Sample Category Title

Dollar Treads Water Ahead Of US Inflation Data

Here are the latest developments in global markets:

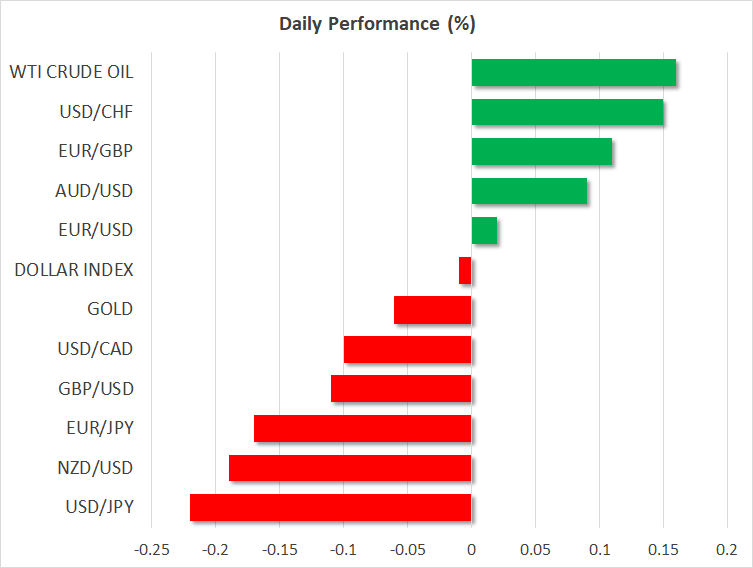

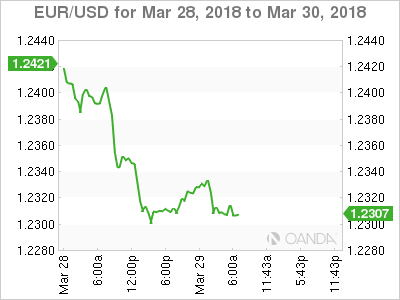

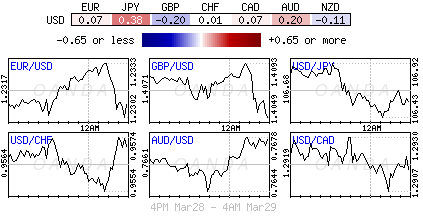

FOREX: The US dollar traded higher against a basket of currencies yesterday, with dollar/yen surging 170 pips in a single day, though its rally is starting to lose steam again in the European session (-0.19%). Today, dollar traders are likely to turn their attention back to the economic calendar and the core PCE index for February. Euro and sterling were sold-off against the US dollar for the second day in a row. Euro/dollar was trading marginally lower by 0.03% during today’s European session, while pound/dollar moved down by 0.06% and retested its opening price again. Antipodean currencies were mixed, with aussie/dollar up at 0.7667 (+0.10%), but kiwi/dollar down at 0.7195 (-0.21%). Dollar/loonie was last seen at 1.2912 (-0.07%).

STOCK: European stocks moved higher after the sharp losses in technology companies yesterday. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.47% and 0.74% respectively. The German DAX 30 rose by 0.74%, the French CAC 40 gained 0.60%, the Italian FTSE MIB traded higher by 0.49% and the UK’s FTSE 100 climbed by 0.37%. Asian equities closed higher, while futures tracking the US indices were pointing to a positive open after two consecutive red days.

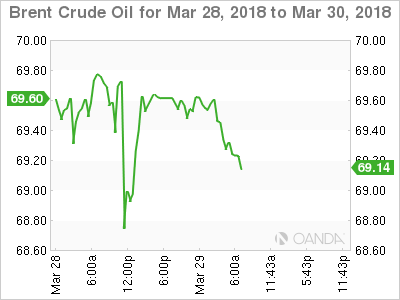

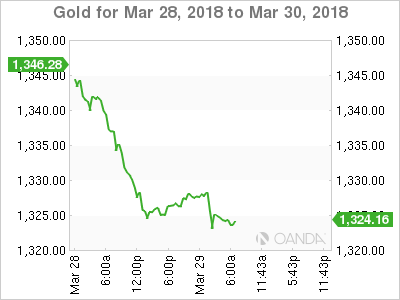

COMMODITIES: In energy markets, West Texas Intermediate (WTI) crude oil and London-based Brent crude oil were mixed. WTI was up by 0.11% at $69.45 per barrel, while Brent was down by 0.29% at $69.33. Moreover, copper jumped above the $3.00 level, rising by 0.27%. Gold held steady on Thursday (-0.03%), a day after posting its biggest one-day fall in the last 9 months, as tensions over North Korea and trade eased, while the US dollar gained.

Day ahead: US and German inflation prints in the limelight, Canadian GDP also eyed

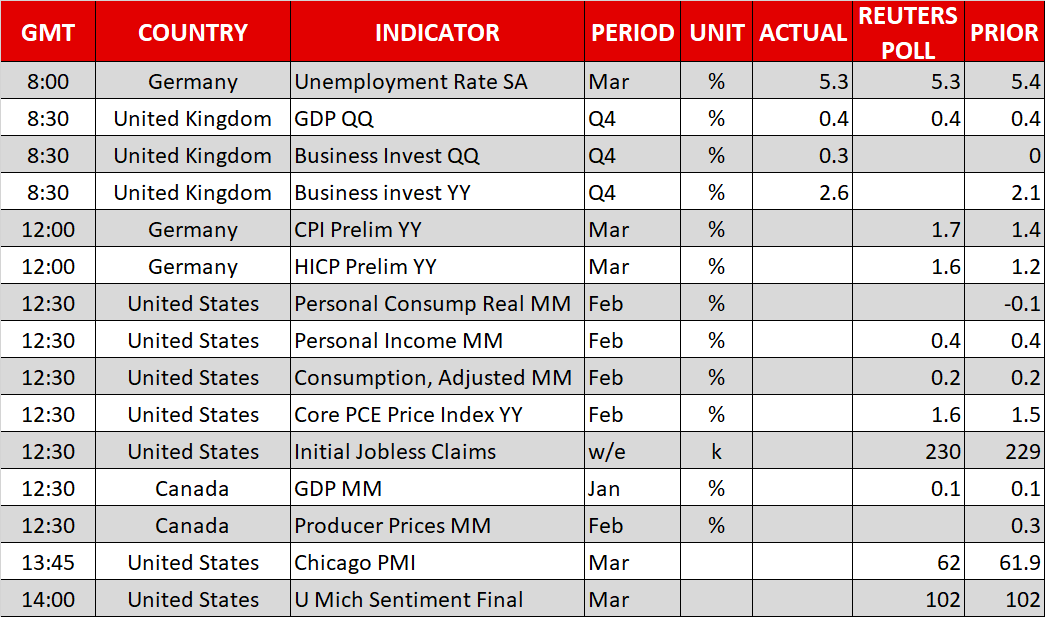

The most significant data release will be the US core Personal Consumption Expenditure (PCE) index for February, the Fed’s favorite inflation measure. It will be released alongside personal income and spending figures for the same month, at 1230 GMT. The forecast is for the core PCE rate to tick up to 1.6% in yearly terms, from 1.5% previously. Meanwhile, both income and spending are projected to have risen at the same pace as in the previous month, at 0.4% m/m and 0.2% m/m respectively.

Regarding potential surprises, note that out of the 39 institutions submitting their forecasts to the Thomson Reuters system, 22 anticipate the core PCE rate to rise to 1.6%, while 16 of them see the rate remaining at 1.5%. Only one expects a pick-up to 1.7%. Thus, the risk appears to be a lower-than-expected reading, as opposed to a higher one like 1.7%. As for spending and income, one is a little cautious to trust the forecasts for unchanged rates considering that retail sales fell for a third straight month in February, pointing to a slowdown in spending, while average hourly earnings slowed. The probability for a Fed rate hike in June is currently 74% and in case these data disappoint, that number could decline, causing the dollar to give back some of its latest gains. Conversely, strong prints could add fresh fuel to the greenback’s recovery.

US initial jobless claims for the week ended March 23, and the Chicago PMI for March are also due out.

At the same time as the US figures, Canada will release its GDP data for January. Economic growth is expected to have held steady at 0.1% month-on-month. While this print could trigger some volatility in the loonie, especially in case of a deviation from expectations, the currency’s broader direction is likely to be dictated primarily by NAFTA updates.

Half an hour ahead of the US and Canadian data, at 1200 GMT, Germany will release its preliminary CPI figures for March. Expectations are for the nation’s EU-harmonized inflation rate to rise to 1.6% in yearly terms, from 1.2% prior. Germany’s regional CPI prints have already been released, and they support the forecast for an increase in the nationwide rate.

In energy markets, the Baker Hughes oil rig count at 1700 GMT will provide a fresh indication of whether US crude production continues to soar.

As for the speakers, Philadelphia Fed President Patrick Harker (non-voter) will deliver remarks at 1700 GMT.

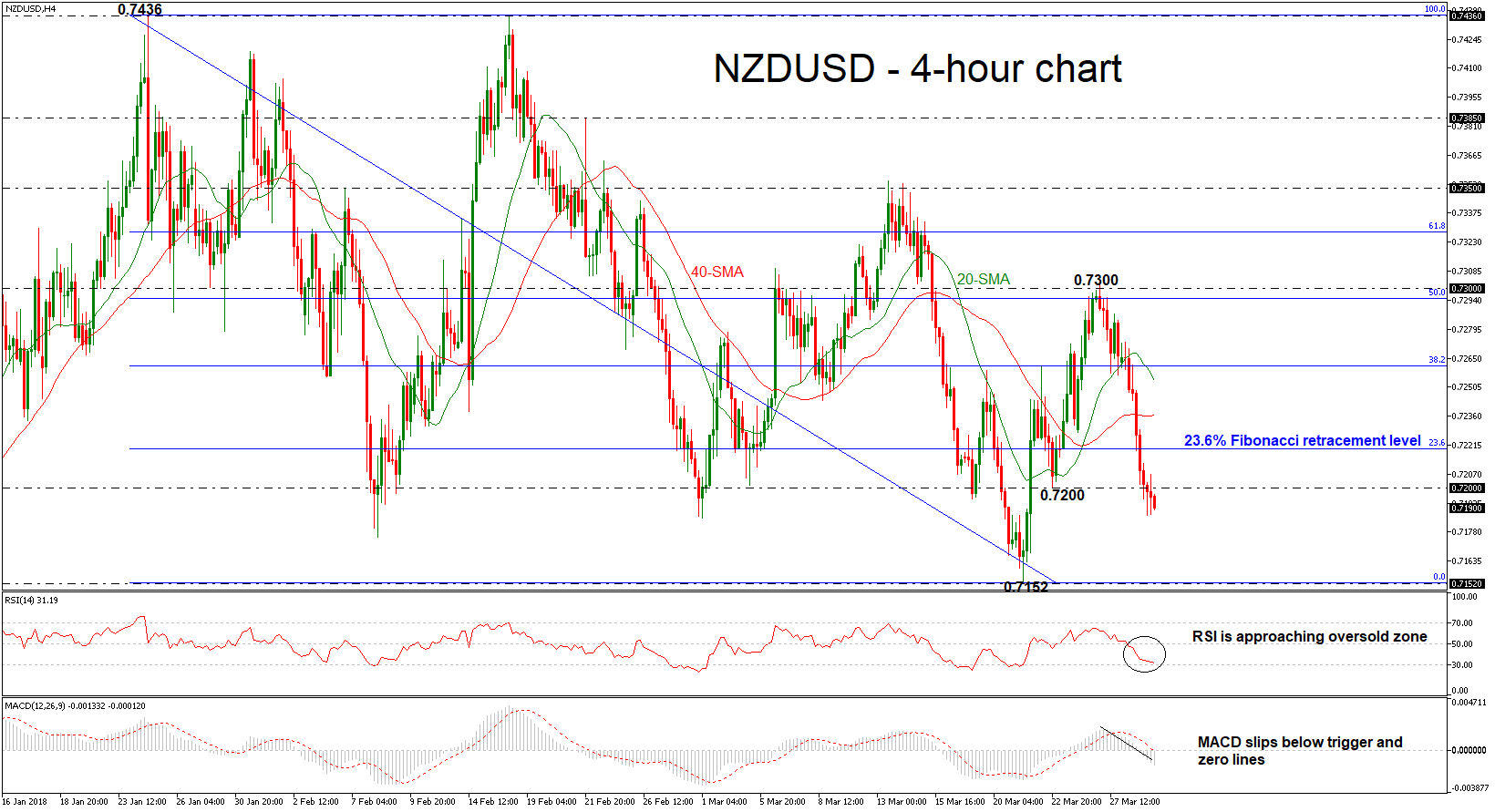

NZDUSD Extends Downtrend After Breaking Below 0.7200

NZDUSD turned increasingly bearish after a bounce off the 0.7300 handle on Tuesday, breaking below the 0.7200 strong psychological level yesterday.

Today the pair continues to head lower, but the RSI in the 4-hour chart is not far away from oversold levels therefore upside movements cannot be excluded yet in the short-term. The MACD gives additional bearish signals, as the index is stretching downwards into negative territory.

If prices extend lower, the next support could come around the 2-month low of 0.7152. A break below this level could endorse the bearish bias and open the way towards the 0.7100 key-level.

However, if prices rebound, the focus could shift to the 23.6% Fibonacci retracement level of 0.7220 of the downleg from 0.7436 to 0.7152. Above this level, the next target could come in the region within the 20- and 40-period simple moving averages (SMAs), this is between 0.7237 – 0.7254.

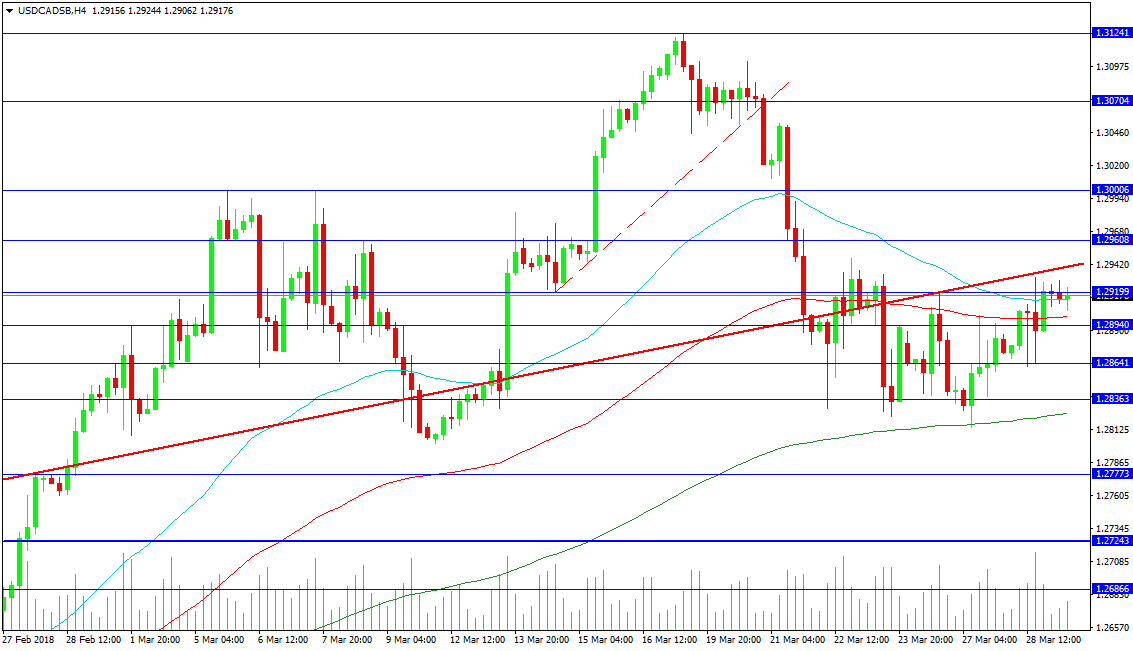

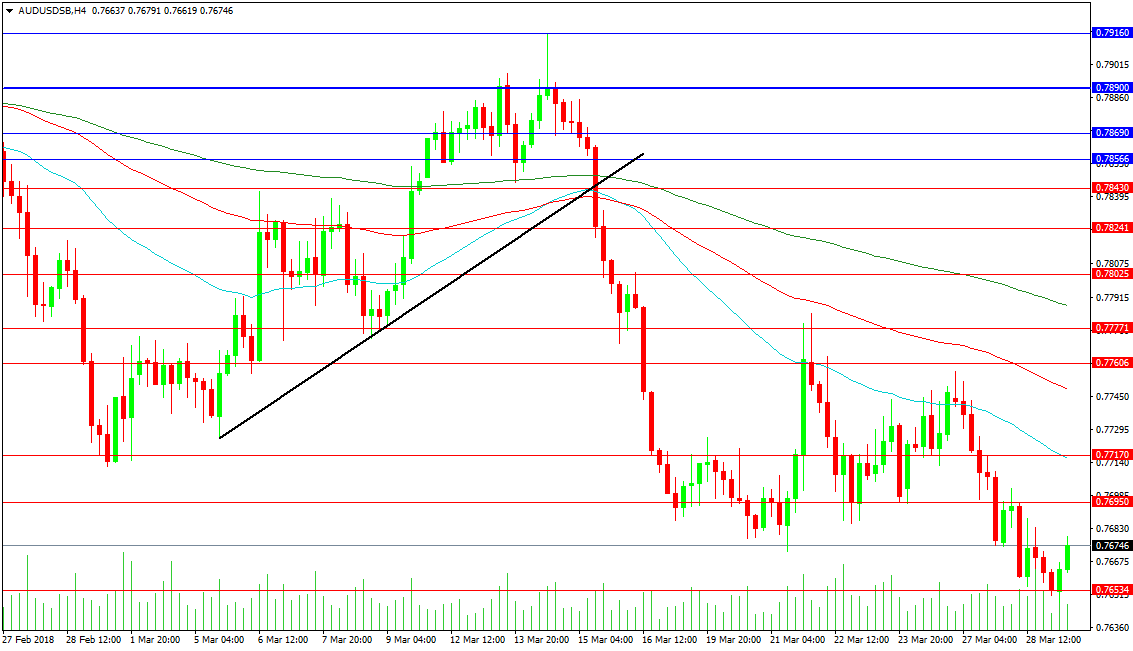

Forex Analysis: USDCAD And AUDUSD

Canadian GDP will be released later today showing slight growth. The USDCAD pair has slipped into a sideways pattern below the area of the red trend line, shown here on the 4-hour chart. This trend line currently represents resistance and is located at the 1.29395. The 50-period MA is at 1.29148, with the 100-period below at 1.29010. The moving averages are playing a role, with the 100 and 200 both being used recently.

The 200-period MA was used as support and created the low from the 27th at 1.28141 but has since moved up to 1.28254. Further support is found at 1.27773 and 1.26866.

Resistance would be tested on a break above the trend line, which was confirmed on Monday. The 1.29608 level has been used as support and resistance and is an outpost of the 1.30000 level. The previous highs are found above 1.30704, at the 1.31241 level.

AUDUSD

This pair has come under pressure, testing and breaking through the 0.77000 level. The moving averages on the 4-hour chart are falling and have been used as resistance. Support is found at 0.76534 and the low from overnight at 0.76422. Below this level, 0.76000 comes into play, with 0.75378 and 0.75000 below. This level is just above the November 2018 low of 0.74990.

Resistance at the 50-period MA is at 0.77170, with the 100-period MA at 0.77484. The 200-period MA is falling through 0.77876, with resistance at the 0.78000 level close above. A reversal above that level would suggest a push higher is on the cards, with 0.78430 a hurdle on the way to targets at 0.78900 and 0.79160.

Sterling Unimpressed By GDP Data, Dollar Steady

Sterling was unsettled and vulnerable on Thursday, after reports showed that Britain remains the world's slowest growing major economy.

The Office for National Statistics confirmed that gross domestic product reached 0.4% in the final quarter of 2017, slowing from growth of 0.5% in Q3. Although the ONS revised estimates for full year growth in 2017 to 1.8% from 1.7%, this still remains the lowest growth rate since 2012. Sterling is likely to remain depressed as investors digest the GDP figures, with a strengthening Dollar fueling further downside on the GBPUSD.

Taking a look at the technical picture, GBPUSD remains under pressure on the daily charts. Sustained weakness below the 1.4100 could invite a decline towards 1.4000.

Markets mixed ahead of Easter break

Global equity markets may struggle for direction today as investors stroll to the sidelines ahead of the long Easter weekend.

Asian stock markets were mostly mixed in thin trade, as a tech-fuelled selloff on Wall Street overnight weighed on investor sentiment. Although European stocks opened slightly higher, gains could be limited as the holiday mood kicks in. With Wall Street still at the mercy of a painful selloff in the technology sector, further losses could be on the cards this afternoon. Although fears of a full blown global trade war have receded, this has been replaced with growing concerns over a regulatory crackdown on technology firms. The uncertainty and market anxiety could expose stock markets to downside risks.

Dollar holds gains post US Q4 GDP

The Dollar held tightly onto its gains against a basket of currencies on Thursday, after fourth quarter US GDP figures were revised up to 2.9% from 2.5% in the previous session.

This upwards revision to the fourth quarter growth boosted sentiment towards the US economy and stimulated expectations over the Federal Reserve adopting a slightly more aggressive approach on rate hikes this year. Speculation around higher rates have injected Dollar bulls with a renewed sense of confidence, elevating the Dollar against its major counterparts.

Taking a look at the technical picture, the Dollar Index is slowly building momentum on the daily charts. The candlesticks are in the process of crossing above the 20 Simple Moving Average, while the MACD is showing early signs of trading to the upside. Prices have breached above the 90.00 resistance level which could encourage an incline higher towards 90.45. Alternatively, a failure for prices to keep above 90.00 may result in a decline lower towards 89.50.

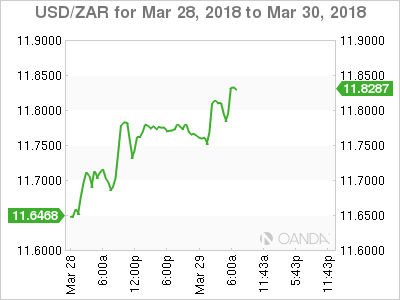

Rand slips on SARB rate cut

South Africa's Rand extended its losses against the Dollar during early trading on Thursday, following yesterday's interest rate cut by the South African Reserve Bank (SARB).

There has been a recovery in the Dollar strength against many of its different counterparts over the past 24 hours, so it is possible that the Dollar's recovery could be a culprit behind some of the current Rand weakness. Comments from SARB Governor Lesetja Kganyago that the Rand is now ‘somewhat' overvalued, is likely to provide a scenario where it may be difficult for the Rand to advance any further than the 4.87% it has already made year-to-date.

Focusing purely on the technical picture, an appreciating Dollar could push the USDZAR towards 11.830 in the near term.

Philadelphia Fed Harker expects three hikes this year on “some firming of inflation”

Philadelphia Fed President Patrick Harker said in a WSJ interview that he now expects three Fed rate hike this year. Harker is seen as on the dovish side of the spectrum as he previously projected just two hikes in 2018.

He pointed to "some firming of inflation" as he reason for the upgrade is his own forecast. He also clarified that he placed more emphasis on inflation than fiscal policy.

And to us, this could be a hint on a major difference between Fed's hawks and doves. The hawks anticipate the growth and inflation impact of the tax cut and other policies. Meanwhile, seeing is believing for the doves.

Nonetheless, Harker also sounded cautious on trade tensions. He noted that risk of increasing trade tariffs as a source of uncertainty for both economic projections and monetary policy.

US Data In Focus As Stocks Recover

- Futures Stage Small Recovery After Another Rough Week;

- Inflation, Income and Spending Figures Eyed;

- Cryptocurrencies Tumble Again as Social Media Companies Fight Back.

Futures Stage Small Recovery After Another Rough Week

Equity markets in Europe are continuing to stage a small recovery on Thursday and US futures are seeing a similar improvement, following what has been a tough week for stocks, particularly in the tech sector.

Trade war fears may be gradually easing with the US and China showing an interest in finding a solution to the dispute but those concerns have simply been transferred to the tech sector, with the Facebook scandal raising significant questions about regulation in the industry. As of yet, only Facebook has been caught up in the scandal and if that remains the case, the sell-off may be short-lived.

However, as we’ve seen with scandals in other industries – banks and automakers for example – these cases quite often aren’t unique. Should this turn out to be the case, the sector could come under further pressure and given its size, that could easily drag the rest of the market with it, as we’ve seen recently. With the Dow back in correction territory, markets still look vulnerable to more losses.

Inflation, Income and Spending Figures Eyed

On a brighter note, the economy is continuing to perform strongly, as noted by yesterday upward revision to fourth quarter GDP. With tax reform providing an additional tailwind for the economy, the numbers in the coming months will be extremely interesting and could force the Federal Reserve into action more than it is currently planning.

Its macro-economic projections last week already included upward revisions to growth and inflation expectations and included an extra rate hike next year than was previously forecast. I don’t think it would take much for that to be brought forward to this year, particularly if inflation and wages pick up more than is currently expected. The inflation, income and spending data today will therefore be of particular interest, particularly the former as it’s the Fed’s preferred measure.

Cryptocurrencies Tumble Again as Social Media Companies Fight Back

It’s been another bad day for cryptocurrencies, with bitcoin slipping another 5% to trade near the lows hit a couple of weeks ago. Not too long ago it was the prospect of heavy-handed regulation or outright bans that was rocking the cryptocurrency market, now it’s social media and other internet platforms banning advertising that’s weighing on prices.

It seems that a lack of understanding about how to manage the situation and prevent fraudsters from gaining access to the public is encouraging these platforms to impose blanket bans in some cases in order to avoid being associated with them. At some point I imagine that will change and only those that are untrustworthy will be targeted but for now, the news is delivering another blow to the industry and dragging down prices, although compared to the start of last year, for example, they’re still very elevated.

Dollar Holds Gains As Trade War Fears Recede

Thursday March 29: Five things the markets are talking about

As we close out quarter and month-end trading, capital market volumes remain subdued, with many investors preferring to wrap up ahead of the Easter holidays.

All week, investors have been liquidating their tech stocks, selling some of the biggest winners from a 'bull' market that's been tested by rising interest rates and an unpredictable Trump administration.

This morning, Euro equities have climbed after a mixed session in Asia, while U.S futures are rallying as markets limp to the end of turbulent quarter.

Treasury yields have steadied as the 'big' dollar heads a tad higher, while the pound is under pressure.

Elsewhere, crude oil prices have rebounded from its longest losing streak in four-weeks, and this despite a build up in U.S stockpiles. Gold remains on the back foot, extending yesterday's decline.

On tap: U.S personal income and spending data for February are due to be released at 08:30 am EDT, along with Canadian GDP.

1. FANG stocks pressure equity markets

FANG (Facebook, Amazon, Netflix and Google) names are under significant pressure. It's no surprise to see trading remaining choppy with the holiday/month/quarter-end calendar seen as a likely volatility inducer. The VIX has lifted back towards 23.

In Japan, the Nikkei share average rallied overnight, helped by gains in domestic-demand stocks. The Nikkei ended +0.6% higher, while the broader Topix closed +0.3% up.

Down-under, Aussie shares fell on Thursday, hitting their lowest close in more than five-months; with material stocks leading the losses as a slide in iron ore prices hurt sentiment. The S&P/ASX 200 index fell -0.5%. In S. Korea, the Kospi closed out in similar fashion as the Nikkei, up +0.6%.

In Hong Kong, stocks ended higher amid perceived progress on N. Korea issues, though caution lingered as investors continued to watch the development of China/U.S. trade spat. At close of trade, the Hang Seng index closed +0.2% up, while the Hang Seng China Enterprises index was flat.

In China, stocks reversed earlier losses to end higher overnight, as investors hunted for bargains. At the close, the Shanghai Composite index was up +1.2%, while the blue-chip CSI300 index was up +1.3%.

In Europe, regional indices are rebounding after yesterday's losses following a raft of inflation data out of Germany and growth data in the U.K.

U.S stocks are set to open in the 'black' (+0.3%).

Indices: Stoxx600 +0.4% at 370.6, FTSE +0.5% at 7079, DAX +0.6% at 12015, CAC-40 +0.5% at 5157, IBEX-35 +1.0% at 9647, FTSE MIB +0.5% at 22440, SMI -0.2% at 8744, S&P 500 Futures +0.3%

2. Oil prices rise as OPEC seen continuing supply cuts, gold unchanged

Oil prices have rallied on Thursday, as OPEC and other suppliers look set to continue withholding output for the rest of the year and potentially into 2019.

Brent crude futures are at +$69.76 per barrel, up +23c, or +0.3%, while U.S WTI crude futures are at +$64.63 a barrel, up +25c, or +0.4% from Wednesday's close.

OPEC together with a group of non-OPEC producers led by Russia started cutting output in 2017 to rein in oversupply and prop up the market. There are rumblings this week that OPEC and its allies are keen to keep this deal on cutting production for the rest of 2018.

Despite this, Brent remains below the psychological +$70 handle and WTI under +$65 per barrel, weighed by rising crude inventories and production in the U.S.

Note: EIA data yesterday showed that commercial U.S. crude inventories rose by +1.6m barrels in the last week to +429.95m barrels.

In China, Shanghai crude oil futures opened their morning session down nearly -2%, pushing the new market near to parity with U.S. prices, before closing at 409.7 yuan ($65.18) per barrel.

Ahead of the U.S open, gold prices are holding steady this morning, a day after posting its biggest one-day percentage fall in nearly 9-months, as tensions over N. Korea and global trade eased. Spot gold is unchanged at +$1,325.16 per ounce, after hitting a low of +$1,322.50 earlier in the session, it's lowest since March 21.

Note: The 'yellow' metals prices dropped -1.5% on Wednesday, its biggest one-day percentage decline since July 3, 2017.

3. Sovereign yields remain tight

Narrow ranges across Bunds and most Euro and U.S spreads amid lower volumes, despite the U.S 's record supply, suggest that the fixed income market has already entered Easter mode.

Note: In total and by week's end, the U.S Treasury will have auctioned approximately +$294B of bills and notes, its largest slate of supply ever.

Ahead of the U.S open, the yield on 10-year U.S Treasuries has dipped -1 bps to +2.78%, the lowest in more than seven-weeks. In the U.K, the 10-year Gilt yield has advanced +1 bps to +1.366%, the biggest gain in more than a week, while in Germany, the 10-year Bund yield increased + 1bps to +0.51%, the first advance in more than a week.

Yesterday, the South African Reserve Bank (SARB) cut interest rates by an expected -25bps to +6.50%. The SARB said the inflation outlook has improved and that “one increase of +25 bps is now implied” instead of three increases of +25 bps by the end of 2019, as previously indicated. South African policy makers expect inflation at +5.2% in 2019, instead of +5.4% previously. For 2018, the central bank hasn't changed its forecasts and still sees inflation at +4.9%.

4. Dollar confined to trading ranges

It's no surprise to see FX price action uninspired ahead of the long holiday weekend and this despite a plethora of European economic releases.

EUR/USD (€1.2309) hovers under the psychological €1.24 level as various German individual states release their March CPI data – most have come in below expectations – dealers are waiting for the overall German inflation data print due out later today. The regional CPI prints reinforce some of the recent cautious remarks by ECB officials on making any abrupt changes in its policy and giving more time to decide about its future moves until summer period.

Sterling is under pressure from quarter-end selling, and seems to be unmoved by this morning's U.K GDP data (unchanged at +0.4% q/q, but confirmed its slowest annual pace in eight years at +1.4% y/y). GBP/USD is trading roughly at the same level it was before the data release, at £1.4053, down -0.2% on the day

5. German jobless rate hits record low

Data in Europe this morning showed that Germany's jobs boom continued this month, as jobless claims fell by more than expected and the unemployment rate hit a new record low.

German jobless claims dropped by -19K in March. The market was forecasting a decline of -17.5K.

This has led to Germany's adjusted jobless rate easing to +5.3% from +5.4% in February, which marks the lowest rate since the beginning of the data series in January 1992.

Analysts expect Germany's jobs market to remain tight this year.

Fundamentals Impacting Bitcoin, Ethereum, Ripple And Other Cryptos

G20 has started formulating regulations over cryptocurrencies

A blockchain funding centre was scrapped in China

Ethereum remains optimistic for two reasons

Bitcoin is under selling pressure again and chances of its recovery are looking slim.The price has traded above the 8000 today but for a brief moment. Ever since, there has been more selling pressure than buying. Last week’s negativity around Bitcoin hasn’t faded away, and there isn’t any significant improvement in the bull power. Bitcoin, from the weekly graph, has slid significantly, since the tech giants’ ban on ICOs.

This is not to say that there hasn’t been any good news for the cryptocurrencies. G20 has started formulating regulations over cryptocurrencies, setting a well-regulated environment for economic superpowers to enter the market. This is great in the long term. However, this development has very limited impact on the price. Having said that traders have also acknowledged how blockchain and crypto hotspots are now mainly in non-G20 countries, e.g. Singapore, Gibraltar, and Malta. Hence, in the long term, with G20 forming a healthy framework for cryptocurrencies maybe a key driving force in crypto-growth. Other optimistic news includes BOE’s willingness to try out distributive ledger technologies, indicating optimism in blockchain and the new tech. The impact has been limited on Bitcoin prices despite the BOE case marked a milestone in governmental blockchain adoption.

Yet, pessimistic news still remain. A blockchain funding centre was scrapped in China as its regulations created obstacles. The news caused traders to dump Bitcoin as it further reinsured China’s negativity and reluctance in using blockchain-related products. China’s future in blockchain remains misty. Danske, Denmark’s largest bank, banned crypto trading, but remains optimistic over blockchain. The ban, like the China blockchain funding center ban, created short run disruption. However, we believe such news would offset the adverse price action for the cryptocurrencies, as Danske showed willingness and optimism in blockchain and the future crypto market if its becomes more transparent. These all pave the way for a long-term crypto and blockchain future positively.

In Ethereum, further radical changes, such as rental fees and sharding is creating more uncertainty in the market. Yet, as proceeds consolidate and improve, Ethereum remains optimistic for two reasons. Firstly, such radical changes improve Ethereum’s long term functions. Second, most ICOs are designed according to Ethereum’s blockchain, and ICO growth correlates to Ethereum growth.

In Ripple, prices didn’t change significantly although Uphold, a platform with $3 billion worth of transactions, enabled members to purchase XRP with zero fees.

Cryptocurrencies are also marking positive growth amongst huge corporations, like Ford. They are now investing and looking into cryptocurrency creation. In essence, the system allows drivers to sell their time by choosing to move to a slower lane, accepting payment from vehicles that don’t want to overtake them. This creates positivity in blockchain, and is most reflected in Bitcoin, being a key indicator to overall market confidence in blockchain

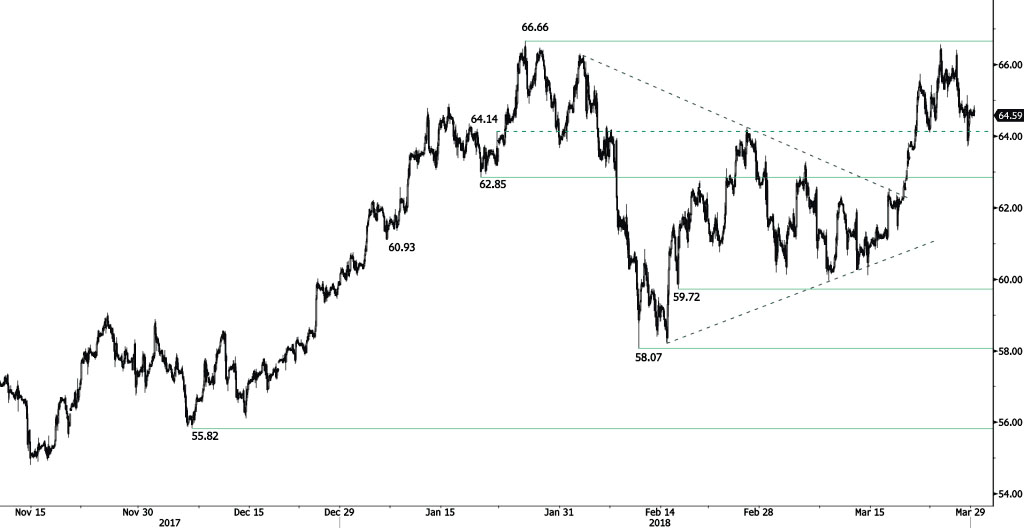

CRUDE OIL Bouncing Off

Crude oil continues its recovery phase after reaching 63.72 low, approaching the 65.20 range. Silver is currently contained between hourly support and resistance at 62.85 (19/01/2018 low) and 66.66 (25/01/2018 high). The technical structure suggests short-term upward moves.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

SILVER Trading Below 16.26

Silver selling pressures continue after trading at 16.80, heading along 16.23. Silver is currently contained between hourly support and resistance given at 16.03 (18/12/2017 low) and 16.98 (15/02/2018 high). The short-term technical structure suggests further decreasing moves.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. The pair is trading below its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).