Sample Category Title

Another 48 hours

The previous 48 hours have been all-encompassing as Forex desks are dealing with a combination of month/quarter end flows, bloodletting in equity and rates, amidst a massive wave of USD short covering. The US dollar was again heavily bid overnight as equity markets had another horrible session getting dragged lower by the blowout in leading technology names and US yields responded by dripping lower.And what do we have to look forward to before diving into our Cadbury Creme Egg’s ?, Another 48 hours of course.

It’s as if someone flipped a switch and now everyone hates the dollar short position with the US administration swinging a massive economic and political stick to pressure friendly exporting nations into trade deals, and by extension, accidentally appreciating the US dollar. Probably not the desired outcome given the administrations trade policy intentions suggest a preference for a weaker USD.

So the combination of early month-end position squaring and icing of trade tensions dominated in an otherwise slipshod day in the currency markets. Devoid of tier one data and with only a positive US GDP to gauge sentiment, but that too provided a sufficient US dollar fillip to accompany the premature month-end short dollar position culling. Indeed a painful few days for USDJPY bears if somehow you had not squared ahead of this potentially upending week given the likelihood of a stronger USD on the rebalancing theme. But there’s a distinct lack of participation from the short dollar perspective, most G-10 traders had already adopted a know when to hold em, and know when to fold em strategy but remain incredibly patient looking for more excellent levels to re-engage their preferred USD short positioning.

But for the mean reversionists in us all, if there was a strong case to be made to “buy on cannons sell on trumpets” it’s certainly shaping up to be a decent opportunity in both the weaker US equity markets and rebounding dollar narrative.

But unquestionably, some very strong persuasions are being tested given the market has been focused on stronger EUR, GBP and JPY storylines for some time. This current USD move will either prove to be a brilliant opportunity to rejoin the battle ( short dollar trade) or a watershed moment for USD bullish contrarians.

However, on the back of a weak tail end bid to cover ratio form of this week’s US treasuries auction supply, USDJPY has moved off its overnight peak on weaker demand. But I wouldn’t make a meal of one tranche in this latest auction results since there’s been a stellar flight to quality demand all week. Indeed rates have proven a cleaner trade to play the evolving major macro themes in current market conditions.

Oil markets

DoE inventories released on Wednesday showed a build of total crude oil inventories of +1.64mn vs -0.85mn draw median, on the back of the eyewatering API build of +5.32mn. But none the less, prices are icing ahead of the holiday weekend as WTI has stabilised towards $ 64.50. Inventory data is turning into more of a guessing game than pure science. So while offering short-term specs an opportunity to job the action, from a longer-term perspective, there are few specific directional takeaways from this extremely volatile data set these days.

There was also news that OPEC could be shifting goalposts once again with OPEC producers and non-OPEC compliant members suggesting a willingness to extend the supply curbs beyond 2018 with both Russia and Saudi Arabia leading the charge.

Gold prices

Gold prices came off heavy on the back of the resurgent dollar and easing of North Asia political tension, as the canary in the goldmine was sending off warning signals. But trading top end breakout signals are incredibly challenging amidst the multitudes of headline risk.But with the COMEX and DXY so strongly correlated, gold bulls were utterly overwhelmed by the resurgent dollar as stop-loss triggers amplified the sell-off. However, positioning should be much cleaner now below $ 1330.00, and if not for the long weekend approaching I suspect more investors would view current levels as very attractive, and while investor demand could wane ahead of the holiday weekend, institutional support at $ 1.323-1325 areas remain solid.

Currency Markets

The Japanese Yen

USDJPY has been steering the bus overnight on the backdrop of easing of regional geopolitical tensions. The equity meltdown has not translated into the expected JPY strength, and flat out levelling the most heavily subscribed USD short position in the markets.

The Euro

In the absence of relevant news, , EUR was prone to the broader USD moves today and made another leg lower, dropping to a low of 1.2335. Big picture, the pair still looks relatively tame and rangy and suggesting Monday’s beak out a false flag signal

The Malaysian Ringgit

A bit of a puzzle with the easing of North Korea tensions indicate a big boost to regional sentiment, but trader remains confounded by the stronger USD narrative.And while the easing of geopolitical tension and the downplaying of trade war rhetoric certainly bodes well, with US yields rallying, this is a definite carry trade signal into the MGS’s even more so for those investors positioning for the re-emergence of USD dollar negativity. However, the stars need to realign again from a yield, risk and a weaker USD perspective to make the push towards 3.85 which is unlikely to occur this week.

Gold Slides as US Final GDP Beats Estimate

Gold has posted sharp losses in the Wednesday session, continuing the downward movement which marked Tuesday trading. In North American trade, the spot price for an ounce of gold is $1328.95, down 1.20% on the day. In economic news, Final GDP impressed with a gain of 2.9%, beating the estimate of 2.7%. There was more good news as Pending Home Sales jumped 3.1%, rebounding after the previous release of -4.7%. On Thursday, the US publishes unemployment claims and UoM Consumer Sentiment.

The US economy continues to fire on all cylinders, with Final GDP for the fourth quarter expanding 2.9%. This was higher than the initial estimate of 2.5% back in February. The strong reading has improved risk appetite and sent gold reeling, as the base metal has fallen 1.6% this week.

The tariff dispute between the US and China has dented investor confidence and triggered strong volatility in gold prices. As a safe-haven commodity, gold jumped 1.8% last week, buoyed by President Trump’s dramatic announcement that he was imposing stiff tariffs on up to $60 billion in Chinese imports. China vowed to retaliate and slap imports on a range of US products. This move came on the heels of a blanket US tariff on steel imports. Although Trump backtracked and exempted Canada, Mexico and other countries from the steel tariffs, the threat of a global trading war has unnerved investors. This week, however, China was singing a more conciliatory tune, saying it would apply to the World Trade Organization to overturn the tariffs. The US has imposed the tariffs under a national security provision, but China has argued that the move is a trade barrier with the intent of protecting domestic producers. Although the dispute has not been resolved, the Chinese move has eased tensions and restored investor risk appetite, in the hope that both the US and China will climb down from their trees and reach some agreement instead of imposing tariffs on each other. This sentiment has boosted the stock markets while sending gold prices lower.

British Pound Softens as Retail Sales Slide

The British pound has lost ground in the Wednesday session, continuing the downward movement seen on Tuesday. In North American trade, GBP/USD is trading at 1.4103, down 0.39% on the day. On the release front, the CBI Realized Sales survey came in at -8, well off the estimate of +7 points. Later in the day, the UK releases GfK Consumer Confidence, with the markets braced for a second consecutive drop of -10 points. Over in the US, Final GDP impressed with a gain of 2.9%, beating the estimate of 2.7%. There was more good news as Pending Home Sales jumped 3.1%, rebounding after the previous release of -4.7%. Later in the day, Japan releases Retail Sales, which is expected to edge up to 1.7%. Thursday promises to be busy on both sides of the pond. The UK releases Current Account and Final GDP, while the US will publish unemployment claims and UoM Consumer Sentiment.

The British economy has performed better than most had expected, with the uncertainty over Britain’s departure from the European Union in March 2019. However, indicators released on Wednesday pointed to some glaring weaknesses in the British economy. The CBI Retail Sales survey has showed sales volumes softening in recent months, and this troubling trend continued in March, with a reading of -8 points. Consumer confidence is also waning, as GfK Consumer Confidence has posted consecutive declines since April 2016. Still, the British pound has enjoyed a solid March, with gains of 2.6% against the US dollar.

The tariff spat between the US and China has shaken up global stock markets and also caused volatility in the currency markets. US President Trump slapped tariffs on Chinese products last week, and China has vowed to retaliate with tariffs on US products. The specter of a global trade war ahs soured investor risk appetite. This week, however, China was singing a more conciliatory tune, saying it would apply to the World Trade Organization to overturn the tariffs. The US has imposed the tariffs under a national security provision, but China has argued that the move is a trade barrier with the intent of protecting domestic producers. Although the dispute has not been resolved, the Chinese move has eased tensions and restored investor risk appetite, in the hope that both the US and China will climb down from their trees and reach some agreement instead of imposing tariffs on each other.

Eco Data 3/29/18

[php_everywhere instance="1"]

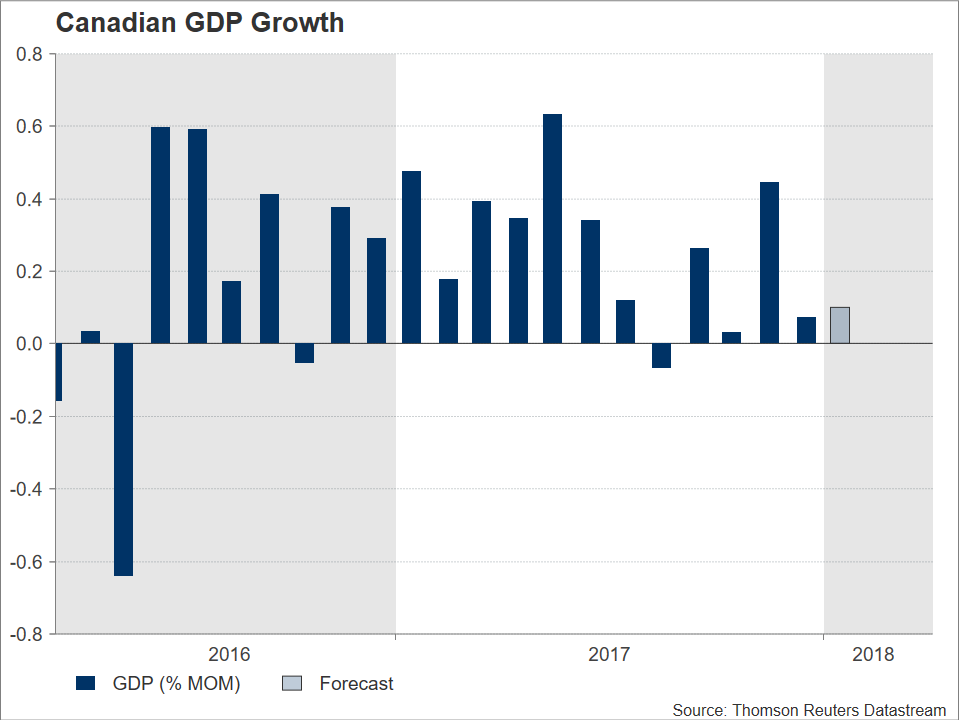

Canadian GDP Due Amid Raft of US Releases

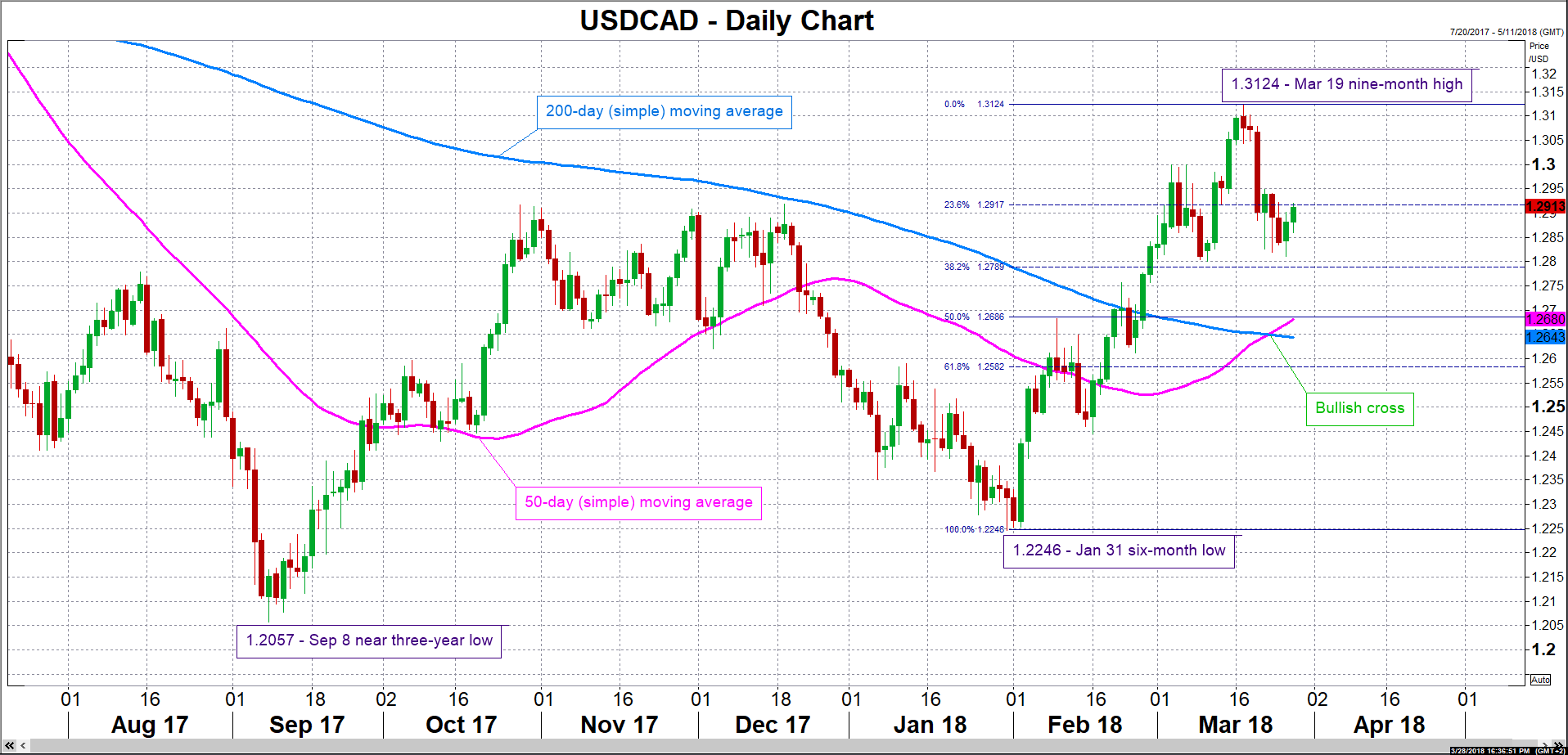

Canadian GDP figures for the month of January are due on Thursday at 1230 GMT. The release could give direction to the local dollar which has been performing poorly relative to its US counterpart, shedding 2.7% year-to-date.

Economic activity in Canada is expected to have expanded by 0.1% m/m during the first month of the year, at the same rate as in December. Strong growth during the first half of 2017 was instrumental for the country’s economy to expand by 3.0% for the year overall, its highest since 2017. Growth after H1 2017 was not as robust though and Thursday’s release is anticipated to show a continuation of this pattern, adding credence to those supporting that the Canadian economy is likely settling to a more sustainable pace of expansion.

Data on Canadian producer prices for the month of February will also be released on Thursday at 1230 GMT, with an increase of 0.5% on a monthly basis being projected by analysts, a faster pace relative to January’s respective reading of 0.3%.

Data on Canadian producer prices for the month of February will also be released on Thursday at 1230 GMT, with an increase of 0.5% on a monthly basis being projected by analysts, a faster pace relative to January’s respective reading of 0.3%.

The Bank of Canada has delivered three 25bps interest rate hikes since July. Market participants currently do not expect a rate increase when the Bank next meets on April 18, while according to Canadian overnight index swaps they project greater than even odds – around 65% – for a quarter percentage point rate hike to be delivered during the meeting in late May. Upbeat GDP and producer price figures have the capacity to push that probability even higher, benefitting the local dollar by pushing dollar/loonie lower.

Support in case of a falling dollar/loonie could come around the 38.2% Fibonacci retracement level of the January 31 to March 19 upleg at 1.2789. The area around this mark also includes the 1.28 round figure, while it was one of congestion in previous months. Disappointing numbers on the other hand might propel the pair higher. Dollar/loonie could be meeting resistance at the moment around the 23.6% Fibonacci level at 1.2917 – the range around this encapsulates the 1.29 handle and a few peaks from the recent past. An upside break would shift the focus to 1.30 that may be of psychological significance and then to March 19’s nine-month high of 1.3124.

Within the context of reaction in the dollar/loonie pair, it should be kept in mind that Canadian releases should not be viewed in isolation, as US personal income and consumption data, as well as the core PCE price index – all for the month of February – will be made public at the same time. In the meantime, markets will also have to digest initial and continued jobless claims for the week ending March 24 out of the US.

Within the context of reaction in the dollar/loonie pair, it should be kept in mind that Canadian releases should not be viewed in isolation, as US personal income and consumption data, as well as the core PCE price index – all for the month of February – will be made public at the same time. In the meantime, markets will also have to digest initial and continued jobless claims for the week ending March 24 out of the US.

In the bigger picture, besides tomorrow’s data out of Canada and how they would affect the BoC, the loonie’s broader direction also seems heavily dependent on the future of NAFTA negotiations; the currency appeared very sensitive to developments on this front in the past. In the latest developments, US Trade Representative Robert Lighthizer said in an interview earlier on Wednesday that he is hopeful that an agreement can be reached “in the next little bit”, though he also made reference to a “short window” for such an outcome, implying that the parties involved should act quickly in the face of presidential and midterm congressional elections in Mexico and the US respectively later in the year. The eighth round of talks is expected to commence sometime in April in Washington.

Lastly, the trajectory in oil prices could also affect the loonie given that Canada is a major exporter of the precious liquid. Rising US shale production is a driver that could exert pressure on prices. On the other hand, the appointment of policy-hawks in the Trump administration, such as new National Security Adviser John Bolton, that could push for fresh sanctions on Iran thus taking a chunk of oil supply out of the market, are supportive of prices.

Dollar Turns its Sights to Core PCE Price Index, Spending & Income Data

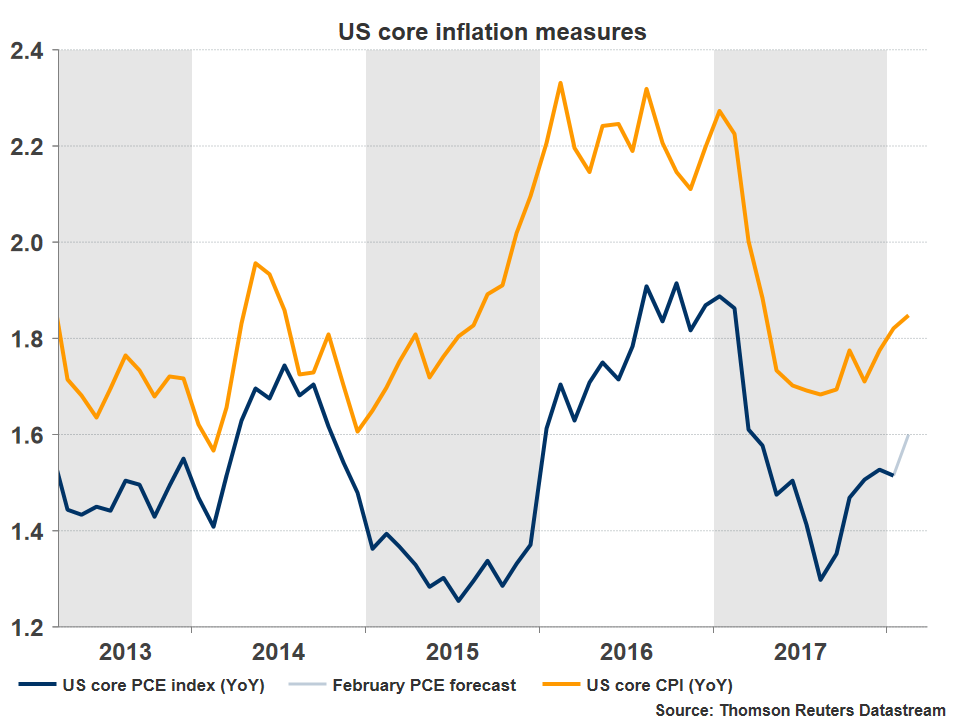

Thursday will probably be the most eventful day for the US dollar this week, from a data perspective at least. The core PCE price index, which is the Fed’s preferred inflation measure, as well as personal income and spending figures are all due for release at 1230 GMT. While forecasts point to a robust set of data, there are reasons to be hesitant to trust these projections, which implies the greenback may be at risk from these releases.

Core inflation – which excludes the effects of volatile items such as energy and food – has been treading water in the US for a while now, regardless of which measure one chooses to focus on. Both the core CPI and the core PCE have remained stuck at 1.8% and 1.5% respectively in yearly terms over recent months, exerting little pressure on the Fed to raise interest rates aggressively. In fact, some of the more dovish policymakers have repeatedly called for the Fed to be patient and wait for higher inflation to materialize before lifting interest rates further. Still, the Fed has raised rates in two out of its three latest meetings, on the expectation that inflation will pick up soon and reach its 2% target.Pertaining to the upcoming data set, in February, the core PCE price index is projected to have risen to 1.6% year-on-year, from 1.5% previously. What is critical here, is that economists consider it a close call whether the PCE rate will rise. Out of the 39 institutions submitting their forecasts to the Thomson Reuters system, 22 anticipate the core PCE to rise to 1.6%, while 16 of them see the PCE rate remaining at 1.5%. Only one expects a pick-up to 1.7%. Not to mention that the core CPI rate stayed flat in February. Thus, the risk appears to be a lower-than-expected reading, as opposed to a higher one, like 1.7%. As for personal spending and income, both are anticipated to have risen at the same pace as in the previous month, by 0.2% and 0.4% m/m correspondingly. However, one is a little cautious to trust these forecasts, considering that retail sales fell for a third straight month in February, pointing to a slowdown in spending, and also that average hourly earnings slowed in the month.

While markets see practically no chance for another move at the next policy gathering in May, they do see a 72% probability for a 25bps rate increase at the June meeting, according to the Fed funds futures. Any signs that inflation is accelerating towards 2%, or that economic growth is picking up speed, are likely to make investors more confident that a June hike will indeed take place and by extent, benefit the dollar. Anything that suggests otherwise though, could spell more bad news for the US currency.

While markets see practically no chance for another move at the next policy gathering in May, they do see a 72% probability for a 25bps rate increase at the June meeting, according to the Fed funds futures. Any signs that inflation is accelerating towards 2%, or that economic growth is picking up speed, are likely to make investors more confident that a June hike will indeed take place and by extent, benefit the dollar. Anything that suggests otherwise though, could spell more bad news for the US currency.

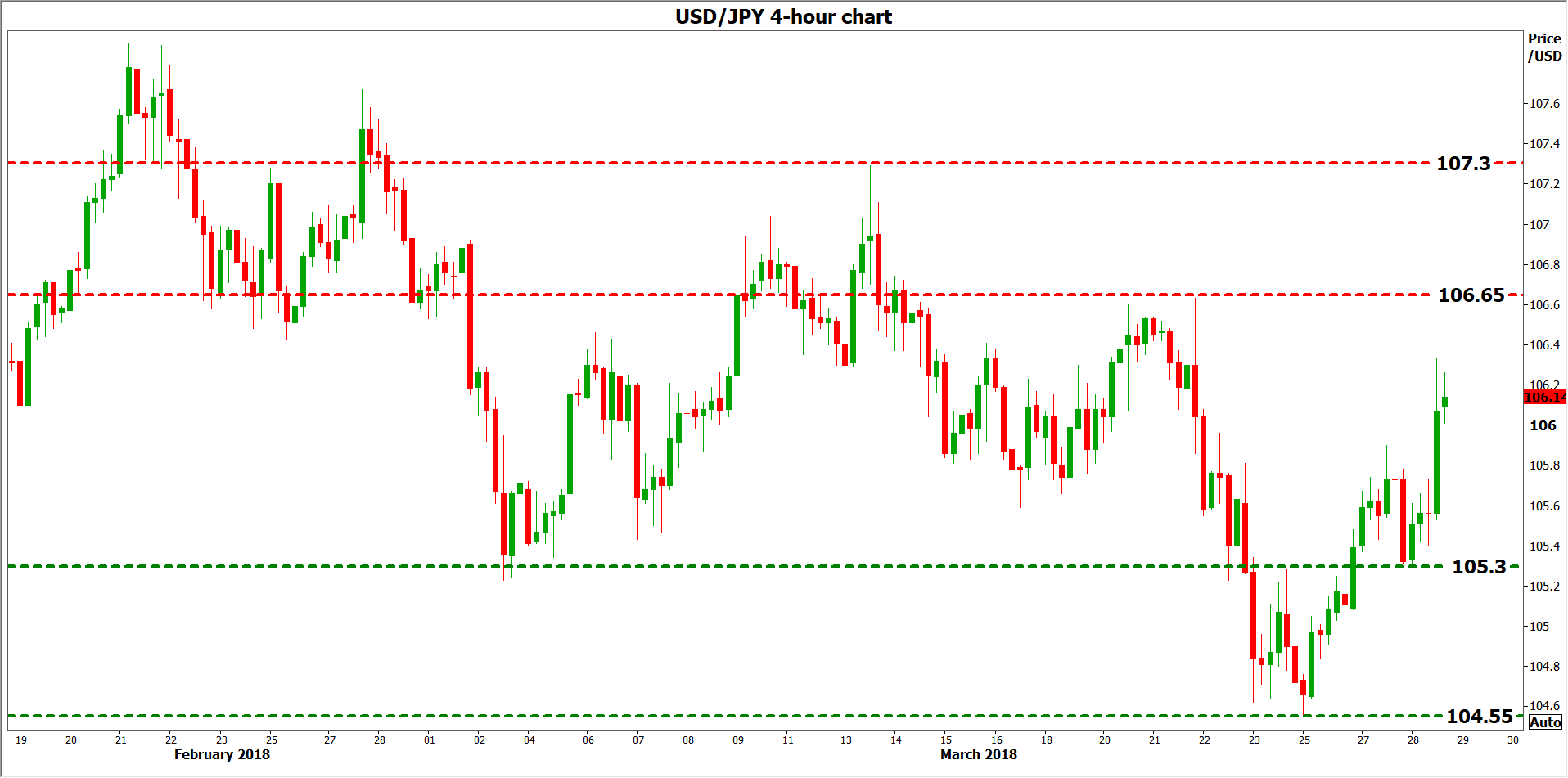

Thus, should these data disappoint – for example if the core PCE rate stays unchanged – the dollar could come under renewed selling interest. Dollar/yen may fall back down for a test of the 105.30 area, identified by the March 27 lows, with even steeper declines likely to bring the 104.55 level in focus, which is a 16-month low for the pair.

Conversely, an upside surprise in these figures could amplify expectations for a Fed hike in June and boost the greenback. Dollar/yen could aim for a test of the 106.65 territory, marked by the March 21 highs. If buyers manage to overcome that hurdle, resistance may be found near the 107.30 barrier, defined by the March 12 top.

Sunset Market Commentary

Markets:

Global core bond markets held a positive bias as rising equity volatility supported a bid for safe havens. End of month extension buying probably remained mildly positive as well. Bunds and Treasuries extended yesterday’s rebound early in European trading. The fall-out from the sell-off in tech equities eased (at least temporary), capping further bond gains. However, equity trading turned again more volatile after the open of the US equity. So, the jury is still out. US eco data were mixed and unimportant for bond trading. The focus remains on equities. At the time of writing, German yields decline less than 1 bp. US yields decline between 0.5 bps (2y) and 2.5 bps (10y). The US Treasury sells $15 bln 2-year floating rate notes and $29 bld 7-year bonds this evening.

The dollar held up well overnight despite a sell-off in (US) tech shares that continued in Asia this morning. USD/JPY in particular held ‘strong’ despite substantial equity losses. Dollar strength was probably also at least partially due to end of month/quarter position squaring. This USD bid was also visible in the trade-weighted dollar (DXY) which rose to 89.60 (from a correction low just below 89 yesterday). The price move in EUR/USD remained modest initially, but the broader bid for the dollar finally pushed the pair lower from the 1.2420 area to below 1.2350. US eco data were mixed with US GDP upwardly revised to 2.9% from 2.5% Q/Qa. Wholesale inventories rose a bigger than expected 1.1% M/M. The data suggest ongoing positive growth momentum in the US economy, but they won’t have a lasting impact on USD trading. Interest rate differentials between the US and Germany stay off recent highs, but were also no big driver for USD trading. Order-driven activity prevailed. USD/JPY is trading in the 106.20 area. Tomorrow’s PCE deflators might provide some more ‘economically inspired’ guidance for the dollar.

Sterling was temporary supported by headlines that the UK was working on a constructive solution to solve the issue of the Irish border post-Brexit. There are no details yet. UK economic news was mixed. CBI retail data were weaker than expected, but poor weather conditions were to blame. A BoE survey published showed UK companies are increasingly reporting shortages of skilled labour. Until now this had only a limited impact on pay growth, but the BoE gradually sees some upward wage drift. This might support the case for higher BoE rates later this year. EUR/GBP trades little changed in the 0.8750 area. Cable eased from the 1.42 area this morning to the low 1.41 area currently, but this is primarily due USD strength rather than GBP weakness.

News Headlines:

The balance of the CBI distributive trades survey declined to -8 in March from +8 in February, suggesting lower sales. The market consensus expected a positive balance of +7. According to CBI, the impact of a stagnating household income and weak consumer confidence was reinforced by unusually cold winter weather in March.

US Q4 2017 GDP was upwardly revised to 2.9% Q/Q (annualized) from 2.5% earlier. Q3 growth was 3.2% Q/Qa. Growth in consumer spending was upwardly revised to 4.0% from 3.8%. A decline in inventories weighed on growth, but the negative impact was smaller than initially reported. Net exports subtracted 1.16 percentage points from GDP.

Advance data from the Commerce department indicated that February US goods trade deficit widened slightly from $75.3 bn to $75.4 bn in February. The February deficit was upwardly revised from $74.4 bn. Goods exports rose 2.2% M/M to USD 136.55 bn. Imports rose 1.4M/M to 212.90 bn.

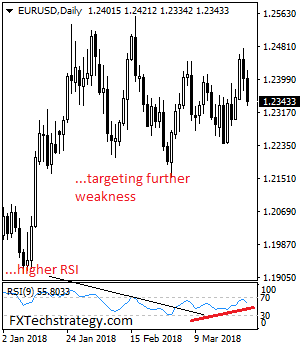

EURUSD: Follows Through Lower On Corrective Pullback

EURUSD: The pair saw a follow through lower on the back of its Tuesday correction on Wednesday. On the upside, resistance comes in at 1.2400 level with a cut through here opening the door for more upside towards the 1.2450 level. Further up, resistance lies at the 1.2500 level where a break will expose the 1.2550 level. Conversely, support lies at the 1.2300 level where a violation will aim at the 1.2250 level. A break of here will aim at the 1.2200 level. Below here will open the door for more weakness towards the 1.2150. All in all, EURUSD faces further downside threats.

Yen Slips to 1-Week Low on Strong US GDP

USD/JPY has posted strong gains in the Wednesday session. In the North American session, USD/JPY is trading at 106.18, up 0.81% on the day. On the release front, US Final GDP impressed with a gain of 2.9%, beating the estimate of 2.7%. There was more good news as Pending Home Sales jumped 3.1%, rebounding after the previous release of -4.7%. Later in the day, Japan releases Retail Sales, which is expected to edge up to 1..7%. On Thursday, US unemployment claims is forecast to tick up to 230 thousand, and UoM Consumer Sentiment is predicted to climb to 101.9 points. Japan will publish Tokyo Core CPI and Preliminary Industrial Production.

The tariff dispute between the US and China has shaken up global stock markets and also caused volatility in the currency markets. The safe-haven yen moved higher last week, after President Trump’s dramatic announcement that he was imposing stiff tariffs on up to $60 billion in Chinese imports. China vowed to retaliate and slap imports on a range of US products. This move came on the heels of a blanket US tariff on steel imports. Although Trump backtracked and exempted Canada, Mexico and other countries from the steel tariffs, the threat of a global trading war has unnerved investors. This week, however, China was singing a more conciliatory tune, saying it would apply to the World Trade Organization to overturn the tariffs. The US has imposed the tariffs under a national security provision, but China has argued that the move is a trade barrier with the intent of protecting domestic producers. Although the dispute has not been resolved, the Chinese move has eased tensions and restored investor risk appetite, in the hope that both the US and China will climb down from their trees and reach some agreement instead of imposing tariffs on each other.

Much like the situation in the eurozone, Japan’s economy continues to expand, but underlying inflation remains at low levels. Inflation is currently around 1%, well below the Bank of Japan target of just below 2 percent. The BoJ has been consistent in its message to the markets, saying that it has no plans to tighten its ultra-accommodative monetary policy until inflation moves closer to target. With the rebound in the Japanese economy, there has been speculation that the BoJ could tighten its policy, which could cause some volatility from the yen.

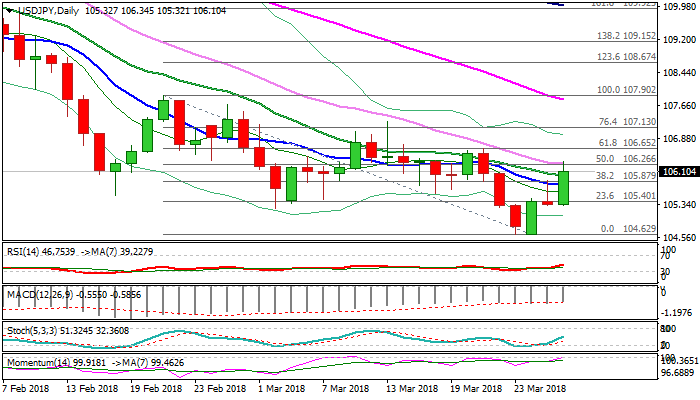

USDJPY – Bullish Acceleration on Upbeat US GDP Cracks Pivotal 30SMA Barrier

The pair surged above 106 barrier and cracked pivotal barrier at 106.30 (falling 30SMA), as dollar rallied across the board on better than expected US GDP data.

US Gross Domestic Product rose by 2.9% in the last quarter of 2017, beating forecast for 2.7% increase and coming well above 2.5% in Q3.

The economy grew 2.3% in 2017, showing strong improvement from 1.5% in 2016.

Fresh dollar’s rally improves USDJPY pair’s near-term picture and sidelined downside risk which persisted while the price stayed below 10SMA and Fibo barrier at 105.80/87. Bulls now look for close above 30SMA to generate fresh bullish signal for further retracement of 107.90/104.63 bear-phase and expose barriers at 106.65 and 107.13 (Fibo 61.8% and 76.4% respectively).

Broken 10SMA now marks solid support at 105.80, which is expected to keep the downside protected and maintain fresh bullish bias.

Res: 106.30; 106.65; 107.13; 107.29

Sup: 105.80; 105.32; 105.24; 105.00