Sample Category Title

Elliott Wave Analysis: FTSE Inflection Area For Next Leg Lower

Latest Elliott Wave view in FTSE suggests that the Index ended Primary wave ((B)) at 7326.02 on 2/27/2018 high. From there, Index starts a decline which is unfolding as a 5 waves impulse Elliott Wave structure with an extensionin wave (3). Down from 2/27/2018 high, Intermediate wave (1) ended at 7062.13, Intermediate wave (2) ended at 7256.33, and Intermediate wave (3) is in progress.

In a 5 waves impulse structure, subdivision of wave (1), (3), and (5) are themselves also in 5 waves (impulsive) in the smaller degree. In the case of FTSE, subdivision of Intermediate wave (1) unfolded as 5 waves impulse where Minor wave 1 ended at 7272.87, Minor wave 2 ended at 7312.92, Minor wave 3 ended at 7063.42, Minor wave 4 ended at 7104.66, and Minor wave 5 of (1) ended at 7062.13. Subdivision of Intermediate wave (2) unfolded as a zigzag Elliott Wave structure where Minor wave A ended at 7197.80, Minor wave B ended at 7109.56, and Minor wave C of (2) ended at 7256.33.

Intermediate wave (3) is currently in progress and also subdivided as 5 waves where Minor wave 1 ended at 6866.94. Minor wave 2 bounce is in play to correct cycle from 3/12/2018 high (7256.33) towards 7099.69 – 7208.97 before the decline resumes. While bounces stay below 7256.33 in the first degree, expect sellers to appear at 7099.69 – 7208.97 and bring the Index lower to resume the Intermediate wave (3) decline. We don’t like buying the Index.

FTSE 1 Hour Elliott Wave Chart

USD/JPY Daily Outlook

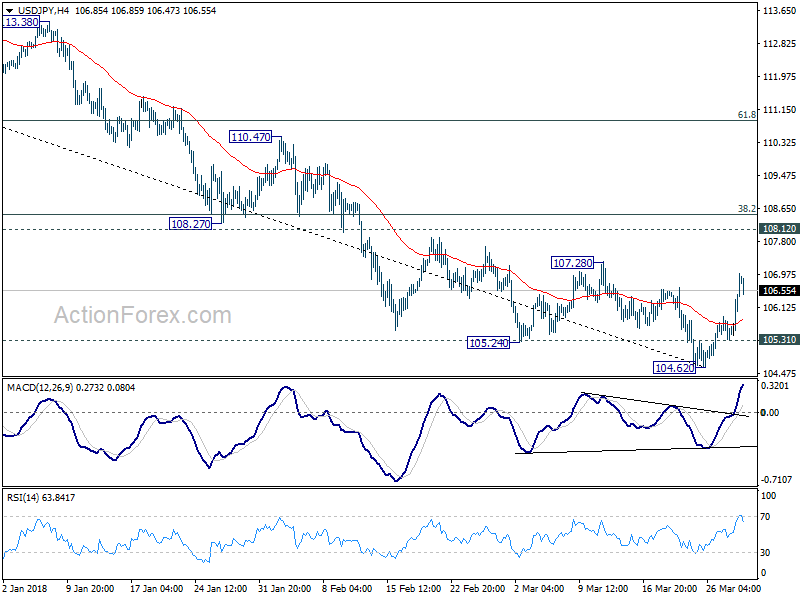

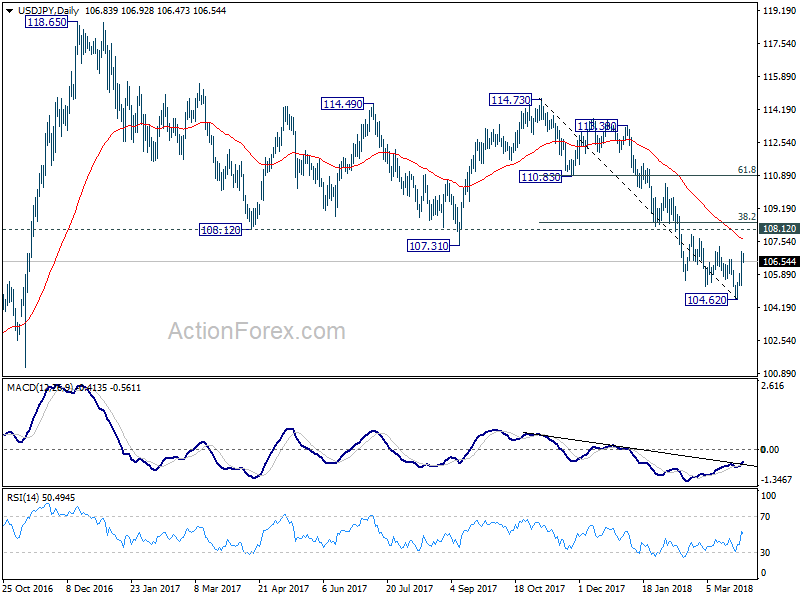

Daily Pivots: (S1) 105.12; (P) 105.51; (R1) 105.71; More...

USD/JPY's rebound from 104.62 extended to as high as 107.00 so far. The break of 106.63 resistance indicates short term bottoming on bullish convergence condition in 4 hour MACD. Intraday bias is back on the upside for 38.2% retracement of 114.73 to 104.62 at 108.48. At this point, there is no confirmation of trend reversal yet. Hence, we'll look at the reaction from 108.48 (which is close to 108.12 too) to assess the chance. On the downside, below 105.31 minor support will indicate that the rebound is completed and turn bias back to the downside instead.

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

Dollar Rebound Lacks Conviction, Except Versus Aussie and Possibly Yen

Dollar jumps broadly overnight but it's rally is starting to lose steam again in Asian session. Instead, while Yen remains the weakest one for the week, it's starting to regain some strength. So far, the Japanese is not benefiting from risk aversion this week. Even though stocks attempted to rebound, there was no sustainable buying. DOW closed nearly flat by -0.04% overnight but NASDAQ extended recent fall by closing down -0.85% at 6949.23, losing 7000 handle. The pre-holiday calendar is rather busy today and we could see some bigger moves as liquidity dries up.

Technically, in spite of the rebound in the past two days, Dollar is kept below near term resistance level against Europeans. That is, EUR/USD is held above 1.2285, GBP/USD above 1.3982. While USD/CHF breached 0.9568 resistance, it's kept well off 0.9626 key fibonacci level. USD/CAD also finds no buying even though it's drawing support above 1.2802, and it's kept well below recent high at 1.3124.

Dollar is showing more persistent strength only against Australian Dollar and Yen. In particular, USD/JPY's break of 106.63 resistance is seen as a sign of trend reversal. Near term focus will now turn to 107.28.

Japan FM Aso: No bilateral trade negotiations with US

Japan finance minister Taro Aso said in the parliament that historically, US Dollar always rise against Japanese Yen when interest rate differentials widened to 3%. Aso added that US interest rates will "undoubtedly rise ahead". And therefore, there won't be "one-sided" Yen appreciation that could hurt the economy.

Regarding trade, Aso emphasized that Japan should "definitely avoid" bilateral trade negotiations with the US. He added that "When two countries negotiate, the stronger country gets stronger. That's unnecessary (for Japan) so we've been saying all along that we would definitely avoid" bilateral trade talks with the United States.

Japan at beginning of consumer spending recovery

Japan retail sales rose 0.4% mom, 1.6% yoy in February, slightly higher than expectation of 0.6% mom, 1.7% yoy. And it's marked improvement from January's -1.6% mom, 1.5% yoy. It's noted that consumer spending could be at the beginning of mild recovery. Improvement is also seen lately in the labor market. Overall picture suggests that consumption is going to pick up momentum. And that should eventually help lift inflation. But for now, core inflation is still way off BoJ's 2% target and it will take some more time for BoJ to start considering stimulus exit.

UK Gfk Consumer Confidence: Definitely a movement in the right direction

UK Gfk consumer confidence rose to -7 in March, up from -10 and above expectation of -10. All five of the constituent measures recorded higher values. Personal financial situation over the past 12 months rose 3 pts to 3. Personal financial situation over next 12 months rose 5 pts to 10. General economic situation over the last 12 month rose 3 pts to -26. General economic situation over next 12 months rose 4 pts to -22. Major purchase index rose 2 pts to 2. Saving index rose 1 pt to 13.

Gfk noted in the release that "the prospect of wage rises finally outstripping declining inflation, high levels of employment with low-level interest rates, and finally some movement on the Brexit front appear to have boosted our spirits." While it's "still a little early to be talking about green-shoots", "this is definitely a movement in the right direction".

Looking ahead

The pre-holiday economic calendar is rather busy today. Swiss will release KOF leading indicator. Germany will release unemployment but more focus would be on CPI. UK will release Q4 GDP final, mortgage approvals, M4 and current account.

Later in US session, Canada will release GDP, IPPI and RMPI. US will release personal income and spending, jobless claims and Chicago PMI. USD/CAD could have some big moves ahead of holidays.

USD/JPY Daily Outlook

Daily Pivots: (S1) 105.12; (P) 105.51; (R1) 105.71; More...

USD/JPY's rebound from 104.62 extended to as high as 107.00 so far. The break of 106.63 resistance indicates short term bottoming on bullish convergence condition in 4 hour MACD. Intraday bias is back on the upside for 38.2% retracement of 114.73 to 104.62 at 108.48. At this point, there is no confirmation of trend reversal yet. Hence, we'll look at the reaction from 108.48 (which is close to 108.12 too) to assess the chance. On the downside, below 105.31 minor support will indicate that the rebound is completed and turn bias back to the downside instead.

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Feb | 5.70% | 0.20% | 0.00% | |

| 23:01 | GBP | GfK Consumer Confidence Mar | -7 | -10 | -10 | |

| 23:50 | JPY | Retail Trade Y/Y Feb | 1.60% | 1.70% | 1.60% | 1.50% |

| 07:00 | CHF | KOF Leading Indicator Mar | 107.2 | 108 | ||

| 07:55 | EUR | German Unemployment Mar | -15K | -22K | ||

| 07:55 | EUR | German Unemployment Claims Rate Mar | 5.30% | 5.40% | ||

| 08:30 | GBP | Mortgage Approvals Feb | 66K | 67K | ||

| 08:30 | GBP | Money Supply M4 M/M Feb | 1.30% | 1.50% | ||

| 08:30 | GBP | Current Account Balance Q4 | -23.7B | -22.8B | ||

| 08:30 | GBP | Index of Services 3M/3M Jan | 0.60% | 0.60% | ||

| 08:30 | GBP | GDP Q/Q Q4 F | 0.40% | 0.40% | ||

| 12:00 | EUR | German CPI M/M Mar P | 0.50% | 0.50% | ||

| 12:00 | EUR | German CPI Y/Y Mar P | 1.70% | 1.40% | ||

| 12:30 | CAD | GDP M/M Jan | 0.10% | 0.10% | ||

| 12:30 | CAD | Industrial Product Price M/M Feb | 0.30% | |||

| 12:30 | CAD | Raw Materials Price Index M/M Feb | 3.30% | |||

| 12:30 | USD | Personal Income Feb | 0.40% | 0.40% | ||

| 12:30 | USD | Personal Spending Feb | 0.20% | 0.20% | ||

| 12:30 | USD | Real Personal Spending Feb | 0.10% | -0.10% | ||

| 12:30 | USD | PCE Deflator M/M Feb | 0.20% | 0.40% | ||

| 12:30 | USD | PCE Deflator Y/Y Feb | 1.70% | 1.70% | ||

| 12:30 | USD | PCE Core M/M Feb | 0.20% | 0.30% | ||

| 12:30 | USD | PCE Core Y/Y Feb | 1.60% | 1.50% | ||

| 12:30 | USD | Initial Jobless Claims (MAR 24) | 231K | 229K | ||

| 13:45 | USD | Chicago PMI Mar | 62 | 61.9 | ||

| 14:00 | USD | U. of Mich. Sentiment Mar F | 102 | 102 | ||

| 14:30 | USD | Natural Gas Storage | -86B |

Japan finance minister Aso: “Definitely avoid” bilateral trade negotiations with US

Japan finance minister Taro Aso said in the parliament that historically, US Dollar always rise against Japanese Yen when interest rate differentials widened to 3%. Aso added that US interest rates will "undoubtedly rise ahead". And therefore, there won't be "one-sided" Yen appreciation that could hurt the economy.

Regarding trade, Aso emphasized that Japan should "definitely avoid" bilateral trade negotiations with the US. He added that "When two countries negotiate, the stronger country gets stronger. That's unnecessary (for Japan) so we've been saying all along that we would definitely avoid" bilateral trade talks with the United States,

Japan retail sales rose 0.4% mom, 1.6% yoy. Consumption at start of mild recovery

Japan retail sales rose 0.4% mom, 1.6% yoy in February, slightly higher than expectation of 0.6% mom, 1.7% yoy. And it's marked improvement from January's -1.6% mom, 1.5% yoy.

It's noted that consumer spending could be at the beginning of mild recovery. Improvement is also seen lately in the labor market. Overall picture suggests that consumption is going to pick up momentum. And that should eventually help lift. inflation.

But for now, core inflation is still way off BoJ's 2% target and it will take some more time for BoJ to start considering stimulus exit.

UK Gfk Consumer Confidence rose to -7 in March, All five measures improved

UK Gfk consumer confidence rose to -7 in March, up from -10 and above expectation of -10. All five of the constituent measures recorded higher values. Personal financial situation over the past 12 months rose 3 pts to 3. Personal financial situation over next 12 months rose 5 pts to 10. General economic situation over the last 12 month rose 3 pts to -26. General economic situation over next 12 months rose 4 pts to -22. Major purchase index rose 2 pts to 2. Saving index rose 1 pt to 13.

Quote from the release:

"Despite the Beast from the East leaving the nation shivering under a blanket of snow, stoic UK consumers turned faintly bullish this March with a three-point uptick in the Overall Index Score to -7. Spring is in the air with increases across the board on personal finances, the general economy – over the last year and next year – and on current major purchase intentions. The prospect of wage rises finally outstripping declining inflation, high levels of employment with low-level interest rates, and finally some movement on the Brexit front appear to have boosted our spirits. It's still a little early to be talking about green-shoots, and the core score is of course still negative, but this is definitely a movement in the right direction. Consumers are feeling a tiny spring in their step – let's see next month if April showers dampen the mood."

Can EUR/JPY Recover Above 132.50?

Key Highlights

- The Euro made a major top near the 137.50 level against the Japanese Yen.

- There was a break below an important bullish trend line with support at 134.20 on the daily chart of EUR/JPY.

- The German GfK Consumer Confidence for April 2018 posted a minor rise from 10.8 to 10.9.

- Today, the German CPI report for March 2018 (Prelim) will be released, which is forecasted to post a rise of 1.7% (YoY).

EUR/JPY Technical Analysis

There was a major downside move initiated in the Euro from the 137.50 high against the Japanese Yen. The EUR/JPY pair traded towards the 129.00 level where buyers protected further declines.

Looking at the daily chart of EUR/JPY, it seems like a good support is forming above the 129.00 level. The pair even moved above the 23.6% Fib retracement level of the last decline from the 137.50 high to 128.94 low.

However, there are many resistances on the upside near the 131.50, 132.00 and 132.50 levels. A proper close above the 132.00 level and the 200 simple moving average (green, 4-hour) is needed for further gains in the near term.

On the downside, the 129.00 support holds the key. If the pair fails to stay above 129.00, the last downtrend may resume.

Recently, the German GfK Consumer Confidence for April 2018 was released. The market was looking for a minor decline from the last reading of 10.8 to 10.7.

However, the actual result was better since there was a rise from 10.8 to 10.9. The report added that:

The consumer mood in Germany has stabilized in March after the previous month’s minor setback. Both economic and income expectations, as well as propensity to buy, are on the increase again. GfK forecasts an increase in consumer climate for April of 0.1 points in comparison to the previous month to 10.9 points.

Overall, downsides could be limited in EUR/JPY, but it must gain momentum above 132.00 and 132.50 to continue moving higher.

Economic Releases to Watch Today

- UK GDP for Q4 2017 (YoY) – Forecast +1.4% versus +1.4% previous.

- German Consumer Price Index for March 2018 (Prelim) (YoY) – Forecast +1.7%, versus +1.4% previous.

- German Consumer Price Index for March 2018 (Prelim) (MoM) – Forecast +0.5%, versus +0.5% previous.

- US Initial Jobless Claims – Forecast 230K, versus 229K previous.

- US Personal Income for Feb 2018 (MoM) – Forecast +0.4%, versus +0.4% previous.

New Zealand building consents rose 5.7% mom in Feb

New Zealand building consents rose 5.7% mom in February verusus 0.0% mom in January.

Key facts from noted in the release:

- The seasonally adjusted number of new dwellings consented rose 5.7%.

- In the year ended February 2018, 31,245 new dwellings were consented, up 3.6%.

- The annual value of building work consented was $20.4 billion, up 9.9% from the February 2017 year.

Regional numbers of new dwellings consented in the February 2018 year were:

- Auckland - up 10% to 11,052

- Waikato - down 1.2% to 3,469

- Wellington - up 20% to 2,432

- Rest of North Island - up 0.6% to 5,794

- Canterbury - down 14% to 4,962

- Rest of South Island - up 17% to 3,532 - driven by Otago

All building consents

Including alterations, the value of all building work consented in the year ended February 2018 was $20.4 billion, comprising $13.7 billion of residential work and $6.8 million of non-residential work. The annual total value rose 9.9 percent when compared with the February 2017 year.

Tech stock recovery short-lived as NASDAQ dropped 0.85%, 10 year yield hit 7-week low

The recovery in tech stocks in the US proved to be weak and short-lived. NASDAQ hit 7036.09 initially but failed to sustain above 7000 handle. It closed down -59.58 pts or -0.85% at 6949.23. Near term direction is still on the way down considering it's staying comfortably below falling 55 H EMA. Note that it's now trying to sustain below 61.8% retracement of 6630.67 to 7637.27. Next target will be 6630.67 key structural support.

The deterioration in investor sentiments seem to be finally having an impact in the bond markets too. 10 year yield closed down -0.11 to 2.775 after hitting a 7-week low. Safe haven flow is noted as the correction in equity markets look far from being over. TNX is now sitting on 55 day EMA but we'd see it probably dip further to 38.2% retracement of 2.033 to 2.943 at 2.595 before bottoming.

The deterioration in investor sentiments seem to be finally having an impact in the bond markets too. 10 year yield closed down -0.11 to 2.775 after hitting a 7-week low. Safe haven flow is noted as the correction in equity markets look far from being over. TNX is now sitting on 55 day EMA but we'd see it probably dip further to 38.2% retracement of 2.033 to 2.943 at 2.595 before bottoming.

U.S. Inflation to Gain Speed As Headwinds Turn to Tailwinds

Highlights

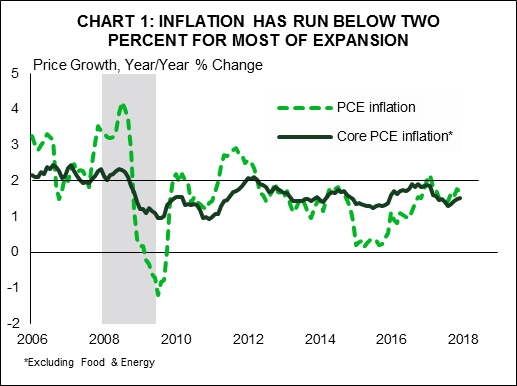

- The recovery from the Great Recession has been characterized by low inflation. Since it ended in 2009, PCE inflation (the Federal Reserve's preferred measure) has averaged just 1.6%. Inflation rose above 2% only briefly in 2012 before dipping back below it again.

- The weakness in U.S. inflation reflects several factors including: cyclical elements - a rising U.S. dollar, declining energy prices, and soft global growth; idiosyncratic elements - new cell phone contracts and the Affordable Care Act's dampening effect on health care prices; and structural elements - increased digitization and retail competition.

- Soft inflation has contributed to the low level of interest rates and gradual policy response from the Federal Reserve to normalizing monetary policy. Higher inflation should give them the confidence to continue to raise rates, potentially offsetting some of the positive impact of fiscal stimulus.

Inflation, as measured by the Federal Reserve's preferred metric - the core personal consumption expenditures (PCE) deflator - has been running below 2% since January 2012 (Chart 1). Recognition that inflation has come in below its long-run objective has been a key feature of the Fed's policy communique for several years. It remained there in the most-recent statement in March.

Still, the Fed's characterization of inflation has begun to shift. The March statement noted that "inflation is expected to move up in coming months" - marking to market the momentum we have seen in the price data recently. Over the past six months, core prices have risen 2.0% (annualized). Federal Reserve members' median projection for core inflation is for it to move above 2.0% in 2019 (to 2.1%) - the first time it has ever crossed this threshold.

As the Fed projections imply, there is a good case that we are at pivot point with respect to price pressures. Yes, we know, economists have said this before! There are several factors unfolding that differentiate this point in the economic cycle. First, many of the headwinds to inflation over the past several years - the decline and subdued recovery in commodity prices, soft global demand growth, a rising U.S. dollar - have turned to tailwinds over the past year. Second, idiosyncratic factors that have depressed consumer prices (such as changes to cell phone contract offerings) will fall out of the data in the next few months. Third, there's a new kid on the block: fiscal stimulus. Economic growth is projected by the vast majority of forecasters (including us) to move well above its trend rate. Capacity pressures are building, nowhere more evident than in an unemployment rate that is likely to hit a 50 year low this year or next. This is an important layer to inflation pressures, which will be further nudged by tariff action and negative trade rhetoric that adds a final upward dimension to price pressures.

There are some factors that should mitigate the speed of adjustment. For instance, corporate tax cuts give businesses additional margin to absorb some of the rising cost pressures, while digitization will keep the dial turned up on competitive pressures. However, these factors argue against a sudden jump to a much higher inflation rate. They do not argue for these forces to completely offset the rising tide. Consumer price inflation should finally surpass the Fed's 2% target over the next year.1

Global backdrop is no longer disinflationary

The weakness in price growth has not just been a U.S. story. Inflation has disappointed across advanced economies and has decelerated in emerging markets over the past several years. The slowdown in global inflation was echoed in a disappointing pace of global growth. This was particularly true in Europe following the sovereign debt crisis, but extended to emerging markets through trade channels and commodity prices.

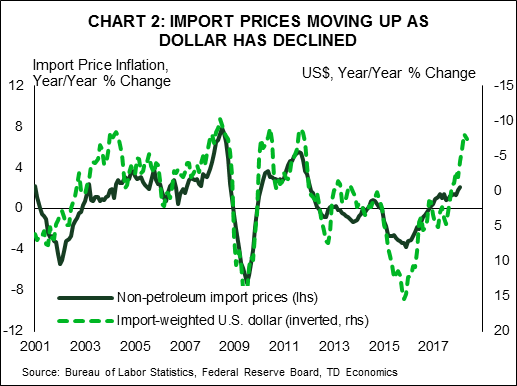

The past year has brought a sea change in the performance of global economies relative to expectations. Rather than disappoint, economic growth has exceeded forecasts. This has led the U.S. dollar to depreciate even as America's economic growth prospects have faced a rapid-fire of upgrades due to fiscal stimulus. Since the end of 2016, the trade-weighted U.S. dollar has fallen close to 8%.

This, in combination with more robust global economic activity, should place greater upward pressure on U.S. prices from external channels. Import prices are already capturing these influences (Chart 2). The pass through to consumer price inflation has been mild up until now, but is not absent. Items with higher imported content, such as clothing, saw price growth accelerate rapidly in January and February.

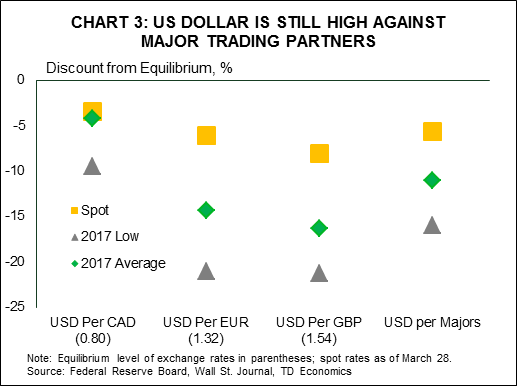

It's possible (and reasonable) that the greenback will face bouts of upward pressure in the near-term, but the majority of currencies are still trading at a discount to their fair values (Chart 3). We anticipate a further modest depreciation in the U.S. dollar over the next year or, at the very least, for any upward pressure to prove fleeting. As there are lags from when import price pressures pass-through to consumers, the lower valued greenback should raise core consumer inflation (excluding food and energy) by 0.2 percentage points over the next twelve to eighteen months.

It's possible (and reasonable) that the greenback will face bouts of upward pressure in the near-term, but the majority of currencies are still trading at a discount to their fair values (Chart 3). We anticipate a further modest depreciation in the U.S. dollar over the next year or, at the very least, for any upward pressure to prove fleeting. As there are lags from when import price pressures pass-through to consumers, the lower valued greenback should raise core consumer inflation (excluding food and energy) by 0.2 percentage points over the next twelve to eighteen months.

Idiosyncratic factors are fading

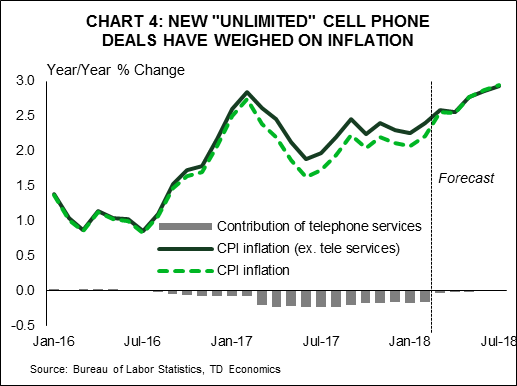

Another idiosyncratic weight on inflation is also coming to an end. Consumer price indexes over the past year captured unusually large downward pressure from relative small components that had swung deeply negative. In particular, telephone service prices fell 5.0% (month-on-month) in March last year, which was immediately followed by another large stepdown of 1% in April. Competition saw new wireless phone companies offer discounted unlimited data plans. While telephone services make up only 2% of the CPI basket, the large and sudden price swing saw it subtract 0.2 percentage points from inflation over the past year. This one-time price decline is unlikely to be repeated and is about to fall out of the year-over-year inflation calculation (Chart 4).

This isn't the only influence that will be reversing course. The Affordable Care Act (ACA) had placed downward pressure on healthcare-services inflation since 2008, captured in lower prices for physician and hospital services. As a result, healthcare price growth has averaged just 1.7% annually over the past decade, compared to 3% the decade prior. Moreover, the contribution to PCE inflation from healthcare has been about 0.3 percentage points lower over this time frame relative to the earlier decade.2

This isn't the only influence that will be reversing course. The Affordable Care Act (ACA) had placed downward pressure on healthcare-services inflation since 2008, captured in lower prices for physician and hospital services. As a result, healthcare price growth has averaged just 1.7% annually over the past decade, compared to 3% the decade prior. Moreover, the contribution to PCE inflation from healthcare has been about 0.3 percentage points lower over this time frame relative to the earlier decade.2

Recently, however, healthcare inflation has moved higher. In January, it was up 2.0% year-on-year, with even stronger gains in the hospital category. Increases in the Medicare payments schedule are expected to lead to higher health care prices over the next year.3 Moreover, some of the legislated cuts in Medicare payments are set to expire in 2019, potentially leading to further increases. While healthcare price growth may not return to rates seen prior to the financial crisis, its disinflationary impact looks to be a thing of the past in the absence of another policy change.

The Phillips curve (still) isn't dead

Up until now, the discussion has been focused on features that will cease to depress inflation. However, these influences will be layered on top of a grand theme that will carry the bigger influence: a continued improvement in the economy and labor market. We have looked at the relationship between unemployment and inflation (known as the Phillips curve) through several lenses in past reports, including across states (here) and countries (here). All of this analysis dispelled the belief that the Phillips curve is dead. We estimate that the coefficient on the "output gap" (the gap between unemployment and its natural rate) is in the range of 0.1% to 0.3%. This means that every 1 percentage point move in the unemployment rate (relative to its natural rate) should move inflation by roughly 0.2%.

This may seem small on the surface, but is becoming an important figure at this point in the business cycle. With fiscal stimulus expected to boost economic growth to around 3% over the next two years, the unemployment rate is likely to reach lows not seen in the United States in 50 years. While there is some debate about how low the structural rate of unemployment actually is, it's fair to say that at 3.7%, the rate would be in the neighborhood of 0.5 to 1 percentage points below its natural rate. Embedded in this view is the continued absorption of "shadow slack" that has helped keep wage pressures at bay up until now.4 The participation rate of the core-working age people (25 to 54) has trended steadily up over the past two years, and will return to its pre-recession peak by the end of 2019 (Chart 5).

When combining the influences of waning idiosyncratic price influences alongside strengthening tailwinds from economic pressures, it's becoming harder and harder to stay in the no-inflation camp. In fact, it would be a leap of faith to expect consumer prices to remain completely unresponsive. We estimate that tightening labor markets will lift inflation by between 0.1 to 0.3 percentage points, with close to half of this coming from the impact of fiscal stimulus.

When combining the influences of waning idiosyncratic price influences alongside strengthening tailwinds from economic pressures, it's becoming harder and harder to stay in the no-inflation camp. In fact, it would be a leap of faith to expect consumer prices to remain completely unresponsive. We estimate that tightening labor markets will lift inflation by between 0.1 to 0.3 percentage points, with close to half of this coming from the impact of fiscal stimulus.

Tariffs will not help

As if the inflation tailwinds weren't already gathering force, enter the trade winds. We assessed the economic impacts from the Trump administration's recently announced tariffs in recent reports (here and here). In addition to tariffs on steel and aluminum, The Trump administration has announced a package of tariffs targeting $50 billion or more of Chinese imports annually. While the details of which products most impacted are forthcoming, the U.S. administration has announced that it will target imports of aerospace, information and communications technology, and machinery. This is likely to add further to inflation over the next two years. All told, these tariffs are likely to raise inflation by 0.1 to 0.2 percentage points annually over the next two years.

These are not the only trade winds flowing through consumer prices. Tariffs have also been placed on Canadian softwood lumber and on washing machines and solar panels from Asia. These are small items in the consumption basket but will also add (albeit marginally) to price growth over the next few years.

Bottom line

U.S. inflation is at a turning point. As headwinds to price growth turn to tailwinds, inflation is likely to turn higher. A higher inflation rate has a number of important implications for investors and economy watchers. First, it means the Federal Reserve will continue to raise its key lending rate possibly even above its intended terminal rate in order to keep inflationary pressures contained. Second, it will counteract some of the fiscal stimulus and enthusiasm around the benefits of tax cuts, particularly on the personal side. Households will face higher interest rates and higher prices, eating into the gains from tax cuts. Third, higher inflation may require a higher risk premium for inflation to be built into longer-term yields, putting pressure on highly-leveraged corporate borrowers and mitigating the salutary effects lower corporate tax rates on investment.

End Notes

- As measured by the price index for personal consumption expenditures (PCE). CPI inflation sat at 2.3%(year-on-year) as of February, 2018.

- The impact is more pronounced on the PCE index than in CPI due to the fact that PCE includes healthcare items that are not directly paid for by households.

- Mahedy, Tim and Adam Shapiro (2017). "What's Down with Inflation." FRBSF Economic Letter. 2017-35 (November 2017) https://www.frbsf.org/economic-research/files/el2017-35.pdf

- Hong, Koczan, Lian, Nabar (2018). "More Slack than Meets the Eye? Recent Wage Dynamics in Advanced Economies" IMF Working Paper. WP/18/50 http://www.imf.org/~/media/Files/Publications/WP/2018/wp1850.ashx