Sample Category Title

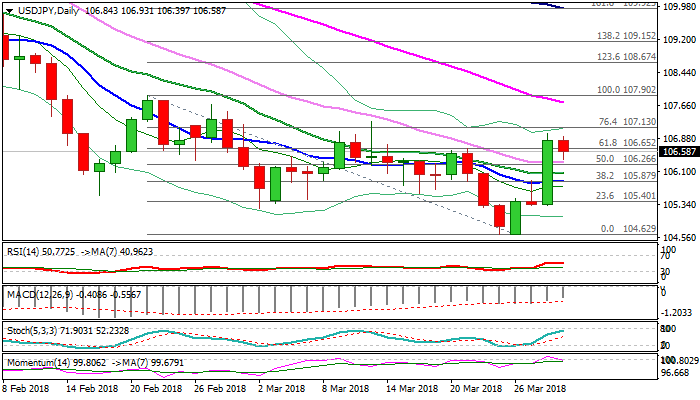

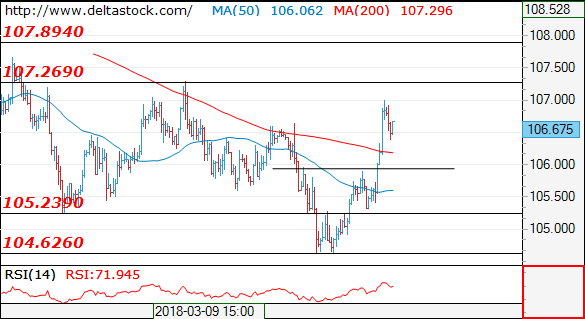

USDJPY Consolidates Under Fresh Recovery High, Bullish N/T Structure To Remain Intact While Above Broken 30SMA

The pair is consolidating under fresh recovery high at 107.01 on Thursday, after previous day’s strong rally when dollar was up 1.5% against yen, on the biggest one-day rally s since 15 June 2017.

The structure on daily chart improved after Wednesday’s rally as the price broke above a cluster of MA’s and another bullish signal was generated on close above 106.65 (Fibo 61.8% of 107.90/104.63 descend, which keeps near-term focus at the upside, but the sentiment could be soured by weakening momentum studies.

Corrective easing is expected to hold above broken 30SMA (106.34), former pivotal barrier, now strong support, to keep fresh bulls intact. Sustained break above psychological 107 barrier would open way for test of 107.29 (13 Mar high) and would expose key barrier at 107.90 (21 Feb high/base of falling daily cloud).

Conversely, xtension below 30SMA would sideline immediate bears, while return below broken 10SMA (105.89) is needed to neutralize and signal lower top at 107.01.

Res: 107.01, 107.13, 107.29, 107.90

Sup: 106.34, 106.07, 105.89, 105.32

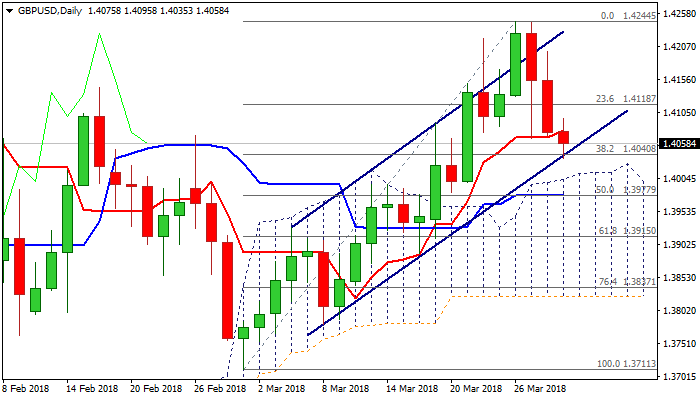

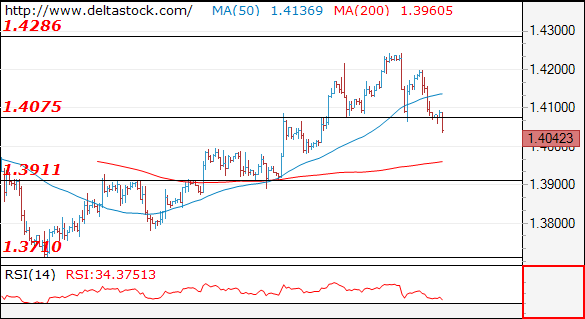

GBPUSD – Bears Tested Strong Support At 1.4040, UK GDP/CA Data In Focus For Fresh Signals

Cable extends lower in early hours of European session on Thursday after consolidating losses of past two days in Asia.

Fresh weakness cracked strong support at 1.4040 (bull-channel support line/Fibo 38.2% of 1.3711/1.4244 rally) and eyes next pivot at 1.4000 (top of thick daily cloud/psychological support). Pullback from double-top at 1.4244 weakened near-term structure, increasing risk of deeper correction.

Batch of UK data are due today and closely watched for fresh direction signal. Focus is on UK Q4 GDP and current account. Gross domestic product is forecasted to remain unchanged in Q4 at 0.4% (q/q) and annualized figure at 1.4%.

Current account deficit is expected to widen (-24B f/c vs -22.8B in Q3) and with than expected figures expected to put sterling under increased pressure for acceleration through 1.4040/00 pivots which could extend towards 1.3915 (Fibo 61.8% of 1.3711/1.4244).

Conversely, cable could bounce and signal an end of corrective phase if UK data beat forecasts.

Broken 10SMA caps today's action for now and marks initial resistance at 1.4085, with break above needed to ease immediate bearish pressure.

Res: 1.4085, 1.4118, 1.4163, 1.4200

Sup: 1.4040, 1.4000, 1.3970, 1.3915

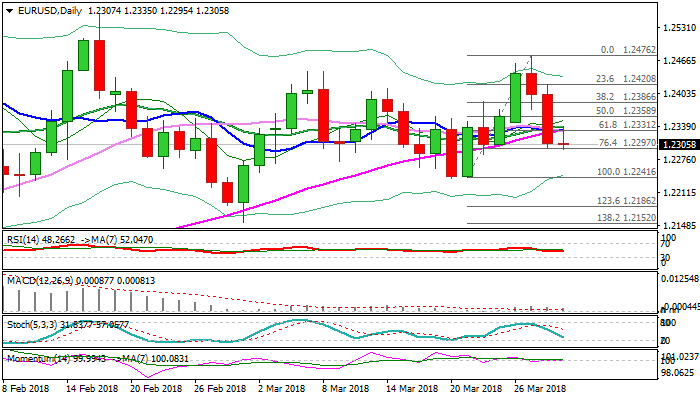

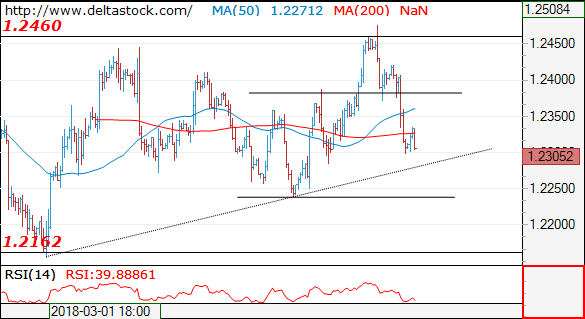

EURUSD Stands At The Back Foot After Heavy Looses On Wednesday, Risks Bearish Extension Towards Key Support At 1.2241

The Euro traded within 30-pips range on in Asia / early Europe on Thursday, consolidating after previous day's strong fall.

Extension of pullback from 1.2476 (Tuesday's peak) found footstep at 1.2300 (Fibo 76.4% of 1.2241/1.2476 upleg) but generated strong bearish signal on close below pivots at 1.2370 (daily cloud top) and 1.2331 (Fibo 61.8% / converged 10/55SMA's) which now act as resistance and keeps recovery attempts limited.

Daily techs are turning in bearish mode as MA's are in bearish setup and 14-d momentum is holding at the border of negative territory.

Bears could extend towards key support at 1.2241 (20/21 Mar double-top) while 1.2331 barrier holds.

Better than expected German jobs data (Mar unemployment change -19K vs -15K f/c and unemployment rate 5.3% from 5.4 in Feb) did not show significant impact.

Res: 1.2331, 1.2359, 1.2370, 1.2421

Sup: 1.2295, 1.2260, 1.2241, 1.2200

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2305

The slide through 1.2380 confirms the bearish bias, for a break through 1.2280 dynamic support, towards 1.2240 low. Key resistance is projected at 1.2380.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2380 | 1.2560 | 1.2280 | 1.2160 |

| 1.2460 | 1.2560 | 1.2240 | 1.2090 |

USD/JPY

USD/JPY

Current level - 106.67

The bias is positive after the break though 105.90, for a rise towards 107.90 zone. Key support is projected at 105.90.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 107.00 | 108.30 | 105.90 | 105.20 |

| 107.90 | 110.40 | 105.20 | 104.60 |

GBP/USD

GBP/USD

Current level - 1.4042

With the recent break through 1.4075 support the outlook remains bearish, for a slide towards 1.3910 zone. Initial intraday resistance lies at 1.4130.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4130 | 1.4280 | 1.3980 | 1.3710 |

| 1.4240 | 1.4340 | 1.3910 | 1.3620 |

Dollar Stages Comeback As Yen Crumbles, US Core PCE Index Eyed

Here are the latest developments in global markets:

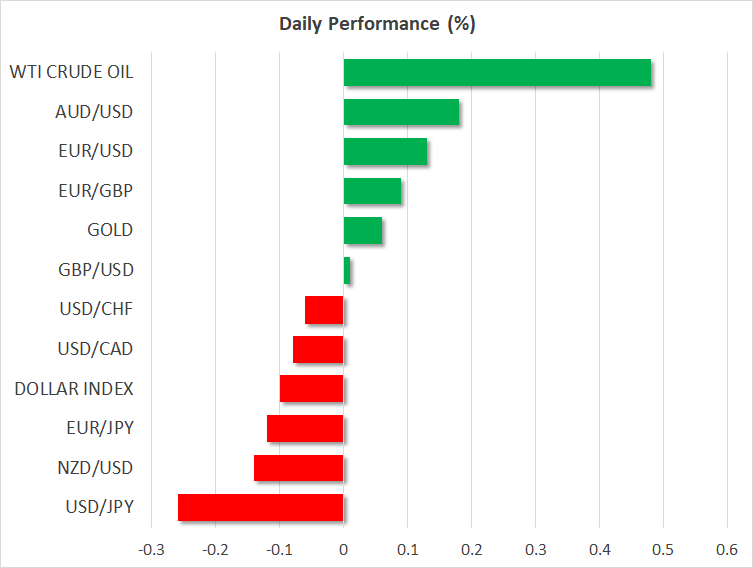

FOREX: The dollar index declined 0.1% today, giving back some of the significant gains it posted yesterday when it recorded its biggest daily surge in six months. Meanwhile, the yen was losing ground as geopolitical tensions appeared to ease further, and amid increased flows in light of the Japanese fiscal year ending tomorrow.

STOCKS: US markets closed lower again, though the magnitude of the declines was much smaller compared to recent days. The tech-heavy Nasdaq Composite led the charge down, shedding 0.85% of its value, dragged by the likes of Tesla (-7.67%), Netflix (-4.96%) and Amazon (-4.38%). The S&P 500 fell by 0.3%, while the Dow Jones was only 0.04% lower. Futures tracking the Dow, S&P, and Nasdaq 100 are all flashing green currently, pointing to a higher open today. Asia was a different story, with Japan's Nikkei 225 and Topix rising by 0.6% and 0.26% respectively, while Hong Kong's Hang Seng gained 0.7%. In Europe, futures tracking all the major benchmarks are signaling these indices could open higher today.

COMMODITIES: In energy markets, WTI crude and Brent gained 0.5% and 0.6% respectively, both recouping the losses they posted yesterday after the EIA data surprisingly showed a build in stockpiles, instead of a small drawdown that was expected. News yesterday that more OPEC producers are willing to extend the production cuts into 2019 likely boosted overall sentiment in oil markets. In precious metals, gold is marginally higher today, after having declined significantly in the previous session. The yellow metal's underperformance is probably owed to a combination of a stronger US dollar, as well as a reduction in geopolitical risks that likely hurt demand for the safe haven.

Major movers: Dollar surges, yen crumbles as geopolitical risk premium declines

The US dollar index rose by more than 1.4% yesterday, without any clear fundamental catalyst behind the surge. That said, it is not unusual for such moves to occur before the end of the month – and in this case the quarter too – as fund managers rebalance their portfolios and cover some of their prior short-dollar positions. An upward revision in the final estimate of US GDP for Q4 may have helped the move as well.

The dollar index is 0.1% lower today, currently trading near the 89.95 level, after having touched 90.14 yesterday. Euro/dollar was 0.1% higher, recovering part of its recent losses, while sterling/dollar was practically flat, last seen near 1.4080.

Elsewhere, the yen lost ground yesterday. The move was likely aided by signs of progress on the geopolitical front – with JPY being a safe haven asset, it tends to gain when uncertainties are high, but tumble when tensions decline. Following headlines that North Korea is considering denuclearization, risk sentiment was boosted further by news the regime will seek diplomatic talks with Japan. This likely enhanced speculation for a prudent and peaceful resolution to tensions, diverting flows out of safe assets like the yen and gold. Yen traders should remain vigilant though, as the Japanese fiscal year ends tomorrow. This suggests the currency could continue to experience heightened volatility, as some investors repatriate cash, and as others place fresh bets for the new financial year.

Dollar/loonie is marginally lower today, after US Trade Representative Robert Lighthizer said yesterday he is “hopeful” of reaching a NAFTA deal soon. The next round of talks is tentatively scheduled for mid-April, and all sides appear to be seeking a breakthrough before the Mexican elections in July. Thus, optimistic headlines on the subject that boost the CAD and MXN are not to be ruled out over the next weeks. The antipodeans were mixed, with aussie/dollar gaining 0.2%, but still trading near a 3-month low, while kiwi/dollar declined 0.1%.

Day ahead: Focus on US core PCE index, personal income & personal spending; Canada delivers GDP growth figures

Friday will be a busy day in terms of economic releases ahead of a long Easter-holiday weekend starting tomorrow, with the US, UK, Canada, and Germany being among the countries to deliver data.

At 0830 GMT, the Office for National Statistics in the UK will deliver its final GDP growth readings for Q4 2017, with analysts predicting an expansion rate of 0.4% month-on-month and 1.4% year-on-year as was previously estimated.

Staying in Europe, investors will also keep a close eye on German preliminary inflation estimates due at 1200 GMT. Particularly, consumer prices in the largest EU economy are anticipated to come in stronger at 1.7% y/y in March after falling the past two months. In February the measure stood at 1.4% y/y.

Canada will also report on GDP growth today at 1230 GMT. According to forecasts, the Canadian economy is expected to have grown at December's pace of 0.1% m/m, probably recording a yearly expansion of 2.9%. While a positive surprise in these data could boost the loonie, the currency's broader direction will likely be decided by any updates in the NAFTA negotiations.

In the US, the Fed's favorite inflation measure, the core Personal Consumption Expenditure index (PCE), and data on personal spending and personal income due at 1230 GMT will probably be of greater interest as markets are highly expecting the Fed to raise interest rates two more times this year and an unexpected increase in the numbers could be an indication that monetary policy is in the right direction. For now, forecasts are for the PCE index to inch up by 0.1 percentage points to 1.6% y/y in February, while personal income and personal spending are seen steady at 0.4% m/m and 0.2% m/m respectively. Encouraging outcomes could lift the dollar but any negative headlines regarding Trump's trade policy could erase potential gains.

In other data out of the US, initial jobless claims, the Chicago PMI and Michigan's final consumer sentiment will be in focus as well.

In energy markets, Baker Hughes will issue its weekly report on active US oil drillings for the week ending March 23 at 1700 GMT. Note that both the API and EIA weekly stats showed an unexpected rise in crude oil inventories, therefore pressure on oil prices could continue to persist if Baker Hughes backs a rise in US oil production.

Regarding today's public appearances, the Philadelphia Fed President Patrick Harker, a non-voting member, is scheduled to speak at 1700 GMT.

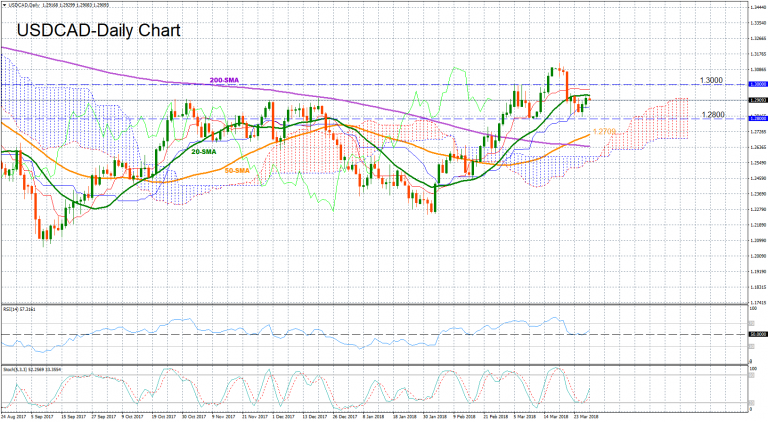

Technical Analysis – USDCAD neutral; risk tilted to the upside

USDCAD lost momentum after a sharp fall last Wednesday, moving sideways since then between 1.2800-1.2900. The RSI, however, suggests that the pair could gain some ground in the short-term as the index is currently positively sloped above 50, while the fast Stochastics support this view as well, with the blue %K line moving now above the red %D line.

In the wake of surprising strength in Canadian GDP growth, the loonie could pick up speed, driving the pair probably down to the 1.2800 key-mark. Even lower, the market could touch the 50-day simple moving average which currently stands at 1.2709.

In the alternative scenario, a disappointing growth rate could work well for the dollar and push dollar/loonie above the 20-day SMA of 1.2935, while larger negative surprises could open the way towards the 1.3000 key-level.

USDJPY Posts Some Losses After Aggressive Bullish Day

USDJPY bounced sharply during Wednesday’s trading session, adding 170 pips to its performance in just one day. The price rebounded on the 16-month low near 104.60 and tried to challenge the 107.30 resistance level. The pair, however, is currently looking weaker, trading below the 40-day simple moving average in the daily timeframe.

The MACD oscillator is rising above its red trigger line at the moment, giving some positive signals but is still in bearish territory, while the RSI is struggling to hold above 50, suggesting that the latest upswing may be running out of steam.

Should prices reverse lower, immediate support could come at the 20-day SMA around the 106.10 level. Below that, the 16-month low of 104.60 is another major support. An aggressive drop below this area could take the price closer to the 101.00 strong psychological level, taken from the low in November 2016.

Conversely, in case of an upside movement, there is an immediate resistance at 107.30, while above that, the next major barrier to watch is the 23.6% Fibonacci retracement level of 107.90 of the downleg from 118.60 to 104.60. Further gains would lead the way towards the 108.20 level and a jump above it could see a retest of the 38.2% Fibonacci mark near 110.00.

UK Gross Domestic Product Expected To Be In Line With Consensus

At 09:00 GMT, German Unemployment Change (Mar) is expected to be -15K against the previous -22K. Unemployment Rate s.a. (Mar) is expected to be 5.3% against the previous 5.4%. This number is expected to slip further after falling last month. The previous reading came in at the highest level in more than ten years. EUR traders will be closely following this data release.

At 09:30 GMT, UK Gross Domestic Product (YoY) (Q4) will be released and is expected to be unchanged from the previous reading, at 1.4%. Gross Domestic Product (QoQ) (Q4) is also expected to be unchanged at 0.4%. Mortgage Approvals (Feb) data will also be released at this time, with a consensus for 66.000K against 67.478K previously. The consensus is for a reading generally in line with expectations and previous releases so any deviation may spark a turn in market sentiment. GBP pair may see volatility around these data releases.

At 13:00 GMT, German Harmonised Index of Consumer Prices (YoY) (Mar) will be released. The consensus is for 1.6% from 1.2% previously. This data is expected to pick up from the reading last month, which was affected by seasonal factors. Any deviation from the expected would cause a market reaction, as the figure is usually accurately predicted. The preliminary release shows an increase of 0.5% in consumer prices. EUR pairs could have positions opened or closed due to this data.

At 13:30 GMT, US Personal Consumption Expenditures – Price Index (YoY) (Feb) is expected to be unchanged at 1.7%. Core Personal Consumption Expenditures – Price Index (MoM) (Feb) is expected to be 0.2% from 0.3% previously. Personal Consumption Expenditures – Price Index (MoM) (Feb) is expected to come in at 0.0% from 0.4% previously. Personal Income (MoM) (Feb) is expected to be unchanged at 0.4%. Personal Spending (Feb) is also expected to be unchanged at 0.2%. Core Personal Consumption Expenditures – Price Index (YoY) (Feb) is expected to be 1.6% from 1.5% previously. Continuing Jobless Claims (Mar16) is expected to be 1.875M against 1.828M previously. Initial Jobless Claims (Mar 23) is expected to come in at 230K against 229K previously. USD crosses may be heavily traded as a result of this data.

At 13:30 GMT, Canadian Gross Domestic Product (MoM) (Jan) is expected to be unchanged at 0.1%. This data is expected to show that growth remains in expansion but barely so, after falling in H2 of 2017. CAD pairs may be moved by this release.

At 14:45 GMT US Chicago Purchasing Managers’ Index (Mar) is expected to be 62.0 against a prior read of 61.9. The consensus is for a slight pickup in the index since the last release.

At 18:00 GMT, FOMC Member Harker is due to speak. Comments may result in moves in USD crosses.

Volatility Picks Up As USD Strengthens Into Quarter End

With US Personal Consumption Expenditures – Price Index on the way later today, as well as US Jobless data, traders will be watching the USD, which is showing strength as we approach the last trading days of March. USDJPY was up to 107.00 at one point overnight, helped by easing tensions with North Korea. Gold was down to a low of 1322.00 due to a strong USD. Stocks had a mixed day, with Europe flat or higher but the US markets remained down, especially the Nasdaq, which was 1.06% lower at the close.

German Gfk Consumer Confidence Survey (Apr) was 10.9 v an expected 10.7, against the previous 10.8. This number came in better than expected and is almost back to the February high of 11.0, which was the highest level in more than seventeen years. With confidence being so high amongst consumers, the economy and demand in-general remains high. EURUSD slipped from 1.24069 to 1.23835 following this data release.

US Gross Domestic Product Annualized (Q4) data came in at 2.9%, from an expected 2.7%, against a previous 2.5%. Gross Domestic Product Price Index (Q4) data was as expected, unchanged at 2.3%. Also at this time, Core Personal Consumption Expenditures (QoQ) (Q4) was as expected, unchanged from the Q3 reading, at 1.9%. Personal Consumption Expenditure Prices (QoQ) (Q4) was also as expected, unchanged at 2.7%. USDJPY fell from 106.340 to 106.066 in reaction to the numbers released.

Pending Home Sales (YoY) (Feb) came in at -4.4% v an expected -0.2%, against a prior reading of -1.7%, which was revised down to -1.9%. Pending Home Sales (MoM) (Feb) was 3.1% v an expected 2.1%, against a prior reading of -4.7%, which was revised down to -5.0%. These data points were a mixed bag. While both previous numbers were revised lower, the year-on-year figure declined substantially and the month-on-month figure showed a strong rebound after the decline last month. The New Year is usually the worst time for US home sales, with a strong rebound in February. EURUSD moved up from 1.23369 to 1.23598 due to this data release.

FOMC Member Bostic spoke at the Atlanta Society of Finance and Investment Professionals luncheon. Some of his comments were: that he thinks the Fed needs to get back to neutral rate and he doesn’t read too much into stock market volatility. A gradual approach to interest rates is better than big jumps and inflation is rising, looking at 6-month core gauge.

New Zealand Building Permits s.a. (MoM) (Feb) were released, coming in at 5.7% against 0.2% previously, which was revised down to 0.0%. This data series can be quite volatile, having swung between 20 and -10 over the last six years. The November reading was 10.8%, while December was -9.6%. NZDUSD fell from 0.72094 to 0.72023.

EURUSD is up 0.21% overnight, trading around 1.23334.

USDJPY is down -0.33% in early session trading at around 106.490.

GBPUSD is up 0.209% this morning, trading around 1.40897.

USDCAD is down -0.10% in early trade at around 1.29082.

Gold is up 0.22% in early morning trading at around $1,328.27.

WTI is down -0.06% this morning, trading around $64.65.

German unemployment rate hit record low, but no support to Euro

German unemployment dropped -19k to 2.373m in March, more than expectation of -15k.

Unemployment rate dropped from 5.4% to 5.3%, met expectation. That's also the lowest level on record.

EUR, however, receives no support from the data. It's trading down against all major current in the current 4H bar. And for the week, EUR is also reversing much of the earlier gains and is turning mixed.

The only exception is against CHF, which is trading as the second weakest one for the week, next to JPY. EUR/CHF is still on track to test 1.1832 resistance.

The only exception is against CHF, which is trading as the second weakest one for the week, next to JPY. EUR/CHF is still on track to test 1.1832 resistance.

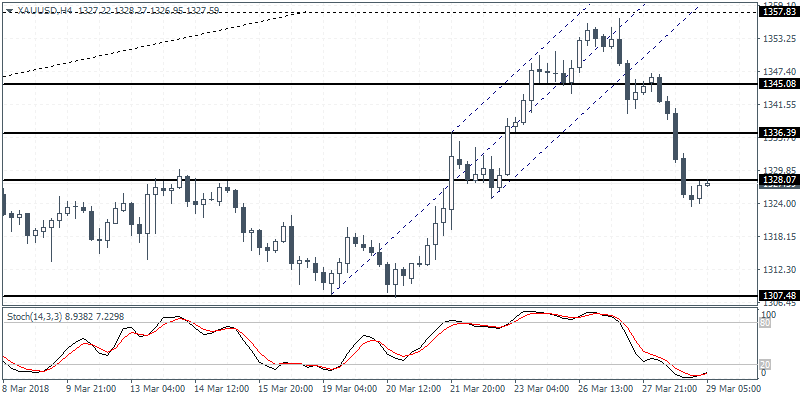

XAUUSD Intraday Analysis

XAUUSD (1327.59): Gold prices fell sharply yesterday testing the support level at 1328. With price now at support, we expect to see a modest rebound shaping up. The bullish divergence on the 4-hour chart signals a near term upside in price. Gold price will need to first retest the 1336 level where resistance could be formed. However, a breakout above this level will see gold prices testing the 1345 level once again. To the downside, a break below 1328 could signal a move lower to 1307.50.