Sample Category Title

USDJPY Sentiment Bullish Above 105.50 Level

The U.S dollar continues to hold above key support against the Japanese yen currency, with strong demand for greenbacks helping to underpin a bid tone in the pair. The intraday sentiment surrounding the USDJPY pair, remains bullish whilst price-action trading above the 105.50 level. Moving into the U.S session, traders await the release of U.S GDP numbers and the FED’s preferred measure of U.S inflation, Core Personal Expenditure.

The USDJPY pair retains a bullish bias whilst trading above the 105.50 level, further upside towards the 105.90 and 106.45 levels remains possible.

If the USDJPY pair trades below the 105.50 level for an extended period, sellers will likely move price-action towards the 105.24 and 104.64 support levels.

GBPUSD Bearish After Technical Failure

The British pound has turned lower against the U.S dollar during the European trading session, after a lack of overall buying interest above the 1.4200 technical level encourage sellers. The GBPUSD pair has now fallen back towards the 1.4146 level, with price action also creating a bearish double-top pattern across lower time-frame charts. Sterling traders now look towards a raft of top-tier macroeconomic data releases from the U.S economy, and the key 1.4133 technical support level.

The GBPUSD pair retains a bearish trading bias below the 1.4200 level, further losses towards the 1.4133 and 1.4087 levels remains possible.

Should the GBPUSD move above the 1.4200 level, the pairs trading sentiment will shift to bullish. Key resistance is then found at the 1.4244 and 1.4268 levels.

Risk Aversion Has Stamina As Tech Sector Quivers

Wednesday March 28: Five things the markets are talking about

Global equities trade on the back foot, with tech and mining names leading the charge lower.

Yesterday stateside, U.S tech shares suffered their worst drop in over a month on concerns over trade tensions, motivated by President Trump's protectionists' moves.

President Trumps latest plan to punish China for violations of U.S's intellectual-property rights has the White House administration pondering a crackdown on Chinese investments in technologies the U.S considers sensitive.

Amid the risk-off trading environment, U.S Treasuries have extended their price gains, pushing yields to seven-week lows. In currencies, the yen (¥105.52) has slipped while the pound (£1.4172) fluctuates as the market waits for signs of progress on the problem of the Irish border after Brexit.

On tap: After this morning's U.S final GDP reading (08:30 am EDT), U.S personal income and spending data for February are due to be released on Thursday (08:30 am EDT). In Europe, German March preliminary CPI data will be released tomorrow, while France delivers on Friday.

1. Tech stocks see red

Japanese stocks fell overnight, led by a sell-off in tech firms, while ex-dividend trades added to the broader losses. The Nikkei share average closed out -1.3% lower, while the broader Topix dropped -1%.

Down-under, Aussie shares skidded overnight, mirroring Wall Street's fall. At the close of trade, the S&P/ASX 200 index was down -0.7% – the same percentage it added on in its previous session. In S. Korea, the Kospi stock index weakened on Wednesday, falling -1.3% at the close.

In Hong Kong, stocks fell to their lowest closing level in three-weeks, amid renewed fears of a Sino/U.S trade war. The Hang Seng index fell -2.5%, the lowest closing level since March 5. The China Enterprises Index lost -2.4%.

In China, equities were guilty by association, with tech firms hit hard on concerns over tighter government scrutiny on the industry. At the close, the Shanghai Composite index was down -1.4%, while the blue-chip CSI300 index closed down -1.8%.

U.S stocks look set to open in the ‘red' (-0.3%).

Indices: Stoxx600 -1.3% at 362.8, FTSE -1.1% at 6924, DAX -1.7% at 11772, CAC-40 -1.5% at 5040, IBEX-35 -1.2% at 9364, FTSE MIB -1.3% at 21935, SMI -1.2% at 8534, S&P 500 Futures -0.3%

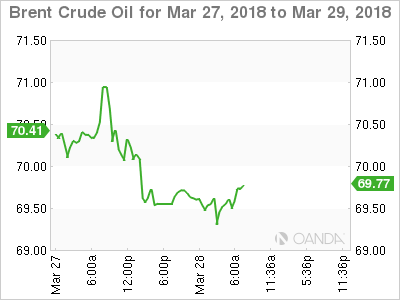

2. Oil prices fall on surprise U.S. inventory rise, gold higher

Oil prices trade under pressure, pulled down by a U.S report of increasing crude inventories.

Brent crude futures are at +$69.69 per barrel, down -42c, or -0.6%, while U.S WTI crude futures are at +$64.72 a barrel, down -53c, or -0.8% percent, from yesterday's close.

U.S API data late Tuesday reported a surprise +5.3m barrels rise in crude stocks in the week to March 23, to +430.6m barrels.

Note: U.S. oil production has already jumped by almost a quarter since mid-2016, to +10.4m bpd, taking it past top exporter Saudi Arabia and within reach of the biggest producer, Russia, which pumps around +11m bpd.

Expect investors to take their cues from today's official U.S API inventory print (10:30 am EDT).

Note: OPEC said to be looking for long-term cooperation with non-OPEC members. Reports circulated yesterday that the Saudi Crown Prince Mohammed bin Salman was looking to reach a +10 to 20-year supply agreement with Russia and other producers.

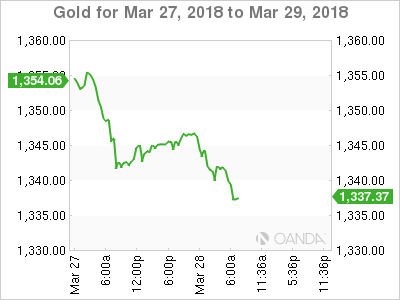

Ahead of the U.S open, gold prices have edged a tad higher overnight, supported by a ‘soft'ish' dollar, a day after the yellow metal recorded its biggest one-day percentage fall in nearly two-weeks as a U.S/China trade spat worries eased. Spot gold is up +0.2% at +$1,346.96 per ounce.

Note: The yellow metals prices dropped -0.6% on Tuesday, their biggest one-day percentage decline since March 15.

3. Sovereign yields fall to multi-week lows

Narrow ranges across Bunds and most Euro and U.S spreads amid lower volumes, despite the U.S ‘s record supply, suggest that the fixed income market has already entered Easter mode.

Note: In total and by week's end, the U.S Treasury will have auctioned approximately +$294B of bills and notes, its largest slate of supply ever.

Ahead of the U.S open, the yield on 10-year U.S Treasuries has dipped -2 bps to +2.76%, the lowest in more than seven-weeks. In the U.K, the 10-year Gilt yield has declined -5 bps to +1.371%, the lowest in two-months, while in Germany, the 10-year Bund yield has dipped -2 bps to +0.48%, reaching the lowest in 11-weeks on its fifth straight decline.

Elsewhere, the Bank of Thailand (BoT) left interest rates unchanged overnight as it awaits more signs of a broad-based recovery in the economy and monitors developments in U.S policy that could hurt global trade. Officials kept its one-day repurchase rate at +1.5%. One member of the seven-person committee voted to raise the rate by +0.25%.

4. Dollar confined to trading ranges

The ‘mighty' dollar remains well contained within its 2018 trading range.

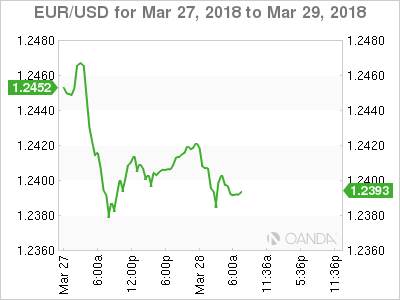

The EUR/USD (€1.2393) continues to hover atop of the psychological €1.2400 handle ahead of some key Euro inflation data in coming sessions. EU inflation is not making it easy for ECB officials to begin its ‘normalization' process. Of late, a number of ECB members (Praet and Liikanen) have cautioned against premature tightening.

Note: German March preliminary CPI data will be released tomorrow, while France delivers on Friday. The advance Euro-Zone CPI is set for release next week (April 4).

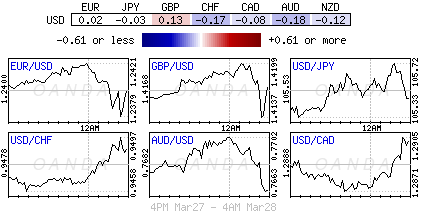

GBP/USD (£1.4150) continues to fail to hold onto gains above the key psychological £1.4200 level. Initial pound strength stemmed from reports that U.K was to offer a Brexit “hard Irish border” resolution imminently, with details beyond just the so-called backstop plan.

Safe-haven flows are failing to support yen (¥105.69) as the market focuses on some de-escalation of Korean peninsula tensions. North Korea leader Kim stated that his country was willing to hold dialogue with U.S.

Elsewhere, SEK (€10.2986) has slide to an 8-year low against the EUR due to market expectations that the Riksbank may postpone hiking interest rates until next-year on worries about the Swedish housing market as house prices continue to fall.

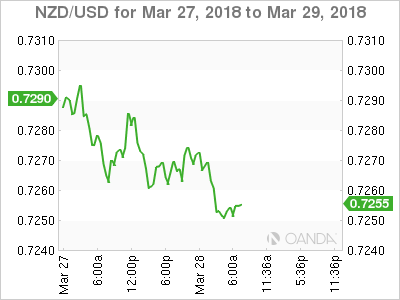

5. Some positives in stalled NZ business sentiment

While New Zealand's overall business confidence weakened slightly in March, as gloom continues in the agricultural sector, there are positives in yesterday's ANZ business outlook survey.

Digging deeper, a net +12% of companies are expecting to increase investment, up from +7% in February, and employment and export intentions also improved.

Companies also expect profits to increase by +6% compared with a slight fall expected just a month ago.

Nevertheless, the overall index did slip to -20 from -19 as the recovery from a post-election slide in sentiment stalls for now.

Trump pledges to maintain maximum sanctions and pressure on North Korea “at all cost”

Trump tweeted early in the morning:

"Received message last night from XI JINPING of China that his meeting with KIM JONG UN went very well and that KIM looks forward to his meeting with me. In the meantime, and unfortunately, maximum sanctions and pressure must be maintained at all cost!"

Recall earlier today, China's official news agency Xinhua reported North Korean Leader Kim Jong-un saying that "the issue of denuclearization of the Korean Peninsula can be resolved, if South Korea and the United States respond to our efforts with goodwill, create an atmosphere of peace and stability while taking progressive and synchronous measures for the realization of peace."

Now, does Kim feel that "maximum sanctions and pressure must be maintained at all cost" is something that create peacful and stable atmosphere?

Or, does Trump's "at all cost" mean maintianing maximum pressure even though it will turn North Korea away? Or he actually believes what he said is responding to North Korea with "good will"?

Probably, both of them need to go back to school to learn what to say what one means exactly.

Euro Trading Sideways Ahead Of US GDP

EUR/USD is unchanged in the Wednesday session. Currently, the pair is trading at 1.2393, down 0.07% on the day. On the release front, German GfK Consumer Climate ticked higher to 10.9, above the estimate of 10.7 points. In the US, Final GDP is expected to be revised upwards to 2.7%, after the initial reading of 2.5% back in February. US Pending Homes is forecast to rebound with a strong gain of 2.1%. On Thursday, Germany releases Preliminary CPI, which is expected to remain unchanged at 0.5%. German unemployment change is forecast to post another strong decline of 15 thousand. In the US, unemployment claims is forecast to tick up to 230 thousand, and UoM Consumer Sentiment is predicted to climb to 101.9 points.

In the eurozone, the storyline of stronger economic conditions but low inflation continues in 2018. This trend adds up to the ECB staying the course with regard to its stimulus program, according to a senior ECB policymaker. Governing Council member Erkki Liikanen said on Tuesday that the ECB will have to remain patient with its stimulus program, noting underlying inflation could remain at low levels, even if the economy performs well, since reducing economic slack may no longer trigger higher inflation, as has been the case in the past. With the current bond purchase program set to expire in September, there is speculation that the ECB will wind up the program, after years of pursuing an accommodative policy. If inflation does move closer to the ECB’s target of around 2 percent, there is a greater likelihood that the bank will not extend stimulus, and could entertain raising interest rates in 2018.

The tariff dispute between the US and China has shaken up global stock markets and also caused volatility in the currency markets. The dollar recorded losses last week, after President Trump’s dramatic announcement that he was imposing stiff tariffs on up to $60 billion in Chinese imports. China vowed to retaliate and slap imports on a range of US products. This move came on the heels of a blanket US tariff on steel imports. Although Trump backtracked and exempted Canada, Mexico and other countries from the steel tariffs, the threat of a global trading war has unnerved investors. This week, however, China was singing a more conciliatory tune, saying it would apply to the World Trade Organization to overturn the tariffs. The US has imposed the tariffs under a national security provision, but China has argued that the move is a trade barrier with the intent of protecting domestic producers. Although the dispute has not been resolved, the Chinese move has eased tensions and restored investor risk appetite, in the hope that both the US and China will climb down from their trees and reach some agreement instead of imposing tariffs on each other.

US Slowdown Ahead?

US slowdown ahead?

Today's announcement that January US Pending Home Sales fell 4.7% points to an economic slowdown. It is triggered by the US Federal Reserve's money-tightening strategy that is finally taking hold, but also by winter weather. Rising mortgage rates should depress consumer demand, making a strong rebound unlikely.

As a long Easter weekend approaches, risk sentiment is weak. Equities failed to maintain momentum from Tuesday's upward bounce. Profit taking dragged tech and consumer shares, while defensive plays in utilities and telecoms outperformed as yield harvesting is driving investors. That did not spill into forex as high-yielding emerging market currencies were softer across the board. Even big gainers MXN and ZAR were flagging. EUR/USD came off highs as the USD clawed back gains. US Treasuries rallied (specifically in the middle of the curve). After Easter, risk appetite is likely to resume.

Eurozone economy solid

The European Central Bank says the Eurozone economy is healthy. Lending to non-financial corporations and households increased by 3% in February, a slight decrease from 3.30% in January and slightly higher than December's 2.90%. February's annualised growth of adjusted loans for households and non-financial companies were 2.90% and 3.10%. Inflation is down slightly, as M3 money supply decreased to 4.20% from 4.60% in January, suggesting a slowdown in overnight deposits for non-financial corporations. February's consumer price index remains at 1.10% annualised, signalling a deceleration in retail sales and industrial activity. Economic confidence is falling slightly, in Germany -2.4, Italy -1.8, Spain -1.2, Netherlands -0.5 and France -0.4. Consumer confidence remains stable at 0.1.

EUR/USD's slight weakness stems from yesterday's disappointing US March consumer confidence data (127.7 compared to 130.8 in February. As Easter holidays approach, we expect the current level of 1.2385 (+3.11 this year) to decrease to the 1.2377 range.

Germany rumored to be willing to offer concessions to US on trade, European Commission rules that out

Bloomberg reported the European Commission urged the region's governments today to stand united in trade talks with the US, and be ready to "think out of the box fast". EU is seeking to follow South Korea to get indefinite exemption on the steel and aluminum tariffs by May 1.

But, the option of re-negotiation of EU-US free trade agreement is ruled out by EC. Unilateral European concessions to the US is also ruled out. It seems that EC is asking the officials to stay "inside" the box but think "out of" it. Well, there is no logical contradiction.

It was also reported by Bloomberg that Germany is adopting a flexible approach in dealing with the US and is willing to offer concession to the US. Germany Chancellor Angel Merkel is believed to be ready to lower the 10% EU tariff on autos to avoid a trade dispute.

But that is in total opposite position to France. President Emmanuel Macron is clear in his message that European steel and aluminum exports pose no security threat to the US. And the rules of international trade need to be "reinforced" to ensure such a level playing field.

So, the EC's message seemed to be directed at Germany.

More Pain Ahead For Equity Markets | Fangs Getting Banged

US equity markets are in for some rough time

FANG stocks are in pretty rough shape

Sterling traders are going to gauge the health of the consumers

European markets are in for another brutal day. As proven by the US equities markets yesterday, the big bounce we experienced was nothing more than a dead cat bounce. No surprise there at all. We think the US equity markets are in for some rough time and we could see the markets falling another 5% from here.

FANG stocks are in pretty rough shape, and are getting banged brutely by short sellers. The FANG stocks had the worst day yesterday since February 2016. Most of the gains over in the US for the last 18 months were supported by the tech sector. Having said that, the NASDAQ index is still relatively much stronger as compared to the S&P500 index, which has moved closer towards the 200-day moving average for the third time in three months. Break of the 200-day moving average usually confirms the bear markets.

The tech sector is predominantly getting battered, mainly due to the woes of Facebook’s data breach. We clearly have three kind of investors when it comes to the Facebook; firstly there are some who are jumping out of the ship, pushing the stock price lower. Secondly, we have investors who are watching the show from the sideline and thinking there is more pain to come as we do not know how big the potential fine could be. This is not helping the stock price either. Finally, we have those who are not interested in Facebook anymore as they think that the regulatory burdensome on Facebook is too risky for their appetite and they do not want to get involved in this stock.

We personally think, that Facebook has strong fundamentals and it has become the part of everyone’s daily life, so once we have a clear idea about the potential sum which the firm would have to pay as a result of this situation, the stock price could present a potential opportunity.

As for the FANG stock including Microsoft, Twitter, it is likely that the Facebook incident would open the door for more scrutiny for other firms, and lawmakers would see how other firms are using user data. This could really open the can of worms and open a potential opportunity for short sellers.

Back in the U.K., Sterling traders are going to gauge the health of the consumers by monitoring the CBI sales data. Sterling has gained major strength against the dollar and the euro since the start of this year and this is mainly due to positive development around Brexit negotiation.

Higher inflation and lower wage growth is still a major hurdle for the policymakers. Businesses were quick in passing the higher cost to consumers, as derived from a sudden drop in the currency. But we have come far away from the Brexit lows for sterling, although consumers are still facing higher prices. The forecast for today’s data is 7 while the previous reading was at 8. If a number comes below the forecast reading, it would signal weakness in the economy and that could push the Sterling lower against a basket of major currencies.

Risk Aversion Still Has Legs As Tech Sector Wobbles

Notes/Observations

- Weakness in tech sector prompting continued risk aversion flows

Asia:

- Japan and US to hold leader talks on April 17-18th to discuss strategy before proposed meeting between US/North Korea leaders

- North Korea leader Kim stated that his country was willing to hold dialogue with USA . Denuclearization could be resolved provided South Korea and the US respond with "goodwill, create an atmosphere of peace and stability while taking progressive and synchronous measures for the realization of peace.

- Japan PM Abe: Reiterates view that Govt to raise the sales tax to 10% as planned; would consider another delay if a financial crisis-level shock came

- Bank of Japan (BOJ) Gov Kuroda reiterated to continue with powerful easing, had taken appropriate policy at the right time

- China said to draft guidelines to increase imports. US trade measures would not have a big impact on overall Chinese trade situation. Reiterates that China might retaliate if tensions escalate

- China said to be preparing retaliatory tariffs on US imports and deal a “heavy blow” to Washington that aggressively threatened a trade war

Europe:

- EU Commission in Brussels said to be considering taking €56B from ECB profits to plug budget hole after Brexit

- UK govt said to be offering a hard border resolution imminently regarding Ireland. Officials in Ireland are said to have been told to expect the new plan in the near-term and have been promised concrete details on what the alternative plans the UK govt has.

Americas:

- Fed's Bostic (FOMC voter, dove): sympathetic towards adopting price level targeting as a new Fed framework. Wants to stick to 2% inflation target but as an avg rate over time rather than a fixed goal

Energy:

- Weekly API Oil Inventories: Crude: +5.3M v -2.7M prior

Economic Data:

- (DE) Germany Apr GfK Consumer Confidence (beat): 10.9 v 10.7e

- (NO) Norway Feb Retail Sales W/Auto Fuel M/M: -0.6% v +0.5%e

- (FI) Finland Feb House Price Index M/M: +0.6% v -0.7% prior; Y/Y: 0.9% v 0.7% prior

- (FR) France Mar Consumer Confidence: 100 v 100e

- (ES) Spain Feb Adj Retail Sales Y/Y: 1.9% v 2.0%e; Retail Sales (unadj) Y/Y: 2.2% v 2.4% prior

- (HU) Hungary Feb Unemployment Rate: 3.8% v 3.9%e

- (TH) Thailand Central Bank (BOT) left its Benchmark Interest Rate unchanged at 1.50%; as expected

- (SE) Sweden Feb Retail Sales M/M: 0.3% v 0.3%e; Y/Y: 1.5% v 1.5%e

- (CH) Swiss Mar Credit Suisse Expectations Survey: 16.7 v 25.8 prior

- (AT) Austria Mar Manufacturing PMI: 58.0 v 59.2 prior (26th month of expansion)

- (IT) Italy Jan Industrial Sales M/M: -2.8% v +2.5% prior; Y/Y: 5.3% v 7.4% prior

- (IT) Italy Jan Industrial Orders M/M: -4.5% v +4.6% prior; Y/Y: 9.6% v 4.1% prior

- (NO) Norway Central Bank (Norges) Apr Daily FX Purchases (NOK): -800MM v -800Me

- (ES) Spain Jan Current Account: -€0.5B v +€2.6B prior

Fixed Income Issuance:

- (FR) France Debt Agency (AFT) opened its book to sell EUR-denominated July 2036 Inflation-linked Bond (Oatei); guidance seen high 20bps area

- (EU) ECB allotted $5.01B in 7-day USD Liquidity Tender at fixed 2.15% vs $79M prior

- (SE) Sweden sold SEK5.0B vs. SEK5.0B indicated in 3-month Bills; Avg Yield: -0.8596% v -0.7221% prior; bid-to-cover: 3.46x v 3.17x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -1.3% at 362.8, FTSE -1.1% at 6924, DAX -1.7% at 11772, CAC-40 -1.5% at 5040, IBEX-35 -1.2% at 9364, FTSE MIB -1.3% at 21935 , SMI -1.2% at 8534, S&P 500 Futures -0.3%]

- Market Focal Points/Key Themes: European Indices trade lower across the board continuing the volatility which has been observed in the past few sessions following a selloff in the Tech Sector overnight. On the corporate front Fincantieri underperforms following results, with SMA Solar, Hamburger Hafen und Logistik and Evotec other names trading lower following results. Whilst Hilton Foods Group and DFS trade higher after full year results. Looking ahead notable earners include Blackberry, Walgreen Boots Alliance and UniFirst.

Movers

- Consumer Discretionary [ DFS [DFS.UK] +7.4% (Earnings) ]

- Consumer Staples [Hiltonfoods Group [HFG.UK] +3.6% (Earnings)]

- Industrials [Fincantieri [FCT.IT] -10.4% (Earnings), HHFA [HHFA.DE] -9.6% (Earnings)

- Heatlthcare [ Evotec [EVT.DE} -1.4% (Earnings) ]

- Financial [ Deutsche Bank [DBK.DE] -1.8% (Reportedly board split over CEO)]

- Energy [SMA Solar [S92.DE] -4.9% (Earnings) ]

Speakers

- BOE Agents Summary of Business Conditions: Robust growth in goods exports had tightened capacity and, together with improving profit margins, strengthened investment intentions in manufacturing slightly. Recruitment difficulties remained a primary concern, though the impact on pay growth had been limited. Some evidence of financial distress in retail and leisure, reflecting weak consumer spending growth.

- Swiss KOF Institute Spring Economic Forecast raised both 2018 and 2019 GDP growth forecasts and 2018 inflation from 0.5% to 0.7%. Swiss economy was currently on an upward trajectory

- Thailand Central Bank (BOT) Policy Statement noted that the vote to keep rate unchanged was 6-1. Reiterated view that monetary policy should remain accommodative and saw FX volatility continuing. Forecasted both 2018 and 2019 GDP growth at 4.1% and cut 2018 Headline CPI from 1.1% to 1.0% and Core CPI from 0.8% to 0.7%

- Bank of Japan (BOJ) Gov Kuroda reiterated view that not in situation where would need to buy US treasuries (**Note: BoJ law has the central bank forbidden from buying foreign bonds for the purpose of influencing FX rates)

- China President Xi Jinping to visit South Korea Mar 29-30th

- China National Development and Reform Commission (NDRC): To promote further connect in capital markets with Hong Kong

- Malaysia Central bank: 2018 monetary policy report raised its 2018 GDP growth from 5.0-5.5% range to 5.5-6.0%. Saw 2018 Inflation lower between 2.0-3.0% range vs. 3.7% in 2017

- Iraq Oil Min Al-Luaibi reiterated view that Iraq would not deviate from any OPEC decision on crude supply. To decide by end-2018 whether to keep oil production cuts

- OPEC said to be looking for long-term cooperation with non-Opec members (in-line with recent Saudi comments)

Currencies

- EUR/USD hovering around the 1.24 area ahead of some key European inflation data in coming sessions. Analysts note that EMU inflation has not made it easy for ECB to begin its normalization process. A few ECB members (Praet and Liikanen) have cautioned against premature ECB tightening. The German March preliminary CPI data will be released on Thursday and France on Friday. The Advance Euro Zone CPI set for release next week.

- The GBP/USD continued to fail to hold gains above the 1.42 level. Initial GBP strength stemmed from reports that UK was to offer a hard border resolution imminently, with details beyond just the so-called backstop plan. GBP/USD little changed at 1.4160

- Safe-haven flows failed to prop up the JPY currency with focus on some de-escalation of Korean Peninsula tensions. North Korea leader Kim stated that his country was willing to hold dialogue with USA . Denuclearization could be resolved

Fixed Income

- Bund Futures trade 16 ticks higher at 159.54 as bund near levels that may trigger shorts. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 122.57 up 43 ticks as month-end hot spots outperform. Support continues stands at 121.25 then 120.85, with upside resistance at 123.35 then 123.85.

- Wednesday's liquidity report showed Tuesday's excess liquidity fell to €1.789T from €1.802T prior. Use of the marginal lending facility increased from €105M to €110M.

- Corporate issuance saw 6 issuers raise $4.5B in the primary market

Looking Ahead

- (IT) Italy Debt Agency (Tesoro) to sell €4.5-5.5B in 5-year and 10-year BTP Bonds

- (IT) Italy Debt Agency (Tesoro) to sell €1.5-2.0B in Apr 2025 Floating rate Note (CCTeu)

- (MX) Mexico Feb YTD Budget Balance (MXN): No est v -20.4B prior

- (BR) Brazil Mar CNI Consumer Confidence: No est v 102.7 prior

- (PT) Bank of Portugal update on Economic Forecasts

- 05:30 (EU) ECB allotment in 3-month LTRO operation

- 06:00 (UK) Mar CBI Retailing Reported Sales: 7e v 8 prior, Total Distribution: No est v 14 prior

- 06:00 (IE) Ireland Feb Retail Sales Volume M/M: No est v -0.6% prior; Y/Y: No est v 1.3% prior

- 06:00 (RU) Russia to sell combined RUB30B in 2024 and 2034 OFZ bonds - 06:45 (US) Daily Libor Fixing

- 07:00 (BR) Brazil Mar FGV Inflation IGPM M/M: 0.6%e v 0.1% prior; Y/Y: +0.2%e v -0.4% prior

- 07:00 (US) MBA Mortgage Applications w/e Aug Mar 23rd: No est v -1.1% prior

- 08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming issuance

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Q4 Final GDP Annualized Q/Q: 2.7%e v 2.5% prelim; Personal Consumption: 3.8%e v 3.8% prelim

- 08:30 (US) Q4 Final GDP Price Index: 2.3%e v 2.3% prelim; Core PCE Q/Q: 1.9%e v 1.9% prelim

- 08:30 (US) Feb Advance Goods Trade Balance: -$74.2Be v -$75.3B prior (revised from -$74.4B)

- 08:30 (US) Feb Preliminary Wholesale Inventories M/M: 0.5%e v 0.8% prior, Retail Inventories M/M: No est v 0.8% prior

- 09:00 (ZA) South Africa Central Bank (SARB) Interest Rate Decision: Expected to leave Interest Rates unchanged at 6.75%

- 09:30 (BR) Brazil Feb Nominal Budget Balance (BRL): -46.1Be v +18.6B prior; Primary Budget Balance: -18.0Be v +46.9B prior

- 09:45 (UK) BOE to buy £1.22B in in APF Gilt purchase operation (7-15-years)

- 10:00 (US) Feb Pending Home Sales M/M: +2.0%e v -4.7% prior; Y/Y: No est v -1.7% prior

- 10:30 (US) Weekly DOE Crude Oil Inventories

- 11:00 (MX) Mexico Feb Net Outstanding Loans (MXN): No est v 4.031T prior

- 11:00 (CO) Colombia Feb National Unemployment Rate: No est v 11.8% prior; Urban Unemployment Rate: 11.4%e v 13.4% prior

- 11:30 (US) Treasury to sell 2-Year Floating Rate Notes Reopening

- 12:00 (US) Fed’s Bostoc (2018 voter, dove) in Atlanta

- 13:00 (US) Treasury to sell 7-Year Notes

- 15:00 (US) Feb Agriculture Prices Received: No est v 0.2% prior

- 15:00 (AR) Argentina Jan Economic Activity Index (Monthly GDP) M/M: No est v 0.6% prior; Y/Y: 2.5%e v 2.0% prior

- 15:00 (AR) Argentina Feb Industrial Production Y/Y: 7.6%e v 2.6% prior, Construction Activity Y/Y: No est v 19.0% prior

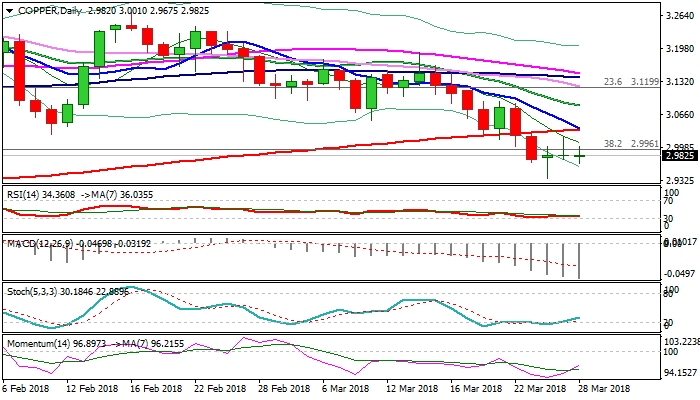

Copper – The Third Long Legged Doji Signals Extended Directionless Mode, Overall Structure Remains Firmly Bearish

Copper holds in directionless mode for the third straight day after Monday's downside attempts were strongly rejected at $2.9370 (the lowest since late Sep 2017), but subsequent recovery actions were limited, resulting in double long-legged Dojis on Mon/Tue and Wednesday's trading holding so far in the same shape.

Situation about current dispute between the USA and China over tariffs on imported goods is unclear, though persisting fears of trade war keep metal's price at risk of further fall.

The notion is supported by firmly bearish daily studies, with today's attempts to form 10/200SMA death-cross, expected to further weigh on copper's price.

Clear break out of current congestion is needed to generate firmer direction signal. Bears need eventual close below cracked key support at $2.9425 (05 Dec low) and break below Monday's spike low at $2.9370 to confirm bearish continuation, as completion of asymmetric H&S pattern on weekly chart on last week's break below the neckline was strong bearish signal.

Conversely, bullish scenario needs close above $3.0225/39 pivots (Tuesday's spike high / Fibo 38.2% of $3.1645/$2.9370 bear-leg) to signal recovery.

Res: 3.0000, 3.0250, 3.0322, 3.0540

Sup: 2.9675, 2.9370, 2.9000, 2.8960