Sample Category Title

Sunset Market Commentary

Markets:

Global core bond markets held a positive bias as rising equity volatility supported a bid for safe havens. End of month extension buying probably remained mildly positive as well. Bunds and Treasuries extended yesterday's rebound early in European trading. The fall-out from the sell-off in tech equities eased (at least temporary), capping further bond gains. However, equity trading turned again more volatile after the open of the US equity. So, the jury is still out. US eco data were mixed and unimportant for bond trading. The focus remains on equities. At the time of writing, German yields decline less than 1 bp. US yields decline between 0.5 bps (2y) and 2.5 bps (10y). The US Treasury sells $15 bln 2-year floating rate notes and $29 bld 7-year bonds this evening.

The dollar held up well overnight despite a sell-off in (US) tech shares that continued in Asia this morning. USD/JPY in particular held 'strong' despite substantial equity losses. Dollar strength was probably also at least partially due to end of month/quarter position squaring. This USD bid was also visible in the trade-weighted dollar (DXY) which rose to 89.60 (from a correction low just below 89 yesterday). The price move in EUR/USD remained modest initially, but the broader bid for the dollar finally pushed the pair lower from the 1.2420 area to below 1.2350. US eco data were mixed with US GDP upwardly revised to 2.9% from 2.5% Q/Qa. Wholesale inventories rose a bigger than expected 1.1% M/M. The data suggest ongoing positive growth momentum in the US economy, but they won't have a lasting impact on USD trading. Interest rate differentials between the US and Germany stay off recent highs, but were also no big driver for USD trading. Order-driven activity prevailed. USD/JPY is trading in the 106.20 area. Tomorrow's PCE deflators might provide some more 'economically inspired' guidance for the dollar.

Sterling was temporary supported by headlines that the UK was working on a constructive solution to solve the issue of the Irish border post-Brexit. There are no details yet. UK economic news was mixed. CBI retail data were weaker than expected, but poor weather conditions were to blame. A BoE survey published showed UK companies are increasingly reporting shortages of skilled labour. Until now this had only a limited impact on pay growth, but the BoE gradually sees some upward wage drift. This might support the case for higher BoE rates later this year. EUR/GBP trades little changed in the 0.8750 area. Cable eased from the 1.42 area this morning to the low 1.41 area currently, but this is primarily due USD strength rather than GBP weakness.

News Headlines:

The balance of the CBI distributive trades survey declined to -8 in March from +8 in February, suggesting lower sales. The market consensus expected a positive balance of +7. According to CBI, the impact of a stagnating household income and weak consumer confidence was reinforced by unusually cold winter weather in March.

US Q4 2017 GDP was upwardly revised to 2.9% Q/Q (annualized) from 2.5% earlier. Q3 growth was 3.2% Q/Qa. Growth in consumer spending was upwardly revised to 4.0% from 3.8%. A decline in inventories weighed on growth, but the negative impact was smaller than initially reported. Net exports subtracted 1.16 percentage points from GDP.

Advance data from the Commerce department indicated that February US goods trade deficit widened slightly from $75.3 bn to $75.4 bn in February. The February deficit was upwardly revised from $74.4 bn. Goods exports rose 2.2% M/M to USD 136.55 bn. Imports rose 1.4M/M to 212.90 bn.

US: Income Remained Strong, Spending Not So Much

Income remained relatively strong in February, but Americans seem to be taking a break from what was a breakneck pace of consumption during the last quarter of 2017. Inflation moved higher on a year-earlier basis.

Americans Seem to be Taking a Break

The revision to Q4 personal consumption expenditures (PCE) released yesterday saw a breakneck pace of consumer demand during the last quarter of 2017, a pace that was not sustainable considering the growth rates of income we saw in late 2016 as well as in 2017. For this, it is not completely surprising that Americans have taken a break during the first quarter of the year. February's 0.2 percent gain in personal spending after a similar nominal rate increase in January shows a very weak consumer during the first quarter of the year. In fact, in real terms, PCE was revised down from a decline of 0.1 percent in January to a decline of 0.2 percent, while remaining flat in February. If there are no further revisions to these numbers in the months ahead, then March real personal spending will have to show a relatively strong performance to avoid a flat first quarter for PCE, if not a flat-out decline.

We still believe that real consumption will rebound in March, but the recent weather in the Northeast may also have helped depress consumer demand in March. This added to what has been typical of first quarter results since the recovery from the Great Recession, that is, residual seasonality, could make for an interesting reading for first quarter GDP.

Income is Recovering Nicely

Another reason to think that consumption is going to rebound soon is that consumer confidence remains high, and income growth has rebounded nicely over the past several quarters. Personal income grew 0.4 percent in February after a similar increase in January. Real disposable income, on the other hand, increased by 0.6 percent in January and by 0.2 percent in February as the effects of tax reform dissipated. However, income from wages and salaries remained strong, growing $41.1 billion in February after a $50.0 billion increase in January. But what was more important was that wages and salaries from goods-producing industries increased $24.8 billion in the month after an increase of $13.2 billion in January.

Meanwhile, proprietors' income, which had been weak in December and January, recovered in February and increased at a $15.3 billion annual rate. Personal income receipts on assets were also strong, increasing $7.0 billion in February after a decline of $4.8 billion in January. While personal interest income declined $1.5 billion, personal dividend income surged $8.6 billion at an annual rate.

The saving rate increased to 3.4 percent in February, while growth in wages and salaries slowed down a bit on a year-earlier basis, to 4.5 percent compared to 4.7 percent in January. Meanwhile, inflation moderated on a month-on-month basis but moved higher on a year-earlier basis.

Canadian GDP Down in January as Mining and Real-Estate Contract

Highlights:

- Canadian GDP fell 0.1% in January — below market expectations for a 0.1% increase

- Weakness was concentrated in a (likely transitory) decline in oil sands output and a pullback in home resales. Outside of the oil and real-estate components, output increased about 0.2% by our calculation.

- The softer-than-expected start to the year leaves risks tilted to the downside relative to our call for a 1.9% Q1 GDP gain — but we still expect growth is tracking in a 1.5% to 2% range that would be at or a bit above the economy’s long-run potential growth rate.

Our Take:

GDP unexpectedly fell 0.1% in January. Markets expected closer to a 0.1% gain in the month, on balance. The news wasn’t all bad, though. The big drop in home resales in January alone subtracted about 0.1 percentage points from headline GDP growth. Home resales have remained soft, but that decline probably won’t be repeated to the same extent. Much of a big 7% drop in oil sands production was reportedly the result of transitory maintenance shutdowns that will be unwound in coming months. Outside of those two components, output edged up about 0.2% by our calculation — led by a 0.7% increase in manufacturing output and a 0.5% construction increase.

The softer-than-expected start to the year still leaves risks tilted to the downside relative to our call for a 1.9% Q1 GDP gain — and further downside relative to the Bank of Canada’s 2.5% forecast for the quarter. The prospect for some bounce-back in coming months as transitory January weakness reverses, as well as an upward revision to December GDP growth to 0.2% from 0.1%, still leaves growth tracking in a 1 1/2% to 2% range though. To be sure, that is well-below the 4% pace of growth the economy was running at a year ago but with the economy likely at capacity that stronger growth is more difficult to accommodate. Looking through monthly volatility the economy still looks to be growing at a rate at or a bit above its long-run potential growth rate.

Canada Starts 2018 With a Slight Step Backwards

The Canadian economy started 2018 with a modest contraction of output, down 0.1% in January. While a few industries stood out for the strength of their retrenchments, weakness was fairly widespread as only 10 of 20 major industries reported gains on the month.

Leading the way lower were the goods-producing sectors. A sizeable pullback in mining, quarrying, and oil and gas extraction (-2.7%) was led by declines in oil and gas as a number of facilities saw unplanned maintenance shutdowns. The remaining goods industries displayed mixed performances, with surprising strength in construction (+0.5%) and manufacturing (+0.7%).

On the services side, despite a sizeable pull-back in a number of sectors, notably real estate (-0.5%) and arts and entertainment (-0.8%), service producing sectors as a whole eked out a tiny gain (+0.007%), good enough to mark a 22nd straight month of expansion. This is now the second-longest expansion of the sector on record. Helping keep the sign positive were wholesale and retail trade (+0.5% and +0.2% respectively), as well as administrative and related services (+0.5%) and finance and insurance (+0.3%)

Key Implications

This year started off with more of a whimper than a bang, at least from a growth perspective. Part of this was by design, as government policy changes hammered real estate activity. There were also some one-off movements elsewhere, including an unexpected pull-back of oil and gas on the back of unscheduled maintenance activities. However, with only 10 of 20 industries in the green, it is hard to find a lot to like in today's numbers. If there is a silver lining, it is that some areas, notably oil and gas, are likely to see a rebound in February.

As usual though, the trend is more important than the noise. Clearly the pace of economic activity has moderated from last year's red-hot first half performance, but this is to be expected in an economy with little slack remaining. Our current tracking of 1.4% growth in the first quarter may be a reflection of the noise, but over the medium-term, Canada's economic fundamentals remain consistent with growth in the 1.5% to 1.9% range – enough to maintain inflationary pressures and ongoing (modest) job gains.

All the noise of late does make the Bank of Canada's job that much harder however. The 1.4% tracking is a far cry from the 2.5% the Bank of Canada was expecting in January, but at the same time, inflation has ticked up markedly so far this year. All eyes are bound to be focused on how these developments are treated in April's interest rate decision and Monetary Policy Report. With economic risks still elevated and inflation seemingly boosted by a number of one-offs (such as minimum wage changes), it is likely that the output data will carry the day. This should result in continued caution from the Bank of Canada, consistent with recent communications.

US: Soft Spending in February Spells Another Weak Start to the Year

As expected, personal income rose 0.4% in February. Disposable income posted a matching gain of 0.4% on the month, and when adjusted for inflation, real disposable income was up a more modest 0.2%.

Personal spending was also in line with expectations, rising 0.2% in nominal terms. In real (inflation-adjusted) terms however, spending was flat. Real spending in January was also revised down.

By component, real spending on durable goods recovered part of January's 1.6% decline, up 0.6%. Non-durable goods spending declined (-0.3%) for the third month in a row, following a period of strength at the end of 2017. Services spending was flat in real terms.

Prices rose 0.2% month-on-month in February, lifting headline inflation a tick to 1.8%. Core prices also firmed, rising 0.2% (m/m) in February, taking core inflation up slightly to 1.6% year-on-year.

The personal saving rate rose slightly to 3.4% in February, as it recovers from very low levels at the end of last year. The saving rate remains below its five year average of 5%.

Key Implications

Just as it did in 2016 and 2017, consumer spending started the year on a soft note. Even a strong showing for consumer spending in March won't be enough to save the first quarter, where consumer spending growth is tracking not much above 1% growth in real terms. Some of the spending weakness is simply give back following hurricane-induced buying late in 2017. But, it is difficult not to notice the apparent seasonal pattern even in the "seasonally adjusted data"; a weak first quarter is followed by strength through the remainder of the year.

The weakness to start the year is likely to imply a one-handle for real GDP too, notably weaker than in our recent forecast. Still, we are not concerned with the apparent setback, which should prove to be short lived if history is any guide. With both tax cuts and a tightening labor market likely to push up income, household demand is expected to accelerate enough to pull growth to a well above-trend rate over the remainder of 2018.

The encouraging part of this report is on the inflation front. Momentum has picked up in recent months, and the annualized three-month moving average core inflation rate currently sits at 2.3%. There is cause to fade some of this strength – the residual seasonality in the real spending data is the flip side of seasonality on the inflation front, where price growth appears understated at the end of the calendar year and overstated in January. Short-term gyrations aside, inflation is at a turning point. We expect that upward momentum in inflation will continue over the medium term, underpinning further rate hikes by the Federal Reserve.

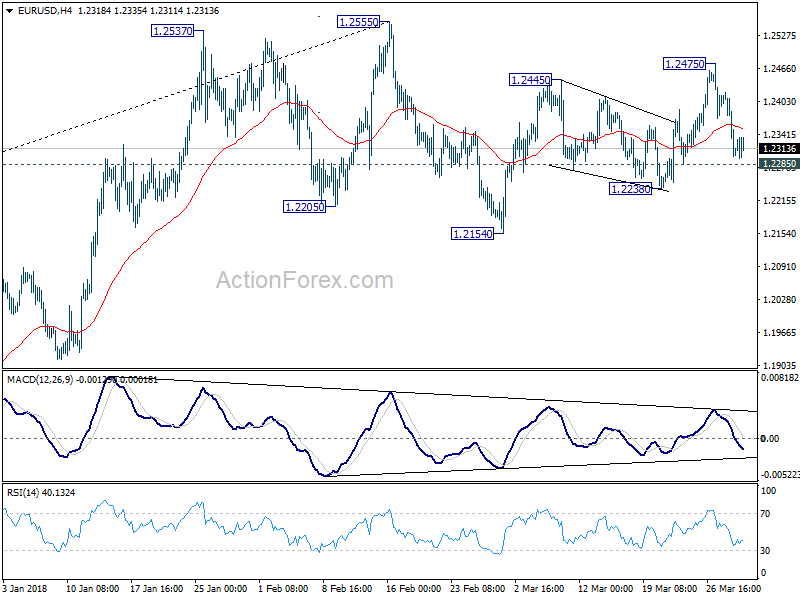

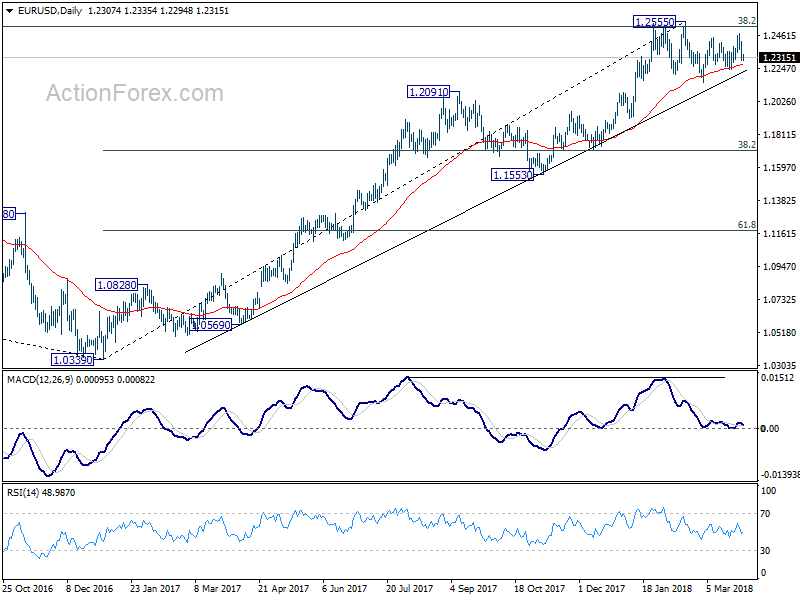

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2264; (P) 1.2342 (R1) 1.2386; More....

EUR/USD is still holding above 1.2285 minor support. Intraday bias is staying neutral at this point. On the upside, above 1.2475 will target a test on 1.2555 high, which is close to 1.2516 key long term fibonacci level. We'd be cautious on reversal from there. But decisive break will carry larger bullish implications. On the downside, below 1.2285 minor support will turn bias to the downside for 1.2154 and possibly below.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

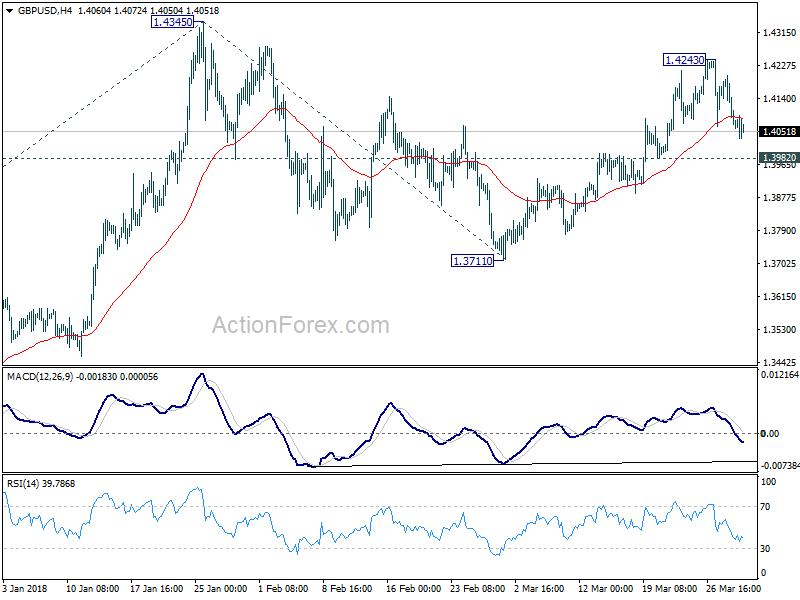

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4030; (P) 1.4115; (R1) 1.4160; More....

Intraday bias in GBP/USD remains neutral. With 1.3982 minor support intact further rise is mildly in favor. On the upside, above 1.4243 will resume the rise from 1.3711 and target 1.4345 high first. Decisive break there will resume larger up trend and target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 next. On the downside, however, firm break of 1.3982 will indicate completion of rebound from 1.3711. In that case, intraday bias will be turned back to the downside for retesting 1.3711.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

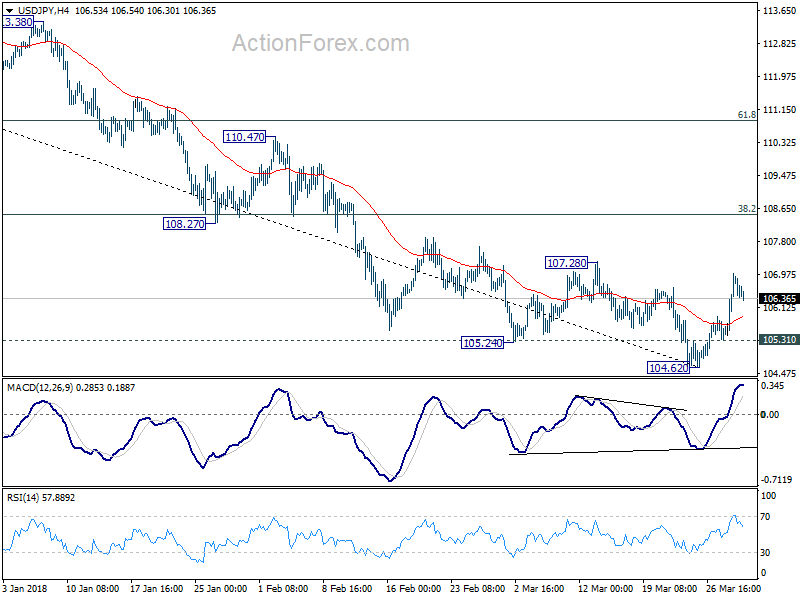

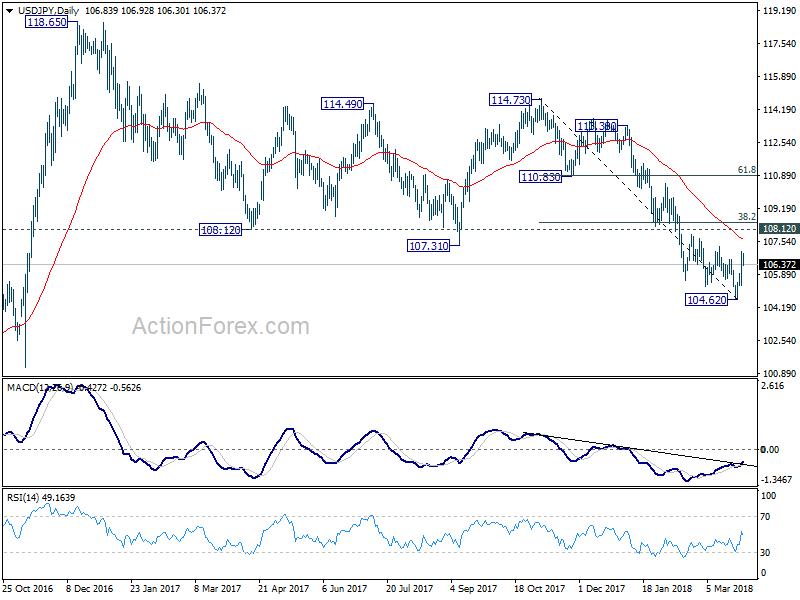

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.12; (P) 105.51; (R1) 105.71; More...

Further rise is expected in USD/JPY as the rebound from 104.62 short term bottom should extend. USD/JPY should target 38.2% retracement of 114.73 to 104.62 at 108.48. At this point, there is no confirmation of trend reversal yet. Hence, we'll look at the reaction from 108.48 (which is close to 108.12 too) to assess the chance. On the downside, below 105.31 minor support will indicate that the rebound is completed and turn bias back to the downside instead.

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

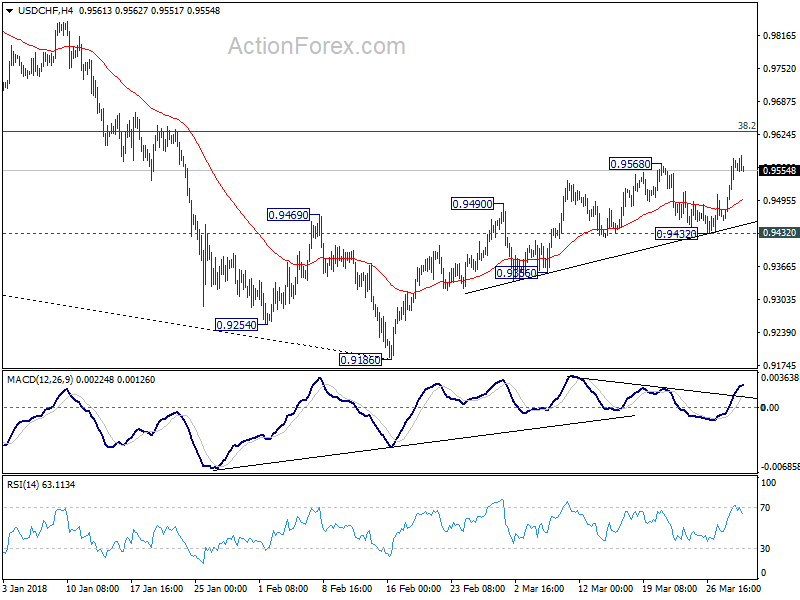

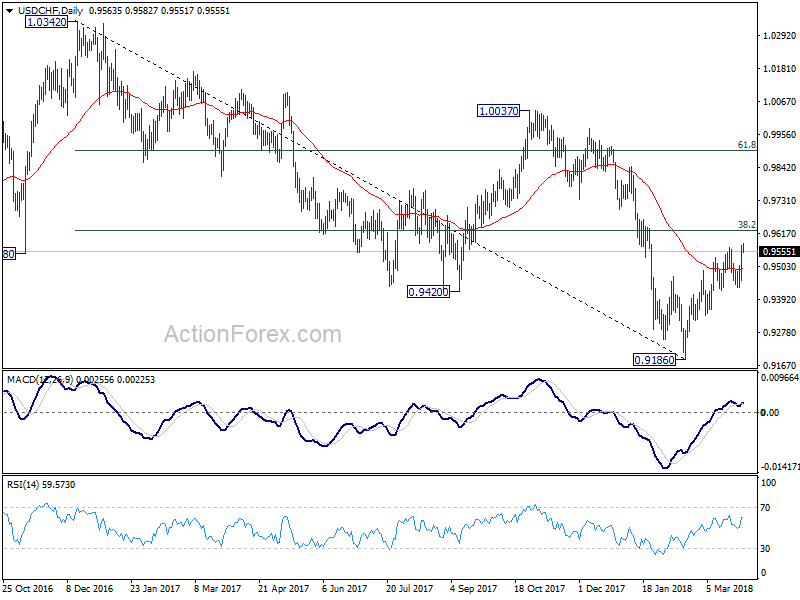

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9431; (P) 0.9470; (R1) 0.9505; More...

No change in USD/CHF's outlook. Rebound from 0.9186 is still in progress but it's seen as a corrective move. Hence, we'd expect strong resistance from 0.9626 key fibonacci level to limit upside. On the downside, break of 0.9432 support will indicate near term reversal and completion of rebound from 0.9186. In this case, intraday bias will be turned back to the downside for retesting 0.9186 low. However, sustained break of 0.9626 will be another evidence of larger reversal. In this case, further rise would be seen to next fibonacci level at 0.9900.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

Markets Tread Water as Traders’ Minds are Already on Holiday

The forex market are starting to ignore economic data release today and tread water, just ahead of long weekend. Dollar is trading in black across the board for the week. But better than expectation job data doesn't the greenback a boost to extend its rally. Canadian Dollar also shrugs off worse than expected GDP data and stays as the second strongest for the week. Meanwhile, Yen and Swiss France are the weakest.

US jobless claims dropped to lowest since 1973, Canada GDP missed expectations

US personal income rose 0.5% in February, spending rose 0.2% and both met expectations. Headline CPI accelerated to 1.8% yoy while core PCE also accelerated to 1.6% yoy. Initial jobless claims dropped -12k to 215k in the weekended March 254. That's notably below expectation of 231k. That's also the lowest level since January 1973. Four week moving average of initial claims dropped 0.5k to 224.5k. Continuing claims rose 35k to 1.87m in the weekended March 17.

Canadian data are generally disappointingly. GDP contracted -0.1% mom in January versus expectation of 0.1% mom. IPPI rose 0.1% mom in February versus expectation of 0.4% mom. RMPI dropped -0.3% mom versus expectation of 2.8% mom rise.

Philadelphia Fed Harker expects three hikes this year on "some firming of inflation"

Philadelphia Fed President Patrick Harker said in a WSJ interview that he now expects three Fed rate hike this year. Harker is seen as on the dovish side of the spectrum as he previously projected just two hikes in 2018. He pointed to "some firming of inflation" as he reason for the upgrade is his own forecast. He also clarified that he placed more emphasis on inflation than fiscal policy. Nonetheless, Harker also sounded cautious on trade tensions. He noted that risk of increasing trade tariffs as a source of uncertainty for both economic projections and monetary policy.

ECB Knot: Market expectations and ECB policy actions converged into a "sweet spot"

ECB Governing Council member, Dutch central bank Governor Klaas Knot talked about monetary policy as he presented his bank's annual report in Amsterdam today. He emphasized that the top priority for ECB now is to "normalize monetary policy and strengthen the economic and monetary union". And, market expectations of ECB's policy action "have more or less converged at what I call a sweet spot", with " a fair degree of consensus around these expectations."Therefore, the likelihood of being "too cautious" is a bit larger than being "too bold".

Regarding trade relationship with the US, he said "he question is if Europe will come with countermeasures which could make us slip into a trade war." But he also emphasized that " if the US were to implement trade restrictions on say steel, it will be the American consumer paying the price."

Released from Eurozone, German unemployment dropped -19k to 2.373m in March, more than expectation of -15k. Unemployment rate dropped from 5.4% to 5.3%, met expectation. That's also the lowest level on record. Also from Germany, CPI rose 0.4% mom, 1.6% yoy in March, up from prior's 1.4% yoy but missed expectation of 1.7% yoy.

Swiss KOF: Dropped but still indicates above average growth

Swiss KOF economic barometer dropped to 106.0 in March, down from 108.4, below expectation of 107.2. KOF noted in the release that "notwithstanding this decline, the present position is still on a level clearly above its long-term average." This indicates that in the near future the Swiss economy should continue to "grow at rates above average".

UK Gfk Consumer Confidence: Definitely a movement in the right direction

UK Gfk consumer confidence rose to -7 in March, up from -10 and above expectation of -10. All five of the constituent measures recorded higher values. Personal financial situation over the past 12 months rose 3 pts to 3. Personal financial situation over next 12 months rose 5 pts to 10. General economic situation over the last 12 month rose 3 pts to -26. General economic situation over next 12 months rose 4 pts to -22. Major purchase index rose 2 pts to 2. Saving index rose 1 pt to 13.

Gfk noted in the release that "the prospect of wage rises finally outstripping declining inflation, high levels of employment with low-level interest rates, and finally some movement on the Brexit front appear to have boosted our spirits." While it's "still a little early to be talking about green-shoots", "this is definitely a movement in the right direction".

Also from UK, Q4 GDP was finalized at 0.4% qoq, unrevised. Current account deficit narrowed to GBP -18.4b in Q4. Index of serves rose 0.6% 3mo3m in January. M4 money supply dropped -0.4% mom in February. Mortgage approvals dropped to 64k in February.

Japan at beginning of consumer spending recovery

Japan retail sales rose 0.4% mom, 1.6% yoy in February, slightly higher than expectation of 0.6% mom, 1.7% yoy. And it's marked improvement from January's -1.6% mom, 1.5% yoy. It's noted that consumer spending could be at the beginning of mild recovery. Improvement is also seen lately in the labor market. Overall picture suggests that consumption is going to pick up momentum. And that should eventually help lift inflation. But for now, core inflation is still way off BoJ's 2% target and it will take some more time for BoJ to start considering stimulus exit.

Japan FM Aso: No bilateral trade negotiations with US

Japan finance minister Taro Aso said in the parliament that historically, US Dollar always rise against Japanese Yen when interest rate differentials widened to 3%. Aso added that US interest rates will "undoubtedly rise ahead". And therefore, there won't be "one-sided" Yen appreciation that could hurt the economy.

Regarding trade, Aso emphasized that Japan should "definitely avoid" bilateral trade negotiations with the US. He added that "When two countries negotiate, the stronger country gets stronger. That's unnecessary (for Japan) so we've been saying all along that we would definitely avoid" bilateral trade talks with the United States.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9431; (P) 0.9470; (R1) 0.9505; More...

No change in USD/CHF's outlook. Rebound from 0.9186 is still in progress but it's seen as a corrective move. Hence, we'd expect strong resistance from 0.9626 key fibonacci level to limit upside. On the downside, break of 0.9432 support will indicate near term reversal and completion of rebound from 0.9186. In this case, intraday bias will be turned back to the downside for retesting 0.9186 low. However, sustained break of 0.9626 will be another evidence of larger reversal. In this case, further rise would be seen to next fibonacci level at 0.9900.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Feb | 5.70% | 0.20% | 0.00% | |

| 23:01 | GBP | GfK Consumer Confidence Mar | -7 | -10 | -10 | |

| 23:50 | JPY | Retail Trade Y/Y Feb | 1.60% | 1.70% | 1.60% | 1.50% |

| 07:00 | CHF | KOF Leading Indicator Mar | 106 | 107.2 | 108 | 108.4 |

| 07:55 | EUR | German Unemployment Mar | -19K | -15K | -22K | -23K |

| 07:55 | EUR | German Unemployment Claims Rate Mar | 5.30% | 5.30% | 5.40% | |

| 08:30 | GBP | Mortgage Approvals Feb | 64K | 66K | 67K | |

| 08:30 | GBP | Money Supply M4 M/M Feb | -0.40% | 1.30% | 1.50% | |

| 08:30 | GBP | Current Account Balance Q4 | -18.4B | -23.7B | -22.8B | |

| 08:30 | GBP | Index of Services 3M/3M Jan | 0.60% | 0.60% | 0.60% | |

| 08:30 | GBP | GDP Q/Q Q4 F | 0.40% | 0.40% | 0.40% | |

| 12:00 | EUR | German CPI M/M Mar P | 0.40% | 0.50% | 0.50% | |

| 12:00 | EUR | German CPI Y/Y Mar P | 1.60% | 1.70% | 1.40% | |

| 12:30 | CAD | GDP M/M Jan | -0.10% | 0.10% | 0.10% | 0.20% |

| 12:30 | CAD | Industrial Product Price M/M Feb | 0.10% | 0.40% | 0.30% | 0.40% |

| 12:30 | CAD | Raw Materials Price Index M/M Feb | -0.30% | 2.80% | 3.30% | 3.40% |

| 12:30 | USD | Personal Income Feb | 0.40% | 0.40% | 0.40% | |

| 12:30 | USD | Personal Spending Feb | 0.20% | 0.20% | 0.20% | |

| 12:30 | USD | PCE Deflator M/M Feb | 0.20% | 0.20% | 0.40% | |

| 12:30 | USD | PCE Deflator Y/Y Feb | 1.80% | 1.70% | 1.70% | |

| 12:30 | USD | PCE Core M/M Feb | 0.20% | 0.20% | 0.30% | |

| 12:30 | USD | PCE Core Y/Y Feb | 1.60% | 1.60% | 1.50% | |

| 12:30 | USD | Initial Jobless Claims (MAR 24) | 215K | 231K | 229K | 227K |

| 13:45 | USD | Chicago PMI Mar | 62 | 61.9 | ||

| 14:00 | USD | U. of Mich. Sentiment Mar F | 102 | 102 | ||

| 14:30 | USD | Natural Gas Storage | -86B |