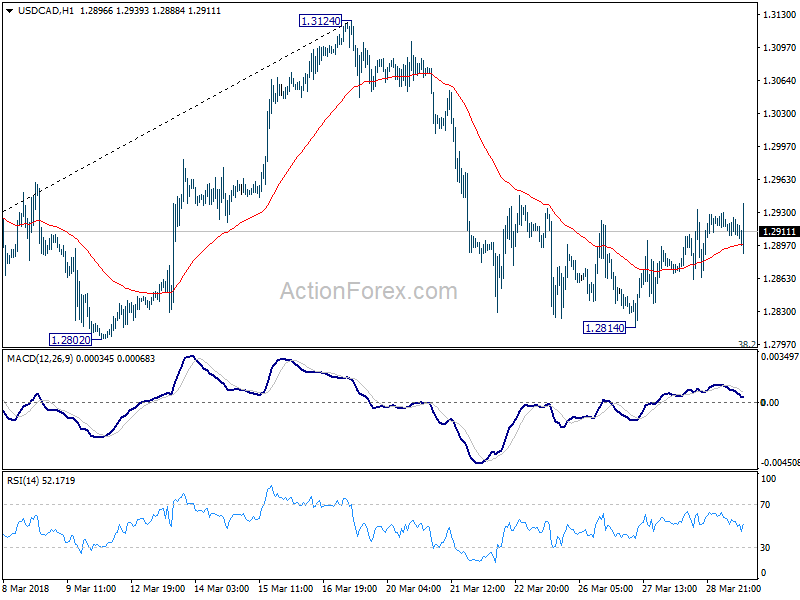

US jobless claims dropped to lowest since 1973, Canada GDP missed, USDCAD yawns

Canadian data are generally disappointingly. GDP contracted -0.1% mom in January versus expectation of 0.1% mom. IPPI rose 0.1% mom in February versus expectation of 0.4% mom. RMPI dropped -0.3% mom versus expectation of 2.8% mom rise.

US personal income rose 0.5% in February, spending rose 0.2% and both met expectations. Headline CPI accelerated to 1.8% yoy while core PCE also accelerated to 1.6% yoy.

Initial jobless claims dropped -12k to 215k in the weekended March 254. That's notably below expectation of 231k. That's also the lowest level since January 1973.

Four week moving average of initial claims dropped 0.5k to 224.5k.

Continuing claims rose 35k to 1.87m in the weekended March 17.

There's a bit of spikes on both direction after the releases. But that's it as USD/CAD quickly settle back into today's tight range.

Canadian Dollar Steady Ahead of GDP

The Canadian dollar continues to trade quietly. In the Wednesday session, USD/CAD is trading at 1.2905, down 0.14% on the day. On the release front, Canada releases the monthly GDP report and the Raw Materials Price Index. There are a host of key indicators in the US, led by unemployment claims and consumer confidence. The markets are expecting unemployment claims to tick higher to 230 thousand, while UoM Consumer Sentiment is forecast to rise to 131.2 points.

The US economy continues to show strong expansion. Revised GDP for the third quarter came in at 2.9%, beating the estimate of 2.7%. This reading was revised upwards from the initial GDP estimate of 2.5%. Fourth quarter growth, although solid, could not keep up with a superb third quarter, which posted a gain of 3.2%. As for 2018, first quarter growth is expected to soften to 1.8%, but there is still a strong chance that the economy could hit 3% growth this year, as promised by US President Trump. The catalysts for such a rosy prediction are the massive tax cut and higher government spending. Where does this leave the Federal Reserve, which raised interest rates last week? Currently, the Fed is projecting to more rate hikes this year, but if the economy remains strong and inflation levels move closer to the Fed target of 2%, we could see four rate increases in 2018.

Negotiations over the NAFTA agreement continue, and positive statements from US negotiators have raised hopes that a new agreement will be reached between Canada, Mexico and the US. A key sticking point has been a US demand to increase the US content in vehicles made in NAFTA members, but the Trump administration has apparently backed down on this requirement. The gloomy air around the talks has improved, and there is cautious optimism that the sides can hammer out a new agreement in the next few weeks.

ECB Knot: Market expectations and ECB policy actions converged into a “sweet spot”

ECB Governing Council member, Dutch central bank Governor Klaas Knot talked about monetary policy as he presented his bank's annual report in Amsterdam today. He said:

- "The top priority is to normalize monetary policy and strengthen the economic and monetary union,"

- "This is now a widely-shared realization, certainly also in the financial markets."

- "If you look at the market expectations of our policy action, I would say they have more or less converged at what I call a sweet spot,"

- "There is a fair degree of consensus around these expectations."

- "I would say the likelihood of us erring on the side of being too cautious is a bit larger than for us being too bold,"

- "All in all, undoing these unorthodox, unconventional instruments could easily last for most of a decade."

Regarding trade relationship with the US, he said:

- "The question is if Europe will come with countermeasures which could make us slip into a trade war,"

- "But don't be mistaken, if the U.S. were to implement trade restrictions on say steel, it will be the American consumer paying the price."

GBPUSD – Remains Vulnerable On Further Pullbacks

GBPUSD - The pair weakened further on Wednesday opening for more declines in the days ahead. Support lies at the 1.4050 level where a break will turn attention to the 1.4000 level. Further down, support lies at the 1.3950 level. Below here will set the stage for more weakness towards the 1.3900 level. Conversely, resistance stands at the 1.4100 levels with a turn above here allowing more strength to build up towards the 1.4150 level. Further out, resistance resides at the 1.4200 level followed by the 1.4250 level. On the whole, GBPUSD remains biased to downside on correction.

Various German Individual States Mar CPI Data Come In Below Expectations

Notes/Observations

- German Economy continued to hum along as Mar Unemployment Rate hit a fresh record low of 5.3%

- Various German individual States Mar CPI data come in below expectations of the overall composite figure (due out later today)

- UK Q4 Final GDP data was unrevised but confirmed its slowest annual pace since 2012 (YoY: 1.4%)

- One year to go for Brexit to become a reality (takes effect March 29, 2019 at 2300 GMT)

Asia:

- Japan Fin Min Aso stated that the country’s long standing stance was to definitely avoid bilateral trade negotiations with US

- China Commerce Ministry (MOFCOM) reiterated it hoped US took measures and resolved conflict with China through dialogue, did not want a trade war with the US

- South Korea Finance Ministry reiterated that its FX policy related talks with the US were separate from trade talks. Disclosing FX intervention details was likely to ease worries about Korea getting a currency manipulator label.

Europe:

- EU canceled a scheduled Brexit meeting for Apr 17th due to lack of new topics to discuss (Reminder: On Mar 19th EU and UK agreed on Brexit transition terms but Ireland issue remained)

- UK Labour Party (opposition) said to be likely to vote in favor of a final Brexit agreement

- UK Mar GfK Consumer Confidence data at a 10-month high (-7 v -10e)

Americas:

- Fed's Bostic (FOMC voter, dove): not seeing upward wage pressure despite low level of unemployment

Economic Data

- (NL) Netherlands Mar Producer Confidence: 9.5 v 10.9 prior

- (UK) Mar Nationwide House Price M/M: -0.2% v +0.2%e; Y/Y: 2.1% v 2.6%e

- (ZA) South Africa Feb M3 Money Supply Y/Y: 6.9% v 6.0%e; Private Sector Credit Y/Y: 5.7% v 5.5%e

- (FI) Finland Jan Final Trade Balance: -€0.1B v -€0.2B prelim

- (DE) Germany Mar CPI Saxony M/M: 0.4% v 0.4% prior; Y/Y: 1.5% v 1.3% prior

- (CH) Swiss Mar KOF Leading Indicator: 106.0 v 107.2e

- (TR) Turkey Q4 GDP Q/Q: 1.8% v 1.2%e; Y/Y: 7.3% v 6.7%e

- (AT) Austria Feb PPI M/M: 0.0% v 0.4% prior; Y/Y: 1.2% v 1.3% prior

- (HU) Hungary Feb PPI M/M: 0.8% v 0.3% prior; Y/Y: 3.9% v 3.3% prior

- (CZ) Czech Jan Export Price Index Y/Y: -4.1% v -2.8% prior; Import Price Index Y/Y: -5.8% v -4.2% prior

- (HU) Hungary Jan Final Trade Balance: €0.7B v €0.7B prelim

- (DE) Germany Mar Unemployment Change: -19K v -15Ke; Unemployment Claims Rate: 5.3% (record low) v 5.3%e

- (DE) Germany Mar CPI Brandenburg M/M: 0.4% v 0.3% prior; Y/Y: 1.6% v 1.5% prior

- (DE) Germany Mar CPI Hesse M/M: 0.4% v 0.4% prior; Y/Y: 1.5% v 1.1% prior

- (DE) Germany Mar CPI Bavaria M/M: 0.5% v 0.5% prior; Y/Y: 1.7% v 1.6% prior

- (CZ) Czech Feb M2 Money Supply Y/Y: 7.2% v 7.7% prior

- (IT) Italy Feb PPI M/M: 0.3% v 0.8% prior; Y/Y: 1.8% v 1.8% prior

- (DE) Germany Mar CPI Baden Wuerttemberg M/M: 0.4% v 0.5% prior; Y/Y: 1.7% v 1.6% prior

- (DE) Germany Mar CPI North Rhine Westphalia M/M: 0.4% v 0.5% prior; Y/Y: 1.6% v 1.3% prior

- (UK) Q4 Final GDP (3rd reading) Q/Q: 0.4% v 0.4%e; Y/Y: % v 1.4%e

- (UK) Q4 Final Total Business Investment Q/Q: 0.3% v 0.0%e; Y/Y: 2.6% v 2.1%e

- (UK) Q4 Current Account: -£18.4B v -£24.0Be

- (UK) Feb Net Consumer Credit: £1.6B v £1.4Be; Net Lending: £3.7B v £3.4Be

- (UK) Feb Mortgage Approvals: 63.9K v 66.0Ke

- (UK) Feb M4 Money Supply M/M: -0.3% v +1.5% prior; Y/Y: 4.1% v 4.3% prior, M4 Ex IOFCs 3M Annualized: 3.3% v 5.5% prior

- (UK) Jan Index of Services M/M: 0.2% v 0.2%e; 3M/3M: 0.6% v 0.6%e

- (PT) Portugal Mar Preliminary CPI M/M: +1.9% v -0.7% prior; Y/Y: 0.7% v 0.6% prior

- (PT) Portugal Mar CPI EU Harmonized M/M: 2.2% v -0.6% prior; Y/Y: 0.8% v 0.7% prior

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.4% at 370.6, FTSE +0.5% at 7079, DAX +0.6% at 12015, CAC-40 +0.5% at 5157, IBEX-35 +1.0% at 9647, FTSE MIB +0.5% at 22440 , SMI -0.2% at 8744, S&P 500 Futures +0.3%]

Market Focal Points/Key Themes:

- European Indices rebound after yesterdays losses following a raft of inflation data out of Europe and data in the UK. M&A remains the dominant theme with Nex Group confirming its to be acquired by the CME in a £3.9B deals, with shares of Renault trading higher after talk of a potential tie up with Nissan, Swiss Re trades higher after talk of Softbank acquiring a $9.6B stake; Tomtom trades higher after denying it engaged with advisers to look for buyers.

- On the earnings front, Sodexo trades sharply lower after cutting its outlook on a weaker Q2, Manz and Nemetschek trade higher following results.

- Looking ahead notable earners include Constellation Brands, Worthington and Movado.

Movers

- Consumer Discretionary [TomTom [TOM2.NL] +2.6% (Denies reports on hiring advisors for sale of co), Sodexo [SW.FR] -14.2% (Earnings, Cuts outlook), Compass [CPG.UK] -2.8% (In sympathy with Sodexo)]

- Industrials [ Renault [RNO.FR] +4.4% (Report on potential merger with Nissan), Manz Automation [M5Z.DE]+2.3% (Earnings)]

- Financial [ CMC Markets [CMCX.UK] +8.6% (Trading update), Swiss Re [SREN.CH] +2.9% (Reportedly Softbank mulling $9.6B stake)]

- Technology [TeleColumbus [TC1.DE] -0.3% (Earnings), Nemtschek [NEM.DE] +6.7% (Earnings) ]

Speakers

- UK Trade Sec Fox: Brexit transition period beyond 2020 is unlikely and would not support any extension. Believed UK govt would get a Brexit deal that is acceptable to parliament

- Italy President Mattarella to begin talks on forming new govt on Wed, Apr 4th

- Romania Central Bank gov Isarescus stated that it had raised rates rapidly to calm inflation. RON currency (Leu) facing depreciation pressures

- Canada Fin Min Morneau reiterated view that NAFTA negotiations were going well

- South Korea Unification Ministry official confirmed that South and North Korea leaders to hold a summit on April 27th to discuss denuclearization and a peace treaty. The two countries to also hold a meeting regarding the summit's security on April 4th.

- China State Council: To review proposed intellectual property transfers that might affect national security

Currencies

- FX price action was sparse ahead of the Easter and Passover holidays with the greenback holding on to recent gains. A plethora of European economic released did little to quell any fresh position taking

- GBP was softer for a 3rd straight session and hovered around 1-week lows in the mid-1.40 area. UK Q4 Final GDP was unrevised but confirmed its slowest annual pace since 2012

- EUR/USD hovered around the 1.24 level as various German individual States Mar CPI data came in below expectations of the overall German inflation data due out later today. The CPI reinforced some of the recent cautious remarks by ECB officials on making any abrupt changes in its policy and giving more time to decide about its future moves until summer period

Fixed Income

- Bund Futures trade 16 ticks higher at 159.34 as the German unemployment rate hits a record low. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 122.77 up 17 ticks as the third and final gdp reading comes in unrevised. Support continues stands at 121.25 then 120.85, with upside resistance at 123.35 then 123.85.

- Thursday's liquidity report showed Wednesday's excess liquidity rose to €1.798T from €1.789T prior. Use of the marginal lending facility increased from €110M to €131M.

Looking Ahead

- (EG) Egypt Central Bank Interest Rate Decision: Expected to cut Deposit Rate by 100bps to 16.75%

- (CA) Canada Mar CFIB Business Barometer: No est v 62.4 prior

- (BE) Belgium Mar CPI M/M: No est v 0.2% prior; Y/Y: No est v 1.5% prior

- (MX) Mexico Election deadline for parties to register their candidate for 2018 election

- (UK) Last Day of Commons Session Before Easter Recess

- 05:30 (ZA) South Africa Feb PPI M/M: 0.5%e v 0.3% prior; Y/Y: 5.0%e v 5.1% prior

- 05:30 (SL) Sri Lanka Mar CPI Y/Y: No est v 4.5% prior

- 05:30 (HU) Hungary Debt Agency (AKK) to sell Bonds (3 tranches)

- 06:00 (IL) Israel Feb Unemployment Rate: No est v 3.7% prior

- 06:00 (PT) Portugal Feb Industrial Production M/M: No est v 2.5% prior; Y/Y: No est v 2.8% prior

- 06:00 (PT) Portugal Feb Retail Sales M/M: No est v -0.5% prior; Y/Y: No est v 5.4% prior

- 06:00 (FI) Finland Quarterly Review

- 06:00 (UK) DMO to sell combined £3.5B in 1-month, 3-month and 6-month Bills (£0.5B, £1.0B and £2.0B respectively)

- 06:00 (HU) Hungary Central Bank holds Interest Rate Swap (IRS) Tender

- 07:00 (BR) Brazil Central Bank (BCB) Quarterly Inflation Report

- 07:00 (CZ) Czech Central Bank (CNB) Interest Rate Decision: Expected to leave Repurchase Rate unchanged at 0.75%

- 08:00 (DE) Germany Mar Preliminary CPI M/M: 0.5%e v 0.5% prior; Y/Y: 1.7%e v 1.4% prior

- 08:00 (DE) Germany Mar Preliminary CPI EU Harmonized M/M: 0.5%e v 0.5% prior; Y/Y: 1.6%e v 1.2% prior

- 08:00 (ZA) South Africa Feb Budget Balance (ZAR): No est v -41.3B prior

- 08:00 (ZA) South Africa Feb Trade Balance (ZAR): +1.0Be v -27.7B prior

- 08:00 (BR) Brazil Feb PPI Manufacturing M/M: No est v 0.4% prior; Y/Y: No est v 4.0% prior

- 08:00 (BR) Brazil Feb National Unemployment Rate: 12.5%e v 12.2% prior

- 08:00 (CL) Chile Feb Industrial Production Y/Y: 9.0%e v 5.3% prior, Manufacturing Production Y/Y: 5.9%e v 5.7% prior, Total Copper Production: No est v 503.8K prior

- 08:00 (CL) Chile Feb Unemployment Rate: 6.6%e v 6.5% prior

- 08:05 (UK) Baltic Dry Bulk Index

- 08:15 (CZ) Czech Central Bank Gov Rusnok post rate decision press conference

- 08:30 (US) Initial Jobless Claims: 230Ke v 229K prior; Continuing Claims: 1.87Me v 1.828M prior

- 08:30 (US) Feb Personal Income: 0.4%e v 0.4% prior; Personal Spending: 0.2%e v 0.2% prior; Real Personal Spending (PCE): +0.1%e v -0.1% prior

- 08:30 (US) Feb PCE Deflator M/M: 0.2%e v 0.4% prior; Y/Y: 1.7%e v 1.7% prior

- 08:30 (US) Feb PCE Core M/M: 0.2%e v 0.3% prior; Y/Y: 1.6%e v 1.5% prior

- 08:30 (CA) Canada Jan GDP M/M: 0.1%e v 0.1% prior; Y/Y: 2.9%e v 3.3% prior

- 08:30 (CA) Canada Feb Industrial Product Price M/M: No est v 0.3% prior; Raw Materials Price Index M/M: No est v 3.3% prior

- 08:30 (US) Weekly USDA Net Export Sales

- 09:00 (RU) Russia Gold and Forex Reserve w/e Mar 23rd: No est v $455.4B prior

- 09:45 (US) Mar Chicago Purchasing Manager: 62.0e v 61.9 prior

- 10:00 (US) Mar Final University of Michigan Confidence: 102.0e v 102.0 prelim

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 12:00 (US) USDA Q1 Grain Stocks Report

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 13:00 (US) Fed's Harker (non-voter, moderate) speaks on the Economic Outlook

DAX Moves Higher As Trade War Fears Ease

The DAX index has posted considerable gains in the Thursday session. Currently, the DAX is trading at 12,027 points, up 0.73% on the day. In economic news, German unemployment change posted a strong decline of 19 thousand, beating the estimate of 15 thousand. German unemployment change posted a strong decline of 19 thousand, better than the estimate of 15 thousand.

The US economy continues to show strong expansion. Revised GDP for the third quarter came in at 2.9%, beating the estimate of 2.7%. This reading was revised upwards from the initial GDP estimate of 2.5%. Fourth quarter growth, although solid, could not keep up with a superb third quarter, which posted a gain of 3.2%. As for 2018, first quarter growth is expected to soften to 1.8%, but there is still a strong chance that the economy could hit 3% growth this year, as promised by US President Trump. The catalysts for such a rosy prediction are the massive tax cut and higher government spending. Where does this leave the Federal Reserve, which raised interest rates last week? Currently, the Fed is projecting to more rate hikes this year, but if the economy remains strong and inflation levels move closer to the Fed target of 2%, we could see four rate increases in 2018.

The tariff dispute between the US and China has shaken up global stock markets. Investors lost their risk appetite last week after President Trump’s dramatic announcement that he was imposing stiff tariffs on up to $60 billion in Chinese imports. China vowed to retaliate and slap imports on a range of US products. This move came on the heels of a blanket US tariff on steel imports. Although Trump backtracked and exempted Canada, Mexico and other countries from the steel tariffs, the threat of a global trading war has unnerved investors. This week, however, China was singing a more conciliatory tune, saying it would apply to the World Trade Organization to overturn the tariffs. The US has imposed the tariffs under a national security provision, but China has argued that the move is a trade barrier with the intent of protecting domestic producers. Although the dispute has not been resolved, the Chinese move has eased tensions and restored investor risk appetite this week, in the hope that both the US and China policymakers will climb down from their trees and reach some agreement instead of slapping tariffs on each other.

Euro Stems Slide, Markets Await German CPI

EUR/USD is unchanged in the Thursday session, after recording losses in the past two sessions. Currently, the pair is trading at 1.2308, down 0.01% on the day. On the release front, Germany releases Preliminary CPI, which is expected to remain unchanged at 0.5%. German unemployment change posted a strong decline of 19 thousand, better than the estimate of 15 thousand. There are a host of key indicators in the US, led by unemployment claims and consumer confidence. The markets are expecting unemployment claims to tick higher to 230 thousand, while UoM Consumer Sentiment is forecast to rise to 131.2 points.

There was good news for the US dollar on Wednesday, as US revised GDP for the third quarter came in at 2.9%, beating the estimate of 2.7%. This reading was revised upwards from the initial GDP estimate of 2.5%. Fourth quarter growth, although solid, could not keep up with a superb third quarter, which posted a gain of 3.2%. As for 2018, first quarter growth is expected to soften to 1.8%, but there is still a strong chance that the economy could hit 3% growth this year, as promised by US President Trump. The catalysts for such a rosy prediction are the massive tax cut and higher government spending. Where does this leave the Federal Reserve, which raised interest rates last week? Currently, the Fed is projecting to more rate hikes this year, but if the economy remains strong and inflation levels move closer to the Fed target of 2%, we could see four rate increases in 2018.

In the eurozone, the storyline of stronger economic conditions but low inflation continues in 2018. This trend adds up to the ECB staying the course with regard to its stimulus program, according to a senior ECB policymaker. Governing Council member Erkki Liikanen said on Tuesday that the ECB will have to remain patient with its stimulus program, noting underlying inflation could remain at low levels, even if the economy performs well, since reducing economic slack may no longer trigger higher inflation, as has been the case in the past. With the current bond purchase program set to expire in September, there is speculation that the ECB will wind up the program, after years of pursuing an accommodative policy. If inflation does move closer to the ECB’s target of around 2 percent, there is a greater likelihood that the bank will not extend stimulus, and could entertain raising interest rates in 2018.

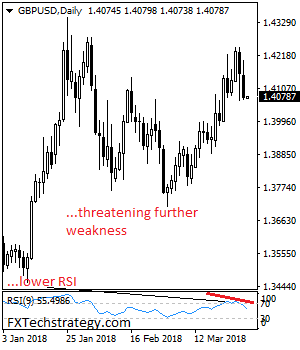

Sterling Further Bearish Below 1.4087 Level

The British pound continues to unwind against the U.S dollar, with downside selling pressures building and price-action now trading well below the 1.4087 key support level. The U.S dollar index has now moved above the 90.00 level, further boosting the intraday sentiment surrounding the greenback. Moving into the U.S session traders now look towards the release of inflation, income and jobs data from the United States economy.

The GBPUSD pair remains intraday bearish whilst trading below the 1.4087 level, further declines towards the 1.4000 and 1.3959 levels seems possible.

If the GBPUSD pair moves above the 1.4087 level for a sustained basis, a correction towards the 1.4146 and 1.4200 levels may occur.

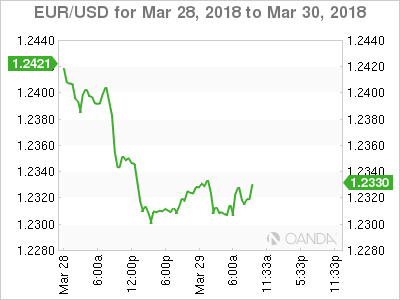

EURUSD Pair Testing 1.2300 Support Level

The euro continues to trade to the downside against the greenback, as the U.S dollar index pushes higher, and euro sellers starting to probe the 1.2300 support level. The EURUSD pair looked past record German employment data earlier, as the countries Unemployment rate fell to its lowest ever monthly level. Below the 1.2300 support level, the 1.2239 March-low is the key support area to watch, whilst the 1.2382 level remains key daily resistance area.

The EURUSD pair is likely to see strong selling below the 1.2300 level, with key support then found at the 1.2275 and 1.2239 levels.

Should the EURUSD pair manage to correct above the 1.2382 level, further upside towards the 1.2400 and 1.2430 levels seems possible.